Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

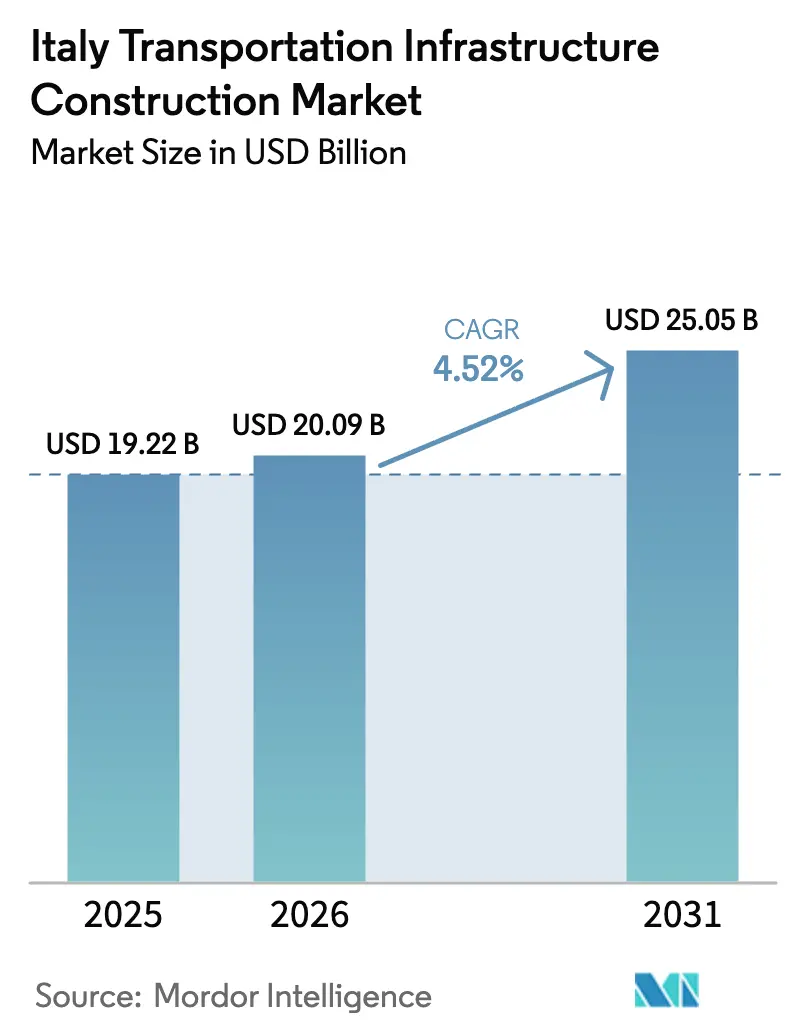

| Base Year Market Size (2025) | USD 19.22 Billion |

| Market Size (2026) | USD 20.09 Billion |

| Market Size (2031) | USD 25.05 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The Italy Transportation Infrastructure Construction market size is expected to grow from USD 19.22 billion in 2025 to USD 20.09 billion in 2026 and is forecast to reach USD 25.05 billion by 2031 at 4.52% CAGR over 2026-2031. Public funding from the National Recovery and Resilience Plan (PNRR) supplies USD 211.9 billion, with transport projects absorbing a significant share, while the European Union’s Connecting Europe Facility adds USD 7.63 billion in 2024, accelerating corridor upgrades[1]Directorate-General for Mobility and Transport, “2024 Connecting Europe Facility Transport Call Results,” European Commission, europa.eu. The Italy transportation infrastructure construction market benefits from record allocations to high-speed rail, intermodal hubs, and port expansions that align national priorities with climate objectives. Private‐sector appetite is growing through public-private partnerships as investors look to tap the USD 28.12 billion Connecting Europe Facility Transport programme. However, lingering cost inflation and lengthy permitting cycles temper the growth outlook, even as recent reforms and digital procurement tools aim to shorten delivery times.

Key Report Takeaways

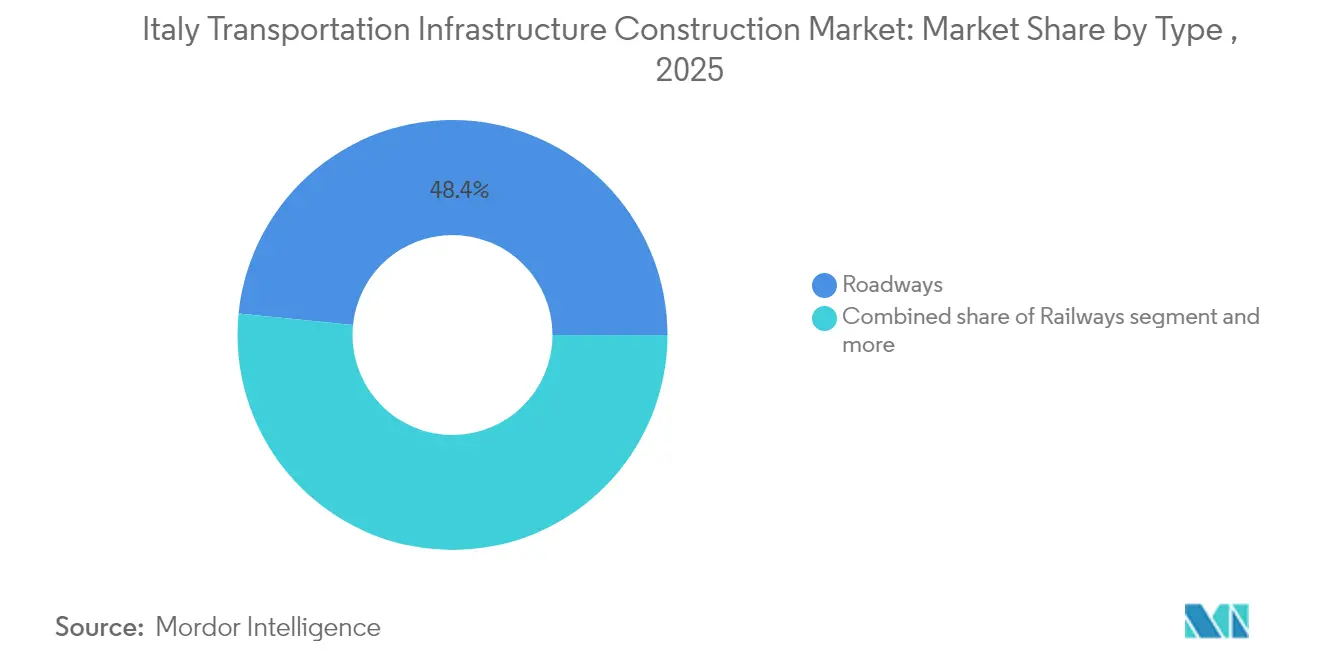

- By type, roadways led with 48.40% of the Italy transportation infrastructure construction market share in 2025, whereas railways post the fastest 5.05% CAGR through 2031.

- By construction activity, new construction captured 52.35% share of the Italy transportation infrastructure construction market size in 2025, while renovation expands at a 5.17% CAGR to 2031.

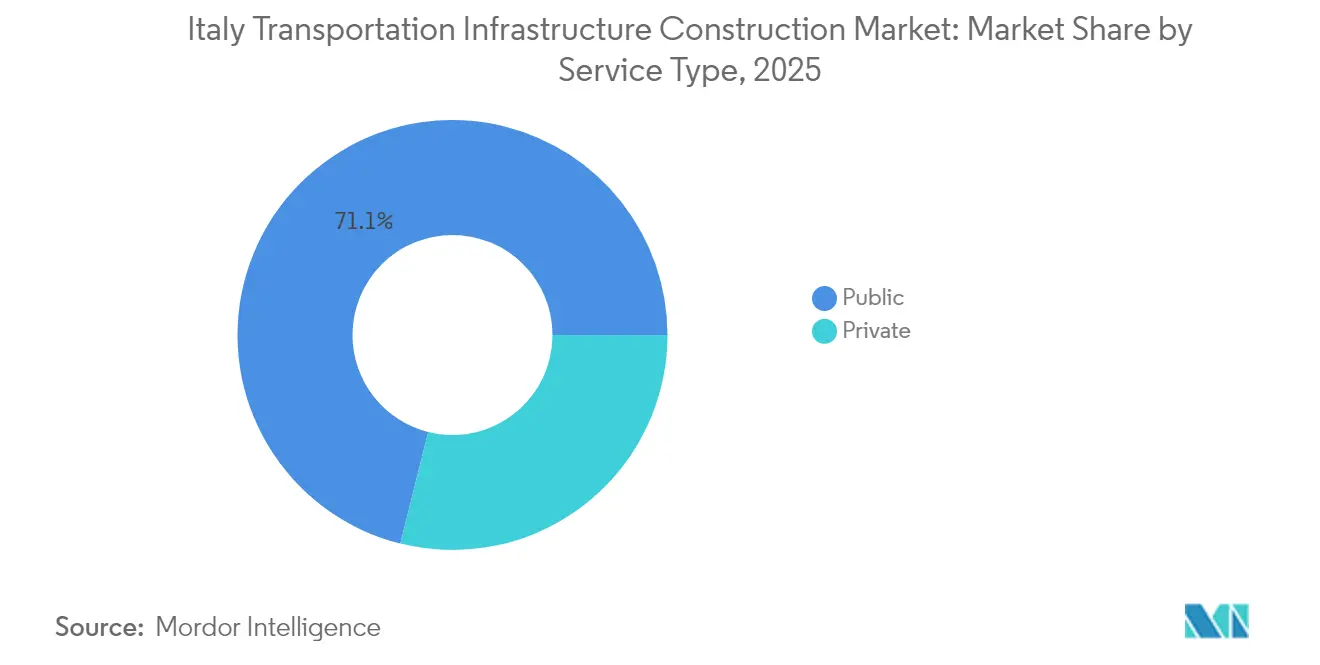

- By funding source, public investment retained 71.10% share of the Italy transportation infrastructure construction market size in 2025; private participation records a 5.30% CAGR, reflecting wider PPP adoption.

- By geography, Rome commanded 26.95% of market activity in 2025, and Turin is the fastest-rising area at a 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed investment programs to modernize road and rail networks | +1.2% | National, North-South corridors | Medium term (2-4 years) |

| EU funding support for sustainable and trans-European transport corridors | +0.9% | National, Core Network | Long term (≥ 4 years) |

| High demand for intermodal logistics and port expansion projects | +0.7% | Coastal hubs in Liguria, Veneto, South | Medium term (2-4 years) |

| Infrastructure-led regional development plans in Southern Italy and inland areas | +0.6% | Calabria, Sicily, Basilicata | Medium term (2-4 years) |

| Urban mobility initiatives driving metro and tramway upgrades | +0.5% | Rome, Milan, Turin, Bologna, Naples | Short term (≤ 2 years) |

| Increasing focus on climate-resilient transport infrastructure development | +0.4% | Alpine and coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed Investment Programs to Modernize Road and Rail Networks

The government channels unprecedented capital into the Italy transportation infrastructure construction market through the PNRR, assigning USD 211.9 billion to modernisation initiatives. Ferrovie dello Stato Italiane has earmarked USD 54.5 billion for rail and USD 43.6 billion for road upgrades between 2025 and 2029, narrowing the logistics gap with northern Europe. Extraordinary commissioners oversee 57 strategic projects worth USD 90.14 billion, creating 68,000 annual jobs and peaking at 100,000 in 2025. This state-led momentum is matched by the state-owned Cassa Depositi e Prestiti, whose USD 88.29 billion plan leverages finance to mobilise USD 170 billion of total investments. Collectively, these moves strengthen domestic supply chains and anchor long-term demand for design, engineering, and construction services.

EU Funding Support for Sustainable and Trans-European Transport Corridors

EU mechanisms are a potent tailwind for the Italy transportation infrastructure construction market. The 2024 Connecting Europe Facility allocated USD 7.63 billion, 80% of which is rail-oriented, supporting core TEN-T routes such as the Mediterranean and Rhine-Alps corridors. The landmark Lyon-Turin Base Tunnel has already awarded USD 4.36 billion in civil works contracts and excavated 39.5 km of tunnels, underscoring the momentum of cross-border megaprojects. Italy’s sovereign green bonds channel USD 15.15 billion into low-carbon transport infrastructure, integrating EU climate goals with national infrastructure blueprints. The revised TEN-T regulation sets a 2030 deadline for core-network completion, concentrating funding and political support on timely delivery[2]Ministero dell’Economia e delle Finanze, “Green Bond Allocation & Impact Report 2024,” Ministry of Economy and Finance, mef.gov.it.

High Demand for Intermodal Logistics and Port Expansion Projects

Post-pandemic supply-chain realignment increases throughput at Mediterranean gateways, boosting the Italy transportation infrastructure construction market. The Port of Taranto’s multimodal expansion connects directly to the A14 motorway and Bari-Bologna rail line, elevating its role in Europe-Asia trade flows. Rete Ferroviaria Italiana invests USD 2.73 billion to double national rail-freight capacity by 2031, while the USD 7.63 billion Third Giovi Pass cuts travel times between Genoa, Milan, and Turin. Modal shift mandates in the PNRR steer freight from road to rail, and expanding inland terminals unlocks capacity for containerised cargo, making intermodal infrastructure a vital growth lever.

Urban Mobility Initiatives Driving Metro and Tramway Infrastructure Upgrades

Sustainability rules and city-level climate commitments boost metro, tramway, and rapid-bus schemes, feeding new work into the Italy transportation infrastructure construction market. Bologna’s USD 554 million Red Line tram entered construction in April 2023; Bergamo’s electric BRT system adds a USD 46.9 million contract financed by EU funds. Milan’s Innovation District embeds net-zero objectives into transport planning, and Campania’s 43 km regional metro integrates 30 stations under unified ticketing to spark urban regeneration. These projects raise demand for signalling, rolling stock, and depot infrastructure, making urban mobility a near-term revenue driver for contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction material and labor costs affecting project viability | -1.1% | National, industrial north | Short term (≤ 2 years) |

| Prolonged regulatory approval timelines delaying project execution | -0.8% | National, > USD 54 million projects | Medium term (2-4 years) |

| Fragmented tendering and procurement processes limiting efficiency and competition | -0.6% | Smaller municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Regulatory Approval Timelines Delaying Project Execution

Complex permitting frameworks still prolong delivery in the Italy transportation infrastructure construction market. Public works average 4.4 years from tender to completion, with major schemes exceeding USD 54 million taking even longer. Although a 2023 Public Contracts Code reform trimmed rail authorisation cycles from 11 to 6 months, overlapping local and national approvals persist. Extraordinary commissioners mitigate some bottlenecks yet introduce parallel governance tracks. Continued digitalisation and one-stop authorisation portals are essential to lock in recent time-saving gains and reduce investor risk.

Rising Construction Material and Labor Costs Affecting Project Viability

The Construction Cost Index climbed 20% post-2021, squeezing margins across the Italy transportation infrastructure construction market. Steel and cement price volatility is particularly acute for rail and bridge contracts reliant on specialised materials. Labour shortages amplify pressure; Webuild will recruit 10,000 workers by 2026 to cover critical skills gaps. Strategic workforce programmes—such as Alstom’s USD 68.7 million localisation initiative that supports 14,087 jobs—illustrate how supply-side responses can curb cost escalation. Without broad adoption of similar measures, budget overruns may delay or resize planned projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Roadways Hold Lead as Railways Accelerate

Roadways delivered 48.40% of the Italy transportation infrastructure construction market share in 2025, reflecting the country’s dense 6,000 km motorway grid and ongoing climate-proofing upgrades. Autostrade per l’Italia invested USD 1.85 billion in the first nine months of 2024 to reinforce viaducts and tunnels exposed to extreme weather, showing sustained capital flows into the dominant segment. Despite this lead, railways outpace all other modes with a 5.05% CAGR to 2031 as the government prioritises carbon-efficient transport. The USD 14.40 billion high-speed rail programme adds 274 km of new southern lines and 165 km of northern links, compressing domestic travel times and freeing capacity for freight. The rail surge feeds orders for signalling, track, and catenary suppliers, positioning rolling-stock makers and civil contractors for steady award pipelines. The Italy transportation infrastructure construction market size for rail schemes is forecast to expand quickly as EU taxonomy rules steer funds into low-carbon corridors.

The shift toward a greener network triggers rising interest in multimodal nodes where rail connects to road and port facilities. Under the Italy transportation infrastructure construction market, the Liguria-Alps high-speed connection worth USD 4.69 billion forms the backbone of the Genoa Logistic System, complementing the Third Giovi Pass and boosting port throughput. Road contractors respond by embedding recycled asphalt and smart-traffic sensors into upgrade works to align with environmental tender criteria. Conversely, rail builders leverage modular bridge designs and digital twins to shorten construction cycles. Together, these advances create a more resilient, technology-enhanced network that’s better suited to shifting freight patterns and climate risks.

By Construction Type: New Projects Lead as Renovation Gains Pace

New construction accounted for 52.35% of the Italy transportation infrastructure construction market share in 2025, reflecting the priority that policymakers and network managers place on expanding capacity and closing connectivity gaps. Fresh highway segments, high-speed rail corridors, and new metro lines dominate tender pipelines because they draw directly on National Recovery and Resilience Plan and EU-facility grants. Contractors highlight that green-field works allow the use of modern design standards and digital engineering tools from project inception, which improves life-cycle performance and aligns with climate-resilience targets. As a result, the Italy transportation infrastructure construction market size attached to turnkey road and rail packages remains substantial, supporting steady orders for civil works, signalling, and rolling-stock suppliers.

Renovation projects are advancing at a faster 5.17% CAGR through 2031 as authorities move to retrofit ageing bridges, tunnels, and viaducts to withstand more intense weather events and heavier freight loads. The surge is visible in safety-upgrade programmes on historic autostrade viaducts and in platform-lengthening efforts across regional rail networks that must accommodate longer trains. Digital twins and non-invasive inspection technologies shorten asset-condition assessments, allowing builders to phase works around live traffic and limit service disruptions. With climate-proofing rules becoming more stringent, renovation spending is set to rise further, driving specialised demand for structural reinforcement materials and smart-monitoring systems.

By Investment Source: Public Capital Dominates while Private Finance Rises

Public funding supplied 71.10% of Italy's transportation infrastructure construction market share in 2025, a result of substantial allocations from the USD 211.9 billion National Recovery and Resilience Plan and long-standing state support for strategic corridors. Sovereign borrowing costs remain favourable, so central and regional governments continue to underwrite big-ticket rail tunnels, motorway widenings, and intra-city metro extensions. These outlays anchor the Italy transportation infrastructure construction market size and give contractors predictable pipelines. Procurement frameworks increasingly mandate environmental and social criteria, encouraging public sponsors to bundle decarbonisation requirements into civil works contracts.

Private financing is expanding at a 5.30% CAGR as institutional investors and infrastructure funds seek long-duration assets with inflation-linked revenue. Public–private partnerships back tolled bridges, rolling-stock leasing pools, and automated freight terminals, often combining availability payments with performance incentives. The opening of the USD 28.12 billion Connecting Europe Facility Transport programme has spurred several hybrid-finance deals, where EU grants de-risk senior debt tranches and attract pension-fund equity. Concessionaires are also issuing sustainability-linked bonds that tie interest margins to emissions targets, signalling a shift toward market-based discipline in project performance. Adoption of these structures is set to grow, broadening the capital base for Italy’s next generation of transport upgrades.

Geography Analysis

Rome retained the largest slice of the Italy transportation infrastructure construction market in 2025 at 26.95% as the Mediterranean Corridor funnels cargo through the capital’s freight villages toward northern consumer centres. Significant initiatives include the 18 km Tiburtina rail node upgrade and the Fiumicino road widening, both financed via PNRR funds. Multiple metro extensions—Lines C and D—add further civil works volume, sustaining local contractor order books.

Northern cities are experiencing the fastest growth. Turin, at a 5.62% CAGR, benefits from proximity to the Lyon-Turin Base Tunnel and the USD 4.69 billion Liguria-Alps high-speed link, anchoring the Piedmont logistics cluster. The Italy transportation infrastructure construction market size attached to Piedmont rail and road schemes expands as automakers shift freight from road to rail to meet decarbonisation goals. Milan complements this with ring-road resiliency projects that integrate smart mobility platforms, and Lombardy’s PPP pipeline now includes light-rail and e-bus depots financed by institutional investors.

In the south, the Mezzogiorno region absorbs growing funding to close the infrastructure gap with the industrial north. Naples modernises its regional metro while Bari redevelops its harbour rail interface, signalling fresh opportunities for mid-tier builders. EU cohesion funds and the “Bridge the Divide” regional programme earmark grants for climate-resilient bridges and landslide mitigation on mountain roads, expanding the overall Italy transportation infrastructure construction market. These capital flows stimulate local economies and gradually reduce the historical north-south logistics divide.

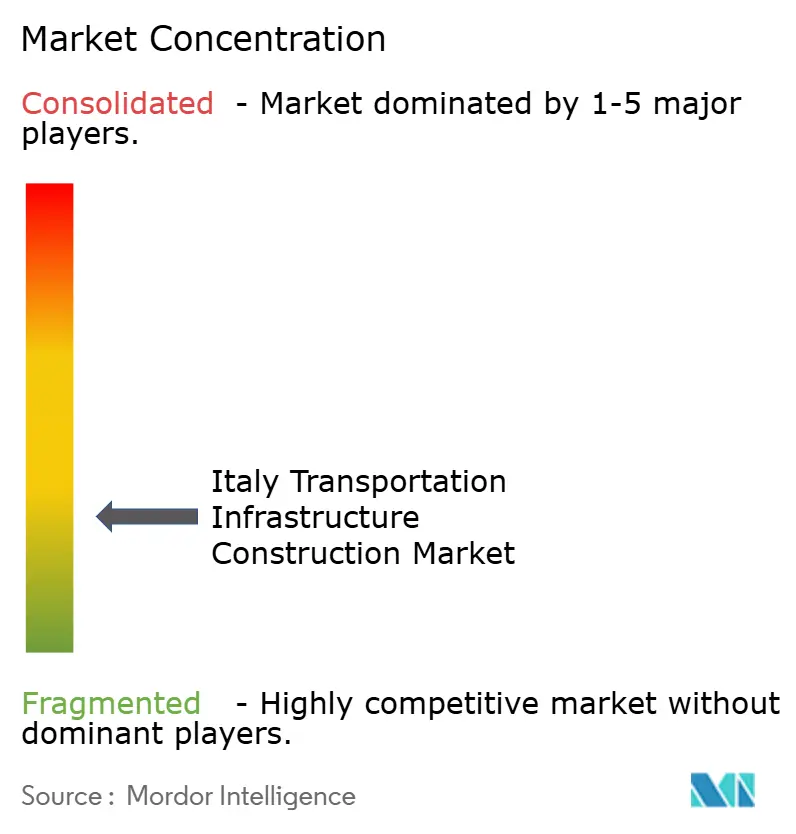

Competitive Landscape

Competition in the Italy transportation infrastructure construction market remains fragmented, yet scale is increasingly decisive. Webuild Group reported USD 8.18 billion in new orders during H1 2024, spanning high-speed rail, hydropower dams, and metro lines. Its integrated engineering-procurement-construction-management model is attractive for megaprojects requiring tunnelling and geotechnical prowess. Salini Impregilo’s digital twin deployment on the Naples-Bari high-speed rail underscores a pivot toward predictive maintenance solutions that enhance life-cycle value.

Mid-size contractors collaborate through consortia to secure larger bids that exceed individual bonding capacity. For example, a joint venture led by Astaldi and Ghella captured tunnelling packages on the Lyon-Turin Base Tunnel by pooling equipment fleets and risk-sharing arrangements. Engineering service providers such as Italferr leverage BIM services to gain recurring revenue as design complexity rises. Foreign entrants, notably Spanish and French rail specialists, target signalling and electrification lots, stimulating technology transfer and raising domestic capability.

Strategically, leading players anchor corporate governance to ESG metrics to satisfy EU and domestic green-finance criteria. Webuild issued sustainability-linked bonds tied to emission reduction targets, while Ferrovie dello Stato assigns tender scoring premiums for contractors that exceed circular-economy benchmarks. Supply-chain localisation also gains traction; Alstom’s USD 68.7 million plan to expand manufacturing in Savigliano illustrates how multinationals increase domestic footprint to win procurement points and mitigate import bottlenecks.

Italy Transportation Infrastructure Construction Industry Leaders

WeBuild

Salcef Group

Astaldi

Rizzani de Eccher

Colas Rail Italia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ferrovie dello Stato Italiane awarded a USD 1.2 billion contract for the Battipaglia-Romagnano high-speed rail section, advancing southern corridor completion.

- November 2024: Webuild Group signed a USD 712 million agreement to design and build Line C, Section T2 of the Rome Metro.

- April 2024: Construction began on Bologna’s USD 554 million Red Line tram after securing environmental clearance.

- February 2024: Rete Ferroviaria Italiana launched USD 2.73 billion in tenders for new intermodal freight terminals under the PNRR framework.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats Italy's transportation infrastructure construction market as all investment directed toward planning, building, upgrading, and repairing public roadways, rail corridors, airports, ports, and related civil assets that move passengers or freight within the country. Expenditure linked to purely energy, telecommunication, or private real-estate facilities sits outside this boundary.

(Excludes power transmission lines, oil and gas pipelines, and building refurbishments unrelated to mobility.)

Segmentation Overview

- By Type

- Roadways

- Railways

- Airways

- Ports & Inland Waterways

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Key Cities

- Rome

- Milan

- Turin

- Rest of Italy

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed project engineers in Rome and Milan, procurement officers at port authorities, and financial controllers inside tier-one contractors. These discussions tested cost assumptions, validated start dates for National Recovery and Resilience Plan (PNRR) projects, and clarified how EU Connecting Europe Facility grants flow into yearly spend.

Desk Research

We began with open datasets from Eurostat, ISTAT, and the Ministry of Infrastructure and Transport, which map annual outlays, project pipelines, and modal traffic volumes. Industry updates from the European Commission's TEN-T progress tracker, ANAS road statistics, and Bank of Italy macro releases helped cross-check budget execution and inflation factors. Company filings, parliamentary budget bills, and press archives on Dow Jones Factiva and D&B Hoovers filled gaps on contract values and contractor backlogs. Additional insights were drawn from trade bodies such as ANCE and UNRAIL. This list illustrates but does not exhaust the secondary sources used during data gathering and verification.

Market-Sizing and Forecasting

A top-down build started with government capital-budget allocations and EU co-financing, which are then aligned to historic utilization rates and shifted into constant-price euros before being converted to USD. Select bottom-up checks, supplier roll-ups and sampled contract award values, fine-tuned totals. Key drivers inside the multivariate regression include PNRR disbursement cadence, FS Group rail CAPEX, cement and labor cost indices, and PPP tender backlog. Forecasts extend to 2030, with scenario bands reflecting material-cost inflation and permitting delays.

Data Validation and Update Cycle

Outputs pass a three-step review: automated variance scans versus past series, analyst peer checks, and research-manager sign-off. Reports refresh each year; interim updates trigger when funding revisions or mega-project awards move the baseline materially.

Why Our Italy Transportation Infrastructure Construction Baseline Commands Reliability

Published figures often diverge because firms choose different asset scopes, currency treatments, and refresh intervals. According to Mordor Intelligence, disciplined source screening and annual recalibration keep our baseline firmly anchored to official budgets and on-ground progress.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.22 B (2025) | Mordor Intelligence | - |

| USD 22.60 B (2024) | Regional Consultancy A | Narrows scope to direct construction spend, excludes major maintenance; applies static exchange rate |

| USD 52.78 B (2023) | Trade Journal B | Bundles utilities and long-term commitments with construction outlays; model updated less frequently |

These comparisons show that when scope inflation or omission occurs, estimates shift widely. Our balanced top-down and bottom-up approach, refreshed each year, offers decision-makers a transparent figure they can trace back to clearly published variables.

Key Questions Answered in the Report

What is the current size of the Italy transportation infrastructure construction market?

The market is valued at USD 20.09 billion in 2026 and is forecast to hit USD 25.05 billion by 2031.

What is the expected growth rate of Italy’s transportation infrastructure construction sector?

The market is projected to expand at a 4.52% CAGR between 2026 and 2031.

Which segment leads the Italy transportation infrastructure construction market?

Roadways dominate with 48.40% market share in 2025, while railways register the fastest 5.05% CAGR through 2031.

How much public funding is backing Italy’s infrastructure pipeline?

The National Recovery and Resilience Plan provides USD 211.9 billion, complemented by EU Connecting Europe Facility grants worth USD 7.63 billion in 2024.

Which city shows the highest growth potential for transport infrastructure projects?

Turin posts the fastest regional expansion at a 5.62% CAGR, driven by the Lyon-Turin Base Tunnel and Liguria-Alps high-speed rail link.

Who are the top players shaping Italy’s transportation infrastructure market?

Webuild Group, Ferrovie dello Stato Italiane (Italferr), Salini Impregilo, Astaldi, and Ghella collectively control around 45% of contract value, indicating a moderately consolidated landscape.

Page last updated on: