Switzerland Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

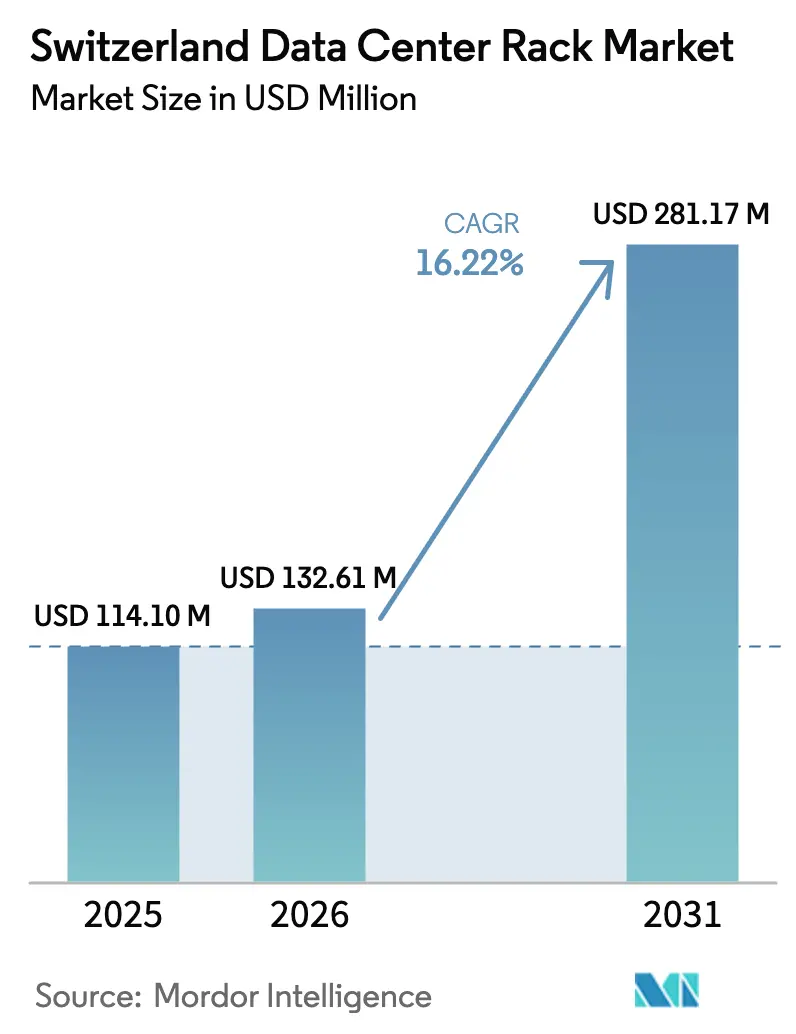

| Base Year Market Size (2025) | USD 114.1 Million |

| Market Size (2026) | USD 132.61 Million |

| Market Size (2031) | USD 281.17 Million |

| Growth Rate (2026 - 2031) | 16.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Data Center Rack Market Analysis by Mordor Intelligence

The Switzerland data center rack market size was valued at USD 114.1 million in 2025 and estimated to grow from USD 132.61 million in 2026 to reach USD 281.17 million by 2031, at a CAGR of 16.22% during the forecast period (2026-2031). Heightened investments by global cloud providers, including Microsoft’s multi-year expansion of AI-ready infrastructure in Zurich and Geneva, continue to anchor growth. [1]Microsoft Corporation, “Investing in Switzerland’s Digital Future,” microsoft.comFinancial-services digitalization, pharma research digitization, and Switzerland’s expanding role as a European data-sovereignty hub amplify demand for high-density cabinets that pair seamlessly with liquid cooling systems. A supportive regulatory backdrop—ranging from cantonal waste-heat reuse mandates to federal incentives that favor renewable power—pushes operators toward energy-efficient rack designs that blend steel strength with lighter aluminum innovations. At the same time, the nation’s land scarcity accelerates micro-modular deployments that pack more compute into smaller footprints while easing grid constraints. Supply-chain volatility, notably a 5.9% jump in steel prices during 2025, is nudging buyers to diversify materials and source locally. [2]Engineering News-Record Staff, “Steel Prices Spike on Tariffs,” enr.com

Key Report Takeaways

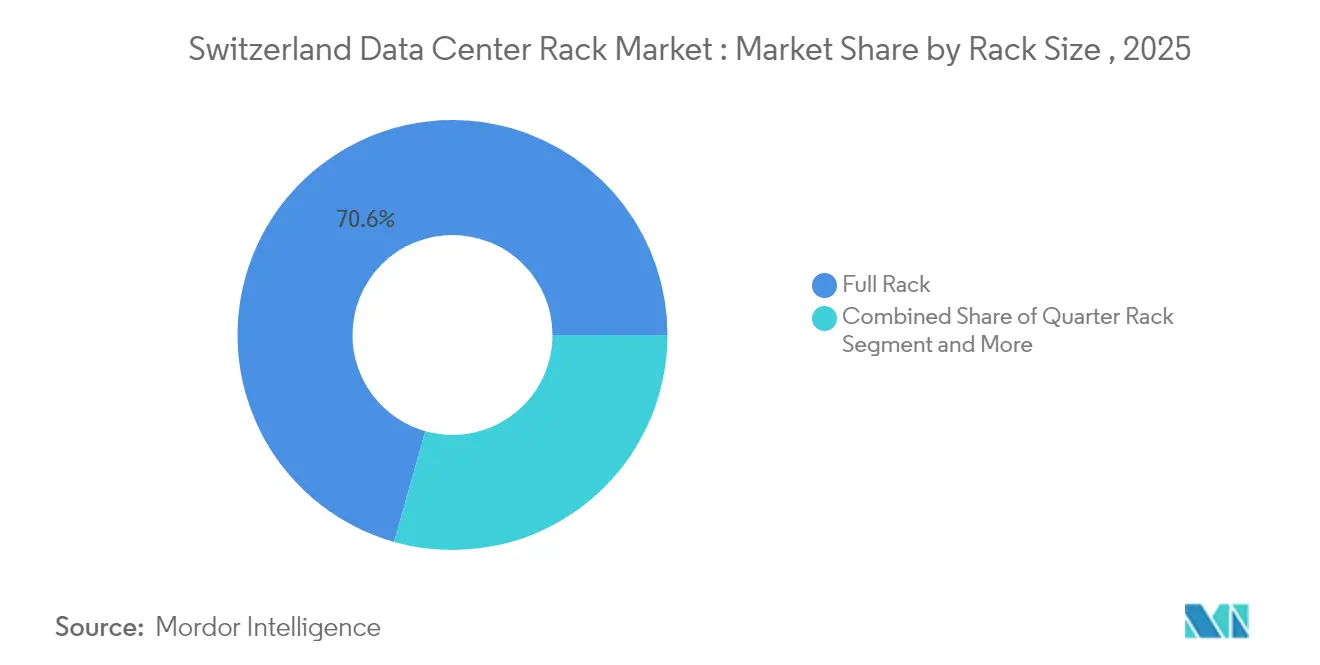

- By rack size, full rack configurations led with 70.62% of Switzerland data center rack market share in 2025; half rack installations are projected to rise at a 19.12% CAGR to 2031.

- By rack height, the 42U format dominated with 54.55% of Switzerland data center rack market size in 2025, while 48U designs are advancing at an 18.27% CAGR through 2031.

- By rack type, cabinet enclosures captured 75.62% revenue share in 2025; they also deliver the swiftest growth at 19.06% CAGR through 2031.

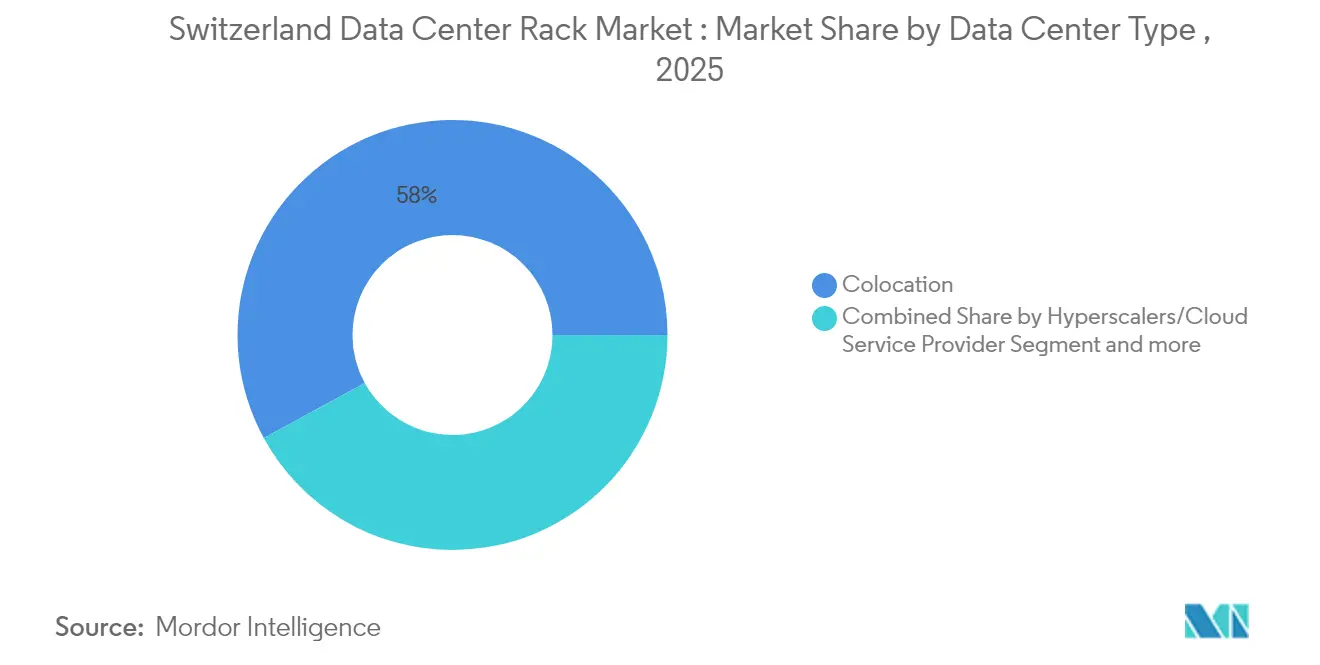

- By data-center type, colocation sites held 57.95% of Switzerland data center rack market size in 2025, whereas hyperscale facilities are expanding fastest at a 20.14% CAGR to 2031.

- By material, steel accounted for 74.58% of Switzerland data center rack market share in 2025; aluminum adoption is accelerating at a 19.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Viewed independently, Switzerland offers depth on local conditions but not full coverage of the overall global system. Mordor Intelligence's coverage on the data center rack market brings the wider geographic picture into focus.

Switzerland Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased migration to cloud-based business operations | +3.2% | Switzerland and wider DACH region | Medium term (2-4 years) |

| Internet adoption and IT-services boom | +2.8% | Zurich and Geneva metro areas | Short term (≤ 2 years) |

| Surge in AI/ high-density workloads | +4.1% | Swiss financial and pharma hubs | Medium term (2-4 years) |

| Federal and cantonal green-energy incentives | +2.3% | Nationwide | Long term (≥ 4 years) |

| Adoption of in-rack liquid cooling | +2.9% | Switzerland plus aligned EU markets | Medium term (2-4 years) |

| Land scarcity driving micro-modular roll-outs | +1.5% | Urban cores in Zurich and Basel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Migration to Cloud-Based Business Operations

Swiss enterprises rapidly shifted workloads off-premises after Digital Realty enlarged its Zurich power capacity from 4 MW in 2019 to 45 MW in 2024, a more than ten-fold jump. Less than half of corporate applications now remain in-house, fueling standard cabinet demand that supports multi-tenant colocation security. Financial-services firms spearhead the move, favoring racks that enable hybrid architectures across low-latency edge nodes and central hyperscale halls. These factors firmly reinforce purchasing momentum for the Switzerland data center rack market.

Internet Adoption & IT Services Boom

Zurich alone hosts 25 carrier-dense data-center sites spanning 668,501 sq.ft and 198 MW of IT load, underscoring the nation’s digital-service appetite. Operators gravitate toward 42U full racks to maximize cubic efficiency inside premium real estate. Swisscom’s CHF 60 million Wankdorf site operates at a 1.2 PUE, well below the European average of 1.95, setting a local benchmark for rack-level thermal management. [3]Swisscom AG, “Wankdorf Data Center Factsheet,” swisscom.ch These efficiency contrasts drive competitive differentiation and incentivize adoption of energy-conscious rack frames in the Switzerland data center rack market.

Surge in AI / High-Density Workloads

Average power draw per rack has doubled, climbing from 8 kW to 17 kW today with trajectories toward 30 kW by 2027. Roughly 22% of Swiss operators already employ direct liquid cooling, and abundant hydro-electric supply bolsters uptake. Dell’s Integrated Rack 7000 and similar lines merge liquid manifolds, higher static loading, and integrated monitoring to serve GPU-rich clusters . These capabilities lower cooling energy by as much as 88%, cementing a structural tailwind for the Switzerland data center rack market.

Federal & Cantonal Green-Energy Incentives for Data Centers

Switzerland targets 35,000 GWh of renewable electricity by 2035, with federal grants favoring data centers that cut carbon intensity. Zurich’s 2023 Energy Act obligates new facilities to harness waste heat, prompting rack suppliers to deliver thermal-recovery-ready cabinets. Incentives also promote lighter aluminum frames that ease floor loading and heighten thermal conductivity, nudging purchasing in the Switzerland data center rack market toward innovative alloys.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited land and power availability | -2.1% | Zurich and Geneva cores | Short term (≤ 2 years) |

| High capex for state-of-the-art rack systems | -1.8% | Nationwide and premium EU | Medium term (2-4 years) |

| Stringent Swiss carbon-disclosure regulations | -1.2% | Federal jurisdiction | Long term (≥ 4 years) |

| Skilled-labour shortage for high-density racks | -1.6% | Switzerland and DACH | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Land & Power Availability

Land scarcity presses operators to compress compute footprint, embracing 48U racks that yield more kilowatts per square meter. EU studies forecast data-center energy consumption to quadruple to 160 TWh by 2030, magnifying grid strain dentons. Vendors answer with taller frames, integrated chillers, and modular edge pods that circumvent the real-estate bottleneck yet temper overall growth in the Switzerland data center rack market.

High Capex for State-of-the-Art Rack Systems

Advanced liquid-ready racks carry higher price tags just as steel tariffs elevated construction inputs 7-8% during 2025, squeezing ROI for midsized operators. Many Swiss firms now prolong equipment life cycles or stagger upgrades in modular increments. Consolidation among manufacturers accelerates as capital intensity climbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Rack Dominance Driven by AI Workload Consolidation

Full racks owned 70.62% of Switzerland data center rack market share in 2025, and they are set to expand at 18.35% CAGR because AI clusters benefit from contiguous GPU pools and manifold-based cooling. Dell’s AI Factory bundles underscore how pre-engineered full racks streamline deployment and hasten inference speed. Half racks remain relevant for distributed finance nodes that seek geographic diversity, while quarter racks cater to containerized micro sites lodged near users to shave latency.

Emerging regulatory and energy incentives strengthen the full-rack thesis. As power densities breach 20 kW per frame, Swiss colocation providers invest in manifold-equipped steel enclosures that accept chilled plates without downtime. This operational agility keeps the Switzerland data center rack market positioned for continued full-rack leadership across new builds and retrofit projects alike.

By Rack Height: 42U Standard Persists Despite 48U Innovation Push

The 42U profile held 54.55% of Switzerland data center rack market size during 2025, thanks to abundant supply, mature accessory ecosystems, and installer familiarity. Yet 48U frames outpace all others at an 18.27% CAGR, propelled by GPU-dense servers that require extra clearance for vertical airflow and coolant hoses. nVent’s liquid cooling suite exemplifies how taller cabinets accommodate heavier AI nodes without sacrificing serviceability.

Operators weigh trade-offs: 42U racks simplify mixing older and newer gear, whereas 48U variants maximize power density in land-constrained metro halls. Dual-format strategies surface, wherein legacy halls stay 42U while new AI labs pivot to 48U, sustaining flexible asset management within the Switzerland data center rack market.

By Rack Type: Cabinet Solutions Lead Through Security and Cooling Integration

Cabinets captured 75.62% market share in 2025, reflecting strict data-sovereignty rules that demand physical safeguards for sensitive workloads. Enclosed designs isolate hot and cold aisles, reduce electromagnetic interference, and simplify immersion or manifold cooling attachment. NVIDIA’s recent patents for configurable closed-loop racks highlight industry focus on sealed environments that prevent coolant leaks.

Open-frame racks appeal to telecom rooms and test labs where airflow and easy access dominate concerns, but their presence wanes as security expectations tighten. Wall-mount enclosures gain traction at distributed fintech and healthcare nodes that require tamper resistance in non-traditional spaces, yet they remain a niche slice of the Switzerland data center rack market.

By Data Center Type: Colocation Leadership Challenged by Hyperscale Acceleration

Colocation providers stood atop the market with 57.95% of Switzerland data center rack market size in 2025, buoyed by multinational clients pursuing neutral ground for European data. However, hyperscale operators are logging a blistering 20.14% CAGR through 2031 as Amazon, Google, and Microsoft accelerate AI cluster rollouts. Vantage’s CHF 370 million second site in Glattfelden epitomizes the capex surge and appetite for standardized racks at scale.

Edge and enterprise builds persist for latency-sensitive or regulated workflows but yield slower growth. To stay competitive, colocation firms now retrofit halls with liquid-ready cabinets and AI cages, narrowing performance gaps and sustaining their share of the Switzerland data center rack market.

By Material: Steel Dominance Faces Aluminum Challenge from Weight Optimization

Steel framed 74.58% of shipments in 2025 because of superior load bearing and cost advantages, yet aluminum racks are accelerating at 19.19% CAGR as operators seek easier handling and better thermal conductivity. The 2025 tariff-linked steel price uptick sharpened aluminum’s total-cost appeal. Lighter alloys cut floor loading, simplify top-rack manifold installs, and support rapid reconfiguration in micro-modular pods.

Composite and hybrid materials appear in research labs and military data shelters where corrosion resistance or electromagnetic shielding overrides cost. Overall, steel remains entrenched, but high-density AI sites increasingly pilot aluminum frames, diversifying material demand within the Switzerland data center rack market.

Geography Analysis

Switzerland’s data-center footprint clusters around the Zurich metropolitan area, home to 25 facilities and 198 MW of IT capacity, ranking ninth in EMEA scale. The city’s concentration of financial services and cloud on-ramps creates a vibrant corridor for high-density rack deployments. Federalism shapes the regulatory canvas: Zurich’s 2023 Energy Act obliges waste-heat reuse, so racks with heat-exchanger stubs gain preference.

Outside Zurich, Geneva and Basel host secondary clusters where land scarcity boosts micro-modular adoption. NorthC’s Winterthur launch in early 2025 expanded colocation capacity and signalled confidence in demand beyond Zurich’s urban core. Cantonal permitting agility remains key; Basel’s life-science hub often fast-tracks AI-driven research workloads, leading to cabinet selections that prioritize security and liquid cooling in constrained footprints.

Switzerland’s linkage to pan-European data-residency mandates draws cross-border clients seeking neutrality. The Swiss Datacenter Efficiency Association’s new sustainability label—achieved by merely one-third of domestic halls—acts as a differentiator for foreign tenants who face ESG scrutiny. Racks with embedded metering empower operators to document energy consumption and carbon intensity, aligning with EU taxonomy criteria and reinforcing market momentum.

Mordor Intelligence evaluates the data center rack market across all key regional markets, including Europe, North America, and Africa, with deeper country-level insights covering Denmark, United Kingdom, United States, South Africa, Sweden, and Canada.

Competitive Landscape

Competition in the Switzerland data center rack market remains moderate. Global heavyweights Schneider Electric, Rittal, Vertiv, and Eaton anchor share yet face nimble Swiss specialists that carve out niches in micro-modular and immersion-ready cabinets. Schneider’s acquisition of Motivair embedded direct-to-chip cooling expertise, enabling a turnkey stack from chassis to coolant distribution schneider-electric. Eaton’s USD 1.65 billion Tripp Lite deal expanded edge UPS-rack bundles, sharpening its appeal for branch-office deployments .

Innovation skews toward liquid cooling, tool-less assembly, and embedded telemetry. NVIDIA’s heavy filing of rack-level cold-plate patents underscores rising chipset influence on enclosure design . Meanwhile, emergent vendors deliver 48U aluminum racks pre-plumbed for dielectric immersion, targeting AI startups that lease pods inside colocation halls. Supply-chain volatility rewards manufacturers with Swiss-based assembly that trims lead times and meets stringent origin documentation for public-sector bids.

Strategic alliances also proliferate. Siemens joined Cadolto and Legrand to roll out a prefab edge module headquartered in Zug that integrates racks, chillers, and switchgear for rapid deployment inside 6 months. Such ecosystem plays sharpen differentiation, yet rising capex complexities drive gradual consolidation as smaller fabricators struggle to bankroll R&D for high-density liquid systems.

Switzerland Data Center Rack Industry Leaders

Eaton Corporation

Rittal GMBH & Co.KG

Schneider Electric SE

Vertiv Group Corp.

Reichle and De-Massari AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Siemens, Cadolto, and Legrand unveiled a modular edge data-center platform supporting AI-ready 48U racks and rapid six-month deployment cycles

- June 2025: Microsoft committed new cloud and AI infrastructure investments in Zurich and Geneva, bolstering demand for next-generation rack capacity

- March 2025: NorthC opened a Winterthur colocation facility, adding Swiss white space for cabinet deployments

- March 2025: Schneider Electric’s 2024 Universal Registration Document confirmed its acquisition of Motivair to strengthen liquid-cooling offerings

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Switzerland data center rack market as revenue derived from new, factory-built enclosures, cabinet, open-frame, and wall-mount made of steel, aluminum, or comparable composites, deployed inside colocation, hyperscale, enterprise, and edge facilities nationwide. We count only the rack hardware's invoice value, which lets buyers compare "like for like" figures across facilities of different sizes.

Scope Exclusions: Refurbished racks, second-hand cabinets, in-row containment pods, power distribution units sold separately, and any services bundled with installation are left outside the baseline.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

We interviewed facility managers at tier III and tier IV sites, procurement heads at cloud-service operators, and regional systems integrators. Their volume projections, ASP updates, and lead-time signals helped us fill data gaps that published numbers could not address and guided final assumption checks across German, French, and Italian speaking cantons.

Desk Research

Our analysts began with Swiss federal trade statistics, customs import codes for HS 847330, and energy regulator updates on power density norms, and then reviewed data center project lists from the Swiss Data Center Association, ENISA guidelines on physical security, and ESG disclosures that detail rack counts inside new Zurich and Geneva builds. Company 10-Ks and investor decks, together with technical papers in IEEE Xplore that benchmark rack airflow and load profiles, enriched the technical context. Data pulls from D&B Hoovers and Dow Jones Factiva supplied financials and news on rack vendors entering the market.

These sources illustrate; they do not exhaust the secondary evidence consulted. Many more public and paid references were read to confirm figures and definitions.

Market-Sizing & Forecasting

The baseline value is first built top down by reconstructing rack demand from installed IT load, average power density, and prevailing full cabinet utilization ratios, before sampled vendor shipment tallies and channel checks validate the totals. Key variables like annual rack additions per megawatt, shift toward 48U height, steel price movement, exchange rate swings, and hyperscale build pipeline feed a multivariate regression that projects 2025 to 2030 growth. Bottom up rollups on sample contracts adjust the model when utilization diverges from norms.

Data Validation & Update Cycle

Each draft model passes a two-step peer review, anomaly flags trigger re-checks with sources, and variance beyond three percent requires a fresh call with at least one primary respondent. Reports refresh yearly, and material announcements, such as a new 20 MW campus, prompt interim updates so clients always receive the latest view.

Why Mordor's Switzerland Data Center Rack Baseline Commands Reliability

Published numbers differ because firms pick different rack add-ons, density assumptions, and refresh speeds.

Our disciplined scope and annual recount keep totals anchored to hardware that buyers actually procure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 114.1 M (2025) | Mordor Intelligence | - |

| USD 1.37 B (2024) | Regional Consultancy A | Includes containment, PDUs, and services, and uses broad data center capex multipliers without rack only filtering |

| USD 100 M (2025) | Trade Journal B | Relies on limited vendor shipment surveys focused on telecom vertical, applies flat growth rate, and refreshes every two years |

These comparisons show that when scope widens or validation thins, estimates swing widely. Mordor's clear rack only definition, multi-source inputs, and yearly refresh give decision makers a balanced, transparent baseline they can retrace and reuse with confidence.

Key Questions Answered in the Report

What is the current value of the Switzerland data center rack market?

The market stands at USD 132.61 million as of 2026 and is projected to reach USD 281.17 million by 2031.

Which rack configuration dominates Swiss data centers?

Full racks command 70.62% share, favored for consolidating GPU-dense AI workloads.

How fast are 48U racks growing in Switzerland?

The 48U segment is expanding at an 18.27% CAGR through 2031 owing to taller server architectures and liquid cooling needs.

Why are aluminum racks gaining popularity?

Aluminum’s lighter weight and superior thermal conductivity support high-density racks, accelerating adoption at a 19.19% CAGR even though steel still holds 74.58% share.

Page last updated on: