Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

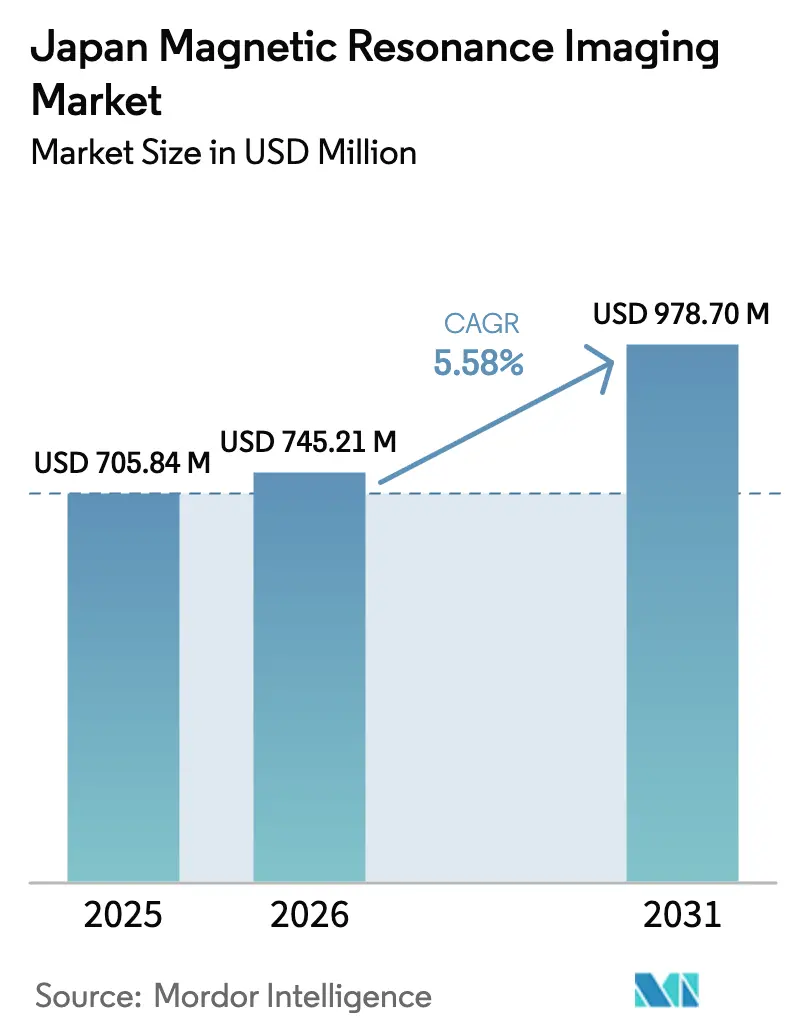

| Base Year Market Size (2025) | USD 705.84 Million |

| Market Size (2026) | USD 745.21 Million |

| Market Size (2031) | USD 978.70 Million |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The Japan Magnetic Resonance Imaging Market size is projected to be USD 705.84 million in 2025, USD 745.21 million in 2026, and reach USD 978.70 million by 2031, growing at a CAGR of 5.58% from 2026 to 2031.

Hospitals remain the dominant consumers of imaging services, while independent imaging centers are extending operating hours and capturing more referrals. This trend is exerting pressure on vendor margins despite rising demand. Closed-bore 1.5 T and 3 T systems continue to dominate sales, driven by the reliance of neurology and oncology protocols on these high-field magnets. However, with reimbursement rates being equal for both 1.5 T and 3 T scans, providers are increasingly prioritizing software upgrades over hardware replacements. Domestic companies such as Canon Medical, Fujifilm Healthcare, and Shimadzu leverage established service networks and public hospital procurement preferences to maintain their market share against multinational competitors. At the same time, AI-focused entrants, such as AIRS Medical, are proving that profitability in the imaging market can be achieved without owning magnet technology.

Key Report Takeaways

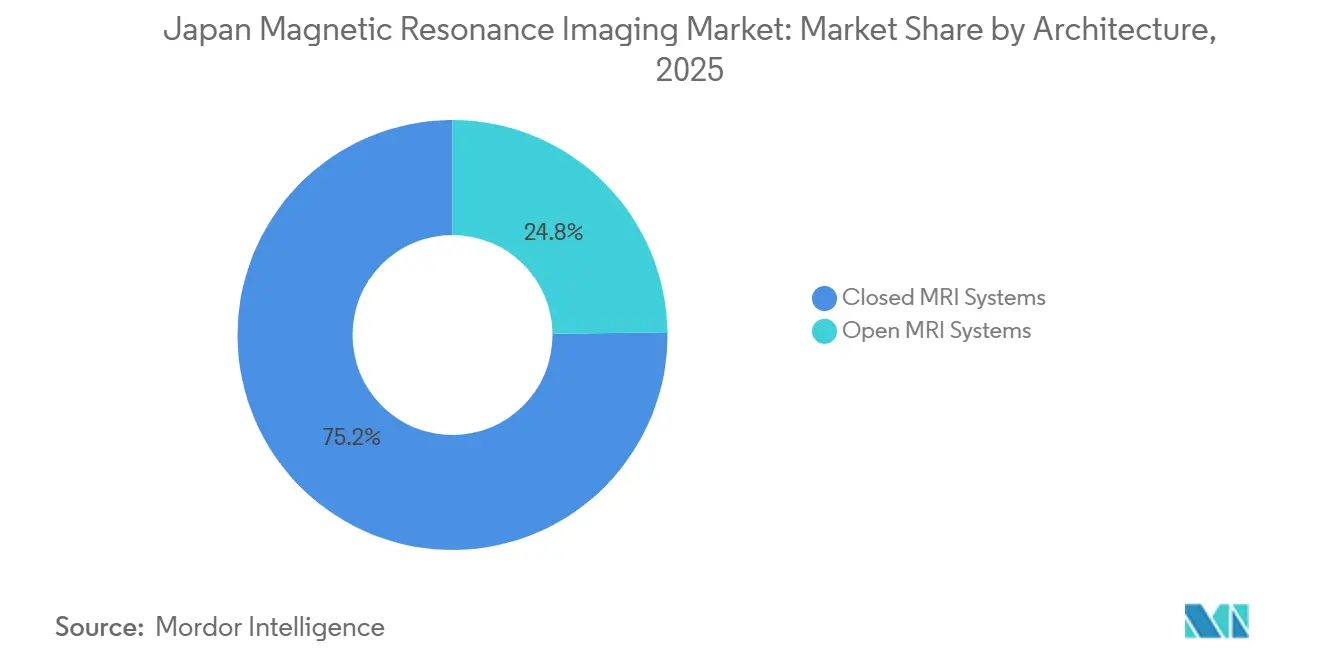

- By architecture, closed-bore systems led with 75.21% of Japan's MRI market share in 2025, while open MRIs are projected to advance at a 6.02% CAGR through 2031.

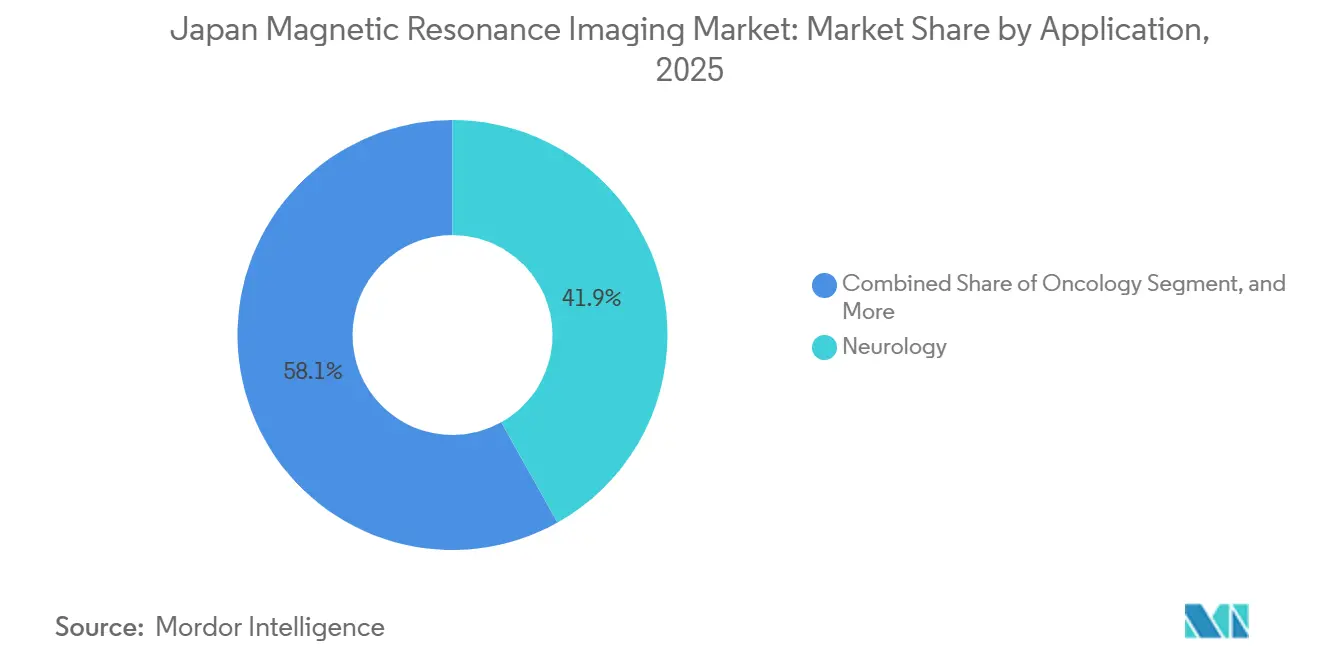

- By application, neurology captured 41.88% of 2025 demand; oncology is forecast to grow at a 6.05% CAGR to 2031 as MR-guided radiotherapy gains traction.

- By field strength, 1.5 T platforms held 55.64% share of the Japan MRI market size in 2025; the 7 T research sub-segment is expected to post the fastest 5.71% CAGR.

- By end user, hospitals accounted for 47.62% of 2025 revenue, while stand-alone imaging centers are expanding at a 6.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Universal health-insurance coverage | +0.8% | National | Long term (≥ 4 years) |

| Rapid expansion of 3 T installations in secondary-care hospitals | +1.2% | West Japan | Medium term (2–4 years) |

| Emergence of AI-based image reconstruction that reduces scan time | +1.4% | National | Short term (≤ 2 years) |

| Government neuro-imaging R&D subsidies tied to dementia measures | +0.7% | Tokyo, Osaka, Kyoto | Medium term (2–4 years) |

| Rise of hybrid intra-operative MRI in orthopedic & sports clinics | +0.5% | Major metros | Medium term (2–4 years) |

| Cloud-based national image database (J-MID) enabling algorithm training | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Universal Health-Insurance Coverage Anchors Stable Demand

In 2024, 28.9% of Japan's residents were aged 65 or older, a demographic trend that underscores the nation's commitment to healthcare.[1]OECD, “OECD Health Statistics,” oecd.org Japan's single-payer system covers 70% of MRI procedure costs, ensuring a consistent patient volume. While flat-scan fees, irrespective of magnet strength, lean toward commoditization, specialized centers capitalize on pediatric sedation protocols, commanding an 80% premium. These centers are increasingly investing in open-bore units, thereby reducing anesthesia requirements. The standardized tariff structure not only guarantees baseline MRI access across every prefecture but also incentivizes providers to extend replacement cycles to 12–15 years. This balance has propelled Japan's MRI market to boast one of the globe's highest utilization rates, compensating for modest per-scan margins with sheer volume. The vendors are setting themselves apart not by field strength but through enhanced service reliability and AI-driven workflow integrations.

Rapid Expansion of 3 T Installations in Secondary-Care Hospitals

As competition for neurosurgery referrals heated up, secondary hospitals in Osaka, Kyoto, and Hyogo raced ahead, installing 3 T scanners at a pace 22% quicker than their eastern peers during 2024–2025. Canon Medical's Vantage Galan 3 T Supreme Edition, which began shipping in April 2024, slashed lead times from 18 to 10 months by utilizing in-house magnets.[2] Canon Medical Systems, “ISMRM 2025 Presentations,” canon-medical.com This innovation made 3 T technology more accessible to mid-sized institutions. The Japan Radiological Society has now made it a benchmark: to achieve advanced-imaging accreditation, hospitals must own at least one 3 T unit. What was once a neutral upgrade in terms of reimbursement has morphed into a vital marketing asset. Hospitals are now pursuing 3T technology not just for its superior image quality but also as a badge of clinical sophistication. Consequently, despite facing tariff challenges, hardware orders in the Japanese MRI market are increasingly concentrated in the growth corridors of western Japan.

Emergence of AI-Based Image Reconstruction That Reduces Scan Time

Leading algorithms, including Canon's AiCE, Siemens' Deep Resolve, GE's AIR Recon DL, and Philips' SmartSpeed, have achieved a remarkable feat: compressing scan sequences by 40–50%. This advancement effectively doubles the throughput on existing MRI hardware. AIRS Medical's SwiftMR, which received clearance in June 2024, offers a game-changing solution by retrofitting legacy 1.5 T systems in community hospitals.[3]Asian Oceanian Society of Radiology, “Green Radiology Survey 2025,” aosr.org This innovation democratizes access to faster exams without the burden of capital expenditure. Research from the University of Tokyo has shown that AI-enhanced 1.5 T neuro images can match the diagnostic quality of 3 T scans, challenging long-held beliefs about field-strength hierarchies. In a significant technological leap, GMO Internet and Fujitsu have harnessed the power of the Fugaku supercomputer to create a cloud pipeline. This system can preprocess an impressive 10,000 brain studies in just 2 days, significantly speeding up the release of algorithms. In response to these rapid advancements, regulators have taken note.

Government Neuro-Imaging R&D Subsidies Tied to Dementia Measures

In a proactive move, MEXT allocated a substantial JPY 9.3 billion (USD 62 million) in 2024 to bolster its national brain-imaging database. This initiative mandates routine MRI monitoring for patients undergoing Alzheimer's antibody therapies, such as lecanemab. New guidelines stipulate both baseline and follow-up MR scans, directly amplifying patient volume at certified centers. The subsidies predominantly benefit university hospitals in Tokyo, Osaka, and Kyoto, which are at the forefront of multi-site dementia trials. This strategic positioning has led to collaborative ventures, with vendors partnering for co-development of AI models utilizing the J-MID data. Additionally, wellness clinics have seized the opportunity, introducing "brain-dock" cash-pay packages, thereby carving out a premium niche in the Japanese MRI landscape.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of board-certified radiologists and unequal rural coverage | −0.4% | Nationwide, acute in north & islands | Long term (≥ 4 years) |

| High 3 T / 7 T acquisition & service costs | −0.6% | National | Medium term (2–4 years) |

| Stringent RF-safety rules that limit 7 T clinical rollout | −0.2% | National | Long term (≥ 4 years) |

| Reimbursement cuts for follow-up musculoskeletal MRI exams | −0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Board-Certified Radiologists and Unequal Rural Coverage

Japan has 36 radiologists per million residents compared with the OECD average of 101, forcing each specialist to interpret 6,130 CT/MR studies per year. Overwork elevates burnout risk and could compromise diagnostic accuracy. Rural areas experience the sharpest gaps; more than half of prefectures report vacancy rates above 25% for hospital radiology posts. Teleradiology firms step in, but they add costs and potential turnaround delays. The Japan Radiological Society expanded fellowship quotas in 2024, yet training pipelines lag behind the proliferation of equipment. Without a larger workforce, under-utilization of installed scanners will cap volume growth despite favorable reimbursement.

High Acquisition & Maintenance Costs of 3 T & 7 T Units

A single 7 T system can require double the capital and 50% higher annual service fees than a 1.5 T unit. Reimbursement revisions that peg prices to foreign averages have trimmed margins, discouraging smaller providers from ordering high-field units. Although helium-free magnet designs like Philips BlueSeal reduce operating expenses, upfront price points remain steep. Rural hospitals often struggle to secure specialist service contracts, extending downtime risks. These economic hurdles prolong adoption cycles and may widen the technology gap between urban and non-urban regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Helium-Free Designs Unlock Basement Installations

Closed scanners accounted for 75.21% of the Japan MRI market share in 2025, reflecting hospital preference for maximum gradient performance in neurological and oncological protocols. Open units, however, are gaining traction with a 6.02% CAGR as providers target claustrophobic, pediatric, and interventional cases. The Japan MRI market size for open configurations is projected to exceed USD 235.4 million by 2031, underpinning diversification of vendor portfolios. Manufacturers now launch semi-open 1.2 T systems that preserve gradient strength while offering 270-degree patient access, balancing comfort and image quality. Private imaging centers located in retail clinics leverage these units to differentiate on patient experience and drive evening operation schedules that appeal to working adults.

The shift also aligns with Japan’s strategy to expand outpatient surgical suites. Arthroscopic and pain-management procedures increasingly rely on real-time imaging; open magnets facilitate physician access without compromising sterility. Government safety guidelines published in 2024 set standardized RF-exposure limits for intraoperative use, accelerating approvals. In parallel, AI-reconstruction algorithms mitigate lower signal-to-noise ratios inherent in open designs, narrowing the image-quality gap with closed scanners and bolstering clinical confidence among skeptical radiologists.

By Field Strength: Reimbursement Parity Caps 3 T Premium

High-Field 1.5 T scanners hold 55.64% of current installations, supported by broad clinical versatility and favorable cost-of-ownership metrics. Deep-learning upgrades further solidify their position by delivering 3 T-like clarity at reduced helium consumption. Hospitals in regional hubs often deploy dual 1.5 T rooms to manage night-shift emergency imaging, reducing wait times while avoiding the need for extra 3 T personnel. As AI platforms mature, the 1.5 T segment of the Japan MRI market is estimated to grow at a 4.72% CAGR through 2031, driven by replacement demand.

Ultra-High-Field 7 T devices, though fewer in number, represent the research frontier with a 5.71% CAGR and will surpass 35 installed units nationwide by 2031. Neuroscience centers leverage 7 T’s superior susceptibility contrast to map micro-vascular dementia biomarkers, an area of heightened interest for Japan’s aging society. The Japan MRI market share for 7 T is small, but it commands premium service contracts that entice vendors to localize coil manufacturing and support teams for physicists. Regulatory clarity arrived in 2024 when the Pharmaceuticals and Medical Devices Agency published dedicated RF-safety protocols, shortening site-planning cycles and boosting buyer confidence among tertiary hospitals.

By Application: Anti-Amyloid Therapy Monitoring Lifts Neurology

Neurological imaging accounted for 41.88% of segment revenue in 2025, as stroke, dementia, and epilepsy remain national health priorities. Clinical guidelines for anti-amyloid therapies mandate baseline and follow-up MRI, anchoring steady scan volumes. Academic hospitals deploy functional MRI to evaluate surgical options for refractory epilepsy, further elevating high-field utilization. The Japan MRI market for neurology scans is anticipated to exceed USD 410.3 million by 2031, underscoring its foundational role.

Oncology is the fastest-growing segment, with a 6.05% CAGR, propelled by expanded prostate and pancreatic cancer screening programs. Multi-parametric protocols that use diffusion and spectroscopy are reimbursable, encouraging providers to upgrade to advanced gradient packages. AI-driven contouring tools shorten reporting times, partly offsetting radiologist shortages. Musculoskeletal, cardiology, and abdominal indications continue to climb steadily, with specialized protocols such as liver elastography gaining favor for cirrhosis management. Pediatric imaging maintains a niche yet essential presence, with child-friendly coils and cartoon-themed bore lighting that reduce sedation needs.

By End User: Stand-Alone Centers Optimize Utilization

Hospitals accounted for 47.62% of Japan's MRI market share in 2025, owing to integrated emergency departments and surgical capabilities. Comprehensive stroke centers require 24/7 MRI access, underscoring the need for on-site systems even in mid-sized facilities. Government subsidies covering up to 30% of capital costs for disaster-resilient installations further support hospital ownership. Academic centers leverage research grants to pilot AI reconstruction and 7T neuroimaging, driving early-adopter momentum.

Stand-alone imaging centers record a 6.25% CAGR as medical malls proliferate across metropolitan suburbs. Flexible evening and weekend slots attract workers who defer weekday appointments. Centers differentiate through patient-centric amenities such as noise-reducing sequences and same-day results delivered via secure apps. Corporate check-up packages bundling whole-body MRI stimulate additional traffic. An emerging “Others” category includes mobile units serving sports stadiums and rural townships, supported by car-mounted 0.4 T systems that diagnose wrist injuries onsite.

Geography Analysis

Japan’s MRI landscape concentrates 76.85% of scanners within Tokyo, Kanagawa, Saitama, Chiba, Osaka, and Hyogo, mirroring population density and specialist distribution. The capital region hosts premier neuroscience institutes engaged in Brain/MINDS Beyond, spurring early adoption of 7 T and AI-enhanced protocols. Urban demand also benefits from higher per-capita disposable income, enabling private centers to thrive without relying solely on insurance margins.

Secondary cities such as Nagoya, Fukuoka, and Sapporo are witnessing accelerating 3 T uptake in municipal hospitals, as they seek to stem patient outflows to megacity hospitals. Local governments allocate subsidies for disaster-resistant imaging suites, a policy response to earthquake risks that threaten the continuity of critical services. Tele-interpretation networks link these regional scanners to metropolitan radiology hubs, mitigating the workforce imbalance. Rural prefectures leverage mobile MRI vans and public-private partnerships to ensure quarterly diagnostic outreaches, though scan turnaround time still lags urban standards.

National regulators enforce uniform quality through periodic site inspections and mandatory operator certification. PMDA’s GMP disclosure program publicizes compliance records, fostering trust among patients who must travel long distances for high-field exams. The coming decade will likely see targeted investments in hybrid and low-field portable units to bridge the urban-rural access gap while containing capital spending.

Competitive Landscape

Four multinationals Canon Medical, Siemens Healthineers, GE HealthCare, and Philips—anchor the Japan MRI market, jointly controlling an estimated 70% of installations. Canon leverages domestic manufacturing and government relationships to dominate replacement cycles, recently launching an AI-powered 3 T platform that integrates SmartSpeed reconstruction. Siemens is investing USD 314 million in a new magnet-coil plant, signaling a long-term commitment to local supply stability.

GE HealthCare strengthened its footprint by acquiring radiopharmaceutical producer Nihon Medi-Physics for USD 183 million, creating a vertically integrated imaging-diagnostics ecosystem. Philips focuses on cutting lifetime costs through helium-free BlueSeal magnets, resonating with clinics facing volatile helium pricing. Niche innovators such as SyntheticMR and AIRS Medical supply AI add-ons that retrofit legacy fleets, expanding addressable revenue without hardware swaps.

Competition hinges on AI workflow integration, helium management innovation, and service network reliability rather than discounting—vendor-managed service agreements with 99%+ uptime guarantees sway risk-averse hospitals. Academic partnerships remain a key differentiator; firms that support grant-funded research secure early clinical champions who influence procurement across wider hospital networks. Meanwhile, portable-MRI start-ups target sports-medicine and emergency-response niches, potentially redrawing the competitive map if reimbursement codes materialize.

Japan Magnetic Resonance Imaging Industry Leaders

-

GE Healthcare

-

Koninklijke Philips N.V.

-

Fujifilm Healthcare Corp.

-

Canon Medical Systems Corp.

-

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Callisto Inc. marked the 2nd anniversary of its medical image data platform, "Callisto DataHub," by offering free datasets. These included 50 chest X-rays suspected of lung cancer with lesion bounding boxes and 50 prostate cancer MRI cases with lesion segmentations (PI-RADS 4 and 5).

- June 2025: Canon Medical received the Invention Award for a multiplanar real-time cardiac MRI patent, paving the way for breath-hold-free cardiac exams.

- May 2025: AIRS Medical introduced deep-learning software that improves legacy image quality while shortening acquisition sequences.

- January 2025: SyntheticMR obtained Japanese clearance for its SyMRI 3D quantitative-imaging suite, enabling automatic myelin and CSF mapping on 1.5 T and 3 T scanners.

Japan Magnetic Resonance Imaging Market Report Scope

As per the scope of this report, magnetic resonance imaging is a medical imaging technique used in radiology to produce images of the body's anatomy and physiological processes. These pictures are also used to diagnose and detect abnormalities in the body.

The Japan Magnetic Resonance Imaging (MRI) Market is segmented by architecture, field strength, application, and geography. By architecture, the market is segmented into closed MRI systems and open MRI systems. By field strength, the market is segmented into low-field MRI systems, high-field MRI systems, very high-field MRI systems, and ultra-high-field MRI systems. By application, the market is segmented into oncology, neurology, cardiology, gastroenterology, musculoskeletal, and other applications. The report offers market size and forecasts in value (USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (< 1 T) |

| High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T) |

By Application

| Neurology |

| Oncology |

| Cardiology |

| Musculoskeletal |

| Abdominal & Pelvic |

| Pediatric Imaging |

By End User

| Hospitals |

| Stand-Alone Imaging Centers |

| Others |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (< 1 T) |

| High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T) | |

| By Application | Neurology |

| Oncology | |

| Cardiology | |

| Musculoskeletal | |

| Abdominal & Pelvic | |

| Pediatric Imaging | |

| By End User | Hospitals |

| Stand-Alone Imaging Centers | |

| Others |

Key Questions Answered in the Report

How big is the Japan Magnetic Resonance Imaging Market?

The Japan Magnetic Resonance Imaging Market size is expected to reach USD 745.21 million in 2026 and grow at a CAGR of 5.58% to reach USD 978.7 million by 2031.

Which MRI architecture is most common in Japan?

Closed MRI systems dominate with 75.21% share in 2025 because hospitals value their superior image quality for stroke and dementia care.

Who are the key players in Japan Magnetic Resonance Imaging Market?

Siemens AG, Canon Medical Systems, GE Healthcare, Fujifilm Holidngs Corporation and Koninklijke Philips N.V. are the major companies operating in the Japan Magnetic Resonance Imaging Market.

Which application segment is expanding fastest?

Oncology imaging shows the highest growth, registering a 6.05% CAGR through 2031 thanks to broader prostate and pancreatic cancer screening.

Page last updated on: