Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 38.81 Billion |

| Market Size (2031) | USD 52.59 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Japan Luxury Residential Real Estate Market size is estimated at USD 38.81 billion in 2026, and is expected to reach USD 52.59 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031). Currency depreciation, finite land supply in Tokyo’s core wards, and redevelopment pipelines that embed advanced seismic engineering combine to keep pricing firm despite demographic headwinds. Offshore capital benefits from a yen that stayed near 150 per USD through 2025, effectively discounting trophy assets by as much as one-third for dollar-denominated investors. Developers with integrated land banks are absorbing construction-cost inflation, while branded-residence operators widen the rental pool and lift service expectations. Demand spillovers from infrastructure projects in Nagoya and Osaka are diversifying geographic exposure within the Japan luxury residential real estate market, even as natural-hazard and demographic risks temper sentiment outside prime metros.

Key Report Takeaways

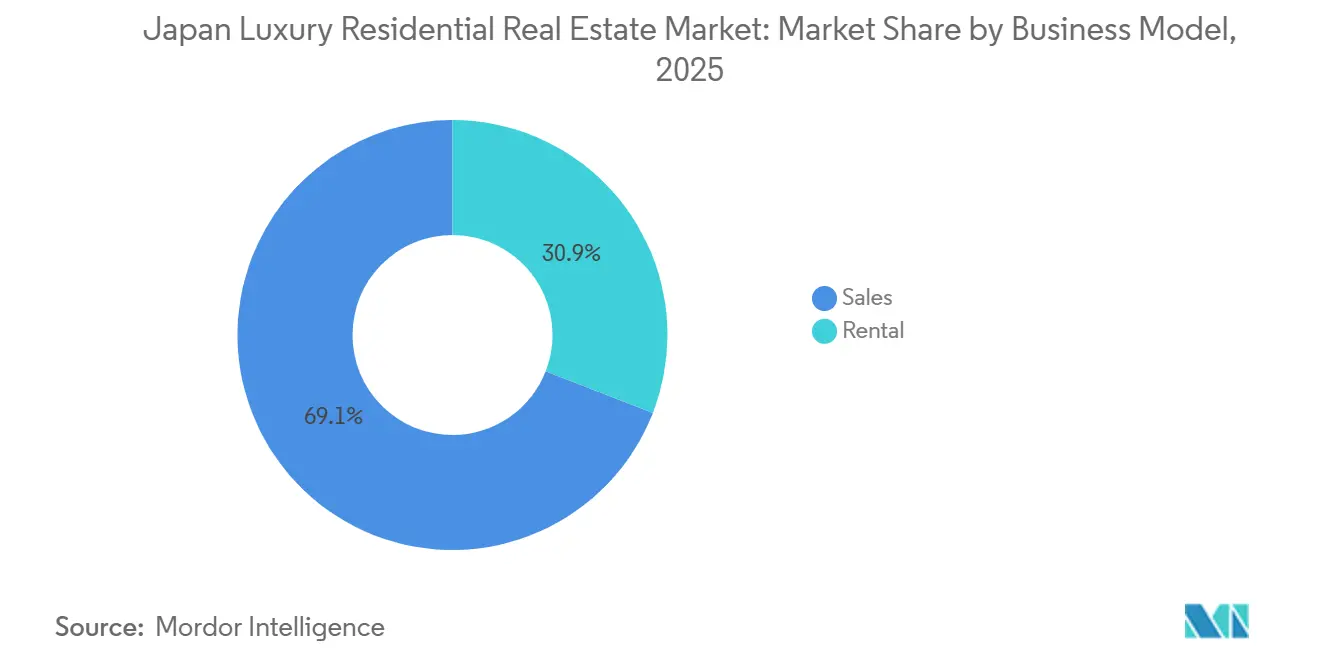

- By business model, the sales segment accounted for 69.1% of the Japan luxury residential real estate market share in 2025, whereas rental is forecast to grow at a 7.31% CAGR to 2031.

- By property type, apartments and condominiums held 77.4% of the Japan luxury residential real estate market size in 2025, while villas and landed houses are projected to expand at a 7.82% CAGR between 2026-2031.

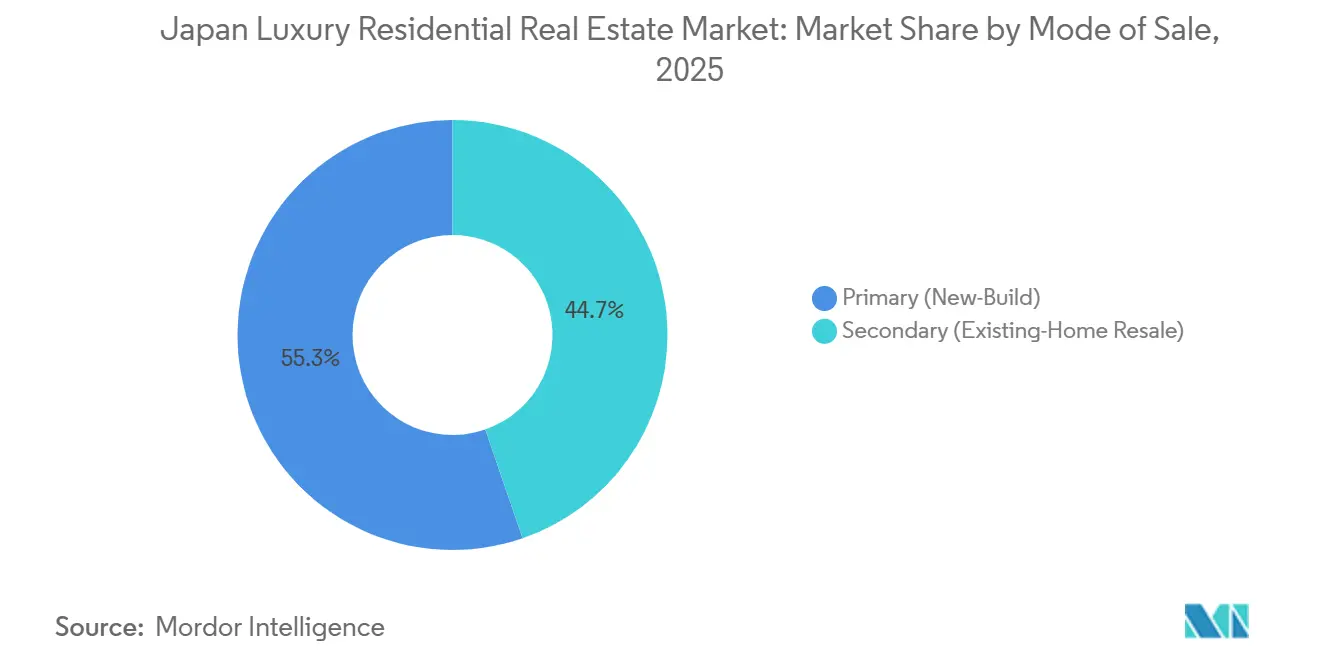

- By mode of sale, primary new-builds captured 55.3% of sales in 2025; the secondary channel is advancing at a 6.95% CAGR through 2031.

- By geography, Tokyo led with 50.2% revenue share in 2025, while Nagoya is on track for the fastest 8.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yen weakness boosts foreign HNWI purchasing | +1.5% | Tokyo, Osaka, Kyoto, Niseko | Medium term (2-4 years) |

| Scarcity of prime land and view corridors | +1.2% | Tokyo (Minato, Chiyoda, Shibuya) | Long term (≥ 4 years) |

| Safe-haven appeal of Japan | +1.0% | National, concentrated in Tokyo | Long term (≥ 4 years) |

| Redevelopment and teardown-to-custom rebuild | +0.9% | Tokyo core wards, Osaka central districts | Medium term (2-4 years) |

| Rise of branded residences | +0.8% | Tokyo, Osaka, Niseko | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Prime Land and View Corridors Supports Price Resilience

Net new residential zoning in Minato, Chiyoda, and Shibuya wards averaged below 0.5% of total land area each year from 2023-2025, creating a structural ceiling on fresh supply. Multi-generational owners hold many of the best parcels, making site assembly slow and expensive. Asahi Shimbun recorded an 8.2% year-on-year land-price jump in Minato for 2024, the steepest since 1991, as developers compete for scarce plots with unobstructed bay or palace vistas[1]Asahi Shimbun Editors, “Tokyo Land Prices Rise Most in Three Decades on Redevelopment Boom,” asahi.com . Upper-floor units commanding landmark views now achieve 25-35% premiums over mid-tier stock, double the spread seen in 2020. The Tokyo Metropolitan Government has no plans to enlarge residential zoning in these wards through 2031, locking scarcity into the outlook.

Yen Weakness Boosts Foreign and Expat HNWI Purchasing Power

The yen’s slide to 150 per USD in mid-2024 sliced headline prices by roughly 30% relative to 2021 levels for dollar and euro buyers. Foreign direct investment in Japanese real estate hit USD 14 billion in fiscal 2024, up 42% year-on-year, with luxury housing absorbing close to one-fifth of that flow[2]Bank of Japan, “Foreign Direct Investment Statistics,” boj.or.jp . Resort markets such as Niseko saw international buyers secure nearly 60% of new-build units in 2024, versus 45% two years earlier. Policy risk emerged in late 2025 when officials floated foreign-buyer screening thresholds, but no formal cap has yet been enacted. Monetary-policy divergence suggests currency support will remain in place at least into 2027.

Redevelopment and Teardown-to-Custom Rebuilds Command Premiums

Flagship mixed-use towers are redefining price ceilings. Mori Building’s Toranomon-Azabudai Hills delivered branded Aman units that cleared at USD 100,000 per sq m, roughly double non-branded peers in Minato. The Second Roppongi Hills project, under construction, will add 1,200 apartments atop a transit hub by 2027. Custom rebuilds of aged villas integrate base-isolation and net-zero systems, but push construction budgets above USD 10,000 per sq m. These premiums compensate for higher risk and material costs while recycling under-utilized parcels into ultra-prime inventory.

Rise of Branded Residences and Serviced/Hotel Hybrids

Hospitality brands - Aman, Four Seasons, Ritz-Carlton - lend cachet and turnkey services, accelerating sell-outs among time-constrained global buyers[3]Nikkei Asia Reporters, “Japan Construction Costs Soar on Labor Shortage,” asia.nikkei.com. Aman Residences Tokyo sold its 91 units within 18 months, 40% to non-resident purchasers. Serviced-apartment portfolios in Tokyo and Osaka posted 90%+ occupancy and rising average daily rates in 2024, evidence that corporate relocations favor flexible, amenitized living. New rules adopted in 2025 require hotel licenses when short-stay use exceeds 30% of room-nights, nudging operators to fine-tune mix but not dampening structural demand. Growth momentum in branded stock is set to outpace the broader Japan luxury residential real estate market through 2031.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic headwinds and thin liquidity outside core metros | -0.8% | Regional cities, suburban Tokyo | Long term (≥ 4 years) |

| Rising construction and fit-out costs | -0.6% | National, most acute in Tokyo | Medium term (2-4 years) |

| Natural-hazard exposure and insurance friction | -0.5% | Coastal wards, reclaimed-land areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic Headwinds and Thin Liquidity Outside Core Metros

The share of residents aged 65+ reached 28.9% in 2024 and is on course to top 30% by 2030, reducing household formation in prefectures beyond Tokyo, Osaka, and Nagoya. Luxury transactions in Shizuoka and Niigata fell 12% year-on-year during 2024 as local buyer pools shrank. Estate disposals by aging owners are flooding regional markets with dated stock, stretching selling periods, and pushing discounts. Institutional and foreign investors, who could provide liquidity, remain focused on core metros, leaving secondary markets exposed to price drift. Without a demographic reversal, exit options for non-prime high-end assets will stay constrained through the forecast horizon.

Rising Construction and Fit-Out Costs Compress Feasibility

Overall construction costs increased roughly 15% from 2023-2025, propelled by labor shortages and pricier imported materials. Revised 2024 building codes added requirements for 20% energy savings versus 2013 baselines, lifting mechanical and envelope budgets by USD 1,300–2,000 per unit. Seismic-isolation mandates that withstand 0.5g ground motion add another 8-12% to structural cost. Smaller developers lacking balance-sheet depth migrate toward partnerships with the major conglomerates, narrowing competitive diversity. Cost pressure should moderate post-2028 as prefabrication improves, but near-term feasibility hurdles persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rental Momentum Narrows the Gap

Sales transactions dominated with a 69.1% share of the Japan luxury residential real estate market in 2025, yet rentals are rising on the back of expatriate inflows and branded-residence offerings. Rental stock posted 90%+ occupancy across key Mori Living properties and average lease tenures extended to 24 months in 2024, signaling stickier demand. Elevated sales pricing above USD 100,000 per sq m in ultra-prime towers narrows the buyer pool, prompting developers to pivot toward build-to-rent pipelines. The rental segment’s 7.31% CAGR to 2031 exceeds the overall Japan luxury residential real estate market size trajectory, suggesting investors will allocate more capital to income-producing models.

Flexibility and turnkey services differentiate rental offerings, especially among international assignees who value predictable monthly outgo over large down payments. Branded-residence leases often include concierge, housekeeping, and wellness amenities bundled into the rent, raising achievable yields. Tax rules also permit depreciation benefits that shelter rental income for certain investor profiles. As corporations adopt hybrid working, executives favor centrally located, fully serviced apartments over suburban ownership, reinforcing rental demand. This evolution indicates that rentals could approach parity with sales by 2031, reshaping revenue mix for integrated developers active in the Japan luxury residential real estate market.

By Property Type: Villas Capture Privacy Premium

Apartments and condominiums captured 77.4% market share in 2025, reflecting vertical urbanism in Tokyo, yet the villa segment is on course for the fastest 7.82% CAGR through 2031. Orders for custom villas priced above USD 2 million rose 18% in 2024 at Sumitomo Forestry, as buyers sought outdoor space and net-zero designs. Teardown-rebuild activity in Setagaya and Meguro converts obsolete houses into modern, low-rise luxury that commands premiums approaching high-rise pricing per square foot, narrowing historical gaps.

The villa push dovetails with policy incentives: revised 2024 codes offer expedited permits and lower property taxes for energy-efficient low-rise construction, making suburban plots more attractive. Smart-home integration, EV-charging, and extensive landscaping further elevate appeal. While apartments remain predominant in the Japan luxury residential real estate market, the privacy trend signals a bifurcation, requiring developers to field both vertical and low-rise capabilities to serve diverging buyer priorities.

By Mode of Sale: Estate Turnover Energizes Secondary Market

Primary new-builds held 55.3% of 2025 volume, but the resale channel’s 6.95% CAGR is closing the gap. Brokerage divisions at Tokyo Tatemono and Mitsui Fudosan Realty reported double-digit growth in 2024 resale deals, aided by currency-advantaged foreign buyers seeking immediate occupancy. Discounts between pre-owned and new units in Minato narrowed to under 5%, evidence that location and building reputation trump age in buyer calculations.

Secondary liquidity benefits from Japan’s aging demographic: estate disposals inject well-located stock that often needs only cosmetic upgrades to meet modern standards. Developers are launching renovation-and-resale programs that retrofit energy systems and digital amenities, effectively blending primary and secondary business lines. Rising construction costs also nudge budget-minded buyers toward proven, slightly older inventory, sustaining upward momentum in the secondary slice of the Japan luxury residential real estate market.

Geography Analysis

Tokyo retained 50.2% of 2025 spending, supported by scarce land, diverse expatriate services, and integrated mixed-use projects such as Toranomon-Azabudai Hills that raised average central-ward condo prices by 8.2% year-on-year. Yet Nagoya is set to grow fastest at an 8.06% CAGR to 2031, catalyzed by the 2027 maglev line that will connect it to Tokyo in 40 minutes and by major auto-industry relocations seeking lower operating costs. Early evidence came from Daiwa House’s Grand Maison Fushimi launch, where 80% of units were reserved within six months, underscoring pent-up demand.

Osaka, with 22% 2025 share, benefits from Expo-driven infrastructure, a burgeoning financial district, and the Yumeshima integrated resort that elevates executive housing needs. Rents in Sumitomo Realty’s Osaka portfolio increased 6% in 2024, supported by 92% occupancy. Kyoto leverages cultural-tourism recovery to market refurbished machiya townhouses as niche luxury residences. Resort markets such as Niseko remain volatile - prices jumped 35% between 2022-2024, but transactions dipped 18% in 2025 after cost spikes and regulatory chatter on foreign ownership. Policy signals still prioritize infrastructure in the Tokyo-Osaka-Nagoya corridor, implying sustained capital magnetism to these hubs.

Peripheral cities face liquidity risk as population declines weigh on buyer waves, though improved Shinkansen links and digital-nomad inflows provide selective support. Investors, therefore, overweight core metros in portfolio allocations within the Japan luxury residential real estate market, using regional exposure sparingly for yield lift and diversification.

Competitive Landscape

A moderate-concentration structure defines the Japan luxury residential real estate market: five vertically integrated conglomerates—Mitsubishi Estate, Mitsui Fudosan, Mori Building, Sumitomo Realty & Development, and Tokyu Land—control prime land banks and bundled design-build-manage capabilities. Mitsui Fudosan delivered 3,200 luxury units in 2024 with average project sizes exceeding USD 333 million, showcasing financial heft that smaller rivals lack. Mitsubishi Estate’s Marunouchi tower pipeline embeds residences into office-retail ecosystems, diversifying income and locking in tenant synergies.

Strategic focus tilts toward large-scale redevelopment requiring multiyear capital and stakeholder coordination. Mori Building partnered with Aman for the Aman Residences Tokyo, achieving a full sell-out in 18 months and highlighting the pricing upside of hospitality branding. Technology adoption is growing: Sekisui House and Daiwa House integrate AI-driven energy-management and IoT sensors to meet sustainability mandates and attract eco-conscious buyers.

Entry barriers rise as construction inflation and strict codes demand scale and cash reserves. Niche players find openings in suburban villas, resort towns, and renovation-and-resale programs where agility matters more than land bank size. Partnerships between local developers and overseas capital—such as Daiwa House’s 2025 Nagoya venture with a Singapore family office—signal a collaborative path in otherwise concentrated terrain.

Japan Luxury Residential Real Estate Industry Leaders

Mitsubishi Estate Co. Ltd.

Mitsui Fudosan Co. Ltd.

Mori Trust Co. Ltd.

Mori Building Co. Ltd.

Sumitomo Realty & Development Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mori Building and Sumitomo Realty & Development broke ground on the USD 2 billion Second Roppongi Hills project featuring 1,200 high-end units, completion slated for 2027.

- December 2025: Government began evaluating non-resident purchase approvals above USD 667,000 to cool affordability pressures, potentially affecting 30% of ultra-prime deals.

- November 2025: Mitsubishi Estate sold out its 320-unit Marunouchi Park Building at an average USD 120,000 per sq m, integrating smart-home tech and station access.

- September 2025: Tokyu confirmed 60% completion of the USD 3.3 billion Shibuya redevelopment, with 800 luxury units opening late 2026.

- August 2025: Nomura Real Estate launched the 450-unit Blue Front Shibaura tower, 40% pre-sold to foreign buyers within three months.

Japan Luxury Residential Real Estate Market Report Scope

Prime location, high-end interior finishes such as marble countertops, professional-quality kitchen appliances, customized closets, and hotel-like amenities such as concierge services, a top-of-the-line fitness center, and a spa center are often staples of a luxury building. The luxury residential real estate market in Japan is segmented by type and by city. By type, the market is segmented into apartments and condominiums, villas, and landed houses. By cities, the market is segmented into Tokyo, Kyoto, Osaka, and other cities.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the Japan luxury residential real estate market in 2026?

The market is valued at USD 38.81 billion in 2026 and is set to expand to USD 52.59 billion by 2031.

What is driving foreign investment into Japanese luxury housing?

Yen weakness near 150 per USD gives foreign buyers up to a 30% price edge versus 2021 levels, spurring cross-border acquisitions.

Which Japanese city is forecast to grow fastest for luxury residences?

Nagoya leads with an expected 8.06% CAGR through 2031, helped by the upcoming maglev link and corporate relocations.

Why are branded residences popular in Tokyo?

They bundle hotel-grade concierge, maintenance, and leasing services, offering turnkey ownership that appeals to time-pressed global buyers.

What risks could slow market growth?

Demographic decline outside major metros, escalating construction costs, and potential foreign-buyer restrictions are the main headwinds.

Page last updated on: