IVF Devices And Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

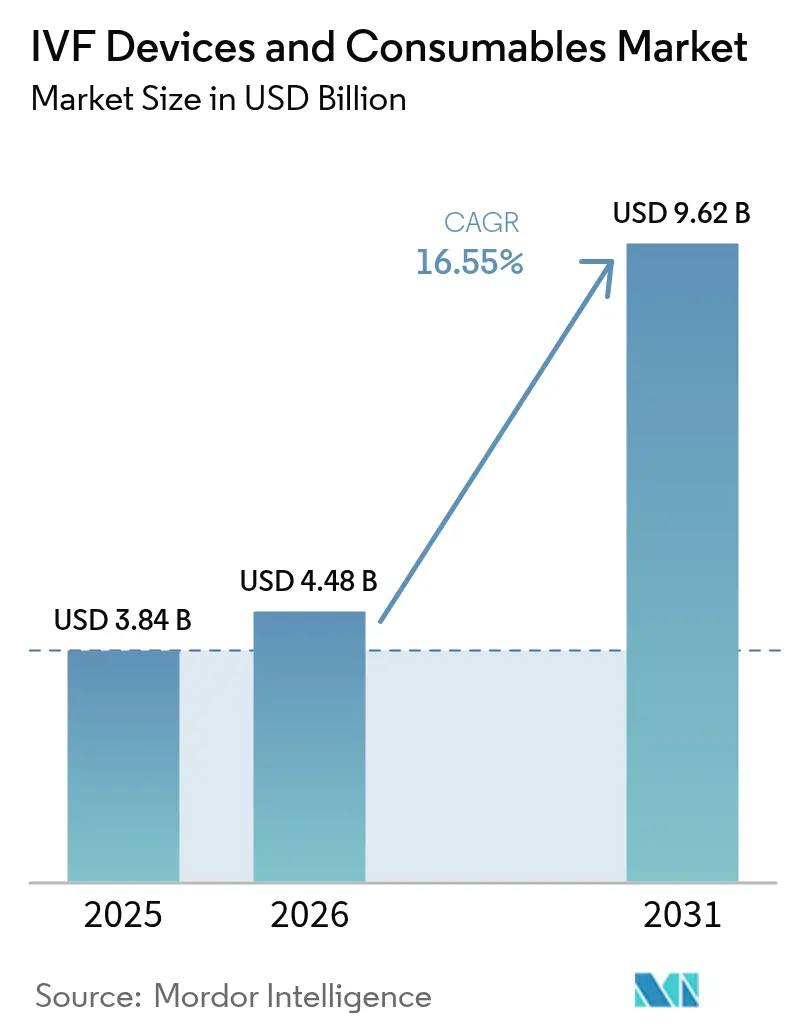

| Market Size (2026) | USD 4.48 Billion |

| Market Size (2031) | USD 9.62 Billion |

| Growth Rate (2026 - 2031) | 16.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IVF Devices And Consumables Market Analysis by Mordor Intelligence

The IVF devices and consumables market size was valued at USD 3.84 billion in 2025 and estimated to grow from USD 4.48 billion in 2026 to reach USD 9.62 billion by 2031, at a CAGR of 16.55% during the forecast period (2026-2031). The expansion reflects a steady climb in clinically diagnosed infertility, wider reimbursement mandates, and rapid gains in laboratory automation that lower cycle times and raise success rates. Female infertility prevalence has risen 84% since 1990, with the greatest burden in the 35-to-39 age group, while AI-supported embryo grading increases implantation precision and reduces multiple pregnancies[1]Xiaoming Vicky Lu et al., “Global female infertility prevalence,” nature.com. Private equity capital exceeding USD 875 million in 2024 accelerated consolidation, allowing manufacturers to bundle instruments, media, and analytics into turnkey solutions. Policy tailwinds add further momentum as large group health plans in California must fund up to three IVF cycles starting July 2025, expanding coverage to 9 million residents.

Key Report Takeaways

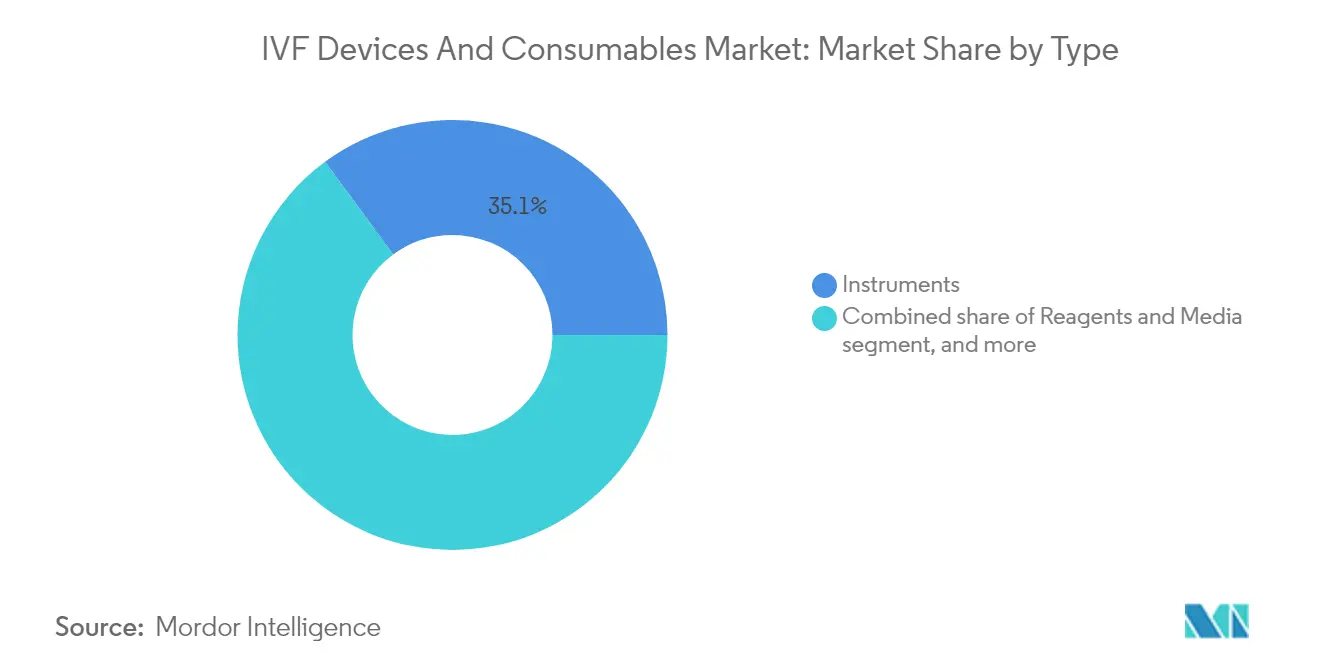

- By type, instruments led with 35.10% of the IVF devices and consumables market share in 2025, while reagents and media are forecast to rise at an 18.25% CAGR to 2031.

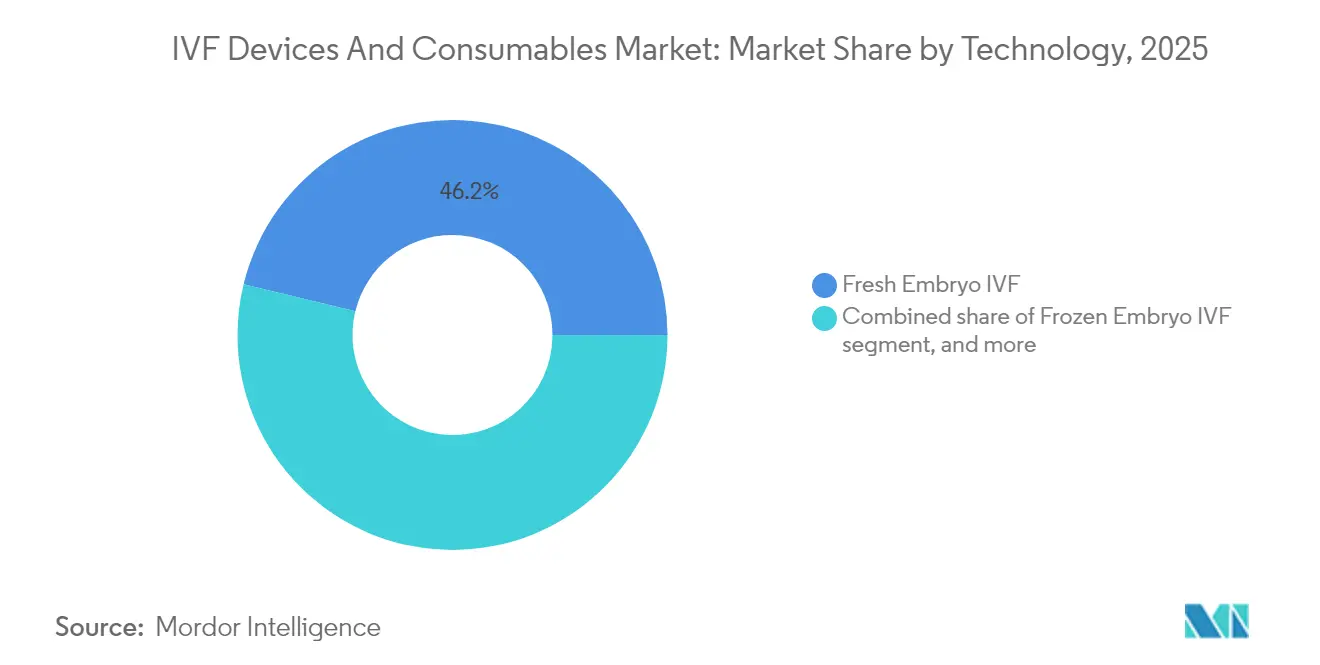

- By technology, fresh embryo IVF held 46.20% revenue share in 2025 and frozen embryo IVF is projected to grow at a 18.70% CAGR through 2031.

- By end user, fertility clinics accounted for 57.95% of the IVF devices and consumables market size in 2025; cryobanks and genetic laboratories are advancing at a 19.20% CAGR from 2026-2031.

- By geography, North America dominated with 42.80% share of the IVF devices and consumables market in 2025, whereas Asia-Pacific is expanding at 17.30% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IVF Devices And Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global infertility prevalence | +3.2% | Global; most pronounced in Asia-Pacific and North America | Long term (≥ 4 years) |

| Delayed parenthood and higher maternal age | +2.8% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Technological advancements in IVF devices and media | +4.1% | Global; led by North America and Europe | Medium term (2-4 years) |

| Expanding insurance coverage and government support | +3.5% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Growth of cross-border fertility tourism | +1.8% | Asia-Pacific, Europe, Middle East | Short term (≤ 2 years) |

| Increasing success rates via AI and genetic screening | +2.9% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Infertility Prevalence

The World Health Organization observes that 1 in 6 individuals face infertility at some point in life, a burden worsened by sexually transmitted infections and post-partum complications in low socio-demographic regions. Age-standardized infertility rates continue climbing even where absolute case counts stabilize, sustaining long-run demand for assisted reproduction. Asia-Pacific records notable growth in secondary infertility as lifestyle-related polycystic ovary syndrome gains prevalence. As natural conception declines, clinics invest in high-throughput intracytoplasmic sperm injection (ICSI) workstations and time-lapse incubators to meet rising caseloads. These conditions underpin a substantial portion of the expected CAGR in the IVF devices and consumables market.

Technological Advances in IVF Devices and Media

Laboratory automation marks the single largest efficiency leap in two decades. Conceivable Life Sciences achieved the first robot-controlled ICSI birth, demonstrating that a fully automated chain can complete 23 procedural steps without human intervention. AI-guided embryo classifiers reach 70-80% accuracy on ploidy prediction, letting clinics reduce invasive biopsies while improving implantation odds[2]NewYork-Presbyterian, “AI embryo selection platforms,” nyp.org. Microfluidic vitrification chips now yield 86% oocyte survival, surpassing manual methods and lowering the per-cycle cost baseline. Continuous imaging incubators integrate analytics dashboards, allowing embryologists to review developmental trajectories remotely. These developments collectively add more than four percentage points to the forecast CAGR.

Expanding Insurance Coverage and Government Support

Legislators are widening reimbursement scope to alleviate the financial load of a typical USD 20,000 cycle. California’s SB-729 compels large plans to cover up to three oocyte retrievals plus unlimited embryo transfers, creating predictable demand curves for clinics and vendors[3]California Legislature, “SB-729 text,” leginfo.legislature.ca.gov. The U.S. Department of Veterans Affairs expanded benefits to include unmarried veterans and donor gametes, a policy that aligns federal employee health benefit plans toward richer fertility coverage. Outside North America, Australia and Singapore maintain partial public funding, while Malaysia cultivates fertility tourism through accredited centers. Such measures reduce out-of-pocket barriers and accelerate equipment refresh cycles, directly boosting the IVF devices and consumables market.

Growth of Cross-Border Fertility Tourism

Price differentials between mature and emerging markets now exceed 300%, motivating patient travel. Procedures that cost USD 10,200 in Singapore can be completed for USD 2,700 in India, even after adding travel and lodging. Regional hubs streamline entry visas and bundle medical services, stimulating local demand for laboratory gear and consumables. Quality accreditation schemes spread best-practice standards, encouraging technology transfer from Western vendors to Asian clinics. The resulting network effects lift consumables turnover and widen distribution footprints for global suppliers.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | -2.7% | Global; most severe in emerging markets | Long term (≥ 4 years) |

| Ethical and regulatory complexities | N/A | Global; varies by jurisdiction | Medium term (2-4 years) |

| Variable success rates and emotional burden | N/A | Global | Short to medium term (≤ 4 years) |

| Supply-chain constraints for specialized consumables | -1.9% | Global; acute in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Costs

Single-cycle outlays range from USD 15,000-30,000 in developed markets, pushing many couples to attempt multiple rounds that can exceed USD 60,000. Public funding shortfalls worsen access; National Health Service support in the United Kingdom fell to 27% of treatments in 2022. Financing programs from specialist lenders emerge, yet interest rate premiums inflate the final expense, extending repayment well beyond the birth event. Capital equipment such as time-lapse incubators or integrated micromanipulation systems carry price tags in the mid-six-figure range, slowing adoption in mid-tier clinics. Rising medication prices compound the burden, narrowing the eligible patient pool and trimming potential unit volumes in the IVF devices and consumables market.

Supply-Chain Constraints for Specialized Consumables

The U.S. Food and Drug Administration continues listing shortages for culture media, cryo-straws, and pipettes that meet stringent sterility and toxicity standards. Global healthcare systems absorb USD 359 million in extra labor costs and USD 200 million in therapy substitutions each year because of these disruptions. Tariff regimes on imported plastics and electronics elevate landed costs, particularly in Asia-Pacific markets reliant on overseas suppliers. Regulatory certification bottlenecks further delay alternative sourcing, compelling clinics to prolong reorder cycles and hold higher safety stock. While larger chains diversify vendors to hedge risk, smaller facilities face procedure postponements, cutting into consumable throughput and dampening short-term CAGR prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Instruments Anchor Revenue While Media Accelerate Growth

Instruments generated 35.10% of 2025 revenue, confirming their role as the backbone of embryology laboratories. Demand concentrates on incubators with integrated cameras, micromanipulators capable of sub-micron accuracy, and automated vitrification systems that standardize workflows and reduce operator variability. Robotic ICSI platforms improve precision while lowering training curves, encouraging new entrants to build capacity quickly. Continuous usage of these capital assets also drives steady aftermarket sales for calibration tools and single-use tips, expanding the serviceable portion of the IVF devices and consumables market. Clinics frequently align capital budgets with reimbursement schedules, creating multiyear replacement cycles that suppliers can forecast with confidence.

Reagents and culture media form the fastest-growing line, advancing at an 18.25% CAGR through 2031. Growth stems from specialized formulations optimized for extended culture to day-5 blastocyst stage and for AI-assisted imaging compatibility. Cryopreservation media leverage non-permeating cryoprotectants that dampen osmotic shock, raising post-thaw survival above 90% in many programs. Sperm preparation buffers adopt antioxidant additives that enhance motility under oxidative stress, supporting the wider shift toward single-sperm tracking algorithms. Personalized media that mimic a patient’s follicular fluid profile are in early rollout, offering incremental revenue opportunities and higher margins. As a result, consumables suppliers secure recurring income streams that outpace the slower capital replacement pace, tilting overall growth dynamics in the IVF devices and consumables market.

By Technology: Fresh Embryo IVF Retains Lead While Frozen Cycles Gain Pace

Fresh embryo transfers accounted for 46.20% of 2025 procedures, largely because many clinics prefer immediate transfer to cut medication expense and minimize storage fees. Advances in luteal phase support and endometrial receptivity tests further improve fresh-cycle outcomes, reinforcing demand for rapid-use culture dishes and time-sensitive media. However, frozen embryo IVF exhibits a 18.70% CAGR, buoyed by microfluidic vitrification devices that sharply raise embryo survival and reduce scheduling pressure on clinical teams. Evidence shows frozen transfers can double cumulative live-birth rates in women over 35, persuading physicians to adopt a freeze-all strategy for higher-risk patients.

Niche procedures such as donor-egg IVF and PGT-assisted IVF add volume diversity. Donor cycles benefit from robust screening protocols that require specialized genetic assay kits, while PGT-assisted cycles integrate cell-free DNA collection hardware compatible with non-invasive workflows. The technology mix diversifies equipment orders, ensuring consistent pull-through for consumables tailored to each protocol. These shifts collectively expand addressable segments of the IVF devices and consumables market.

By End User: Fertility Clinics Dominate, Genetic Labs Emerge as Fast Movers

Fertility clinics managed 57.95% of global cycles in 2025, and chain consolidation is accelerating. Studies published in Management Science report 27% cycle volume growth and a 14% lift in live-birth rates after clinics join a network, driven by centralized training, procurement leverage, and uniform data capture. Such scale encourages bulk purchases of high-value incubators, micromanipulators, and proprietary media lines, concentrating spending within the IVF devices and consumables market. Hospitals maintain solid share by integrating fertility care into women’s health departments, leveraging shared imaging and surgical suites.

Cryobanks and genetic laboratories record the highest expansion at a 19.20% CAGR. Uptake stems from rising elective fertility preservation, employer-sponsored oocyte freezing benefits, and the broader shift toward comprehensive aneuploidy screening. Automated straw-loading robots and barcode-linked inventory systems improve storage accuracy, boosting demand for specialized consumables, nitrogen-efficient freezers, and thawing accessories. Partnerships between cryobanks and direct-to-consumer genetic services propel additional kit sales, underscoring the symbiotic growth between genetic analysis and core IVF workflows.

Geography Analysis

North America commanded 42.80% of 2025 revenue thanks to favorable reimbursement statutes, high procedural volumes, and a robust pipeline of automation startups. California’s impending coverage mandate promises a meaningful step-change in addressable patients once enforcement begins in July 2025. Clinics in Boston, Houston, and the Bay Area pilot robot-assisted ICSI, creating lighthouse installations that influence purchasing trends across the continent. Federal initiatives that extend IVF benefits to veterans and federal employees expand procedural financing further and reinforce equipment refresh budgets. As a result, capital expenditure per clinic remains the highest globally, anchoring premium pricing within the IVF devices and consumables market.

Asia-Pacific delivers the fastest growth at 17.30% CAGR, spurred by shifting demographics, higher disposable incomes, and rapid capacity building. India opens dozens of clinics annually, while Chinese municipal governments subsidize local laboratories to raise national birth rates. Regional centers in Malaysia and Thailand position themselves as medical tourism hubs by offering bundled treatment, accommodation, and tourism services at a fraction of Western costs. These hubs rely heavily on imported class IIb and class III medical devices, supporting a vibrant distribution ecosystem. The progressive adoption curve sustains rising orders for flexible tubing sets, universal warming dishes, and programmable freezers, extending the revenue stream for suppliers active in the IVF devices and consumables market.

Europe posts steady single-digit growth, underpinned by advanced research infrastructure and harmonized regulatory frameworks. Extended transition timelines under the In Vitro Diagnostic Regulation give manufacturers more headroom to certify devices, preventing supply gaps in critical consumables. However, lower public funding in parts of the region dampens procedural uptake, especially in the United Kingdom where NHS coverage has fallen. Southern European countries compensate by courting international patients, driving cross-border flows that partially offset domestic funding constraints. Collectively, these dynamics ensure diversified geographic revenue sources for multinational vendors.

Regulatory Landscape

IVF devices and consumables are subject to tighter medical-device quality controls and premarket requirements across major regions, with more focus on software-driven embryo assessment and traceability for human-origin materials used in ART workflows. In the United States, the FDA regulates assisted reproduction embryo image assessment systems as Class II devices (Product Code: PBH) through the 510(k) pathway. The Quality Management System Regulation (QMSR) took effect in February 2026, aligning device QMS requirements more closely with ISO 13485:2016 and raising compliance expectations for manufacturers and contract manufacturers supporting IVF consumables and lab instruments.

In Europe, IVF/ART laboratory devices that process or preserve cells and tissues are governed under Regulation (EU) 2017/745 (MDR). In May 2026, the European Commission adopted Implementing Regulation (EU) 2026/977, setting more uniform requirements and maximum timelines for Notified Body conformity assessments, which can affect certification planning for suppliers of incubators, cryosystems, and related disposables. In India, the CDSCO issued an April 2026 directive enforcing stricter licensing requirements for IVF and ART-related medical devices, including categories such as IUI kits and sperm-washing centrifuges, under the Drugs and Cosmetics Act, 1940. This increases formal market-entry and post-market obligations for vendors selling into fast-growing clinic networks.

Competitive Landscape

Private equity inflows surpassed USD 875 million in 2024, underscoring investor confidence in sustained double-digit growth. Cooper Companies finalized the USD 875 million purchase of Cook Medical’s reproductive health portfolio, securing a complementary consumables lineup and widening service contracts. Meanwhile, Astorg acquired Hamilton Thorne for USD 228 million, signaling a preference for precision instruments and software-enabled platforms that cross-sell disposables. Consolidators leverage shared sales teams and digital ordering portals to optimize product bundles, improving customer stickiness across the IVF devices and consumables market.

Strategic incumbents press ahead with manufacturing-led differentiation. Thermo Fisher Scientific allocated USD 2 billion to U.S. manufacturing and R&D through 2029, including capacity for culture media and advanced plastic ware. Vitrolife Group invested in AutoIVF, betting on remote egg collection systems that extend clinical reach into underserved geographies. Patent filings reveal heightened activity in AI-driven embryo assessment, non-contact micromanipulation, and cryogenic microfluidics, suggesting an innovation race likely to reset product lifecycles faster than historical norms.

Emerging disruptors bring fresh automation paradigms. Conceivable Life Sciences demonstrated end-to-end robotic ICSI, reducing embryologist intervention time to minutes and driving reproducibility. Overture Life attracted venture financing to refine single-use vitrification cartridges paired with smart warming blocks, positioning itself for outpatient fertility settings. These entrants focus on cloud-integrated dashboards, automated QC logging, and subscription-based consumable replenishment, strategies designed to carve share from traditional hardware-centric models within the IVF devices and consumables market.

IVF Devices And Consumables Industry Leaders

Cook Group

CooperSurgical Fertility Company

Merck KGaA

FUJIFILM Holdings Corporation

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization and automation in IVF laboratories are creating opportunities for vendors that can package instruments, media, and software into validated, site-to-site reproducible workflows. This is becoming more relevant as professional guidance and oversight tighten around lab practices and data capture, including the ESHRE IVF lab good-practice recommendations (2026 stakeholder-review update) and heightened ART surveillance attention in the United States through scrutiny of outcome and complication tracking. These developments support demand for integrated digital QC logs, traceability, and performance monitoring in tools used for AI embryo assessment, time-lapse incubation, and cryostorage inventory systems.

Network consolidation is also increasing multi-site tenders for standardized devices and consumables. Recent platform expansion and operator scaling, including FutureLife completing the acquisition of the Bahceci Group in June 2026 (with reported annual cycle volume of over 74,000 across Turkey and parts of the Balkans) and Nova IVF Fertility acquiring a majority stake in Kerala-based CRAFT Hospitals in March 2026, highlight procurement preferences for consistent consumable specifications and interoperable lab equipment across clinics. In the United States, INVO Fertility Inc. consummated the acquisition of Family Beginnings, P.C. in February 2026, further supporting demand for turnkey lab buildouts and ongoing consumables pull-through as provider footprints expand.

Recent Industry Developments

- May 2026: Alife Health received US FDA clearance for Embryo Predict, an AI-powered embryo assessment software used in assisted reproductive technology workflows. The clearance supports commercialization of regulated, clinic-deployable AI tools and increases competitive pressure on vendors building integrated imaging, analytics, and embryo-selection ecosystems.

- June 2025: Thermo Fisher Scientific launched the Orbitrap Astral Zoom and Orbitrap Excedion Pro mass spectrometers at ASMS 2025 to expand high-end proteomics capability used in fertility and reproductive research. The launch strengthens upstream R&D and translational pipelines that influence adoption of advanced media, biomarkers, and laboratory analytics linked to IVF workflows.

- June 2024: CooperSurgical acquired ZyMot Fertility (DxNow, Inc.) to add sperm separation technology to its assisted reproductive technology portfolio. The deal broadened CooperSurgical's ability to bundle procedure-specific consumables with existing IVF lab offerings, tightening customer stickiness for clinics seeking fewer suppliers for critical workflow components.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the IVF devices and consumables market covers the products used inside IVF labs and procedure rooms to prepare, fertilize, culture, and handle eggs and embryos, along with supporting disposables and media that get consumed during routine cycles.

Scope exclusions: This sizing does not count IVF clinical service fees, physician procedures, or fertility drugs that are billed as part of treatment packages.

Segmentation Overview

- By Type

- Instruments

- Sperm Separation System

- Incubator

- Cryosystem

- Other Instruments

- Reagents & Media

- Cryopreservation Media

- Semen Processing Media

- Other Reagents and Media

- Accessories & Disposables

- Instruments

- By Technology

- Fresh Embryo IVF

- Frozen Embryo IVF

- Donor Egg IVF

- Intracytoplasmic Sperm Injection (ICSI)

- PGT-Assisted IVF

- By End User

- Fertility Clinics

- Hospitals

- Surgical Centers

- Clinical Research Institutes

- Cryobanks & Genetic Labs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to pin down the demand pool and the product mix that typically sits inside an IVF lab purchase cycle. Public sources are used to understand cycle volumes, patient access, and policy signals, such as CDC ART surveillance, WHO infertility and reproductive health publications, OECD health statistics, and ESHRE and ASRM guidelines and annual updates.

To translate demand into product consumption, we also review sources like FDA device databases (for product categories and clearances), selected peer reviewed journals on IVF lab workflows and outcomes, and customs or trade statistics where relevant for equipment movement. Company annual reports, investor decks, and credible press are used to validate revenue exposure and geographic mix. For smaller private players and product innovation cadence, paid subscriptions for company financials and patent databases help close gaps. These are illustrative examples, and many other public and paid sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure test key assumptions that desk research cannot fully settle, especially consumables usage per cycle, replacement timing for lab instruments, and typical pricing bands by region. We speak with a mix of fertility clinic operators, embryologists, lab managers, distributors, and device side specialists across major geographies so the model reflects procurement and utilization patterns in day-to-day IVF delivery.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 45% |

| Mid tier: 55% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 19% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

The core sizing starts from a top-down build where IVF procedure volumes by country are reconstructed from ART registries and health statistics, and then mapped to a realistic bill of materials for lab devices and recurring consumables. Once the demand pool is built, value is calculated using average selling prices that are adjusted for regional price corridors and product mix.

To keep totals grounded, we corroborate the output with selective bottom-up checks, such as supplier revenue splits, distributor channel checks, and sampled price x volume sanity tests for key items. Inputs that materially move the model include IVF cycle counts and growth, frozen versus fresh transfer mix, lab capacity utilization and new clinic additions, replacement cycles for major instruments like incubators and micromanipulators, and per-cycle consumption patterns for culture media and disposables. When a country level series is incomplete, we use proxy indicators such as treatment tourism flows, clinic density, and reimbursement or regulatory changes, and then validate the implied volumes in follow-up calls.

For forecasting, scenario analysis is used because demand can shift quickly with policy, macro confidence, and clinic expansion plans. Assumptions for cycle growth, pricing progression, and mix shift are set with expert consensus, then stress tested by applying conservative and aggressive cases around utilization and procurement timing.

Data Validation & Update Cycle

We run triangulation checks by comparing the modeled market value against independent signals, such as reported ART cycle totals, device import patterns where relevant, and publicly discussed clinic expansion plans. Outliers are flagged when implied per-cycle spend or equipment replacement rates drift away from what interviews and published clinical workflows suggest, and those lines are revisited before sign-off.

A second analyst review is completed to confirm that scope, unit logic, and currency conversions are applied consistently across countries and years. The report is refreshed annually, and interim updates are done when material events occur, such as major regulatory changes, reimbursement shifts, or notable technology updates that alter adoption. Before delivery, we do a final pass to incorporate the most recent public releases and any newly collected interview feedback.

Mordor Intelligence's Ivf Devices and Consumables Market Size Compared With Other Published Estimates

Published numbers for IVF devices and consumables often differ because firms do not always count the same products, they may anchor on different base years, and their pricing assumptions can move a lot when consumables are modeled per cycle. Differences also show up when one estimate relies more on shipment signals, while another relies more on clinic revenue splits.

Fertility drugs and clinic procedure fees sit outside Mordor Intelligence's scope for this market, which is one reason the total can look lower than estimates that bundle IVF equipment with the full treatment bill. Gaps also come from how the fresh versus frozen mix is projected, whether recurring media and disposables are tied to verified cycle volumes, and how currency timing is handled when converting multi-country pricing into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.48 B (2026) | |

| Trade Journal A | USD 3.33 B (2025) | Uses an earlier base year and typically applies a narrower product basket centered on core lab instruments and standard media, with limited adjustment for country level cycle mix shifts. |

| Industry Research B | USD 2.85 B (2024) | Leans on a conservative cycle growth path and older price points, and the consumables run rate is often averaged broadly rather than being tied to fresh versus frozen workflow differences. |

The spread across the three figures is mainly explained by what gets counted with IVF purchasing and how tightly consumables are linked to real procedure volumes. By keeping the build traceable to cycle counts, product usage per cycle, and practical price corridors, the model stays repeatable and easier to validate country by country.

Key Questions Answered in the Report

What is the current value of the IVF devices and consumables market?

The IVF devices and consumables market size is USD 4.48 billion in 2026 and is forecast to reach USD 9.62 billion by 2031.

Which product category leads market revenue?

Instruments generate the largest revenue, holding 35.10% of the IVF devices and consumables market share in 2025.

Why is Asia-Pacific the fastest-growing region?

Rapid clinic expansion, favorable demographics, and cost-competitive treatment pricing lift Asia-Pacific at a 17.30% CAGR between 2026-2031.

How does automation influence IVF success rates?

Robotic ICSI and AI-based embryo selection raise procedural precision and implantation accuracy, contributing to higher live-birth outcomes.

What policy change will most affect U.S. demand?

California’s SB-729 mandates coverage for up to three IVF cycles from July 2025, significantly enlarging the insured patient pool.

Which end-user segment is expanding quickest?

Cryobanks and genetic laboratories are growing at a 19.20% CAGR through 2031, propelled by fertility preservation and broader genetic screening.

Page last updated on: