Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 3.58 Billion |

| Market Size (2031) | USD 4.67 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Energy Drink Market Analysis by Mordor Intelligence

The Japan energy drink market size is estimated at USD 3.58 billion in 2026, and is expected to reach USD 4.67 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031). This trajectory reflects a market balancing entrenched consumer habits around traditional vitamin-fortified energy tonics with accelerating demand for natural formulations, premium packaging, and functional ingredients targeting muscle recovery and cognitive performance. Japan's aging workforce and surging e-sports participation create divergent consumption patterns. Older cohorts favor pharmaceutical-heritage brands dispensed through 3.97 million vending machines, while younger gamers gravitate toward carbonated imports and low-sugar variants sold in convenience stores that command the majority of food and beverage sales[1]Source: Ministry of Economy, Trade and Industry, "Monthly Report on the Current Survey of Commerce", meti.go.jp. The interplay between regulatory stringency under the Ministry of Health, Labour and Welfare, and brand localization strategies determines which players capture share in a market where distribution density, not just brand equity, drives profitability.

Key Report Takeaways

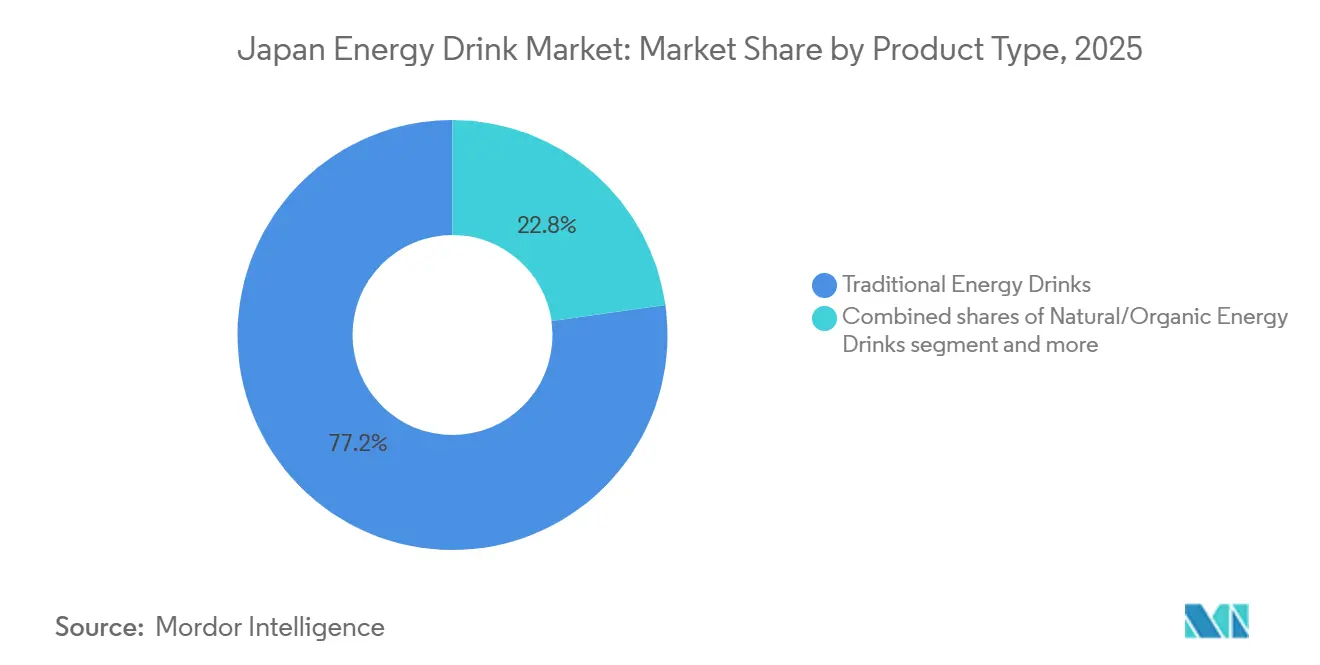

- By product type, traditional energy drinks controlled 77.23% of the Japan energy drinks market share in 2025; natural/organic energy drinks are on course to expand at a 5.56% CAGR to 2031.

- By packaging, PET bottles accounted for 40.22% of the Japan energy drinks market size in 2025, while metal cans are growing at a 5.72% CAGR on the back of a 96.6% aluminium recycling rate.

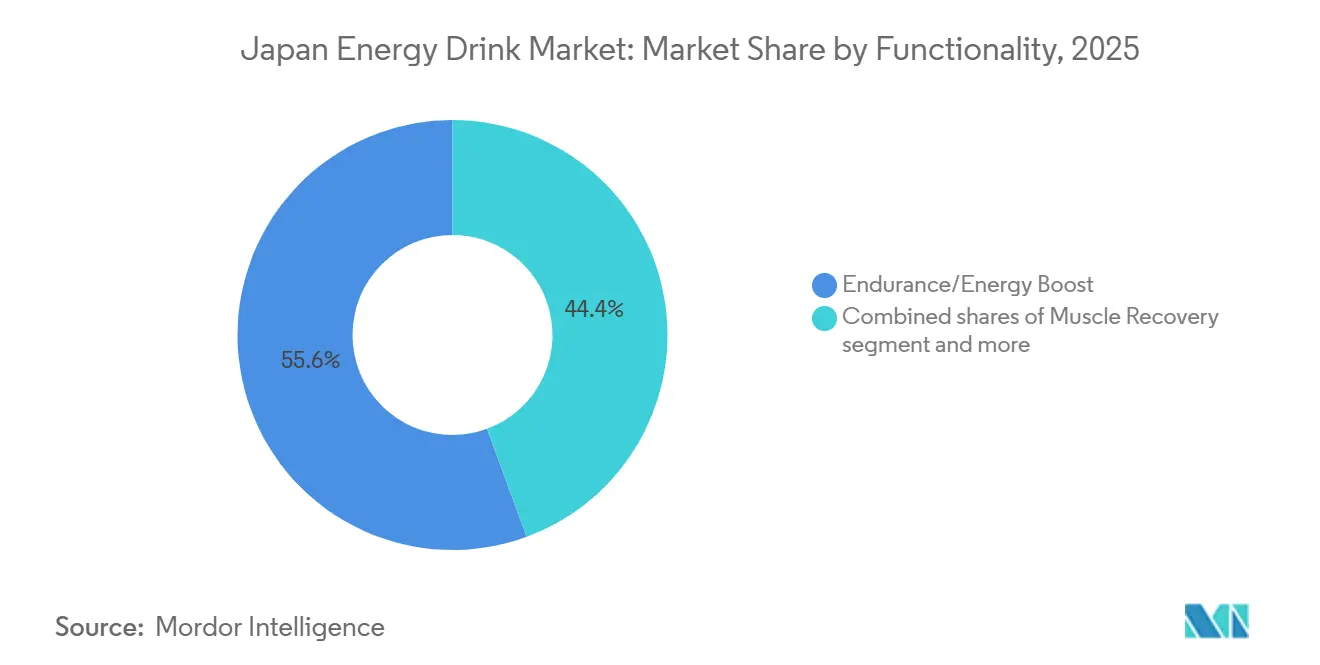

- By functionality, endurance/energy boost held 55.62% revenue share of the Japan energy drinks market size in 2025; muscle recovery is registering the fastest 6.27% CAGR through 2031.

- By distribution channel, retail captured 52.23% of the Japan energy drinks market size in 2025, whereas HoReCa is rising at a 6.08% CAGR as tourism and on-premises dining rebound.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Energy Drink Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and fitness lifestyle influence | +0.8% | National, concentrated in Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Product innovation and flavor diversification expansion | +0.9% | National, with early adoption in urban centers and convenience store chains | Short term (≤ 2 years) |

| Growing e-sports and gaming culture engagement | +0.7% | National, strongest in 13-24 age demographic across major cities | Medium term (2-4 years) |

| Functional beverages with added health benefits | +0.8% | National, aligned with Foods with Function Claims regulatory pathway | Long term (≥ 4 years) |

| Wellness trends encouraging low-sugar formulations | +0.7% | National, driven by health-conscious urban consumers | Medium term (2-4 years) |

| Convenience of ready-to-drink energy beverages | +0.6% | National, leveraging vending machine and convenience store density | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing e-sports and gaming culture engagement

Japan's gaming culture is fuelling energy drink adoption among younger demographics, particularly the 13-24 age cohort that comprises the core e-sports audience. Red Bull's global sponsorship of e-sports teams and tournaments translates into localized activations in Japan, where gaming cafes and LAN centers serve as consumption hubs for carbonated energy drinks. Monster is expanding sports marketing in Japan through baseball sponsorships to recruit new consumers and increase visibility in on-premises channels managed by Asahi. The convergence of gaming marathons and energy drink consumption creates a usage occasion distinct from traditional workplace fatigue relief, enabling brands to segment messaging and SKU development around sustained alertness and reaction-time enhancement.

Product innovation and flavor diversification expansion

Flavor localization and functional ingredient layering are reshaping product portfolios as brands compete for shelf space in Japan's 58,000 convenience stores. Kaneka launched Q10 yogurt drinks in March 2024 under the Foods with Function Claims pathway, targeting brain care and stress reduction, a positioning that overlaps with energy drinks' cognitive-enhancement messaging. Kirin relaunched immune-care beverages fortified with LC-Plasma in March 2024, achieving year-over-year growth and targeting 10 million+ cases in 2023, demonstrating consumer appetite for functional claims beyond caffeine. Craft entrants like Penta CRAFT ENERGY SYRUP differentiate through caffeine-free formulations using medicinal herbs, galangal, hops, and cinnamon, positioning as "next-generation energy drinks" that appeal to wellness-oriented consumers wary of stimulant dependency. Suntory's Dekavita C competes with Coca-Cola Japan's Real Gold, Asahi's Dodekamin, and approximately 25 other vitamin drinks, forcing continuous reformulation to maintain relevance.

Functional beverages with added health benefits

The Foods with Function Claims regulatory pathway, administered by Japan's Consumer Affairs Agency, enables manufacturers to make specific health claims without pre-approval, accelerating time-to-market for functional energy drinks. Japan's functional foods market reached billions in FY2020, with the Foods with Function Claims segment growing at a year-over-year rate, signalling regulatory acceptance of self-substantiated health positioning. Energy claims are the most popular functional benefit, followed by gut health (35% consumer interest), sleep and stress management, creating opportunities for energy drinks to layer amino acids, adaptogens, and vitamins atop caffeine bases. Otsuka's BODYMAINTÉ and Amino-Value exemplify this convergence, blending branched-chain amino acids with electrolytes to target exercise recovery, a positioning that bridges sports nutrition and energy categories. The regulatory framework's flexibility allows rapid iteration, but high caffeine content triggers mandatory warnings ("not recommended for children or pregnant/breastfeeding women"), which can deter health-focused consumers and limit promotional latitude in family-oriented retail environments.

Wellness trends encouraging low-sugar formulations

Sugar-free and low-calorie energy drinks are gaining traction as Japan's labelling regulations define "sugar-free" as ≤0.5 grams per 100 millilitres and "low calorie" as ≤20 kilocalories per 100 millilitres, creating clear thresholds that enable credible health positioning. Erythritol, classified as zero-calorie in Japan, is widely adopted by energy drink manufacturers, with Mitsubishi Chemical promoting its use in functional beverages. Sucralose and acesulfame K are also prevalent, enabling brands to maintain sweetness profiles while meeting regulatory definitions. Suntory's portfolio is majority sugar-free in Japan, reflecting the corporate strategy to align with wellness trends and differentiate from legacy vitamin drinks that contain 15-20 grams of sugar per 120-milliliter bottle. Japan's aging population (30% will be 65+ by 2030) amplifies demand for low-sugar options as diabetes prevalence rises and health-conscious consumption becomes a demographic imperative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative functional beverage categories | -0.5% | National, especially in convenience stores and vending machines | Short term (≤ 2 years) |

| Health concerns over high caffeine content | -0.4% | National, with heightened scrutiny from MHLW and consumer advocacy groups | Medium term (2-4 years) |

| Sugar content deterring health-focused consumers | -0.3% | National, concentrated among aging demographics and wellness-oriented urban consumers | Medium term (2-4 years) |

| Stringent labeling and age restriction policies | -0.3% | National, enforced by MHLW and Consumer Affairs Agency | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over high caffeine content

Caffeine content scrutiny is intensifying as Japan's Ministry of Health, Labour and Welfare mandates warnings on high-caffeine products, requiring labels to state "not recommended for children or pregnant/breastfeeding women". While Japan lacks specific caffeine limits per serving, the warning requirement signals regulatory caution and can deter health-conscious consumers or parents purchasing for adolescents. International precedents, such as proposals to restrict energy drink sales to minors in various jurisdictions, create the risk that Japan could adopt age-verification requirements at retail, which would compress the addressable market and increase compliance costs. Otsuka's Oronamin C contains caffeine but positions as a vitamin drink rather than an energy drink, sidestepping some scrutiny through heritage and pharmaceutical credibility. The regulatory environment creates a two-tier market: pharmaceutical brands with decades-long safety records face less resistance, while imported carbonated energy drinks with 150-200 milligrams of caffeine per can attract consumer advocacy attention and potential future restrictions.

Stringent labelling and age restriction policies

Japan's food labelling framework, governed by the Ministry of Health, Labour and Welfare and the Consumer Affairs Agency, requires comprehensive disclosure of energy, protein, fat, carbohydrates, and sodium content, with specific thresholds for nutrient claims such as "high in vitamin C" (≥12 milligrams per 100 milliliters) [2]Source: Ministry of Health, Labour and Welfare, "Labeling System for Nutrient", mhlw.go.jp. All additives must be designated and approved, and therapeutic claims are prohibited unless products qualify under Foods with Function Claims or Foods for Specified Health Uses pathways. Import requirements mandate notification to MHLW quarantine stations, creating barriers for smaller international brands lacking regulatory expertise. While explicit age restrictions on energy drink sales are not yet enforced, the warning label requirement for high-caffeine products and global momentum toward age-gating sales create compliance uncertainty that could deter investment in youth-targeted marketing or SKU development. The regulatory burden favors incumbents with established compliance infrastructure and distributor relationships, making market entry capital-intensive and time-consuming for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Dominance Faces Natural Disruption

Traditional energy drinks commanded 77.23% market share in 2025, reflecting decades of consumer loyalty to pharmaceutical-heritage brands like Otsuka's Oronamin C (launched in 1965 in 120-milliliter glass bottles fortified with vitamins B2, B6, C, and caffeine) and Taisho's Lipovitan. These vitamin drinks are dispensed through vending machines and convenience stores, leveraging ubiquitous distribution and workplace fatigue-relief positioning. Yet natural/organic energy drinks are projected to grow at a 5.56% CAGR from 2026 to 2031, driven by clean-label demand and craft entrants like Penta CRAFT ENERGY SYRUP, which uses caffeine-free medicinal herbs (galangal, hops, cinnamon) to appeal to wellness-oriented consumers. Sugar-free or low-calorie energy drinks are expanding as Suntory's 60% sugar-free portfolio in Japan demonstrates corporate commitment to wellness trends, while energy shots remain niche due to limited retail acceptance and consumer preference for larger-format beverages that double as hydration.

The traditional segment's resilience stems from pharmaceutical companies' credibility in functional formulation and their control of vending-machine placements, where Coca-Cola Bottlers Japan's 1.2–1.4 million machines and real-time IoT-enabled assortment optimization create switching costs for consumers accustomed to specific SKU availability. Otsuka introduced label-free Oronamin C bottles in July 2021 to reduce plastic waste, and launched the product in Egypt in April 2024, signaling international expansion ambitions. Natural/organic entrants face distribution barriers but benefit from Foods with Function Claims regulatory flexibility, which allows rapid market entry without pre-approval for health claims. Other energy drinks, including carbonated imports like Monster and Red Bull, occupy a premium niche targeting younger, urban consumers willing to pay 200-300 yen per can versus 120-150 yen for traditional vitamin drinks.

By Packaging: Aluminum Cans Gain Sustainability Edge

Metal cans are expanding at a 5.72% CAGR from 2026 to 2031, outpacing PET Bottles' 40.22% market share in 2025, propelled by Japan's aluminum can recycling rate (2021) and horizontal recycling rate, compared to PET's. Suntory and UACJ developed the world's first 100% recycled aluminum can, cutting CO₂ emissions by 60% and deploying it initially in beer products, with energy drink applications likely to follow. Japanese beverage vendors, including Muji and Dydo, are replacing PET bottles with aluminum cans for sustainability and extended shelf life (90-270 days), creating momentum that benefits energy drink brands seeking premium positioning. MA Aluminum operates Japan's largest can recycling plant, ensuring closed-loop supply chains that appeal to environmentally conscious consumers and corporate sustainability mandates.

PET bottles retain the largest share due to vending machine compatibility, consumer preference for resealable formats during commutes, and lower per-unit costs for high-volume pharmaceutical brands. Glass bottles are declining but persist in heritage products like Oronamin C, where the 120-milliliter glass bottle reinforces pharmaceutical credibility and premium perception. Aseptic Packages (Tetra Pak, cartons, pouches) remain marginal in energy drinks due to consumer associations with juice and milk categories, though functional beverage convergence could expand usage. Disposable cups are negligible, limited to on-premises consumption in cafes and HoReCa settings. Kirin invested Yen 10 billion in 100-milliliter PET bottle production for vending machines, targeting immune-care beverages but signalling broader industry commitment to small-format PET for functional drinks.

By Functionality: Muscle Recovery Surges on Sports Nutrition Convergence

Muscle recovery is the fastest-growing functionality subsegment at 6.27% CAGR from 2026 to 2031, driven by sports nutrition convergence and amino acid fortification popularized by Otsuka's Amino-Value (BCAA drink for exercise) and Ajinomoto's aminoVITAL®, which claims the No.1 sports drink position in Japan. This subsegment targets gym-goers, amateur athletes, and aging consumers seeking to maintain muscle mass, positioning energy drinks as post-workout recovery aids rather than pre-activity stimulants. Otsuka's BODYMAINTÉ blends functional ingredients with energy-drink formats, bridging categories and expanding addressable occasions. Endurance/energy boost held 55.62% market share in 2025, reflecting traditional workplace fatigue-relief positioning and caffeine-centric formulations that dominate vending machine and convenience store sales.

The shift toward muscle recovery functionality reflects Japan's aging demographics, 30% of the population will be 65+ by 2030, and rising fitness club memberships among urban professionals. Brands are layering branched-chain amino acids, electrolytes, and protein isolates atop caffeine bases to justify premium pricing and differentiate from legacy vitamin drinks. Other functionalities, including cognitive enhancement and stress reduction, are gaining traction as Kaneka's Q10 yogurt drinks (brain care, stress care) demonstrate consumer willingness to pay for targeted benefits. The Foods with Function Claims pathway enables rapid SKU proliferation, but high caffeine content warnings limit promotional latitude for products targeting older or health-conscious consumers, creating a strategic tension between functional differentiation and regulatory compliance.

By Distribution Channel: HoReCa Rebounds on Tourism and Dining Recovery

HoReCa is advancing at 6.08% CAGR from 2026 to 2031, outpacing retail's 52.23% market share in 2025, as post-pandemic dining recovery and tourism rebound expand on-premises consumption. Monster is leveraging Asahi's distribution network to penetrate supermarkets, e-commerce, and on-premises channels, with sports marketing (baseball sponsorships) driving visibility in restaurants, cafes, and bars. Japan's tourism sector is recovering, with inbound visitors creating demand for premium energy drinks in hotels, airports, and entertainment venues[3]Source: Ministry of Transport, "Inbound Consumption Trend Survey", mlit.go.jp. HoReCa's growth also reflects energy drinks' adoption as cocktail mixers in nightlife settings, expanding usage occasions beyond workplace fatigue relief.

Retail remains the largest channel due to Japan's 58,000 convenience stores and 3.97 million vending machines. Supermarkets/hypermarkets offer broader assortments and promotional opportunities but lack the impulse-purchase convenience of konbini and vending machines. Convenience/grocery stores dominate due to 24/7 accessibility and high foot traffic in urban centers, with 7-Eleven, FamilyMart, and Lawson controlling the majority of the convenience store market. Online retail stores are expanding as Monster emphasizes e-commerce penetration and Coca-Cola Bottlers Japan invests Yen 10 billion in digital marketing and e-commerce infrastructure. Other distribution channels, including drugstores and specialty retailers, remain marginal but offer opportunities for functional energy drinks targeting health-conscious consumers.

Competitive Landscape

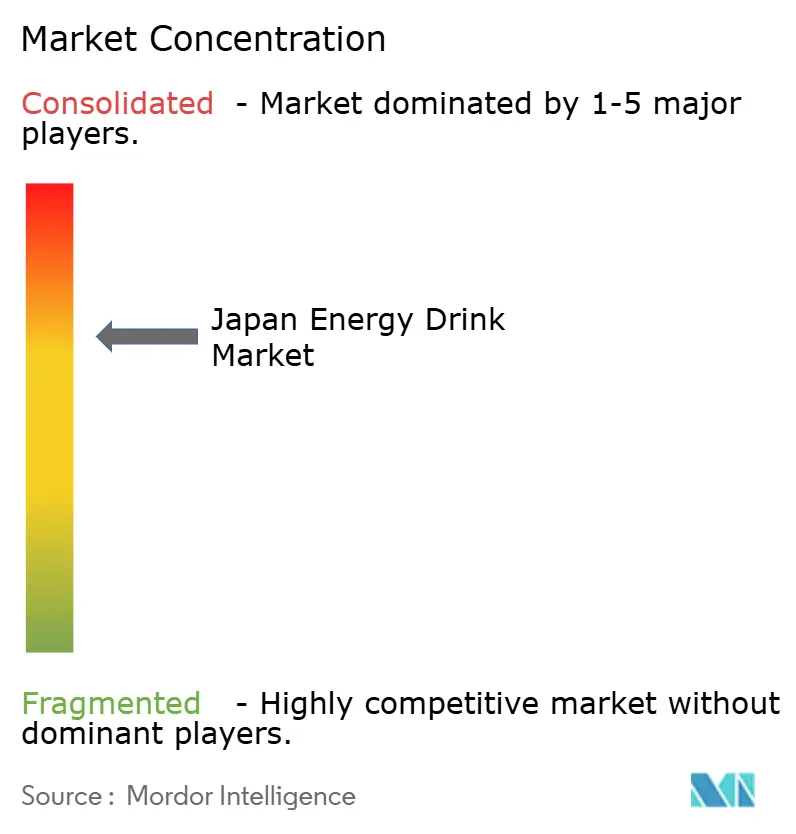

Japan's energy drinks market exhibits a moderate concentration, reflecting the dominance of pharmaceutical incumbents, including Otsuka, Taisho, and Sato, whose decades-old vitamin drink franchises leverage distribution density and consumer trust. In contrast, global energy giants Monster and Red Bull execute localized strategies through exclusive distributor partnerships. Monster's Japan operations, managed by Asahi rather than Coca-Cola, position the brand as the leading energy drink in the Asia-Pacific region, boasting the widest portfolio and the highest market share. Coca-Cola Bottlers Japan's 1.2–1.4 million vending machines and significant share of the non-alcoholic beverage market create a distribution moat that new entrants struggle to breach, as real-time IoT-enabled assortment optimization allows operators to adjust SKU mix by time-of-day and demographic preference.

Strategic patterns include flavor localization (Monster's package and flavor adaptations for Asian markets), functional positioning (Otsuka's BODYMAINTÉ blending amino acids with energy formats), and distribution leverage (Asahi's on-premise reach for Monster, Coca-Cola's vending dominance for its portfolio). White-space opportunities include premium natural segments targeting female consumers (Monster's FLRT launch in March 2026), senior energy solutions addressing aging demographics, and muscle-recovery formulations bridging sports nutrition and energy categories. Emerging disruptors like Penta CRAFT ENERGY SYRUP differentiate through caffeine-free medicinal herb formulations (galangal, hops, cinnamon), sidestepping regulatory scrutiny and appealing to wellness-oriented consumers wary of stimulant dependency.

Technology adoption is reshaping competitive dynamics: Coca-Cola Bottlers Japan's Teradata data warehouse integration with wireless POS from vending machines achieved sales increases, overtime cost reductions, and improvements in machines served per salesperson during pilot deployments, demonstrating how data-driven assortment optimization confers margin advantages. Asahi Group Holdings announced in February 2024 plans to pursue overseas M&A to quadruple Super Dry beer sales, signaling capital allocation toward beverage category expansion that could include energy drink acquisitions or partnerships. The Coca-Cola Company's 2015 strategic partnership with Monster, and transferring its worldwide energy brands (NOS, Full Throttle, Burn, Mother) to Monster, consolidated global distribution and positioned Coca-Cola as Monster's preferred global distributor, a framework that could enable expanded Monster brand distribution into Japan via Coca-Cola's bottling system, though Japan operations remain with Asahi.

Japan Energy Drink Industry Leaders

-

The Coca-Cola Company

-

Red Bull GmbH

-

Monster Energy

-

PepsiCo

-

Suntory Beverage & Food Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Monster Energy introduced a new non-caffeine variant called “Monster Energy Can 250ml for Business Use” in Japan, intended for restaurants and foodservice as a mixer rather than general retail. This represents a strategic expansion into niche product formats and settings beyond typical convenience store channels.

- November 2024: Red Bull Japan collaborated with ski jumper Ryo Kobayashi to release a special design, limited-edition can celebrating his world record achievement. This product was launched through select distribution channels in Japan and targeted collectors and brand enthusiasts.

- July 2024: Monster launched its “Ultra Series” zero-sugar energy drink lineup in Japan, focusing on health-conscious consumers with sugar-free options, expanding product diversity in the sugar-free/low-calorie segment.

Japan Energy Drink Market Report Scope

Energy drinks contain stimulant compounds, usually caffeine, which provide physical and mental stimulation. The Japanese energy drink market is segmented by product type, packaging, functionality, and distribution channels. By type, the market is segmented into traditional energy drinks, energy shots, and more. By functionality, the market is segmented into muscle recovery and more. By packaging, the market is segmented into bottles and cans, and more. By distribution channel, the market is segmented into Horeca and retail. The market forecasts are provided in terms of value (USD) and Volume (Litres)

Product Type

| Traditional Energy Drinks |

| Sugar-free or Low-calories Energy Drinks |

| Natural/Organic Energy Drinks |

| Energy Shots |

| Other Energy Drinks |

Packaging

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic packages |

| Disposable Cups |

Functionality

| Endurance/Energy Boost |

| Muscle Recovery |

| Others |

Distribution Channel

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| Product Type | Traditional Energy Drinks | |

| Sugar-free or Low-calories Energy Drinks | ||

| Natural/Organic Energy Drinks | ||

| Energy Shots | ||

| Other Energy Drinks | ||

| Packaging | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic packages | ||

| Disposable Cups | ||

| Functionality | Endurance/Energy Boost | |

| Muscle Recovery | ||

| Others | ||

| Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the current value of the Japan energy drinks market?

The market is worth USD 3.58 billion in 2026, placing it among the largest energy drink markets in the country.

How fast will sales grow in coming years?

Revenue is forecast to rise at a 5.44% CAGR, lifting value to USD 4.67 billion by 2031.

Which product segment is expanding most rapidly?

Natural and organic drinks are recording the quickest gains at a 5.56% CAGR, reflecting stronger demand for clean labels.

Page last updated on: