United States Automotive Dealership Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

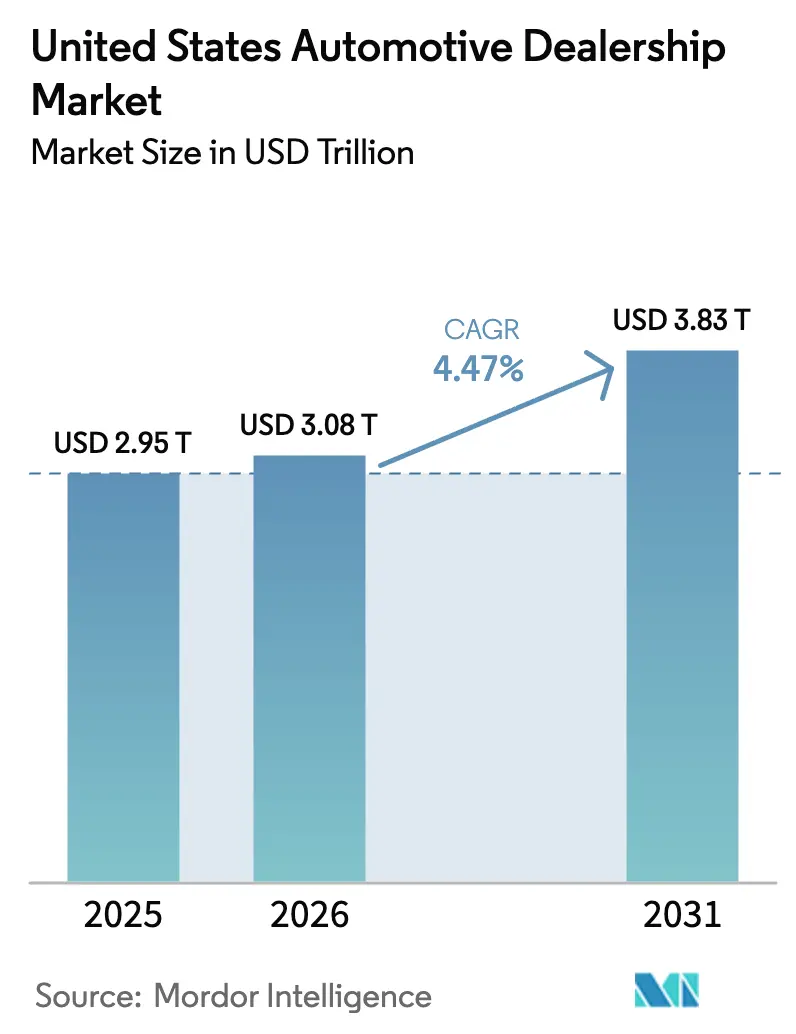

| Base Year Market Size (2025) | USD 2.95 Trillion |

| Market Size (2026) | USD 3.08 Trillion |

| Market Size (2031) | USD 3.83 Trillion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Automotive Dealership Market Analysis by Mordor Intelligence

The United States automotive dealership market size is expected to grow from USD 2.95 trillion in 2025 to USD 3.08 trillion in 2026 and is forecast to reach USD 3.83 trillion by 2031 at 4.47% CAGR over 2026-2031. Well-balanced inventories, surging certified pre-owned (CPO) demand, and heavy electrification investments are underpinning steady revenue gains even as online price transparency squeezes gross margins. Dealer-led expansion of finance and insurance (F&I) portfolios is offsetting pressure on front-end profitability, while favorable state legislation is accelerating digital retail adoption. Rising medium and heavy-commercial-vehicle sales tied to fleet electrification offer an incremental profit pool, and sustained consumer preference for light trucks and SUVs continues to lift average transaction values. At the same time, substantial capital requirements for EV-ready service bays and over-the-air (OTA) software capability are widening the competitive gap between well-funded consolidators and under-capitalized independents.

Key Report Takeaways

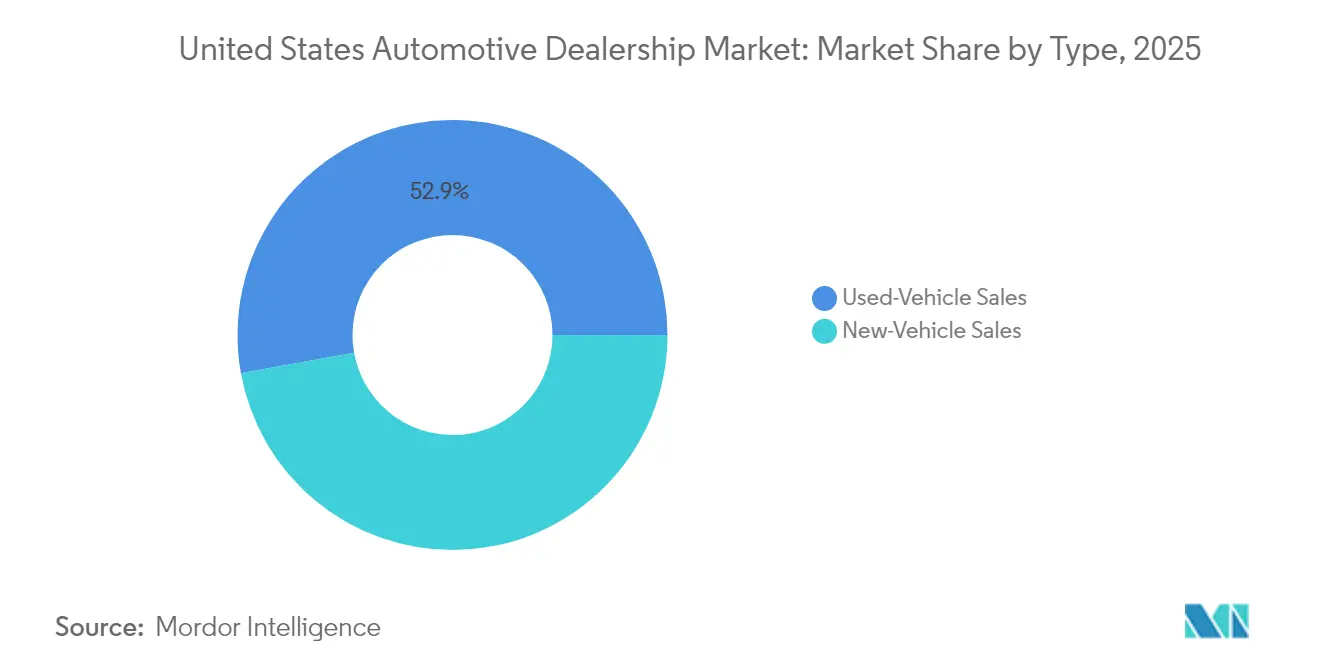

- By type, used-vehicle transactions captured 52.85% of the United States automotive dealership market share in 2025, whereas new-vehicle sales are poised to grow at a 5.41% CAGR through 2031.

- By retailer, franchised dealers retained a 57.60% share of the United States automotive dealership market size in 2025, while direct-to-consumer digital platforms record the highest forecast CAGR at 6.02% to 2031.

- By vehicle type, light trucks and SUVs led 60.70% of the United States automotive dealership market share in 2025; medium and heavy commercial vehicles are projected to advance at a 4.97% CAGR to 2031.

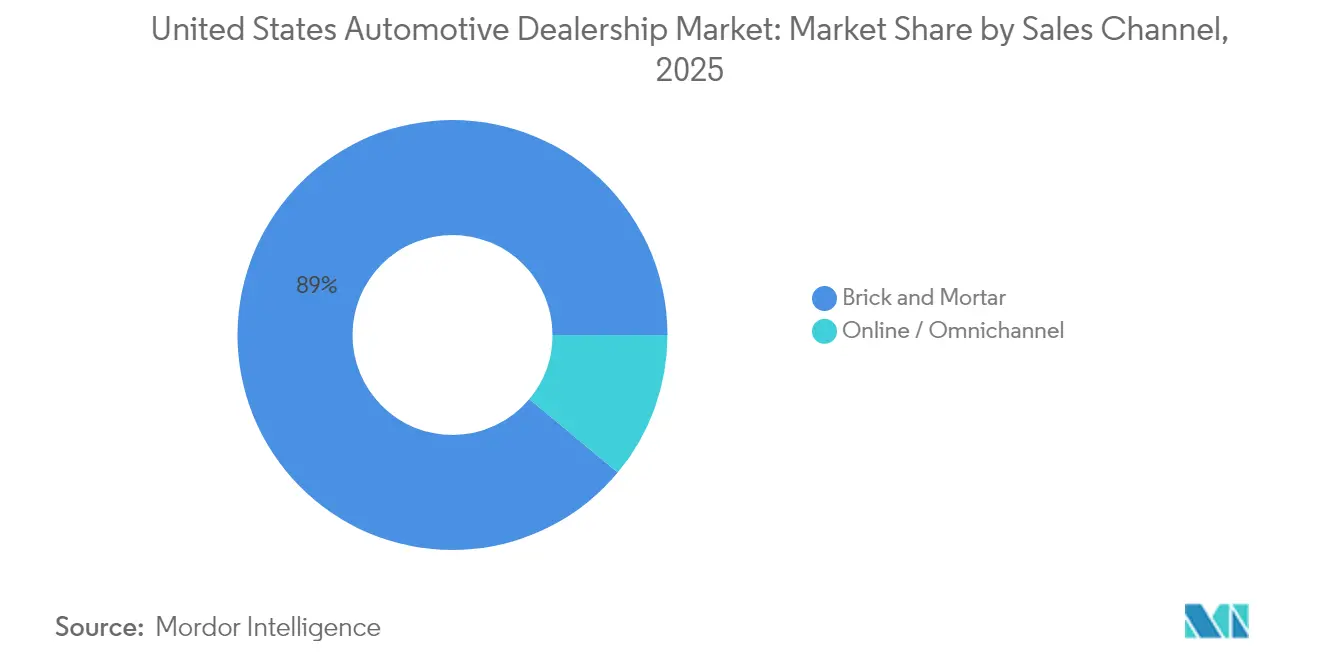

- By sales channel, brick-and-mortar outlets accounted for 88.95% of the United States automotive dealership market share in 2025; online and omnichannel sales are expanding 6.01% annually to 2031.

- By customer segment, individual buyers constituted 76.55% of the United States automotive dealership market share in 2025, yet fleet and corporate clients are scaling at a 6.32% CAGR to 2031.

- By region, the South dominated with 36.20% of the United States automotive dealership market share in 2025 and is set to grow fastest at 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Automotive Dealership Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV Model Launches | +0.9% | West and Northeast lead, spreading South and Midwest | Long term (≥ 4 years) |

| New Vehicle Inventory Recover | +0.8% | National, strongest in South and West | Short term (≤ 2 years) |

| Dealers Expand F&I Products | +0.7% | National, state regulations vary | Medium term (2-4 years) |

| Growing Certified Pre-Owned Programs | +0.6% | Nationwide, premium in Northeast luxury hubs | Medium term (2-4 years) |

| State-Level Digital Retailing Laws | +0.4% | Key states such as California, Texas, Illinois | Medium term (2-4 years) |

| OEM Subscription Models | +0.3% | National, concentrated in urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Model Launches

Franchise groups have pledged billions for EV-ready showrooms and service bays [1]“NADA Data 2025,” National Automobile Dealers Association, nada.org. Capital outlays per location range from USD 100,000 for Level 2 chargers to more than USD 1 million, where Level 3 DC fast-charging plus utility upgrades are required. Ford’s Model e Certified Elite program illustrates OEM mandates that bundle training, tooling, and charger installation under strict timelines, reshaping cap-ex planning cycles for retailers. Early movers capture incremental service profits from battery warranty work and software-subscription enablement, offsetting EVs’ lower mechanical-repair frequency. Geographic disparity persists; dealers in California and New York see higher charger utilization than peers in the Upper Midwest, yet nationwide EV registration growth in 2024 supports long-run investment viability.

Recovery in New-Vehicle Inventory Levels

OEM production stability lifted dealer stock to 3.23 million units by November 2024, close to the 3.4 – 3.5 million pre-pandemic norm. Improved supply lets retailers restore traditional incentive programs and recoup volume-based bonuses, reversing two years of margin erosion caused by constrained pipelines. Domestic brands, supported by normalized chip supply, re-establish competitive lease offers that draw payment-sensitive buyers back to showrooms. Dealers must manage slower turn-rates than in 2022’s shortage era, prompting heavier reliance on AI-driven demand-forecasting engines to avoid over-stocking. Robust inventory also strengthens the negotiating power of large dealer groups, who can bulk-purchase allocations, widening their cost advantage over smaller independents.

Dealer-Led Expansion of F&I Products

New-vehicle payment elongation has heightened consumer anxiety over long-term repair costs, making service contracts and GAP coverage feel essential rather than optional. Dealers are customizing F&I menus by powertrain, including ICE, hybrid, and EV, to optimize penetration while adhering to disparate state disclosure rules. Digital contracting platforms accelerate approvals and cut delivery times, helping preserve CSI scores even as lenders tighten underwriting standards. The January 2025 vacancy of the FTC’s CARS Rule ended imminent rulemaking. Yet, its compliance benchmarks remain industry best practice, prompting dealers to invest in auditing tools that cut exposure to penalties. Enhanced transparency boosts consumer uptake, transforming F&I into a stabilizing profit hedge against front-end price compression.

Growth of Certified Pre-Owned (CPO) Programs

Certified Pre-Owned (CPO) volumes rebounded in 2024 as warranty-seeking buyers migrated from historically expensive new vehicles, pushing CPO margins for standard used cars. Manufacturers such as Toyota broadened program tiers, allowing franchised outlets to capture 10-15% premiums above comparable non-certified units while keeping days-supply lean. Dealers that embed CPO inventory analytics into acquisition platforms secure faster turns, roughly 25% quicker than non-certified stock, freeing floorplan capacity for higher-margin vehicles. Continuous shortages of lease returns until late 2025 further elevate residual values, preserving dealer gross even in the face of tighter credit conditions. As CPO transforms from an ancillary offer into a core profit pillar, independent operators without OEM certification pathways risk ceding share to franchise rivals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher CAPEX For Service Upgrades | -0.6% | National, rural dealers face toughest hurdle | Medium term (2-4 years) |

| OEM Direct-to-Consumer Models | -0.5% | National, strongest in EV-friendly states | Long term (≥ 4 years) |

| Price Transparency Compresses Profit Margins | -0.4% | Urban markets most affected | Short term (≤ 2 years) |

| Increased FTC Compliance Costs | -0.2% | National, state-level variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX for EV and ADAS Service Upgrades

EV battery hoists, insulated storage, and ADAS calibration rigs cost USD 56,000-650,000 per rooftop [2]“The High Cost of EV-Service Readiness,” WardsAuto, wardsauto.com. Access to affordable power feeds and specialized technicians is especially constrained in rural markets, forcing some single-point operators to exit instead of refinancing aging facilities. Consolidators enjoy scale cost leverage and can amortize tooling over larger throughput, widening their variable-cost gap. OEM reimbursement programs partially defray expenses but usually require volume commitments, embedding further consolidation incentives. Consequently, capital intensity is the most immediate structural headwind for independents, lowering market-wide growth by an estimated 0.6 percentage points.

OEM Direct-to-Consumer Models

Tesla’s established agency approach and emerging entrants' advertising order-online delivery-storefront hybrids test the durability of franchise protections. While 48 states still restrict factory sales, several OEMs pilot agency pricing that fixes MSRP and positions dealers mainly as delivery and service partners. Such frameworks could erode traditional front-end grosses but stabilize inventory cost risk during downturns. Dealer associations continue lobbying to embed compensation guarantees into any new legislative carve-outs. Yet, a long-term margin drag of roughly 0.5 percentage points on the United States automotive dealership market CAGR is anticipated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Used Vehicles Anchor Revenue, New Inventory Fuels Growth

The United States automotive dealership market size for used vehicles held a 52.85% share in 2025, cementing its role as the channel’s economic backbone. Elevated residual values, bolstered by curtailed lease returns, helped dealers protect grosses even as wholesale indices normalized. Margins continue to benefit from private-party acquisition tools that circumvent auction fees and reduce inbound logistics costs. Certified tiers maintain premium pricing and 25% faster turn-rates, improving cash velocity that supports floorplan interest outlays.

New vehicles are projected to log a 5.41% CAGR, outpacing used growth through 2031 as OEM production constraints fade. Incentives averaging 6.8% of transaction price in early 2025 have pulled sidelined buyers back into showrooms, especially on entry-level trims. As supply normalizes, the United States automotive dealership market share for new vehicles is expected to climb modestly, though pricing transparency and agency pilots will cap front-end gross upside. Dealers tighten reconditioning cycles on trade-ins, aiming to flip used inventory within 27 days versus the 35-day industry median, sustaining blended gross performance across both vehicle streams.

By Retailer: Franchise Scale Meets Digital Agility

Franchised groups controlled 57.60% of the United States automotive dealership market in 2025, and direct-to-consumer digital platforms record the highest forecast CAGR at 6.02% to 2031, underpinned by exclusive OEM allocations, warranty authority, and financing captive ties that erect high entry barriers. Market consolidators leverage acquisition synergies such as Lithia’s economies in procurement and marketing to expand EBITDA per rooftop. Digital pure-plays leverage asset-light models, booking double-digit unit gains despite narrow contribution margins. Still, omnichannel hybrids are emerging, with Amazon Autos integrating dealer fulfillment to keep last-mile logistics cost-effective while preserving consumer convenience.

Independent lots retain relevance where price-sensitive shoppers value negotiation flexibility and non-OEM warranty bundles. Yet franchise operators’ mandated EV tooling and OTA software rights grant them a structural advantage in an electrified future. Over time, the United States automotive dealership market size is expected to skew toward high-performing multi-state groups as succession planning and capital intensity prompt single-store owners to divest. Franchisees that invest in click-to-buy platforms and same-day service lanes will outperform peers relying solely on legacy walk-in traffic.

By Vehicle Type: Trucks Dominate, Commercial EVs Accelerate

Light trucks and SUVs captured 60.70% revenue of the United States automotive dealership market in 2025, aided by favorable fuel-economy regulations for body-on-frame designs and strong residuals that keep payment-to-utility ratios attractive. Automakers’ shift from sedans continues, compressing passenger-car selection on dealer lots and channeling marketing dollars toward profitable pickup trims.

Medium and heavy commercial vehicle demand is climbing at a 4.97% CAGR as e-commerce and last-mile delivery fleets electrify to meet decarbonization mandates. Dealers can certify high-voltage technicians and unlock annuity-like service streams from battery inspection contracts and telemetry-driven preventive maintenance. The United States automotive dealership industry is also seeing OEMs bundle fleet-management software into vehicle sales, expanding dealers’ consultative role and embedding them deeper into client operations.

By Sales Channel: Showrooms Reinvent the In-Store Experience

Physical storefronts (Brick and Mortar) still processed 88.95% of the United States automotive dealership market transactions in 2025, reinforcing the enduring importance of tactile vehicle evaluation and trade-in appraisal. Dealers redesign facilities with express delivery bays and customer lounge workspaces to shorten cycle time and lift CSI metrics.

Online pathways are projected to scale at a 6.01% CAGR, fueled by state legalization of e-contracting, remote wet-signature equivalency, and home-delivery provisions. Retailers adopting unified data stacks seamlessly migrate consumers between website, chatbot, and in-store desks, slashing deal time by 42 minutes on average. As omnichannel matures, the United States automotive dealership market volume will still originate from dealers who master hybrid engagement rather than pure online sales.

By Customer Segment: Fleet Electrification Outpaces Retail Gains

Retail buyers delivered 76.55% of the United States automotive dealership market in 2025, but are slowing as urban consumers gravitate toward subscription models offering lower commitment and bundled insurance. OEM-backed subscriptions sold through dealers, such as Ford Pro, are scaling rapidly, with 400,000 accounts generating SaaS-like recurring revenue streams.

Fleet and corporate volumes are expanding 6.32% annually, bolstered by federal commercial EV tax incentives that cut the total cost of ownership. Dealers offering volume-purchase rebates, consolidated billing, and depot-charging consulting lock in multi-year service revenue. Consequently, the United States automotive dealership market share attributed to fleets is projected to rise by 2031, creating a more balanced customer mix that stabilizes cyclical retail swings.

Geography Analysis

The South contributed 36.55% of 2024 turnover and is projected to advance at a 5.85% CAGR through 2030, buoyed by robust in-migration, comparatively lenient franchise regulations, and a vehicle mix tilted 68% toward light trucks that command higher front-end grosses. States such as Texas and Georgia continue to green-light direct E-signature closings, accelerating omnichannel penetration and lifting per-rooftop volumes as labor markets remain tight in the Sun Belt.

The Northeast is shaped by dense metros where showrooms occupy high-cost real estate, and stringent emission rules accelerate EV adoption. New York’s target for 35% zero-emission sales penetration by 2026 is forcing dealers to retrofit legacy rooftops with DC fast chargers, often supported by utility rebates covering up to 80% of make-ready costs. While passenger-car share is higher here than in other regions, rising insurance premiums nudge buyers toward compact crossovers that balance space with cost.

Midwestern dealers benefit from deep supplier ecosystems and a customer base loyal to domestic brands, sustaining steady replacement demand for pickups used in agriculture and construction. Infrastructure bill spending on highways and bridges is stimulating heavy-duty truck sales, opening service-contract volume that offsets slower retail sedan turnover. Meanwhile, the West’s early-adopter population and state EV rebates of USD 2,000-USD 4,500 have propelled battery-electric registrations to 18% of new-vehicle sales in 2024, stimulating dealership investment in venture-shared charging plazas.

Competitive Landscape

Market consolidation continues as large publicly traded groups deploy cash flows from record 2021-2023 profits to acquire smaller rooftops. Lithia Motors eclipsed AutoNation in 2024 unit sales after a string of Midwest and Southeast acquisitions, pushing the top-10 groups’ combined share to a significant share of the United States automotive dealership market. Despite this upswing, the field remains moderately concentrated, leaving room for regional champions to defend territory through community engagement and bespoke service offerings.

Strategic themes include luxury-brand clustering, omnichannel technology rollout, and EV-infrastructure scaling. Group 1 Automotive’s USD 210 million-revenue Mercedes-Benz of Buckhead buyout secured premium mix growth and consolidated parts distribution efficiencies[3]“Investor Presentation May 2025,” Group 1 Automotive, Inc., group1auto.com. Reynolds and Reynolds’ partnership with UVeye is delivering AI-driven underbody inspection lanes, enhancing upsell rates for tires and safety repairs. Meanwhile, retailers in low-EV-adoption states are deferring charger spend, potentially losing allocation priority once federal tax credits tighten post-2026.

Competitive threats from nontraditional players are crystallizing. Amazon Autos launched national used-vehicle listings in August 2025, leveraging Prime-scale logistics while keeping dealer compliance intact by routing final paperwork through licensed retailers. Direct-to-consumer startups eyeing agency models must still navigate franchise statutes, but their marketing spend is compressing search-engine ad rates for traditional dealers. Consequently, success hinges on balanced capital allocation: investing enough in digital and EV capabilities to remain relevant, yet safeguarding liquidity for cyclical downturn resilience.

United States Automotive Dealership Industry Leaders

Auto Nation Inc.

Lithia Motors Inc.

Group 1 Automotive Inc.

Penske Automotive Group

Sonic Automotive Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Amazon broadened Amazon Autos to list used and certified pre-owned vehicles nationwide, debuting in Los Angeles and partnering with local franchised dealers.

- May 2025: Group 1 Automotive acquired three luxury dealerships in Florida and Texas (Lexus, Acura, Mercedes-Benz), adding USD 330 million in annual sales.

- March 2025: Carvana purchased its first franchised dealership in Arizona to expand into new-car sales via a hybrid retail model.

- February 2025: Asbury Automotive Group agreed to buy The Herb Chambers Companies, encompassing 33 dealerships and 52 franchises, with closing expected in Q2 2025.

United States Automotive Dealership Market Report Scope

A car dealership, or car dealer, is a business that sells new or used cars, at the retail level, based on a dealership contract with an automaker or its sales subsidiary. It can also carry a variety of certified pre-owned vehicles. Car dealerships employ automobile salespeople to sell their automotive vehicles, provide maintenance services for cars, and employ automotive technicians to stock and sell spare automobile parts. They also process warranty claims. The US automotive dealership market has been segmented by type (new vehicle dealership, used vehicle dealership, parts and services, and finance and insurance), retailer (franchised retailer and non-franchised retailer), and vehicle type (passenger cars and commercial vehicles). The market size and forecast for each segment have been calculated based on value (USD billion).

| New-Vehicle Sales |

| Used-Vehicle Sales |

| Franchised Dealers |

| Independent Dealers |

| Direct-to-Consumer Digital Retailers |

| Passenger Cars |

| Light Trucks and SUVs |

| Medium and Heavy Commercial Vehicles |

| Brick and Mortar |

| Online / Omnichannel |

| Individual Consumers |

| Fleet and Corporate |

| Northeast |

| Midwest |

| South |

| West |

| By Type | New-Vehicle Sales |

| Used-Vehicle Sales | |

| By Retailer | Franchised Dealers |

| Independent Dealers | |

| Direct-to-Consumer Digital Retailers | |

| By Vehicle Type | Passenger Cars |

| Light Trucks and SUVs | |

| Medium and Heavy Commercial Vehicles | |

| By Sales Channel | Brick and Mortar |

| Online / Omnichannel | |

| By Customer Segment | Individual Consumers |

| Fleet and Corporate | |

| By Region (United States) | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How large is the United States automotive dealership market in 2026?

The United States automotive dealership market size is USD 3.08 trillion in 2026, with a forecast value of USD 3.83 trillion by 2031.

Which segment is growing fastest within dealership sales?

Medium and heavy commercial vehicles are projected to expand at a 4.97% CAGR as fleet electrification gains momentum.

How are online channels affecting dealership profitability?

Omnichannel sales are growing 6.01% annually, forcing dealers to invest in digital tools that maintain gross margins while improving customer convenience.

Which region leads U.S. dealership revenues?

The South holds the largest share at 36.20% and is forecast to grow fastest at 5.78% CAGR through 2031.

Page last updated on: