Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.87 Billion |

| Market Size (2026) | USD 9.01 Billion |

| Market Size (2031) | USD 9.74 Billion |

| Growth Rate (2026 - 2031) | 1.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Home Textile Market Analysis by Mordor Intelligence

The Japan home textile market size was valued at USD 8.87 billion in 2025 and estimated to grow from USD 9.01 billion in 2026 to reach USD 9.74 billion by 2031, at a CAGR of 1.56% during the forecast period (2026-2031). This growth path mirrors a mature consumer landscape where premiumization offsets low replacement rates, demographic aging fuels comfort-centric purchasing, and sustainability concerns nudge fiber choices toward bamboo blends and recycled synthetics. Single-person households, especially in Tokyo, accelerate demand for compact, multifunctional products, while retirees seek easy-care items that minimize physical effort. E-commerce penetration exceeding 31% for household goods introduces new competitive dynamics, with Korean and European brands challenging domestic incumbents [1]Ministry of Economy, Trade and Industry, “FY 2023 E-Commerce Market Survey,” meti.go.jp. At the same time, tourism recovery revives commercial orders from hotels upgrading linens to differentiate guest experience. Government energy-efficiency subsidies and green-textile grants cushion manufacturers against raw-material volatility and encourage innovation in circular solutions.

Key Report Takeaways

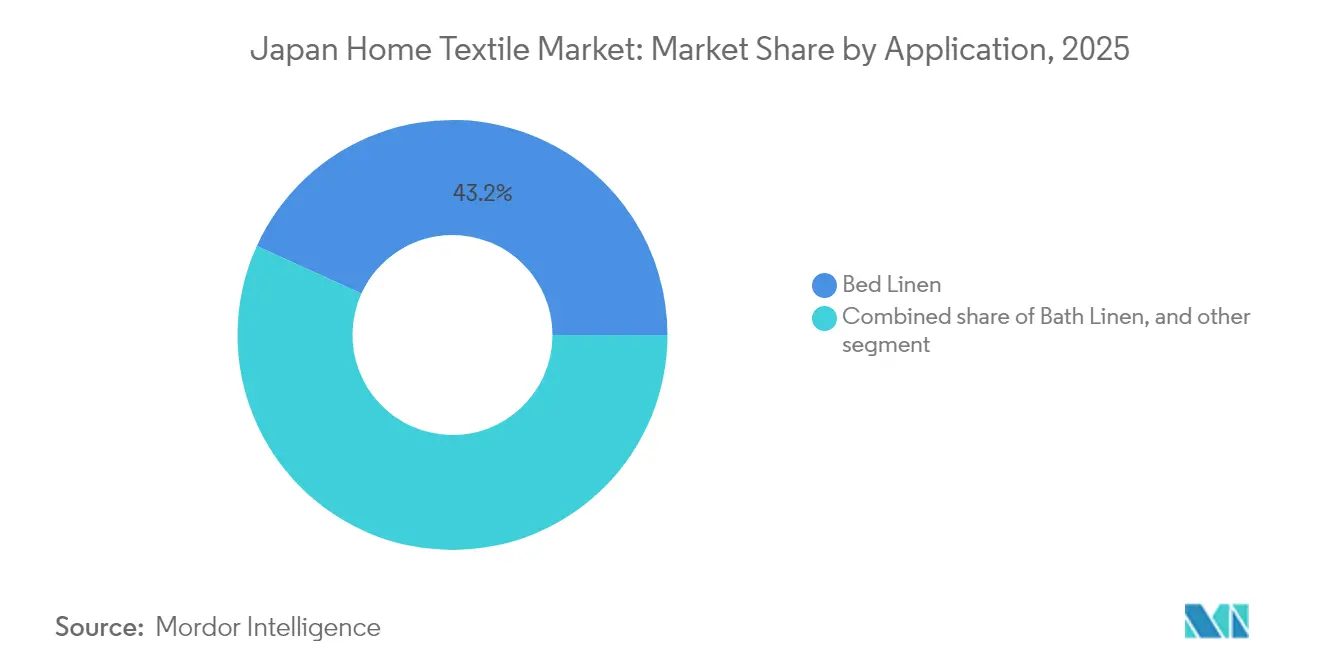

- By application, bed linen led with a 43.21% share of the Japan home textile market in 2025, while upholstery is projected to record the fastest 7.41% CAGR through 2031.

- By material, cotton commanded 50.88% of the Japan home textile market size in 2025, whereas bamboo and other cellulosic materials are forecast to expand at an 7.89% CAGR to 2031.

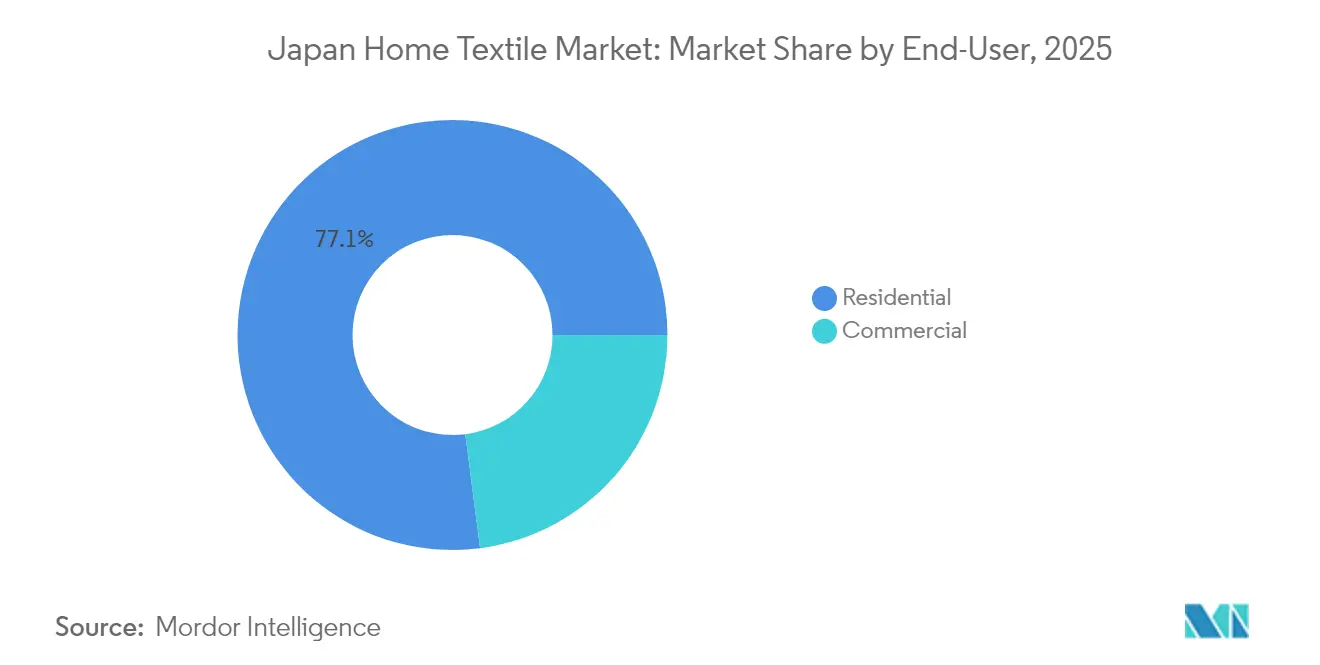

- By end-user, the residential segment captured 77.05% of the Japan home textile market share in 2025, while the commercial segment is advancing at a 6.31% CAGR through 2031.

- By distribution channel, offline retail retained a 65.74% of Japan Home Textile Market in 2025, but online channels are growing at a 9.78% CAGR to the end of the decade.

- By geography, Kanto accounted for 36.10% of the Japan home textile market in 2025; Kyushu-Okinawa is poised for the highest 5.06% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban single-person households | +0.4% | Tokyo, Osaka, Kanagawa, Kyoto | Medium term (2-4 years) |

| Premiumization of bed & bath linen | +0.3% | Kanto, Kansai, major urban centers | Short term (≤ 2 years) |

| Expansion of home-décor e-commerce | +0.5% | National, strongest in urban areas | Short term (≤ 2 years) |

| Hospitality rebound post-COVID | +0.2% | Kyoto, Hokkaido, and other tourism hubs | Medium term (2-4 years) |

| Government green-textile subsidies | +0.1% | National | Long term (≥ 4 years) |

| Smart-fabric sleep-health demand | +0.2% | Urban centers, aging-population clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Single-Person Households Drive Compact Living Solutions

Single-person households are projected to surpass 23.3 million by 2050, accounting for 44.3% of national households [2]The Mainichi, “Singles to make up over half of Tokyo households in 2050,” mainichi.jp. In Tokyo, the ratio is expected to top 54%, prompting a decisive swing toward space-saving bedding, towels, and modular upholstery that fit micro-apartments. Search interest in single-seat sofas jumped 248% year over year, underscoring the appetite for compact upholstered items. Retailers now promote foldable futons, washable slipcovers, and storage-integrated cushions that amplify functionality per square meter. Uptake skews highest in dense metro areas, whereas rural consumers continue to prefer full-size formats. As the average household size falls toward 2.21 persons, the Japan home textile market benefits from steady demand for products scaled to smaller living environments.

Premiumization Transforms Bed and Bath Categories Through Wellness Positioning

Consumer willingness to pay for better sleep has multiplied bedding sales on major platforms 6.4-fold since 2019. Seniors’ report heightened cold sensitivity, making thermal-regulating fabrics attractive. Nishikawa’s MuAtsu mattresses, marketed with 30-year durability claims, grew shipments 123% year on year after a celebrity campaign [3]Cosmo Health, “Senior Cold-Sensitivity Survey 2025,” prtimes.jp. Nitori’s SH01 long-pile towel line sold 2 million units within 18 months by combining premium absorbency with midrange pricing. Functional value now outweighs traditional luxury signals, and antimicrobial, quick-drying bath textiles command widening premiums as hygiene considerations linger post-pandemic.

E-Commerce Expansion Accelerates Through Platform Diversification and Mobile Adoption

Household-goods e-commerce reached JPY 2.47 trillion (USD 15.7 billion) in 2023 with 31.54% penetration, more than triple the overall B2C average. Mobile devices accounted for 46.6% of transactions, forcing retailers to refine smartphone imagery and one-click payment flows. Korean platforms such as Ohouse tap style-conscious younger shoppers, chipping away at domestic incumbents. Online searches for duvet covers surged 682% and for pajamas 259%, underscoring the migration of formerly tactile categories to digital purchase paths. Cross-border spending hit USD 2.5 billion, opening doors for overseas brands while squeezing domestic price realizations.

Hospitality Recovery Stimulates Commercial Textile Demand and Innovation

Inbound visitors reached 25.07 million in 2023, driving a resurgence in hotel linen upgrades. Yamashita's new factory in Nara is designed to process 40 tons daily, with plans to expand capacity to 86 tons by 2030 to meet the needs of Kansai's lodging operators. Hotels are increasingly opting for natural-gauze towels due to their quick-drying properties and suitability for sensitive skin. Kyoto has recorded the highest number of towel orders, reflecting its strong tourism inflows. To address labor shortages, the industry is focusing on innovative fabrics that are antimicrobial and easy to wash. These advancements aim to reduce laundry cycles and lower utility costs for hotels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation & slow volume growth | −0.3% | Nationwide, acute in mature urban markets | Short term (≤ 2 years) |

| Cotton-price volatility | −0.2% | Global supply chain, domestic manufacturing hubs | Medium term (2-4 years) |

| Costly circular-economy compliance | −0.1% | National, heavier on large producers | Long term (≥ 4 years) |

| Skilled labor shortage in weaving | −0.2% | Fukui, Imabari, Hokuriku textile clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Market Saturation Constrains Volume Growth Despite Value Expansion

Japan's home textile market experiences modest growth due to long replacement cycles and a strong consumer focus on durability. Fukui, known for its high per-capita orders of technical textiles, still faces limited volume growth. Manufacturers are addressing these challenges by introducing adjacent product lines and improving product functionalities. However, premiumization efforts are insufficient to fully counteract the decline in household formations. Bedding illustrates this issue, as high-quality sets designed to last for decades reduce the frequency of replacements. Although average ticket values are increasing, the extended lifespan of these products limits overall market growth.

Raw Material Price Volatility Pressures Margins and Supply-Chain Stability

By 2024, linen prices rose to 2.5 times their 2019 levels due to crop failures in Europe. The weakening yen further increased the cost of imported cotton, adding to the financial strain. Traceability mandates have driven up sourcing expenses, while sustainably verified cotton now comes with a premium. In the U.S., tariffs on Japanese textile exports climbed to 28.81%, complicating vendor strategies and accelerating a shift toward Southeast Asian mills [4]Fibre2Fashion, “U.S. tariff surge: Implications for textile exporters,” fibre2fashion.com. Vendors are increasingly exploring diversification to mitigate these challenges. Although vertical integration projects offer some risk mitigation, they require significant capital investment, posing additional hurdles for businesses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Premium Bedding Drives Market Evolution

Bed linen led the Japan home textile market with a 43.21% share in 2025. The segment benefits from demographic aging, humid summers, and wellness awareness that promote cooling, antimicrobial, and moisture-wicking fabrics. Nitori’s N-Cool series illustrates how contact-cooling technology secures repeat purchases even in a saturated bedding field. Functional advances justify price premiums and compensate for longer replacement cycles. Bath linen remains the second-largest category, leveraging Japan’s bathing culture and tourism revival. Kitchen linen holds stable through stain-resistant coatings, while upholstery’s 7.41% CAGR is tied to compact living trends and the need for modular seating in single-person dwellings.

Demand nuances differ by region. Kyoto’s hospitality sector drives exceptional towel volumes, whereas rural prefectures maintain demand for full-size futons and floor cushions. Upholstery uptake is fastest in new urban apartments where floor space averages below 40 square meters, spurring interest in stain-guarded, easy-wash slipcovers. Kitchen linen innovation focuses on heat-resistant mitts and antibacterial dishcloths that fit smaller kitchens. Carpets and rugs decline as modern flooring gains share, but niche growth persists for lightweight portable rugs suited to tatami conversions.

By Material: Sustainability Drives Fiber Innovation

Cotton secured a 50.88% share of the Japan home textile market in 2025. Consumers favor natural hand feel, but price swings and water-use concerns accelerate the shift toward blends. Bamboo and other cellulosic materials, the fastest-growing material cohort at 7.89% CAGR, attract buyers with antimicrobial and moisture-management traits without sacrificing softness. Synthetic fibers retain relevance for durability and easy care; initiatives such as the 2025 Recycled Polyester Challenge target 45% recycled content, prompting domestic mills to trial bottle-to-fiber conversions.

Linen stays premium despite supply constraints, used in high-ticket bedding and decorative cushion covers. Wool gains renewed attention after Nippon Keori’s AXIO yarn demonstrated superior odor control in performance blankets. Silk re-enters mainstream discussion through washable variants like Nishikawa’s Newmine collection that pairs moisture retention with beauty-sleep positioning. Across categories, circular-economy principles guide R&D toward fiber recovery and low-impact dyeing.

By End-User: Commercial Segment Accelerates Through Hospitality Recovery

Residential buyers represented 77.05% of the Japan home textile market share in 2025. Aging singles and couples prioritize compact, lightweight, and low-maintenance goods. Surveys show 52.3% of residents already own some functional apparel and display high latent demand for sleep-support textiles, despite under-3% adoption today. Product marketers increasingly bundle wellness narratives and smart sensors to capture this potential.

The commercial channel, posting a 6.31% CAGR, pivots on hotel, healthcare, and senior-living projects. Hotels are increasingly using natural-gauze bath linens and premium duvets to enhance guest satisfaction levels. This shift reflects the growing emphasis on providing a superior guest experience. Elder-care facilities, benefiting from government healthcare funding, are adopting antimicrobial bedding to streamline laundering processes and lower infection risks. These measures align with the sector's focus on hygiene and operational efficiency. Corporate and educational campuses, on the other hand, ensure a steady demand by prioritizing fire-retardant curtains and durable upholstery. Their focus remains on safety and longevity, catering to the specific needs of these environments.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Offline venues preserved 65.74% of the Japan home textile market in 2025 [STAT.GO.JP]. Department stores curate sensory displays where shoppers touch fabrics and receive sizing advice. Specialty chains integrate in-store laundry labs to demonstrate wash durability. Rural prefectures remain brick-and-mortar strongholds due to lower e-commerce penetration.

Online retail, growing at a 9.78% CAGR, prospers on high-resolution imaging, user reviews, and AI fit-guides. Domestic leaders are enhancing last-mile delivery by offering same-day bedding swaps and hassle-free returns, aiming to improve customer satisfaction. Korean entrants are leveraging influencer collaborations to appeal to style-conscious millennials and gain market share. Omnichannel pioneers are integrating QR codes on product tags, enabling customers to access AR-powered room visualization tools for a more interactive shopping experience. Cross-border marketplaces are expanding product selections, but this has intensified price competition. As a result, domestic brands are focusing on emphasizing their provenance and strengthening after-sales services to maintain competitiveness. The use of advanced technologies like AR is helping brands differentiate themselves in a crowded market. Additionally, the growing influence of social media and collaborations with influencers is reshaping consumer preferences, particularly among younger demographics. These trends highlight the evolving strategies employed by both domestic and international players to capture market share and meet changing consumer demands.

Geography Analysis

Kanto commanded 36.10% of Japan Home Textile Market size 2025 as Tokyo households combine high disposable income with dense apartment living. Premium cooling bedding and modular sofas dominate the assortment. Kansai follows, supported by Osaka’s fashion orientation and Kyoto’s hotel upgrade cycle. Chubu benefits from Toyota-linked economic stability, stimulating corporate dormitory orders for durable linens.

Hokkaido displays outsized demand for cold-weather textiles as average annual temperatures sit at 11.0 °C and winter lows dip to −7.4 °C. Thick knit throws, dual-tog comforters, and thermal drapes record brisk sales. The Tohoku region mirrors Hokkaido’s climate but skews older demographically, pushing easy-care wool blend blankets positioned for arthritis relief.

The Chugoku region is split between Sanyo’s urban Seto Inland Sea corridor and Sanin’s onsen-oriented coastal towns; the latter favors traditional tenugui towels and bath textiles reflecting local tourism themes. Shikoku’s aging profile supports hygiene-centric items, whereas Kyushu-Okinawa, forecast for a 5.06% CAGR, leverages inbound tourism and subtropical weather to promote quick-dry linen. Disaster preparedness culture in typhoon-prone prefectures drives interest in emergency sleeping bags and waterproof floor cushions.

Localized marketing proves critical. Successful brands tailor color palettes to regional tastes—pastels in Hokkaido, deep indigos in Kansai—and align sizing with prevalent housing stock. National players maintain efficiency by centralizing R&D while granting regional managers flexibility over assortments and promotions.

Regulatory Landscape

Japan home textile products are governed by consumer-facing labeling and safety rules. The Consumer Affairs Agency enforces the Household Goods Quality Labeling Act, which requires clear disclosure of fiber composition and care instructions for designated household goods, shaping packaging and SKU setup across offline and online channels.

Chemical safety compliance is anchored by the Ministry of Health, Labour and Welfare under the Act on Control of Household Products Containing Harmful Substances. The act restricts specified hazardous substances in textiles, including certain azo dyes and free formaldehyde. Standardization sits with JISC and the JIS system. METI announced a revision to JIS L 0001 in August 2024 covering symbols and methods for textile handling instructions, prompting updates to care-label systems and testing references used by brands and converters supplying the Japanese market.

Value Chain Analysis

The value chain starts with fiber and yarn sourcing (cotton, synthetic fibers, and growing cellulosics such as bamboo blends), then moves through spinning, weaving/knitting, dyeing/finishing, and cut-and-sew conversion into categories such as bed linen, bath linen, kitchen linen, and upholstery covers. Japan retains capability in specialty and technical textiles, but many mass-market home textile SKUs rely on imported finished goods and contracted conversion. Trading houses and specialist importers coordinate vendor selection, quality assurance, and landed-cost management.

Downstream, products reach large home-furnishing retailers, department stores, specialty shops, and e-commerce platforms, where online channels have gained importance as household-goods e-commerce penetration exceeds 31%. Quality and compliance checkpoints are increasingly formalized through industry-led programs (for example, JBA programs promoting domestic quality identification) and audit frameworks such as METI's Japanese Audit Standard for Textile Industry (JASTI) formulated in March 2025. JASTI adds structure to supplier due diligence, chemical management documentation, and traceability practices across multi-country sourcing.

Competitive Landscape

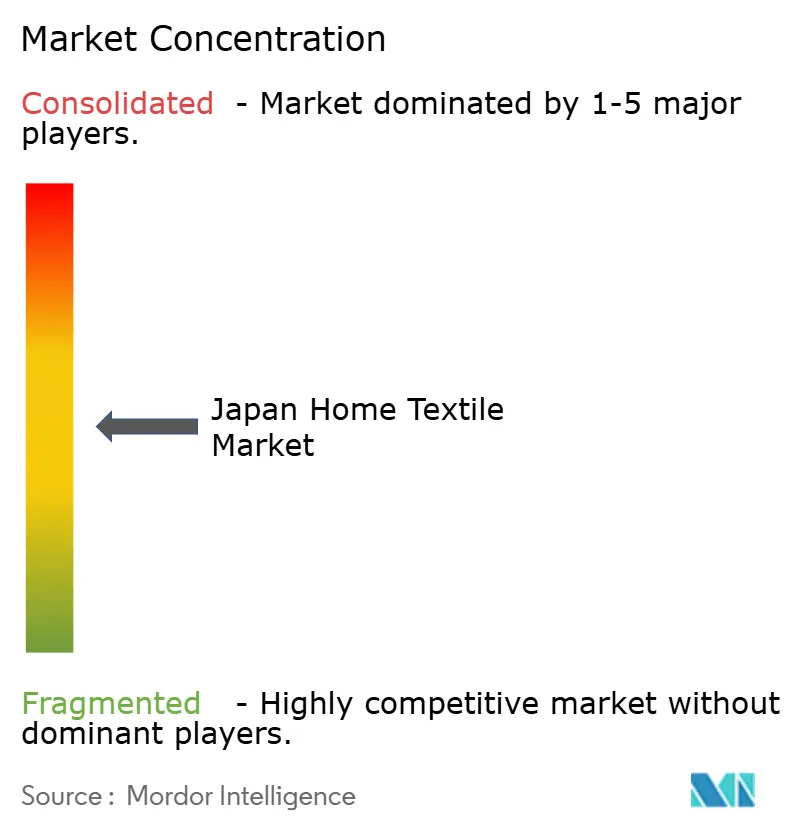

Japan home textile market exhibits medium concentration, with the five largest firms controlling roughly 55% of sales. Nitori combines vertical integration with disciplined merchandising to post FY 2024 revenue of JPY 895.8 billion (USD 5.7 billion). Its logistics network enables weekly SKU refreshes, reducing stock-out risk. Nishikawa prioritizes sleep science, bundling connected sensors with MuAtsu mattresses and achieving triple-digit shipment growth after a high-profile advertising blitz.

MUJI embraces minimalist aesthetics and recycled cotton programs to appeal to eco-aware millennials. Emerging challengers include Korean brands that exploit algorithmic merchandising on specialized apps, and technology entrants such as Sony and Mitsufuji that embed sensors into bedding and apparel. Domestic mid-tier producers counter by highlighting Japan-quality stitching and heritage weaving, but labor shortages raise the cost per unit.

Strategic moves focus on sustainability certification, smart fabric partnerships, and omnichannel expansion. Nitori piloted in-house PET-to-fiber recycling plants. Nishikawa collaborates with glamping resorts to showcase high-end mattresses in experiential settings. Feiler leverages German chenille craftsmanship through limited-edition collaborations that command premium price points. Government circular-economy targets may accelerate consolidation as smaller mills struggle with compliance investment.

Japan Home Textile Industry Leaders

Nitori Holdings Co., Ltd.

Nishikawa Co., Ltd.

Ryohin Keikaku Co., Ltd. (MUJI

IKEA Japan K.K.

Francfranc Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Closed-loop and recycled-synthetic textiles offer a defined whitespace as brands balance cost volatility, traceability demands, and sustainability positioning. Market activity already points in this direction through initiatives referenced in the report, including recycled polyester content targets and in-house PET-to-fiber pilots by large retailers. That creates room to scale bottle-to-fiber inputs, substantiate verified recycled claims, and expand product lines that pair easy-care performance with lower-impact materials.

Functional bedding and hygiene-forward textiles for aging households and institutional buyers also open expansion room. Products that reduce laundering burden and improve comfort (antimicrobial, quick-dry, thermo-regulating) align with this shift. On the demand side, Japan's inter-ministerial Residential Energy Conservation 2026 Campaign, including the Mirai Eco Housing 2026 Project with a JPY 175 billion budget, concentrates renovation and housing upgrades around defined performance criteria. This supports opportunities for home textile players to align assortments and merchandising with energy-efficiency renovations, such as thermal drapes and seasonal comfort bedding, and to partner with large retail platforms that bundle home-improvement spending into coordinated campaigns.

Recent Industry Developments

- July 2026: Nitori Holdings launched a new monthly sales campaign, Mainichi no Kurashi Oen, Kongetsu no Okaidoku-hin, starting July 10, 2026 with a Summer Countermeasures theme and discounts that include bedding. The campaign increases the cadence of theme-based promotions and ties cooling home textiles to seasonal demand peaks, supporting faster inventory turns in a mature replacement market.

- June 2026: Nishikawa introduced a gel-equipped urethane top unit option for its custom-order pillows to deliver a firmer feel while suppressing temperature rise. This adds a tangible technology hook to premium sleep accessories, reinforcing the markets shift toward thermo-comfort and wellness positioning in core bedding purchases.

- June 2024: Showa Nishikawa highlighted a sharp year-over-year rise in MuAtsu mattress shipments following a celebrity-backed durability campaign and the publication of internal sales rankings. The approach leverages social proof to steer consumers toward proven SKUs, strengthening premiumization tactics that lift value even when unit replacement cycles are long.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of home-use textile products sold in Japan that are used to furnish, decorate, or maintain living spaces, including items typically bought for bedrooms, bathrooms, kitchens, and living rooms.

Scope exclusions: We exclude apparel textiles, industrial and medical textiles, and pure furniture sales where a textile component is not the purchased item.

Segmentation Overview

- By Application

- Bed Linen

- Bath Linen

- Kitchen Linen

- Upholstery

- Others (Carpets and Area Rugs)

- By Material

- Cotton

- Linen

- Synthetic Fibers

- Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.)

- By End-User

- Residential

- Commercial

- By Distribution Channel

- Offline

- Online

- By Geography

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu and Okinawa

Data Sources, Market Sizing, and Validation

Desk Research

To build the basic market picture, we first pulled public information that shows how Japan households buy and use textiles at home and how prices have moved over time. Our review focused on Japan's official household spending and retail activity statistics (for example, Statistics Bureau of Japan), trade and tariff data for textile categories (for example, UN Comtrade and Japan Customs summaries), inflation and consumer price series (for example, Bank of Japan), and textile and fiber publications from trade bodies (for example, Japan Textile Federation).

We also used company filings and investor decks to understand product mix, channel emphasis, and pricing direction, and then set assumptions by product type and channel. Where public filings were uneven, we relied on a paid company financials and intelligence subscription to standardize revenue and ownership details. The desk research sources listed above are illustrative only, and we checked additional public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

For fieldwork, we spoke with people across the value chain in Japan, including manufacturers, brand teams, wholesalers, and retail and e-commerce decision-makers who track sell-through and promotions. These interviews helped us confirm which product groups are growing, how average selling prices are changing by fabric and construction, and where online share is taking demand from offline stores.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 42% | Functional/Unit leaders: 36% | |

| Smaller Players: 22% | Managers: 51% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where household demand and retail sales signals are reconstructed into a home-textile value pool for Japan, and then separated into the typical home categories before final totals are set. To keep the output realistic, we cross-check the result with selective bottom-up approximations such as sampled price x volume for key items, supplier revenue pointers, and channel checks from retailers, and we adjust when the two views do not align.

Key inputs include household consumption patterns for home-related goods, shifts in online versus offline share, import trends for textile and made-up textile articles, cotton and synthetic fiber cost movements that affect pricing, and promotional intensity that changes realized selling prices. Forecasts were built using scenario analysis, linking the demand outlook to expert views on consumer spending, housing-related replacement cycles, and expected price normalization, then stress-tested with simple time-series smoothing for categories that move more slowly. Where product-level data was thin, we used conservative proxy splits from interviews and public trade patterns, and then reconciled those splits back to the total demand pool so category gaps did not inflate the market.

Data Validation & Update Cycle

Each key assumption is checked through more than one angle, so the totals are compared against independent signals such as retail value movement, trade direction, and price trends before we finalize the numbers. Outliers are flagged early, the model is re-run after assumptions are refined, and an additional analyst reviews the changes for consistency.

The report is refreshed on an annual cycle, with interim updates triggered when material events occur, including sharp currency moves, major price resets in fibers, or sudden demand shifts in large channels. Before delivery, we run a final pass to ensure the latest public releases and interview findings are reflected in both the numbers and narrative.

Mordor Intelligence's Japan Home Textile Market Size Measured Against Other Published Estimates

It is normal to see different market sizes for Japan home textiles because publishers do not always count the same products, channels, and pricing points in the same way, and they may also choose different base years. In our checks, the largest gaps usually come from scope choices (what counts as home textile) and how price levels are converted and updated.

Some estimates roll adjacent categories like broader home furnishings or floor coverings into the total, and others use a faster price-growth curve based on premium product narratives rather than realized selling prices in Japan. Another driver is timing, since exchange rates and inflation can swing a USD view within a single year, and refresh cadence determines whether the latest retail softening or recovery is captured, which is a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.87 B (2025) | |

| Global Consultancy A | USD 12.38 B (2025) | This figure appears to use a wider product basket and higher realized value assumptions, which can happen when broader floor and furnishing textiles are included and channel prices are not adjusted for discounting. |

| Industry Publisher B | USD 6.00 B (2025) | This estimate likely applies a narrower inclusion list and may undercount domestic sales that do not map cleanly to trade-based sizing, which pulls down the total even when retail activity is steady. |

The comparison shows that most of the spread is explained by what gets counted as home textile and how prices are treated in USD terms for Japan. By keeping the scope tied to commonly purchased household textile categories and validating price and channel shares through interviews, the model stays traceable to a few clear inputs that can be repeated each year.

Key Questions Answered in the Report

How large is the Japan home textile market in 2026?

The Japan home textile market size is USD 9.01 billion in 2026.

What is the projected growth rate to 2031?

The market is expected to grow at a 1.56% CAGR, reaching USD 9.74 billion by 2031.

Which application segment commands the highest share?

Bed linen holds 43.21% of total sales, retaining leadership in 2025.

Which material is expanding the fastest?

Bamboo and other cellulosic materials are forecast to advance at an 7.89% CAGR through 2031.

How quickly are online sales growing?

Online channels are expanding at a 9.78% CAGR, driven by 31.54% e-commerce penetration in household goods.

Which region offers the most growth potential?

Kyushu-Okinawa shows the highest forecast CAGR at 5.06% through 2031.

Page last updated on: