Japan Diagnostic Imaging Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

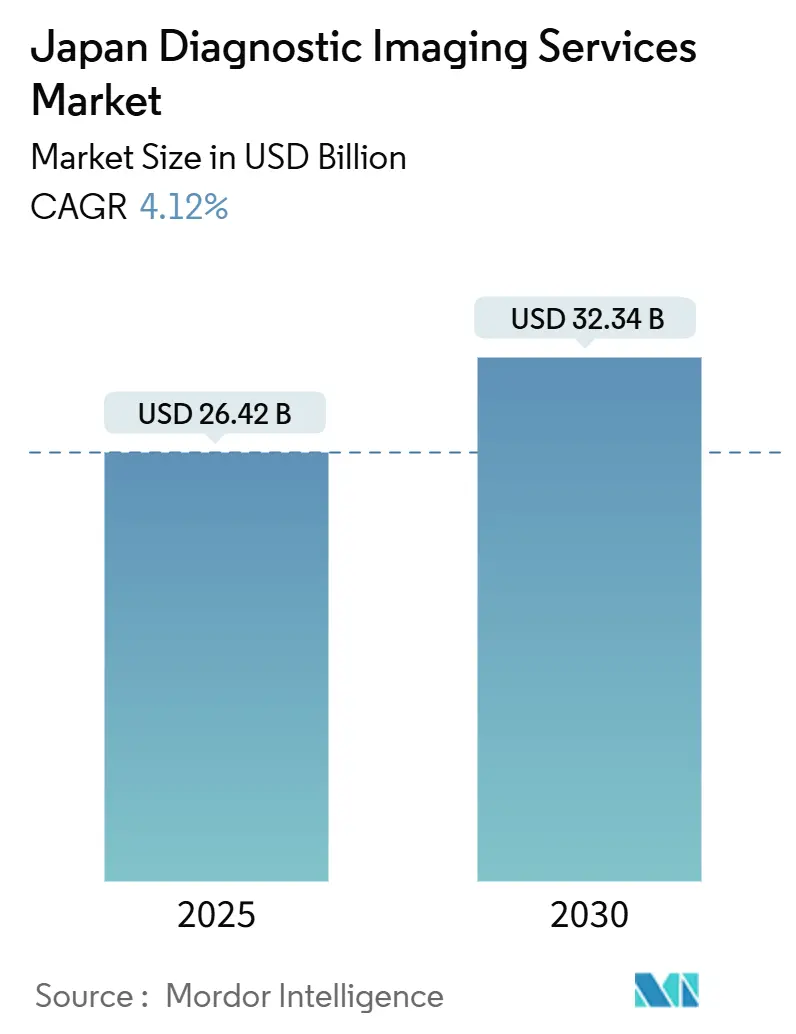

| Market Size (2025) | USD 26.42 Billion |

| Market Size (2030) | USD 32.34 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

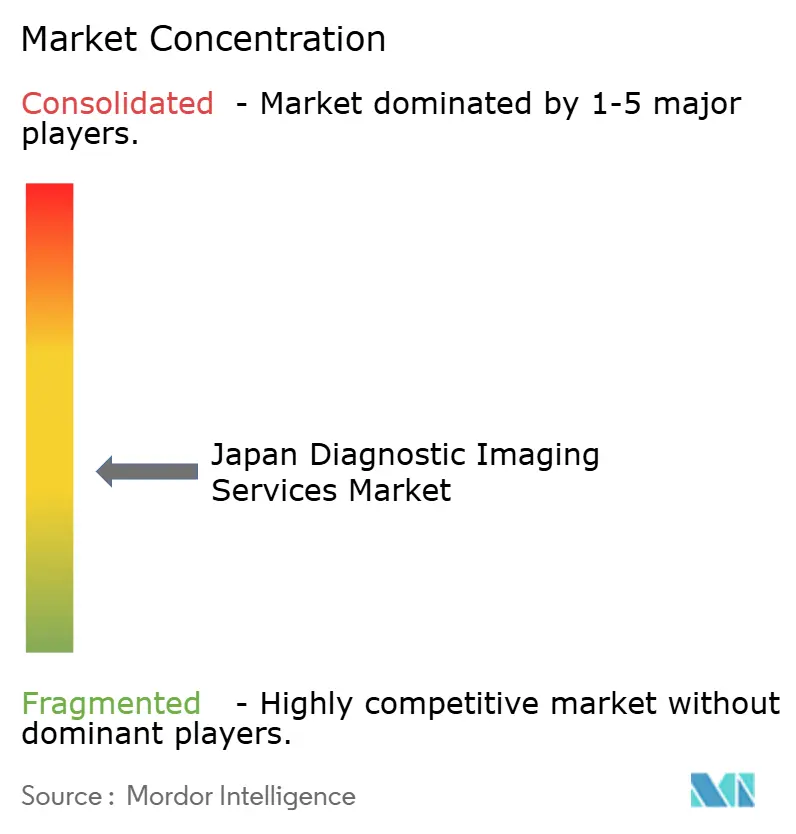

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Diagnostic Imaging Services Market Analysis by Mordor Intelligence

The Japan Diagnostic Imaging Services Market size is estimated at USD 26.42 billion in 2025, and is expected to reach USD 32.34 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

The upward trajectory is propelled by the country’s super-aged demographic structure, rapid diffusion of artificial intelligence across imaging workflows, and steady capital spending on modality upgrades despite hospital budget constraints. Consistent volume growth across X-ray, CT, MRI, ultrasound, and nuclear imaging counters workforce shortages by encouraging efficiency-boosting technologies such as triage algorithms and structured reporting. Portable ultrasound and flat-panel detector (FPD) radiography widen access in smaller facilities, while teleradiology hubs narrow urban–rural gaps. The combined effect is that the Japan diagnostic imaging services market now operates at the crossroads of population pressure and digital transformation, creating parallel opportunities for equipment vendors, software developers, and service providers prepared to embrace outcome-based care models.

Key Report Takeaways

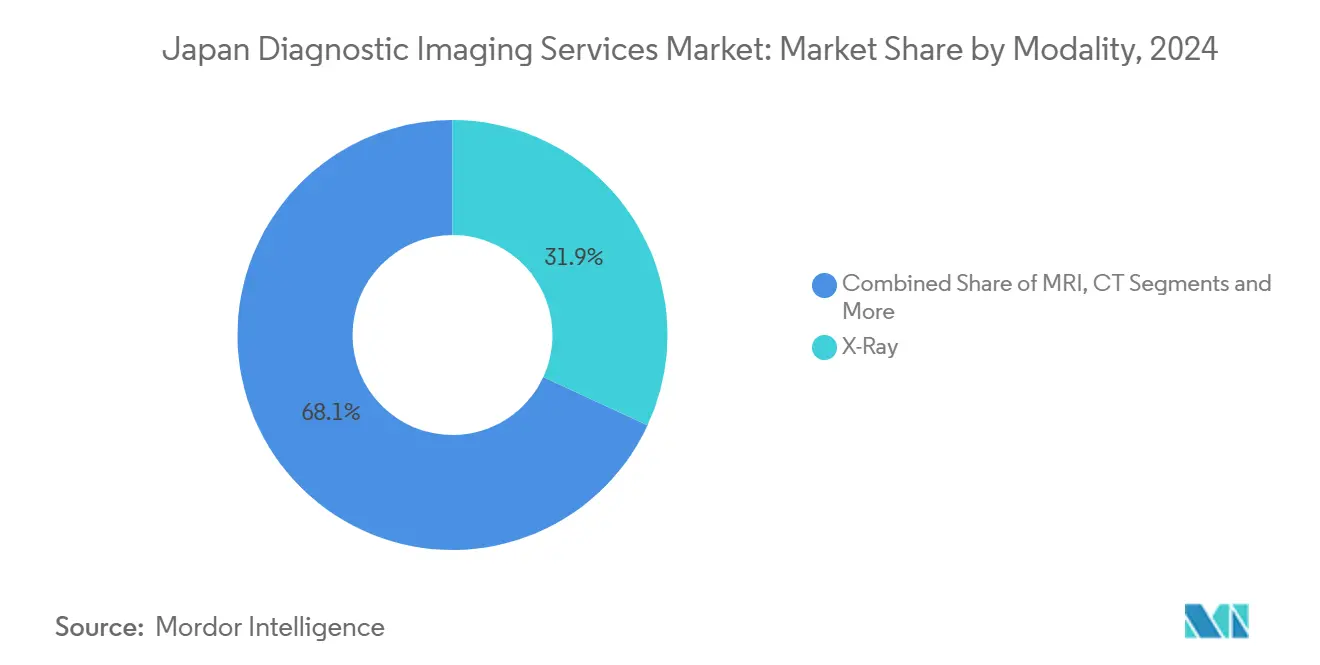

- By modality, X-ray services led with 31.86% revenue share in 2024; ultrasound is forecast to grow at a 5.16% CAGR to 2030.

- By application, oncology accounted for 25.12% of market revenue in 2024; cardiology applications are projected to register a 5.69% CAGR through 2030.

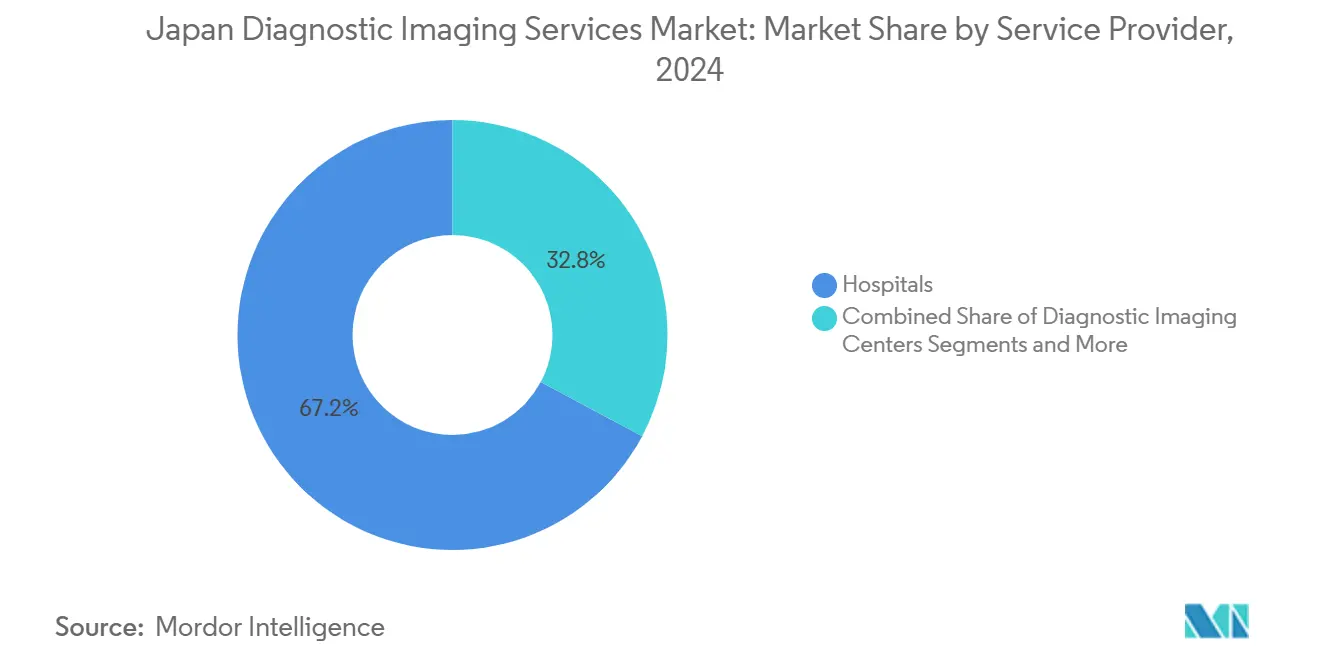

- By service provider, hospitals held 67.16% of the Japan diagnostic imaging services market share in 2024; diagnostic imaging centers are expected to expand at a 4.91% CAGR over the same period

Japan Diagnostic Imaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of AI-Reimbursed Imaging Procedures | +0.8% | National, concentrated in urban centers | Medium term (2-4 years) |

| Accelerating Replacement of Aging Analog Units With DR/FPD X-Ray Systems | +0.6% | National, priority in rural facilities | Short term (≤ 2 years) |

| Government Stimulus for Rural Teleradiology Hubs | +0.4% | Rural prefectures, Tohoku region focus | Medium term (2-4 years) |

| Rising Chronic-Disease Workload in Super-Aged Prefectures | +0.9% | Rural prefectures, Akita, Shimane leading | Long term (≥ 4 years) |

| Vendor Financing & Pay-Per-Scan Business Models | +0.3% | Sub-100 bed hospitals nationwide | Short term (≤ 2 years) |

| Surge In Demand for Pre-Therapeutic Imaging in Proton-Beam & CAR-T Centers | +0.2% | Major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of AI-Reimbursed Imaging Procedures

Japan’s 2024 reimbursement reform covering computer-aided detection (CAD) tools transformed imaging economics by neutralizing adoption costs for hospitals and imaging centers. Early adopters report 30% faster read times and higher lesion-detection sensitivity, enabling facilities to handle more studies without increasing radiologist headcount.[1]Masashi Misawa et al., “Implementation of Artificial Intelligence in Colonoscopy Practice in Japan,” JMA Journal, JMAJ.JP The policy especially benefits high-volume mammography, chest CT, and gastrointestinal endoscopy programs where throughput gains translate into direct revenue. Seamless PACS integration and cloud deployment allow rapid scaling across institutions, positioning first movers to consolidate referral networks. As additional modalities secure coverage, the Japan diagnostic imaging services market is expected to record accelerated AI deployment, reinforcing productivity gains while improving diagnostic standardization.

Accelerating Replacement of Aging Analog Units With DR/FPD X-Ray Systems

More than 60% of rural hospitals were still operating cassette-based radiography units in 2024, prompting a nationwide push toward FPD systems that cut radiation dose by up to 36% and boost exam throughput by 25%.[2]Hiroki Kawashima et al., “Radiation Dose Considerations in Digital Radiography with an Anti-Scatter Grid,” PubMed, NCBI.NLM.NIH.GOV Government subsidies and vendor-backed financing mitigate up-front capital needs, particularly for sub-100-bed facilities that face tight budgets. Fast image availability shortens patient wait times, while automated exposure settings raise image consistency, easing radiologist workload. The modernization wave enlarges the addressable equipment base for manufacturers and underpins steady service contract revenue, reinforcing the evolution of the Japan diagnostic imaging services market toward fully digital workflows.

Government Stimulus for Rural Teleradiology Hubs

Dedicated funding has established six regional hub-and-spoke networks that route studies from small clinics to metropolitan specialists in real time. Each hub serves multiple spoke sites within a 50 km radius, leveraging high-speed fiber and standardized DICOM protocols. Emergency CT cases now receive expert reads within 15 minutes instead of overnight, directly improving stroke and trauma outcomes. Sustainability hinges on robust service-level agreements, image quality assurance procedures, and coordinated staffing schedules. Successful pilots are expected to be replicated across rural prefectures, improving access to advanced diagnostics and increasing utilization across the Japan diagnostic imaging services market.

Rising Chronic-Disease Workload in Super-Aged Prefectures

Older adults account for 70% of imaging volumes in prefectures where aging ratios exceed 35%. Multimorbidity drives serial imaging for cardiovascular, oncologic, and musculoskeletal conditions, creating predictable demand that underwrites investment in multi-modality suites. Smaller hospitals introduce geriatric-focused protocols incorporating low-dose CT and abbreviated MRI to minimize patient stress. Chronic disease clustering thus reinforces a stable, volume-based revenue foundation that sustains the long-run expansion of the Japan diagnostic imaging services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Physicist & Radiologist Shortages Constrain Scanner Utilisation | -1.2% | National, acute in rural areas | Long term (≥ 4 years) |

| Lengthy PMDA Approval Cycles for SaMD/AI Algorithms | -0.4% | National regulatory impact | Medium term (2-4 years) |

| High Total Cost of Ownership for Multi-Slice CT & 3T MRI In Sub-100-Bed Hospitals | -0.6% | Rural and suburban facilities | Short term (≤ 2 years) |

| Rising Public Anxiety Over Cumulative Radiation Dose | -0.3% | National, post-Fukushima sensitivity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Physicist & Radiologist Shortages Constrain Scanner Utilisation

Only 8,610 radiologists are available nationwide, far below demand, with attrition now running at 3% annually.[3]“Radiologists in Japan are Scanning the Horizon,” Nature, NATURE.COM Staffing gaps force many scanners to sit idle during evenings and weekends, capping throughput at 60% of potential capacity in some prefectures. The shortage also slows the rollout of advanced modalities that require sub-specialty expertise, thereby tempering the expansion pace of the Japan diagnostic imaging services market. AI triage tools alleviate but do not eliminate the constraint, as final reads still require certified physicians.

Lengthy PMDA Approval Cycles for SaMD/AI Algorithms

The Pharmaceuticals and Medical Devices Agency's regulatory framework for software as medical devices creates approval timelines that lag behind rapid AI technology development cycles. While Japan’s Pharmaceuticals and Medical Devices Agency has modernized its framework, complex adaptive algorithms still face 12–18 month assessment timelines. The delay slows access to bleeding-edge diagnostic support systems, forcing providers to rely on legacy software. The approval delays force healthcare providers to rely on legacy diagnostic methods while advanced AI solutions remain in regulatory review, limiting potential efficiency gains and competitive advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-Ray Dominance Amid Ultrasound Innovation

X-ray retained 31.86% of the Japan diagnostic imaging services market share in 2024, generating stable revenue from routine chest, skeletal, and abdominal studies. Portable FPD systems now penetrate emergency departments and nursing homes, lifting daily exam counts and reducing patient transfer needs. In parallel, the Japan diagnostic imaging services market size for ultrasound is projected to expand briskly as Compact 5000 series platforms enable cardiology, obstetrics, and point-of-care assessments at the bedside.

Ultrasound’s 5.16% CAGR is further supported by AI modules that automate left-ventricular ejection fraction and thyroid nodule classification, freeing clinicians to focus on complex findings. CT and MRI remain indispensable for oncology staging and neurologic workups, yet their growth is moderated by price ceilings and staffing limits. Nuclear imaging benefits from GE HealthCare’s acquisition of the remaining stake in Nihon Medi-Physics, which secures domestic radioisotope supply and safeguards continuity for cardiology SPECT and PET oncology protocols.

By Application: Oncology Leadership Drives Cardiology Growth

Oncology generated 25.12% of 2024 revenues, confirming its role as the leading application cluster in the Japan diagnostic imaging services market. Multi-modal workflows span low-dose CT for lung cancer screening, MRI for prostate staging, and PET-CT for therapy monitoring. Complementary reimbursement incentives ensure sustained throughput and stable payer mix, anchoring investment in hybrid scanners.

Cardiology, advancing at a 5.69% CAGR, is propelled by rising arrhythmia detection programs and coronary CT angiography adoption. AI-enabled plaque quantification adds clinical value and shortens report cycles, making advanced cardiac imaging commercially viable for community providers. Neurology, orthopedics, and gastroenterology follow closely, supported by aging-related disease prevalence and periodic screening mandates that collectively reinforce the long-run resilience of the Japan diagnostic imaging services market.

By Service Provider: Hospital Dominance Shifts Toward Specialized Centers

Hospitals contributed 67.16% of market value in 2024, capitalizing on comprehensive modality portfolios and integrated care pathways. Academic centers in Tokyo and Osaka wield research grants and specialist depth to introduce cutting-edge protocols, setting performance benchmarks for smaller institutions. Nevertheless, the Japan diagnostic imaging services market size captured by independent imaging centers is climbing, as high-throughput operations reduce per-scan costs and deliver rapid turnaround that appeals to self-referring physicians.

Centers leverage extended hours, AI-prioritized worklists, and patient-friendly scheduling apps to win share from crowded outpatient departments. Clinics and specialty centers address niche requirements such as musculoskeletal MRI for sports injuries or obstetric ultrasound for maternity care, rounding out a diversified provider ecosystem that channels patient choice across the Japan diagnostic imaging services market.

Geography Analysis

Tokyo, Kanagawa, and Osaka collectively account for a significant portion of the Japan diagnostic imaging services market, reflecting dense hospital clusters, abundant subspecialists, and higher disposable incomes. Urban providers routinely adopt AI decision-support earlier and invest in multi-layer PACS-RIS integrations, creating a technology gap with peripheral regions. Rural prefectures, notably Akita where residents aged 65+ constitute 39%, face limited scanner availability and longer appointment queues, accelerating telehealth reliance.

Government-funded teleradiology hubs have demonstrated a 25% reduction in report turnaround times in pilot municipalities, bridging access gaps while stimulating incremental volumes in local spokes. Mobile CT and mammography vans further extend reach, enabling annual screenings in mountainous communities where hospital density is low. The geography-driven utilization asymmetry is expected to narrow gradually as fiber connectivity widens and cloud-native AI platforms facilitate centralized reading across the Japan diagnostic imaging services market.

University hospitals in metropolitan areas function as referral magnets, drawing complex oncology, cardiology, and neurology cases from neighboring prefectures. Patient migration underscores the need for interoperable imaging archives that accompany individuals across care settings, a trend that encourages vendors to offer vendor-neutral archives (VNA) with national patient ID mapping. As demographic pressure intensifies, regional authorities collaborate with industry to launch capacity-building programs for radiographers and nuclear medicine technologists, ensuring that modality expansions translate into realized scanning hours rather than idle assets. The combined urban leadership and rural catch-up dynamic will shape the spatial evolution of the Japan diagnostic imaging services market over the next decade.

Competitive Landscape

The Japan diagnostic imaging services industry exhibits moderate concentration, with top university hospitals, public cancer centers, and metropolitan medical corporations anchoring market leadership. These entities differentiate through sub-specialty expertise, active clinical trials, and early deployment of photon-counting CT or 7 T MRI. Mid-sized community hospitals defend share by bundling imaging with chronic-care management programs and leveraging vendor financing to upgrade to 80-slice CT systems without capital strain.

Technology partnerships are emerging as decisive differentiators. Multiple providers have signed multi-year managed-services agreements whereby equipment manufacturers supply scanners, lifecycle services, and cloud-based AI suites under outcome-linked pricing. Early AI adopters report 10–15% higher throughput and improved standard deviation of report turnaround, an operational edge that helps attract referring clinicians. Meanwhile, foreign AI startups must navigate PMDA registration timelines, prompting them to partner with domestic distributors for faster commercial entry.

Reimbursement clarity for AI-assisted reads has energized domestic software vendors, many spun out of academic labs, to focus on niche algorithms such as gastric endoscopy lesion detection or orthopedic MRI cartilage mapping. The interplay of incumbents and new entrants continues to reshape competitive contours, but rising demand ensures ample headroom for both groups. Overall, the Japan diagnostic imaging services market rewards scale, digital maturity, and collaborative innovation, setting the stage for sustained rivalry focused on value-based care delivery.

Japan Diagnostic Imaging Services Industry Leaders

The University of Tokyo Hospital

St. Luke’s International Hospital

Keio University Hospital

Osaka University Hospital

Juntendo University Hospital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Government of Japan supplied six ambulances, a CT scanner for CWM Hospital, and additional medical equipment to the Ministry of Health.

- May 2024: A new CT scanner funded through Japan’s Social and Economic Development Programme was installed at the National Hospital in Bishkek.

- May 2024: Japan donated digital X-ray machines and related health equipment valued at roughly JPY 600 million (USD 4.4 million) to Vila Central Hospital and other facilities.

Japan Diagnostic Imaging Services Market Report Scope

As per the scope of the report, diagnostic imaging services are medical procedures that use technologies such as X-rays, CT scans, MRIs, ultrasounds, and PET scans to non-invasively capture images of the body's internal structures and functions. These services assist in diagnosing illnesses, evaluating injuries, and monitoring treatments by visualizing conditions like tumors, fractures, and organ abnormalities, ultimately guiding treatment decisions and improving patient outcomes. The market is segmented by Modality (MRI, Computed Tomography, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, and Mammography), Application (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, and Other Applications), and Service Provider (Hospitals, Diagnostic Centers and Others). The report offers the value (in USD million) for the above segments.

| MRI |

| CT |

| Ultrasound |

| X-Ray |

| Nuclear Imaging |

| Fluoroscopy |

| Mammography |

| Cardiology |

| Oncology |

| Neurology |

| Orthopedics |

| Gastroenterology |

| Gynecology |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centers |

| Clinics and Specialty Centers |

| Others |

| By Modality | MRI |

| CT | |

| Ultrasound | |

| X-Ray | |

| Nuclear Imaging | |

| Fluoroscopy | |

| Mammography | |

| By Application | Cardiology |

| Oncology | |

| Neurology | |

| Orthopedics | |

| Gastroenterology | |

| Gynecology | |

| Other Applications | |

| By Service Provider | Hospitals |

| Diagnostic Imaging Centers | |

| Clinics and Specialty Centers | |

| Others |

Key Questions Answered in the Report

What is the current size of the Japan diagnostic imaging services market?

The market generated USD 26.42 billion in 2025 and is forecast to reach USD 32.34 billion by 2030.

Which imaging modality leads the Japan diagnostic imaging services market?

X-ray remains the largest modality with 31.86% revenue share in 2024.

Why is ultrasound growing fastest within the modality mix?

Portable platforms and AI-enabled measurement tools are expanding point-of-care use, supporting a 5.16% CAGR through 2030.

What role does government policy play in market growth?

Reimbursement for AI-assisted reads and subsidies for teleradiology hubs accelerate technology adoption and expand access, boosting overall market growth.

Which application segment shows the highest growth potential?

Cardiology imaging is projected to rise at 5.69% CAGR, driven by preventive care programs and advanced cardiac CT protocols.

Page last updated on: