Iran Vehicles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 41.57 Billion |

| Market Size (2026) | USD 43.86 Billion |

| Market Size (2031) | USD 57.31 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

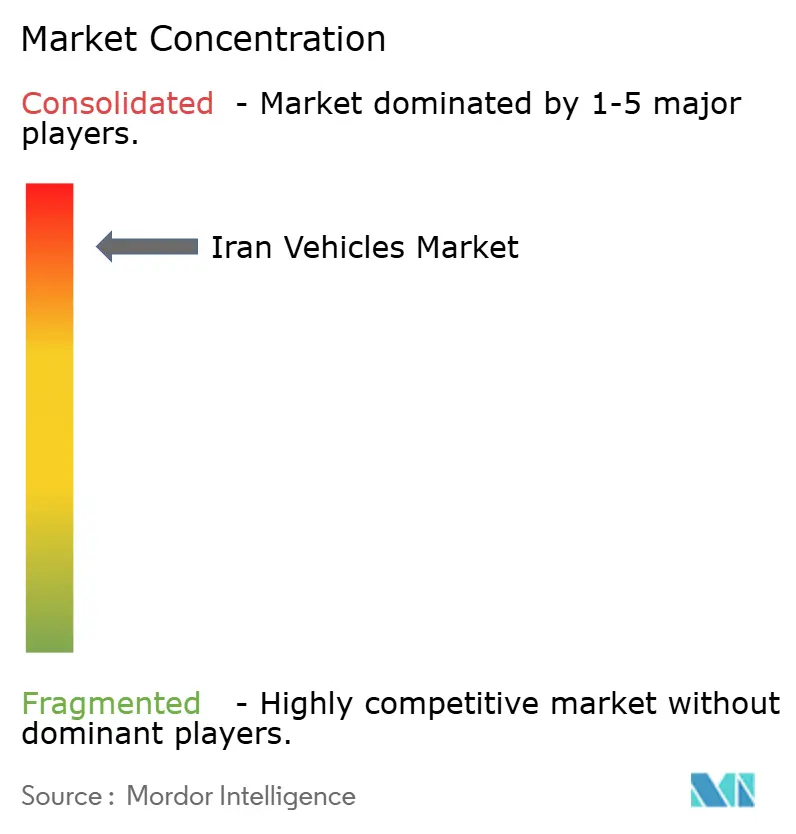

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Vehicles Market Analysis by Mordor Intelligence

The Iranian vehicle market size in 2026 is estimated at USD 43.86 billion, growing from 2025 value of USD 41.57 billion with 2031 projections showing USD 57.31 billion, growing at 5.5% CAGR over 2026-2031. Demand momentum is tied to robust domestic production of vehicles in 2023, wider policy support for compressed natural gas (CNG) vehicles, and a gradual reopening to foreign joint ventures. Competitive intensity remains moderate because the top two domestic manufacturers together control almost 80% of sales. Power-train diversification, ride-hailing growth, and barter-based supply-chain fixes are shaping investment priorities while currency volatility and electricity-grid constraints temper near-term optimism.

Key Report Takeaways

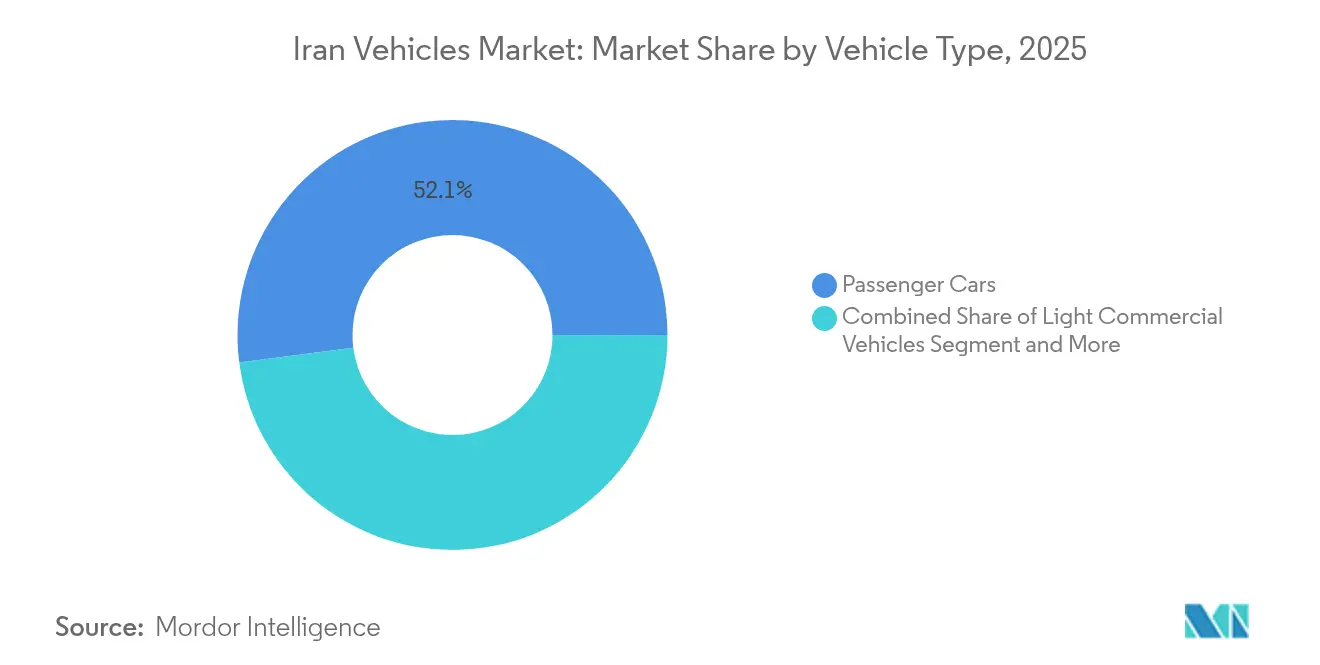

- By vehicle type, passenger cars led with 52.05% of Iran's automotive market share in 2025 and are projected to expand at an 11.05% CAGR through 2031.

- By fuel type, gasoline models commanded 67.10% of the Iranian automotive market size in 2025, whereas hybrid electric vehicles are advancing at 12.55% CAGR to 2031.

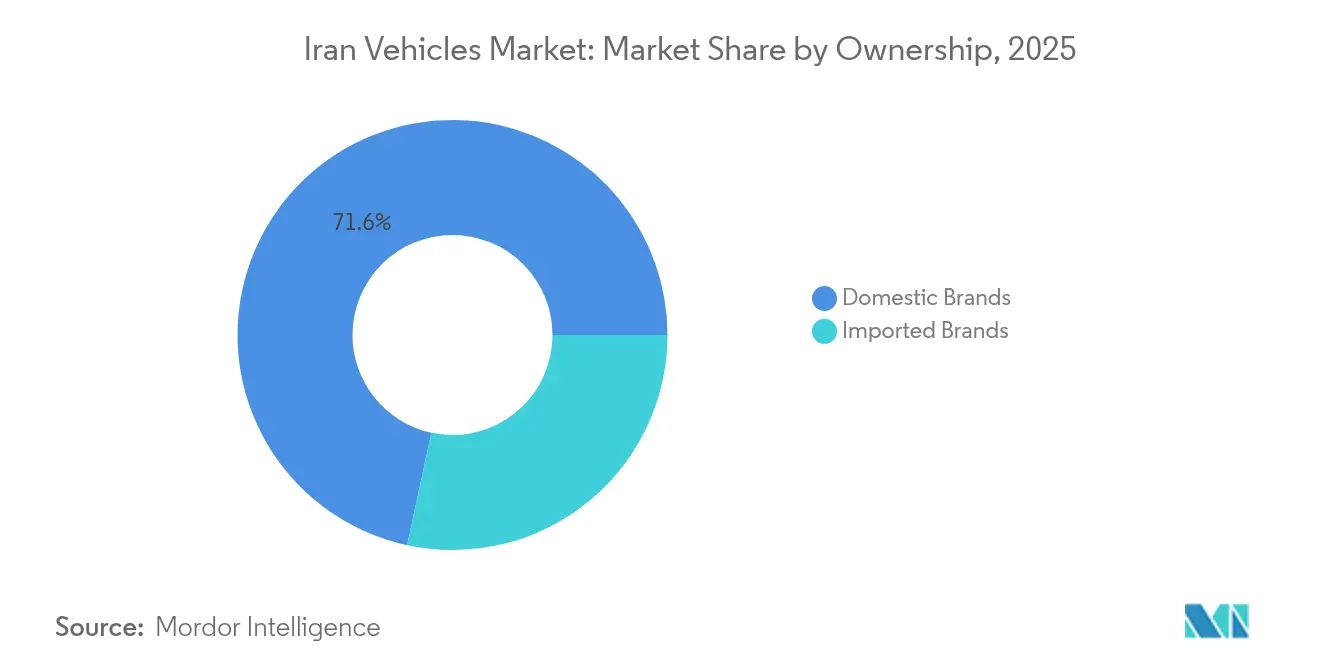

- By ownership, domestic brands held 71.62% of Iran automotive market share in 2025; imported brands recorded the fastest CAGR at 9.52% for 2026-2031.

- By customer type, individual consumers accounted for 61.40% of the Iranian automotive market size in 2025; fleet and commercial buyers posted the highest 8.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iran Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push For CNG-Compatible Powertrains | +1.8% | Tehran, Isfahan, Tabriz, Khuzestan | Medium term (2-4 years) |

| Re-Opening of Selected Jvs After 2023 Sanctions Waivers | +1.2% | Tehran, Isfahan, East Azerbaijan | Short term (≤ 2 years) |

| Subsidy-Backed Demand for Small Passenger Cars | +1.1% | Tehran, Isfahan, Khorasan Razavi, Fars | Long term (≥ 4 years) |

| Automakers' Barter Trade Unlocking Production Lines | +0.9% | Tehran, Isfahan, Markazi | Medium term (2-4 years) |

| Ride-Hailing Fleets Driving LCV Demand | +0.7% | Tehran, Isfahan, Mashhad, Shiraz | Short term (≤ 2 years) |

| Military Demand for Locally-Armoured Pickups | +0.4% | Tehran, Isfahan, Khuzestan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government push for CNG-compatible powertrains

Authorities target a 35% CNG share of national fuel use, up from 23%, and have mandated that half of new vehicles integrate CNG functionality.[1]Financial Tribune, “CNG-Hybrid Vehicles to Bridge Gasoline Supply-Demand Gap,” financialtribune.com Domestic automakers already field 3.5 million CNG vehicles supported by 2,385 active stations, a network the oil ministry is expanding. Stable CNG pricing relative to rising gasoline costs underpins consumer uptake, while Iran’s vast natural-gas reserves ensure supply security. The CNG pivot enhances energy independence, claws back gasoline imports, and positions manufacturers for export opportunities to other gas-rich economies.

Re-opening of selected JVs after 2023 sanctions waivers

Sanctions relief rekindled foreign partnerships, exemplified by Renault’s 150,000-unit plant and Mercedes-Benz Trucks’ after-sales accord.[2]Reuters Staff, “Renault forms new joint venture company in Iran,” reuters.com These collaborations inject advanced power-train know-how, raise quality standards, and unlock idle capacity precisely as a quarter of Iran’s fleet exceeds 20 years in age. Technology transfer and global supply-chain access are accelerating platform modernization across the Iran automotive market.

Subsidy-backed demand for small passenger cars

Gasoline remains subsidized at 15,000 rials per liter, sustaining consumer preference for compact sedans. Although government reforms are trimming monthly subsidized quotas, low pump prices still favor small engine volumes. The subsidy design also channels demand toward locally made models, reinforcing domestic brand dominance in the Iranian automotive market while creating fiscal tension as outlays top USD 80 billion annually.

Automakers’ barter trade unlocking production lines

A 43% plunge in imported components during 2024 exposed supply-chain fragility. Manufacturers responded by exchanging pistachio exports for Chinese parts, restoring throughput and averting protracted plant stoppages. The scheme demonstrates adaptive resilience yet ties automotive output to commodity price swings and agricultural yields.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX-Driven Parts Import Shortages | -1.4% | Tehran, Isfahan, Tabriz, Markazi | Short term (≤ 2 years) |

| Chronic Currency Depreciation Inflating Prices | -0.8% | Tehran, Isfahan, Khorasan Razavi, Fars | Medium term (2-4 years) |

| Power-Grid Shortfalls Delaying EV Charging Rollout | -0.6% | Tehran, Isfahan, Khuzestan, Mazandaran | Long term (≥ 4 years) |

| Pistachio-Price Backlash Vs Barter Schemes | -0.3% | Kerman, Fars, Khorasan Razavi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FX-driven parts import shortages

Component inflows fell to USD 653 million in 2024 and briefly collapsed to USD 26 million, forcing intermittent shutdowns. Domestic suppliers lack scale in engines and electronics, so OEMs depend on foreign currency allocations that remain constrained. Extended delivery lead times dent consumer confidence and dilute the Iranian automotive market’s growth pace.

Chronic currency depreciation inflating prices

The rial’s slide lifts input costs while state price caps limit pass-through, saddling automakers with losses. Credit lines have been expanded but remain insufficient to offset working-capital drains. Currency instability also erodes consumers’ real incomes, delaying purchases and compressing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sedans Hold Leadership as EVs Accelerate

Passenger cars, particularly sedans, retained a 52.05% share of the Iranian vehicle market in 2025, underpinned by urban commuting needs and well-established domestic platforms. Legacy models such as Iran Khodro Samand and SAIPA Tiba deliver familiar serviceability and low operating costs. The segment is growing at an 11.05% CAGR on the back of government programmes to deploy 100,000 electric taxis and expanding public charging corridors. The sedan segment, therefore, faces an evolutionary pivot toward electrified variants, while light commercial vehicles ride the surge in ride-hailing and last-mile delivery. Sport utility and multi-purpose vehicles remain aspirational choices for an emerging middle class.

Platform updates reflect a strategic shift to designs that accommodate multiple fuel types and enhanced safety features, replacing legacy models whose production has recently been halted. Manufacturers are retooling lines for flexible body-on-frame architectures aimed at both passenger and commercial derivatives. The Iranian vehicle market also sees bus and coach renewal programmes that retire aging diesel fleets in favor of CNG and hybrid units, supporting public-transport modernization initiatives.

By Fuel Type: Gasoline Dominance Meets Hybrid Momentum

Gasoline vehicles still command 67.10% of Iran's vehicle market share in 2025 because refinery output satisfies most domestic demand, and subsidies keep pump prices low. Nevertheless, the Iranian vehicle market size for hybrid models is projected to climb rapidly at 12.55% CAGR, alongside policy mandates stipulating that half of annual production include alternative power-trains. Grid bottlenecks and a lack of fast chargers slow pure-battery adoption, but hybrids circumvent range anxiety while cutting fuel bills.

Hybrid uptake is accelerated by looming gasoline deficits that could force USD 2 billion in imports annually if consumption outpaces refinery upgrades. The government’s green-fleet targets and approval of premium gasoline imports at market rates encourage consumers toward fuel-efficient technology. Diesel vehicles remain essential for heavy freight, whereas CNG usage leverages Iran’s abundant natural gas, helping stabilize fuel security.

By Ownership: Domestic Stronghold Faces Import Liberalization

Domestic manufacturers controlled 71.62% of Iran's vehicle market share in 2025, owing to decades-long import curbs and a supportive industrial policy. Up to 1,200 parts makers feed this ecosystem, delivering cost advantages versus imported competitors. However, eased import regulations post-2023 enable foreign brands to capture pent-up demand for enhanced quality and feature sets, especially in premium and electric segments. Imported vehicles will likely erode their share gradually, but domestic OEMs benefit from continued scale and preferential financing.

Joint ventures serve as an intermediate path, combining local assembly economics with international technology, mitigating foreign-exchange demands tied to fully built imports. The marketplace is evolving into a mixed arena where domestic champions must raise product sophistication to retain relevance.

By Customer Type: Individuals Lead, Fleets Surge

Individual buyers accounted for 61.40% of sales in 2025, reflecting the cultural premium on private mobility and the relative affordability conferred by low fuel prices. Yet fleet and commercial operators show the fastest 8.74% CAGR as ride-hailing platforms proliferate and e-commerce logistics mature. The Iranian vehicle market thus bifurcates: mass-market sedan volumes cater to households, while LCV and hybrid taxi demand grow among professional operators.

Government procurement also shapes specialized requirements such as armored pickups and public-transport buses. Fleet orders deliver higher utilization and predictable replacement cycles, encouraging OEMs to develop purpose-built commercial variants. Over time, shared mobility may temper individual ownership growth, but population dynamics and inadequate mass transit ensure a sizeable retail base.

Geography Analysis

Tehran province anchors the Iranian vehicle market with its dense population, skilled workforce, and adjacency to Iran Khodro and SAIPA plants. The clustering effect nurtures supplier ecosystems and research centers, reinforcing the capital’s centrality. Isfahan province follows, leveraging metallurgical assets and strategic crossroads that link national highways, making it a manufacturing and distribution hub. East Azerbaijan, with Tabriz as its capital, offers proximity to Turkey and the Caucasus, giving joint ventures an export gateway. Khuzestan contributes petrochemical raw materials for plastics and hosts niche military vehicle production, integrating upstream and downstream value chains. Northern provinces benefit from gas pipelines that buttress CNG vehicle rollouts, whereas southern coastal provinces provide port capacity for component inflows and prospective vehicle exports. Regional specialization balances national resilience: engine machining in Markazi, electronics in Qom, and glass in Yazd. The integrated geography supports the Iranian vehicle market’s ability to absorb shocks such as FX shortages by reallocating subassembly contracts within the country.

Competitive Landscape

Market structure is highly concentrated: Iran Khodro and SAIPA, together accounting for nearly half of unit sales. This duopoly tempers price competition but imposes high entry barriers for newcomers. The strategy revolves around scaling joint-venture technology, securing parts through barter, and upgrading platforms to meet evolving safety and emission regulations.

Capacity expansion plans include a 150,000-unit Renault facility and localized assembly of Mercedes-Benz Actros trucks. Domestic firms explore vertical integration for key components to cut FX exposure, while barter deals trading pistachios for electronics substitute conventional import finance. White-space opportunities in electric vehicles and premium SUVs attract smaller players such as Bahman Group, which leverage CKD kits from Chinese partners.

Ride-hailing giant Snapp exerts downstream influence, potentially shaping OEM fleet specifications. The Iranian vehicle market could see consolidation as smaller assemblers struggle with currency volatility, compliance expenses, and technology gaps. In parallel, export ambitions to neighboring markets hinge on meeting regional homologation standards, for which international partnerships remain crucial.

Iran Vehicles Industry Leaders

Iran Khodro

SAIPA Group

Pars Khodro

Bahman Group

Kerman Motor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AvtoVAZ announced localization plans to assemble the latest Lada model in Iran, aiming to expand exports to Iran, Kazakhstan, and Vietnam.

- July 2024: Pars Khodro unveiled its first full electric hatchback, a rebadged Leapmotor T03, offering 107 hp and a 403 km NEDC range.

- April 2024: MAPNA Group confirmed construction of 20 EV charging stations nationwide to underpin the rollout of 100,000 electric taxis.

Iran Vehicles Market Report Scope

A vehicle is a machine that transports people or cargo from one place to the desired location. The Iranian automotive industry is focused on passenger and commercial vehicles.

The Iranian automotive industry market is segmented by vehicle type and fuel type. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By fuel type, the market is segmented into IC engines and electric.

For each segment, the market sizing and forecast are done in terms of value (USD).

| Passenger Cars | Hatchback |

| Sedan | |

| Sport Utility Vehicle | |

| Multi-Purpose Vehicle | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches |

| Gasoline |

| Diesel |

| Hybrid Electric |

| Battery Electric |

| Other |

| Domestic Brands |

| Imported Brands |

| Individual Consumers |

| Fleet and Commercial Operators |

| Government and Defense |

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| Sport Utility Vehicle | ||

| Multi-Purpose Vehicle | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Hybrid Electric | ||

| Battery Electric | ||

| Other | ||

| By Ownership | Domestic Brands | |

| Imported Brands | ||

| By Customer Type | Individual Consumers | |

| Fleet and Commercial Operators | ||

| Government and Defense |

Key Questions Answered in the Report

What is the current size of the Iran automotive market?

The Iran automotive market stands at USD 43.86 billion in 2026 and is projected to grow to USD 57.31 billion by 2031.

Which companies dominate the Iran automotive market?

Iran Khodro and SAIPA collectively hold nearly 80% of total sales, establishing a duopoly structure.

How fast are electric vehicles growing in Iran?

Battery electric vehicles are forecast to register a 17.10% CAGR from 2026 to 2031 as government taxi electrification programmes expand.

Why is CNG important to Iran’s automotive strategy?

CNG leverages Iran’s vast natural-gas reserves, reduces gasoline import pressure, and benefits from over 2,300 fueling stations nationwide.

What challenges restrain the market’s growth?

Foreign-exchange shortages limiting parts imports, chronic currency depreciation inflating production costs, and electricity-grid limits on EV charging capacity are key restraints.

Page last updated on: