Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.27 Billion |

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 6.95 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

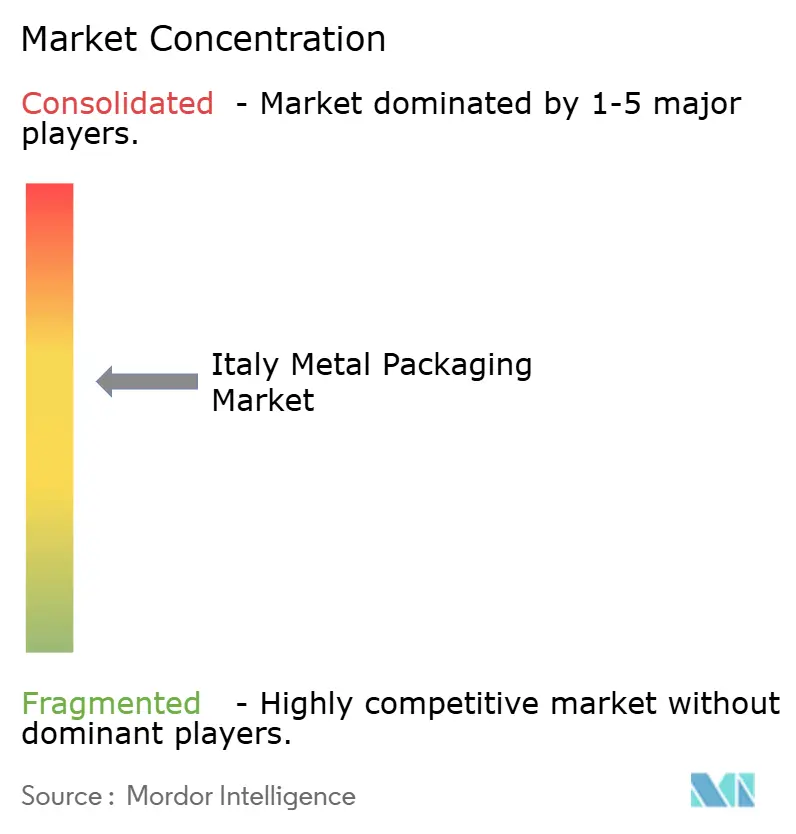

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Metal Packaging Market Analysis by Mordor Intelligence

The Italy metal packaging market size was valued at USD 5.27 billion in 2025 and estimated to grow from USD 5.52 billion in 2026 to reach USD 6.95 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Sustained growth rests on the nation’s robust export-oriented food and beverage industries, tightening European recycling rules and steady adoption of advanced digital printing technologies. Aluminum keeps its dominance through lightweight, high-barrier performance, while steel gains momentum as industrial users seek durable bulk packaging. Domestic craft brewers and cosmetics producers encourage shorter production runs and premium decoration, allowing suppliers to charge higher margins. Simultaneously, raw material price swings and energy costs challenge competitiveness, pushing manufacturers toward secondary metal sourcing and energy-efficient processes.

Key Report Takeaways

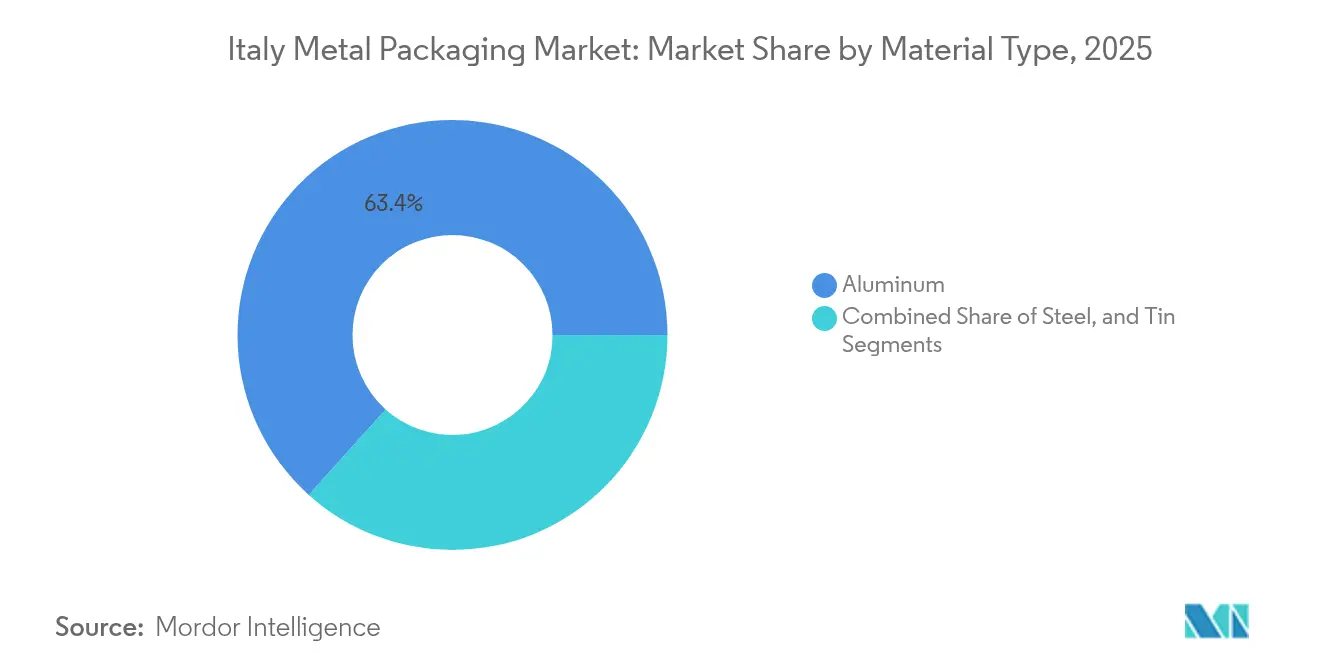

- By material type, aluminum commanded 63.35% of Italy metal packaging market share in 2025, whereas steel is projected to expand at a 5.63% CAGR through 2031.

- By product type, cans retained a 39.65% revenue share in 2025, while bulk containers are anticipated to grow at a 4.86% CAGR to 2031.

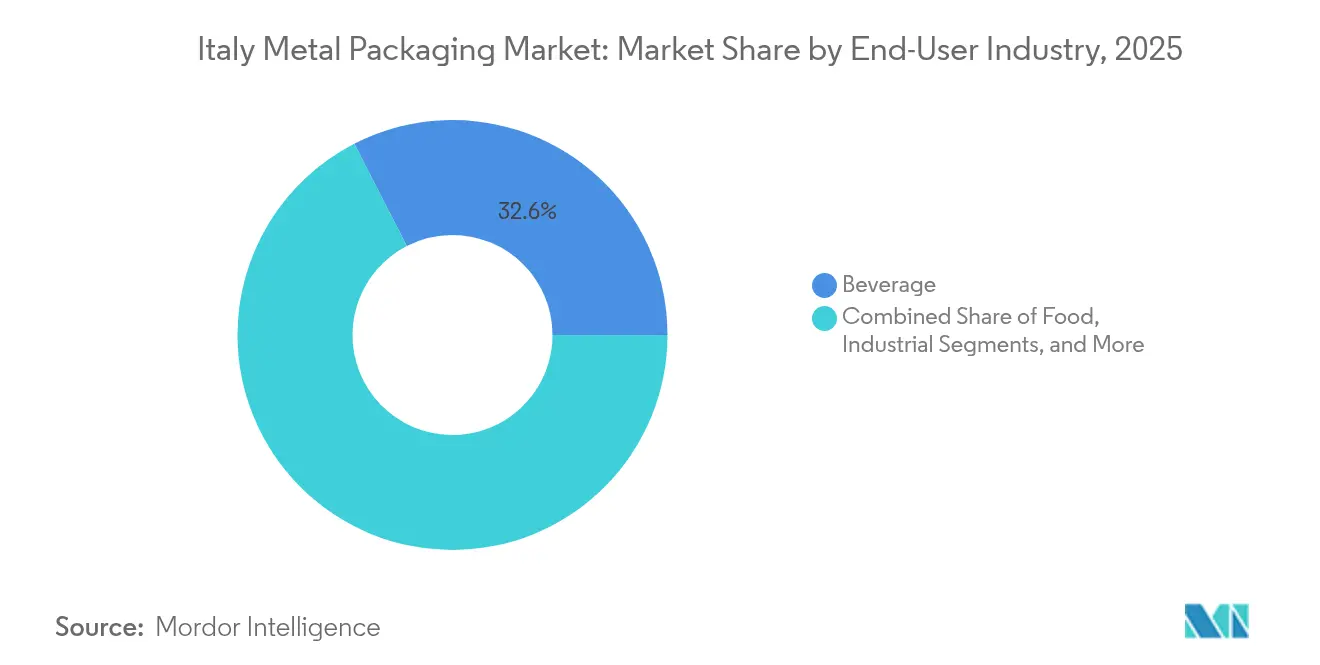

- By end-user industry, beverages led with 32.55% share of Italy metal packaging market size in 2025 and the industrial segment is advancing at a 5.55% CAGR through 2031.

- By coating type, epoxy phenolic accounted for 45.60% Italy metal packaging market share in 2025, whereas BPA-free systems are forecast to post a 5.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Ready-to-Eat Food Consumption | +1.2% | National – Northern industrial corridors | Medium term (2-4 years) |

| Growing Craft Beverage Production in Italy | +0.9% | National – clusters in Lombardy, Veneto, Piedmont | Short term (≤ 2 years) |

| Mandatory EU Recycling Targets for Metal | +0.8% | EU-wide – compliance driven in Italy | Long term (≥ 4 years) |

| Rising Demand for Aerosol Personal-Care Products | +0.7% | National – export-oriented manufacturing | Medium term (2-4 years) |

| Advanced Digital Printing on Metal Packaging | +0.5% | Global – Italy technology adoption | Medium term (2-4 years) |

| Expansion of Italian Export-Oriented Gourmet Foods | +0.6% | National production – global distribution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Ready-to-Eat Food Consumption

Ready-to-eat meals remain popular with urban households that value convenience and portion control. Frozen goods hit 1.02 million t and EUR 5.8 billion (USD 6.4 billion) turnover in 2024, while processed vegetable exports rose to EUR 2.5 billion (USD 2.7 billion). Metal cans ensure a long shelf life for these premium items, thereby protecting the brand's reputation in distant markets. E-commerce adds momentum because rigid cans withstand parcel handling better than flexible films. As Italian producers increasingly sell to regions with less-reliable logistics, barrier integrity becomes a non-negotiable purchase criterion. The trend also accelerates demand for smaller metal formats that suit single-person households.

Growing Craft Beverage Production in Italy

The country counted 1,326 craft breweries with 17.6 million hl output valued at EUR 10.2 billion (USD 11.2 billion) in 2024. Artisanal brewers overwhelmingly favor aluminum cans for light protection and shipping efficiency. Digital printing enables colorful graphics in low volumes, aligning with limited-edition releases. The craft spirits niche follows a similar path, placing small-batch gin or amaro in sleek metal bottles designed for export. Northern clusters benefit from proximity to can makers, shortening lead times. Because brand storytelling matters to independent brewers, suppliers offering rapid design changes gain a competitive edge.

Mandatory EU Recycling Targets for Metal

The Packaging and Packaging Waste Regulation pushes Italy toward a 90% metal recycling rate by 2030.[1]European Commission, “Packaging and Packaging Waste Regulation,” European Commission, ec.europa.eu Local recovery already stands near 85%, but meeting the goal calls for expanded collection schemes and eco-design adjustments such as lightweighting and mono-material structures. Infinite recyclability lets aluminum and steel outshine multilayer plastics in a circular economy narrative. Producers that integrate high post-consumer recycled content can access green financing incentives. The directive also tilts export competitiveness in favor of Italian suppliers who achieve compliance ahead of schedule, especially for premium food brands sold across Europe.

Rising Demand for Aerosol Personal-Care Products

Italian cosmetics revenue climbed to EUR 16.5 billion (USD 18.2 billion) in 2024 with exports near EUR 8.0 billion (USD 8.8 billion). Metal aerosol cans deliver controlled dispensing and long shelf life essential for high-end formulations. Lightweight aluminum reduces freight costs for Asia-bound shipments, boosting brand margins. Consumers also prefer metal because of higher recycling rates compared with plastic propellant containers. Technology upgrades in valves and actuators allow finer spray patterns, supporting premium positioning. Limited-run decorations, achievable via digital printing, further cement metal as the package of choice for luxury personal-care lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Volatility of Primary Aluminum | −0.8% | Global supply chains affecting Italian manufacturers | Short term (≤ 2 years) |

| Consumer Shift Toward Lightweight Plastics in Paints | −0.4% | National – industrial applications | Medium term (2-4 years) |

| Regulatory Uncertainty Around BPA Substitutes | −0.3% | EU-wide – Italy compliance requirements | Long term (≥ 4 years) |

| High Initial Capital for Metal Can Manufacturing | −0.5% | National – new market entrants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Volatility of Primary Aluminum

Primary aluminum prices swung 15-20% during 2024 amid energy shocks and geopolitical strains. Italy imports roughly 95% of its ingots, exposing converters to exchange-rate risk and freight surcharges. Although Hydro invested EUR 14.8 million (USD 16.3 million) to lift Atessa’s recycling capacity by 10,000 t yr⁻¹,[2]Hydro, “Hydro Invests EUR 14.8 Million in Atessa Recycling Facility,” Hydro, hydro.com food-grade scrap remains scarce. Producers hedge with long-term contracts yet still face margin compression. The volatility briefly prompts some buyers to consider steel or composite solutions for non-critical uses, tempering near-term growth in aluminum cans.

Consumer Shift Toward Lightweight Plastics in Paints

DIY paint buyers choose plastic pails for easy handling, cutting into metal demand in value ranges. While professional coatings still rely on steel for chemical resistance, mainstream emulsion paint makers increasingly offer polymer tubs that weigh less and lower logistics costs. Italian suppliers respond by designing thinner-wall steel cans fitted with ergonomic handles, attempting to retain share. Nevertheless, the convenience appeal of plastics in retail paint remains a headwind through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominates as Steel Gains Industrial Traction

Aluminum held 63.35% Italy metal packaging market share in 2025, mirroring its entrenched role in beverages and shelf-stable foods. Steel, however, is poised for a 5.63% CAGR on the back of drum, pail, and IBC demand from automotive fluids, agrochemicals, and lubricants. Italy metal packaging market size, attributed to aluminum, is projected to approach USD 4.55 billion by 2031, while steel could surpass USD 2.05 billion. Aluminum’s growth stays tethered to increasing craft beer and energy drink production, but its high electricity intensity poses cost risks that favor closed-loop scrap systems. Steel benefits from Italy’s upstream coil capacity clustered around Lombardy, offering short lead times for industrial fillers.

Advanced coatings ensure both metals comply with EU food-contact regulations. BPA-free variants such as Accelshield 700 widen aluminum’s use in infant formula cans, whereas polyester-epoxy hybrids enable steel aerosol cans for solvent-heavy hair sprays. High recycled content targets-75% by 2030 for aluminum containers-encourage alloy optimization without sacrificing drawability. Simultaneously, lightweight steel designs using micro-alloying technologies lower gauge by up to 8%, helping industrial packers meet eco-tax thresholds. As procurement teams evaluate total cost of ownership, value propositions pivot on circularity credentials rather than upfront material price.

By Product Type: Bulk Containers Accelerate Beyond Core Can Formats

Cans retained 39.65% of the revenue in 2025 and remain the face of consumer-contact applications; yet, bulk containers are forecast to grow at a rate of 4.86% annually through 2031 as the export-heavy chemical and pharmaceutical industries scale. Within cans, sleek 250ml beverage formats are gaining favor among craft brewers seeking differentiation on crowded retail shelves. Meanwhile, Italy metal packaging market size generated by bulk containers could hit USD 1.14 billion by 2031, reflecting shifting industrial logistics. Rigid IBCs, tight-head drums, and large pails cater to the increasing volumes of lubricant blends associated with electric-vehicle part manufacturing.

Digital printing unlocks SKU proliferation for cans without prohibitive plate costs. Ball’s Dynamark platform, relaunched across EMEA, prints variable graphics at commercial speed, ideal for seasonal beer lines. Conversely, bulk container manufacturers focus on UN-certified designs, corrosion-resistant linings, and RFID tagging for supply chain transparency. Demand for aerosol cans also advances, buoyed by double-digit growth in sun-care sprays marketed to tourists in Southern Italy. Decorative tins for olive oil and confectionery maintain a small but stable niche, capitalizing on the nation’s gift-oriented gourmet culture.

By End-User Industry: Industrial Applications Emerge as Fastest Riser

Beverages represented 32.55% Italy metal packaging market share in 2025, yet the industrial segment’s 5.55% CAGR positions it as the leading growth engine. Automotive fluids, specialty chemicals, and process reagents lift orders for large-volume steel drums and pails. Italy’s manufacturing value added reached EUR 280 billion (USD 309 billion) in 2024, and industrial packagers increasingly specify tamper-proof closures and solvent-resistant linings. Italy metal packaging market size for industrial uses is likely to breach USD 1.64 billion by 2031.

Food remains a steady pillar, helped by rising exports of canned tomatoes, sauces, and legumes to North America and the Middle East. The pharmaceutical sub-segment leans on aluminum tubes and collapsible containers for topical ointments where sterility is paramount. Cosmetics, chasing premium positioning in Asia, order intricately decorated aerosols and metal jars that elevate shelf presence. As EU green deal policies reward circular packaging, metal’s recyclability strengthens procurement preferences across all sectors.

By Coating Type: BPA-Free Solutions Gain Speed Under Regulatory Spotlight

Epoxy phenolic systems delivered 45.60% revenue in 2025 owing to proven food safety and versatility, but BPA-free alternatives led growth at a 5.78% CAGR through 2031. Italy metal packaging industry moves swiftly to pre-empt future endocrine-disruptor restrictions. Italy metal packaging market size attributable to BPA-free coatings could approach USD 1.41 billion by 2031. Acrylic-silicone hybrids are favored in beverage ends that require flexibility, while waterborne polyesters help meet factory VOC caps.

R&D centers in Piedmont are working on tomato-pomace-derived resins that mimic traditional epoxy adhesion while eliminating bisphenol traces. Lighter coat weights save up to 1.5 g of metal per 330 ml can, trimming cost and carbon intensity. Coating suppliers train filler plants on line-speed adjustments necessary for new chemistries, ensuring seamless productivity. With the European Food Safety Authority poised to tighten specific migration limits, early adopters of validated BPA-free systems hold a marketing edge when exporting premium canned goods.

Geography Analysis

Northern Italy’s Lombardy, Veneto, and Piedmont account for nearly 70% of the country's production capacity, leveraging their proximity to automotive, chemical, and beverage hubs. These regions also host aluminum recyclers and coil coaters, creating a dense ecosystem of suppliers and technical laboratories. Central and Southern provinces contribute largely through agri-food processing, demanding robust cans for tomatoes, legumes, and seafood. Italy metal packaging market share tied to exports rose as food shipments reached EUR 47.4 billion (USD 52.1 billion) in 2024, underscoring packaging’s role in brand protection during maritime transit.

Cross-border logistics with Germany, France, and Switzerland provide a steady aftermarket for specialty drums and caps. Mediterranean sea lanes open routes to North Africa and the Middle East, where Italian olive oil and confectionery packed in decorative tins resonate with gift-giving traditions. Government incentives under the National Recovery and Resilience Plan channel EUR 2.1 billion (USD 2.3 billion) into recycling infrastructure and deposit-return pilots, further tipping the scales toward metal containers. Yet, elevated electricity prices relative to Scandinavia pressure electrolytic facilities, prompting renewed investments in rooftop solar at can plants in Emilia-Romagna.

Digital printing hubs in Veneto collaborate with German machinery builders, reinforcing Northern clusters as innovation testbeds. Meanwhile, small converters in Apulia focus on short-run tins for regional olive growers. The geographic dispersion cushions Italy metal packaging market from sector-specific downturns, enhancing resilience.

Competitive Landscape

The landscape is moderately consolidated, with the top three multinationals plus two domestic specialists capturing roughly 50% of national revenue. Ardagh Metal Packaging operates two high-speed beverage can lines, integrated with on-site end production, which secures economies of scale. Ball Corporation exploits its Dynamark platform to serve craft brewers seeking distinctive designs without large inventories. Crown Holdings differentiates through lightweight DWI technology suited to energy drinks exported across Europe.

Italian champions Gruppo ASA and Tecnocap excel in custom tins and metal closures for gourmet and personal care brands. Recent M&A shows a pivot to higher-margin niches: Omnia Technologies spent EUR 280 million (USD 309 million) assembling a beverage equipment powerhouse that now cross-sells filling and labeling systems to canners. Trivium Packaging Italy specializes in metal bottles for premium spirits, utilizing proprietary shaping methods.

Players race to decarbonize. Joint procurement of renewable electricity and trials of hydrogen-fired furnaces aim to cut scope 1 emissions 30% by 2028. Collaboration with coating suppliers on water-based chemistries enables quicker line changeovers, supporting short-run business models. Given these dynamics, market power rests with firms balancing global scale and local agility.

Italy Metal Packaging Industry Leaders

Ardagh Metal Packaging Italy S.r.l.

Ball Beverage Packaging Italia S.r.l.

Crown Packaging Manufacturing UK Limited – Italian Operations

Silgan Holdings Inc.

Gruppo ASA S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Italy’s Ministry of Ecological Transition earmarked EUR 2.1 billion (USD 2.44 billion) for circular economy projects, including metal deposit-return pilots.

- August 2025: The European Commission’s PPWR implementation began in Italy, prompting firms to strive for 90% recyclability by 2030.

- July 2025: A Buon Rendere coalition reported a 73% can-litter reduction in Milan pilot zones under deposit-return trials.

- June 2025: Italian metal packaging makers announced EUR 450 million (USD 522.36 million) sustainability investments through 2027.

Italy Metal Packaging Market Report Scope

Metal packaging, primarily crafted from aluminum or steel, encloses and safeguards various products, including food, beverages, personal care items, and chemicals. Its significance lies in its superior defense against light, air, and moisture, ensuring the preservation of product quality. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Italy Metal Packaging Market is segmented by materials type (Aluminum, and Steel), product type (Cans (Food Cans, Beverage Cans, Aerosol Cans), Bulk Containers, Shipping Barrels and Drums, and Caps and Closures and Other Product Types), end-user vertical (Beverage, Food, Paints, and Chemicals, Industrial and Other End-User Verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Aluminum |

| Steel |

| Tin |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Decorative Cans | |

| Bulk Containers | |

| Drums and Barrels | |

| Caps and Closures | |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Paints, Coatings and Chemicals |

| Pharmaceuticals and Healthcare |

| Industrial |

| Other End-user Industries |

By Coating Type

| Epoxy Phenolic |

| Acrylic |

| Polyester |

| BPA-Free Alternatives |

| Other Coating Types |

| By Material Type | Aluminum | |

| Steel | ||

| Tin | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Decorative Cans | ||

| Bulk Containers | ||

| Drums and Barrels | ||

| Caps and Closures | ||

| Other Product Types | ||

| By End-User Industry | Food | |

| Beverage | ||

| Paints, Coatings and Chemicals | ||

| Pharmaceuticals and Healthcare | ||

| Industrial | ||

| Other End-user Industries | ||

| By Coating Type | Epoxy Phenolic | |

| Acrylic | ||

| Polyester | ||

| BPA-Free Alternatives | ||

| Other Coating Types | ||

Key Questions Answered in the Report

How large is the Italy metal packaging market in 2026?

The market is valued at USD 5.52 billion and is projected to reach USD 6.95 billion by 2031 at a 4.72% CAGR.

Which material leads demand in Italian metal packaging?

Aluminum dominates with 63.35% share in 2025, favored for lightweight beverage and food applications.

What sector will drive future growth beyond food and beverages?

Industrial applications such as chemicals, lubricants and automotive fluids are forecast to grow at 5.55% CAGR through 2031.

Why are BPA-free coatings gaining momentum in Italy?

EU rules and consumer preferences push converters toward BPA-free chemistries, growing this coating segment at 5.78% CAGR.

How are EU recycling targets influencing Italian converters?

PPWR mandates 90% metal recycling by 2030, prompting investments in lightweight design and high recycled content packages.

Which companies lead the competitive landscape?

Global majors Ardagh, Ball and Crown plus domestic specialists Gruppo ASA and Tecnocap collectively hold about 50% share.

Page last updated on: