Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.02 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Automobile Market Analysis by Mordor Intelligence

The Ghana automotive market size is expected to grow from USD 2.02 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 3.41 billion by 2031 at 9.1% CAGR over 2026-2031. Demand rises due to tax holidays for assemblers, customs concessions for electric two and three-wheelers, and expanding ride-hailing fleets that refresh vehicles more frequently. Currency stabilization in 2025 trimmed import costs and encouraged dealers to replenish inventories, while ongoing corridor road upgrades lowered transport overheads for distributors. At the same time, local content rules are steering component makers to set up in industrial parks near Accra and Kumasi, anchoring a nascent supply chain that can feed both domestic buyers and AfCFTA customers. Moderate lending rates remain a hurdle, yet pilot leasing schemes from commercial banks are widening access to new-car financing in urban centers.

Key Report Takeaways

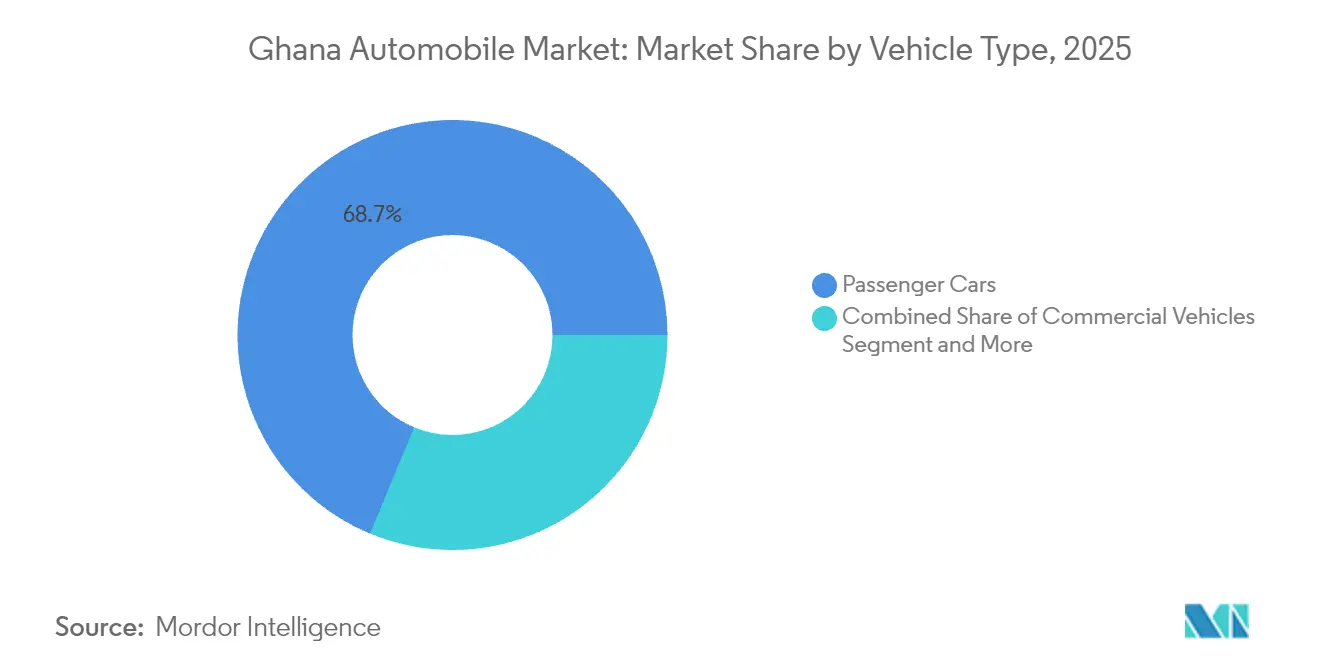

- By vehicle type, passenger cars led with 68.74% of the Ghana automotive market share in 2025, while three-wheelers posted the quickest expansion at a 9.39% CAGR through 2031.

- By propulsion type, internal combustion engines held 88.85% of the Ghana automotive market share in 2025, and battery electric vehicles are set to grow at a 28.90% CAGR to 2031.

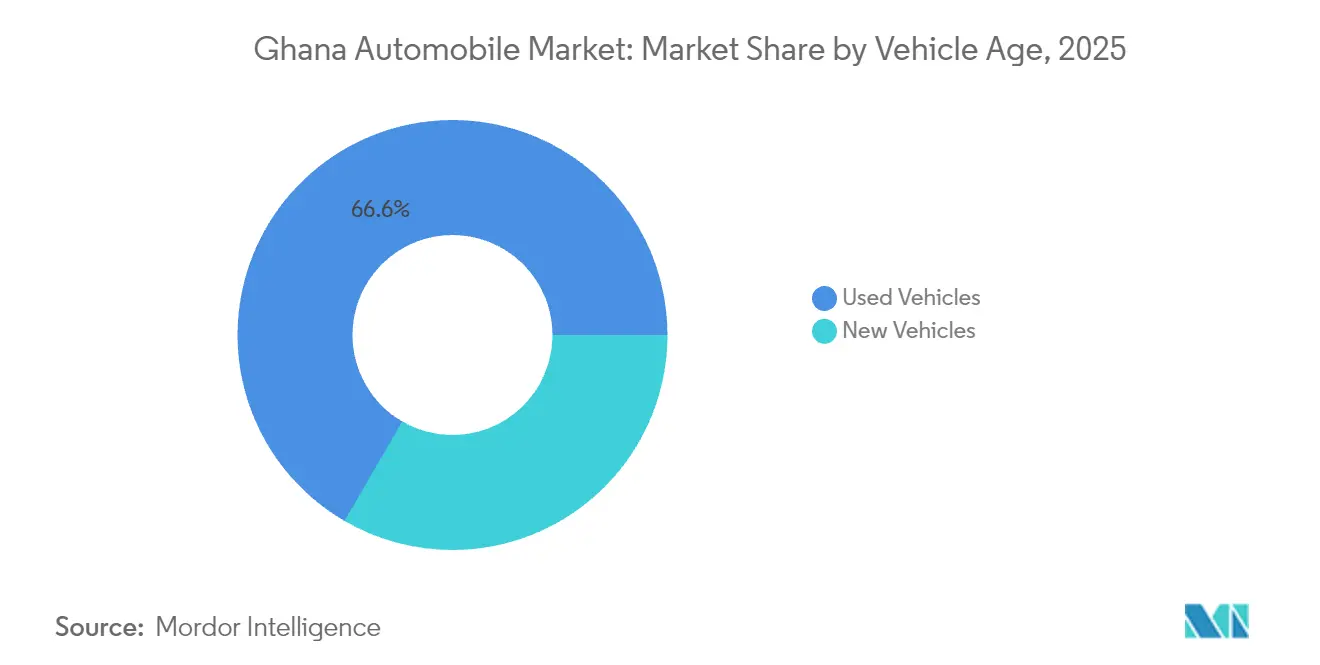

- By vehicle age, used imports accounted for 66.62% of the Ghana automotive market size in 2025 and remain the fastest-growing category at 9.18% CAGR.

- By end-use application, personal mobility dominated with a 69.05% of the Ghana automotive market share in 2025, whereas commercial and fleet demand is projected to climb at an 11.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ghana Automobile Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Local Assembly Expansion and 10-Year Tax Holidays | +2.1% | Greater Accra and Ashanti | Medium term (2-4 years) |

| Rising Household Incomes and Motorization | +1.8% | Urban regions nationwide | Long term (≥ 4 years) |

| Eight-Year EV Duty Waiver and Production Incentives | +1.4% | Accra, Kumasi, Takoradi | Short term (≤ 2 years) |

| Eastern and Coastal Corridor Road Upgrades | +1.2% | Eastern and Western | Medium term (2-4 years) |

| Ride-Hailing Platform Growth | +0.9% | Greater Accra and Kumasi | Short term (≤ 2 years) |

| Surplus Electricity for Low-Cost EV Charging | +0.7% | National grid zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Local Assembly Expansion & Automotive Development Policy

Government tax holidays introduced in 2019 triggered assembly investments from Toyota, Volkswagen, and Nissan, each targeting AfCFTA export opportunities from Ghana’s centrally located plants[1]“Automotive Development Policy 2019,”, Ministry of Trade & Industry, moti.gov.gh. Ghana's automotive assembly sector is on the rise. Local sourcing of stampings and harnesses is boosting industrial employment and facilitating the transfer of technical skills. Duty drawbacks on components enhance cash flow, allowing for a scale-up in production. Thanks to the AfCFTA, Ghana successfully ships regional kits to Côte d'Ivoire and Nigeria. However, there's a pressing need to upgrade engine machining capabilities for sustained growth, which is currently dependent on foreign tooling. This underscores a crucial area for both investment and localization.

Eight-Year EV Duty Waiver and Tax Incentives

The 2025 Budget removed import duties on electric vehicles for eight years, matching customs rebates for locally assembled two- and three-wheeled models [2]“Customs Amendment Act 2025,”, Parliament of Ghana, parliament.gh. A recent policy initiative significantly reduced the cost of imported compact vehicles, making them more accessible to consumers. It also encouraged investment in battery production, with support from Ghana’s sovereign wealth fund. In Accra, fleet operators began using affordable electric hatchbacks for ride-hailing services, finding them more energy-efficient than traditional gasoline cars. The private sector responded actively, with a notable partnership between Jospong Group and VinFast aiming to expand the country’s charging infrastructure. While early adoption is concentrated in Greater Accra, broader expansion will hinge on improvements in the power grid and the availability of skilled technicians.

Road-Infrastructure Upgrades (Eastern and Coastal Corridors)

Completing 120 km of dual-carriage on the Eastern Corridor reduced haulage time between Tema Port and Tamale by 25% and spurred purchases of 3-ton trucks by produce traders[3]“Eastern Corridor Progress Update 2025,”, Ministry of Works & Housing, mwh.gov.gh. Asphalt resurfacing on the Coastal Highway facilitated tourism traffic to Cape Coast, translating into minibus and SUV demand for hospitality operators. Lower suspension damage claims reduced the total cost of ownership, persuading banks to extend five-year terms on commercial-vehicle loans. Dealers responded by opening satellite service centers in Ho and Keta, expanding geographic coverage. Continued road works are expected to add 1.2% to the market’s CAGR over the medium term.

Ride-Hailing Platform Expansion Boosting Fleet Turnover

Daily ride requests on leading platforms rose 18% year-on-year in H1 2025, prompting drivers to replace older sedans with newer models to comply with platform age caps [4]“Ride Data Dashboard 2025,”, Uber Ghana, uber.com. Operators favor fuel-efficient 1.3-liter compacts backed by three-year warranties, while corporate fleets switch to low-maintenance hybrids for airport transfers. Digital payment penetration through mobile money eased fare settlement, improving driver cash flow and supporting loan repayments. Fleet owners report average replacement cycles shortening to three years, almost half the national average for personal vehicles. Platform entry into Sunyani and Bolgatanga is widening regional vehicle demand beyond traditional hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Tariffs and Para-Tariffs | -1.9% | Nationwide | Short term (≤ 2 years) |

| Limited Auto-Credit Penetration | -1.6% | Nationwide, rural focus | Medium term (2-4 years) |

| Cedi Volatility | -1.3% | Import-heavy markets | Short term (≤ 2 years) |

| Skills and Parts Gap For EV/Hybrid Service | -0.8% | National training hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Auto-Credit Penetration and >25% Lending Rates

Average commercial-bank lending rates touched 26.4% in April 2025 despite gradual policy easing [5]“Credit Conditions Survey Q1 2025,”, Bank of Ghana, bog.gov.gh. High risk premiums reflect persisting non-performing loans, discouraging banks from long-term vehicle financing. Informal lenders fill part of the gap but charge equivalent annual rates, restraining volume growth. Mobile-money-based micro-lease pilots show promise, yet scale-up requires credit-bureau data integration and collateral registry reforms.

Skills and Parts Gap for Advanced Powertrains

Only a handful of vocational colleges currently offer specialized electric vehicle (EV) maintenance modules, highlighting a significant gap in technical training. This scarcity of certified technicians compromises service quality, particularly in regions like Takoradi and Tamale. Here, workshops depend on imported diagnostic tools, resulting in prolonged repair times. Additionally, sourcing essential EV components from Europe inflates costs and extends delays. To counteract buyer apprehensions, automakers have begun providing extended service packages. Yet, worries about after-sales support persist, hindering adoption in rural locales. While the government and industry collaborate to refresh training curricula, achieving comprehensive nationwide coverage remains challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type – Three-Wheelers Drive Commercial Innovation

Passenger cars accounted for 68.74% of the Ghana automotive market size in 2025 as urban households prioritized flexible mobility over public transport. Three-wheelers, however, recorded a 9.39% CAGR to 2031, reflecting demand for cost-effective last-mile delivery and micro-transit services.

Rising e-commerce orders in Accra bolster three-wheeler purchases by courier firms, and low fuel consumption appeals to self-employed drivers. Passenger cars continue to benefit from ride-hailing apps that impose age caps, ensuring regular fleet renewal. Commercial trucks enjoy steady uptake from construction projects financed under One District One Factory, while motorcycle penetration plateaus due to safety concerns and limited credit access.

By Propulsion Type – Electric Transition Accelerates Despite ICE Dominance

Internal combustion engines retained 88.85% of the Ghana automotive market share in 2025, but electric vehicles are projected to post a 28.90% CAGR through 2031. Hybrids, though small today, appeal to taxi operators seeking fuel savings without range anxiety.

EV growth is catalyzed by zero-duty imports and the sovereign fund’s battery investment that trims local pack costs. ICE sales still dominate rural areas where fuel stations outnumber chargers by twenty to one. Grid upgrades and technician training will dictate how soon EV adoption spreads beyond Accra and Kumasi.

By Vehicle Age – Used Vehicle Dominance Reflects Economic Realities

Used imports comprised 66.62% of the Ghana automotive market in 2025, expanding at a 9.18% CAGR as consumers balanced price and reliability. Models aged three to seven years offer modern safety features without the steep depreciation of new cars.

Currency swings and high duties reinforce the appeal of used cars, and informal credit lines from dealers smooth purchase hurdles. Government targets for local assembly may eventually chip away at this segment once price parity improves and warranty coverage gains trust.

By End-Use Application – Commercial Fleet Expansion Outpaces Personal Mobility

Personal use held a 69.05% share in 2025, but commercial and fleet demand is forecast to grow 11.33% annually due to ride-hailing, parcel delivery, and corporate leasing. Enterprises favor vehicles with telematics for route optimization and preventative maintenance.

Taxi cooperatives in Kumasi are trialing EV sedans under subsidized charging tariffs, while e-commerce players lease three-wheelers for inner-city drops. Government fleet renewal under the Public Transport Support Program injects periodic bulk orders that stabilize factory utilization rates at local assembly plants.

Geography Analysis

Greater Accra and Ashanti regions account for more vehicle registrations due to higher incomes, denser road networks, and concentrated dealer outlets. The Ghana automotive market benefits from Accra’s role as AfCFTA headquarters, giving assemblers streamlined export documentation for shipments to Côte d’Ivoire and Togo.

Eastern and Coastal corridor upgrades are unlocking demand in Volta and Western regions, where improved roads cut travel time and encourage intercity commuting. Dealers have opened satellite showrooms in Koforidua and Takoradi to capture first-time buyers, offering warranties tied to mobile service vans.

Northern regions still trail in penetration due to lower income levels and sparse service infrastructure, yet agricultural mechanization and mining exploration are generating interest in pickups and light trucks. Expansion of ride-hailing into Tamale hints at rising urban mobility needs that could narrow the geographic gap over the forecast horizon

Regulatory Landscape

Ghana's automobile sector operates under the Ghana Automotive Development Policy (GADP), administered by the Ministry of Trade, Agribusiness and Industry (MOTAI) through a two-tier registration framework for assemblers. Incentive access is linked to compliance requirements and a stated pathway toward higher local value addition. The Customs (Amendment) Act provides the legislative basis for duty and tax incentives for registered manufacturers and also anchors import compliance, including requirements for homologation documentation or a certificate of conformance for imported motor vehicles.

Product and import compliance is reinforced via the Ghana Standards Authority (GSA), which issues safety and inspection standards for both new and used vehicles (including the standards referenced in the market such as braking and used-vehicle requirements). In January 2026, MOTAI held a stakeholder engagement to review a draft GADP Phase Two, with focus on bringing electric vehicles and two- and three-wheelers more explicitly into the assembly program and aligning related charging infrastructure standards. This signaled a tightening of the policy-to-implementation link for e-mobility and light-mobility segments.

Value Chain Analysis

Ghana's vehicle supply chain is import-led upstream, with OEMs and local assemblers relying predominantly on SKD/CKD kits and imported components. After that, they handle assembly, quality checks, and limited localization (such as selected stampings and harnesses) around industrial nodes near Accra and Kumasi. Under the GADP framework, assemblers register with MOTAI and structure operations around duty concessions on components. Inbound logistics flows through key ports, notably Tema, into assembly sites and distributor compounds that supply dealer networks across Greater Accra, Ashanti, and secondary corridors.

Midstream and downstream activities include nationwide sales, parts warehousing, and after-sales service, where warranty terms, parts availability, and workshop capability increasingly influence brand choice, especially for ride-hailing and fleet buyers that refresh vehicles more frequently. A notable integration step occurred in February 2026, when CFAO Mobility consolidated Toyota and Hino assembly, sales, and after-sales into Toyota Tsusho Manufacturing Ghana (TTMG), tightening coordination between production planning, inventory, and service support. Bottlenecks persist around limited domestic component manufacturing, affordability constraints for new locally assembled vehicles versus used imports, and skills and tool gaps for EV and hybrid service, which keeps reliance on imported diagnostics and spares elevated.

Competitive Landscape

Ghana’s assembler roster is headed by Toyota, Volkswagen, and Nissan, each operating CKD lines that qualify for 10-year corporate tax relief. These firms collectively cover a significant output, leveraging nationwide parts depots and dense dealer networks.

EV entrants such as VinFast have teamed with Jospong Group to erect a 5,000-unit-per-year plant and 3,000-point charging grid, aiming at fleet customers in ride-hailing and logistics. Chinese brands explore SKD pathways focusing on pickups and budget sedans, using flexible tariffs for partially assembled kits.

Independent service chains are expanding outside Accra, offering multi-brand maintenance packages that erode OEM after-sales advantages. Competition now pivots on warranty length, financing tie-ins, and data-driven fleet management rather than sticker prices alone.

Ghana Automobile Industry Leaders

Toyota Motor Corporation

Volkswagen AG

Nissan Motor Co. Ltd

Hyundai Motor Company

Kantanka Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-driven localization creates gaps in components and supplier services as Ghana moves from SKD-heavy assembly toward deeper local value addition under the GADP pathway. Government workstreams referenced in 2026 around an automotive component manufacturing policy, alongside industrial plans such as local production of industrial fasteners (bolts, nuts, springs) targeted for Q3 2026, open entry points for SMEs in metal fabrication, plastics, wiring, and consumables. The same direction also creates space for testing, certification, and logistics providers that support assemblers clustered near Accra and Kumasi.

Electric mobility is shifting the focus from incentives toward enforceable infrastructure governance, which opens opportunities across charging deployment, operations, and compliant installation services. The Energy Commission advanced draft EV charging infrastructure and battery swap regulations through a February 2026 workshop to license and regulate the EV infrastructure value chain, while the National Electric Vehicle Policy frames 2024-2026 as a preparation phase for take-off. On the demand side, fleet turnover and after-sales coverage remain practical levers, including the integration step by Toyota Tsusho Manufacturing Ghana that combined assembly with distribution and service. Industry engagement with government on the competitiveness of locally assembled vehicles, including VAT exemption discussions in June 2026, also affects OEM pricing structures and financing partnerships for fleets and retail buyers.

Recent Industry Developments

- June 2026: Ghana's Ministry of Trade, Agribusiness and Industry indicated it was considering restoration of the 20% VAT exemption on locally assembled vehicles after assemblers raised concerns about production slowdowns. The update points to how fiscal incentives influence the price gap versus used imports and the utilization rates of local assembly lines.

- February 2026: Toyota Tsusho Manufacturing Ghana (TTMG) launched a consolidated operating model in Ghana, integrating assembly with nationwide distribution for Toyota and Hino. The structure strengthens end-to-end control of inventory, parts availability, and after-sales coverage, which is central to fleet buyers and ride-hailing operators that depend on uptime.

- October 2025: Volkswagen Ghana marked five years in the market and launched the T-Cross compact SUV, adding to its local assembly lineup. The expanded model mix supports broader price-point coverage and adds more locally assembled options for personal mobility and fleet procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value generated in Ghana from motor vehicles across the core industry chain, including vehicle production or assembly, wholesale and retail sales, and related maintenance activity tied to vehicles in use.

Scope exclusions: It does not count upstream raw materials and generic workshop tools that are not primarily purchased for vehicle-specific service work.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- Three-Wheelers

- By Propulsion Type

- Internal-Combustion Engines

- Electric Vehicles

- By Vehicle Age

- New Vehicles

- Used Vehicles

- By End-Use Application

- Personal Mobility

- Commercial & Fleet (ride-hailing, logistics, public transport)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping what moves the Ghana vehicle market in practical terms, which is the flow of imported vehicles, local assembly progress, and how fast the active vehicle fleet changes. We used public sources such as customs and trade releases from Ghana Revenue Authority and UN Comtrade, macro indicators from the World Bank and IMF, and transport and road-safety statistics from relevant national authorities.

To ground the model assumptions, we also reviewed company disclosures like annual reports and investor presentations, association updates, and reputable local and international press that tracks pricing and policy changes. When needed, we supplemented gaps using paid subscriptions focused on company financials and intelligence, patent and technology tracking, and shipment-level trade data to sense-check volumes and price bands. These sources are illustrative only, and other public and paid references were also used during data collection and cross-checking.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around the split between new and used vehicles, typical price realization, and how policies and financing are affecting purchase behavior. We spoke with a mix of vehicle import and distribution participants, local assembly or aftersales stakeholders, and fleet-oriented buyers so the final sizing reflects demand signals from personal mobility as well as commercial use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 22% | APAC: 52% |

| Mid tier: 42% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 22% | Managers: 41% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where Ghana demand is reconstructed from vehicle inflow and parc signals, and then translated into value using realistic price ranges by vehicle type and age. After that, we used selective bottom-up approximations, such as rolling up a sample of distributor and importer revenue patterns and checking implied unit volumes against trade and registration signals, which helped adjust totals when the first pass looked too high or too low.

Key inputs used in the model include imported vehicle volumes, the new versus used mix, typical CIF and retail price bands, FX movement and pass-through timing, and policy shifts affecting duties or incentives. We also treated fleet demand as its own check by looking at procurement cycles and replacement behavior, because it can move differently than retail demand. For forecasting, scenario analysis was used around FX and policy paths, and then smoothed using trend-based techniques so the year-to-year curve stays realistic. Where bottom-up detail was missing for smaller channels, the gap was handled using penetration assumptions anchored to trade volumes and validated in calls.

Data Validation & Update Cycle

Outputs were checked against independent signals such as import value trends, vehicle parc direction, and observed retail pricing changes, and then any large variance was investigated before finalizing. If an assumption shifted the market sharply, it was re-checked through follow-up outreach and a second analyst review so that arithmetic issues and definition drift are caught early.

The report is refreshed annually, and interim updates are triggered when material events occur, such as a significant duty change or a major FX shock. Before delivery, we run a final pass to confirm the latest macro and trade indicators are reflected, and then the model is rebalanced where needed.

Mordor Intelligence's Ghana Analysis of Automobile Market Sizing Compared With Other Published Estimates

It is normal to see different published market sizes for Ghana automobiles, even when the titles look similar. The gaps usually come from what is counted in the market, which year is treated as the base, and how prices are converted into USD when exchange rates are moving.

Some estimates also lean more on a single demand proxy like new-car sales, while others blend used imports, local assembly, and aftersales value into one number. Forecast styles differ too, since one publisher may assume stable duties and smoother FX, while another builds in conservative affordability and financing constraints.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.02 B (2025) | |

| Academic-Industry Report A | USD 1.96 B (2025) | Uses a narrower value build that leans on aggregated sector estimates and can undercount aftermarket and service value that follows vehicles already in the parc. |

| Auto Media Outlet B | USD 1.93 B (2024) | Reports an earlier-year snapshot and provides limited clarity on whether the value includes only vehicle sales or also distribution and maintenance activity, which shifts the total. |

The table shows a spread that is mainly explained by year selection and what parts of the industry chain are counted. In the Mordor Intelligence model, the value is built to include wholesaling, retailing, and vehicle-linked maintenance activity rather than only counting vehicle sales. When the scope and USD conversion timing are aligned, the gap typically narrows, and the remaining difference comes from how used-import pricing and mix are treated.

Key Questions Answered in the Report

How big is the Ghana automotive market in 2026?

It reached USD 2.21 billion in 2026 and is projected to climb to USD 3.41 billion by 2031.

What is driving electric vehicle uptake in Ghana?

An eight-year import duty waiver, sovereign fund backing for batteries, and expanding charging infrastructure underpin a projected 28.90% CAGR for EVs.

Which vehicle segment is growing fastest?

Three-wheelers are expanding at 9.39% annually due to last-mile delivery and urban micro-transit demand.

How does currency volatility affect car prices?

Fluctuations in the cedi cause importers to widen price margins, leaving retail prices elevated even after temporary appreciation.

What regions show the most potential beyond Accra?

Road upgrades are spurring demand in Eastern and Western regions, with dealers opening branches in Koforidua and Takoradi.

Page last updated on: