Europe Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

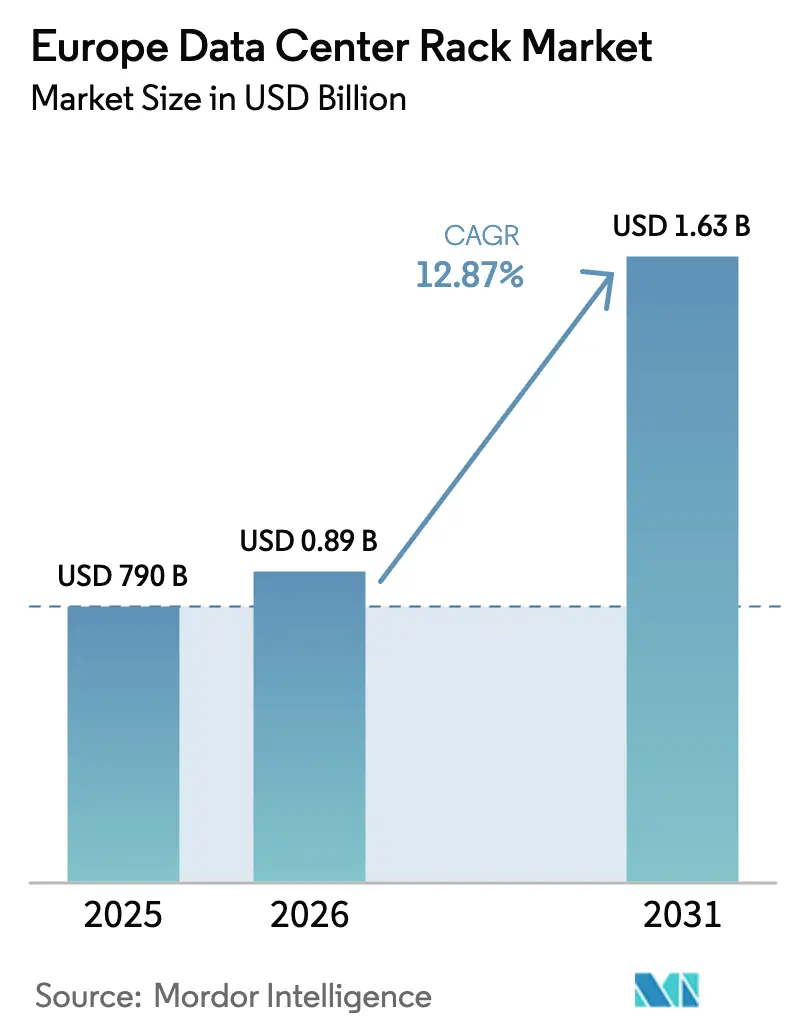

| Base Year Market Size (2025) | USD 790 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 12.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center Rack Market Analysis by Mordor Intelligence

The Europe data center rack market size in 2026 is estimated at USD 891.7 million, growing from 2025 value of USD 790 million with 2031 projections showing USD 1.63 billion, growing at 12.87% CAGR over 2026-2031. Strong demand reflects regulatory commitments to local data processing, a sharp rise in hyperscale construction, and an industry-wide move to liquid-cooled, 1 MW rack configurations that support artificial intelligence workloads. Operators now treat thermal management as a core design variable, prompting rapid upgrades from air-cooled to integrated liquid solutions. Procurement strategies increasingly favor standardized open-rack designs that shorten build cycles, align with new energy-efficiency mandates, and reduce total cost of ownership. Materials innovation, led by aluminum adoption, underscores the drive for lighter frames that dissipate heat more effectively and facilitate quick installation across expanding European campuses.

Key Report Takeaways

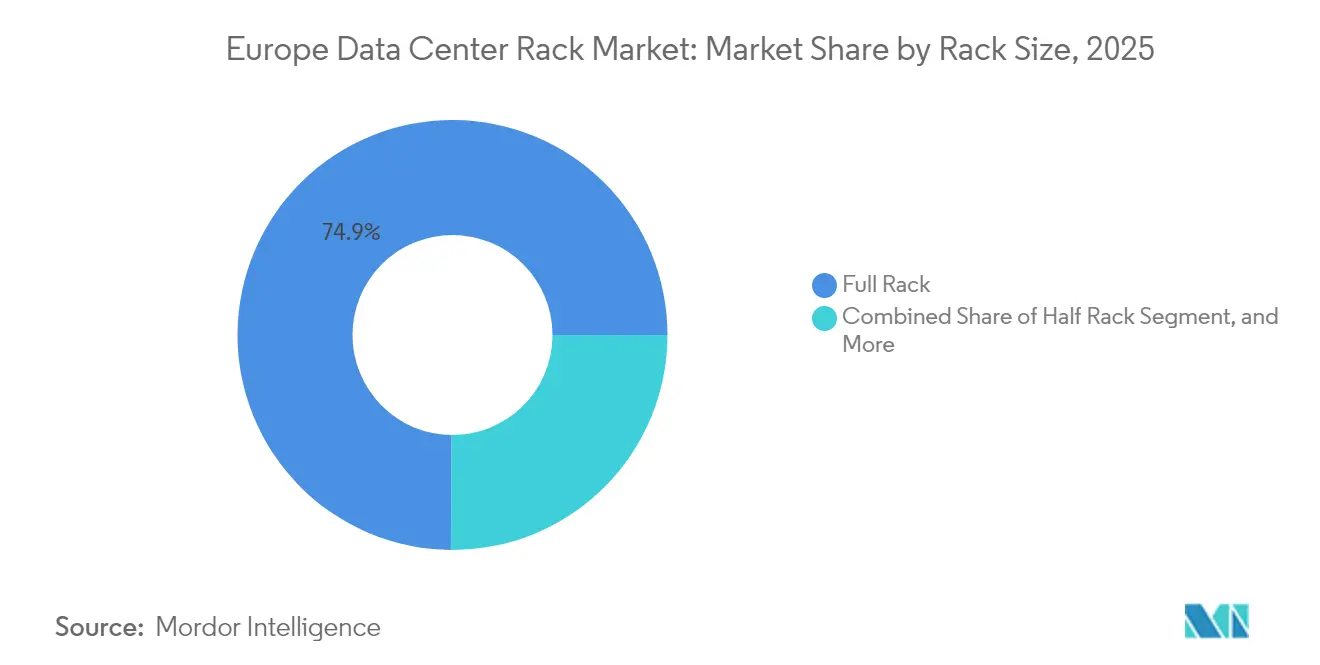

- By rack size, full racks held 74.88% revenue share in 2025; quarter racks posted the highest 15.02% CAGR through 2031.

- By rack height, the 42U format commanded 60.95% of the Europe data center rack market share in 2025, while 48U tallied the fastest 17.05% CAGR to 2031.

- By rack type, cabinet enclosures secured 81.75% share in 2025 and are advancing at a 15.95% CAGR through the forecast period.

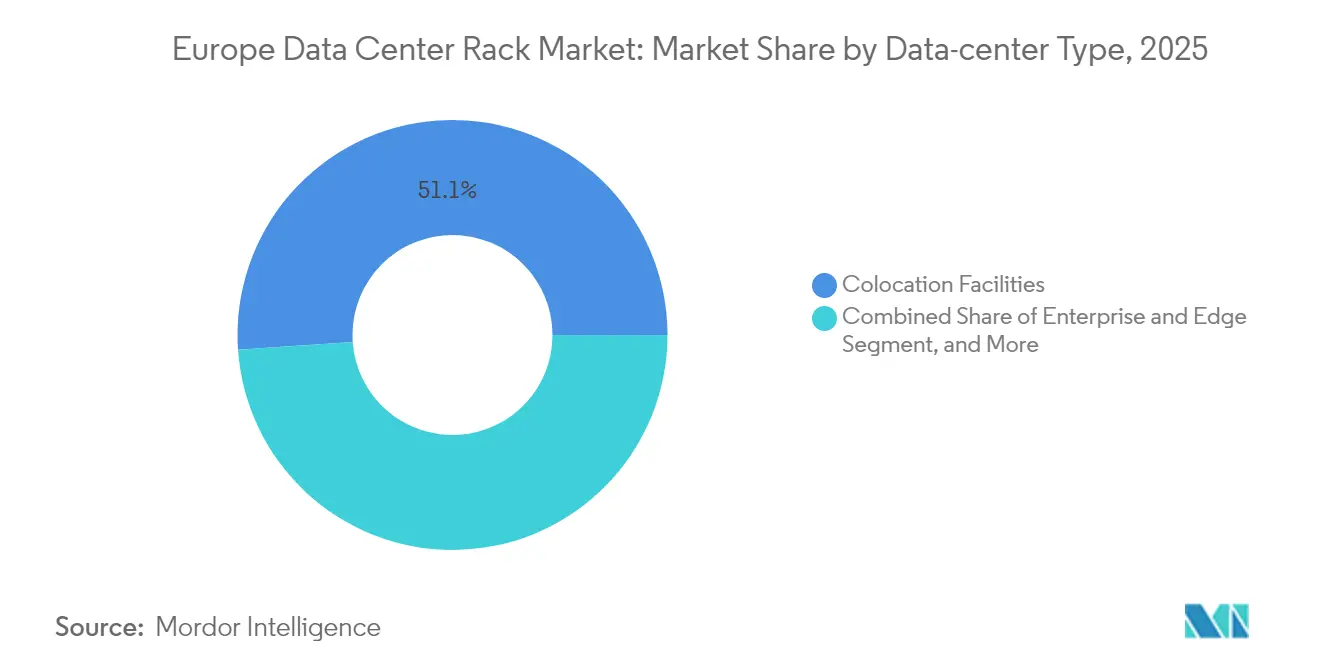

- By data center type, colocation facilities accounted for 51.10% of the Europe data center rack market size in 2025, whereas hyperscale and cloud facilities are expanding at a 14.35% CAGR to 2031.

- By material, steel retained 82.85% share in 2025, yet aluminum records the quickest 16.55% CAGR over 2026-2031.

- By country, Germany led with 18.95% share in 2025, while Ireland is set to grow at 15.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures for Europe feed into a broader worldwide estimate rather than constituting a standalone measure. Mordor Intelligence’s data center rack market size captures this aggregation across all regions, globally.

Market Trends and Insights

Drivers Impact Analysis of Europe Data Center Rack Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hyperscale expansion | +3.2% | Germany, Netherlands, Ireland, France | Medium term (2-4 years) |

| Rising adoption of high-density computing | +2.8% | FLAP-D hubs | Short term (≤ 2 years) |

| Government digitalisation initiatives | +1.9% | EU-wide, Nordic focus | Long term (≥ 4 years) |

| Growth of colocation services | +2.1% | Western and Eastern Europe | Medium term (2-4 years) |

| Shift to OCP-compliant open-rack designs | +1.4% | Netherlands, Germany, Nordics | Medium term (2-4 years) |

| Surge of edge micro-data centers | +1.6% | Spain, Italy, Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Hyperscale Expansion

Hyperscale operators are rolling out capacity at an unprecedented cadence across the continent, making standard 1 MW racks commonplace instead of experimental. Project timelines now compress to months, compelling suppliers to pre-engineer modular frames that arrive ready for liquid cooling. Sovereign data rules amplify this momentum because global cloud providers must localize processing inside national borders. Bulk orders in the tens of thousands of units drive economies of scale, allowing hyperscalers to dictate design parameters that become de facto European benchmarks. The resulting volume lifts the Europe data center rack market by accelerating replacement cycles at existing campuses and doubling footprints at new greenfield sites.[1]European Commission, “Digital Decade Policy Program,” EUROPA.EU

Rising Adoption of High-Density Computing

Artificial intelligence and machine-learning clusters now consume up to 500 kW per rack, far exceeding the airflow limits of legacy frames. European facilities respond by adopting direct-to-chip or immersion cooling modules that bolt into new rack designs. Thermal performance becomes a lead specification, prompting manufacturers to embed coolant manifolds, heat exchangers, and redundant pump kits within the rack envelope. High-density rollouts no longer stay inside hyperscale walls; research labs, automotive design houses, and financial traders also procure specialized frames, expanding the addressable market. These deployments shorten refresh intervals because GPU roadmaps outpace earlier server generations, pushing the Europe data center rack market toward higher unit sales.[2]Research Institutes of Sweden Team, “Thermal Management for High-Density Racks,” RISE.SE

Government Digitalisation Initiatives

The European Union’s Digital Decade targets that 75% of enterprises adopt cloud, big data, or AI by 2030, and this policy steers public and private investment into new capacity. National programs in France, Germany, and the Nordics provide tax incentives for domestically sourced equipment, including racks built with recycled steel or low-carbon aluminum. Operators bidding on government workloads must document supply-chain provenance and energy performance, rewarding vendors that integrate monitoring sensors and power-usage-effectiveness dashboards at the factory stage. Such policy-driven demand gives European manufacturers a competitive edge and stabilizes long-term order pipelines.[3]Eurostat Staff, “Digital Economy and Society Statistics,” EUROSTAT.EC.EUROPA.EU

Growth of Colocation Services

Institutional capital flows into European colocation continue to rise, fueled by enterprises divesting on-premise IT rooms in favor of shared facilities that guarantee compliance and uptime. Colocation providers differentiate by offering pre-cabled, high-density racks certified for GPU clusters alongside standard enterprise SKUs. Multi-tenant environments require flexible load ratings, secure side panels, and adjustable airflow baffles, spurring innovation among rack vendors. Standardization across portfolios reduces maintenance costs, while scalable design options attract tenants from varied industries. This virtuous cycle enlarges the Europe data center rack market because every new colocation hall launches with thousands of cabinets installed on day one.

Restraints Impact Analysis of Europe Data Center Rack Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX of advanced racks | −1.8% | Smaller European markets | Short term (≤ 2 years) |

| Supply-chain disruptions and steel volatility | −1.2% | EU manufacturing hubs | Medium term (2-4 years) |

| Stringent energy-efficiency regulations | −0.9% | Germany, Netherlands, Denmark | Long term (≥ 4 years) |

| Skilled rack-integration talent shortage | −1.1% | Western and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX of Advanced Racks

Liquid-cooled frames with integrated manifolds and redundant busbars cost three to four times more than traditional air-cooled cabinets. Smaller enterprises hesitate to absorb this premium without clear return-on-investment projections, especially when workloads remain below 50 kW per rack. Colocation operators must balance premium SKU demand with price-sensitive tenants, often delaying full-scale rollouts until anchor customers sign. National incentive programs vary widely, creating a patchwork of subsidy eligibility that complicates budgeting. These financial hurdles slow adoption velocity and shave points off the Europe data center rack market CAGR during the next two years.

Limited Availability of Skilled Rack-Integration Technicians

European operators report that one in two projects experiences staffing delays because crews trained on liquid cooling, high-voltage wiring, and leak-detection maintenance are scarce. The skill shortage lengthens commissioning timelines and forces premium pay rates that inflate total project cost. Apprenticeship programs lag behind technology evolution, leaving new graduates unfamiliar with immersion baths or dielectric fluid handling. Edge deployments in tier-2 cities face even steeper challenges because specialists gravitate to established FLAP-D hubs. Unless training capacity scales quickly, technician scarcity will cap the ramp-up speed of advanced racks and temper growth prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Data Center Rack Market Segment Analysis

By Rack Size:

Full Racks Propel Density GainsFull racks generated the bulk of unit demand and captured 74.88% share in 2025, a dominance that continues as enterprises consolidate scattered half-rack footprints into fewer, denser enclosures. This format now anchors large orders from colocation and hyperscale campuses, each seeking uniform rows that simplify power whips and cooling manifolds. Wider frames support side-to-side cooling loops and heavy immersion tanks, features essential for AI clusters. At the opposite end, quarter racks remain favored in retail branches and micro-edge shelters where floor space is expensive. Supply-chain efficiencies accrue because vendors mass-produce accessories, cable trays, and rear-door heat exchangers sized for full racks, further reinforcing their leadership in the Europe data center rack market.

Operators also appreciate full racks for lifecycle economics. Uniform dimensions allow reuse during data hall revamps, reducing capital outlay. Service teams carry fewer spare kits, and monitoring software can apply one template across thousands of identical cabinets. The Europe data center rack industry views these attributes as critical when forecasting workloads that may double inside five years, especially as new chip roadmaps demand ever greater wattage per square meter. Consequently, full racks will remain the primary growth engine even as niche sizes sustain specialized roles.

By Rack Height:

48U Configurations Maximize Retrofit ValueWhile the legacy 42U height retained 60.95% share in 2025, demand now swings toward 48U alternatives that yield six extra unit positions without raising ceiling height requirements. Facility owners prefer this incremental density gain because it avoids structural renovation yet creates room for power distribution units and liquid manifold trays. High-growth sectors such as automotive design, genomic research, and financial analytics load heavy GPU nodes that benefit from the added vertical clearance. The Europe data center rack market size for 48U models is projected to expand at 17.05% CAGR, outpacing every other height category.

The taller format also simplifies cable management by separating network, power, and cooling bundles into distinct vertical zones. Manufacturers respond by reinforcing frame torsion tolerance to counterbalance uneven weight distribution in partially populated cabinets. As racks approach 1 MW power loads, stability under vibration and thermal expansion becomes critical. Height evolution thus mirrors the overall trajectory toward higher density and integrated fluid cooling, reinforcing 48U’s ascent throughout new build and retrofit programs.

By Rack Type:

Cabinet Enclosures Deliver Secure, Controlled EnvironmentsCabinet designs dominated 81.75% of installations in 2025 because enclosed frames protect mission-critical hardware from unauthorized contact, dust ingress, and electromagnetic interference. Enclosures also let operators implement hot-aisle or cold-aisle containment more effectively by regulating intake and exhaust airflow. The shift toward liquid cooling intensifies cabinet adoption since door-mounted heat exchangers and side-walled distribution plates attach easily to closed frames. Consequently, cabinet shipments grow at a 15.95% CAGR, further lifting the Europe data center rack market.

Open-frame racks continue to serve non-production labs and secure staging areas where technicians need rapid component access. Wall-mount variants occupy edge closets in retail stores and cell towers, offering a compact footprint for limited-scale workloads. Even so, demand concentration remains solidly behind cabinet enclosures because European data protection rules increasingly classify the rack itself as part of the security perimeter. Manufacturers strengthen doors, hinges, and lock sets to meet evolving compliance audits, reinforcing the trend toward enclosed architectures.

By Data Center Type:

Colocation Dominates, Hyperscale AcceleratesColocation facilities absorbed 51.10% of rack shipments in 2025, reflecting enterprise migration from on-premise server rooms toward professional hosting environments. Uniform cabinet rows simplify multi-tenant layouts, and service-level agreements require racks with integrated environmental monitoring. However, hyperscale and cloud platforms represent the fastest growing deployment model at 14.35% CAGR, propelled by AI cluster expansion and sovereign cloud mandates. Hyperscalers negotiate direct agreements with rack manufacturers, often stipulating OCP-compatible frames tailored for liquid cooling and robotic deployment. These orders come in unprecedented volumes, giving suppliers firm visibility into multiyear pipelines and galvanizing the Europe data center rack market.

Enterprise and edge categories continue to serve specialized use cases such as latency-sensitive industrial automation and healthcare imaging. Edge rollouts favor shallow, climate-sealed micro cabinets that withstand warehouse dust, factory vibration, or remote outdoor placement. Vendors broaden their catalogs to include ruggedized models, yet overall volume remains modest compared with core colocation and hyperscale segments.

By Material:

Aluminum Gains Ground on Steel DominanceSteel remained the workhorse material at 82.85% share in 2025 thanks to its strength-to-price advantage and long-standing production infrastructure. Nonetheless, aluminum shipments are rising 16.55% annually because lighter frames reduce floor loading and freight costs while enhancing thermal dispersion. Alloy development now matches steel in tensile strength, enabling racks that hold 1 MW liquid baths without deformation. The European Green Deal also spotlights embodied carbon, pushing operators toward recyclable metals with lower upstream emissions. This policy tailwind extends aluminum’s appeal across Ireland, the Netherlands, and Nordic markets where renewable energy smelting further lowers lifecycle footprints. Continued innovation in extruded profiles and modular joint systems will expand aluminum’s role in the Europe data center rack market without eliminating steel’s cost-driven presence.

Hybrid designs emerge as a compromise, combining steel posts for structural rigidity with aluminum panels and doors for weight savings. Such blends optimize cost, strength, and heat conduction. Manufacturers invest in multi-metal fabrication lines capable of mixing materials on the same production run, providing customers flexibility while mitigating commodity price volatility.

Geography Analysis

Germany Data Center Rack Market

Germany maintained pole position with 18.95% share in 2025 because Frankfurt anchors the continent’s largest internet exchange and attracts capital stacks exceeding EUR 2.9 billion (USD 3.36 billion) annually for new data center infrastructure. Operators in Frankfurt, Berlin, and Munich collectively manage over 2,700 MW of IT capacity, and compliance with the national Energy Efficiency Act drives adoption of racks with embedded power-usage-effectiveness sensors. Local demand also benefits from industrial enterprises running digital twins and real-time analytics that require onsite GPU clusters. Germany’s mature ecosystem of integrators, component suppliers, and logistic corridors accelerates deployment cycles, reinforcing its leadership in the Europe data center rack market.

Ireland Data Center Rack Market

Ireland, while smaller in absolute terms, advances at a 15.85% CAGR because hyperscale investors value its wind-rich energy grid and data sovereignty alignment inside the European Union. New campuses near Dublin integrate racks rated for immersion tanks to exploit cooler ambient temperatures, supporting AI clusters with power densities above 350 kW per cabinet. Government incentives and rapid grid-connection approvals further ease expansion, turning Ireland into a strategic redundancy node for U.S. and Asian cloud providers. These dynamics enlarge the Europe data center rack market size for Irish facilities well beyond what historical population metrics might suggest.

Broader European Markets

Elsewhere, the Netherlands, Switzerland, and Nordic nations each carve specialized niches. Amsterdam remains a connectivity hot spot despite local moratoria, so operators optimize existing halls by switching to 48U aluminum racks that squeeze more compute into legacy footprints. Switzerland’s strict confidentiality standards spur demand for domestically manufactured racks with tamper-evident seals. Denmark, Sweden, and Norway exploit hydropower and free-air cooling to attract green-minded tenants, installing cabinet enclosures equipped with door heat exchangers that leverage naturally low temperatures. Eastern European countries, led by Poland, offer lower land costs and improving fiber routes, prompting edge deployments that pair compact racks with modular power pods. Collectively, these diverse geographic strategies broaden the Europe data center rack market footprint and distribute growth beyond the traditional FLAP-D corridor.

Mordor Intelligence evaluates the data center rack market across all key regional markets, including North America, Africa, and Middle East, with deeper country-level insights covering United Kingdom, Sweden, Belgium, Ireland, Poland, and Norway.

Competitive Landscape

Competition remains moderately fragmented because no single vendor can fulfill the diverse requirements spanning hyperscale, colocation, edge, and enterprise use cases. Schneider Electric, Rittal, and Vertiv lead on integrated solutions that bundle power distribution units, cooling manifolds, and remote-monitoring software inside pre-engineered racks. Their strong field support and extensive partner ecosystems sustain share amid continual design refreshes. Eaton and Panduit complement this group by supplying cable management and busway components that snap into multiple rack brands, fostering interoperability. The Europe data center rack industry also includes Open Compute Project contributors that champion cost-optimized frames built on shared specifications, eroding proprietary lock-in and abbreviating certification cycles.

Technological differentiation now centers on cooling integration. Vertiv released a turnkey liquid-cooling service line that couples coolant distribution units with rack-mounted cold plates, appealing to operators wary of multi-vendor coordination. Rittal invests in rear-door heat exchangers that retrofit onto installed cabinets, extending the life of earlier assets. Meanwhile, Schneider Electric pilots robotic rack handling to streamline server swaps and reduce technician fatigue. Start-ups target edge niches with rugged micro racks capable of withstanding wide temperature swings and physical shocks, features less critical in climate-controlled hyperscale halls.

Vendor strategies also respond to regulatory change. European Union mandates for reporting and reducing greenhouse emissions reward suppliers that disclose cradle-to-gate carbon metrics and embed telemetry for ongoing measurement. Manufacturers incorporating recycled aluminum or low-carbon steel can bid on public-sector projects reserved for sustainable equipment. The resulting competitive matrix favors companies that marry engineering prowess with transparent environmental credentials, factors that will reshuffle share positions over the forecast horizon.

Europe Data Center Rack Industry Leaders

Rittal GMBH & Co.KG

Schneider Electric SE

Legrand SA

Eaton Corporation plc

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Europe Data Center Rack Market Companies Covered in this Report

- Schneider Electric SE

- Rittal GmbH and Co. KG

- Vertiv Group Corporation

- Eaton Corporation plc

- Legrand SA

- nVent Electric plc

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- Fujitsu Ltd.

- Cisco Systems Inc.

- Lenovo Group Ltd.

- Huawei Technologies Co. Ltd.

- International Business Machines Corp.

- Panduit Corp.

- Super Micro Computer Inc.

- Tripp Lite (Eaton)

- Chatsworth Products Inc.

- Black Box Corp.

- APC by Schneider Electric

- Vertiv (Geist)

Recent Industry Developments in Europe Data Center Rack Market

- June 2025: Apto unveiled plans for a EUR 3 billion (USD 3.47 billion) campus in Lacchiarella, Italy, spanning 228,000 square meters and stipulating liquid-ready 1 MW rack rows for hyperscale tenants.

- May 2025: A joint venture among MGX, BPIFrance, MistralAI, and Nvidia announced an exascale data center campus in France focused on low-carbon operations and AI-centric rack designs.

- April 2025: Smart Campus and Schneider Electric agreed to develop a 26 MW facility in Sines, Portugal, powered entirely by renewable energy and outfitted with racks featuring integrated heat-recovery loops.

- April 2025: Apollo Funds finalized the purchase of Stack Infrastructure’s European colocation business, adding seven sites across Stockholm, Oslo, Copenhagen, Milan, and Geneva and standardizing cabinet models across the portfolio.

Europe Data Center Rack Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the Europe data center rack market as all new, factory-built enclosures that house compute, storage, or network gear inside colocation, hyperscale, enterprise, and edge facilities across the European Union, United Kingdom, EFTA states, and candidate nations. A rack, in this context, is a metal frame or cabinet configured to the EIA-310 19- or 23-inch width standard and sold with load-bearing rails, cable management, and airflow features. According to Mordor Intelligence, demand is tracked in value terms, expressed in U.S. dollars at constant 2024 exchange rates.

Scope exclusion: Aftermarket accessories, refurbished racks, containment aisles, and non-IT industrial cabinets remain outside our coverage.

Segments Covered in This Report

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Rack Height

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Material

- By Country

- Germany

- United Kingdom

- France

- Netherlands

- Ireland

- Switzerland

- Denmark

- Sweden

- Italy

- Spain

- Poland

- Norway

- Austria

- Rest of Europe

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed data-center design engineers, colocation procurement heads, and regional systems integrators across Germany, Ireland, the Nordics, and Southern Europe. These discussions clarified average selling prices, emerging liquid-ready rack specifications, and lead-time shifts, allowing us to reconcile secondary indicators with on-ground purchasing behavior.

Desk Research

We began by mapping the installed data-center footprint through publicly available sources such as Eurostat capacity statistics, national ICT spending dashboards, the European Data Centre Association project list, and customs shipment records. Government tender portals, financial filings, and technical journals provided power-density norms and typical rack pricing. Our analysts then tapped paid datasets, D&B Hoovers for vendor revenues, Dow Jones Factiva for deal flow, and Marklines for OEM supply to cross-reference shipment volumes and contract values.

Trade association white papers, patent abstracts in Questel, and energy-efficiency guidelines from EN 50600 rounded out the picture. The sources cited are illustrative rather than exhaustive; many additional publications supported data validation and concept clarity.

Market-Sizing & Forecasting

A top-down production and trade reconstruction establishes the 2024 baseline, drawing on rack import declarations, domestic fabrication output, and CAPEX disclosures, which are then corroborated through selective bottom-up checks such as sampled ASP × shipment counts from six prominent suppliers. Key variables like average rack count per added megawatt of IT load, rack height migration (42U to 48U), price premiums for cabinet enclosures, data-center construction pipeline, and hyperscale expansion rate feed a multivariate regression that projects demand to 2030. Gaps in bottom-up inputs, for example, missing open-frame volumes, are bridged by applying validated penetration ratios from primary interviews.

Data Validation & Update Cycle

Before sign-off, analysts perform variance scans against independent metrics like European server shipments and colocation absorption. Any anomaly above five percent triggers a model rerun and expert reconfirmation. Reports refresh every twelve months, with interim updates if material events, major hyperscale investment or regulatory shifts, occur.

How Mordor Intelligence's Europe Data Center Rack Market Size Compares to Other Published Estimates

Published estimates often differ because firms choose dissimilar geographic scopes, bundle accessories, or inflate prices to account for supply-chain volatility.

Key gap drivers in this market include whether second-hand racks are counted, if Middle East sales slip into regional totals, the handling of FX translation, and the cadence at which hyperscale build-outs are refreshed. Mordor Intelligence anchors results to a narrowly defined scope, yearly primary validations, and constant-currency treatment, so decision-makers receive a balanced, transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 785.1 million (2025) | Mordor Intelligence | - |

| USD 6.22 billion (2024) | Global Consultancy A | Includes power distribution units and Middle East data, applies fixed ASP uplift |

| USD 1.08 billion (2023) | Regional Consultancy B | Uses installed-base valuation and static FX rates |

| USD 1.5 billion (2025) | Trade Journal C | Excludes open-frame racks and skips primary validation |

Taken together, the comparison shows that once accessory bundles, geography creep, and pricing assumptions are stripped away, our disciplined selection of variables delivers a dependable reference point that clients can confidently build upon.

Key Questions Answered in the Report

How fast is demand for racks in European hyperscale facilities growing?

In the Europe data center rack market, hyperscale and cloud campuses represent the fastest segment, expanding at 14.35% CAGR as operators deploy 1 MW liquid-cooled cabinets for AI workloads.

Which rack height is preferred for retrofit projects across Europe?

In the Europe data center rack market, the 48U format leads retrofits because it adds six rack units of capacity without altering ceiling heights, growing at 17.05% CAGR.

Why are aluminum racks gaining traction in new European data centers?

In the Europe data center rack market, aluminum frames lower floor loads, improve heat dispersion, and meet embodied-carbon goals, contributing to a 16.55% CAGR for the material segment.

What role do government policies play in rack procurement?

EU digitalisation targets and energy-efficiency rules require telemetry-enabled, locally sourced racks, steering orders toward compliant suppliers.

Which country provides the highest growth opportunity through 2031?

In the Europe data center rack market, Ireland posts the quickest 15.85% CAGR because renewable power and favorable tax regimes attract extensive hyperscale investment.

What is the main barrier slowing advanced rack adoption among smaller operators?

High upfront capital expenditure for liquid-ready racks, priced up to four times higher than air-cooled alternatives, deters budget-constrained buyers.

Page last updated on: