Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

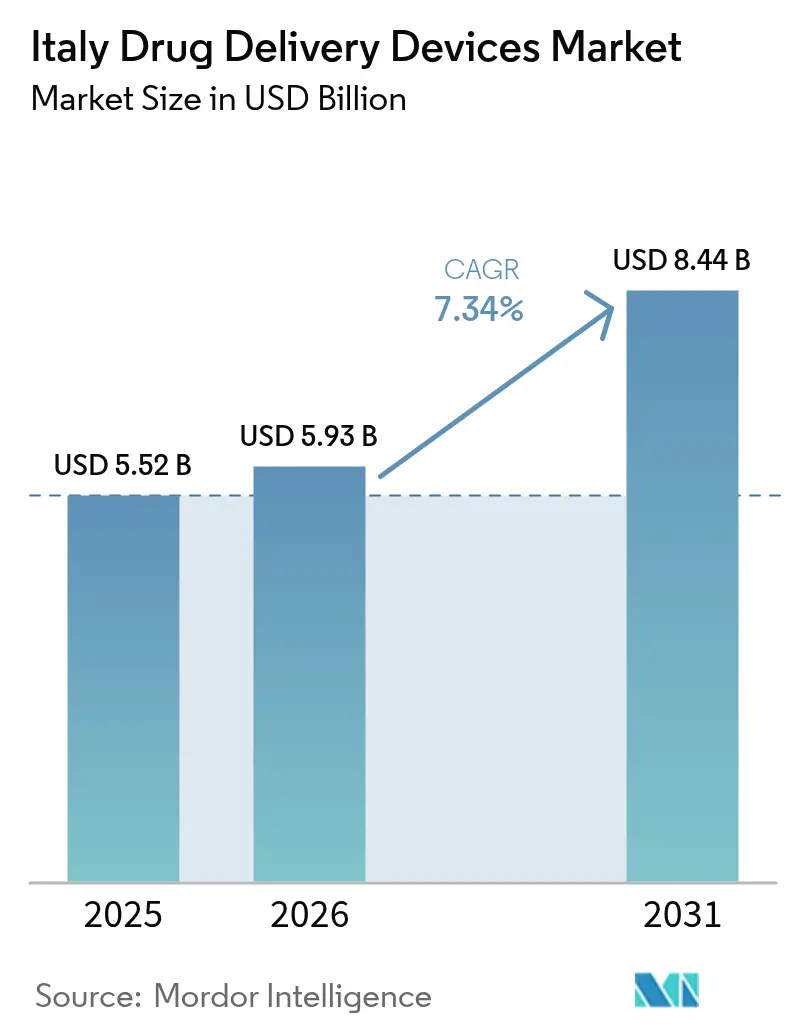

| Base Year Market Size (2025) | USD 5.52 Billion |

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

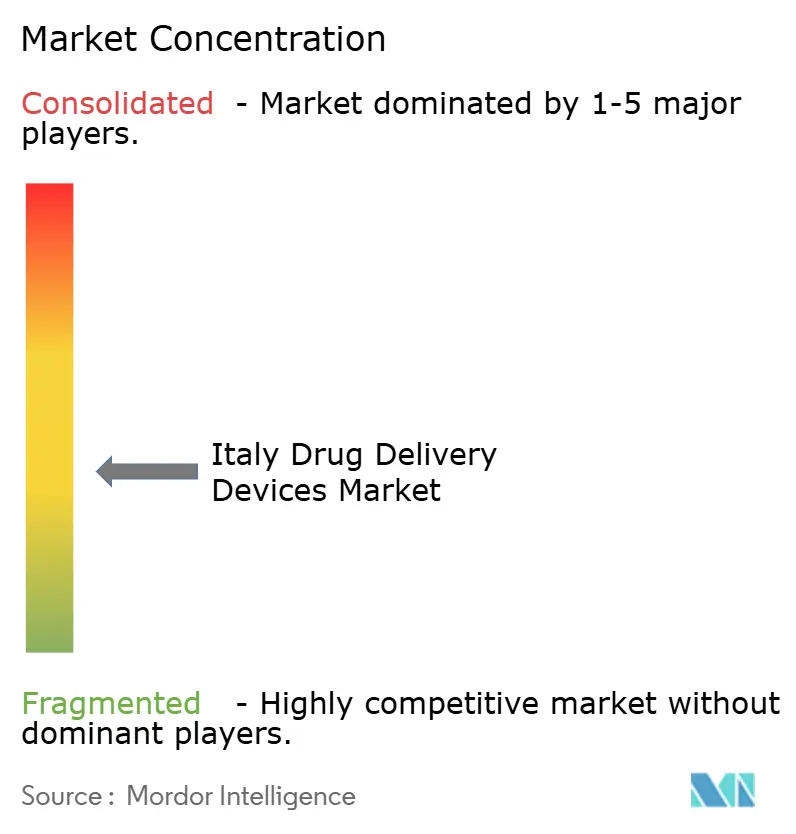

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Drug Delivery Devices Market Analysis by Mordor Intelligence

The Italy drug delivery devices market size was valued at USD 5.52 billion in 2025 and estimated to grow from USD 5.93 billion in 2026 to reach USD 8.44 billion by 2031, at a CAGR of 7.34% during the forecast period (2026-2031). Growth is anchored in the country’s rapidly aging population, the high and rising prevalence of chronic diseases such as diabetes and COPD, and a policy shift that favors self-administration over hospital-based care. Regulatory streamlining by the Italian Medicines Agency (AIFA) since January 2024 has shortened approval cycles for innovative products, while investment in connected technologies is improving adherence and real-time monitoring. At the same time, specialty pharmacies and community-based distribution models are extending access beyond large hospitals, accelerating uptake across the Italy drug delivery devices market.

Key Report Takeaways

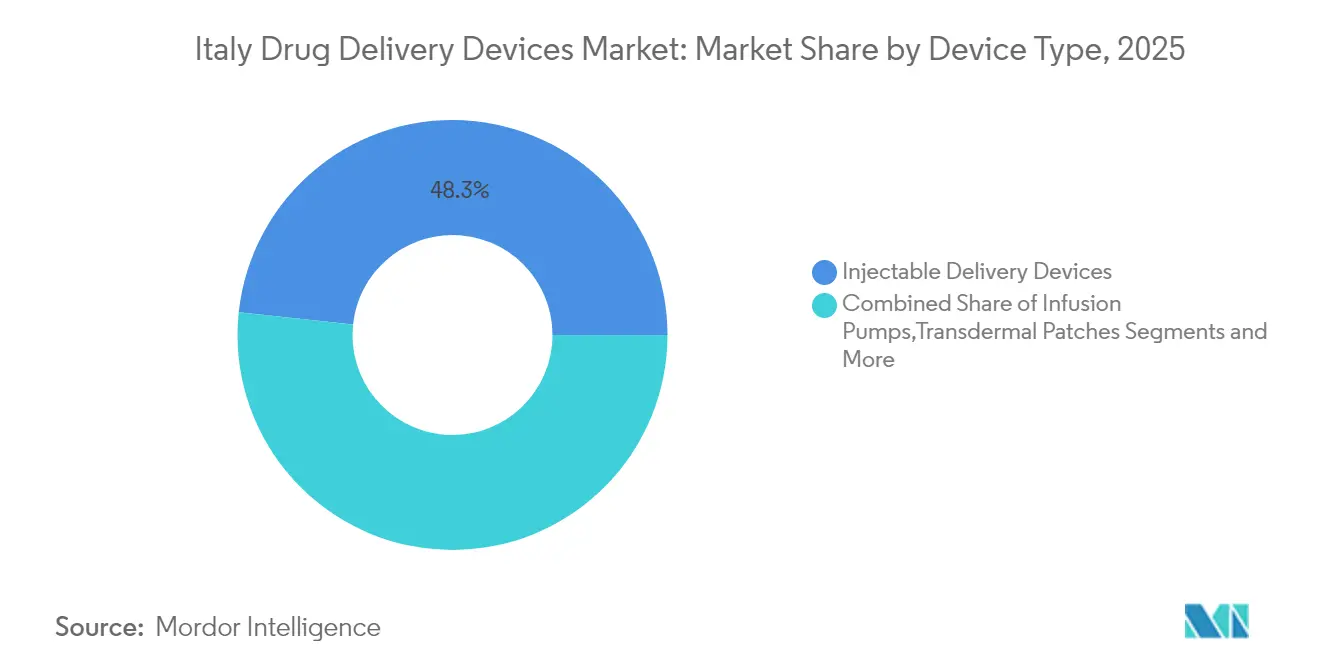

- By device type, injectable devices held 48.31% of Italy drug delivery devices market share in 2025, while implantable systems are projected to expand at a 8.79% CAGR to 2031.

- By route of administration, injectables accounted for 60.78% share of the Italy drug delivery devices market size in 2025, whereas inhalation routes are advancing at a 8.21% CAGR through 2031.

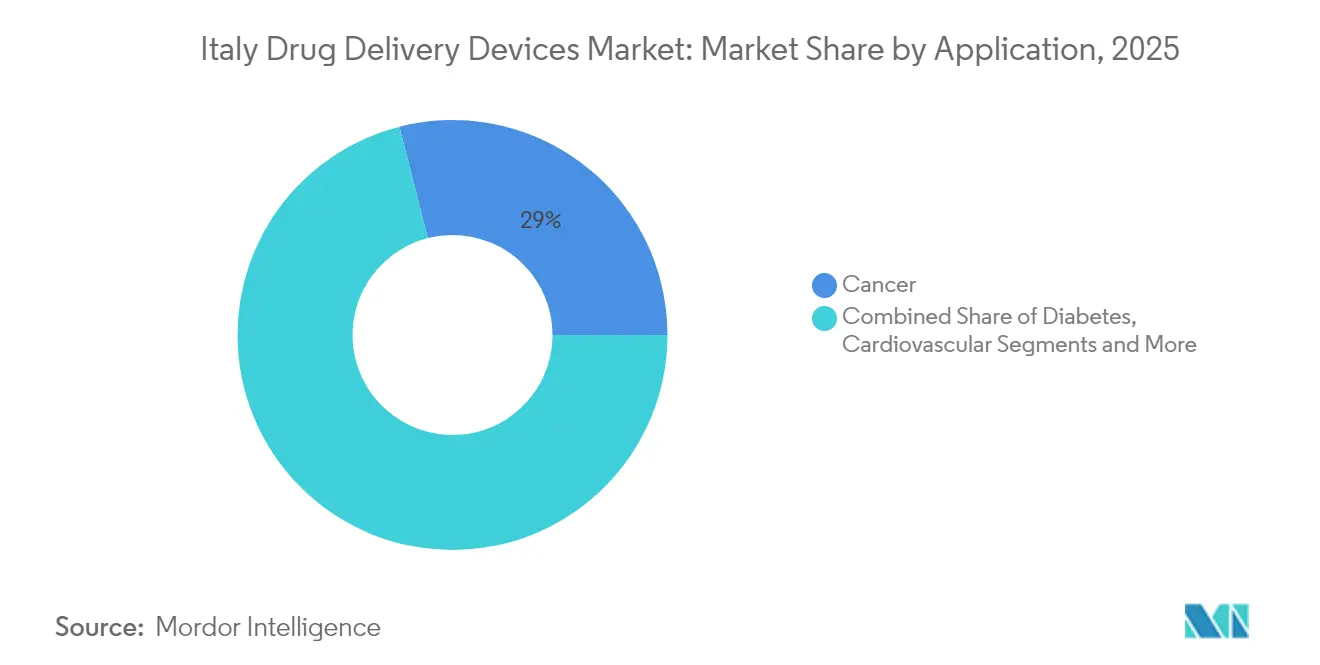

- By application, diabetes management led with 30.12% share of the Italy drug delivery devices market in 2025; oncology applications are forecast to grow at a 8.66% CAGR toward 2031.

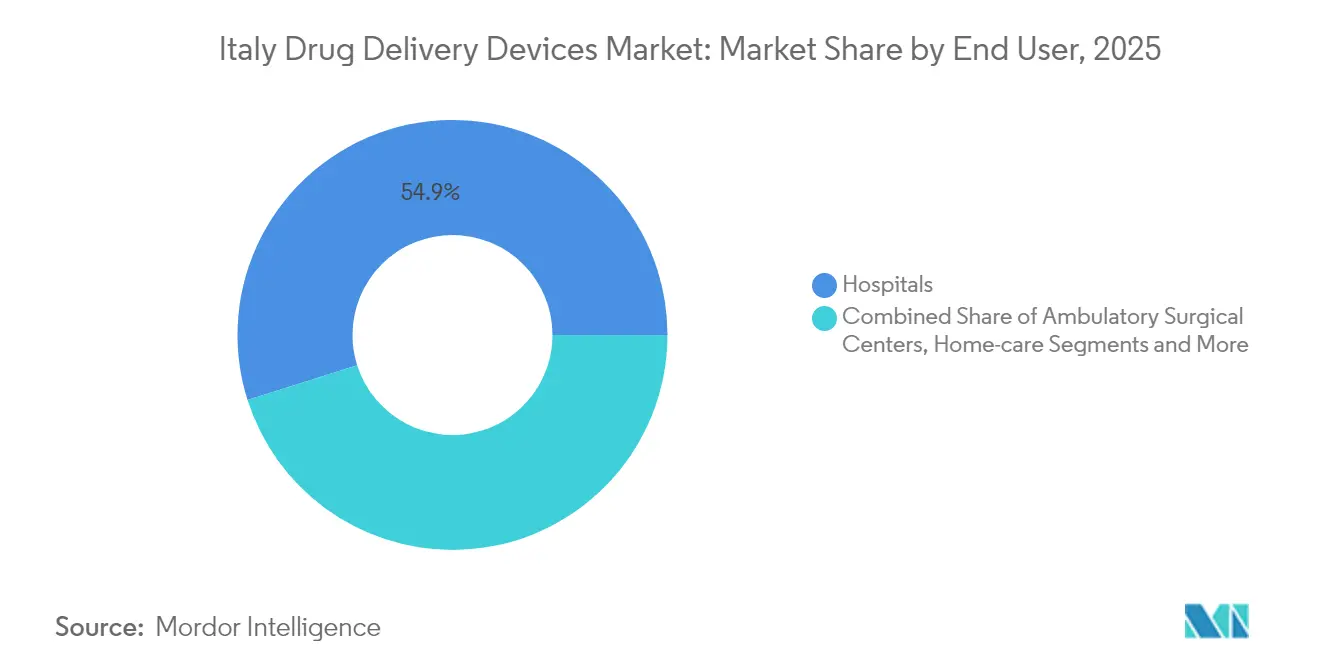

- By end user, hospitals captured 54.88% of Italy drug delivery devices market share in 2025, while homecare settings are projected to expand at a 9.84% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of pre-filled injectable pens | +1.8% | National, higher adoption in Lombardy, Veneto, Emilia-Romagna | Medium term (2–4 years) |

| Expansion of specialty pharmacies boosting biologic self-administration | +1.5% | Urban centers (Milan, Rome, Bologna, Florence) | Medium term (2–4 years) |

| Technological advancement and adoption of smart, connected devices | +1.2% | National, early uptake in metropolitan biotech hubs | Long term (≥ 4 years) |

| High burden of chronic diseases and aging population | +1.0% | National, sharper impact in Marche, Liguria, Umbria | Long term (≥ 4 years) |

| Expansion of home-care and self-administration | +0.8% | Northern and Central regions grow fastest | Medium term (2–4 years) |

| Reimbursement support for biosimilar pens and prefilled formats | +0.7% | National, subject to regional variation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Pre-Filled Injectable Pens

Demand for shorter 4 mm needles and 32 G gauges is rising because they lessen tissue trauma and improve adherence, a priority underscored by national guidelines from the Italian Society of Metabolism and Obesity (SIMDO).[1]MDPI, “Injectable Pen Needle Guidelines,” mdpi.com Next-generation connected pens automatically log dose data and sync to smartphone apps, closing information gaps in diabetes care. However, uptake remains uneven due to limited provider training, leaving space for targeted education and value-demonstration programs.

Expansion of Specialty Pharmacies Boosting Biologic Self-Administration

Italy’s decentralized distribution approach—direct hospital supply (DD), distribution on behalf of hospitals (DPC), and affiliated channels—has widened patient access to complex biologics outside tertiary centers. Analytics models piloted during the pandemic show potential to redirect a larger drug volume through community outlets, cutting travel time and hospital bottlenecks while maintaining cost control.

Technological Advancement and Increasing Adoption of Smart and Connected Drug Delivery Devices

Digital health is backed by EUR 1.6 billion in National Recovery and Resilience Plan funds, accelerating the roll-out of automated insulin delivery systems that couple pumps with continuous glucose monitoring. Clinical evidence shows higher time-in-range and lower hypoglycemia rates, validating their role in the Italy drug delivery devices market.

High Burden of Chronic Diseases and Aging Population

More than one quarter of residents in several regions are already over 65. Administrative-database analyses confirm escalating neurodegenerative and metabolic disease prevalence, driving pharmaceutical spending up 6.0% in 2024 and intensifying demand for reliable long-term delivery modalities.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic compliance costs and wider ESG mandates | −1.2% | Highest impact on manufacturing hubs in Northern Italy | Medium term (2–4 years) |

| Safety concerns and needlestick injuries | −0.8% | National, especially in clinical and home-care settings | Short term (≤ 2 years) |

| High development and manufacturing cost | −0.7% | Across all market participants | Long term (≥ 4 years) |

| Cultural reluctance toward self-injection impacting adherence | −0.6% | More pronounced in Southern regions and rural areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Slow Reimbursement Approval

Average reimbursement time for orphan products remains 413 days, far exceeding the 100-day statutory target and slowing roll-out of advanced drug delivery devices.[2]European Federation of Pharmaceutical Industries and Associations, “Root Causes of Unavailability and Delay,” efpia.eu Regional follow-through can add between 1 day and 773 days before products reach patients, creating pronounced territorial inequity.

High Development and Manufacturing Cost

MDR and AI-focused regulations require more rigorous technical dossiers, raising pre-market spending and timelines. Dossier compilation under the Common Technical Document format plus dual national–EU scientific assessment add further complexity.[3]Italian Medicines Agency, “Authorization of Medicines,” aifa.gov.it

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Injectable Devices Lead While Implantables Surge Ahead

Injectable formats generated 48.31% of Italy drug delivery devices market share in 2025 due to their established role in diabetes and autoimmune therapy regimens. Continuous refinement—such as 4 mm, 32 G insulin pen needles—improves tolerability and maintains the segment’s broad user base. High-viscosity biologics are also benefiting from glass syringes engineered for superior break-resistance. In parallel, implantables are projected to post a 8.79% CAGR to 2031, marking the fastest trajectory within the Italy drug delivery devices market. Advances like 3-D printed polyvinyl alcohol matrices loaded with Rose Bengal enable sustained anticancer drug release for up to 90 days. Inhalation devices are pivoting to low-GWP propellants, while transdermal, ocular, and nasal platforms gain from novel polymers that extend residence time. Collectively, these innovations reinforce the long-term expansion of the Italy drug delivery devices market size at the modality level.

By Route of Administration: Injectable Dominance Meets Inhalation Innovation

Injectables accounted for 60.78% of the Italy drug delivery devices market size in 2025, upheld by entrenched clinical protocols and the acceleration of automated insulin delivery systems that link pumps with continuous glucose monitors.Smart algorithms raise time-in-range and ease the burden of frequent dose decisions. Inhalation routes, expanding at a 8.21% CAGR, are propelled by triple combination pMDIs using the new HFA-152a propellant, which matches legacy efficacy while cutting global-warming potential by 90%. Transdermal, buccal, ocular, and nasal approaches are benefiting from micro-needle arrays and muco-adhesive gels that boost bioavailability yet face sterility and stability challenges.

By Application: Diabetes Management Leads While Oncology Accelerates

Diabetes applications projected to rise by 7.62% CAGR in Italy drug delivery devices market, reflecting high disease prevalence and the migration to Bluetooth-enabled pens that log every administration event. Oncology, registered 28.97 % market in Italy drug delivery devices market, by leveraging nanocarriers capable of traversing the blood–brain barrier to deliver chemotherapeutics directly to tumor sites. Cardiovascular uses draw on newer drug-eluting stents, while infectious-disease therapy is embracing long-acting injectables that hold therapeutic levels for months. Respiratory and neurological indications round out the portfolio, each gaining from formulation tweaks that extend dose intervals.

By End User: Hospitals Maintain Leadership as Home-Care Settings Accelerate

Hospitals retained 54.88% of Italy drug delivery devices market share in 2025 owing to their centralized capacity to deliver complex biologics and manage acute events. Yet the share is gradually eroding as reforms champion decentralized supply chains. Direct Distribution through hospitals coexists with Distribution Through Community Pharmacies on Behalf of Hospitals, a hybrid model validated during the pandemic for maintaining continuity of care. Home-care settings are poised for a 9.84% CAGR, powered by payer endorsements for outpatient infusion pumps and remote monitoring. Medication-error studies in domiciliary care frame the need for integrated digital platforms that reconcile prescriptions and support nursing teams. Ambulatory surgery centers and specialty clinics are also increasing uptake of single-use wearable injectors, citing improved throughput and patient satisfaction.

Geography Analysis

Northern Italy—Lombardy, Veneto, and Emilia-Romagna—collectively commands roughly 44.60% of total 2025 sales within the Italy drug delivery devices market. High per-capita income and dense hospital networks underpin early adoption, while local industry, exemplified by Chiesi’s EUR 400 million Biotech Center of Excellence in Parma, accelerates technology transfer and supply chain speed. Lombardy alone contributes close to 20% of nationwide revenue, supported by regional reimbursement that favors home-use injectors and connected inhalers.

Central regions, principally Lazio and Tuscany, account for about 30.20% of spending. They host leading academic centers and clinical-trial infrastructure, amplifying innovation diffusion. Florence-based Menarini Diagnostics, in partnership with Innovation Zed, distributes connectivity-ready pen-caps across Europe, highlighting the zone’s export orientation. Time-to-patient metrics remain uneven: some local health authorities approve new devices within weeks, while others extend timelines beyond one year, adding complexity to market roll-out.

Southern Italy and the islands comprise the remaining 25.20% share, constrained by lower healthcare capacity and slower reimbursement clearance. The 2022 recall of an inaccurate continuous glucose monitor in Campania illustrates quality-assurance gaps that can undermine confidence. To bridge disparities, pilot programs are integrating tele-consultations with community pharmacies, enabling remote titration for insulin and COPD inhalers.

Competitive Landscape

Market concentration is moderate. BD anchors the field with its BD iDFill prefillable syringe and Neopak XtraFlow glass platform, both introduced at CPhI Milan 2024 as high-viscosity solutions that streamline fill-finish operations. Berry Global’s 30% capacity expansion at its Osnago and Sirone plants has reinforced blister and bottle supply for inhalation therapies, bolstering resilience against demand spikes.

Novo Nordisk’s acquisition of the Anagni fill-finish facility improves vertical integration, enabling rapid scale-up for GLP-1 analog injectors. Ypsomed’s YpsoDose large-volume patch injector and BD’s Libertas wearable remain focal points for self-administration innovation. Patient-preference trials show higher acceptance of wearable formats when injection frequency drops below weekly, pushing manufacturers toward ultra-concentrated formulations.

Strategic alliances are multiplying: Menarini-Innovation Zed collaboration extends a Bluetooth smart cap for standard insulin pens to 44 European markets, while Chiesi has signed supply agreements for low-GWP propellants that safeguard its respiratory franchise. Collectively, these moves emphasize the sector’s pivot toward connected, eco-responsible devices without compromising therapeutic performance.

Italy Drug Delivery Devices Industry Leaders

Gerresheimer AG

BD (Becton, Dickinson and Company)

Ypsomed AG

Nemera

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bari’s Policlinico implanted the Port Delivery System for age-related macular degeneration, the first such surgery in Southern Italy.

- December 2024: Novo Nordisk launched the Mallya smart cap that records insulin doses and transmits data via Bluetooth to caregivers.

- October 2024: BD showcased BD iDFill, Neopak XtraFlow, and SCF PremiumCoat components at CPhI Milan, emphasizing traceability and high-viscosity biologic compatibility.

- October 2024: Chiesi inaugurated a EUR 400 million Biotech Center of Excellence in Parma to expand antibody and enzyme production.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian drug-delivery devices market as every regulated device that transports a therapeutic agent into the body through injectable, inhalation, transdermal, transmucosal, ocular, implantable, or infusion routes; this covers pens, auto-injectors, wearable or implantable pumps, smart inhalers, transdermal patches, and prefilled systems that are newly placed on the Italian market. We rely on this practical, route-based view because it mirrors how payers and AIFA track spending.

Scope exclusion: diagnostic catheters, compounding accessories, and trial-only prototypes remain outside scope.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- By Application

- Cancer

- Cardiovascular

- Diabetes

- Infectious Diseases

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home-care Settings

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview Italian endocrinologists, respiratory therapists, hospital pharmacists, device-design engineers, and distributors across Lombardy, Lazio, and Emilia-Romagna. These conversations clarify real-world usage rates, channel margins, and upcoming reimbursement tweaks, allowing us to reconcile secondary indicators and fine-tune cost assumptions.

Desk Research

We begin with publicly available data from bodies such as the Italian Medicines Agency (AIFA), ISTAT health accounts, Eurostat trade codes for HS 9018, WHO ATC/DDD utilization files, and the European Federation of Pharmaceutical Industries, which together outline therapy volumes, reimbursement ceilings, and import flows. Company 10-Ks, investor decks, and hospital procurement portals then help our team benchmark average selling prices and installed bases, while paid databases, D&B Hoovers for company financials, Questel for delivery-patent activity, and Dow Jones Factiva for real-time news, fill key historical gaps.

Additional sources, including Italian Medical Device Association papers, peer-reviewed clinical studies, and media releases, round out the evidence set. The list above is illustrative; analysts consult many more references during validation.

Market-Sizing & Forecasting

Our model launches with a top-down reconstruct of 2024 reimbursement sales reported by AIFA and imports/exports from Eurostat, which are then adjusted for hospital self-procurement and parallel trade before being spread across device classes. Select bottom-up checks, sampled ASP x unit volumes from 35 hospitals and three national wholesalers, validate totals and highlight miscounts. Key variables feeding the model include diabetic prevalence, COPD incidence, per-capita drug spend, 65+ aging index, and smart-device penetration; their trajectories are forecast through multivariate regression that blends official statistics with consensus insights from our primary interviews. Gap values where hospital data are missing are imputed using nearest-neighbor averages weighted by regional GDP.

Data Validation & Update Cycle

Outputs pass a three-step peer review; variance thresholds trigger re-checks with primary contacts, and we refresh the model each year. Interim updates follow material events such as reimbursement code changes, major recalls, or currency swings, ensuring clients always receive the latest view.

Why Mordor's Italy Drug Delivery Devices Baseline Is Dependable

Published numbers often differ because firms pick dissimilar device lists, price benchmarks, and refresh cadences, and because some convert currencies at varied dates.

Key gap drivers for this market include whether wearables sold direct to patient are counted, how sub-segments like connected pens are valued, and the base year chosen for forecasting. Mordor's scope reflects full therapeutic-route coverage, annual currency averaging, and a mix of top-down and corroborative bottom-up tests, giving decision-makers a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.52 Billion (2025) | Mordor Intelligence | |

| USD 2.95 Billion (2023) | Regional Consultancy A | Excludes direct-sale wearable pumps; earlier base year |

| USD 0.76 Billion (2024) | Industry Journal B | Focuses only on subcutaneous devices; narrow product scope |

Differences stem mainly from product-scope limits and older baselines, whereas our disciplined approach ties every figure to public metrics, expert insight, and repeatable steps, making Mordor's view the most reliable starting point for strategic planning.

Key Questions Answered in the Report

What is the current size of the Italy drug delivery devices market?

What is the current size of the Italy drug delivery devices market?

Which device category leads the market?

Injectable devices lead with 48.31% market share in 2025, owing to their widespread use in diabetes and autoimmune therapy

Why are implantable drug delivery systems gaining attention?

Implantables are forecast to grow at 8.79% CAGR through 2031 because they offer sustained, localized release that reduces dosing frequency and improves adherence.

How does regional reimbursement affect market access?

Reimbursement timelines vary from 1 day to 773 days after national approval, creating significant regional differences in device availability.

What role do connected devices play in market growth?

Smart pens, pumps, and wearable injectors enable real-time data capture, boosting adherence and supporting remote care models that are expanding at double-digit rates across Italy.

Page last updated on: