Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

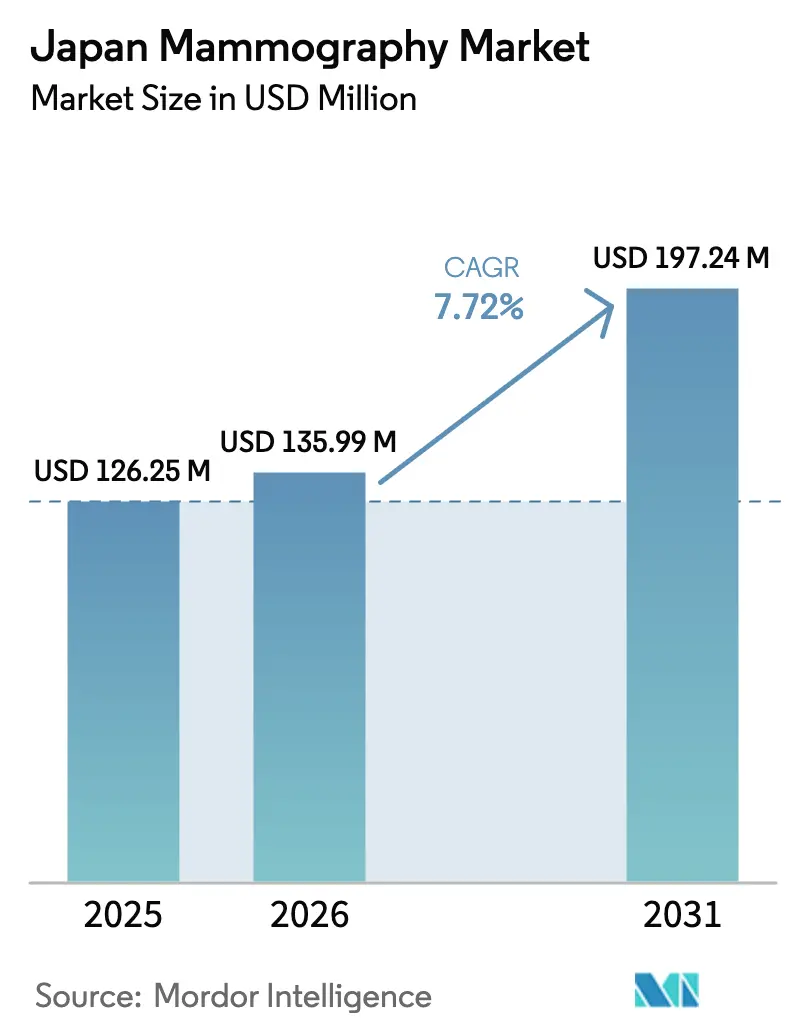

| Base Year Market Size (2025) | USD 126.25 Million |

| Market Size (2026) | USD 135.99 Million |

| Market Size (2031) | USD 197.24 Million |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Mammography Market Analysis by Mordor Intelligence

Japan mammography market size in 2026 is estimated at USD 135.99 million, growing from 2025 value of USD 126.25 million with 2031 projections showing USD 197.24 million, growing at 7.72% CAGR over 2026-2031. Strong demand stems from Japan’s super-aged demographics, regulatory mandates that force analog room replacement, the 2024 reimbursement uplift for digital breast tomosynthesis (DBT), and rapid artificial intelligence (AI) integration into image-reading workflows. Breast cancer remains the most frequently diagnosed malignancy among Japanese women, with 91,800 new cases projected for 2024, ensuring a consistent clinical need for screening capacity. Hospitals continue to renew fleets ahead of the 2027 radiation-dose deadline and to leverage AI-enabled triage that cuts radiologist read-time by 41.6%. Specialty clinics are gaining momentum because expanded National Health Insurance (NHI) coverage for DBT lowers out-of-pocket costs and because corporate “Pink Health” check-ups embed screening in employee benefit plans. Domestic manufacturers build on deep service networks, while global vendors partner with Japanese AI firms to fine-tune algorithms for dense Asian breast tissue, enhancing competitive intensity.

Key Report Takeaways

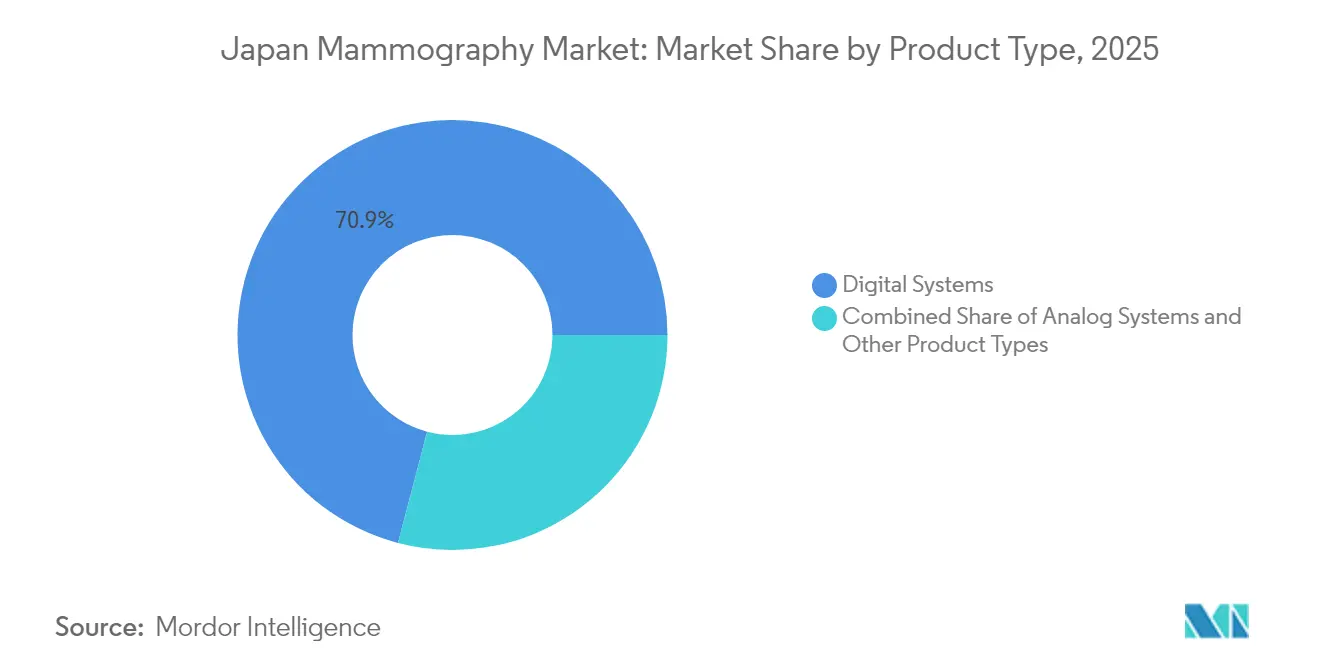

- By product type, Digital Systems led with 70.92% of the Japan mammography market share in 2025; Other Product Types are projected to expand at an 8.85% CAGR through 2031.

- By end user, Hospitals accounted for 63.58% share of the Japan mammography market size in 2025, whereas Specialty Clinics are advancing at an 8.49% CAGR through 2031.

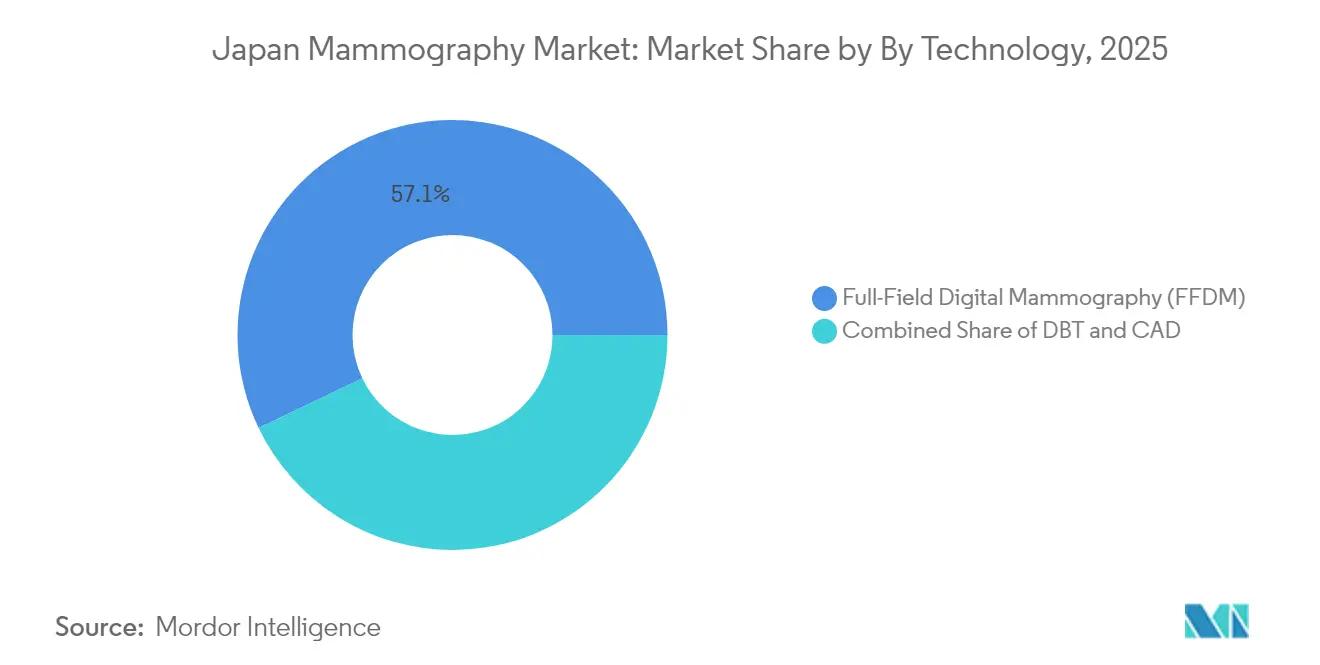

- By technology, Full-Field Digital Mammography captured 57.12% of the Japan mammography market share in 2025, while Digital Breast Tomosynthesis is forecast to grow at a 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-women demographic bulge intensifying biennial screening targets | +2.1% | Nationwide, highest in Tokyo, Osaka, Nagoya | Long term (≥ 4 years) |

| Mandatory switch-out of analog rooms to meet 2027 dose cap | +1.8% | Nationwide, fastest in urban hospitals | Short term (≤ 2 years) |

| Reimbursement uplift for DBT under NHI 2024 | +1.5% | Nationwide, strongest in private clinics | Medium term (2-4 years) |

| AI-enabled triage platforms slashing read-times | +1.2% | Urban centers first, rural uptake next | Medium term (2-4 years) |

| Corporate “Pink Health” check-ups in benefit menu | +0.9% | Corporate hubs, gradual national roll-out | Long term (≥ 4 years) |

| Mobile mammography vans for depopulated prefectures | +0.6% | Rural Tohoku and Kyushu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-Women Demographic Bulge Intensifying Biennial Screening Targets

The expanding female cohort aged 50-74 underpins long-run volume growth because Japan mandates biennial screening for women aged 40-74, generating a structural demand floor. Breast-cancer incidence is projected at 91,800 new cases in 2024 and mortality at 15,900 deaths, reinforcing the importance of high detection rates. Post-pandemic recovery accelerated participation: screening uptake climbed to 46.9% in the 2023-2024 span from 38.2% pre-COVID-19, signaling resilient patient awareness. Average life expectancy now exceeds 87 years for women, so health systems prepare for repeated exposures over longer lifespans, sharpening the focus on low-dose yet high-resolution modalities. The demographic bulge also triggers earlier equipment replacement because providers seek faster throughput and better workflow analytics to manage larger cohorts. Manufacturers respond with ergonomic gantries and comfort paddles that improve patient adherence, supporting recurring service contracts on installed systems.

Mandatory Switch-Out of Analog Rooms to Meet MHLW Radiation-Dose Cap 2027

The Ministry of Health, Labour and Welfare (MHLW) requires conversion from computed radiography (CR) to digital radiography (DR) no later than 2027 to reduce cumulative radiation exposure. Comparative trials show DR improves detection by 15-22% versus CR while cutting mean glandular dose, validating the policy. Roughly one-third of Japan’s installed base remains analog, so providers face a non-discretionary refresh cycle. Accelerated review pathways at the Pharmaceuticals and Medical Devices Agency (PMDA) shorten time-to-market for next-generation DR detectors [1]“PMDA Opens the Door to Innovative Products in Japan,” Global Forum, diaglobal.org. Vendors bundle financing and dose-audit software to lower upfront hurdles, and group purchasing organizations negotiate multiyear contracts, smoothing demand visibility through 2027.

Reimbursement Uplift for DBT under NHI 2024

NHI began reimbursing DBT for both screening and diagnostic claims in April 2024, eliminating a key barrier to broader adoption. Domestic studies show DBT lifts cancer detection by 32.2% and trims recall rates by 17.8%, giving clinics a strong quality-of-care argument. Private specialty centers quickly ordered upgrade kits for existing FFDM platforms, while hospitals budgeted full DBT rooms for high-volume bays. Because DBT yields more images per exam, radiologists deploy cloud-based storage and AI sorting tools, creating incremental opportunities for software vendors. The policy also supports mobile units: vans equipped with DBT now qualify for the higher reimbursement, improving financial viability on rural routes.

AI-Enabled Triage Platforms Slashing Radiologist Read-Times

Japan’s radiologist shortage—vacancy rates rose from 4.3% to 13.6% between 2021 and 2023—drives interest in AI triage. The prospective AI-STREAM cohort demonstrated 140 cancers found with AI assistance versus 123 without, with no rise in recalls, proving clinical efficacy. Hospitals report 30-40% shorter interpretation queues, letting limited staff handle larger caseloads. AI also flags positioning errors, supporting quality metrics tied to reimbursement bonuses. The PMDA introduced a rolling‐review pathway for adaptive algorithms in 2024, letting vendors push improvements under post-market surveillance rather than full re-submission, accelerating innovation. Early adopters market “AI-verified” packages to attract tech-savvy patients.

Corporate “Pink Health” Check-Ups Added to Shakai-Hoken Benefit Menu

Large employers now bundle biennial mammography in corporate medicals, shifting screening away from hospital settings to onsite or partner clinics. Corporations see productivity gains from early detection, while employees appreciate time-efficient services. Clinics gain predictable volumes and negotiate multi-year service contracts. The trend tightens procurement alliances: equipment suppliers co-host wellness events that demonstrate low-dose tomosynthesis and AI-aided reporting. Uptake is highest in corporate headquarters districts such as Marunouchi and Umeda, yet insurers expect gradual penetration into regional plants. Over the long term, this employer-sponsored model may smooth demand cycles and diversify payer mix.

Mobile Mammography Vans Serving Depopulated Prefectures

Rural prefectures face both aging populations and hospital consolidation, so mobile vans bridge access gaps. Evidence shows mobile units add incremental volume without cannibalizing facility-based screening. Vans integrate DR detectors and DBT-ready tubes powered by onboard generators, while 5G links transmit studies to urban reading centers. Prefectural governments co-finance fleet purchases through the 2025 social-security budget, easing capital strain. Deployment favors Tohoku and Kyushu, where public-health nurse density is lowest. Vendors bundle service contracts that include remote diagnostics and replacement units, anchoring long-term revenue.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High replacement cost of legacy CR/DR detectors | -1.4% | Nationwide, hardest on rural hospitals | Short term (≤ 2 years) |

| Shortage of JABTS-certified radiographers | -1.1% | Rural prefectures in Tohoku, Kyushu, Shikoku | Long term (≥ 4 years) |

| Patient anxiety over cumulative radiation | -0.8% | Urban areas with health-conscious consumers | Medium term (2-4 years) |

| Slow prefectural approval cycle for new DBT rooms | -0.6% | Prefecture-dependent, slower in rural regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Replacement Cost of Legacy CR/DR Detectors

Premium mammography rooms carry prices between USD 215,000 and USD 275,000, while mid-tier systems cost USD 90,000-165,000, stretching budgets of smaller hospitals. Japan’s medical outlays may rise to 64.2 trillion JPY by 2050, pushing administrators to delay purchases. High-interest lease terms weigh on rural providers that serve fewer patients, prolonging amortization periods. Government subsidies cover only part of the capital, and competition for those funds is fierce. To respond, vendors extend zero-interest financing and certified refurbished programs; however, these measures only partially mitigate the upfront burden in the next two years.

Shortage of JABTS-Certified Radiographers in Rural Areas

Vacancy rates for mammography technologists jumped to 13.6% in 2023, reflecting retirements and migration to urban centers [2]“2024 Consensus Committee on the Future of Medical Imaging and Radiation Therapy,” ASRT, asrt.org. JABTS credentialing requires specialized training often unavailable in remote prefectures, causing screening sites to operate below capacity. Tele-training initiatives exist but struggle with broadband limits, and mid-career relocation incentives have yet to reverse the talent flow. Workforce constraints lengthen patient wait times and raise per-exam costs, discouraging smaller clinics from expanding. These shortages will persist over the long term unless regional education grants and flexible licensing pathways scale up.

Patient Anxiety Over Cumulative Radiation Exposure

Health-conscious segments question repeat exposure, even though mammography doses are low. Social media amplifies concerns, pushing some women to skip biennial sessions. Providers combat fear by adopting DR detectors with dose-tracking dashboards that print patient-friendly summaries. Lower-dose DBT and synthesized 2D reconstructions also help, yet adoption takes time. Consumer hesitancy moderates growth in affluent urban wards where wellness blogs gain traction.

Slow Prefectural Approval Cycle for New DBT Installations

Japan’s two-step licensing—national certification then prefectural approval—adds months to DBT room commissioning, particularly in smaller prefectures that meet only quarterly. Delays defer revenue recognition and complicate vendor forecasting. Although PMDA shortened national review, local timelines remain static. Lobbying for centralized e-submission and virtual inspections continues, but near-term headwinds persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Anchor the Shift to Advanced Imaging

Digital Systems controlled 70.92% of the Japan mammography market share in 2025 and remain the backbone of replacement cycles triggered by the 2027 dose mandate. The segment benefits from manufacturers’ updates that retrofit existing gantries with DBT modules, letting providers add 3D capability without full-room rebuilds. Hospitals value dose-tracking software that automates compliance reporting to the MHLW. Local firms refine ergonomic paddles for smaller stature patients, raising image quality and comfort. Service revenues grow because digital detectors require annual calibration; vendors bundle uptime guarantees to differentiate. Meanwhile, Analog Systems rapidly phase out, as fewer parts are stocked and resale values plummet.

Other Product Types, comprising biopsy-guided tables and mobile units, post a 8.85% CAGR, the fastest within the Japan mammography market. DBT-guided vacuum-assisted biopsy reaches 97.7% sampling success, shortening procedures and driving adoption in cancer centers. Mobile vans integrate cloud PACS that archive directly to hospital networks, reducing duplication. Prefectural grants subsidize van procurement when operators commit to rural screening quotas, ensuring a pipeline of unit sales. Collectively, these trends solidify Digital Systems as the volume leader while signaling lucrative niches in specialized devices.

By End User: Hospitals Retain Scale Advantages while Specialty Clinics Surge

Hospitals accounted for 63.58% of 2025 installations, securing the largest slice of the Japan mammography market size. They leverage integrated diagnostics—ultrasound, MRI, and biopsy suites in one campus—so procurement committees favor multi-vendor contracts that bundle service across modalities. AI workstations cut backlog and integrate with radiology information systems, supporting value-based care metrics tied to NHI reimbursement. Large centers adopt enterprise PACS that feed imaging biomarkers into oncology boards, reinforcing hospital dominance.

Specialty Clinics record the quickest rise at an 8.49% CAGR, appealing to women who prefer boutique environments and shorter waiting times. The 2024 NHI DBT fee schedule allows clinics to offset higher acquisition costs, making tomosynthesis a differentiator. Clinics partner with corporations to deliver on-site screening, securing steady patient flow. Cloud-first IT infrastructure lets them outsource image reads to teleradiology hubs, lowering fixed staffing requirements. Others, including mobile units and corporate medical centers, capture incremental demand but remain fragmented. Over time, hospital-clinic collaboration via shared PACS may harmonize referral pathways.

By Technology: FFDM Dominates but DBT Gains Momentum

Full-Field Digital Mammography (FFDM) held 57.12% of the 2025 installed base and continues to underpin routine screening. Providers appreciate its lower exam time and established reimbursement. AI-enhanced computer-aided detection (CAD) increases specificity to 93%, reducing false positives and radiologist fatigue.

Digital Breast Tomosynthesis expands at a 9.05% CAGR, propelled by its 32.2% higher cancer detection rate and 17.8% recall reduction. Vendors integrate synthesized 2D images that eliminate extra exposure, satisfying patient concerns. Tomosynthesis-ready gantries see strong trade-in demand, especially in urban flagship hospitals aiming for accreditation bonuses. CAD vendors tune algorithms for 3D stacks, offering lesion risk scores that feed into AI triage dashboards. Computer-Aided Detection, now bundled with both FFDM and DBT, acts as decision support rather than primary reader, reflecting Japan’s regulatory stance that AI complements but does not replace clinicians.

Geography Analysis

Metropolitan Tokyo-Osaka-Nagoya corridors dominate the Japan mammography market, reflecting dense populations, higher disposable income, and concentration of tertiary hospitals. Facilities here migrate fastest to DBT and AI-enabled CAD because capital budgets are larger and staff shortages less acute. Urban providers participate in multi-center AI validation studies, gaining early access to software updates.

Regional cities such as Sapporo, Fukuoka, and Hiroshima form the mid-tier cluster. They adopt refurbished DR systems to balance cost and compliance, with DBT added selectively. Prefectural governments co-fund mobile screening schedules that rotate through suburban wards, spreading demand across device categories. Workforce issues emerge, but provincial medical schools launch accelerated technologist programs to stem the shortfall.

Rural prefectures in Tohoku and Kyushu trail in adoption yet contribute to niche growth through mobile vans equipped with DBT-ready detectors. Tele-reading links to university hospitals supplement the scarcity of JABTS-certified staff. Broadband investments under Japan’s digital-rural initiative improve image transfer speed, allowing same-day reporting. Over the forecast period, targeted subsidies and mobile solutions narrow regional inequities, supporting uniform uptake nationwide.

Competitive Landscape

The Japan mammography market features moderate concentration. Domestic champions—Canon Medical Systems, Fujifilm, and Shimadzu—capitalize on local service networks and deep knowledge of regulatory nuances. Canon’s iterative upgrades to the Aquilion imaging line enhance cross-modality integration, creating lock-in for hospital groups. Fujifilm’s ASPIRE Cristalle gains DBT modules that retrofit older frames, shortening sales cycles. Shimadzu’s T-smart PRO reconstructs 3D slices with AI noise reduction, positioning the firm at the intersection of hardware and software innovation [3]“Tomosynthesis, Making the Invisible Visible,” Shimadzu Corporation, shimadzu.com.

Global majors—GE Healthcare, Siemens Healthineers, and Hologic—compete through advanced DBT workflows and cloud analytics. GE’s Pristina Via emphasizes ergonomic compression and patient-controlled paddles, marketed alongside AI quality-control modules to address workforce shortages. Siemens integrates breast density notification into its syngo platform, aiding compliance with emerging legislation. Hologic’s recent acquisition of a breast-care peer for USD 310 million signals aggressive portfolio expansion.

AI specialists such as LPIXEL and iCAD focus on algorithm accuracy for dense Asian breast tissue. Partnerships see hardware vendors pre-install AI packages, giving end-users a turnkey option. Vendor financing, trade-in guarantees, and training academies further intensify rivalry. Overall, top five suppliers collectively hold roughly 65% of 2024 revenues, reflecting balanced competition and continuous innovation.

Japan Mammography Industry Leaders

Fujifilm Holdings Corporation

Siemens Healthineers AG

GE Healthcare

Hologic Inc.

Climb Medical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Clairvo Technologies and Shukun Technology form a partnership to introduce Shukun’s multi-modality imaging AI, including mammography, to Japanese providers.

- August 2024: The Kazakh Institute of Oncology and Radiology signs a memorandum with Fujifilm to co-develop transportable mammography and radiology devices.

Japan Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. Japan Mammography Market is Segmented by Product Type (Digital Systems, Analog Systems, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Other Product Types (Biopsy-guided, Mobile units) |

By End User

| Hospitals |

| Specialty Clinics |

| Others |

By Technology

| Full-Field Digital Mammography (FFDM) |

| Digital Breast Tomosynthesis (DBT) |

| Computer-Aided Detection (CAD) |

| By Product Type | Digital Systems |

| Analog Systems | |

| Other Product Types (Biopsy-guided, Mobile units) | |

| By End User | Hospitals |

| Specialty Clinics | |

| Others | |

| By Technology | Full-Field Digital Mammography (FFDM) |

| Digital Breast Tomosynthesis (DBT) | |

| Computer-Aided Detection (CAD) |

Key Questions Answered in the Report

What is the current Japan Mammography Market size?

The Japan mammography equipment market size stands at USD 135.99 million in 2026.

Who are the key players in Japan Mammography Market?

Fujifilm Holdings Corporation, Siemens Healthineers AG, GE Healthcare, Hologic Inc. and Climb Medical Systems, Inc. are the major companies operating in the Japan Mammography Market.

Which product type leads installations?

Digital Systems hold the largest share at 70.92% of 2025 demand.

Why is DBT adoption accelerating?

The 2024 NHI reimbursement uplift and its 32.2% higher cancer detection rate drive a 9.05% CAGR for Digital Breast Tomosynthesis.

Page last updated on: