Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

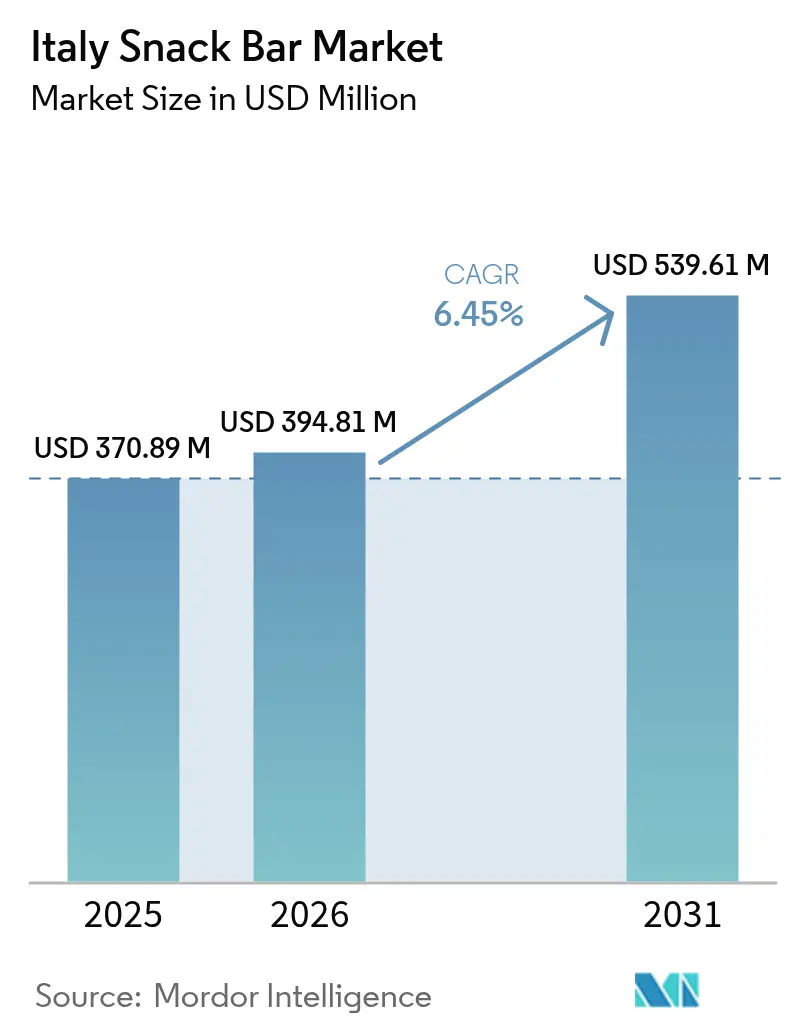

| Base Year Market Size (2025) | USD 370.89 Million |

| Market Size (2026) | USD 394.81 Million |

| Market Size (2031) | USD 539.61 Million |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

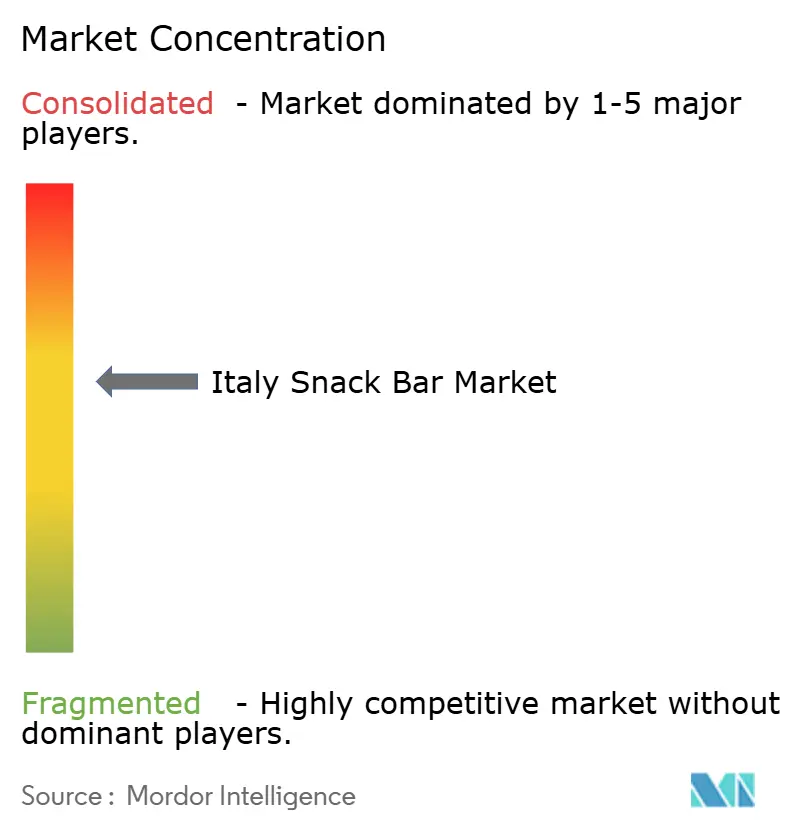

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Snack Bar Market Analysis by Mordor Intelligence

The Italy snack bar market size was valued at USD 370.89 million in 2025 and estimated to grow from USD 394.81 million in 2026 to reach USD 539.61 million by 2031, at a CAGR of 6.45% during the forecast period (2026-2031). Strong category gains in Italy reflect rising demand for quick, nutritious options, the broader retail reach of premium bars, and the proliferation of products fortified with proteins, fibers, and botanicals. While cereal bars still dominate, protein, fruit, and date-based variants are rapidly narrowing the gap as gym culture expands and on-the-go eating becomes routine in urban areas. Mainstream grocers are protecting margins by allocating more shelf space to higher-priced bars, while online health-and-wellness retailers are expanding assortments faster than physical stores can match. Despite sluggish overall grocery volumes across Southern Europe, snack bars continue to outpace the market, driven by the fact that nearly half of Gen Z shoppers now prioritize nutrition when making purchase decisions.

Key Report Takeaways

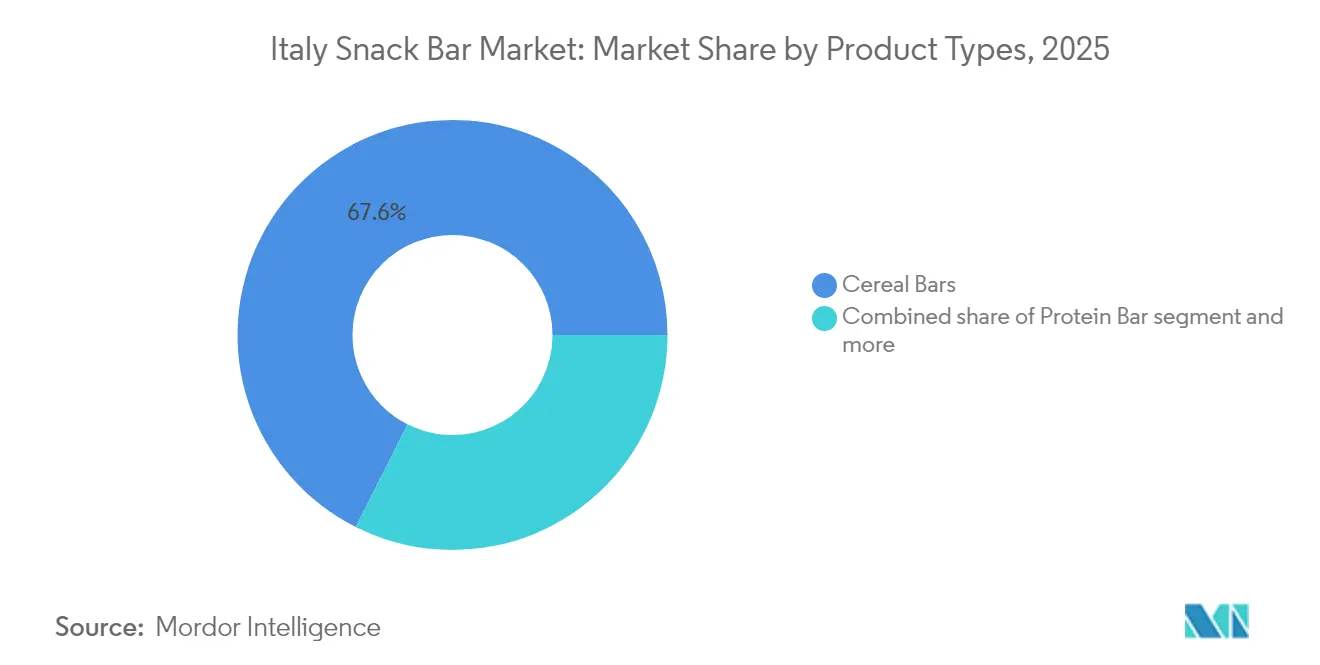

- By product type, cereal bars led with 67.58% revenue share in 2025, while protein bars are forecast to register an 8.31% CAGR through 2031.

- By ingredient base, granola and oat-based formulations captured 38.12% of the Italy snack bar market share in 2025; date-based alternatives are projected to expand at a 8.89% CAGR to 2031.

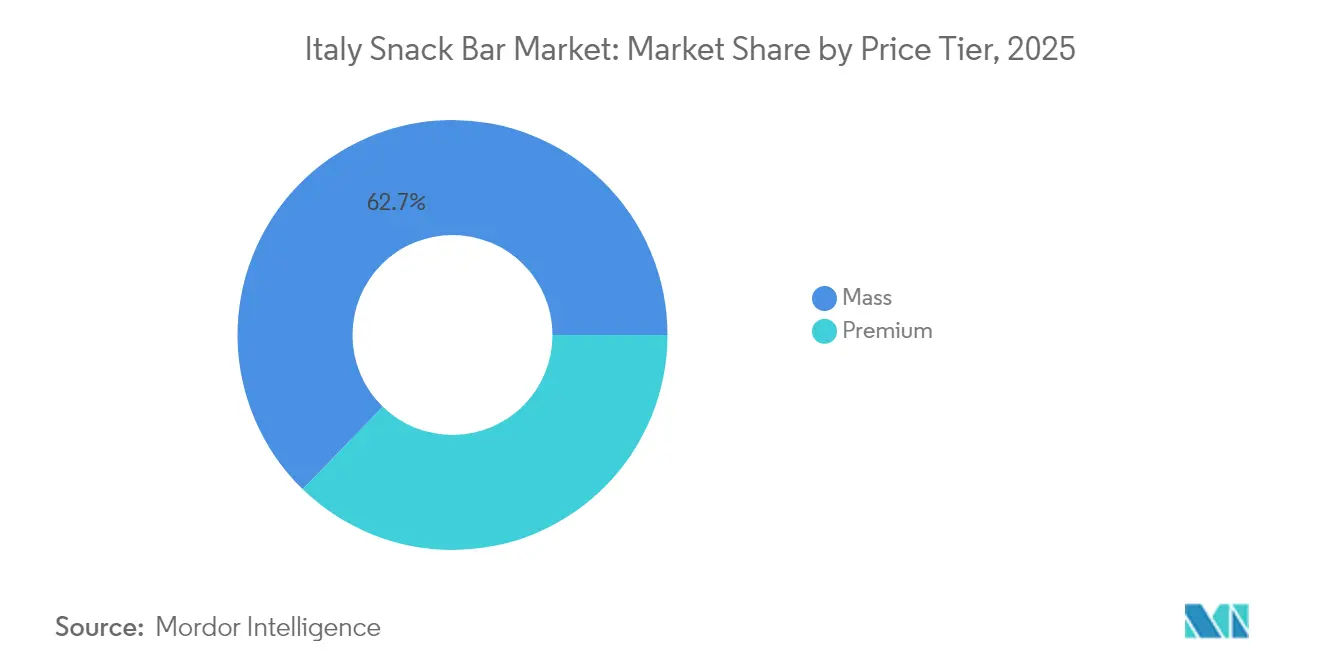

- By price tier, the mass segment accounted for 62.74% of the Italian snack bar market size in 2025, and premium offerings are expected to advance at an 8.55% CAGR through 2031.

- By distribution, supermarkets and hypermarkets accounted for 43.01% of the 2025 value; however, online sales are projected to rise at a 9.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious snacking culture | +1.2% | Milan, Rome, Turin, Bologna | Medium term (2-4 years) |

| Growing demand for on-the-go convenience | +1.4% | Milan, Rome, Naples; commuter corridors | Short term (≤ 2 years) |

| Retail channel premium-space expansion | +0.9% | National; led by Northern banners Conad, Coop, Esselunga | Medium term (2-4 years) |

| Product innovation in functional ingredients | +1.1% | National; early uptake in pharmacy channels | Medium term (2-4 years) |

| Expansion of functional and fortified foods | +0.8% | National; spill-over from sports nutrition | Long term (≥ 4 years) |

| Popularity of functional and nutritional bars | +1.0% | Urban, fitness-oriented demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health-Conscious Snacking Culture

Italian consumers are shifting toward nutrient-dense snacking, driven by a growing awareness of the importance of protein intake and the benefits of micronutrient fortification. The country’s protein product market reached EUR 2 billion, with demand increasing 8.4% in 2023 and supply expanding by 11%, signaling intense competition among manufacturers to capture this shift (GS1 Italy)[1]Source: “Italian Grocery Market Report 2024,” GS1 Italy, gs1it.org. For snack bar makers, this means that formulations must clearly communicate functional benefits, from protein per serving to vitamin fortification, to convert health-motivated intent into actual purchases. Ingredient innovation is accelerating: Ingredion’s VITESSENCE Pea 100 HD, an 84% protein pea isolate that keeps cold-pressed bars soft without refrigeration, exemplifies how brands must balance clean-label expectations with texture performance. While 48% of Italian households purchased snack bars in 2024, the purchase frequency remains at just 5 occasions per year, indicating that habitual consumption is still emerging (GS1 Italy).

Growing Demand for On-the-Go Convenience

Urbanization and commuter lifestyles are reshaping Italian meal occasions, with monthly ready-to-eat purchases now commonplace compared to negligible levels a decade ago. This shift is most evident in proximity retail, where Conad’s TuDay convenience stores experienced a 5.8% growth in 2024, reflecting the rising demand for grab-and-go solutions near transit hubs and office districts. Snack bars are well-positioned to serve breakfast-skipping professionals and mid-afternoon energy needs, especially as only 39% of adults meet daily fruit and vegetable intake guidelines, creating a nutritional gap that fortified bars can help fill, according to the Italian Ministry of Health[2]Source: “IV SCAI Dietary Survey Results,” Italian Ministry of Health, salute.gov.it. The main barrier is Italy’s enduring preference for sit-down espresso and cornetto breaks, particularly in northern cities. Ferrero’s May 2025 launch of Eat Natural, priced at EUR 3.59–3.79 for a 3-pack, directly targets this occasion by emphasizing fruit-and-nut content aligned with traditional Italian snacking habits while offering portability for modern routines.

Retail Channel Premium-Space Expansion

Modern retailers are dedicating expanded shelf space to premium snack bars, recognizing that these products deliver higher per-unit margins than traditional biscuits and wafers. Conad, Italy's largest retail cooperative with EUR 21.1 billion in 2024 turnover, increased private-label penetration to 33.7% and is investing in specialist channels that generated EUR 1.2 billion in revenue[3]Source: “Conad Annual Report 2024,” Conad, conad.it. Despar's Free From line grew 20.2% in value during 2024, while its Enjoy food-to-go range expanded 24.9%, demonstrating that retailers are curating assortments around functional and convenience attributes. This premiumization is also evident in the pharmacy and parapharmacy channel, where Talea Group's Farmaè platform lists 143 snack bar SKUs, including 46 from Enervit and 35 from Namedsport, with prices ranging from EUR 1.60 to EUR 6.55 per bar Farmaè. Talea Group reported EUR 83.4 million in first-half 2024 revenues and acquired VitaminCenter and Best Body in 2023-2024 to consolidate its leadership in health and wellness e-commerce. The strategic implication is that snack bar brands must secure premium shelf placement and pharmacy distribution to access health-motivated consumers willing to pay between EUR 17.93 and EUR 37.80 per kilogram, well above mass-market pricing, according to Farmaè.

Product Innovation in Functional Ingredients

Manufacturers are embedding functional ingredients, such as plant-based proteins, prebiotic fibers, and adaptogenic botanicals, to differentiate products and justify premium pricing. Cereal Docks developed Heliapro, a sunflower protein flour with approximately 50% protein content, offering a non-allergenic alternative to soy and pea proteins for bar formulations. EFSA approved partially hydrolyzed barley and rice protein as a novel food ingredient for cereal bars at concentrations up to 30 grams per 100 grams in July 2024, expanding formulation options for high-protein bars targeting sports nutrition consumers[4]Source: “Novel Food Approvals and Health Claims Assessments,” European Food Safety Authority, efsa.europa.eu. Vitavigor launched its VitaPro protein snack line in 2024, leveraging Italian consumer preference for locally produced functional foods. The challenge lies in navigating EFSA's health claims framework, which imposes a 5-month assessment timeline and has recently rejected claims for spinach extract (February 2025) and isomaltulose energy benefits (July 2024), underscoring the regulatory friction that slows time-to-market for novel formulations. Brands that invest in substantiating claims through clinical trials and aligning with approved nutrient profiles will gain a durable advantage, particularly as the European Parliament's January 2024 resolution calls for mandatory front-of-pack labeling and stricter nutrient profiles to restrict health claims on high-fat, high-sugar, or high-salt products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong preference for traditional Italian snacks | -0.8% | National, most pronounced in Southern Italy and rural areas | Long term (≥ 4 years) |

| Premium pricing limits mass adoption | -0.6% | National, acute in Southern Italy and lower-income households | Short term (≤ 2 years) |

| Regulatory compliance for functional claims | -0.3% | EU-wide, affects all manufacturers seeking health claims | Medium term (2-4 years) |

| Low penetration outside major cities | -0.5% | Rural Italy, towns with <50,000 population | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Preference for Traditional Italian Snacks

Italian consumers exhibit deep-rooted loyalty to biscotti, cornetti, and other baked goods that anchor breakfast and mid-morning rituals, limiting the addressable market for snack bars. The IV SCAI dietary survey found that 79% of Italians consume pasta daily (averaging 49 grams per day) and bread consumption averages 70 grams per day, reflecting a carbohydrate-centric food culture that prioritizes familiar textures and flavors according to the Italian Ministry of Health. This preference is most entrenched in Southern Italy and rural areas, where modern retail penetration is limited and traditional bakeries maintain strong community ties. Ferrero's strategy of launching Eat Natural bars with fruit and nut profiles in May 2025 acknowledges this cultural barrier by mimicking the ingredient composition of traditional Italian snacks while delivering portability. The Italian fruit and dried-fruit bar segment's 34% growth since 2022 suggests that formulations emphasizing whole-food ingredients can bridge the gap between tradition and convenience, as per Ferrero. However, the fact that only 48% of Italian households purchased snack bars in 2024, with an average frequency of 5 occasions per year, underscores that habitual consumption remains elusive according to GS1 Italy. Brands must invest in consumer education and occasion-based marketing to reposition snack bars as complements to, rather than replacements for, traditional snacks.

Premium Pricing Limits Mass Adoption

Snack bars command price points between EUR 1.89 and EUR 6.55 per unit, translating to EUR 17.93 to EUR 37.80 per kilogram, which is 2 to 4 times the cost of traditional biscuits and wafers as per Farmaè. This pricing gap is particularly acute in a market where 75% of consumers prioritize affordability, and discount channels expanded to 23% market share in the first half of 2024, according to GS1 Italy. Food inflation widened price disparities across Italian provinces in 2024, compressing discretionary spending on premium snacks. Private-label snack bars, which account for 38.2% of the market share by volume, offer a lower-cost entry point but often lack the functional ingredient differentiation that justifies premium pricing, according to GS1 Italy. Ferrero's Eat Natural pricing of EUR 3.59 to EUR 3.79 for a 3-pack positions the brand in the mid-premium tier, striking a balance between accessibility and quality perception. Manufacturers targeting mass adoption must either reduce per-unit costs through economies of scale or develop smaller portion sizes (e.g., 20-gram mini-bars) that lower absolute price points while maintaining per-kilogram margins. The mass tier's 63.48% share in 2024 indicates that affordability remains the dominant purchase driver, even as the premium segment grows at 8.97% CAGR through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cereal Bars Anchor Market, Protein Bars Drive Growth

Cereal bars held 67.58% of Italy’s snack bar market in 2025, reflecting their strong alignment with Italian breakfast habits and established placement in supermarkets and hypermarkets. Granola and muesli bars dominate this segment through whole-grain positioning and clean-label appeal, while breakfast cereal bars attract consumers seeking portable alternatives to traditional cornetti. Meanwhile, protein bars are projected to expand at an 8.31% CAGR through 2031, driven by fitness-oriented shoppers and the broader growth of the Italian protein product market. Mondelēz introduced Grenade in October 2024 and partnered with AC Milan to enhance its credibility in the sports nutrition sector.

Fruit and nut bars are also gaining traction, with consumers gravitating toward whole-food formats and natural sweetness. The Italian fruit and dried-fruit bar category is projected to reach EUR 74 million in 2024, marking 34% growth since 2022. Ferrero’s May 2025 launch of Eat Natural, priced at EUR 3.59–3.79 for a 3-pack, exemplifies this positioning through its emphasis on fruit and nut ingredients that resonate with traditional Italian snacking preferences. Beyond these segments, energy bars and meal-replacement bars continue to serve niche needs such as endurance sports and weight management, with the Italian energy bar market reaching EUR 79 million in 2024. Ingredient innovation is accelerating as well: Ingredion’s VITESSENCE Pea 100 HD (an 84% protein pea isolate suited for cold-pressed bars) supports clean-label, high-protein formulations, while EFSA’s July 2024 approval of partially hydrolyzed barley and rice protein, permitting use up to 30 g per 100 g in cereal bars, broadens formulation possibilities for next-generation protein products.

By Ingredient Base: Oat Dominance Meets Date-Based Innovation

Granola and oat-based bars captured 38.12% of the Italian snack bar market in 2025, supported by strong consumer familiarity with oats as a wholesome breakfast staple and their versatility in binding fruits, nuts, and natural sweeteners. Oats also provide beta-glucan soluble fiber, enabling digestive-health claims under EFSA guidelines and giving manufacturers a regulatory edge in functional positioning. Meanwhile, date-based bars are expanding at a 8.89% CAGR through 2031, propelled by clean-label demand and the preference for whole-food sweeteners over refined sugars. Dates deliver natural sweetness, fiber, and micronutrients such as potassium and magnesium, while their sticky texture eliminates the need for binders like glucose syrup or maltodextrin. Nut-based bars, featuring almonds, cashews, and hazelnuts, cater to premium shoppers seeking protein, healthy fats, and indulgent flavor profiles, often retailing above EUR 5.00 per unit in specialty and pharmacy channels.

Dairy- and protein-based bars, which utilize whey, casein, or plant-based proteins, continue to target fitness and sports nutrition consumers. Ingredient innovation is accelerating, exemplified by Cereal Docks’ Heliapro sunflower protein flour (≈50% protein), which offers a non-allergenic alternative to soy and pea proteins and helps manufacturers navigate allergen-labeling sensitivities. Hybrid formulations that combine oats, nuts, dates, and protein isolates are also gaining traction as brands seek to balance taste, texture, nutrition, and cost. Vitavigor’s VitaPro protein snack line, launched in 2024, embodies this blended approach using Italian-sourced ingredients alongside functional protein fortification. Additionally, bases such as rice crisps, quinoa, and ancient grains support niche segments, including gluten-free and allergen-conscious consumers, evidenced by Despar’s Free From line, which grew 20.2% in value in 2024.

By Price Tier: Mass Dominance Coexists with Premium Acceleration

The mass tier captured 62.74% of market share in 2025, reflecting Italian consumers' price sensitivity and the dominance of private-label offerings. Discount channels expanded to 23% of the total grocery market share in the first half of 2024, up from 19% in 2019, as food inflation compressed discretionary spending, according to GS1 Italy. Mass-tier snack bars, priced between EUR 1.60 and EUR 2.50 per unit, compete primarily on affordability and are distributed through supermarkets, hypermarkets, and discount chains such as Lidl, Aldi, and Eurospin. Conad, with EUR 21.1 billion in 2024 turnover and 33.7% private-label penetration, exemplifies the mass-tier strategy by offering own-brand cereal and granola bars at price points 20% to 30% below branded equivalents. Premium bars are projected to grow at an 8.55% CAGR through 2031, driven by functional ingredient differentiation, protein fortification, and specialty distribution in pharmacies, parapharmacies, and online channels.

Ferrero's Fulfil and Eat Natural launches in 2024 and May 2025, priced at EUR 3.59 to EUR 3.79 per 3-pack, position the brands in the mid-premium tier, balancing accessibility with quality perception. Pharmacy and parapharmacy channels, where Talea Group's Farmaè platform lists 143 snack bar SKUs with prices ranging from EUR 1.60 to EUR 6.55 per bar, serve as a critical distribution avenue for premium products targeting health-motivated consumers. Talea Group reported EUR 83.4 million in first-half 2024 revenues and acquired VitaminCenter and Best Body in 2023-2024 to consolidate its health and wellness e-commerce leadership. Premium bars command per-kilogram pricing between EUR 17.93 and EUR 37.80, which is 2 to 4 times the cost of mass-tier alternatives, limiting penetration to affluent urban households and fitness-oriented demographics. The strategic implication is that brands must segment portfolios across price tiers, using mass-tier offerings to build household penetration while reserving premium SKUs for high-margin specialty channels.

By Distribution Channel: Supermarkets Lead, Online Accelerates

Supermarkets and hypermarkets accounted for 43.01% of market share in 2025, anchored by their broad geographic footprint, extensive shelf space, and ability to stock both mass and premium SKUs. Italy's 25,122 grocery shops include 34% supermarkets and 23% discount stores, with density concentrated in Lombardia, Campania, Lazio, and Sicily. Conad, Italy's largest retail cooperative with EUR 21.1 billion in 2024 turnover, exemplifies the supermarket channel's dominance, leveraging private-label penetration of 33.7% and specialist channels generating EUR 1.2 billion in revenue. Online stores are expanding at a 9.28% CAGR through 2031, driven by digital grocery penetration that reached EUR 4.6 billion in 2024, representing 6% of total grocery sales according to GS1 Italy. Talea Group's Farmaè platform, with 1.09 million active customers in 2023 and EUR 83.4 million in first-half 2024 revenues, demonstrates the online channel's potential for distributing premium snack bars.

Convenience stores, which represent 42% of Italy's 25,122 grocery shops, are crucial for on-the-go purchases. According to Savills and Conad, Conad's TuDay proximity format grew by 5.8% in 2024. Specialty stores, including health food retailers, organic shops, and sports nutrition outlets, serve as curated distribution points for premium and functional bars, with Despar's Free From line. Other distribution channels encompass pharmacy and parapharmacy, where Enervit lists 46 SKUs and Namedsport offers 35 SKUs, with prices ranging from EUR 1.60 to EUR 6.55 per bar. Pharmacy distribution is particularly strategic for protein and functional bars, as consumers perceive these outlets as credible sources for health-oriented products. PepsiCo's distribution strategy in Italy combines direct-store-delivery, customer warehouses, third-party distributors, and e-commerce to maximize reach across urban and rural geographies.

Geography Analysis

Italy’s snack bar market exhibits strong geographic polarization, with consumption concentrated in northern urban hubs such as Milan, Turin, Bologna, and Verona. Higher disposable incomes, dense modern retail, and fitness-oriented lifestyles in these areas elevate demand for functional and premium products. Although Lombardia, Campania, Lazio, and Sicilia contain the highest density of Italy’s 25,122 grocery shops, Northern regions still lead in per-capita consumption due to faster adoption of on-the-go eating patterns (Savills). This regional divergence highlights how snack bars are gaining market share from traditional baked goods and impulse confectionery, particularly in commuter corridors and proximity formats, such as Conad’s TuDay stores, which expanded by 5.8% in 2024.

Southern Italy and rural areas exhibit lower penetration, constrained by entrenched preference for traditional snacks, lower disposable incomes, and limited modern retail infrastructure. The IV SCAI dietary survey found that only 39% of Italian adults meet the daily fruit and vegetable intake recommendations. Pasta consumption averages 49 grams per day among 79% of the population, and bread consumption averages 70 grams per day, reflecting a carbohydrate-centric food culture that prioritizes familiar textures and flavors, as noted by the Italian Ministry of Health. Approximately 48% of Italian households purchased snack bars in 2024, with an average frequency of only 5 occasions per year, indicating that habitual consumption has not yet taken root outside major urban centers according to GS1 Italy. Ferrero's dual launch of Fulfil protein bars in 2024 and Eat Natural fruit bars in May 2025 targets this geographic divide by offering protein-focused SKUs for Northern fitness consumers and fruit-based formulations that resonate with Southern traditional snacking preferences.

Rome and Naples, as major Southern metropolitan areas, represent intermediate markets where modern retail is expanding but traditional bakeries retain strong community ties. Private-label snack bars offer a lower-cost entry point that is critical for penetrating Southern households. Online grocery represents 6% of total grocery sales, provides a geographic equalizer by enabling rural and Southern consumers to access premium and specialty snack bars without relying on local retail availability aas per the GS1 Italy. Talea Group's Farmaè platform, with 1.09 million active customers in 2023 and EUR 83.4 million in first-half 2024 revenues, demonstrates the online channel's potential to bridge geographic distribution gaps.

Competitive Landscape

The Italian snack bar market exhibits moderate concentration, with multinational incumbents, such as Kellogg (Kellanova), Ferrero, Nestlé, General Mills, and PepsiCo, operating alongside nimble local specialists, including Enervit, Probios, Valsoia, and Pedon. Ferrero’s aggressive expansion, exemplified by the 2024 launch of Fulfil protein bars and the May 2025 introduction of Eat Natural fruit bars, illustrates how scale players leverage distribution networks and brand equity to simultaneously capture functional and premium segments. Mondelēz’s October 2024 Grenade protein bar launch, supported by AC Milan sponsorship, underscores intensifying competition as global confectionery and snack conglomerates target Italy as a strategic hub for functional snacking in Southern Europe. Market consolidation is poised to deepen further with Mars’ pending USD 35.9 billion acquisition of Kellanova, expected in H1 2025, pending EU antitrust approval, which is likely to trigger portfolio rationalization and distribution synergies.

White-space opportunities persist in date-based bars, which are growing at 9.26% CAGR through 2030, yet remain underrepresented in mainstream supermarket assortments, and in pharmacy and parapharmacy channels, where Talea Group's Farmaè platform lists 143 snack bar SKUs but only 2 major brands (Enervit with 46 SKUs and Namedsport with 35 SKUs) dominate. Emerging disruptors include Italian specialists such as Vitavigor, which launched its VitaPro protein snack line in 2024, and ingredient innovators such as Cereal Docks, which developed Heliapro sunflower protein flour with approximately 50% protein content to offer a non-allergenic alternative to soy and pea proteins.

Technology adoption is accelerating shifts in competitive dynamics as retailers deepen omnichannel integration and digital capabilities. Conad’s investment in its HeyConad app exemplifies this push, while AI-driven assortment optimization tools and mobile-commerce solutions showcased at Forum Retail 2024 signal an industry-wide move toward data-enabled retail execution. Private-label penetration reached 38.2% of total volume in 2024, with Conad attaining 33.7% private-label share, Despar surpassing EUR 1 billion in private-label sales (23.9% share and aiming for 25%), and Crai offering 2,700 private-label SKUs with a target of roughly 40% share by 2027 (GS1 Italy; Conad; Despar). This rapid private-label expansion continues to compress branded players’ pricing power and compels them to differentiate via functional ingredients, clinically substantiated claims, and innovation that can support premium price points despite intensifying competition.

Italy Snack Bar Industry Leaders

-

Kellogg Company

-

Ferrero Group

-

Nestlé S.A.

-

General Mills Inc.

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ferrero launched Eat Natural fruit and nut bars in Italy, priced at EUR 3.59 to EUR 3.79 per 3-pack of 40-gram bars, targeting the Italian fruit and dried-fruit bar segment, valued at EUR 74 million in 2024 and growing at a 34% rate since 2022. This launch complements Ferrero's 2024 introduction of Fulfil protein bars and leverages the company's acquisition of Nutrisun to strengthen bar production capacity.

- October 2024: Mondelēz International entered the Italian protein bar market with its Grenade brand, sponsoring AC Milan to build credibility among sports nutrition consumers.

- August 2024: Mars announced the acquisition of Kellanova for USD 35.9 billion, with closure expected in the first half of 2025 pending EU antitrust clearance. Kellanova operates Kellogg Italia S.p.A. and owns brands including Nutri-Grain, Special K, and RXBAR, positioning Mars to consolidate its presence in the Italian snack bar market.

Italy Snack Bar Market Report Scope

Snack bars are ready-to-eat, portable products designed to provide convenience and nutrition for on-the-go consumption. The Italy snack bar market, by product type, is segmented into cereal bars, protein bars, fruit & nut bars, and other snack bars. Cereal bars are further categorized into granola/muesli bars and breakfast/other cereal bars. By ingredient base, the market is classified into nut-based bars, granola/oat-based bars, date-based bars, dairy/protein-based bars, hybrid blends combining multiple ingredients, and other ingredient bases. In terms of price tier, the market is divided into mass and premium segments. By distribution channel, snack bars are sold through supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other channels.

By Product Type

| Cereal Bars | Granola / Muesli Bars |

| Breakfast / Other Cereal Bars | |

| Protein Bars | |

| Fruit & Nut Bars | |

| Other Snack Bars |

Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

| By Product Type | Cereal Bars | Granola / Muesli Bars |

| Breakfast / Other Cereal Bars | ||

| Protein Bars | ||

| Fruit & Nut Bars | ||

| Other Snack Bars | ||

| Ingredient Base | Nut-based bars | |

| Granola/Oat-based | ||

| Date-based | ||

| Dairy/Protein-based | ||

| Hybrid blends | ||

| Other | ||

| By Price Tier | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Stores | ||

| Other Distribution Channels |

Key Questions Answered in the Report

How large is Italy’s snack bar market in 2026?

The Italy snack bar market size reached USD 394.81 million in 2026 and is set to climb toward USD 539.61 million by 2031.

Which product type sells the most?

Cereal bars command 67.58% of 2025 value, reflecting Italian breakfast preferences.

What is driving protein bar growth?

Fitness culture and sports sponsorships are pushing protein bars toward an 8.31% CAGR through 2031.

Where are premium bars mainly sold?

Premium SKUs gain visibility in pharmacies, parapharmacies, and online platforms such as Farmaè.

Page last updated on: