Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

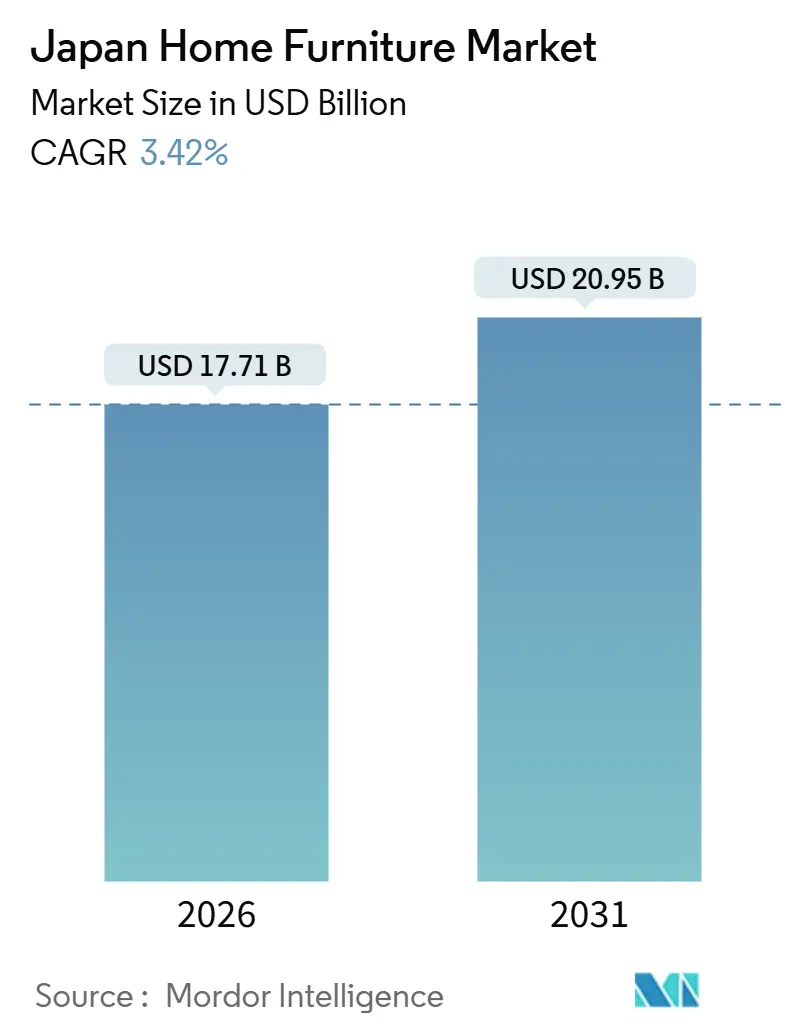

| Market Size (2026) | USD 17.71 Billion |

| Market Size (2031) | USD 20.95 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

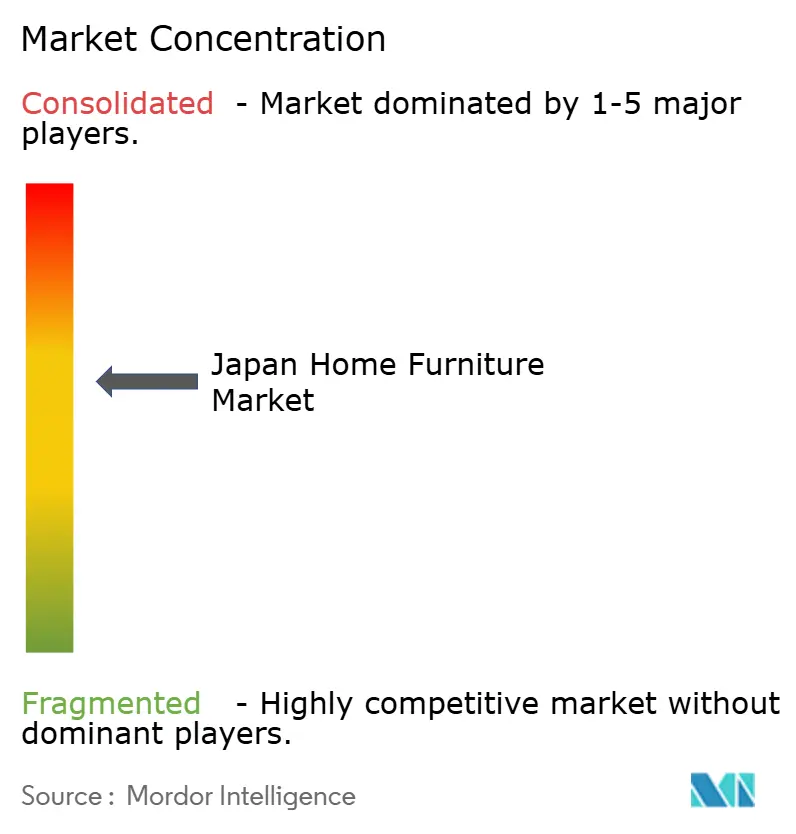

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Home Furniture Market Analysis by Mordor Intelligence

The Japan Home Furniture Market size is estimated at USD 17.71 billion in 2026, and is expected to reach USD 20.95 billion by 2031, at a CAGR of 3.42% during the forecast period (2026-2031).

Limited urban space in major metropolitan areas, combined with a rising share of compact new condominiums, is driving demand for modular storage solutions, foldable furniture, and space-efficient designs that fit apartments under 50 square meters without compromising functionality. With nearly 30% of the population aged 65 and above, there is increasing demand for ergonomic seating, assistive rails, and easily accessible furniture configurations suitable for multi-generational households. Digital commerce is deeply embedded in consumer behavior, as e-commerce accounted for 32.58% of household goods and furniture sales in fiscal 2024, reshaping pricing strategies, delivery models, and service expectations for both online-only and omnichannel retailers[1]Ministry of Economy, Trade and Industry, “Results of FY2024 E-Commerce Market Survey Compiled,” METI, meti.go.jp.. Cost pressures linked to yen depreciation have raised import prices for wood and other raw materials, but manufacturers have mitigated this through subsidies for equipment upgrades and increased adoption of certified domestic timber. Slower growth in new housing starts has limited first-time furnishing cycles, shifting the market focus toward replacement, renovation, and upgrading of existing households. These dynamics are creating opportunities for products that combine functionality, ergonomic design, and durable materials while leveraging both digital and physical channels to meet evolving consumer preferences.

Key Report Takeaways

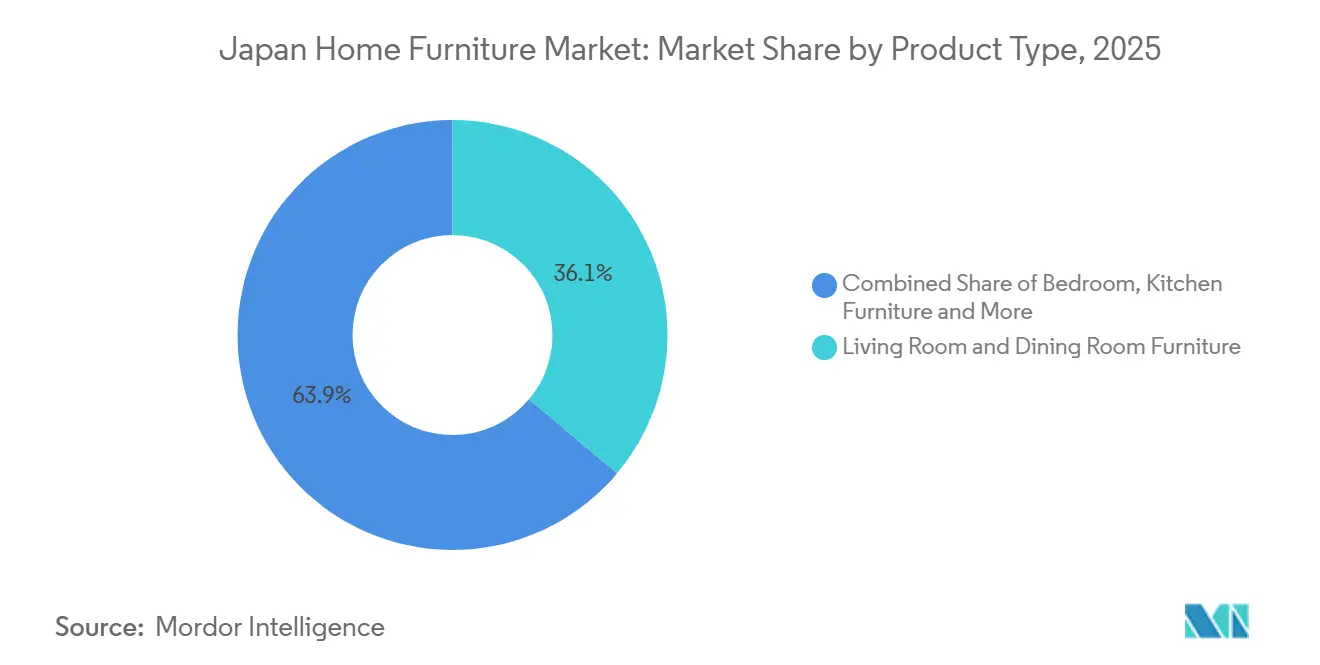

- By product type, living room and dining room furniture led with 36.12% of the Japan home furniture market share in 2025, while home office furniture is projected to expand at a 4.97% CAGR through 2031.

- By material, wood accounted for 56.12% of the Japan home furniture market share in 2025, whereas plastic and polymer are forecast to grow at a 4.56% CAGR through 2031.

- By price range, the economy segment held 45.53% of the Japan home furniture market share in 2025, and the premium segment is set to advance at a 4.87% CAGR through 2031.

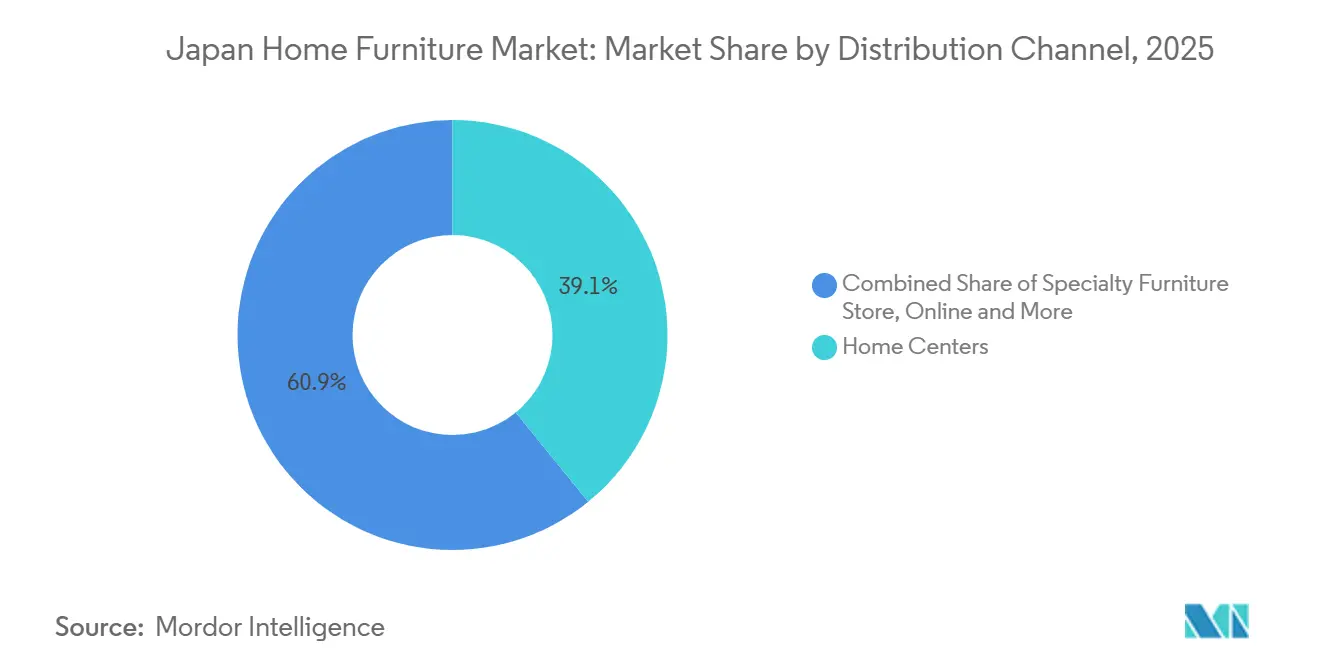

- By distribution channel, home centers held 39.12% of the Japan home furniture market share in 2025, and online is expected to post a 5.75% CAGR through 2031.

- By geography, Kanto accounted for 41.22% of the Japan home furniture market share in 2025, while Kansai is projected to grow at a 4.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Demanding Ergonomic & Assistive Furniture | +0.8% | Global, concentrated in Kanto & Kansai metros | Long term (≥ 4 years) |

| Urban Apartment Downsizing Boosting Multifunctional Furniture Demand | +0.6% | Tokyo 23 wards, Osaka central districts | Medium term (2-4 years) |

| E-commerce Penetration Increasing Furniture Accessibility | +0.5% | National, with early gains in Kanto, Chubu, Kyushu | Short term (≤ 2 years) |

| Government Incentives for Sustainably-sourced Wood Products | +0.4% | National, spill-over to rural prefectures | Medium term (2-4 years) |

| Tatami-inspired Hybrid Minimalist Designs Gaining Popularity | +0.2% | National, elevated uptake in Kansai | Short term (≤ 2 years) |

| Corporate Flex-office Conversions Prompting Bulk Home-office Purchases | +0.2% | Tokyo metropolitan area, Osaka business districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population Demanding Ergonomic & Assistive Furniture

Households with at least one member aged 65 or above already comprise a large share of the base, and the demographic tilt will shape product development and replacement patterns across the Japan home furniture market. Manufacturers are folding assistive features into mainstream ranges so that grab rails, anti-slip fabrics, and powered recline options are available without channeling buyers into specialized catalogs. The long-term expansion of the 75-plus cohort, concentrated in Kanto and western Honshu, establishes a stable renewal cycle as seating and beds are upgraded to models that lower caregiver strain and allow easier transfers. Pilot programs that embed posture sensors and environmental monitoring into chairs and desks remain at pre-commercial maturity, with the bulk of smart-furniture concepts clustered at Technology Readiness Levels 4 to 6 [2]Inês Mimoso et al., “Exploring Smart Furniture: A Systematic Review of Integrated Technologies, Functionalities, and Applications,” Sensors, mdpi.com. . The policy environment is supportive through barrier-free housing standards and guidance on care devices, which signals continued alignment between public health objectives and adaptive furniture features. As these dynamics extend, the Japan home furniture market will see a wider set of residential SKUs designed for mobility, safe access, and age-friendly ergonomics that fit into compact urban spaces.

Urban Apartment Downsizing Boosting Multifunctional Furniture Demand

High new-home prices in the major wards have pushed buyers toward smaller units, which prioritize utility and shift-in-place flexibility in furniture selection. Compact apartments without dedicated rooms are driving the uptake of expandable tables, fold-down desks, and storage-integrated sofas that can pivot between work, dining, and rest within a constrained footprint. Retailers are responding through room-set demonstrations scaled to actual city floor plans and by calibrating assortments for multi-function use, which keeps conversion high even as display areas shrink. Hybrid work preferences also influence home-office accessories, since many employees toggle between office and compact homes and prefer portable seating and collapsible stands to maintain ergonomic standards. Closed-loop manufacturing at domestic sites is maturing, with major integrated players reporting very high recycling rates that support polymer substitution and cost containment in e-commerce shipping. These forces together will continue to channel demand to multi-purpose formats in the Japan home furniture market, as developers and retailers co-optimize for space efficiency and practical comfort in daily use.

E-commerce Penetration Increasing Furniture Accessibility

The e-commerce ratio for household goods, furniture, and interiors reached 32.58% in fiscal 2024, which is several times higher than the overall B2C merchandise average and confirms a structural channel shift [3]Ministry of Economy, Trade and Industry, “Results of FY2024 E-Commerce Market Survey Compiled,” METI, meti.go.jp.. Virtual visualization tools and centimeter-level customization services reduce risk for high-involvement purchases and are reducing reliance on large showrooms in many catchments. Mobile apps with embedded recommendations and omnichannel checkout are enlarging average order values, while retailer networks of pick-up points lower last-mile costs for bulky goods and support reliable delivery time windows. Subscription and rental models for home furniture are gaining traction with frequent movers and with corporate buyers that need flexibility for hybrid workspace layouts, which adds recurring demand into the mix. As more households transact online for this category, fulfillment is concentrating in regional hubs that can handle heavy items with fewer touches and lower damage rates. The Japan home furniture market will continue to benefit from this channel’s service innovations and cost transparency, which will keep pressure on legacy store-only formats to adapt.

Government Incentives for Sustainably-Sourced Wood Products

National programs approved during 2024 to 2026 reimburse up to half of equipment conversion costs for manufacturers that move from imported inputs to domestic cedar and cypress, which tightens the cost gap and raises the wood self-sufficiency rate. These measures have helped offset currency-driven increases in delivered costs for imported plywood and hardwoods, which otherwise would have forced steeper retail price adjustments. Certification regimes such as JAS, FSC, and PEFC are widespread, and a meaningful share of forests now carry third-party verification, which supports premium positioning and B2B procurement criteria. The Clean Wood Act amendment from April 1, 2025, requires legality confirmation by upstream wood-related businesses and importers, and noncompliance triggers penalties and licensing risk that strengthen the case for a traceable supply [4]Forest Trends, “Japan Policies and Legal Requirements for Imported Timber and Timber Products,” Forest Trends, forest-trends.org.. Leading integrated manufacturers report very high coverage from certified sources and robust chain-of-custody systems, which safeguard continuity of supply and align with environmental procurement standards. As these policies take root, the Japan home furniture market will continue to see steady adoption of domestic wood and recycled inputs that reinforce both cost control and sustainability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Housing Starts Limiting New Furniture Purchases | -0.7% | National, acute in suburban Chubu & Kansai | Medium term (2-4 years) |

| Rising Raw-material & Logistics Costs Squeezing Margins | -0.4% | National, particularly import-dependent retailers | Short term (≤ 2 years) |

| Import Disruptions From Stricter Maritime Emissions Rules | -0.3% | National, affecting ocean-freight-dependent suppliers | Medium term (2-4 years) |

| Shrinking Skilled Carpentry Workforce Constraining Premium Supply | -0.2% | National, concentrated in Hokkaido & traditional crafts regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Housing Starts Limiting New Furniture Purchases

Housing starts dropped below long-term averages in 2024, reducing the volume of first-time furnishing demand and shifting market momentum toward replacement and upgrade cycles. Central bank commentary points to structural pressures from demographic decline and price dynamics, which continue to concentrate housing demand in central urban wards while suburban areas experience population outflows. Fewer residential completions have lowered demand for coordinated, full-home furniture purchases, resulting in smaller basket sizes compared with new-build outfitting. As a result, retailers with strong renewal-focused assortments, installation capabilities, and after-sales services are better positioned to stabilize revenues, while operators heavily exposed to new construction cycles face sharper volume declines. In response, the Japan home furniture market is increasingly prioritizing durability, repairability, and modular upgrades, making contractor partnerships and small-space customization essential strategies for sustaining demand amid lower housing completions.

Rising Raw-material & Logistics Costs Squeezing Margins

Yen depreciation has increased the landed cost of imported timber and furniture components, while domestic plywood prices have been revised upward, putting sustained pressure on margins for assortments with high import exposure. International timber market updates also point to rising prices for imported formwork plywood, which has filtered through to wholesale pricing and project costs. Logistics challenges have further intensified cost pressures, as ocean shipping disruptions and schedule volatility coincided with domestic trucking capacity constraints that complicated just-in-time delivery models. Vertically integrated retailers have been better positioned to manage volatility through long-term supply contracts and advance purchasing, whereas smaller operators have had limited flexibility and passed a greater share of cost increases on to consumers. In response, the Japan home furniture market is increasingly turning to recycled materials, certified domestic timber, and optimized distribution strategies that reduce last-mile costs and mitigate exposure to global supply shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Renovation and Hybrid Work Propel Home Office Surge

Living room and dining room furniture holds 36.12% in 2025 and remains the anchor for coordinated purchases, while home office furniture is set to grow at a 4.97% CAGR during 2026 to 2031 as hybrid work stabilizes. Living zones skew toward modular sofas and extendable tables that host multi-generational use without increasing footprint, which aligns with urban layouts where traffic flow and storage are equally important. The Japan home furniture market is also seeing a steady rotation into compact entertainment and display units that free wall space while hiding cables and peripherals. The home-office category is diverging into permanent setups for larger units and portable add-ons for small apartments where dedicated workrooms are not feasible, both of which support sustained growth in seating and ergonomic accessories. Overall, product mix decisions are influenced by space constraints, demographic needs, and workplace patterns, which together reinforce multifunctional, easy-to-move, and easy-to-clean designs across rooms.

Bedroom and kitchen categories track replacement cycles triggered by life events, retrofits, and safety upgrades for seniors, while bathroom and outdoor pieces remain niche within the residential share. The Japan home furniture market favors quiet aesthetics with neutral tones, which supports platform designs that can be reconfigured as needs change without replacing core frames. Consumers are more willing to mix home-office and living-room items when furniture can fold, stack, or telescope, which expands use cases without increasing clutter in small homes. Retailers with strong room visualization and pick-up networks are capturing share, as they can demonstrate function within realistic floor plans and keep delivery fees modest for bulky items. Given these conditions, the Japan home furniture market will continue to see Home Office Furniture outpace the broader category as the hybrid model persists and employers standardize support for at-home ergonomics.

By Material: Plastic Advances as Circular Economy Gains Traction

Wood holds a 56.12% share and remains the mainstay for frames, cabinetry, and premium finishes, supported by policies that encourage domestic species and by widespread certification that sustains trust and pricing power. Plastic and Polymer will advance the fastest at a 4.56% CAGR through 2031 due to lighter weight that lowers shipping costs and due to increased use of recycled inputs that match sustainability targets. The Japan home furniture market is also adopting metal selectively for ergonomic frames and minimalist accents where strength-to-weight ratios are decisive. Industry programs that improve traceability and raise the share of certified wood in total supply are stabilizing costs and ensuring steady access to inputs even when exchange rates move. As material science evolves, the balance of wood, polymer, and metal reflects trade-offs between cost, durability, weight, and environmental claims within the Japan home furniture market.

Circularity is now a competitive differentiator, particularly for high-volume retailers that can specify recycled plastics and bio-composites across hundreds of SKUs with reliable sourcing and quality control. Innovations in low-carbon steel are entering office-adjacent residential items, which signals a broader decarbonization of material choices beyond polymers and wood. In parallel, certified domestic timber helps reduce exposure to foreign supply shocks and aligns with legality requirements that regulators enforce in upstream wood trades. These shifts favor integrated players that can maintain consistent inputs at scale and reinforce the Japan home furniture industry’s push toward documented sustainability attributes. As end buyers place more weight on environmental information, materials strategy will remain central to product design and merchandising.

By Price Range: Premium Segment Defies Economic Headwinds

Economy led with 45.53% in 2025, which reflects strong value propositions and nationwide reach from the largest chains that match compact formats with accessible pricing. Mid-range attracts urban professionals who upgrade as income stabilizes, while Premium is projected to grow the fastest at a 4.87% CAGR through 2031 based on demand for craftsmanship, durable materials, and better ergonomics. Premium also benefits from export-oriented positioning and from collaborations that emphasize tactile qualities and meticulous finishing that stand out in showrooms and online visuals. The Japan home furniture market, therefore, displays a two-track profile in price sensitivity, where value formats scale by store density and logistics, and premium formats scale by brand equity and design leadership. As compliance requirements for timber legality and fire-safety standards tighten, brands with established certification systems may consolidate their share in the premium bracket due to smoother documentation and audit readiness.

Consumers who value premium wood and metal finishes increasingly evaluate supply chain transparency and environmental footprints along with form and function, which elevates the role of certified inputs and lifecycle claims in purchase decisions. In practice, this means premium ranges often highlight traceable wood and recycled content, while providing modular pieces that can adapt to different phases of urban living without compromising on comfort. As budgets polarize, the Japan home furniture market is seeing greater differentiation in warranty terms, service levels, and customization options that map to distinct price tiers. Retailers align this with showroom strategies and digital content that allow touch-and-feel for premium while maintaining the cost advantages of online discovery and pick-up for economy ranges. This architecture provides a steady base for premium to defy macro headwinds through value-added features and export exposure.

By Distribution Channel: Online Outpaces Brick-and-Mortar Across All Metrics

Home Centers commanded 39.12% in 2025, reflecting adjacency to DIY and home improvement categories and the ability to cross-sell furniture with easy pickup or scheduled delivery. Online is the fastest mover with a 5.75% CAGR projected through 2031, supported by a 32.58% e-commerce ratio in fiscal 2024 that shows consumer comfort with digital journeys for even high-ticket furniture. The Japan home furniture market benefits from extensive pick-up networks and compact urban fulfillment nodes that keep service times and costs down for bulky goods. As omnichannel tools improve visualization and inventory visibility, shoppers increasingly browse in-store and complete purchases online or vice versa, which blends the strengths of both channels. Over the forecast period, these shifts continue to raise the bar for traceability and compliance integration in e-commerce flows, especially for wood legality under the Clean Wood Act.

Specialty furniture stores concentrate on curated merchandising and service differentiation, particularly at mid-to-premium price points where consultation adds value to the purchase journey. Department stores and direct-to-consumer formats hold selective roles, often focused on branded showcases that drive awareness more than volume. Online growth is aided by logistics innovation, including pick-up points and automated warehouses that can handle heavier SKUs while mitigating damages and failed deliveries. As living space remains constrained in the largest cities, the Japan home furniture market also sees frequent purchase of micro-furniture and accessories online, which occur at shorter repeat intervals than full-room replacements. In combination, these factors sustain Online as the structural out-performer among channels while Home Centers remain the volume anchor by reach and adjacency.

Geography Analysis

Kanto accounted for 41.22% in 2025 and continues to set the tone for assortment and channel mix, supported by concentrated urban density and a high share of compact homes that require space-efficient furniture. The region’s elevated digital adoption aligns with widespread use of pick-up points and click-and-collect options that minimize delivery fees for bulky goods. The pipeline of new homes remains under pressure, so demand leans toward replacement with an emphasis on ergonomics to serve an older resident base. Retailers deploy room-set demonstrations scaled to realistic footprints that reflect urban floor plans, which improves conversion even when showrooms are modest in size. As housing and workplace patterns evolve, the Japan home furniture market in Kanto is likely to sustain its lead in omnichannel adoption and compact, modular assortments.

Kansai is the fastest growing at a projected 4.74% CAGR to 2031, aided by project cycles related to large events and a strong base of design-forward consumers receptive to minimalist and natural-material themes. The region benefits from hospitality and contract furnishing orders that boost volumes for select suppliers, even as the market prepares for normalization when event-driven demand subsides. Specialty retailers emphasize curated displays and local craftsmanship, and that supports premium positioning within urban centers in Osaka and Kyoto. As in Kanto, digital tools are widening access to home visualization and delivery scheduling, which lifts online conversion in dense neighborhoods that value speed and predictability. Taken together, the Japan home furniture market in Kansai will remain a key proving ground for compact design and omnichannel fulfillment suited to multi-family buildings.

Chubu maintains steady demand anchored by manufacturing hubs and a balanced mix of residential and office-adjacent purchases that spill into the home-office category. The broader Rest of Japan sees uneven trends, since population outflows temper demand in some prefectures while tourism and lifestyle migration lift niches in others, especially in Kyushu and Okinawa. Rural manufacturers face higher compliance and audit costs for timber legality, which can shift processing to better-equipped urban plants and raise procurement costs for distant retailers. Real estate developers are diffusing mixed reality sales tools that show furniture layouts before construction completes, which accelerates decision cycles and raises pre-delivery order rates in more cities over time. The Japan home furniture market size for Kanto and the Japan home furniture market share for Kansai together underscore the split between scale and growth that retailers manage when allocating inventory and marketing budgets.

Competitive Landscape

The market concentration in Japan’s home furniture sector remains moderate, with the top five players holding a combined share that still allows mid-sized specialists, regional chains, and artisanal brands to compete across multiple price tiers. Vertical integration has emerged as a key advantage for leading players that operate overseas manufacturing bases and centralized logistics networks, enabling shorter lead times and greater cost stability amid currency and freight volatility. Omnichannel capabilities further differentiate competitors, as investments in mobile applications, digital visualization tools, and dense pick-up networks help reduce friction while keeping store footprints small in high-rent urban areas. Sustainability credentials are increasingly used to differentiate product ranges and support premium pricing, particularly where circular materials and certified timber can be tracked end-to-end with transparent documentation. As a result, the Japan home furniture market balances scale efficiencies with design-led branding and regulatory compliance, shaping both channel strategies and assortment planning.

Recent strategic initiatives highlight how market leaders are positioning for the next growth cycle. IKEA Japan expanded its urban pick-up network and introduced hundreds of products featuring circular materials, aligning with both regulatory expectations and rising consumer scrutiny of sourcing and recyclability. Inter IKEA Group also emphasized affordability in 2024 by resetting wholesale prices, prioritizing unit volume growth even at the expense of near-term revenue. Okamura strengthened its international presence through the acquisition of a UK-based loose furniture specialist, broadening its portfolio beyond task seating to address hybrid work and home-office demand. Meanwhile, integrated timber groups continued to emphasize high shares of certified wood and strong traceability, supporting public procurement requirements and private-sector ESG standards.

White-space opportunities are emerging in areas such as ergonomic home-office solutions for hybrid workers, subscription-based furniture models for mobile households, and age-friendly smart features as regulatory clarity improves. The market remains open to specialist entrants that pair digital configuration tools with curated assortments and verifiable compliance from raw material to finished product. Increased use of low-carbon metals and recycled polymers is expanding cost-stable options for structural components, helping reduce exposure to freight disruptions and currency swings. Urban-format stores linked to dense pick-up networks allow retailers to raise service levels without investing in large showroom footprints, keeping operating costs aligned with Japan’s high-density retail landscape. Together, these trends reinforce the view that a combination of cost control, compliance credibility, and customer convenience will drive competitive gains in the Japan home furniture market.

Japan Home Furniture Industry Leaders

Nitori Holdings Co., Ltd.

Ryohin Keikaku Co., Ltd. (MUJI)

IKEA Japan K.K.

IDC Otsuka Furniture Co., Ltd.

Francfranc Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: IKEA Japan opened its Hiroshima store, marking the 16th total location and 10th large-format store nationwide, part of an omnichannel strategy integrating 596 pick-up points to reduce last-mile delivery costs and environmental impact.

- September 2025: L Catterton, a global consumer-focused private equity firm, made a strategic investment in Seki Furniture, positioning the Japanese manufacturer for international expansion and operational scaling.

- March 2025: Okamura Corporation resolved to acquire 100% of Boss Design Limited, a UK-based office furniture manufacturer focusing on loose furniture.

- January 2024: IKEA opened its Maebashi store in Japan’s north Kanto region, the first in that area, as part of Ingka Group’s multi-year investment in stores across East Asia.

Japan Home Furniture Market Report Scope

In Japan, the home furniture market encompasses everything from manufacturing and importing to distributing and retailing furniture. This furniture, spanning from mass-market to premium segments, is tailored for residential spaces like living rooms, bedrooms, kitchens, and home offices. Demand is influenced by housing trends, urban density, an aging demographic, renovation activities, and a consumer shift towards compact, high-quality, and space-efficient furnishings. A complete background analysis of the Japan home furniture market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report.

The Japan Home Furniture Market Report is Segmented by Product Type (Living Room and Dining Room Furniture, Bedroom Furniture, Kitchen Furniture, Home Office Furniture, Bathroom Furniture, Outdoor Furniture, Other Furniture), Material (Wood, Metal, Plastic and Polymer, Others), Price Range (Economy, Mid-Range, Premium), Distribution Channel (Home Centers, Specialty Furniture Stores, Online, Other Distribution Channels), and Geography (Kanto Region, Kansai Region, Chubu Region, Rest of Japan). The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| Kanto Region |

| Kansai Region |

| Chubu Region |

| Rest of Japan |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Kanto Region |

| Kansai Region | |

| Chubu Region | |

| Rest of Japan |

Key Questions Answered in the Report

What is the current size and expected growth of the Japan home furniture market?

The Japan home furniture market size stands at USD 17.71 billion in 2026 and is projected to reach USD 20.95 billion by 2031 at a 3.42% CAGR, reflecting steady expansion anchored by compact living trends and an aging population.

Which product category is leading growth in Japan?

Living Room and Dining Room Furniture leads by share at 36.12% in 2025, while Home Office Furniture records the fastest growth at a 4.97% CAGR.

How do demographic shifts influence furniture demand in Japan?

The rising share of residents aged 65 and above increases demand for ergonomic seating, assistive rails, and age-friendly designs, which supports durable, safe, and compact solutions suited to multi-generational homes in dense urban areas.

What materials strategies are gaining traction among Japanese furniture makers?

Certified domestic wood use is expanding due to incentives and legality requirements, while recycled plastics and low-carbon metals are gaining share to improve cost stability and meet sustainability criteria across categories.

Page last updated on: