Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

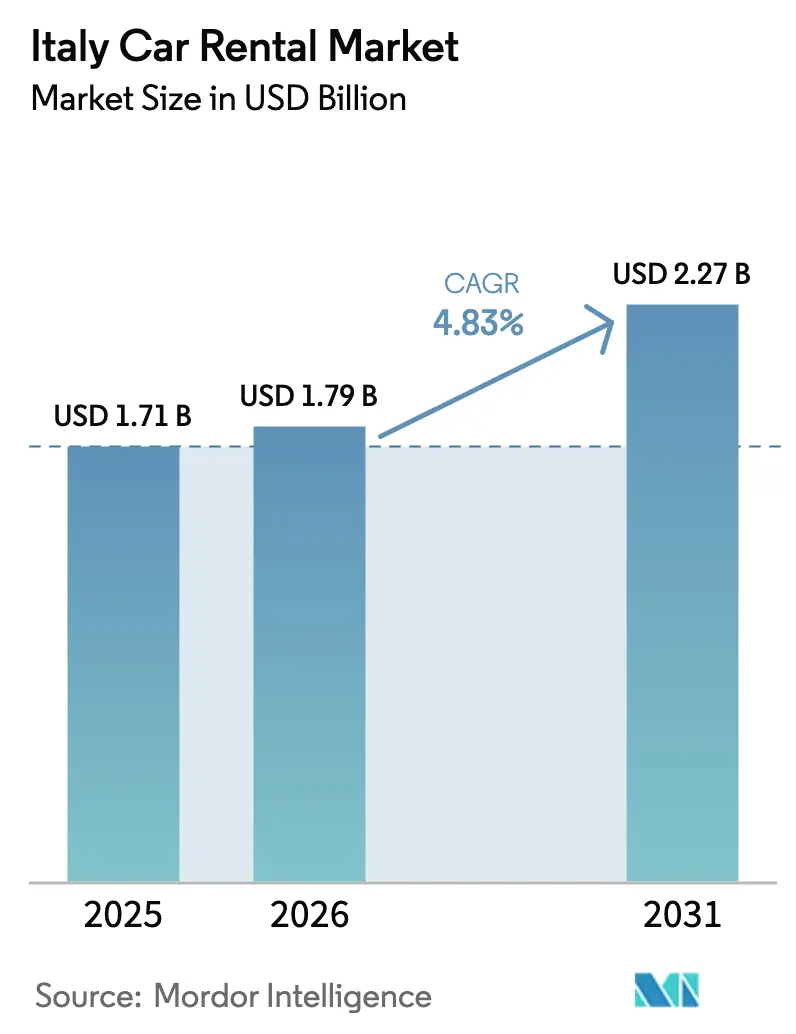

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Car Rental Market Analysis by Mordor Intelligence

The Italian car rental market size is expected to increase from USD 1.71 billion in 2025 to USD 1.79 billion in 2026 and reach USD 2.27 billion by 2031, growing at a CAGR of 4.83% over 2026-2031. As operators navigate rising procurement costs and shifting Zona a Traffico Limitato (ZTL) regulations, fleet electrification, digital booking adoption, and omnichannel distribution are broadening the total addressable market. Online bookings now represent a significant portion of revenue, reducing acquisition costs but also making operators vulnerable to metasearch commissions. While leisure-driven short-term rentals remain the primary revenue source, there's a notable surge in long-term corporate contracts and peer-to-peer platforms, diversifying income streams. Growth is notably stronger in the south, with Sardinia and Sicily witnessing accelerated expansion, fueled by airport enhancements and increased hospitality investments. Key competitive advantages now hinge on real-time fleet visibility, clear pricing, and access to in-house EV charging stations, a feature prominently offered by industry leaders like Drivalia.

Key Report Takeaways

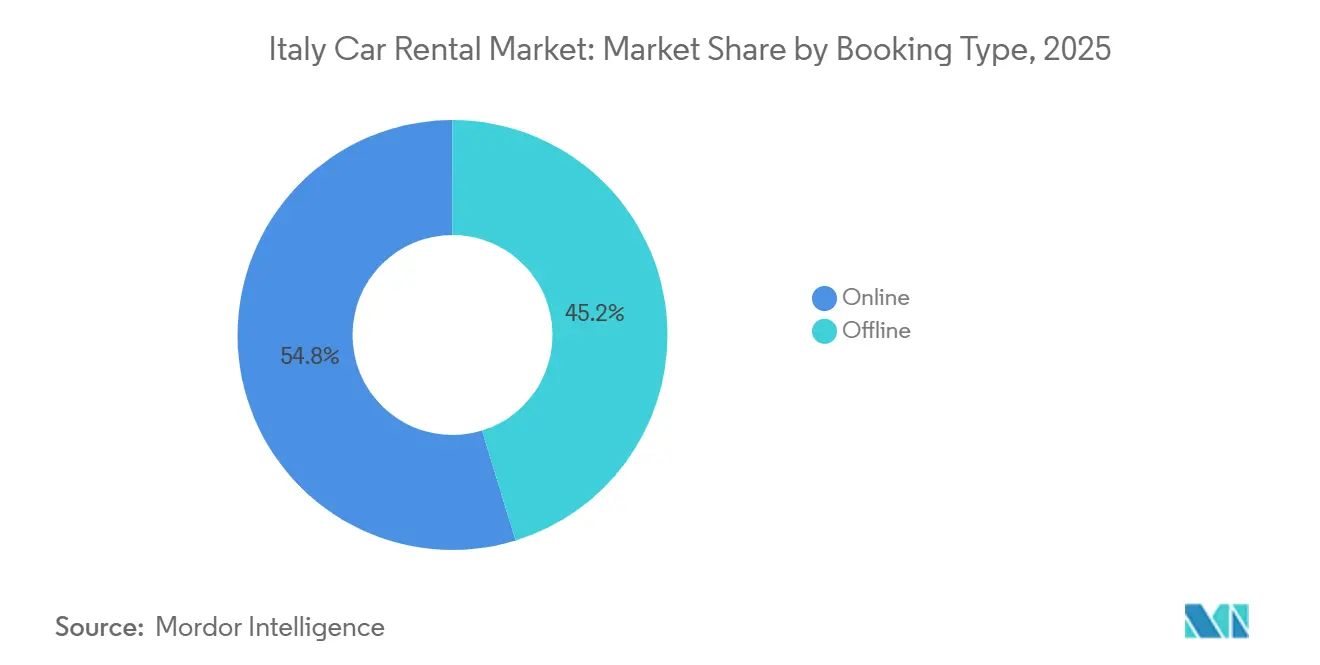

- By booking mode, online platforms led the Italian car rental market with 54.76% market share in 2025 and are projected to grow at a 7.11% CAGR through 2031.

- By application, leisure travel accounted for 64.11% of the Italian car rental market share in 2025 and is forecast to expand at a 7.44% CAGR through 2031.

- By end user, self-drive individual rentals held 43.86% Italian car rental market share in 2025, while peer-to-peer platforms are set to grow the fastest at a 7.78% CAGR through 2031.

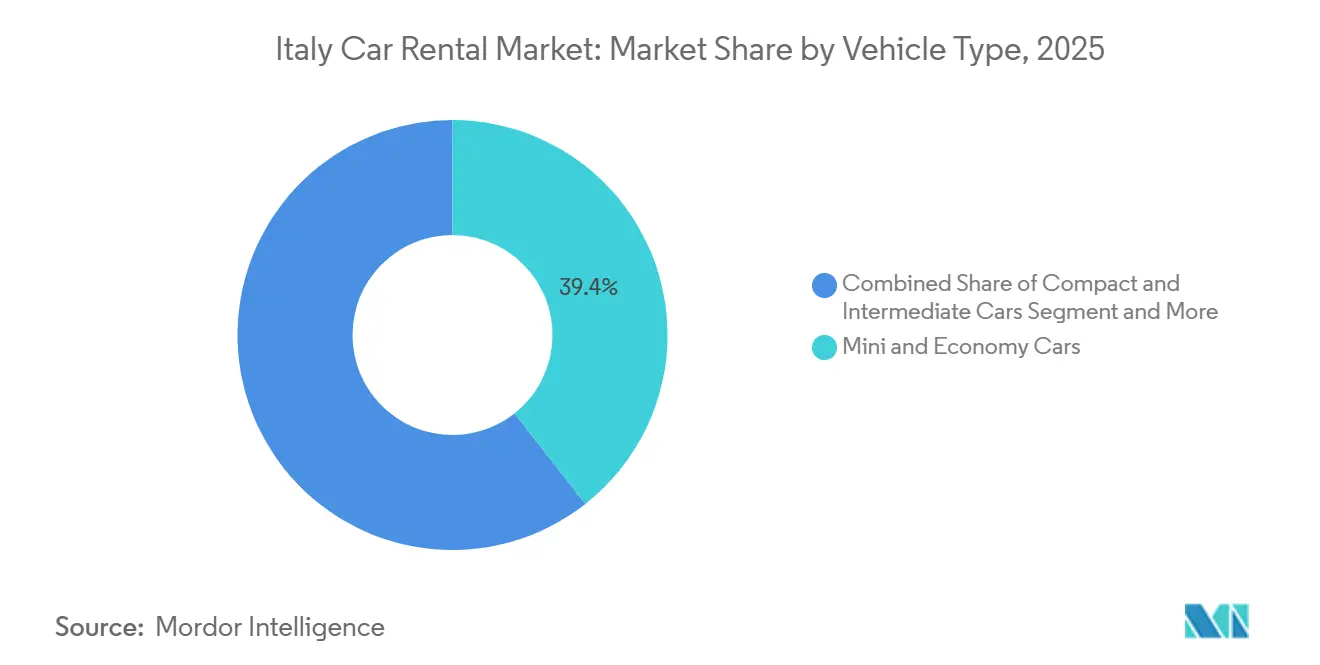

- By vehicle type, mini and economy cars captured 39.38% of the Italian car rental market share in 2025, whereas SUVs and MPVs will post the quickest 7.54% CAGR between 2026 and 2031.

- By rental length, short-term agreements accounted for 72.12% Italian car rental market share in 2025, but long-term contracts are projected to grow at a 7.51% CAGR through 2031.

- By region, Northern Italy dominated the Italian car rental market with 48.16% market share in 2025, while Southern Italy and the Islands are on track for the fastest 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound and Pent-Up Travel Demand | +0.9% | National hot spots—Rome, Florence, Venice, Amalfi | Short term (≤ 2 years) |

| Corporate Travel Recovery in Key Hubs | +0.8% | Milan, Turin, Bologna, Rome | Medium term (2-4 years) |

| Expansion of Omni-Channel and App-Based Booking Platforms | +0.7% | Milan and Rome metros first | Medium term (2-4 years) |

| Rise of EV Rentals Driven by ZTL Incentives | +0.6% | Rome, Milan, Florence, Bologna, Turin | Long term (≥ 4 years) |

| Sustainability-Linked Corporate Fleet Agreements | +0.5% | Northern industrial corridor | Long term (≥ 4 years) |

| Mobility-as-a-Service Subscription Models Gaining Traction | +0.4% | Milan, Rome, Turin; secondary cities next | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound And Pent-Up Travel Demand

International arrivals rose 6.8% in Q4 2024 to 250.1 million overnight stays, lengthening the high season beyond July-August[1]“Overnight Stays in Italian Accommodation,” Istat, istat.it. Fleet utilization benefits from higher shoulder-month volumes, helping to avoid winter troughs that previously dipped significantly. The leisure segment, projected to capture a significant revenue share and achieve steady growth, is banking on maintaining its visitor momentum. In response to new transparency regulations, operators are now packaging fuel and insurance into flat-rate deals, enhancing average ticket values. While rising airfare and lodging costs might dampen discretionary travel, a surge in pent-up demand and the rise of flexible work patterns are bolstering off-peak bookings.

Corporate Travel Recovery In Key Italian Business Hubs

Rental transaction volumes remain below the pre-crisis baseline, while spending per rental has increased significantly, reflecting a robust shift towards premium EV adoption. Multinational corporations are consolidating their procurement strategies, favoring nationwide networks that seamlessly integrate with SAP Concur for automated expense tracking. While Milan’s Malpensa and Rome’s Fiumicino airports continue to serve as primary hubs, Bologna and Turin are emerging as popular alternatives as companies decentralize their offices. Mid-tier independent firms, often with fragmented operations, are feeling the squeeze from corporate volume discounts. The trajectory of growth assumptions hinges on the stabilization of hybrid work models, rather than any further contraction.

Expansion of Omni-Channel and App-Based Booking Platforms

Digital channels dominate bookings and are experiencing steady growth, driven by apps like Drivalia PLANET, which offer contactless contracts and live inventory. Verra Mobility's partnership with Locauto has integrated real-time toll charging, effectively eliminating post-trip disputes[2]“Locauto Partnership,” Verra Mobility, verramobility.com. While metasearch portals aid price discovery, they charge significant commissions. To counter this, operators provide loyalty rebates for bookings made directly through their apps. Although offline counters still attract older and last-minute travelers, their growth suggests a gradual decline. Additionally, an AGCM mandate emphasizes fee transparency, favoring digital disclosures over upselling at counters.

Rise of EV Rentals Driven By ZTL Incentives

Long-term rental fleets saw a significant surge in BEV registrations, while PHEVs experienced a notable increase from a modest baseline. Rome plans to introduce an annual ZTL fee on EVs, potentially dampening previous incentives. Meanwhile, Milan's congestion charge on combustion vehicles skews urban dynamics in favor of zero-emission alternatives. With numerous charging points, Drivalia boasts a competitive edge in cost of ownership, though infrastructure deficiencies remain evident south of Naples. Fleet operators face a dilemma: pre-order more EVs now, risking battery price drops, or risk non-compliance with the impending EU fleet-average mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality and Demand Concentration | -0.6% | Coastal and island regions | Short term (≤ 2 years) |

| High Fleet Procurement and Insurance Costs | -0.5% | National, severe for small firms | Medium term (2-4 years) |

| Competition From Ride-Hailing and Shared-Mobility Options | -0.4% | Large urban centers | Medium term (2-4 years) |

| Semiconductor Shortage Delaying Vehicle Renewals | -0.3% | National market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Seasonality And Demand Concentration

In recent months, overnight stays have increased significantly. However, during the winter, utilization lagged and remained low. Operators, facing peak summer demands, found themselves with idle fleets during the winter months. This not only squeezed their profit margins but also compelled them to offer steep discounts. While southern islands experienced high utilization rates during the summer, they dropped significantly in the winter. This drastic shift incurred repositioning costs as vehicles were moved northward to meet rising demand. The significant revenue share from short-term rentals amplifies market volatility. This instability is expected to persist until subscriptions and long-term leases stabilize the demand curves.

High Fleet Procurement and Insurance Costs

Vehicle prices have risen significantly in recent years. Concurrently, repairs associated with ADAS (Advanced Driver Assistance Systems) have led to a notable increase in premiums in California. Drivalia, benefiting from favorable financing rates, has successfully managed its large fleet and reported substantial profits. In contrast, independent operators lack such financial leverage. While operators are turning to sale-and-leaseback strategies to unlock capital, this move transfers the residual-value risk to lessors, who might respond by increasing rents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Mode: Online Channels Capture Growth Momentum

Online reservations accounted for 54.76% of the Italian car rental market share in 2025, rising at 7.11% CAGR to 2031 as smartphone penetration and metasearch transparency shift buyer behavior. Offline counters are projected to see their market share dip, though modest growth is expected. While commission pressures from aggregators are squeezing near-term margins, direct-app incentives and loyalty tiers are strategically positioned to reclaim that lost value.

Digital fee disclosures, in line with AGCM directives, are bolstering trust and accelerating adoption. Airports remain a stronghold for physical counters, accounting for a significant portion of transactions, underscoring the need for a hybrid operational model. By reallocating staff from traditional desks to kerbside meet-and-greet services, operators are successfully reducing queue times and transitioning upsell opportunities to app notifications. Bolstered by dynamic pricing algorithms and in-app ancillary bundling, the Italian car rental market's digital channel revenue is set to grow significantly.

By Application: Leisure Keeps The Volume Crown While Business Upsells

Leisure use accounted for 64.11% of the Italian car rental market share in 2025 and will expand at a 7.44% CAGR, driven by growth in foreign overnights and broader shoulder seasons. Business rentals, although experiencing modest growth, are yielding higher daily returns as corporations increasingly opt for premium EVs aligned with ESG standards.

Key airport corridors, including Malpensa-Milan, Fiumicino-Rome, and Venice Marco Polo, dominate dual-purpose travel. Operators strategically segment their fleets: offering economy cars for families and connectivity-enhanced sedans for executives, ensuring neither under- nor over-sizing. While leisure's share of the Italian car rental market may increase slightly, it's the growth in business rentals that bolsters profitability and fuels vendor consolidation deals.

By End User: Peer-To-Peer Platforms Surge From A Low Base

Self-drive retail held a 43.86% of the Italian car rental market share in 2025, while peer-to-peer’s sub-5% share is scaling the quickest at a 7.78% CAGR through 2031. Despite regulatory uncertainties hindering widespread adoption, cost savings are enticing budget-conscious Millennials.

Conventional firms are testing white-label P2P marketplaces, aiming to reap benefits without incurring capital costs. While chauffeur-driven services remain a niche, they command significantly higher daily rates, helping offset the steep depreciation of luxury models. Corporate fleet subscriptions are generating consistent B2B revenue, providing a buffer against the seasonal fluctuations common in Italy's broader car rental market.

By Vehicle Type: SUVs And MPVs Outrun Compact Leaders

Mini and economy cars accounted for 39.38% of the Italian car rental market share in 2025, but SUVs/MPVs will grow at a 7.54% CAGR through 2031, supported by multi-generational holiday parties and alpine ski traffic. While the luxury sector sees modest volume growth, it's proving beneficial for margins, especially as premium brands yield significantly higher returns despite only a moderate increase in costs.

Car rental operators in Italy are focusing on increasing the share of SUVs in their fleet. They're placing orders now, even with higher unit prices. If SUV rentals in Italy achieve higher utilization rates, the market could see a notable boost in profitability for each rental.

By Rental Length: Long-Term Contracts Stabilize Cash Flows

Short-term agreements accounted for 72.12% of the Italian car rental market share in 2025, while long-term rentals are expected to grow by 7.51% by 2031. Operating-lease style structures bundle maintenance and insurance, creating a predictable monthly income.

Forecasting residual values is vital, especially as a sluggish used-car market threatens returns. Expatriates and project-based workers find medium-term stays pertinent. By diversifying beyond holiday peaks, operators can navigate the seasonality challenges that plague the broader car rental market in Italy.

Geography Analysis

Northern Italy retained 48.16% of the Italian car rental market share in 2025, with steady business travel through Milan, Turin, and Bologna airports. Malpensa alone handled 25 million passengers, anchoring premium demand with EV preference shaped by Area C restrictions. Strong airport concessions and higher retail rents compress margins but enable same-day vehicle swaps, sustaining service leadership.

Southern Italy and the Islands will grow fastest at 6.93% CAGR through 2031, buoyed by a jump in non-resident overnights and ongoing terminal expansions in Palermo, Catania, Cagliari, and Olbia. Despite limited charging density, operators are piloting hybrid rental programs bundled with scooters to address last-mile challenges. Seasonal spikes necessitate summer fleet transfers, which increase logistics costs.

Central Italy is set to capture a significant market share, growing steadily. However, Rome's introduction of an annual EV ZTL pass could diminish the cost edge that electric fleets once enjoyed. While Fiumicino sees steady passenger traffic, heavy congestion in the city is nudging rentals towards suburban destinations. In response to shifting municipal restrictions, operators are adopting a dual fleet strategy: compact EVs for urban jaunts and larger ICE vehicles for trips to Tuscany or Umbria.

Competitive Landscape

The top suppliers—Europcar, Hertz, Avis, Sixt, and Locauto—commanded a dominant share of revenue, overshadowing a host of regional players such as Maggiore and Sicily by Car. Drivalia set itself apart with proprietary charging stations and the integrated PLANET app. However, a fine from the AGCM highlights regulatory scrutiny of ambiguous fees.

Key airports like Fiumicino, Malpensa, and Venice Marco Polo, accounting for a significant portion of rentals, serve as pivotal competitive hubs. The digital landscape is evolving; virtually all major players now offer features like keyless entry, dynamic pricing, and integrations with platforms like Expedia and Kayak. Meanwhile, smaller operators, constrained by budgets for EVs and app innovations, are shifting towards franchising or targeting luxury markets.

Mobility disruptors, including Share Now with its shared cars, Enjoy's urban presence, and Stellantis-backed Free2move, are focusing on short urban trips. This strategy poses a challenge for high-margin segments, as it diverges from traditional multi-day bookings. In response, the industry is seeing a rise in subscription models and white-label peer-to-peer offerings, aiming to embed users within expansive mobility ecosystems and move beyond mere transactional rentals.

Italy Car Rental Industry Leaders

Avis Rent A Car System, LLC

The Hertz Corporation.

Locauto Group

Sixt SE

EUROPCAR INTERNATIONAL SASU

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SBC has officially opened a new branch in Termini Imerese, marking a significant step in its strategic plan to bolster its presence throughout Sicily. Located at Piazza Europa 14, the new facility is now fully operational, offering both vehicle rental and sales services.

- July 2025: Verra Mobility Corporation, a leading player in smart mobility technology, has partnered with global car rental giant Sixt to roll out an electronic toll payment solution in Italy. Sixt will provide electronic tolling for rentals in major Italian cities: Milano, Roma, Firenze, Venezia, Bergamo, and Bologna.

Italy Car Rental Market Report Scope

The Italy car rental market report is segmented by booking mode (offline, online), application (leisure, business), end user (self-drive individual, chauffeur-drive, corporate fleet subscription, peer-to-peer rental), vehicle type (mini and economy cars, compact and intermediate cars, standard and full-size cars, SUVs and MPVs, luxury/premium cars), rental length (short-term, medium-term, long-term), and region (Northern Italy, Central Italy, Southern Italy and islands). The market forecasts are provided in terms of value (USD).

By Booking Mode

| Offline |

| Online |

By Application

| Leisure |

| Business |

By End User

| Self-Drive Individual |

| Chauffeur-Drive |

| Corporate Fleet Subscription |

| Peer-to-Peer Rental |

By Vehicle Type

| Mini and Economy Cars |

| Compact and Intermediate Cars |

| Standard and Full-Size Cars |

| SUVs and MPVs |

| Luxury / Premium Cars |

By Rental Length

| Short-Term (Less than 30 days) |

| Medium-Term (1-12 months) |

| Long-Term (Above 12 months) |

By Region

| Northern Italy |

| Central Italy |

| Southern Italy and Islands |

| By Booking Mode | Offline |

| Online | |

| By Application | Leisure |

| Business | |

| By End User | Self-Drive Individual |

| Chauffeur-Drive | |

| Corporate Fleet Subscription | |

| Peer-to-Peer Rental | |

| By Vehicle Type | Mini and Economy Cars |

| Compact and Intermediate Cars | |

| Standard and Full-Size Cars | |

| SUVs and MPVs | |

| Luxury / Premium Cars | |

| By Rental Length | Short-Term (Less than 30 days) |

| Medium-Term (1-12 months) | |

| Long-Term (Above 12 months) | |

| By Region | Northern Italy |

| Central Italy | |

| Southern Italy and Islands |

Key Questions Answered in the Report

How large is the Italy car rental market today and how fast is it growing?

The market stands at USD 1.79 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at a 4.83% CAGR.

What share of bookings already happens online?

Online platforms generated 54.76% of 2025 revenue and are expanding at 7.11% CAGR as mobile apps and metasearch sites gain traction.

Which segment is growing fastest within the industry?

Peer-to-peer rentals are the quickest riser, projected to grow 7.78% per year through 2031 as private-vehicle sharing scales in major cities.

How is electrification influencing fleet strategies?

Battery-electric registrations in long-term rental fleets jumped 39.4% in 2025, yet new ZTL fees in Rome complicate the cost case for further EV additions.

Page last updated on: