Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.77 Billion |

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Floor Covering Market Analysis by Mordor Intelligence

The Japan Floor Covering Market size is expected to grow from USD 2.77 billion in 2025 to USD 2.93 billion in 2026 and is forecast to reach USD 3.92 billion by 2031 at 5.97% CAGR over 2026–2031. The trajectory reflects a pivot from new-build activity to renovation-led spending as an aging residential and commercial stock drives systematic upgrades. Demand aligns with improvements in energy efficiency, indoor air quality, and safety in high-use environments, especially in metropolitan areas. Product mix shifts continue to favor modular, fast-install systems that reduce downtime and address labor constraints. Domestic incumbents consolidate share through logistics, technical support, and compliance capabilities that meet procurement standards across public and private projects. Competitive strategies in the Japan Floor Covering market emphasize reliable supply, circular materials, and verified low-emission performance to meet rising regulatory and ESG requirements. Redevelopment cycles around rail hubs and mixed-use corridors in Tokyo and Osaka sustain replacement demand as building owners refresh interiors for flexible use.

Key Report Takeaways

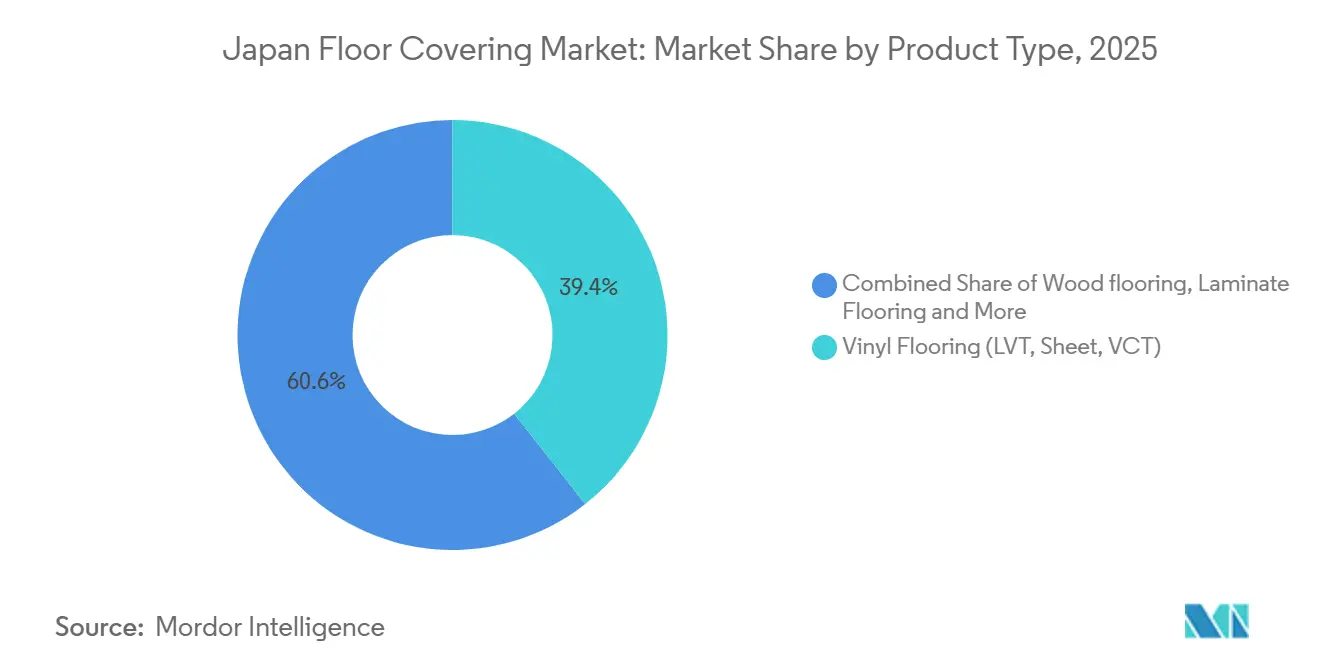

- By product type, vinyl flooring led with 39.35% of revenue in 2025, and Luxury Vinyl Tile is projected to grow at an 8.39% CAGR through 2031, indicating that the Japan Floor Covering market size for vinyl formats is set to expand alongside the fastest subcategory, while the same period confirms vinyl’s leadership in the Japan Floor Covering market share with its 2025 position.

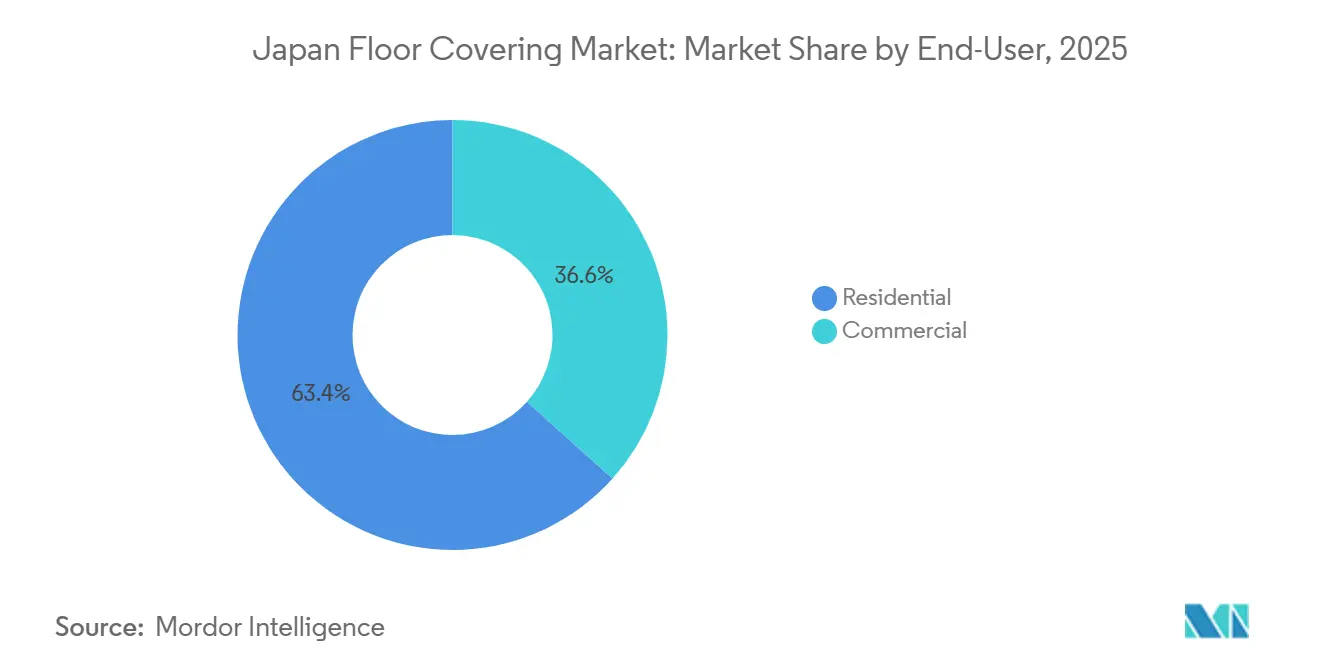

- By end user, residential accounted for 63.36% of 2025 volume, and the commercial segment is forecast to grow at an 8.35% CAGR between 2026 and 2031, which indicates that the Japan Floor Covering market size for commercial applications will advance faster over the forecast horizon, while residential retained the largest 2025 Japan Floor Covering market share.

- By distribution channel, B2C retail held 67.35% in 2025 and is expected to increase at an 8.98% CAGR, showing that the Japan Floor Covering market size within consumer channels is poised for strong growth, while the 2025 Japan Floor Covering market share remained anchored in retail-led sales.

- By geography, Kanto captured 41.44% in 2025, and Kansai is projected to grow at an 8.35% CAGR, which suggests the Japan Floor Covering market size in Kansai is set to expand fastest among regions, while Kanto retained the leading 2025 Japan Floor Covering market share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing stock renovation demand | +1.2% | National, with early gains in Kanto, Kansai, and Chubu metropolitan cores | Medium term (2-4 years) |

| Large-scale infrastructure refurbishments tied to Osaka-Kansai Expo 2025 | +0.8% | Kansai core, spill-over to Chugoku | Short term (≤ 2 years) |

| Growing uptake of resilient flooring in healthcare and senior-care facilities | +0.7% | National, concentration in Kanto and aging rural prefectures | Medium term (2-4 years) |

| Consumer shift toward eco-friendly and low-VOC materials | +1.0% | National, strongest in Tokyo and Osaka metros | Long term (≥ 4 years) |

| Revival of tatami-look vinyl and hybrid floors | +0.3% | National, niche in traditional residential settings | Medium term (2-4 years) |

| Emergence of smart, IoT-enabled flooring solutions | +0.2% | Pilots in Tokyo, Yokohama, Osaka healthcare clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Housing-Stock Renovation Demand

Renovation-led demand has strengthened as policy and demographic realities channel investment from new builds into upgrades across major metros. MLIT data and government statistics confirm sustained periods of weakness in new housing starts through 2024 and into 2025, reinforcing the shift to stock enhancement programs that improve habitability and energy efficiency in existing homes and condos[1]Source: Statistics Bureau, “Statistics Dashboard Graph Screen (Osaka-fu Housing Starts),” Statistics Bureau of Japan, dashboard.e-stat.go.jp. Corporate filings reinforce this pivot, with large suppliers reporting rising renovation sales contribution as owners prioritize floor replacement during multi-room updates to consolidate contractor mobilization and limit disruptions. Long-term industry commentary cites a sizable cohort of homes constructed during the 1990s now entering replacement windows for floors and other interior systems, which aligns with standard lifecycle practices in Japan’s housing stock. Public and private programs encourage barrier-free design and step-difference reduction as single-occupant and elderly households pursue safety-oriented upgrades that favor resilient surfaces and low-threshold transitions in living spaces. The Japan Floor Covering market benefits from this pattern because flooring replacement can be completed quickly with modular formats, enabling staged renovations while residents remain in place.

Large-Scale Infrastructure Refurbishments Tied to Osaka-Kansai Expo 2025

Government-led programs in Kansai achieved notable transit and access upgrades, with bridge works and a metro extension to the Yumeshima site completed on schedule, which helped trigger a wave of ancillary refurbishments in hospitality and commercial properties[2]Source: Kinki Regional Development Bureau, “Initiatives for the Osaka-Kansai Expo,” Ministry of Land, Infrastructure, Transport and Tourism, kkr.mlit.go.jp. Official statistics show pronounced volatility in Osaka housing activity in late 2025, including strong spikes that reflect pre-Expo and tourism-related investment, which lifts near-term demand for fast-turn flooring solutions in hotel corridors and public pavilions. Design choices at the Expo featured durable and modular surface systems to handle heavy foot traffic and condensed construction windows, providing a reference for product durability and installation speed in high-traffic settings. Post-Expo plans designate parts of Yumeshima for continued commercial use, extending the replacement cycle as permanent facilities complete fit-outs in 2026 and 2027. Regional spillovers into Kyoto, Kobe, and Nara sustain demand for compliant, resilient floors that meet local fire and VOC standards, supporting a multi-year uplift in the Japan Floor Covering market across western Japan.

Growing Uptake of Resilient Flooring in Healthcare and Senior-Care Facilities

Senior-care and medical assets continue to attract investment, supported by government care frameworks that prioritize coordinated networks across clinics and long-term facilities, which in turn emphasize flooring that is hygienic, slip-resistant, and easy to disinfect [3]Source: Healthcare & Medical Investment Corporation, “Impact Report | Initiatives for ESG,” Healthcare & Medical Investment Corporation, hcm3455.co.jp. Commercial carpet tiles and resilient sheets are widely specified for their maintenance advantages and acoustic performance in administrative zones and corridors, and product literature from major suppliers highlights antibacterial treatments and recycled content that align with ESG goals. Procurement standards in public and institutional projects favor Eco Mark and 4VOC compliance, steering orders to domestic producers with certified low-emission products and established supply continuity[4]Source: Japan Adhesive Industry Association, “Voluntary VOC Regulating Rule for Indoor Air Pollution Control,” Japan Adhesive Industry Association, jaia.gr.jp. Hospital and care operators value reduced downtime during retrofits, and modular formats allow phased installation around patient occupancy, which helps maintain operations without extended closures. A combination of compliance-driven specifications and the practical benefits of resilient and modular systems in high-usage medical environments, therefore, buoys the Japan Floor Covering market.

Consumer Shift Toward Eco-Friendly and Low-VOC Materials

Indoor air-quality scrutiny has increased as studies document seasonal VOC concentration patterns in occupied homes, which raises awareness of adhesives and floor substrates that can impact indoor environmental health. Manufacturers have responded by clarifying compliance with 4VOC standards across new vinyl-sheet ranges, enabling eligibility for green procurement and adding clear labels for specifiers and public buyers[5]Source: TOLI Corporation, “TOLI Integrated Report 2024,” TOLI Corporation, irpocket.com. Wood-oriented manufacturers emphasize the use of recycled and plantation-based inputs to reduce strain on tropical hardwoods and to align with corporate environmental roadmaps that target deeper emissions reductions by mid-century. Broader interior-products portfolios link flooring to larger renovation baskets that include kitchens and baths, reinforcing sustainability messaging and channel synergies that direct traffic into compliant flooring ranges. Recycling systems that collect used carpet tiles and regenerate backing have expanded in capacity, reflecting both policy momentum and end-customer demand for circular-economy solutions that document CO2 contribution rates within project reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining new housing starts in a mature construction market | -1.5% | National, acute in rural prefectures | Long term (≥ 4 years) |

| Volatility in PVC and petrochemical input prices | -0.6% | National, impacts vinyl producers | Short term (≤ 2 years) |

| Shortage of certified floor-installation labor | -0.4% | National, most acute in Kanto and Kansai | Medium term (2-4 years) |

| Seismic building codes limiting use of heavy tile and stone | -0.2% | Seismic Zone A, mitigated by lightweight innovation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining New Housing Starts in a Mature Construction Market

Government data confirm intermittent declines in national housing starts through late 2024 and into 2025, which constrains new-build demand for floor coverings in detached homes and condominiums. This macro headwind intensifies in rural prefectures that face sharper depopulation and lower replacement rates, creating divergent regional baselines for suppliers. Renovation activity in major metros offsets some of the decline, but the new-build pipeline remains thinner than earlier cycles. Public investment in refurbishments and infrastructure helps stabilize related commercial demand in select regions. The Japan Floor Covering market adapts by aligning sales emphasis with renovation-focused channels and by packaging fast-install systems that reduce time on site.

Volatility in PVC and Petrochemical Input Prices

Price swings in core inputs, including PVC resins and logistics, have prompted wholesale price revisions by domestic firms, which lifted value even when physical volumes slowed. This volatility complicates tender pricing and inventory planning for vinyl formats, which remain a major share of installed floors in healthcare, retail, and residential replacement. Companies increasingly rely on diversified sourcing and recycling loops to buffer cost shocks over shorter windows. Buyers remain sensitive to price but will meet premium points for compliant low-VOC and recycled-content goods. The Japan Floor Covering market preserves margin in part through certified performance that justifies specification in public and institutional projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vinyl Commands, LVT Accelerates Amid Anti-Bacterial and Click-Lock Innovation

Vinyl flooring held 39.35% of 2025 product revenue, and Luxury Vinyl Tile is forecast to rise at an 8.39% CAGR through 2031, with wholesale figures showing robust value momentum in plastic flooring categories due to price revisions that offset softer shipment volumes. Strategic products within corporate portfolios, including modular carpet tiles and vinyl tiles, posted growth as contractors prioritized flexible and rapid installations during phased refurbishments that minimized downtime. Product catalogs emphasize low-VOC claims and recycling systems, with expansion of collection capacity for used carpet tiles and the horizontal recycling of special PVC backing, which supports ESG reporting for corporate buyers. Temporary supply suspensions following a supplier factory fire highlighted concentrated sourcing risk, but phased restoration timelines stabilized shipments over 2025, supporting recovery in vinyl sheet categories. The Japan Floor Covering market continues to rely on click-lock and other labor-saving innovations that reduce installation hours and support renovation rhythms across healthcare, hospitality, and residential replacement.

Carpet and area rugs remain significant in commercial settings, with wholesale values reflecting strong performance for domestic tufted tiles and ongoing preference for modular formats in offices and institutional corridors. Ceramic and porcelain tiles face more cautious use in high-seismic zones and multi-story retrofits that would require additional structural measures, which channels heavier usage to ground floors and areas where loads can be accommodated under code. Wood flooring maintains a design premium and thermal comfort appeal, and manufacturers highlight recycled and plantation substrates to satisfy procurement and sustainability thresholds, which guide choices in public and large private projects. Laminate serves cost-sensitive segments that demand improved moisture resistance, while stone remains a niche in luxury residential entryways and high-end hospitality. Overall, the Japan Floor Covering market shows a durable preference for resilient and modular categories that balance compliance, lifecycle, and installation efficiency.

By End User: Residential Leads, Commercial Accelerates on Healthcare and Corporate Flex-Space

Residential users accounted for 63.36% of the 2025 volume, reflecting deep stock and steady replacement cycles in urban and suburban areas as homeowners pursue manageable upgrades fitting around daily routines. Corporate filings report rising renovation contributions as integrated portfolios bundle floors with kitchens and baths, engaging homeowners in broader interior refreshes through a single procurement flow. Modular vinyl and sheet formats allow one to two-day installation timelines that reduce disruption and align with weekend or staggered contractor schedules. Safety-focused upgrades, including barrier-free transitions and slip-resistant surfaces, align with aging-in-place programs in detached homes and condominiums. The Japan Floor Covering market continues to serve residential demand with click-and-lock formats and low-VOC materials that balance speed and indoor air-quality priorities.

Commercial demand is forecasted to grow at an 8.35% CAGR from 2026 to 2031, driven by healthcare, offices, and select hospitality properties, which will consistently specify resilient and modular carpet systems to optimize maintenance and flexibility. Public and institutional tenders favor certified emissions profiles and recycling schemes that can be documented in ESG reporting, pushing selection toward domestic producers with proven supply continuity. Office retrofits in Tokyo and Osaka implement modular carpet tiles to enable hot-desking and frequent reconfiguration, which shrinks downtime and reduces waste during layout changes. Education and government buildings continue to seek durable, easily maintainable surfaces under budget constraints while observing emission and fire-retardancy norms. The Japan Floor Covering market captures these varied needs with a portfolio spanning resilient sheet, VCT, LVT, and carpet tiles targeted at specific commercial functions.

By Distribution Channel: B2C Retail Leads, Online Gains Share Amid DIY Surge

B2C retail captured 67.35% of distribution in 2025 and is projected to grow at an 8.98% CAGR as home centers and online platforms support manageable renovation projects with pre-cut vinyl, click LVT, and easy-lay carpet tiles. National household spending statistics include classifications for floor-covering purchases that align with steady household-led buying patterns, which support continued growth in consumer channels. Manufacturer-led digital tools that let consumers visualize rooms and order samples reduce friction in product selection and encourage upgrades that fit within family schedules. Integrated interior companies combine floors with kitchens and baths to create a seamless path from inspiration to purchase, helping consumers coordinate materials within one order flow. The Japan Floor Covering market, therefore, reflects an ecosystem where DIY-friendly products and digital journeys reinforce retail-led share.

Contractor channels remain essential for non-residential projects and large residential upgrades that require skilled installers, and dedicated manufacturer teams support major accounts with technical assistance and logistics. Wholesalers aggregate orders for renovation specialists and coordinate just-in-time site deliveries in constrained urban environments, which is a critical service component in dense metros. Workforce constraints push contractors toward fast-install systems to meet schedules under overtime limits, which helps modular formats gain share on job sites. Public-sector compliance requirements for low-VOC and recycled content channel specifications to brands with recognized certifications and product documentation packages. The Japan Floor Covering market continues to balance retail momentum with trade relationships that secure large project outcomes across institutional segments.

Geography Analysis

Kanto accounted for 41.44% of 2025 share, reflecting the region’s scale, density, and continuous renewal of its large condominium stock and corporate offices. Housing-starts data show that Greater Tokyo remains a dominant contributor to national volume even during periods of decline, underscoring the base of activity that supports steady replacement cycles. Healthcare operators and premium senior residences in Tokyo drive specifications for engineered wood in private units and resilient surfaces in common areas, reflecting a hybrid design approach that pairs aesthetics and maintenance needs. Smart-care platforms already deployed in eldercare properties establish the digital backbone that can accommodate on-floor sensing in the future as integration costs fall. The Japan Floor Covering market in Kanto remains anchored in renovation-heavy cycles with steady commercial refits around transit hubs and mixed-use corridors that value speed and compliance.

Kansai is projected to record the fastest regional growth at an 8.35% forecast CAGR, aided by the Osaka-Kansai Expo buildouts and the conversion of the Yumeshima site for continued commercial usage. MLIT documentation confirms the completion of core access projects and the reinforcement of the surrounding development fabric, which drives hotel and facility refurbishments in adjacent districts. Osaka statistics show pronounced movements in monthly housing starts that align with the unique timing of Expo-related activity, which informs suppliers’ capacity planning for modular, resilient materials. Regional tourism recovery and hotel renovations in Kyoto, waterfront redevelopment in Kobe, and cultural-facility upgrades in Nara amplify project volumes and diversify product needs across carpet tiles, vinyl plank, and specialized resilient sheets. The Japan Floor Covering market in Kansai benefits from projects that value rapid installation, robust hygiene performance, and low emissions to comply with metropolitan procurement norms.

Chubu represents a sizable share of the Japan Floor Covering market as Nagoya’s industrial base, logistics hubs, and corporate campuses underpin periodic office refreshes and facility maintenance. Official data indicate sharper drops in residential starts during certain months of 2025 across major metros, including the Greater Nagoya area, pointing to selective pockets where renovation must offset new-build softness. Detached-home prevalence and barrier-free conversions influence residential product choices as owners favor resilient sheet and vinyl transitions for flush thresholds and wet-area durability. Industrial flooring needs in factories and logistics zones add demand for heavy-duty resilient formats, epoxy coatings, and VCT in cost-sensitive areas. The Japan Floor Covering market across smaller regions beyond the three largest metros reflects varied demographics and economic profiles, with eldercare construction and municipal refurbishment programs providing localized growth platforms supported by compliant, durable products.

Competitive Landscape

The competitive field is moderately concentrated, with the top five companies holding a combined majority of market share, while the remainder is distributed among regional specialists, import brands, and private-label lines. TOLI reported net sales of USD 0.65 billion (JPY 102.47 billion) in FY2024 and record operating income, attributing the performance to price revisions and increased recycling capacity that support circularity for carpet tiles. Sangetsu recorded revenue of USD 1.28 billion (JPY 200.4 billion) in FY2024 and detailed the impact and recovery plan after a supplier fire temporarily constrained vinyl-sheet shipments, with phased resumption schedules stabilizing by late 2025. Suminoe maintains leadership in commercial carpet tiles and continues to highlight high recycled-content ratios and antibacterial options for healthcare and hospitality applications, which align with public procurement criteria. The Japan Floor Covering market rewards incumbents that link service quality, technical documentation, and certified compliance with reliable delivery.

Daiken integrates flooring within a broader housing-materials portfolio that emphasizes recycled and plantation-based substrates, improving the sustainability profile of engineered wood offerings and supporting public-sector eligibility. LIXIL formed the Living Business segment in April 2025 by consolidating wooden interior materials with kitchens and vanities to raise cross-category sales and the renovation ratio, which seeks to capture wallet share from homeowners executing comprehensive upgrades. Domestic portfolios are broad, with SKU coverage across resilient, carpet, and wood categories to support one-stop procurement strategies that appeal to specifiers and general contractors. Companies also invest in digital selection and sample logistics to accelerate decision cycles in both B2B and B2C contexts. The Japan Floor Covering market favors brands that can meet low-VOC, recycling, and fire-safety thresholds, with transparent documentation at bid time.

Channel and product strategies reflect three archetypes that remain stable across cycles. Vertical manufacturers leverage scale economics and recycling infrastructure to differentiate cost positions and circular credentials, as seen in carpet tile backing regeneration and JAIA 4VOC compliance across product launches. Asset-light aggregators offer breadth and service speed, aligning with project managers who prefer consolidated ordering and rapid fulfillment across multiple finish categories. Niche specialists dominate applications with high technical barriers, such as rail interiors, where long-standing safety and durability records drive selection over price-only considerations. The Japan Floor Covering market continues to balance consolidation at the top with a competitive mid-tier that serves regional and application-specific needs.

Japan Floor Covering Industry Leaders

TOLI Corporation

Sincol Co Ltd

TOYOTEX

DAIKEN CORPORATION

Hisamatsu Seito Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Green-Flor, a European flooring brand, launched its products in Japan by exhibiting at JAPANTEX 2025, targeting expansion into the Asian market with innovative designs.

- April 2025: Sangetsu Corporation completed the acquisition of SDS Co., Ltd., strengthening its interior materials and floor covering distribution network in Japan.

- April 2025: LIXIL Corporation established the Living Business segment by integrating wooden interior materials with kitchens and vanities, targeting USD 1.3 billion (JPY 210 billion) sales in FY2026 and a 45% renovation-sales ratio, with positioning that links flooring to broader interior upgrade baskets.

- March 2025: TOLI Corporation expanded its carpet-tile recycling capacity with a new plant that enables horizontal recycling of used carpet tiles into special PVC backing, supporting medium-term waste-reduction and recycling-rate targets.

- February 2025: Japan Recycle Carpet Association launched a new certification system for recycled carpet tiles, promoting sustainability in the floor covering industry.

Japan Floor Covering Market Report Scope

A floor covering is a piece of material used to protect or decorate a floor. The report provides a detailed study of the underlying factors for the variations in the floor covering market growth trends. The report also provides a competitive landscape, covering company market shares, with detailed profiling for major revenue-contributing companies.

The Japan floor covering market is segmented by product type, end user, distribution channel, and geography. By product type, the market is segmented into carpet & area rugs, wood flooring, ceramic tile, laminate flooring, vinyl flooring [LVT, Sheet, VCT], stone flooring, and other products. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/retail, B2B/contractors. By geography, the market is segmented into Kanto, Kansai, Chubu, and the Rest of Japan. The report offers market size and forecasts for the Japan floor-covering market in terms of revenue (USD) for all the above segments.

By Product Type

| Carpet & Area Rugs |

| Wood Flooring |

| Ceramic & Porcelain Tiles |

| Laminate Flooring |

| Vinyl Flooring ( LVT, Sheet, VCT) |

| Stone Flooring |

| Other Products |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors |

By Region

| Kanto |

| Kansai |

| Chubu |

| Rest of Japan |

| By Product Type | Carpet & Area Rugs | |

| Wood Flooring | ||

| Ceramic & Porcelain Tiles | ||

| Laminate Flooring | ||

| Vinyl Flooring ( LVT, Sheet, VCT) | ||

| Stone Flooring | ||

| Other Products | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors | ||

| By Region | Kanto | |

| Kansai | ||

| Chubu | ||

| Rest of Japan | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan Floor Covering market?

The market is USD 2.93 billion in 2026 and is forecast to reach USD 3.92 billion by 2031 at a 5.97% CAGR, reflecting steady renovation-led demand in major metros.

Which product category leads demand in Japan’s floor coverings?

Vinyl flooring leads with 39.35% of 2025 product revenue, and Luxury Vinyl Tile is projected to record the fastest growth through 2031 due to installation speed and compliance-friendly specifications.

How is end-user demand shifting across residential and commercial segments?

Residential remains the largest user at 63.36% of 2025 volume, while commercial is expected to grow faster through 2031 as healthcare, offices, and select hospitality drive resilient and modular specifications.

Which distribution channels are gaining share in Japan?

B2C retail accounts for 67.35% of 2025 distribution and is projected to grow at an 8.98% CAGR as home centers and online platforms support DIY-friendly products and digital selection tools.

Which regions are most important for floor covering demand?

Kanto holds the largest share at 41.44% in 2025, while Kansai is projected to grow the fastest on post-Expo buildouts and facility upgrades across Osaka, Kyoto, and Kobe.

What compliance factors shape product selection in Japan?

Low-VOC certification, fire-retardancy, green procurement eligibility, and recycling pathways are critical, with JAIA 4VOC, Eco Mark, and documented recycling programs influencing public and private procurement choices.

Page last updated on: