Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

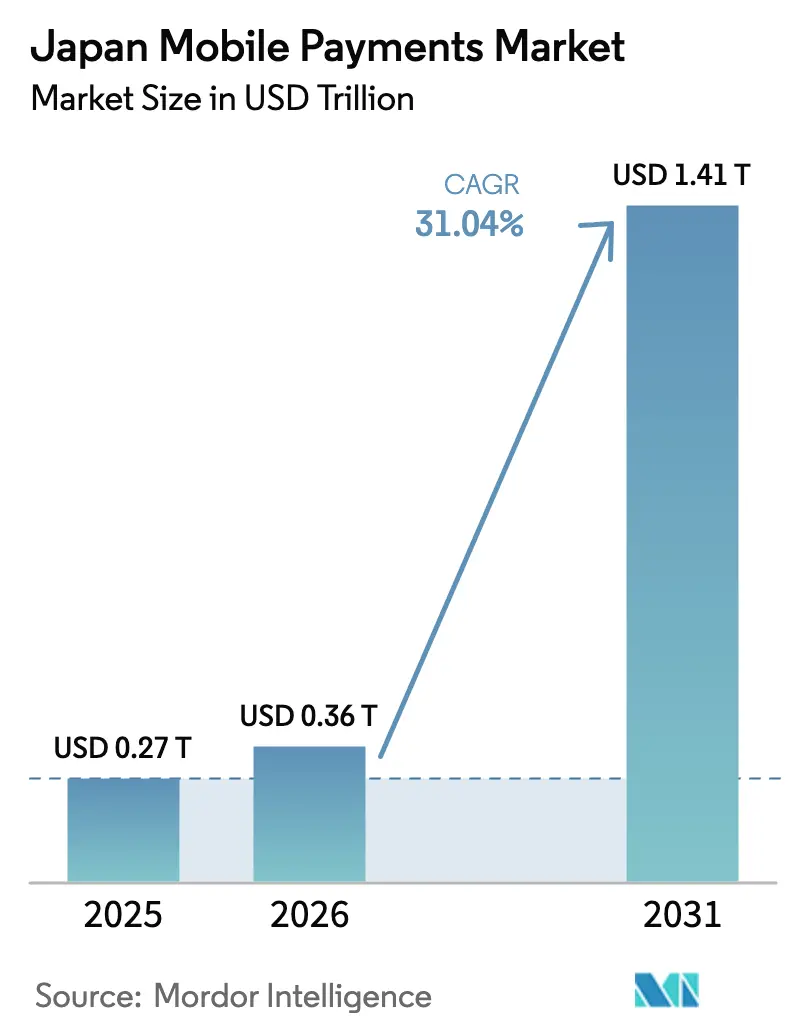

| Base Year Market Size (2025) | USD 0.27 Trillion |

| Market Size (2026) | USD 0.36 Trillion |

| Market Size (2031) | USD 1.41 Trillion |

| Growth Rate (2026 - 2031) | 31.04% CAGR |

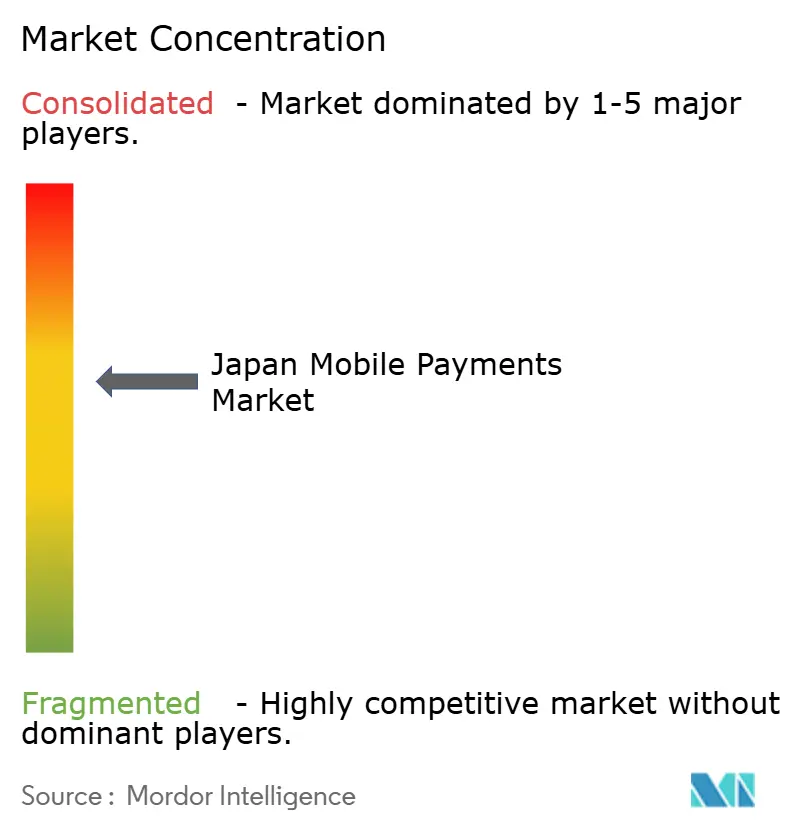

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Mobile Payments Market Analysis by Mordor Intelligence

The Japan mobile payments market size stood at USD 0.36 trillion in 2026 and is projected to reach USD 1.41 trillion by 2031, registering a 31.04% CAGR. The expansion aligns with the government’s Cashless Vision that aims for an 80% cashless ratio by 2030, rising from 42.8% in 2024. Mobile wallet adoption, rapid e-commerce penetration, and 5G-enabled smartphone ubiquity underpin this structural pivot toward digital transactions. Real-time settlements, led by domestic bank transfer infrastructure and emerging real-time payment rails alongside movement toward a digital yen, further compress settlement latencies, while inbound tourism recovery places new volume across retail, hospitality, and transportation spend. Competitive dynamics remain fluid as telecom-backed wallets, e-commerce ecosystems, and payment gateways race to convert Japan’s remaining cash-reliant segments.

Key Report Takeaways

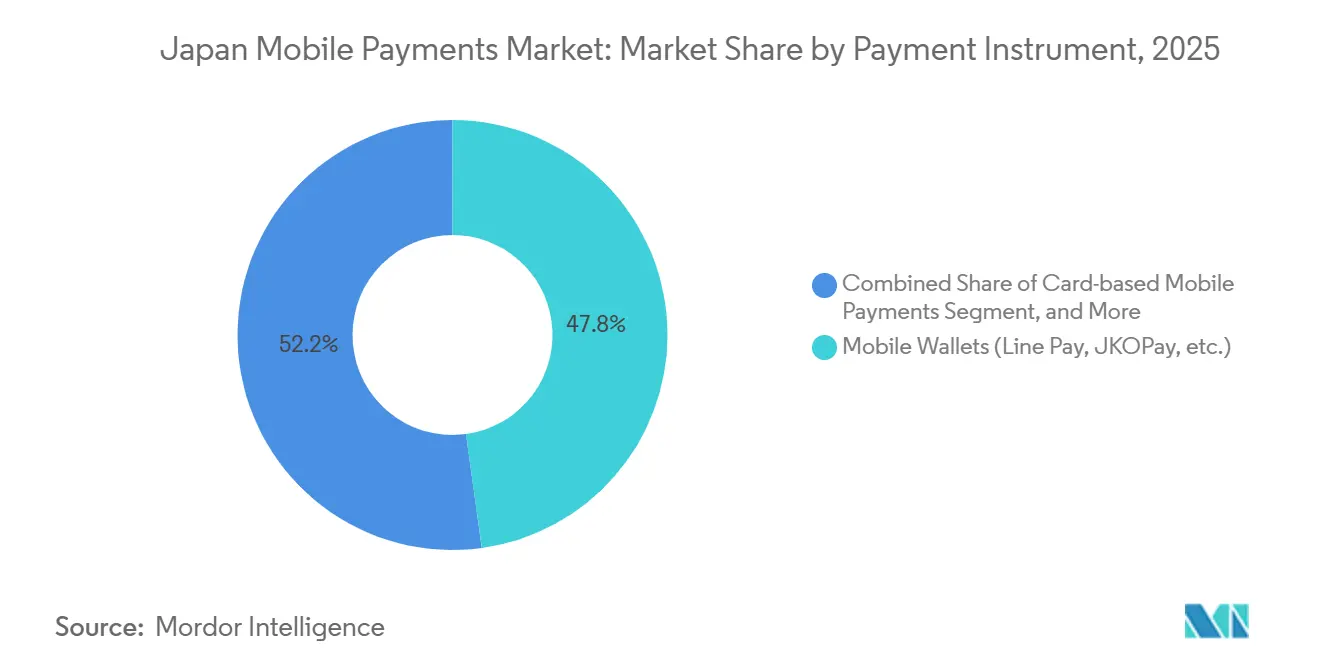

- By payment instrument, mobile wallets secured 47.83% of payment instrument share in 2025, whereas real-time transfers are set to advance at a 31.76% CAGR through 2031.

- By transaction channel, e-commerce channels accounted for 47.83% of transaction volume in 2025, while cross-border and tourist payments are forecast to expand at a 31.83% CAGR through 2031.

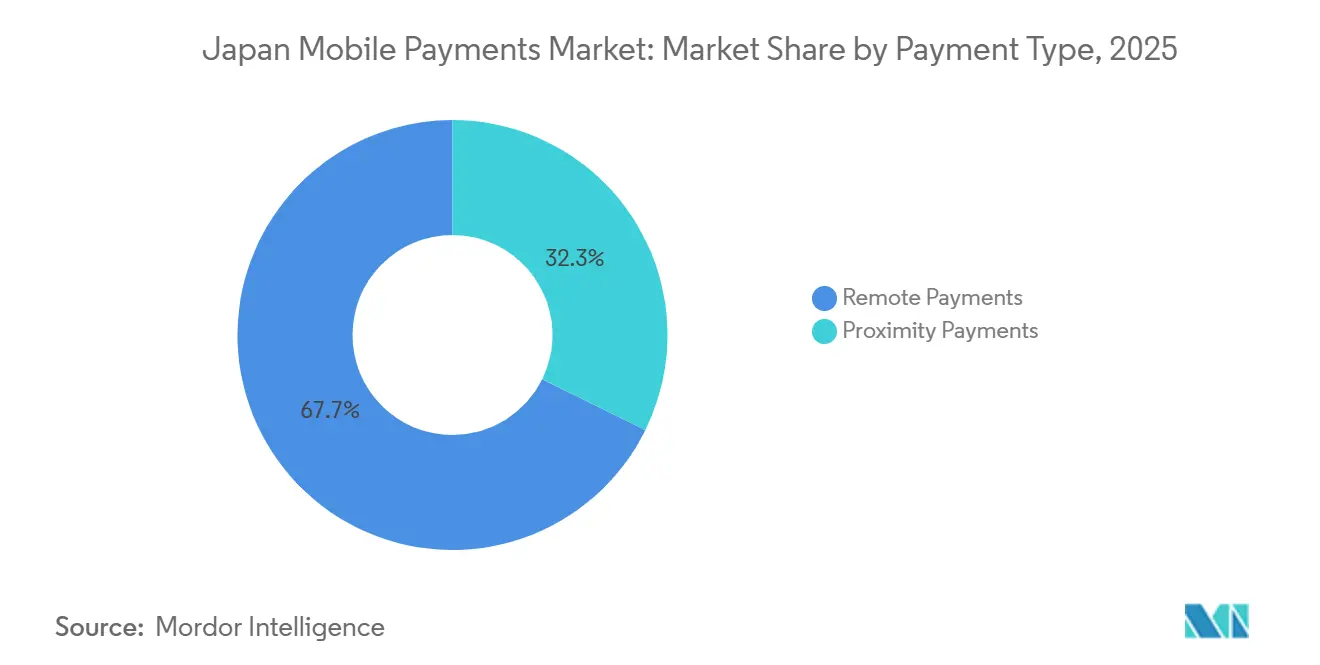

- By payment type, remote payments represented 67.72% of transaction types in 2025 and are projected to grow at a 32.03% CAGR to 2031.

- By end-user industry, retail and fast-moving consumer goods held 34.72% of end-user industry revenue in 2025, whereas hospitality and tourism show the fastest trajectory with a 31.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Cashless Vision 80% Target by 2030 | +8.2% | National – Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| E-commerce and M-commerce Boom | +7.5% | National – urban and logistics hubs | Short term (≤2 years) |

| Nationwide QR-Code Incentives for SMEs | +5.8% | National – regional cities, rural clusters | Medium term (2-4 years) |

| High Smartphone and 5G Penetration | +4.9% | National – 5G corridors | Long term (≥4 years) |

| Digital-yen Pilot Integration Pathways | +2.6% | National – financial districts | Long term (≥4 years) |

| Payroll Digitization After Labor Act Revision | +2.0% | National – large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Cashless Vision 80% Target by 2030

The Ministry of Economy, Trade and Industry raised the national cashless ratio goal to 80% by 2030 after surpassing 40% two years ahead of schedule. Subsidies now offset up to two-thirds of terminal costs for small and medium enterprises, a decisive incentive for nearly 60% of merchants that remained cash-only through 2024. Credit cards still generate most digital turnover, yet QR payments have already reached double-digit share, reflecting a generational pivot toward smartphone-centric transactions. Urban cashless ratios above 50% highlight the momentum in Tokyo, Osaka, and Nagoya, whereas rural prefectures lag, creating expansion headroom for wallet providers. JPQR standardization seeks to unify codes across eight Asian networks in time for Expo 2025, removing a key interoperability hurdle.[1]Ministry of Economy, Trade and Industry, “Cashless Payment Promotion,” meti.go.jp

E-commerce and M-commerce Boom Across Retail and Services

Japan’s e-commerce sector touched USD 112.9 billion in 2024, with mobile commerce already exceeding half of all online turnover. Ecosystem leaders such as Rakuten seamlessly bridge shopping, payment, credit, and loyalty, producing higher repeat-purchase frequency and lower checkout friction. Peer-to-peer platforms like Mercari embed Merpay to keep payments native to the browsing flow, reinforcing conversion gains of 15%-20% over desktop. Mobile-first design has broad appeal in fashion, electronics, and food delivery, while inbound shoppers leverage UnionPay and Alipay Plus to blur domestic and international transaction boundaries.

Nationwide QR-Code Acceptance Incentives for SMEs

Acquirer fees of 2%-4% and legacy hardware costs between USD 500 and USD 2,000 long discouraged smaller merchants. The government’s subsidy scheme reduces capex, while PayPay’s free QR stickers and cashback promotions effectively yield sub-1.5% net fees during campaigns. JPQR now lets stores display a single code that works across PayPay, Rakuten Pay, d-Barai, au PAY, and regional bank wallets, trimming integration effort. Rural adoption, once 18-24 months behind urban centers, is accelerating as local banks co-sponsor training and incentives. This convergence narrows Japan’s digital divide while driving volume into the Japan mobile payments market.

High Smartphone and 5G Penetration Enabling Wallet Adoption

Smartphone connections reached 194 million in 2025, equal to 157% of the population, and 5G already blankets 37% of residents. Low-latency networks support instant confirmations, augmented-reality coupons, and biometric checks that cut checkout times nearly in half versus physical cards. Telecom wallets leverage carrier billing to pre-authenticate users and extend credit via phone invoices, sidestepping conventional scoring hurdles for students and gig workers. Apple Pay and Google Pay dominate premium devices, yet domestic wallets hold mass-market Android positions, prompting the Mobile Payment Alliance to pursue deeper interoperability for seamless experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging SME POS Hardware and High Fees | -3.8% | National – rural, suburban clusters | Short term (≤2 years) |

| Fragmented Wallet Ecosystem | -2.9% | National – multi-brand retail | Medium term (2-4 years) |

| Cyber-fraud and Card-not-Present Chargebacks | -1.7% | National – e-commerce, peer-to-peer | Short term (≤2 years) |

| Slow QR Interoperability Cross-border | -1.2% | China, South Korea, Taiwan, ASEAN corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging SME POS Hardware and High Acquirer Fees

Roughly 60% of small merchants still use outdated terminals or remain cash-only, wary of fees that erode already thin margins. Even with subsidies, residual hardware costs and maintenance deter operators in low-volume rural sites. Wallet providers respond with zero-capex QR decals and periodic fee holidays, yet such promotions need cross-subsidies from urban spend to stay viable. The resulting two-tier ecosystem slows nationwide ubiquity for the Japan mobile payments market.

Fragmented Wallet Ecosystem Confusing Users and Merchants

PayPay, Rakuten Pay, d-Barai, au PAY, Merpay, and numerous regional wallets each push proprietary codes, loyalty schemes, and promotions. Stores juggling up to eight decals face operational clutter, and integrated multi-wallet terminals add USD 1,000-1,500 in upfront expense. JPQR consolidation reached only 15,000 stores by 2024, far from the 100,000 target, partly because each provider hesitates to forfeit brand differentiation. LINE Pay’s 2025 shutdown signals inevitable attrition, yet network-effect scale is still some distance away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Instrument: Wallet Share Anchors While Real-Time Transfers Accelerate

Wallets held 47.83% of payment instrument volume in 2025 within the Japan mobile payments market. PayPay alone processed 7.8 billion transactions worth JPY 12.5 trillion (USD 83.3 billion) in fiscal 2024, leveraging telecom backing and cashback incentives to reach 70 million users. Rakuten Pay turns ecosystem points into tender and ranks highest in satisfaction surveys three years running, while d-Barai and au PAY employ carrier billing to extend micro-credit. Despite this lead, real-time transfers are predicted to post a 31.76% CAGR, underpinned by Bank of Japan settlement upgrades and an impending digital yen decision. The Japan mobile payments market size tied to real-time rails therefore expands faster than any other instrument category. Interbank APIs and yen-backed stablecoin pilots by major banks illustrate a path toward programmable money that could bypass legacy card networks.

Card tokenization via Apple Pay and Google Pay keeps premium iOS and Android users within near-field communication ecosystems, yet these segments remain smaller than QR-driven wallets. Carrier billing supports niche digital-content purchases and prepaid top-ups but faces regulatory limits on credit exposure. Meanwhile, Payment Card Industry Data Security Standard requirements introduced in 2024 raise compliance costs, tilting smaller issuers toward gateway partnerships. These factors collectively maintain wallets as the anchor but set the stage for real-time and central bank digital currency solutions to gain incremental share inside the Japan mobile payments industry.

By Transaction Channel: E-commerce Plateaus as Cross-Border Volumes Surge

E-commerce represented 47.83% of all transaction volume in 2025, buoyed by one-click wallet integrations that cut cart abandonment by up to one-fifth. Mobile commerce’s 58.2% share of online spend underscores consumer comfort with biometric checkouts on handheld devices. Yet the highest growth resides in cross-border and tourist channels at a 31.83% CAGR, a shift that will reshape the Japan mobile payments market. Visitor arrivals rebounded to 36.87 million in 2024 and are headed toward the 60 million goal, funneling additional spend through Alipay Plus and UnionPay networks.

Transport-integrated e-money, namely Suica and PASMO, expands in-store acceptance beyond rail gates, reinforcing hybrid digital-physical commerce. Peer-to-peer transfers also rise, driven by PayPay’s zero-fee model, highlighting consumer appetite for instant, bank-free remittances. Together, these trends diversify revenue streams while increasing competitive pressure on static e-commerce channels within the Japan mobile payments market.

By Payment Type: Remote Transactions Dominate While Hybrid Models Emerge

Remote transactions accounted for 67.72% of payment activity in 2025, driven by robust e-commerce, bill pay, and peer-to-peer use cases. The segment’s 32.03% CAGR signals sustained momentum for the Japan mobile payments market size. However, an uptick in card-not-present fraud underscored the need for 3D Secure version 2.0, which now reduces false approvals by up to 40%.

Proximity payments still anchor in-store retail, hospitality, and transportation. Suica Renaissance, set for autumn 2026, plans to add QR capabilities for 155 million rail e-money users and to narrow the gap between offline and online experiences. As wallets overlay augmented-reality offers, the boundary between remote and proximity payments shrinks, steering the Japan mobile payments market toward unified app architectures that seamlessly manage both modes.

By End-User Industry: Hospitality Outruns Retail Amid Tourism Revival

Retail and fast-moving consumer goods delivered 34.72% of 2025 spend, sustained by convenience-store networks that accept Nanaco, WAON, and universal QR codes. Department stores blend private-label e-money with loyalty analytics, but online-native formats grow quicker by integrating payment deep into browsing journeys. Hospitality and tourism, projected to expand at a 31.98% CAGR, benefit from instantaneous tax-free refunds and multi-wallet acceptance that captures higher-value tourist purchases. This momentum enlarges the Japan mobile payments market share attached to hotels, restaurants, and entertainment, eclipsing traditional retail growth.

Transportation retains relevance via contactless transit cards now extending to retail checkouts, while utilities and telecom rely on carrier billing to aggregate household payments. Healthcare and education show latent demand yet await clearer regulatory pathways. Overall, divergent trajectories across industries reinforce why wallet providers tailor propositions to sector-specific pain points within the broader Japan mobile payments industry.

Geography Analysis

Tokyo, Osaka, and Nagoya accounted for most of the 2025 transaction volume, thanks to dense merchant networks, high smartphone usage, and frequent promotional campaigns. Cashless ratios surpassing most in these cities spotlight rapid adoption, whereas rural prefectures such as Hokkaido and Kyushu remain at a signficiant rate, constrained by aging merchant bases and slower broadband rollout. Regional banks partnered with national wallets in 2025 to deliver localized incentives, yet rural uptake still trails urban uptake by up to 2 years. Achieving most of the national cashless target hinges on closing this digital divide.

Cross-border corridors with China, South Korea, Taiwan, and ASEAN markets gain prominence as JPQR interoperability extends to eight Asian networks. Alipay Plus boasts acceptance at more than 1 million Japanese sites, and UnionPay covers 2 million, turning Ginza, Dotonbori, and Gion districts into frictionless tourist spending zones. The Bank of Japan’s digital yen pilot includes real-time foreign exchange, hinting at fee-free cross-border capabilities by 2026.[2]Bank of Japan, “Digital Yen Pilot Outline,” boj.or.jp

Suburban logistics hubs in Saitama, Chiba, and Kanagawa experienced a sharp uptick in mobile commerce during 2025, driven by same-day delivery models that favor app-based checkouts. As 5G coverage accelerates toward 92% by 2030, augmented-reality promotions and biometric security will migrate into secondary cities, adding new nodes to the Japan mobile payments market.

Competitive Landscape

The market is moderately fragmented. PayPay accounts for most QR payments and captures one-fifth of all cashless volume, yet no single player dominates every instrument or channel. GMO Payment Gateway processes JPY 21 trillion (USD 140 billion) annually for 150,000 merchants, acting as neutral plumbing for multiple wallets.[3]GMO Payment Gateway, “Corporate Fact Book 2025,” gmo-pg.com Telecom-backed offerings leverage carrier billing data to underwrite micro-credit, while Rakuten builds stickiness through an ecosystem prism that links shopping, banking, and securities.

Product roadmaps pivot on biometric authentication, augmented-reality commerce, and server-managed wallets. JR East’s Suica Renaissance illustrates how transportation incumbents can leverage vast cardholder bases to expand beyond transit. Meanwhile, major banks tested yen-backed stablecoins in November 2025, signaling readiness to enter programmable money segments if a digital yen gains official traction. Continued wallet consolidation is probable, following LINE Pay’s 2025 exit and PayPay’s acquisition of a 40% stake in Binance Japan, a move that integrates crypto trading into mainstream consumer wallets.

The Financial Services Agency's Payment Card Industry Data Security Standard compliance mandate enforced in 2024 elevated baseline security requirements, yet persistent card-not-present fraud losses of JPY 54.1 billion (USD 360 million) in 2024 underscore the need for continuous investment in three-dimensional secure authentication and behavioral analytics

Japan Mobile Payments Industry Leaders

GMO Payment Gateway Inc.

SB Payment Service Corp.

PayPay Corporation

Rakuten Payment, Inc.

LY Corporation (Line Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PayPay Corporation filed for a U.S. initial public offering that could exceed USD 20 billion.

- November 2025: East Japan Railway Company and PASMO introduced a shared QR code accepted across 155 million cards.

- October 2025: PayPay acquired 40% of Binance Japan to enable crypto purchases via PayPay Money.

- August 2025: GMO Payment Gateway and GMO Financial Gate received Net Zero certification from the Science Based Targets initiative.

Japan Mobile Payments Market Report Scope

The Japan Mobile Payments Market Report is Segmented by Payment Instrument (PromptPay/RTP Transfers, Mobile Wallets, Card-based Mobile Payments, Carrier Billing/Others), Transaction Channel (In-store POS, E-commerce, P2P Transfers, Bill and Government Payments, Cross-border/Tourist), Payment Type (Proximity Payments, Remote Payments), and End-User Industry (Retail and FMCG, Transportation and Mobility, Hospitality and Tourism, Utilities and Telecom, Healthcare and Education, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Payment Instrument

| PromptPay / RTP Transfers |

| Mobile Wallets (e.g., PayPay, Rakuten Pay, d-Barai) |

| Card-based Mobile Payments |

| Carrier Billing / Others |

By Transaction Channel

| In-store POS |

| E-commerce |

| P2P Transfers |

| Bill and Government Payments |

| Cross-border / Tourist |

By Payment Type

| Proximity Payments |

| Remote Payments |

By End-User Industry

| Retail and FMCG |

| Transportation and Mobility |

| Hospitality and Tourism |

| Utilities and Telecom |

| Healthcare and Education |

| Other End-User Industries |

| By Payment Instrument | PromptPay / RTP Transfers |

| Mobile Wallets (e.g., PayPay, Rakuten Pay, d-Barai) | |

| Card-based Mobile Payments | |

| Carrier Billing / Others | |

| By Transaction Channel | In-store POS |

| E-commerce | |

| P2P Transfers | |

| Bill and Government Payments | |

| Cross-border / Tourist | |

| By Payment Type | Proximity Payments |

| Remote Payments | |

| By End-User Industry | Retail and FMCG |

| Transportation and Mobility | |

| Hospitality and Tourism | |

| Utilities and Telecom | |

| Healthcare and Education | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Japan mobile payments market?

The market stands at USD 0.36 trillion in 2026 and is projected to reach USD 1.41 trillion by 2031.

Which payment instrument holds the largest share?

Mobile wallets lead with 47.83% of payment instrument volume in 2025.

Which segment is growing fastest through 2031?

Real-time payment transfers are forecast to expand at a 31.76% CAGR.

How will inbound tourism influence payment volumes?

Cross-border and tourist channels are expected to grow at a 31.83% CAGR on the way to the government’s 60 million visitor target.

What restrains small merchants from adopting cashless solutions?

High acquirer fees and outdated point-of-sale hardware remain the most prominent barriers despite subsidy programs.

Page last updated on: