Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

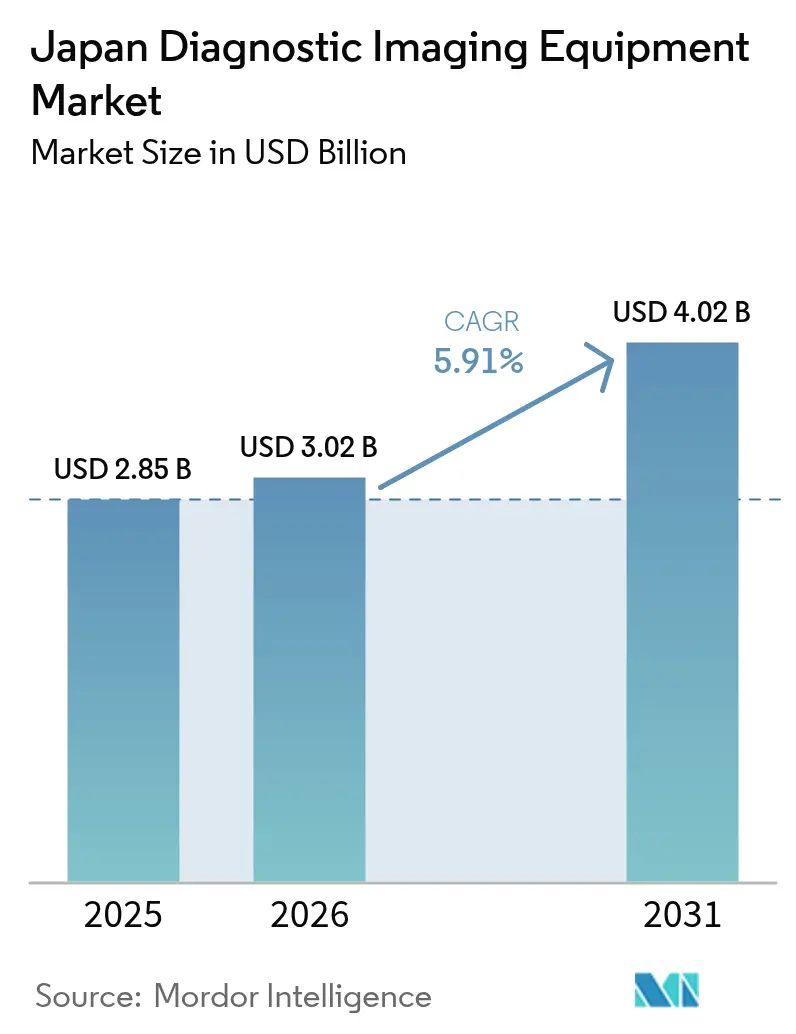

| Base Year Market Size (2025) | USD 2.85 Billion |

| Market Size (2026) | USD 3.02 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Japan diagnostic imaging equipment market size was valued at USD 2.85 billion in 2025 and estimated to grow from USD 3.02 billion in 2026 to reach USD 4.02 billion by 2031, at a CAGR of 5.91% during the forecast period (2026-2031). The current market underscores the country’s strong foundation in medical technology, built on an aging population, high equipment density, and active government digitization programs. Investors view the segment favorably as Society 5.0 and Medical DX policies accelerate AI integration, prompting hospitals to modernize fleets quickly.[1]Source: Ministry of Health, Labour and Welfare, “Medical DX Initiatives,” mhlw.go.jp Manufacturers benefit from rapid replacement cycles; for example, Canon Medical Systems expects imaging revenue to move from JPY 553.8 billion (USD 3.7 billion) in FY-2023 to JPY 582 billion (USD 3.9 billion) in FY-2024. At the same time, radiologist shortages have lifted demand for AI‐assisted workflows and teleradiology, mitigating workforce constraints. Collectively, these factors position the market for sustained mid-single-digit growth through the decade.

Key Report Takeaways

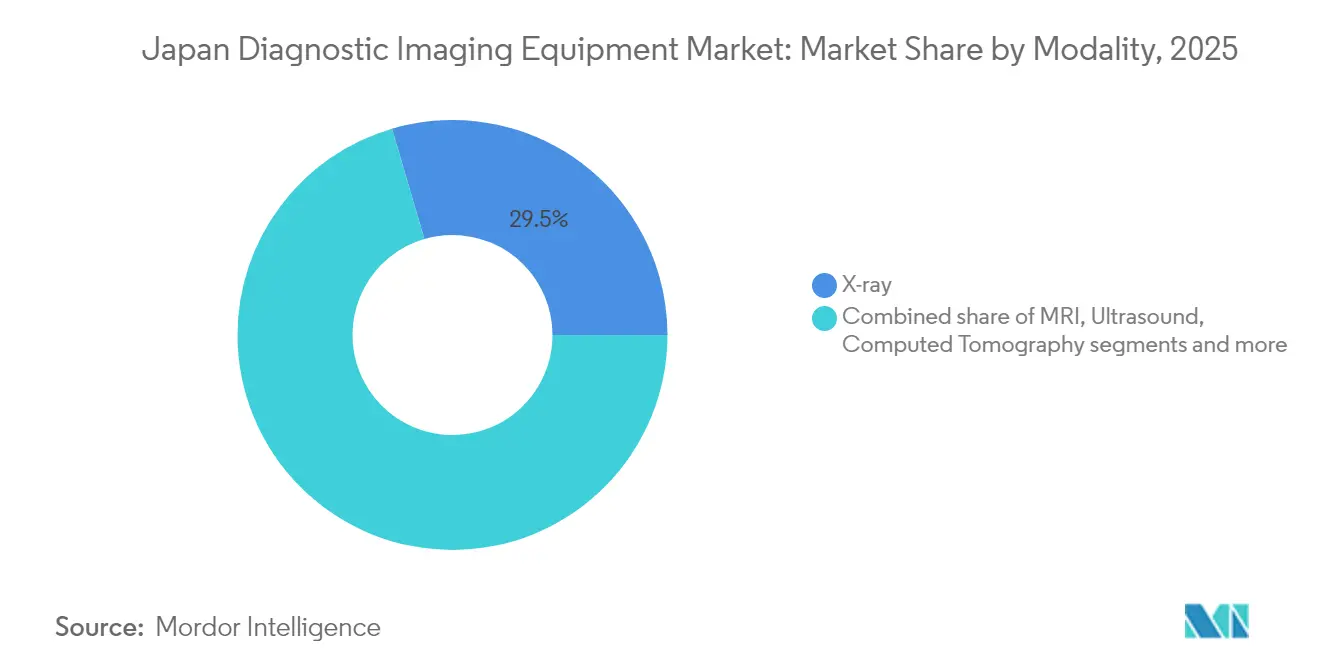

- By modality, X-ray systems held 29.54% of Japan diagnostic imaging equipment market share in 2025; computed tomography is projected to expand at a 6.89% CAGR to 2031.

- By portability, fixed systems accounted for 80.42% of the Japan diagnostic imaging equipment market size in 2025, while mobile and hand-held units are forecast to grow 7.58% per year to 2031.

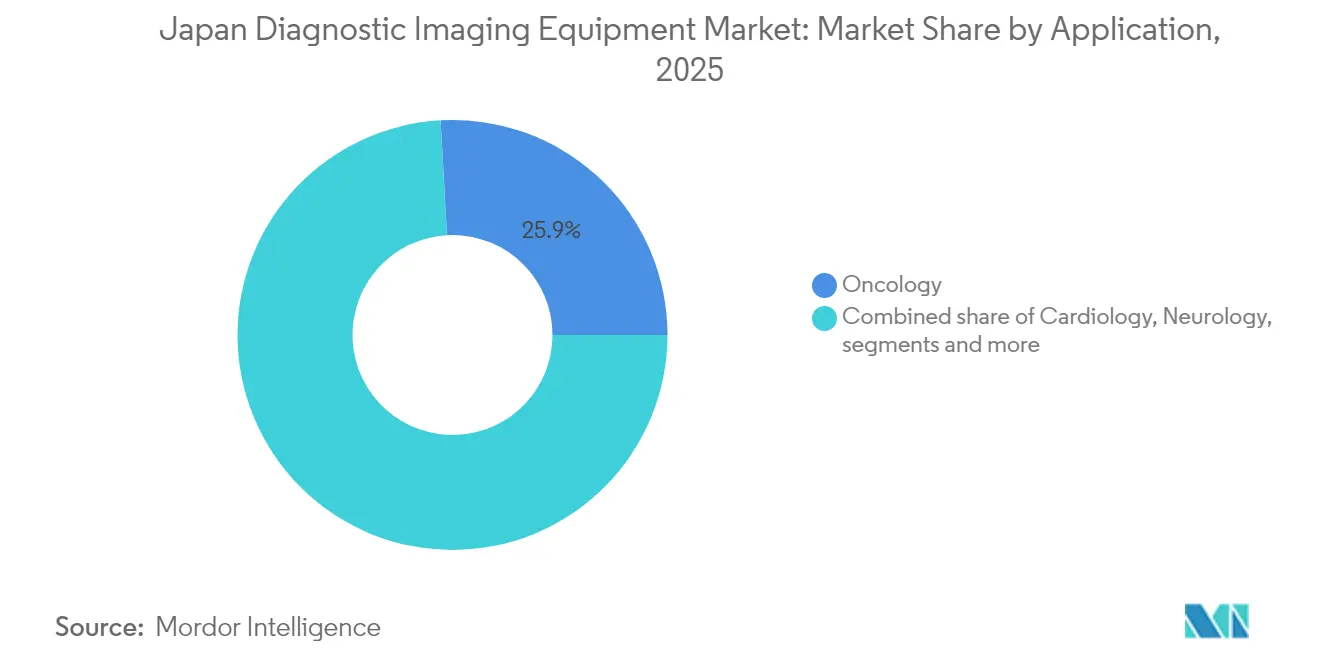

- By application, oncology captured 25.88% of the market in 2025; cardiology applications lead growth at 7.86% CAGR through 2031.

- By end-user, hospitals controlled 66.05% of revenue in 2025; diagnostic imaging centers are set to rise fastest at 7.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases | +1.8% | National, concentrated in urban aging centers | Long term (≥ 4 years) |

| Growing geriatric population | +2.1% | National, with highest impact in rural prefectures | Long term (≥ 4 years) |

| Rapid technological advancement | +1.5% | National, early adoption in major metropolitan areas | Medium term (2-4 years) |

| Government initiatives favoring early-stage screenings and domestic innovations | +1.2% | National, prioritizing underserved regions | Medium term (2-4 years) |

| Point-of-care & portable imaging demand in elder-care facilities | +0.9% | National, concentrated in rural and suburban areas | Short term (≤ 2 years) |

| Expansion of private outpatient imaging centers | +0.7% | Urban and suburban areas, major metropolitan regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising burden of chronic diseases

Cancer prevalence lifts equipment utilization across modalities. Gastric cancer alone affects roughly 1 million Japanese each year, spurring uptake of advanced endoscopic imaging such as AI Medical Service’s gastroAI that delivers 91.4% sensitivity for early lesions. Providers therefore prefer multi-modal suites capable of completing several scans in one visit, a trend boosting high-resolution CT and MRI installs throughout the Japan diagnostic imaging equipment market.

Growing geriatric population

With 29.56% of residents aged 65 or older in 2023—and rural areas surpassing 60%—portable solutions have become critical. Canon’s upright CT, which shortens exams by 40% for musculoskeletal cases, aligns with mobility limits common in elder care. As the Japan diagnostic imaging equipment market expands, point-of-care devices support home-visit nurses and mobile clinics serving super-aged communities.

Rapid technological advancements

Regulators now fast-track AI/ML approvals under dedicated PMDA review pathways, letting vendors like Neuspective integrate generative AI that flags report errors with 90%+ accuracy. Digital pathology pilots at Toyama Prefectural Central Hospital further illustrate convergence of imaging and analytics, encouraging facility-wide upgrades that keep the Japan diagnostic imaging equipment market on a steady modernization cycle.

Government initiatives favoring early-stage screenings and domestic innovations

METI’s Medical Device Industry Vision 2024 earmarks fiscal-2025 budgets to help startups globalize and to subsidize cybersecurity improvements. JIRA’s Industry Vision 2030 sets parallel targets for AI deployment and export promotion, reinforcing a supportive ecosystem that underpins long-term growth of the Japan diagnostic imaging equipment market.[2]Source: Japan Medical Imaging and Radiological Systems Industries Association, “JIRA Industry Profile 2024,” jira-net.or.jp

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & lifecycle costs of products | -1.1% | National, acute impact on smaller healthcare facilities | Short term (≤ 2 years) |

| Stringent regulatory regulations | -0.8% | National, affecting all market participants | Medium term (2-4 years) |

| Shortage of trained radiologists and technologists | -0.6% | National, severe in rural and remote areas | Long term (≥ 4 years) |

| Radiation-dose safety concerns | -0.4% | National, heightened awareness in pediatric facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High acquisition & lifecycle costs of products

Price sensitivity delayed Shimadzu’s domestic imaging sales, which fell 2.3% in 1H-FY 2024 as clinics postponed replacements. Consequently, vendors are piloting pay-per-scan financing and shared-service models to ensure that budget-constrained buyers remain engaged in the Japan diagnostic imaging equipment market.

Stringent regulatory regulations

Class III and IV devices require full MHLW approval and PMDA audits, stretching timelines for photon-counting CT and other complex innovations. Added cybersecurity rules issued in March 2024 raise compliance spend, slowing product launches and trimming growth potential within the Japan diagnostic imaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-ray Dominance Drives Market Foundation

X-ray systems maintained a 29.54% share of the Japan diagnostic imaging equipment market in 2025, underlining their role as the entry point for routine diagnostics in almost all clinical settings. Computed tomography now carries the fastest 6.89% CAGR, supported by photon-counting platforms that lower dose while improving contrast. As a result, the Japan diagnostic imaging equipment market size allocated to CT is projected to outpace traditional modalities by 2031. MRI adoption remains stable, driven by neurological and orthopedic demands, whereas ultrasound enjoys steady upgrades through AI-guided workflow tools. Nuclear imaging and mammography grow steadily under national cancer-screening programs. Together these trends illustrate how the Japan diagnostic imaging equipment industry is migrating from basic radiography to advanced, multimodal precision imaging.

Growing differentiation pressures favor vendors offering hybrid scanners and AI overlays that unify multi-modal outputs on a single viewer. Canon, Fujifilm, and GE HealthCare are investing in algorithm-ready consoles to extend equipment life cycles and safeguard margins within the fiercely competitive Japan diagnostic imaging equipment market.

By Portability: Fixed Systems Scale Meets Mobile Innovation

Fixed rooms captured 80.42% of 2025 revenue and remain the operational backbone for tertiary hospitals. Nevertheless, mobile and hand-held units are forecast to grow 7.58% CAGR through 2031 as remote-island medical MaaS pilots equip vans with bedside X-ray, handheld ultrasound, and cloud PACS links. The market size attached to portable categories could therefore double over the decade. For rural prefectures, compact battery-powered ultrasound devices from Philips and Fujifilm represent a cost-effective path to universal imaging access.

Manufacturers pursue ruggedized designs and AI-on-edge capabilities to withstand transport vibration and patchy connectivity. The Japan diagnostic imaging equipment industry now evaluates total ecosystem value—software, training, and service contracts—rather than unit sales alone, creating space for ancillary players in data security and telehealth platforms.

By Application: Oncology Leadership Amid Cardiology Acceleration

Oncology generated 25.88% of 2025 revenue, reflecting Japan’s intensive cancer-screening infrastructure. Cardiology imaging, however, is expanding fastest at 7.86% CAGR as population aging inflates coronary disease incidence and drives uptake of echocardiography, CT angiography, and MRI perfusion studies. The Japan diagnostic imaging equipment market size devoted to cardiac applications benefits from AI tools that automate ejection-fraction measurement and plaque characterization.

Neurology remains stable thanks to high MRI density, while gastroenterology receives a technological boost from AI endoscopy detecting early gastric lesions. Women’s health relies on advanced ultrasound and digital breast tomosynthesis, and emergency settings increasingly request mobile CT for rapid trauma triage. Together these niches reinforce cross-modality investment plans in the Japan diagnostic imaging equipment market.

By End-User: Hospital Concentration Versus Imaging Center Growth

Hospitals captured 66.05% of market revenue in 2025, leveraging integrated RIS/PACS and in-house specialists. Diagnostic imaging centers, however, register the highest 7.79% CAGR, serving corporate screening programs and patient demand for shorter wait times. As these centers proliferate, the Japan diagnostic imaging equipment market share held by outpatient facilities will continue to climb through 2031.

Ambulatory surgery centers and specialty clinics also expand, enabled by compact 64-slice CT and high-frequency ultrasound that fit limited floor space. Public institutions prioritize comprehensive coverage, whereas private chains emphasize premium modalities to differentiate. Vendors tailoring flexible service contracts and rapid response maintenance will capture loyalty across this diverse buyer base inside the Japan diagnostic imaging equipment market.

Geography Analysis

Regional dynamics show unexpected leadership by rural facilities, which often possess state-of-the-art scanners supplied under equitable allocation programs dating back two decades. Remote areas now complement fixed suites with portable gear and tele-consultation networks, ensuring that aging residents receive comparable diagnostic accuracy to urban peers inside the Japan diagnostic imaging equipment market.

Metropolitan hubs such as Tokyo, Osaka, and Nagoya host academic hospitals with early access to AI prototypes and photon-counting CT. Urban centers also attract software startups, which cooperate with OEMs to embed analytics directly into consoles, reinforcing a virtuous cycle of innovation in the Japan diagnostic imaging equipment market.

The geographic split therefore compels vendors to design modular portfolios: high-throughput scanners for dense cities and rugged portable kits for islands and mountain clinics. Government subsidies encourage this balanced deployment, sustaining equitable imaging access and underpinning universal coverage across the Japan diagnostic imaging equipment market.

Regulatory Landscape

Diagnostic imaging equipment in Japan is regulated under the Act on Securing Quality, Efficacy and Safety of Products Including Pharmaceuticals and Medical Devices (PMD Act), with risk-based classification from Class I to Class IV. The Pharmaceuticals and Medical Devices Agency (PMDA) conducts scientific review and audits, while the Ministry of Health, Labour and Welfare (MHLW) grants marketing authorization. For new medical devices, PMDA publishes target review timelines (commonly cited at around 14 months), which affects launch planning for high-end CT, MRI, and advanced ultrasound platforms.

Policy and compliance requirements have continued to track digitalization and supply resiliency priorities. Amendments to the PMD Act enacted in May 2025 included measures aimed at supply security and product availability, and certain provisions entered into force on May 1, 2026, adding operational focus for manufacturers and MAHs on continuity and governance. Alongside this, PMDA has maintained dedicated evaluation capabilities for Software as a Medical Device (SaMD), including AI-based diagnostic support, supporting clearer pathways for CADe/CADx-type imaging software while increasing the importance of cybersecurity and post-market update discipline for connected imaging systems.

Competitive Landscape

The field is moderately concentrated: Canon Medical Systems, Fujifilm Holdings, and Shimadzu together hold well over half of domestic modality shipments, while GE HealthCare, Siemens Healthineers, and Philips compete via specialized offerings and joint R&D. Canon’s FY-2023 imaging revenue rose 7.9% and management guides for continued growth on the back of AI-ready CT and ultrasound launches. Olympus’s partnership with Canon on the Aplio i800 endoscopic ultrasound underscores a broader trend toward ecosystem alliances that blend optics, software, and hardware.[3]Source: Olympus Corporation, “Canon Medical Systems and Olympus Announce Business Alliance,” olympus.de

New entrants pivot around software; Neuspective’s report-quality AI and Intec’s EXpath digital pathology layer onto existing scanners, enabling hospitals to postpone costly hardware replacement while upgrading diagnostic accuracy. Meanwhile, local startup Lilium Otsuka released the compact ultrasonic bladder device “Lilium One,” distributed nationwide by Otsuka Pharmaceutical Factory to broaden urological use cases within the Japan diagnostic imaging equipment market.

Raising barriers, PMDA instituted a streamlined AI/ML evaluation unit in 2024, giving domestic firms an edge thanks to regulatory familiarity. Multinationals must therefore pursue co-development with Japanese partners or acquire local certification expertise. Looking forward, advantage will belong to vendors offering interoperable suites that bundle scanners, AI applications, cybersecurity, and lifecycle services tailored to disparate care settings of the Japan diagnostic imaging equipment market.

Japan Diagnostic Imaging Equipment Industry Leaders

Koninklijke Philips N.V.

Canon Medical Systems Corporation

Siemens Healthineers AG

GE HealthCare

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Medical DX and the shift toward secure, interoperable health-data infrastructure are creating whitespace in imaging ecosystems that combine hardware refresh with cloud connectivity, cybersecurity, and AI applications. PMDA has established specific review points for CADe/CADx programs for radiological and endoscopic images, and it maintains a dedicated SaMD review function, which supports commercialization of AI overlays that improve throughput and reporting consistency in a market facing workforce constraints.

Platform-led programs also offer near-term routes to scale imaging-adjacent software and data services. In May 2026, SoftBank Corp, SMBC Group, and Fujitsu signed a basic agreement to build a Japan-developed healthcare platform (targeting 60 million users and 4,000 medical institutions). In May 2026, Fujitsu and IBM Japan formalized collaboration to develop a sovereign cloud platform for medical use and joint utilization of medical AI, including EHR solutions running on this platform. Together, these initiatives support diagnostic imaging OEMs and software vendors in cloud-connected modalities, enterprise imaging integration, and AI-assisted workflows that align with data sovereignty and continuous update requirements, helping outpatient imaging centers and multi-site hospital systems standardize imaging pathways across networks.

Recent Industry Developments

- April 2026: Canon Medical Systems launched Ultimion, positioned as the first domestically produced photon-counting CT system in Japan. Clinical research at the National Cancer Center Hospital East supports evidence generation for premium CT differentiation and strengthens local high-end manufacturing positioning.

- February 2025: Canon Medical Systems introduced Aplio Beyond, a high-performance ultrasound platform aimed at improving image quality and workflow across multiple specialties. The launch reinforces competitive intensity in ultrasound upgrades as providers prioritize productivity features and AI-ready consoles.

- September 2024: Olympus began sales in Japan of the Aplio i800 ultrasound system for endoscopic use, co-developed with Canon Medical Systems. The alliance expands access to specialized hepatobiliary and gastrointestinal imaging workflows and highlights ecosystem partnerships that blend optics, software, and ultrasound hardware.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan diagnostic imaging equipment market covers revenues generated from the sale of imaging systems used to create diagnostic images in human healthcare settings across Japan.

Scope exclusions: We exclude refurbished or rental units, standalone service and maintenance contracts, and veterinary imaging systems from this market sizing.

Segmentation Overview

- By Modality

- X-ray

- MRI

- Ultrasound

- Computed Tomography

- Nuclear Imaging

- Mammography

- Other Modalities

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics and Trauma

- Gastroenterology and Hepatology

- Women’s Health and Obstetrics

- Other Applications

- By End-User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgery and Specialty Clinics

- Home-care / Long-term-care Facilities

Data Sources, Market Sizing, and Validation

Desk Research

We first built the market boundaries and demand signals using public sources that consistently report Japan healthcare capacity and utilization, such as the Ministry of Health, Labour and Welfare, Statistics Bureau of Japan, OECD Health Statistics, and the World Bank. We also used publications from imaging and radiology associations, along with peer reviewed clinical journals, to understand modality adoption trends and care pathway changes.

Next, the desk work was used to anchor assumptions like hospital and imaging center counts, equipment density, replacement cycles, and procurement direction. Company annual reports, investor presentations, press releases, and reputable business news were used to map product portfolios and shipment discussions, and then cross checked against a paid subscription for company financials and intelligence where needed. These sources are illustrative only, and many other public references were also used for data collection, validation, and clarifying gaps.

Primary Interviews and Surveys

To convert broad indicators into a workable model, we spoke with a mix of hospital procurement teams, radiology department leaders, diagnostic imaging centers, distributors, and service partners across Japan. These discussions helped confirm what gets purchased versus upgraded, how mobile and fixed systems are prioritized, and how pricing typically changes across modality generations, which then improved our final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | |

| Mid tier: 43% | Functional/Unit leaders: 38% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using top down logic where Japan level demand is reconstructed from the installed base, replacement timing, and annual procurement flow across key modalities (such as X-ray, CT, MRI, ultrasound, nuclear imaging, and mammography). To keep the totals realistic, we then corroborated the result with selective bottom-up approximations, mainly by sampling typical system pricing ranges, checking shipment and tender visibility, and rolling up a limited set of supplier revenues where disclosures were clear.

A few inputs were treated as the main market fingerprints, and they were updated until they aligned with what practitioners see in the field. These included hospital and imaging center procedure volumes, scanner density and utilization patterns, share of fixed systems versus mobile or hand-held, replacement cycles driven by uptime needs, and reimbursement or care pathway shifts that change scan mix. Where bottom-up evidence was incomplete (for example, private pricing dispersion by facility size), we used ranges from interviews and applied conservative midpoint assumptions, which were then stress tested.

Forecasting was done using scenario analysis supported by trend smoothing on historical demand signals, and the scenarios were tied to practical drivers like aging demographics, budget cycles, modality refresh waves, and adoption of AI-enabled workflows. Assumptions were reviewed with interviewees so the forward curve stayed consistent with procurement reality rather than only statistical continuation.

Data Validation & Update Cycle

We validate the model by comparing outputs across multiple independent checks, and then reviewing any variance that cannot be explained by scope or timing. If an assumption drives a large swing (for example, an unusually high replacement rate in one modality), it is flagged for a second analyst review and is rechecked with an additional call.

Each report is refreshed annually, and interim updates are triggered when material events occur, such as reimbursement changes or large scale procurement programs. Before delivery, the analyst team performs a fresh pass on key inputs and currency timing so clients receive an updated view that matches the latest available signals.

Mordor Intelligence's Japan Diagnostic Imaging Equipment Market Market Size Versus Other Published Estimates

It is common to see different market values reported for Japan diagnostic imaging equipment because publishers do not always count the same revenue streams or use the same year and currency timing. Differences also show up when one study emphasizes installed base replacement while another leans more on reported sales snapshots.

By tracking replacement cycle logic and modality level procurement checks, Mordor Intelligence keeps the market total tied to equipment purchases in Japan while avoiding double counting from service contracts or refurbished units, which is a key reason this value can differ from estimates built from broader device definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.85 B (2025) | |

| Industry Research Publisher A | USD 2.10 B (2024) | Uses an earlier valued year and does not clearly separate new system sales from adjacent revenue items, which can shift totals when pricing and procurement timing change year to year. |

| Industry Research Publisher B | USD 1.65 B (2024) | Appears to follow a narrower device scope and a different end user boundary, which can reduce counted revenues when imaging center and hospital procurement pathways are treated differently. |

The spread across sources mainly comes from year selection and what is counted as equipment revenue versus adjacent services or broader device baskets. With a clearly stated scope and repeatable demand drivers, the approach gives buyers a practical number they can trace back to replacement, utilization, and purchasing behavior.

Key Questions Answered in the Report

How is artificial intelligence reshaping diagnostic imaging workflows in Japan?

AI tools now flag reporting errors in real time, guide optimal scan parameters, and prioritize urgent cases, allowing radiologists to focus on complex interpretations while easing nationwide staffing shortages.

Why are mobile and hand-held imaging devices gaining traction in rural prefectures?

Portable scanners enable on-site exams at community clinics and visiting-nurse stations, reducing travel burdens for elderly patients and supporting teleconsultations with urban specialists.

How do government digitization programs influence hospital purchasing decisions?

Society 5.0 and Medical DX policies tie reimbursement to interoperable data standards, so facilities are prioritizing equipment that integrates seamlessly with national health information platforms.

What strategies are Japanese manufacturers using to stay competitive against global brands?

Domestic leaders bundle hardware with proprietary AI software, form alliances that combine optics and imaging, and leverage fast-track local regulatory pathways to shorten time-to-market.

How are outpatient imaging centers reshaping service delivery?

Specialized centers offer faster appointments and focused expertise, prompting hospitals to shift routine scans off-site while retaining advanced procedures in-house to optimize resource use.

In what ways is cybersecurity impacting equipment design and procurement?

New PMDA guidance requires built-in encryption and continuous patch support, so buyers favor vendors with robust update roadmaps and proven compliance records.

Page last updated on: