Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

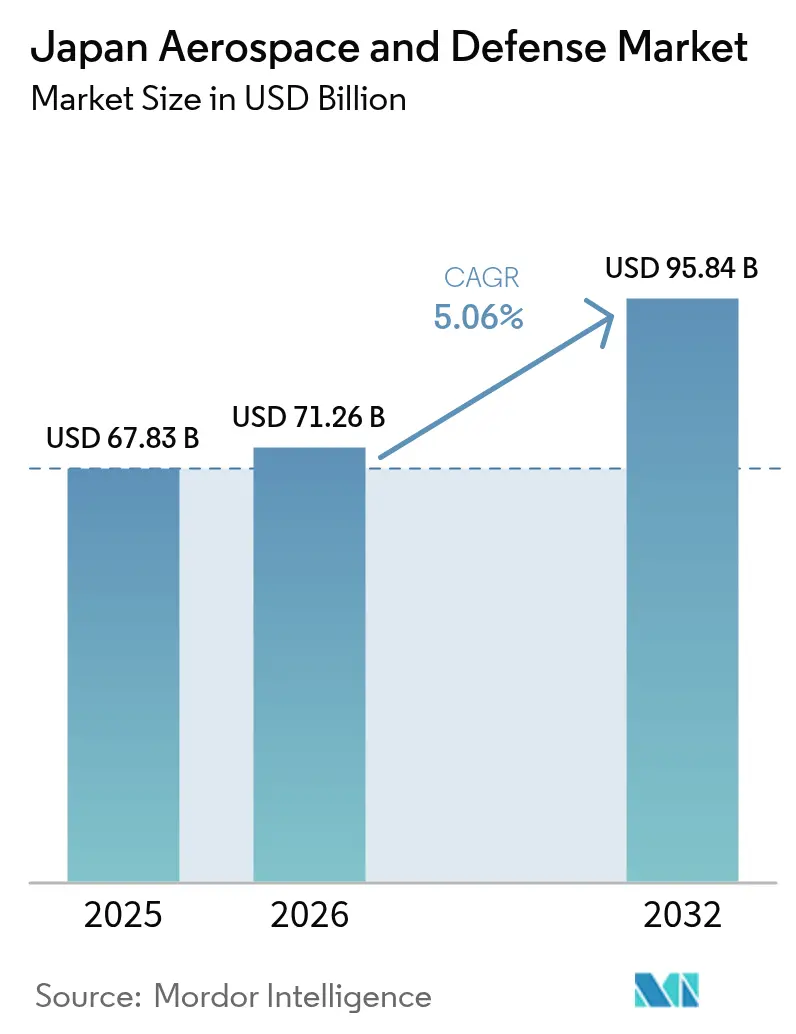

| Base Year Market Size (2025) | USD 67.83 Billion |

| Market Size (2026) | USD 71.26 Billion |

| Market Size (2032) | USD 95.84 Billion |

| Growth Rate (2026 - 2032) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Aerospace And Defense Market Analysis by Mordor Intelligence

Japan aerospace and defense market size in 2026 is estimated at USD 71.26 billion, growing from 2025 value of USD 67.83 billion with 2032 projections showing USD 95.84 billion, growing at 5.06% CAGR over 2026-2032. Tokyo’s multi-year plan to lift defense outlays to 2% of gross domestic product, combined with a rebound in commercial flight activity, underpins the expansion. Rising orders for wide-body aircraft, accelerated delivery schedules for F-35 fighters, and new work on the Global Combat Air Programme (GCAP) broaden the industrial base. Simultaneously, tax measures that take effect in 2026 help secure predictable funding for missile, cyber, and space programs, while joint sustainment frameworks with the US drive incremental maintenance revenue. EW upgrades and sensor procurements pass critical design reviews, creating pull-through demand for domestic semiconductor and composite suppliers. Moderate market concentration persists because Japanese primes rely on US and European design authority for engines and mission systems, even as local content rules channel 60% of spending to in-country vendors.

Key Report Takeaways

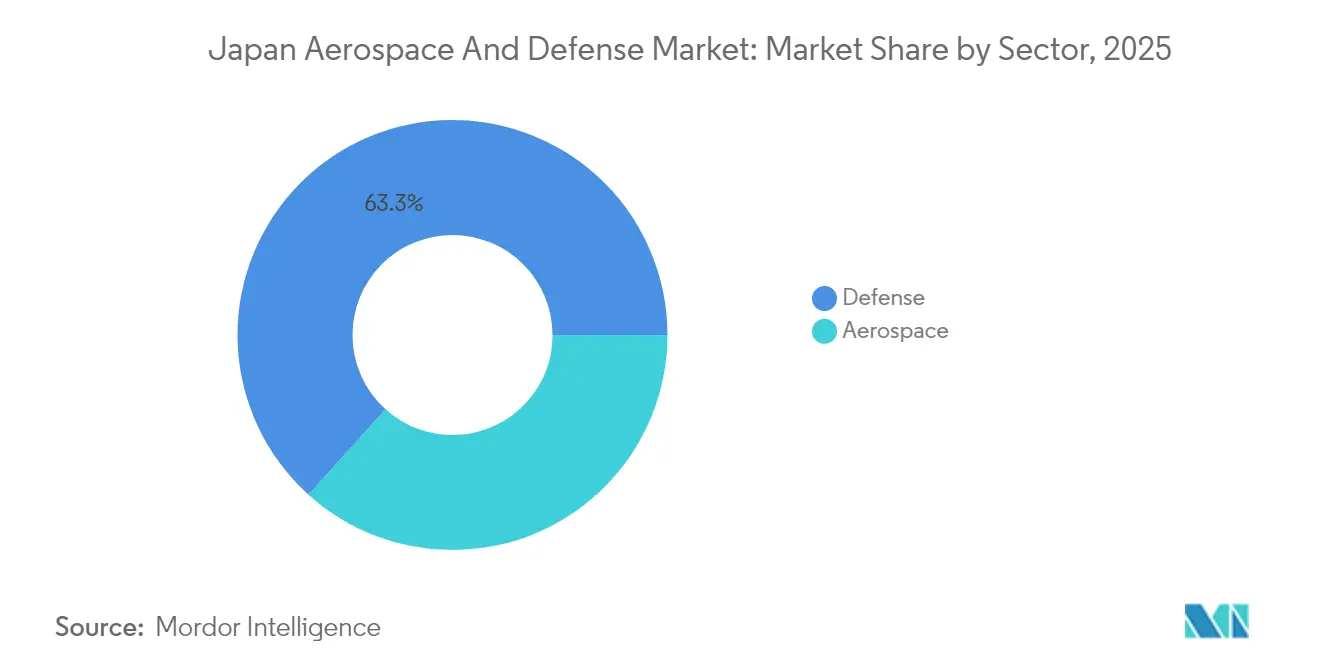

- By sector, defense contributed 63.32% of 2025 revenue, whereas aerospace is projected to record the fastest expansion at a 5.52% CAGR to 2032.

- By platform, aerial systems generated 34.21% of 2025 sales and are poised to advance at a 5.31% CAGR through 2032.

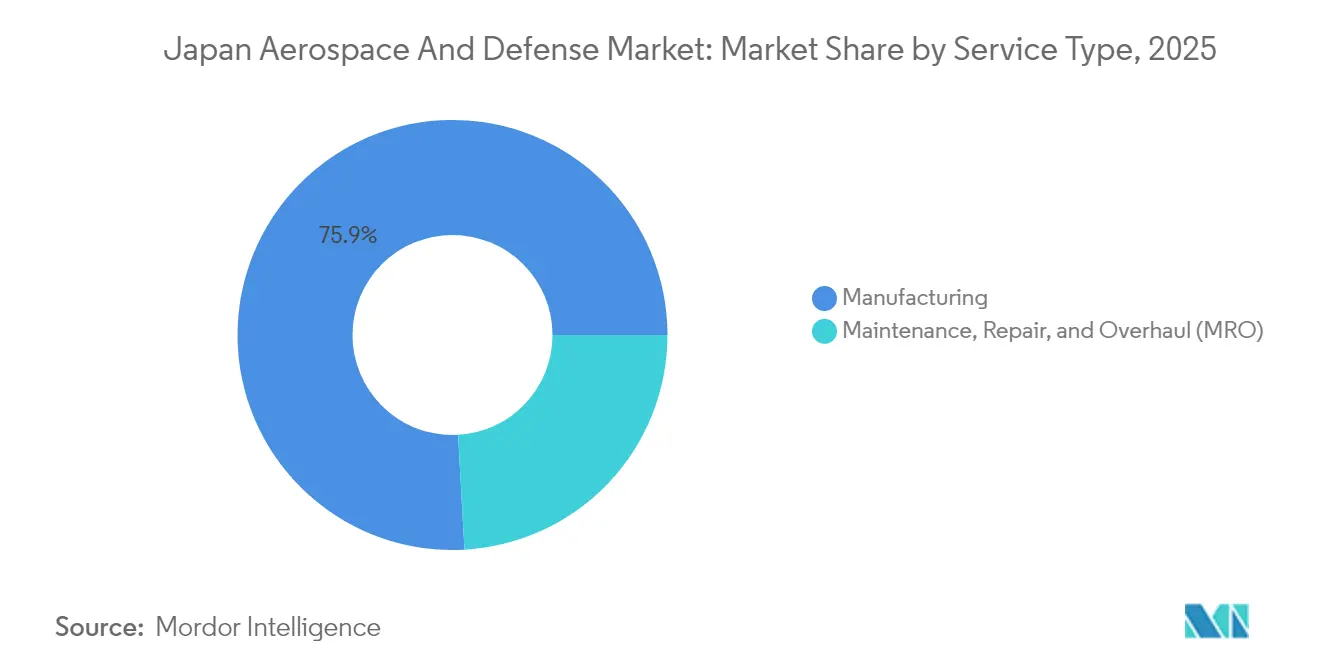

- By service type, manufacturing accounted for 75.89% of 2025 revenue, while MRO is expected to grow at a 7.06% CAGR over the forecast horizon.

- By component, airframes and structures captured 24.41% of 2025 revenue, whereas EW and sensors are forecasted to grow at a 6.12% CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense spending aligned with the 2% of GDP target | +1.2% | National | Medium term (2-4 years) |

| Expansion of next-generation fighter aircraft and combat aviation programmes | +0.9% | National, spillover to United Kingdom and Italy | Long term (≥ 4 years) |

| Post-pandemic recovery in commercial aviation MRO demand | +0.7% | National, regional APAC connectivity | Short term (≤ 2 years) |

| Government incentives for indigenous missile and hypersonic system development | +0.6% | National | Medium term (2-4 years) |

| Transition toward domestic MRO hubs under the US-Japan forward sustainment strategy | +0.5% | National, benefits for US Pacific Fleet | Medium term (2-4 years) |

| Build-out of defense satellite constellations supporting surveillance and targeting | +0.4% | National, regional data sharing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Spending Aligned With the 2% of GDP Target

The FY 2025 defense budget reached JPY 8.7 trillion (USD 56 billion), marking a 7.2% year-on-year increase and positioning the plan on a glide path to achieve the 2% of GDP objective by FY 2027. Tax hikes that take effect in 2026 provide a recurring revenue stream, enabling multi-year missile, cyber-defense, and space projects. Funding priorities shift toward stand-off munitions and network-centric systems, prompting new orders for electronic-warfare suites, data-link terminals, and low-latency satellite links. The December 2024 US-Japan Extended Deterrence Guidelines institutionalize joint contingency planning, which raises interoperability standards and accelerates the procurement of common encrypted communication equipment. These dynamics enlarge the Japan aerospace and defense market by opening budget headroom for both acquisition and sustainment.

Expansion of Next-Generation Fighter Aircraft and Combat Aviation Programs

GCAP launched a trilateral government organization in December 2023 to field a sixth-generation fighter by 2035, with Mitsubishi Heavy Industries leading domestic workshare.[1]“GCAP Fighter Program,” Financial Times, ft.com Revised export rules issued in March 2024 permit the aircraft to be sold to third countries, a move intended to increase production volume and reduce unit cost. Parallel F-35A and F-35B deliveries continue, expanding aerial deterrence while mitigating risks to the GCAP schedule. However, engineering resources are stretched as the same teams juggle F-35 final assembly, F-2 upgrades, and early F-3 prototyping. The workstream fuels subsystem orders for advanced sensors, composite wings, and next-generation turbofans, lifting the Japan aerospace and defense market during the development phase and into serial production.

Post-Pandemic Recovery in Commercial Aviation MRO Demand

Japan Airlines and ANA Holdings placed combined orders for 154 widebody jets, worth more than USD 20 billion, in 2024-2025, signaling renewed confidence in passenger and cargo demand. Legacy hangars that were downsized during the pandemic now confront 12-month engine-overhaul backlogs, driving carriers to expand domestic maintenance capacity. In August 2024, JAL and Mitsubishi Heavy Industries signed a memorandum of understanding aimed at implementing predictive analytics to reduce unscheduled engine removals by 20%.[2] “Type 12 Missile Range Extension,” Nikkei Asia, asia.nikkei.com These moves boost MRO revenue, thereby lifting the share of high-margin services within the Japan aerospace and defense market.

Government Incentives for Indigenous Missile and Hypersonic Development

Mitsubishi Heavy Industries has received contracts to extend the range of the Type 12 Surface-to-Ship Missile beyond 1,000 kilometers, with initial deliveries scheduled between fiscal years 2024 and 2026. Budget earmarks also back the Hyper Velocity Gliding Projectile, where IHI provides scramjet propulsion. Dedicated funding and streamlined acquisition processes shorten lead times; however, limited domestic test infrastructure necessitates partnering with allied ranges, which slows iteration cycles. Nonetheless, program spending enlarges the sensor, propulsion, and guidance subsectors within the Japan aerospace and defense market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent export-control policies limiting production scale and market expansion | -0.4% | National, export markets in APAC and Middle East | Long term (≥ 4 years) |

| Advanced manufacturing talent shortages and supply chain bottlenecks | -0.5% | National | Medium term (2-4 years) |

| Increasing cybersecurity and regulatory compliance costs for defense SMEs | -0.3% | National | Short term (≤ 2 years) |

| Dependence on foreign intellectual property and licensing for core defense platforms | -0.4% | National, ties to US and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Export-Control Policies Limiting Production Scale and Market Expansion

Revised export rules permit the sale of co-developed systems only with unanimous partner approval, introducing a veto risk that curbs production runs and keeps unit costs high. Without foreign orders, the F-3 program would be able to build fewer than 100 airframes, which would undermine economies of scale. Domestic primes continue to lobby for additional liberalization, but public opinion remains cautious about arms exports, constraining the near-term upside for the Japan aerospace and defense market.

Advanced Manufacturing Talent Shortages and Supply Chain Bottlenecks

The average age of engineers at leading primes approaches 50, while universities graduate fewer aerospace majors each year.[3]“Defense Industry IP Licensing Challenges,” Nikkei Asia, asia.nikkei.com Semiconductor availability remains tight, delaying avionics integration, and rare-earth magnet supply chains remain vulnerable to geopolitical shocks. These constraints heighten program risk and temper potential growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Defense Anchors Revenue, Aerospace Accelerates

Defense secured 63.32% of 2025 revenue, reflecting sustained Type 12 missile, F-35, and frigate procurement, while aerospace is projected to grow at a 5.52% CAGR through 2032. The Japan aerospace and defense market relies on defense for scale but turns to commercial aviation for momentum. Japan Airlines and ANA Holdings added 154 wide bodies in 2024-2025, pushing engine and landing gear suppliers to full capacity. Meanwhile, the GCAP fighter injects high-tech workshare, and unmanned systems gain budget priority for island defense.

Commercial recovery also draws global maintenance traffic to domestic hangars, reinforcing service revenue. The government’s mandate that 60% of defense contract value flow to local suppliers nurtures small electronics and composite firms; however, the cap on export volumes restrains aggregate sector growth. Continued liberalization and timely technology transfers will determine whether aerospace achieves parity with defense in the Japan aerospace and defense market by the early 2030s.

By Platform: Aerial Dominance Drives Dual-Use Growth

Aerial platforms generated 34.21% of 2025 revenue and are expected to rise at a 5.31% CAGR, positioning them at the center of future expansion. Fixed-wing programs encompass commercial narrowbody aircraft, F-35 fighters, and P-1 patrol aircraft. Rotary-wing production remains modest but steady, while unmanned aerial systems receive record allocations worth JPY 50 billion (USD 320 million) in FY 2025. The Japan aerospace and defense market size for aerial unmanned assets is projected to widen once GCAP avionics and autonomy modules mature.

Terrestrial systems emphasize 8×8 wheeled vehicles and 155mm howitzers optimized for island maneuvering, whereas naval platforms target frigates and submarines fitted with lithium-ion batteries for extended, silent patrols. All three domains converge on sensor fusion, EW, and secure data links, prompting cross-domain component commonality that lowers sustainment cost and strengthens the Japan aerospace and defense market.

By Service Type: MRO Surge Outpaces Manufacturing

Manufacturing accounted for 75.89% of 2025 service revenue; however, MRO is expected to outstrip it at a 7.06% CAGR as the fleet expands and ages. Carriers are adopting digital twins to predict part fatigue, and a bilateral sustainment plan could add US Navy destroyer work worth up to USD 1 billion annually by 2028. The Japan aerospace and defense market share for MRO is set to climb as new hangars open in Nagoya and Kobe.

Manufacturing still enjoys a robust backlog, led by F-35 final assembly, Mogami-class frigates, and Type 12 missiles; however, small batch sizes elevate unit costs. GCAP exports, if realized, could deliver the scale required for competitive pricing and keep assembly lines running past 2035. In the interim, service revenue narrows the gap and diversifies cash flow across the Japan aerospace and defense market.

By Component: Electronic Warfare Ascends as Airframes Mature

Airframes and structures accounted for 24.41% of 2025 revenue, while electronic warfare and sensors are expected to carry the highest growth outlook at a 6.12% CAGR. Mitsubishi Electric exported its FPS-3ME AESA radar to the Philippines in March 2024, marking Japan’s first radar export under the eased transfer rules. Northrop Grumman and Mitsubishi Electric signed a July 2024 pact to co-develop EW suites and unmanned underwater vehicles (UUVs), pairing US algorithm expertise with Japanese manufacturing precision.

Propulsion work progresses on IHI’s XF9-1 engine, which achieved thrust-to-weight ratios above 15:1 in bench tests. Composite supplier Toray received a supplier award in April 2024 for its T1100G carbon fiber, which enables 15-20% weight savings in the airframe. This component mix positions Japan to capture value from advanced materials, even as traditional airframe demand plateaus, thereby expanding the high-tech tier of the Japan aerospace and defense market.

Geography Analysis

Japan’s island geography and proximity to China and North Korea shape procurement priorities, sustaining a 5.06% CAGR through 2032. The southwestern Nansei Islands strategy funds mobile missile batteries, Li-ion submarines, and unmanned surveillance assets to deter amphibious threats. The Type 16 Maneuver Combat Vehicle airlifts aboard C-2 transports, and stand-off Type 12 missiles reach 1,000 kilometers, extending deterrent coverage. Space-based intelligence increases responsiveness, while Link 16 upgrades ensure data continuity across services, reinforcing growth in the Japan aerospace and defense market.

Inbound tourism exceeded 30 million visitors in 2024, propelling commercial fleet expansion and straining engine-overhaul facilities. Predictive-maintenance collaborations between airlines and primes aim to reduce aircraft-on-ground events, expand domestic service networks, and generate jobs in Nagoya and Tokyo. Interest from the US Navy in stationing a destroyer maintenance facility in Japanese shipyards would increase industrial demand, contingent upon liability agreements and security clearances. These developments expand regional MRO clusters within the Japan aerospace and defense market.

Policy remains a critical variable. Export-control revisions unlock potential GCAP exports but require unanimous approval from partners, limiting near-term upside. The Economic Security Promotion Act raises compliance overhead for small suppliers, consolidating the vendor base and pushing procurement toward accredited mid-tier firms. Balancing autonomy and alliance needs defines the trajectory for future platform integration and shapes regional demand inside the Japan aerospace and defense market.

Competitive Landscape

Market concentration remains moderate. Mitsubishi Heavy Industries, Ltd., Kawasaki Heavy Industries, Ltd., and Subaru Corporation dominate airframe and propulsion work, yet rely on Lockheed Martin Corporation, The Boeing Company, BAE Systems plc, and Northrop Grumman Corporation for design authority on high-profile programs. Revised export rules aim to amortize unit costs through third-country sales, although US technology-release approvals still govern the export of critical software, coatings, and engine materials.

Second-tier players, such as NEC Corporation, Fujitsu, Hitachi, and Toshiba, leverage their strengths in commercial electronics to supply data-link terminals and cybersecurity solutions. Joint ventures address technology gaps: the July 2024 Northrop–Mitsubishi Electric pact targets shared EW product lines for Southeast Asian customers, and Toray’s award positions it as a composite material leader. Meanwhile, the US-Japan sustainment initiative presents new revenue opportunities for shipyard operators, thereby enhancing service capabilities across the Japan aerospace and defense market.

White-space opportunities lie in autonomous systems, advanced sensors, and space-based networks. Domestic suppliers trail foreign rivals in autonomy algorithms and cognitive EW, creating scope for licensing deals. Firms that integrate satellite imagery, electronic order-of-battle data, and missile tracking into a seamless kill chain will capture outsize value in the fastest-growing electronic warfare and sensor segment of the Japan aerospace and defense market.

Japan Aerospace And Defense Industry Leaders

Mitsubishi Heavy Industries, Ltd.

Kawasaki Heavy Industries, Ltd.

ShinMaywa Industries, Ltd.

Toshiba Corporation

IHI AEROSPACE Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Kongsberg Defence & Aerospace signed a fifth follow-on contract with Japan to supply the Joint Strike Missile (JSM) for its F-35A fighter aircraft fleet.

- April 2025: Japan awarded Mitsubishi Heavy Industries a USD 216 million contract to develop advanced long-range, precision-guided missiles, supporting its military modernization program to address increasing regional security challenges in East Asia.

- July 2024: Japan Airlines signed a firm order with Airbus for 20 A350-900 widebody aircraft and 11 single-aisle A321neo aircraft.

Japan Aerospace And Defense Market Report Scope

The study examines Japan's national defense budget, its defense acquisition regulatory environment, and the production capabilities of market players in the country, providing a broader basis for assessing past and future trends in Japanese defense policies and capabilities. The study incorporates data-driven assessments to offer critical insights and opportunities in the Japanese aerospace and defense industry.

The Japan aerospace and defense market is segmented based on sector, platform, service type, and component. By sector, the market is segmented into aerospace and defense. By platform, the market is classified into airborne, terrestrial, and naval. By service type, the market is segmented into manufacturing and maintenance, repair, and overhaul (MRO). By component, the market is segmented into airframes and structures, propulsion systems and engines, electronics and mission systems, composite materials and carbon fibre, and electronic warfare (EW) and sensors. For each segment, the market size is provided in terms of value (USD).

By Sector

| Aerospace | Civil Aerospace |

| Military Aerospace | |

| Defense | Land Systems |

| Naval Systems | |

| Air Combat Systems |

By Platform

| Aerial | Fixed Wing Aircraft |

| Rotary Wing Aircraft | |

| Unmanned Aerial Systems | |

| Terrestrial | Armored Vehicles |

| Artillery and Missile Systems | |

| Soldier Systems and Electronics | |

| Naval | Surface Combatants |

| Submarines | |

| Naval Aviation | |

| Space | Navigation Satellites |

| Earth Observation/Remote Sensing Satellites | |

| Scientific Research/Astronomical Satellites | |

| Communication Satellites |

By Service Type

| Manufacturing |

| Maintenance, Repair, and Overhaul (MRO) |

By Component

| Airframes and Structures |

| Propulsion Systems and Engines |

| Electronics and Mission Systems |

| Composite Materials and Carbon Fibre |

| Electronic Warfare (EW) and Sensors |

| By Sector | Aerospace | Civil Aerospace |

| Military Aerospace | ||

| Defense | Land Systems | |

| Naval Systems | ||

| Air Combat Systems | ||

| By Platform | Aerial | Fixed Wing Aircraft |

| Rotary Wing Aircraft | ||

| Unmanned Aerial Systems | ||

| Terrestrial | Armored Vehicles | |

| Artillery and Missile Systems | ||

| Soldier Systems and Electronics | ||

| Naval | Surface Combatants | |

| Submarines | ||

| Naval Aviation | ||

| Space | Navigation Satellites | |

| Earth Observation/Remote Sensing Satellites | ||

| Scientific Research/Astronomical Satellites | ||

| Communication Satellites | ||

| By Service Type | Manufacturing | |

| Maintenance, Repair, and Overhaul (MRO) | ||

| By Component | Airframes and Structures | |

| Propulsion Systems and Engines | ||

| Electronics and Mission Systems | ||

| Composite Materials and Carbon Fibre | ||

| Electronic Warfare (EW) and Sensors | ||

Key Questions Answered in the Report

What is the 2026 valuation of the Japan aerospace and defense market?

The Japan aerospace and defense market size is USD 71.26 billion in 2026.

How fast is the market expected to grow through 2032?

It is projected to expand at a 5.06% CAGR, reaching USD 95.84 billion by 2032.

Which segment shows the highest growth rate?

Maintenance, repair, and overhaul (MRO) is forecasted to grow at a 7.06% CAGR through 2032, outpacing manufacturing.

What share did defense contribute in 2025?

Defense accounted for 63.32% of sector revenue in 2025.

Which component category is advancing the fastest?

EW and sensors are growing at a 6.12% CAGR through 2032.

How many widebody aircraft did Japanese carriers order recently?

Japan Airlines and ANA Holdings ordered a combined 154 widebody jets in 2024-2025.

Page last updated on: