Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Lithium-Ion Battery Electrolyte Solvent Market Report is Segmented by Solvent Type (Ethylene Carbonate, Diethyl Carbonate, Dimethyl Carbonate, and More), Application (Power Backups/UPS, Consumer Electronics, Electric Mobility, Energy Storage Systems, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

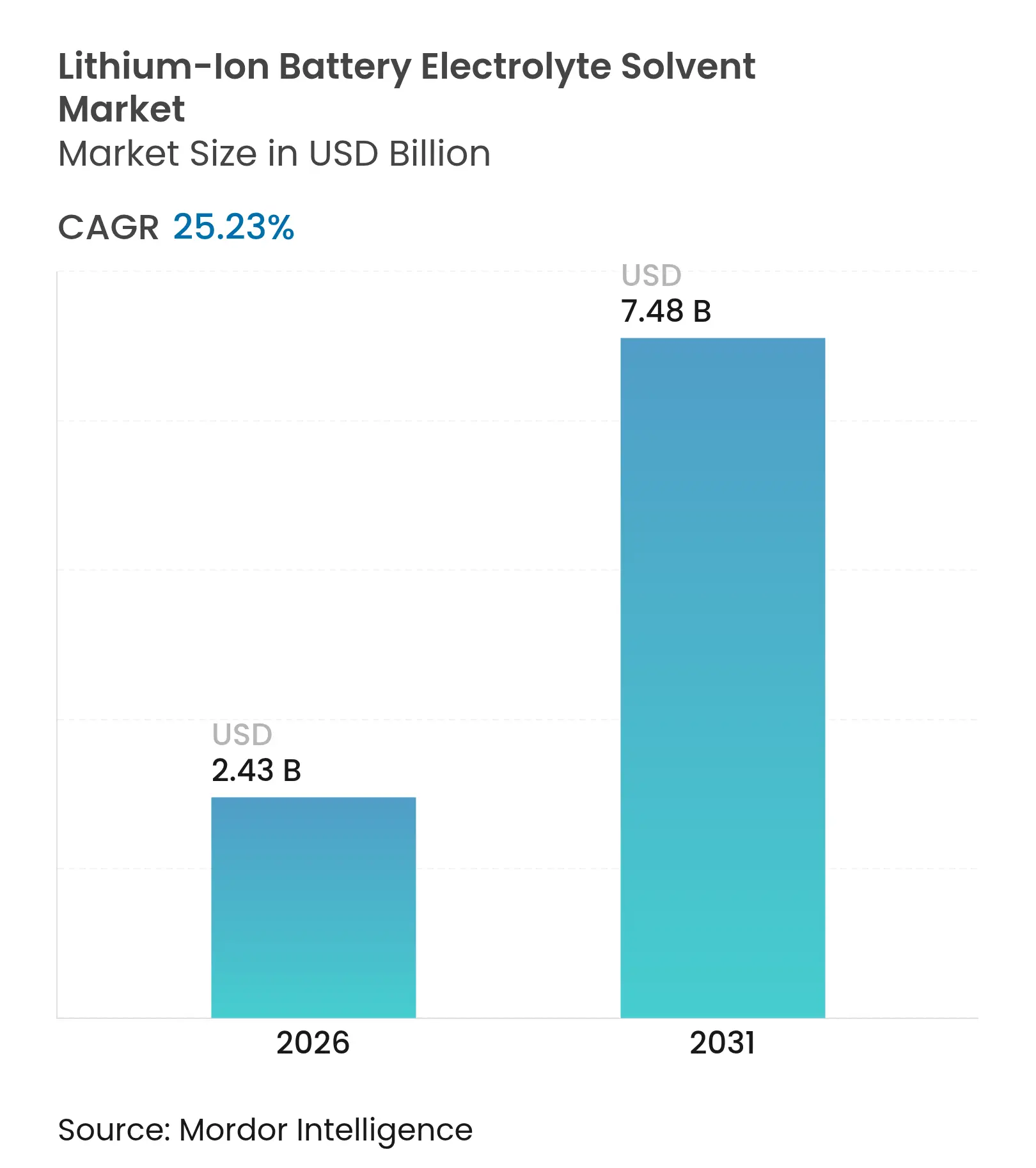

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 7.48 Billion |

| Growth Rate (2026 - 2031) | 25.23 % CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Lithium-Ion Battery Electrolyte Solvent Market size is estimated at USD 2.43 billion in 2026, and is expected to reach USD 7.48 billion by 2031, at a CAGR of 25.23% during the forecast period (2026-2031). This headline growth stems from capacity shifting toward North America and Europe under local-content rules, subsidies, and stricter carbon-footprint mandates. Integrated chemical producers are adding ultra-high-purity carbonate lines so cell makers can adopt silicon-rich and fast-charging chemistries, while rising electric-vehicle penetration and utility-scale battery storage keep volumes on a steep trajectory. Suppliers able to guarantee ISO 14067-compliant production and sub-20 ppm water levels are securing long-term offtake deals, yet price volatility for fluorinated additives and uncertainty over the solid-state timeline are tempering investment appetite in the lithium-ion battery electrolyte solvent market.

Key Report Takeaways

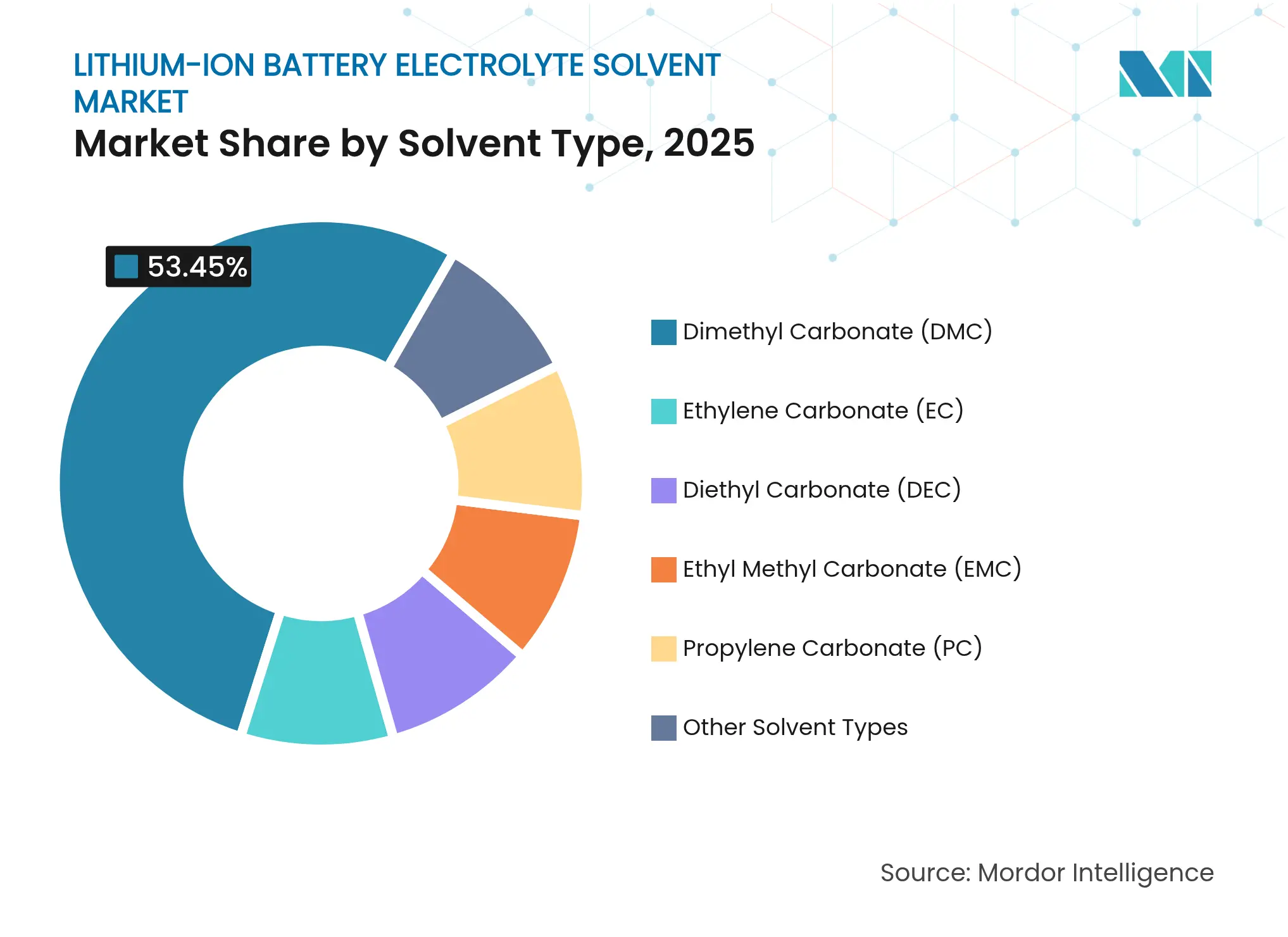

By solvent type, dimethyl carbonate commanded 53.45% of the lithium-ion battery electrolyte solvent market share in 2025 and is forecast to advance at a 29.29% CAGR through 2031.

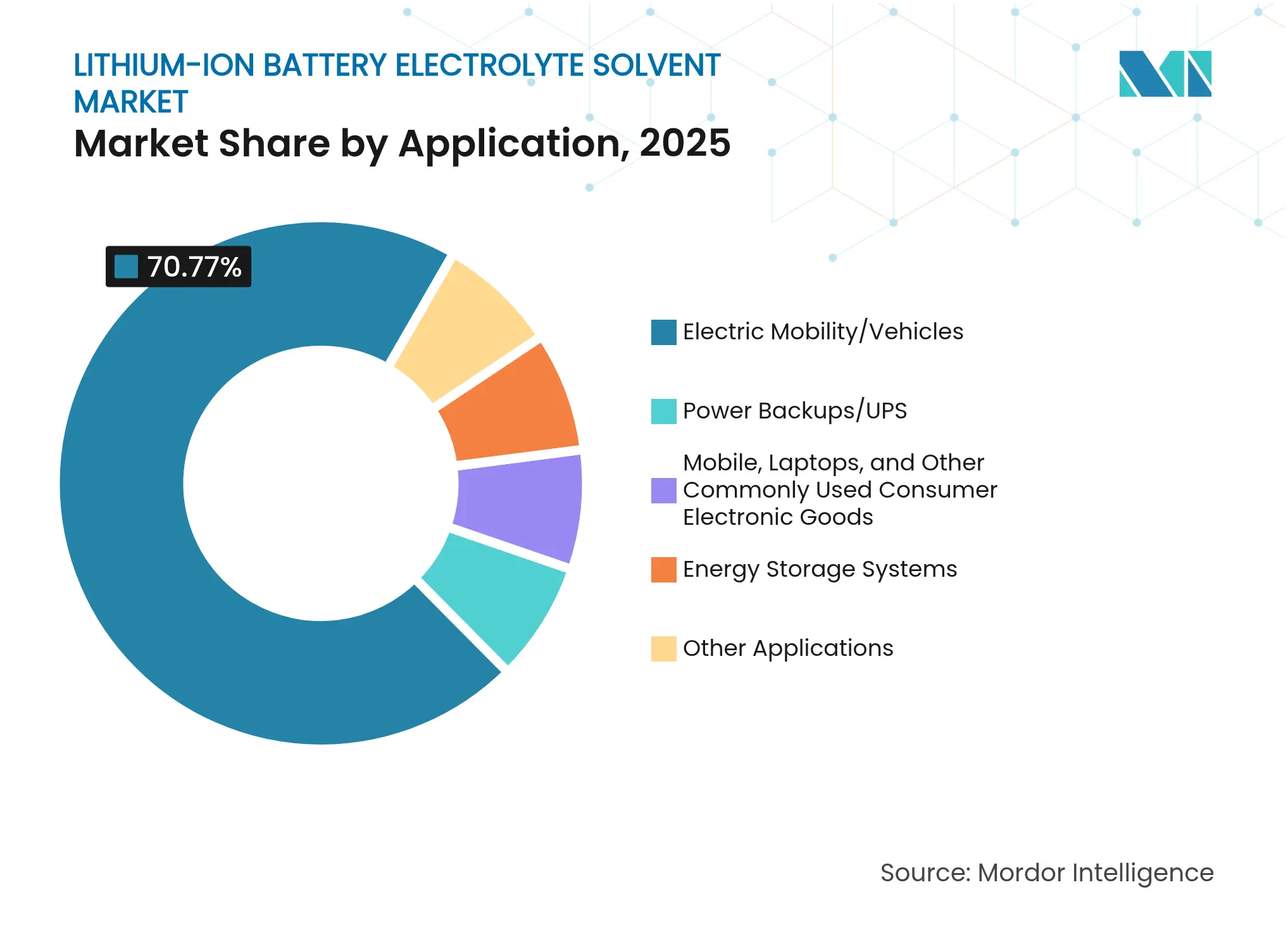

By application, electric mobility held a 70.77% share of the lithium-ion battery electrolyte solvent market size in 2025. Energy storage systems are expanding at a 29.16% CAGR to 2031.

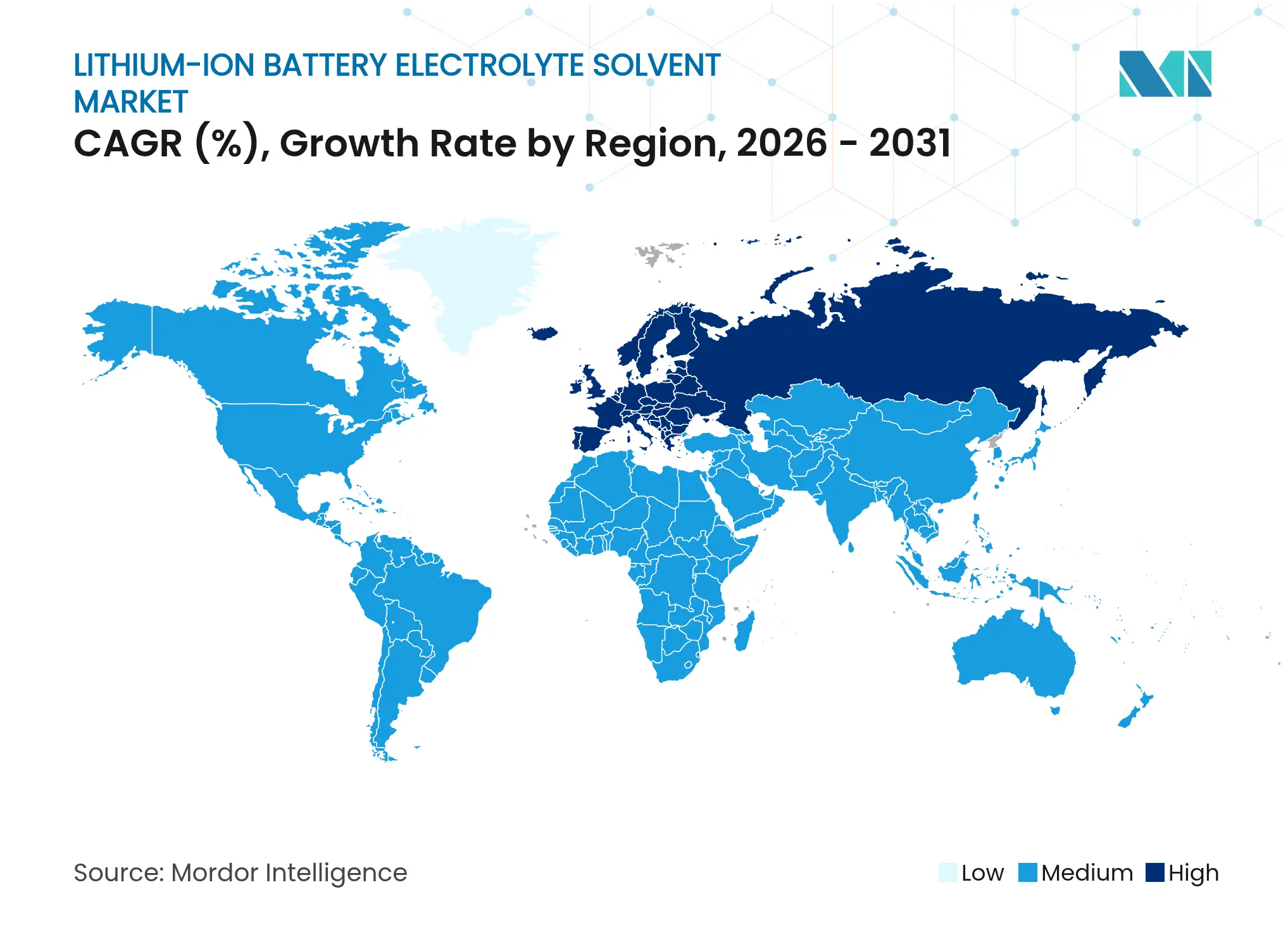

By geography, the Asia-Pacific held an 83.24% share in 2025, while Europe is forecast to post the fastest 53.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Gigafactory build-out outside China creating localized

solvent demand

Gigafactory build-out outside China creating localized

solvent demand

| +7.2% | North America and Europe, spillover to India | Medium term (2–4 years) |

(~) % Impact on CAGR Forecast

:

+7.2%

|

Geographic Relevance

:

North America and Europe, spillover to India

|

Impact Timeline

:

Medium term (2–4 years)

|

Ultra-high-purity carbonate lines to support Si-rich

anodes

Ultra-high-purity carbonate lines to support Si-rich

anodes

| +4.8% | Global, led by Japan and South Korea | Long term (≥4 years) | |||

Government incentives (IRA/EU) driving supply-chain

localization

Government incentives (IRA/EU) driving supply-chain

localization

| +6.5% | North America and EU | Short term (≤2 years) | |||

Fast-charging chemistries requiring low-viscosity blends

Fast-charging chemistries requiring low-viscosity blends

| +3.9% | Global, early adoption in China and North America | Medium term (2–4 years) | |||

Cost advantage of LFP packs scaling solvent volumes in

Asia-Pacific

Cost advantage of LFP packs scaling solvent volumes in

Asia-Pacific

| +5.1% | APAC core, expanding to MEA and South America | Short term (≤2 years) | |||

| Source: Mordor Intelligence | ||||||

Gigafactory Build-Out Outside China Creating Localized Solvent Demand

Subsidy programs in North America and Europe are reshaping the landscape of the lithium-ion battery electrolyte solvent market. The U.S. Inflation Reduction Act incentivizes battery cells adhering to domestic-content rules. This has led to collaborations like GM-LG, which now sources Dimethyl Carbonate from Texas instead of Asia. Europe is following suit: Northvolt has inked a deal with BASF’s Ludwigshafen line, ensuring regional supplies by 2025. Similarly, India's Production Linked Incentive scheme mandates domestic value addition. This has prompted Reliance Industries to assess carbonate production in Jamnagar. Such regulations not only reduce logistics lead times but also decentralize previously unified supply chains. This shift opens avenues for toll distillers and bulk-chemical distributors in the lithium-ion battery electrolyte solvent market.

Emergence of Ultra-High-Purity Carbonate Lines to Support Si-Rich Anodes

Silicon anodes, known for their high energy densities, face rapid degradation when water content exceeds critical levels. In 2025, Mitsubishi Chemical launched a molecular-sieve unit, ensuring Propylene Carbonate production with minimal water content. This move specifically targets industry giants Panasonic and Samsung SDI for their 4680 cells. Following suit, UBE Corporation implemented an ion-exchange retrofit in May 2025, successfully reducing metal impurities[1]UBE Corporation, “Electrolyte Purity Upgrade at Sakai Facility,” ube.com. Such strategic investments not only elevate capital entry barriers but also shift bargaining power towards integrated producers, signaling robust long-term growth prospects in the lithium-ion battery electrolyte solvent market.

Government Incentives Driving Electrolyte Supply-Chain Localization

In June 2024, the EU unveiled its Critical Raw Materials Act, aiming for increased domestic processing of strategic inputs. As part of this initiative, the European Investment Bank rolled out a low-interest facility, specifically targeting carbonate projects. Meanwhile, Canada's Strategic Innovation Fund allocated funding to BASF. This funding is set to power a Dimethyl Carbonate plant, poised to commence solvent shipments across the USMCA region in 2026. Thanks to these subsidies, regional cost disparities have narrowed, rendering "friend-shored" solvent production not just feasible but profitable. This boost has significantly elevated the region's output in the lithium-ion battery electrolyte solvent market.

Shift to Fast-Charging Chemistries Requiring Low-Viscosity Blends

Automakers are racing to achieve faster charge times, necessitating that electrolytes remain at optimal viscosity levels. Tesla's 4680 cells, produced in Texas, utilize a specific ratio of Dimethyl Carbonate to Ethylene Carbonate, facilitating efficient charging. Hyundai's 800-volt platform, in collaboration with LG Chem, is set to implement low-viscosity blends to enable rapid charging starting in 2027. Such innovations are expanding the premium segment of the lithium-ion battery electrolyte solvent market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile prices and supply risk for fluorinated raw

materials

Volatile prices and supply risk for fluorinated raw

materials

| -3.2% | Global, acute in Europe and North America | Short term (≤2 years) |

(~) % Impact on CAGR Forecast

:

-3.2%

|

Geographic Relevance

:

Global, acute in Europe and North America

|

Impact Timeline

:

Short term (≤2 years)

|

Toxicity and tightening regulation on LiPF6/EC handling

Toxicity and tightening regulation on LiPF6/EC handling

| -2.1% | North America and EU, emerging in APAC | Medium term (2–4 years) | |||

Policy pivot toward solid-state batteries reducing liquid

runway

Policy pivot toward solid-state batteries reducing liquid

runway

| -1.8% | Japan and South Korea, spillover to EU | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Prices and Supply Risk for Fluorinated Raw Materials

In early 2025, environmental shutdowns in Jiangxi and Sichuan removed LiPF₆ from the market, causing a surge in spot prices. This price hike tightened blender margins, as LiPF₆ inventory has a strict degradation limit. Meanwhile, European cell manufacturers, facing extended lead times due to REACH dossiers, find themselves reliant on imports for nearly all fluorinated additives. This dependency amplifies the cost pressures in the lithium-ion battery electrolyte solvent market[2]European Chemicals Agency, “Lithium Hexafluorophosphate Substance Information,” echa.europa.eu.

Toxicity and Tightening Regulation on LiPF₆/Ethylene Carbonate Handling

In 2024, OSHA slashed the allowable exposure limit for Ethylene Carbonate vapors to 25 ppm. This regulatory change compelled Panasonic to undertake retrofits at its Nevada gigafactory. Meanwhile, in June 2024, the EU added Ethylene Carbonate to its Candidate List of Substances of Very High Concern, imposing new disclosure obligations on the market for this lithium-ion battery electrolyte solvent.

By Solvent Type: Dimethyl Carbonate Secures Structural Lead

Dimethyl Carbonate captured 53.45% of the lithium-ion battery electrolyte solvent market share in 2025 and is forecast to expand at a 29.29% CAGR through 2031. That dominance reflects its 0.59 cP viscosity, high dielectric constant, and compatibility with both graphite and silicon anodes. Ethylene Carbonate maintains a critical but smaller role because it forms a robust solid-electrolyte interphase on graphite, while Diethyl Carbonate and Ethyl Methyl Carbonate tune viscosity and flash point. Propylene Carbonate survives in niche lithium-titanate oxide cells for grid storage that tolerate its graphite-exfoliation issues but value its low-temperature performance.

The next technology cycle will reinforce Dimethyl Carbonate’s position. Commercial silicon-rich anodes entering production in 2026 require even lower solvent viscosity to offset volume-expansion impedance, pushing DMC loadings higher and sustaining premium pricing. Conversely, lithium-metal anodes for hybrid liquid cells will demand higher levels of fluoroethylene carbonate, creating a specialised sub-segment for ultra-high-purity coproduct solvents. Regulatory burden remains light for carbonate solvents, so competitive dynamics hinge on process know-how and feedstock integration rather than compliance costs, favoring incumbents in the lithium-ion battery electrolyte solvent market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Mobility Still Dominates, Storage Surges

Electric Mobility held 70.77% of the lithium-ion battery electrolyte solvent market in 2025. This dominance is largely attributed to the automotive sector, where a typical 75 kWh pack utilizes a significant amount of electrolyte. Global sales of electric vehicles (EVs) surged, driving substantial solvent demand. Notably, Energy Storage Systems are the fastest-growing application at a 29.16% CAGR. This growth is fueled by utilities doubling their battery capacities to better balance renewable energy sources. Furthermore, the adoption of LFP chemistry has intensified solvent usage per kWh, amplifying the overall volume effects.

While volumes for smartphones, laptops, and other consumer electronics have stabilized, the demand for solvents in these sectors now closely aligns with replacement cycles. Uninterruptible Power Supplies (UPS) and power-backup systems show a preference for high-flash-point blends, like Propylene Carbonate, ensuring optimal performance across diverse climates. Although specialty applications in medical and aerospace fields remain limited in volume, they command premium margins due to stringent qualification requirements. As the industry shifts focus towards stationary storage and commercial vehicles, today's carbonate solvents maintain their significance, effectively delaying the anticipated disruption from solid-state technologies in the lithium-ion battery electrolyte solvent market.

Note: Segment shares of all individual segments available upon report purchase

Asia-Pacific owned 83.24% of the lithium-ion battery electrolyte solvent market share in 2025, largely due to China's substantial stake in global cell capacity. CATL, operating multiple gigafactories, strategically sources Dimethyl Carbonate locally to adhere to just-in-time production windows. Meanwhile, under the K-Battery roadmap, Korean cell manufacturers procure from domestic suppliers. Japan, while boasting advanced material capabilities, is reallocating new capacities to North America, catering to Tesla and Nissan, in alignment with USMCA regulations.

Europe will post the fastest regional CAGR at 53.46% through 2031. With a goal of achieving substantial local cell capacity by 2030, the European Battery Alliance is pushing forward. Companies like Northvolt and Automotive Cells Company are establishing solvent supply chains in Germany and France, ensuring compliance with the EU Battery Regulation’s embedded-carbon mandates. While Poland and Hungary lure second-tier producers with promises of lower operating costs, they grapple with the challenge of high energy prices.

North America is rapidly expanding, driven by the Inflation Reduction Act's content stipulations, which aim for full compliance by 2029. BASF plans to inaugurate a Dimethyl Carbonate facility in Ontario. Concurrently, Tesla's gigafactory in Nuevo León is set to source its solvent from the nearby Huntsman production, solidifying a local supply ecosystem. Both Mexico and Canada offer tariff-free access to U.S. EV supply chains. Meanwhile, Brazil and Argentina are eyeing upstream integration, leveraging their regional lithium resources. Though the Middle East and Africa currently play a minor role, they could witness a surge in demand, especially if ambitious projects like NEOM achieve their 2030 storage targets.

Market Concentration

The lithium-ion battery electrolyte solvent market is moderately consolidated. BASF integrates upstream methanol and downstream purification, offering bundled contracts that lock in volumes for up to five years, while Mitsubishi Chemical focuses on sub-10 ppm water grades that command premiums in silicon-anode cells. Chinese disruptors backward-integrate into LiPF₆ to capture additive margins, and Merck KGaA exploits its semiconductor-grade purification know-how to launch ultra-pure Ethylene Carbonate for solid-state hybrids. Competitive intensity is moving from commodity volume to co-development agreements that embed solvent suppliers inside cell-design cycles, raising switching costs for OEMs and cementing existing relationships within the lithium-ion battery electrolyte solvent market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Electrolytes are vital components of an electrochemical energy storage device. They are usually composed of a solvent or mixture of solvents and a salt or a mixture of salts, which provide the appropriate environment for ionic conduction.

The lithium-ion battery's electrolyte solvent market report is segmented by solvent type, application, and geography. By solvent type, the market is segmented into ethylene carbonate, diethyl carbonate, dimethyl carbonate, ethyl methyl carbonate, propylene carbonate, and other solvent types. By application, the market is segmented into application power backups/UPS, mobile, laptops, and other commonly used consumer electronic goods, electric mobility/vehicles, energy storage systems, and other applications. The report also covers the size and forecasts for the lithium-ion battery's electrolyte solvent market in 18 countries across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.