France Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

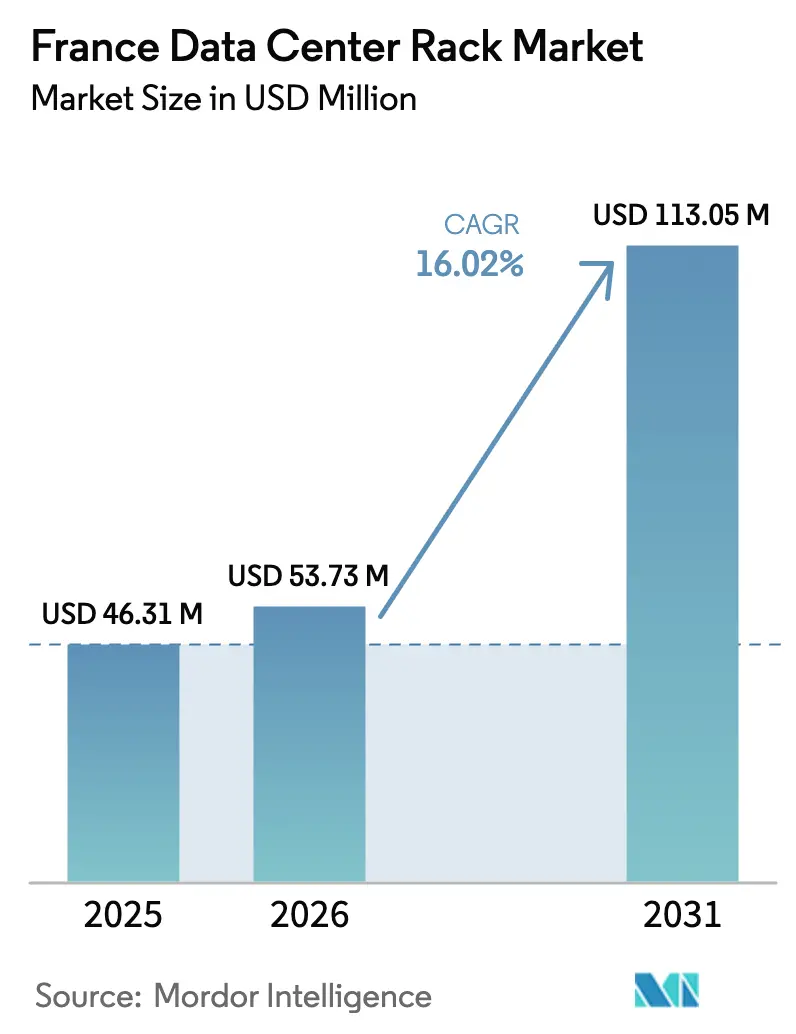

| Base Year Market Size (2025) | USD 46.31 Million |

| Market Size (2026) | USD 53.73 Million |

| Market Size (2031) | USD 113.05 Million |

| Growth Rate (2026 - 2031) | 16.02% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Data Center Rack Market Analysis by Mordor Intelligence

France data center rack market size in 2026 is estimated at USD 53.73 million, growing from 2025 value of USD 46.31 million with 2031 projections showing USD 113.05 million, growing at 16.02% CAGR over 2026-2031. Robust sovereign-cloud incentives, hyperscale build-outs linked to AI training clusters, and a nuclear-powered grid that regularly enables power-usage-effectiveness (PUE) targets below 1.3 collectively underpin this growth trajectory. Standardized full-rack designs, widespread cabinet adoption for GDPR compliance, and the rapid take-up of 48U heights—each tailored to high-density GPU workloads—further consolidate market acceleration. National policies assigning “project of national interest” status to strategic data center investments, combined with 35 government-prepared powered land parcels, mitigate grid-connection moratorium risks and sustain investor confidence. Meanwhile, Brookfield’s EUR 20 billion commitment through Data4, AMD’s rack-level acquisition of ZT Systems, and Schneider Electric’s new AI-ready lab portfolio collectively illustrate the competitive stakes and the premium placed on turnkey rack solutions ready for liquid cooling and advanced power distribution. [1]Datacenter Dynamics, “Brookfield Commits EUR 20 Billion to French Data Centers,” datacenterdynamics.com

Key Report Takeaways

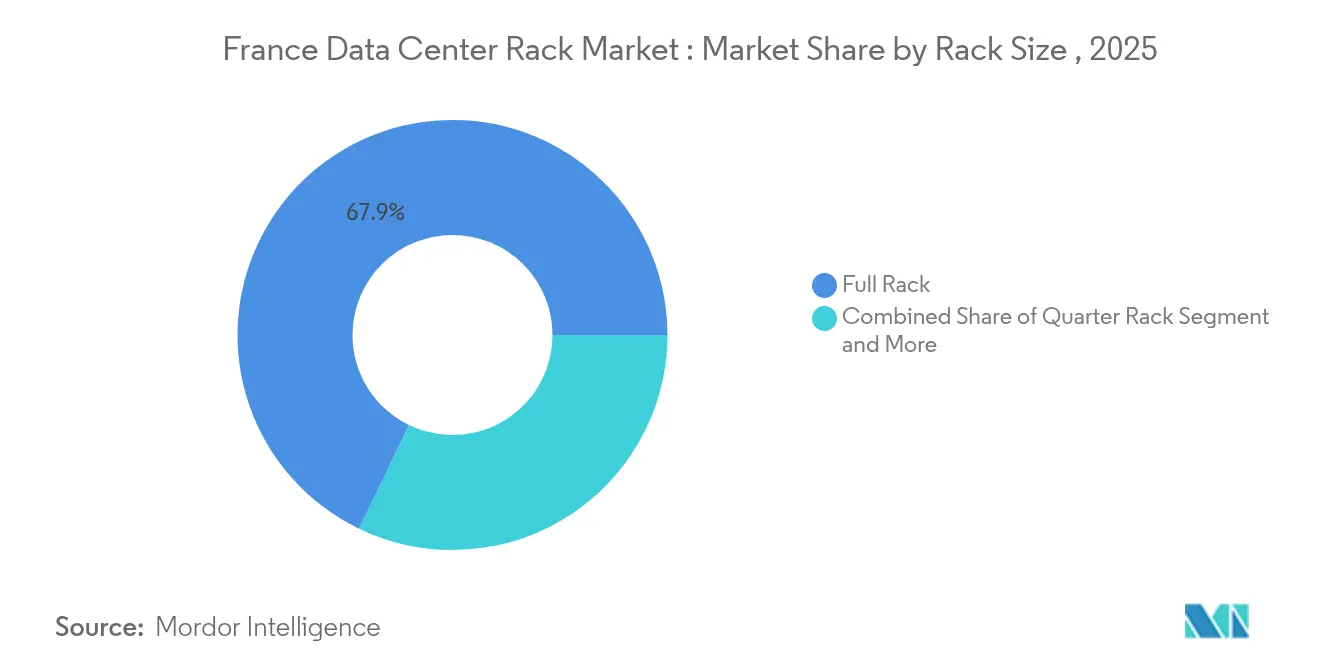

- By rack size, full-rack configurations held 67.85% of France data center rack market share in 2025 and are expanding at an 18.55% CAGR to 2031.

- By rack height, 42U accounted for 52.50% of the France data center rack market size in 2025, while 48U racks are advancing at a 19.02% CAGR.

- By rack type, cabinet solutions captured 74.74% revenue share in 2025; open-frame racks record the fastest projected CAGR at 17.03% through 2031.

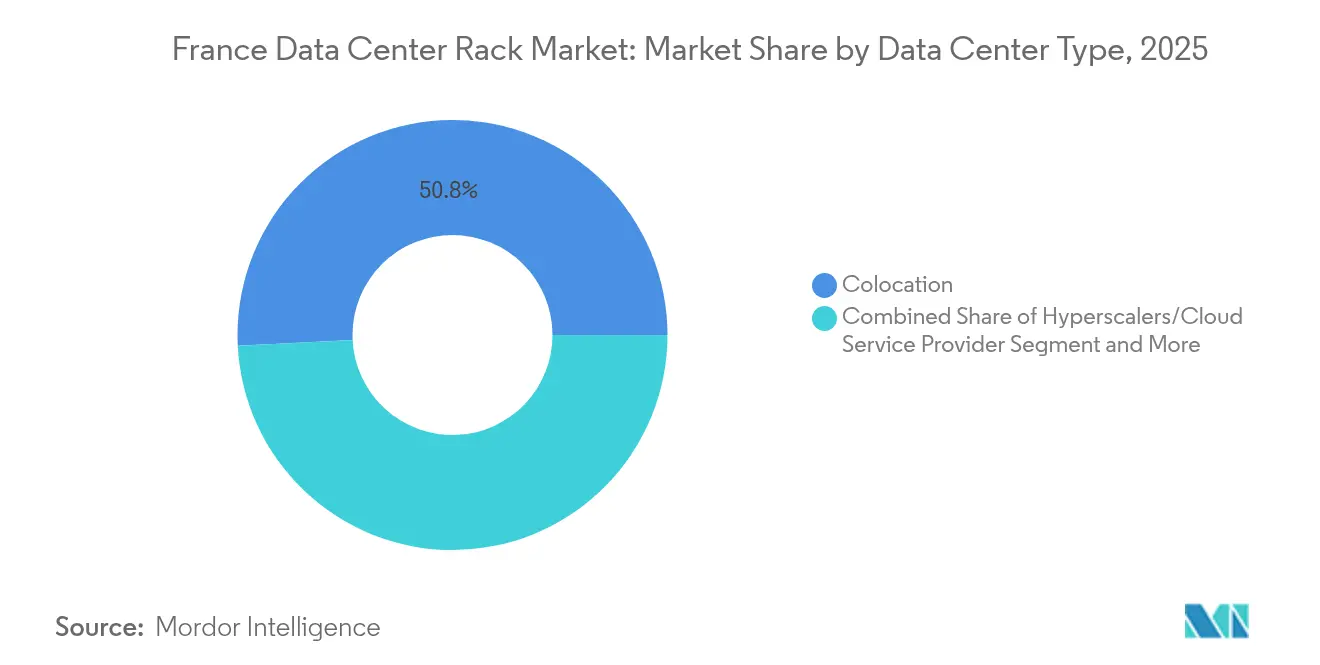

- By data center type, colocation facilities led with 50.80% share of the France data center rack market size in 2025, yet hyperscale investments deliver an 18.02% CAGR.

- By material, steel retained 73.60% share in 2025, while aluminum commands the highest growth at 16.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dynamics observed within France present a country level view when set against the broader international context. The data center rack market analysis by Mordor Intelligence provides that expanded global perspective.

France Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cloud-first enterprise strategies | +2.8% | National, focused on Île-de-France & Marseille | Medium term (2-4 years) |

| Expansion of nationwide fiber backbone | +2.1% | National, corridor links among major cities | Long term (≥ 4 years) |

| “Cloud de Confiance” sovereign-cloud incentives | +3.2% | National, preference for French-controlled sites | Short term (≤ 2 years) |

| AI training clusters exceeding 30 kW per rack | +4.1% | Paris region & Sophia Antipolis | Medium term (2-4 years) |

| Paris-2024 digital-legacy hyperscale build-outs | +1.9% | Île-de-France | Short term (≤ 2 years) |

| Low-carbon nuclear grid enabling <1.3 PUE | +2.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Cloud-First Enterprise Strategies

French enterprises are modernizing IT estates, migrating from legacy on-premise stacks to hybrid architectures that call for resilient, high-density racks inside local data halls. The October 2024 server-procurement program confirmed the government’s pivot toward hybrid infrastructure, unlocking rack orders that support both private-cloud nodes and edge micro-data centers. Legrand now derives 20% of group revenue from data-center activity, confirming the strategic weight of the France data center rack market for diversified industrial suppliers . As edge topologies proliferate, rack designs must deliver uniform power distribution, fast serviceability, and integrated monitoring for AI inference engines as well as conventional enterprise workloads.

Expansion of Nationwide Fiber Backbone

RTE’s EUR 300 million allocation for mutualized reception zones tightly couples backbone fiber with high-capacity substations, encouraging hyperscale and colocation players to position compute sites far beyond Paris. The Hauts-de-France region exemplifies this decentralization, pairing favorable electricity pricing with sub-5 ms latency to London and Amsterdam routes. Vendors competing in the France data center rack market therefore emphasize rapid-assembly cabinet kits, remote locking, and predictive failure analytics—features demanded by remote sites where in-house engineering talent is thinner.

Cloud de Confiance” Sovereign-Cloud Incentives

The Orange-Capgemini venture Bleu and the Thales-Google partnership S3NS illustrate how data-localization rules drive a new procurement calculus that rewards racks with enhanced audit trails, tamper-evident doors, and SecNumCloud-ready documentation. Enclosed cabinet racks with biometric access modules dominate large tenders because French-controlled cloud operators must provide regulators with unequivocal evidence of physical security. Suppliers able to bundle compliance tooling directly into cabinet SKU codes capture premium margins within the France data center rack market.

AI Training Clusters Pushing > 30 kW/Rack Densities

NVIDIA reference designs with Schneider Electric highlight a leap to 132 kW per rack, validating the technical pivot toward rear-door heat exchangers and direct-to-chip liquid. Evroc’s 96-MW campus near Sophia Antipolis will host 50,000 GPUs, requiring rows of 48U and 52U cabinets pre-plumbed for warm-water cooling. This density arms race cements full-height cabinet supremacy in the France data center rack market while opening a parallel lane for aluminum frames that trim weight loads on raised floors without sacrificing torsional rigidity.

Restraints Impact Analysis*

| Escalating cyber-security & GDPR compliance costs | −1.8% | National, higher impact in regulated verticals | Short term (≤ 2 years) |

|---|---|---|---|

| Scarcity of powered land parcels in Île-de-France | −2.4% | Paris metropolitan area | Medium term (2-4 years) |

| Grid-connection moratoriums delaying new builds | −1.6% | Urban growth zones | Short term (≤ 2 years) |

| Embodied-carbon disclosure raising steel CAPEX | −1.1% | National, tied to EU mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Security and GDPR Compliance Costs

Facial-recognition oversight clarified in the 2024 European Data Protection Board guidelines forces operators to retrofit cabinets with multi-factor access controls, RFID audit rails, and environmental sensor arrays. [3] European Data Protection Board, “Guidelines on Facial Recognition,” edpb.europa.eu France’s transposition of the NIS2 directive compels real-time security telemetry, lifting per-rack outlays and elongating certification cycles. For vendors in the France data center rack market, differentiated value now hinges on turnkey security modules pre-aligned with both GDPR and corporate-sustainability mandates.

Scarcity of Powered Land Parcels in Île-de-France

Real-estate premiums and the Zéro Artificialisation Nette law limit greenfield construction, forcing data center investors either into costlier vertical builds or toward dispersed regional campuses. Government-vetted powered sites ease the shortage but often lack dense dark-fiber rings. The France data center rack market therefore leans on taller 48U designs that squeeze higher compute density into pricey footprints, as well as modular containerized racks deployable in secondary zones where utilities and skilled labor remain in flux.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Rack Dominance Driven by Standardization

Full-rack cabinets captured 67.85% of 2025 revenue and continue to outpace other formats with an 18.55% CAGR through 2031. This commanding share of the France data center rack market stems from hyperscale mandates favoring uniform 48U and 52U templates, which simplify capacity planning and cut logistics costs. Operators pursuing 30 kW-plus densities further rely on full racks to spread coolant manifolds seamlessly across contiguous rows. Quarter- and half-rack footprints retain relevance for localized edge nodes, yet procurement managers increasingly redirect budget toward standardized full-rack bundles that ship with pre-integrated busbars, cable troughs, and liquid-cooling stubs.

Consistency dovetails with AI clusters demanding predictable airflow modeling. Schneider Electric’s NVIDIA partnership validates how fully enclosed columns enable repeatable thermal behavior across data halls, a design imperative when thousands of GPU servers run synchronous workloads. Therefore, the France data center rack market size attached to quarter-rack and half-rack variants remains capped by space-limited telecom huts and ancillary control rooms, whereas full-rack cabinets form the economic backbone of new hyperscale wings.

By Rack Height: 48U Emerges as AI-Optimized Standard

Although legacy 42U frames still account for 52.50% of the 2025 France data center rack market size, 48U units post a market-leading 19.02% CAGR to 2031. Height gains accommodate taller GPU sleds, redundant cable trays, and rear-door heat exchangers without breaching standard ceiling clearances. The France data center rack market share held by “other” ≥52U formats is small yet growing, especially inside greenfield AI labs eager to maximize compute per square foot.

AMD’s ZT Systems acquisition underscores the premium on carefully engineered vertical space that avoids recabling when nodes upgrade from air to liquid cooling. French facilities built before 2018 often lack the plenum depth for 52U cabinets, explaining the ongoing dominance of 42U in brownfield sites. New campuses, however, default to 48U in request-for-quotation documents, cementing this height as the median sweet spot between handling ergonomics and GPU density.

By Rack Type: Cabinet Security Drives Market Leadership

Cabinet racks claimed 74.74% revenue in 2025 and will log a 16.92% CAGR through 2031 as regulators scrutinize physical security across all critical-information infrastructure. The France data center rack market prizes locked, gasket-sealed doors that integrate biometric readers and audit logging, thereby easing SecNumCloud accreditation for sovereign-cloud operators. Open-frame alternatives still populate low-risk test labs due to superior airflow and lower cost but rarely pass final compliance checks for healthcare, fintech, or public-sector workloads.

Wall-mount units fill edge deployments such as traffic-camera aggregation points and smart-factory cells, yet their revenue contribution remains minor. Cabinet leadership is reinforced as operators chase electromagnetic-interference shielding to protect dense GPU boards running at boosted memory clocks. Vendors that pair sealed-door construction with hot-aisle containment kits observe rising attach rates, solidifying cabinet dominance within the France data center rack market.

By Data Center Type: Hyperscale Growth Reshapes Market Dynamics

Colocation incumbents maintained a 50.80% slice of revenue in 2025, but hyperscalers exhibit an 18.02% CAGR that is realigning capital allocation. Brookfield’s EUR 20 billion expansion via Data4 underscores hyperscaler influence over purchasing terms, dictating vendor qualifications and emphasizing rack pre-capitalization to accelerate white-space activation. Consequently, the France data center rack market size tied to hyperscalers could overtake colocation revenue before 2028.

Colocation operators are countering by bundling private-AI islands inside multi-tenant campuses, as evidenced by Equinix’s Dell-powered AI Factory rollout. Enterprise and edge categories together form a resilient niche, serving latency-sensitive industrial automation and regional content distribution. Yet hyperscale buyers dominate annual framework agreements, extracting volume discounts and pushing rack makers to shorten lead times to under eight weeks.

By Material: Aluminum Gains Ground in High-Density Applications

Steel retained 73.60% of 2025 revenue given its strength-to-price ratio, yet aluminum climbs at a 16.98% CAGR as floor-loading constraints interact with heavier GPU sleds. Operators targeting 3,000-lb rack loads view aluminum frames that trim mass by up to 40% as insurance against costly slab reinforcement. The France data center rack market now sees new RFPs pairing aluminum exoskeletons with steel mounting rails, offering hybrid mechanical performance.

Embodied-carbon disclosure under EU taxonomy rules also nudges buyers toward aluminum, which carries a lower CO₂ coefficient when sourced from French hydro-powered smelters. Supply-chain resilience remains a watch item because aerospace and automotive sectors compete for the same alloys. Nevertheless, aluminum’s thermal conductivity advantages help dissipate localized GPU heat, a trait that resonates with AI cluster designers forced to limit heat flux across densely packed PCBs.

Geography Analysis

The nuclear-heavy French grid provides average lifecycle carbon intensity below 55 gCO₂/kWh, allowing operators to advertise near-zero-carbon compute, a differentiator against Germany or Poland. Île-de-France still hosts roughly 60% of national IT power but faces EUR 40,000-per-MW grid-deposit requirements that tilt new-site economics toward provincial parcels. Land scarcity elevates ceiling heights and PUE optimization, reinforcing adoption of taller 48U cabinets in the heart of Paris.

Secondary territories such as Hauts-de-France and Normandy lure investors with sub-EUR 90 per m² annual land leases and direct fiber backhaulinto London and Amsterdam, creating fresh addressable demand pockets for the France data center rack market nordfranceinvest. Marseille’s critical role as a Mediterranean cable landing hub translates into rack orders purpose-built for high moisture and saline environments. Sophia Antipolis near Nice has become France’s “AI Riviera,” where facilities like Evroc’s 96-MW project plan to host 50,000 GPUs, cementing a regional preference for liquid-ready 48U and ≥52U cabinets.

Policy alignment further shapes geography. The forthcoming Business Simplification Bill proposes national-interest status for data centers, potentially overriding municipal opposition and accelerating permitting in underserved regions. Coupled with the government’s 35 shovel-ready, high-amp sites, this legislative shift spreads fresh rack deployments across nine regions, lessening Paris congestion while sustaining aggregate growth for the France data center rack market. Local authorities offering tax abatements for heat-reuse systems also tip procurement toward sealed cabinets able to integrate heat-exchanger coils directly at rack level.

Coverage of the data center rack market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Middle East, and South America, alongside detailed country-level intelligence for Spain, Switzerland, Saudi Arabia, Brazil, South Korea, and Russia, each shaped by local operating conditions.

Competitive Landscape

The France data center rack market remains moderately consolidated, with Schneider Electric, Vertiv, and Legrand together holding about 38% of 2024 sales. Schneider’s EcoStruxure racks penetrate hyperscale contracts by bundling liquid-cooling manifolds and microgrid-ready power distribution. Vertiv counters through prefabricated modular rows that shrink installation cycles. Legrand leverages domestic production to shorten supply chains and align with souveraineté numérique initiatives [2]Legrand Group, “FY 2024 Results Presentation,” legrandgroup.com.

Technological differentiation now trumps pure cost. Schneider Electric’s December 2024 co-engineered NVIDIA blueprint supports 132 kW liquid-cooled racks, enabling immediate AI workload absorption. Vertiv joined the Net Zero Innovation Hub to pilot hydrogen backup modules, targeting zero-diesel footprints that attract sustainability-minded European cloud buyers. Metal-fabrication newcomers, meanwhile, market aluminum frames with integrated drip-less quick disconnects, invoking both weight and serviceability advantages to chip away at steel incumbents.

Partnership strategy intensifies. Equinix’s global alliance with Dell pushes private AI nodes into colocation halls, influencing rack demand for pre-wired GPU sleds and security-sealed doors. AMD’s purchase of ZT Systems grants silicon-to-rack vertical integration, signaling that processor vendors consider cabinet engineering pivotal for end-to-end AI performance. Collectively, these moves place innovation velocity and compliance alignment at the center of competition within the France data center rack market.

France Data Center Rack Industry Leaders

-

Schneider Electric SE

-

Legrand S.A.

-

Eaton Corporation

-

Vertiv Group Corp.

-

Rittal GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The French government unveiled a EUR 8.5 billion AI campus in Paris backed by Mistral AI, NVIDIA, and UAE-based MGX, targeting 1.4 GW of compute by 2030

- May 2025: Telehouse International activated a new phase at its TH3 Paris Magny campus with AI-ready infrastructure engineered for next-generation GPUs datacenterknowledge.

- May 2025: AMD completed its acquisition of ZT Systems, adding rack-level expertise to its CPU-GPU-networking portfolio

- February 2025: Brookfield pledged EUR 20 billion—EUR 15 billion through Data4—to triple its French pipeline beyond 500 MW by 2030

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the France data-center rack market as the annual revenue generated from new, factory-built open-frame and enclosed cabinets installed within colocation, hyperscale, enterprise, and edge facilities across France.

Figures exclude aftermarket retrofits, used racks, cable trays, and non-IT enclosures.

Segmentation Overview

-

By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

-

By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

-

By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

-

By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

-

By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

We interviewed facility design engineers in Paris and Marseille, procurement heads at leading colocation providers, and product managers from rack manufacturers. Conversations clarified emerging 48U demand, hyperscale specification trends, and realistic ASP dispersion that are not evident in public filings.

Desk Research

Our analysts began with public datasets from ARCEP, Eurostat trade codes for rack enclosures, and the French Data Center Federation's equipment census, which reveal shipment volumes and import values. We also reviewed energy-mix dashboards from RTE to gauge average rack power density targets, plus tender notices on Tenders Info that signal upcoming build-outs. Company 10-Ks and investor decks supplied average selling price (ASP) clues, while news archives on Dow Jones Factiva helped time-stamp capacity announcements. These sources anchor supply, demand, and pricing baselines. The sources listed are illustrative; many additional references informed the desk phase.

Market-Sizing & Forecasting

A top-down and bottom-up blend is used. First, installed rack counts are reconstructed from data-center IT load, average kW per rack, and utilization ratios published by ARCEP and corroborated through interviews. Revenue is then derived by applying weighted ASPs that vary by height and enclosure type. This total is cross-checked with sampled supplier roll-ups and channel checks. Key variables in our model include hyperscale build pipeline (MW), sovereign-cloud incentives, 42U versus 48U adoption share, average rack density, and steel price trends that sway ASPs. A multivariate regression, updated each quarter, projects these drivers through 2030.

Data Validation & Update Cycle

Outputs pass variance checks against external shipment statistics, and anomalies trigger re-contact with data providers before sign-off. Reports refresh every twelve months, with interim updates after material policy or capacity announcements.

Why Our France Data Center Rack Baseline Earns Trust

Published estimates differ because each study chooses its own scope, pricing basis, and refresh rhythm. Our disciplined inclusion of only new factory-built racks, our annual refresh, and our driver-based forecast keep Mordor's numbers grounded.

Key gap drivers involve whether aftermarket cabinets are counted, if ASPs include power modules, and how often datasets are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 46.31 M | Mordor Intelligence | - |

| USD 163 M | Global Consultancy A | Includes used rack refurbishments and list-price ASPs |

| USD 1,240 M | Industry Association B | Bundles server chassis, power rails, and cooling doors into rack revenue |

In short, our step-wise model, transparent variables, and continuous validation give decision-makers a balanced baseline they can trace and reproduce with confidence.

Key Questions Answered in the Report

What is the current value of the France data center rack market?

The market is valued at USD 53.73 million in 2026 and is forecast to reach USD 113.05 million by 2031.

Which rack size leads in France?

Full-rack cabinets account for 67.85% of 2025 revenue and expand at an 18.55% CAGR through 2031.

Why are 48U racks gaining traction?

They provide extra vertical space for liquid-cooling hardware and GPU servers, supporting AI clusters while fitting within existing ceiling clearances.

How fast is the hyperscale segment growing?

Hyperscale and cloud-service provider facilities are increasing rack purchases at an 18.02% CAGR, outpacing the broader market.

Page last updated on: