IoT Middleware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

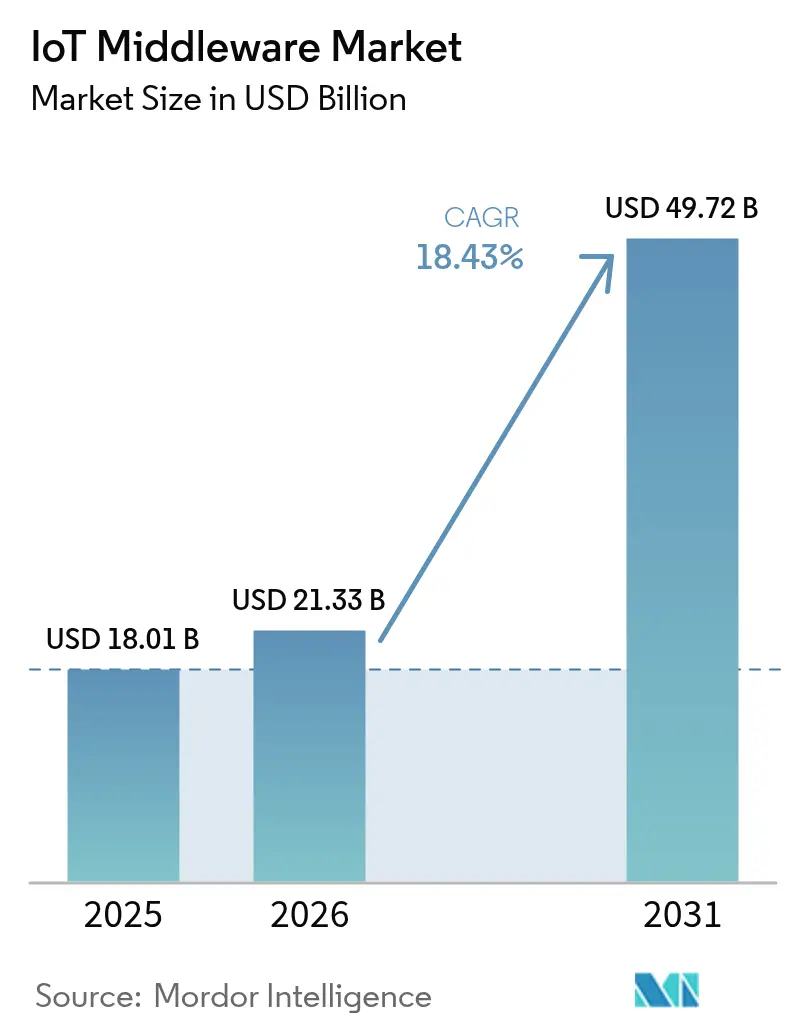

| Market Size (2026) | USD 21.33 Billion |

| Market Size (2031) | USD 49.72 Billion |

| Growth Rate (2026 - 2031) | 18.43% CAGR |

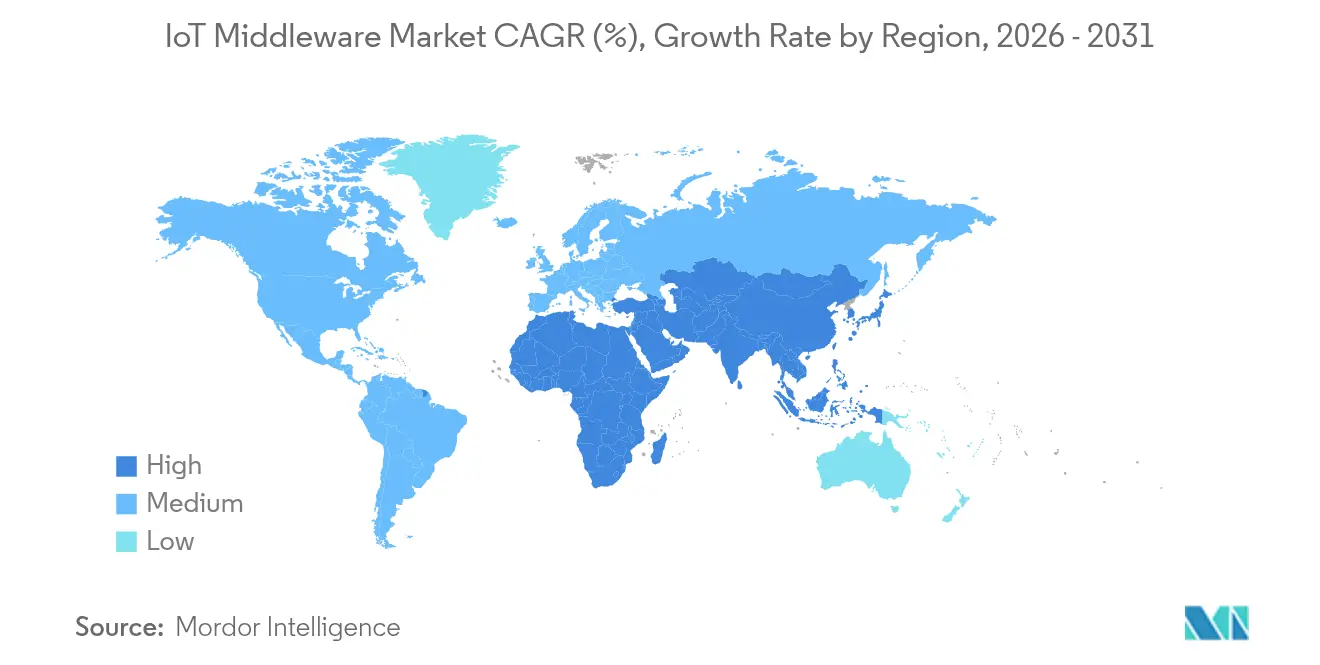

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Middleware Market Analysis by Mordor Intelligence

IoT Middleware Market size in 2026 is estimated at USD 21.33 billion, growing from 2025 value of USD 18.01 billion with 2031 projections showing USD 49.72 billion, growing at 18.43% CAGR over 2026-2031. Rapid 5G RedCap rollouts, LPWAN densification, and cloud-native development methods combine to lift demand for multi-protocol device orchestration that can scale from thousands to millions of endpoints.[1]“The Mobile Economy Asia Pacific 2024,” GSMA, gsma.com Application-enablement suites lead with 48% of 2024 revenue as enterprises prioritize low-code, full-stack environments, while connectivity-management platforms post a 19.67% CAGR on the back of global SIM provisioning and eUICC adoption. Manufacturing claims 29.3% of 2024 spending, yet healthcare’s 20.17% CAGR signals a pivot toward smart-hospital telemetry built on emerging 6G concepts. Cloud deployments still deliver 71% of projects, though edge and fog architectures accelerate at 21.87% as factories pursue sub-millisecond control loops and enterprises respond to data-sovereignty mandates. North America tops the revenue table with 37.5% share on strong enterprise IT budgets, but Asia Pacific’s 21.55% CAGR underscores the momentum created by pervasive 5G coverage and supportive public policy.

Key Report Takeaways

- By platform, application enablement controlled 47.35% of the IoT middleware market share in 2025, while connectivity management is tracking a 19.20% CAGR through 2031.

- By deployment model, cloud captured 70.40% revenue in 2025; edge and fog computing are forecast to climb at a 21.05% CAGR to 2031.

- By end-user, manufacturing led with 28.85% revenue in 2025, whereas healthcare is projected to grow at a 19.65% CAGR to 2031.

- By organization size, large enterprises accounted for 65.35% revenue in 2025, and SMEs are expanding at an 18.40% CAGR through 2031.

- By geography, North America produced 36.90% of 2025 revenue, yet Asia Pacific is on course for a 20.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT Middleware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected-device proliferation raises demand for scalable application platforms | +3.2% | Global, led by Asia Pacific | Medium term (2-4 years) |

| Industry 4.0 and IIoT adoption in manufacturing lines | +2.8% | North America & Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Evolution of 5G and LPWAN enabling massive IoT connectivity | +2.5% | Global, first in developed markets | Short term (≤ 2 years) |

| Cloud-native subscription models lowering capital spending | +2.1% | Global, benefiting SMEs | Medium term (2-4 years) |

| Convergence of AIoT calling for real-time edge-AI middleware | +1.9% | North America & Europe, with Asia Pacific following | Long term (≥ 4 years) |

| Government support for open-source sovereign IoT stacks | +1.4% | Europe & Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Connected Devices Demanding Scalable Application-Enablement Platforms

Cellular IoT links are expected to reach 7.5 billion by 2033, with NB-IoT and LoRaWAN representing 86% of LPWAN connections, creating unprecedented scale requirements for middleware. Platforms must handle 5G RedCap for high-throughput data as well as energy-harvesting ambient IoT tags predicted to surface with 5G-Advanced around 2027. Eaton improved equipment effectiveness by up to 15% after rolling out PTC’s ThingWorx suite across 200 factories, illustrating the ROI of high-capacity application environments.

Rapid Adoption of Industry 4.0 and IIoT in Manufacturing Lines

Although 95% of manufacturers assess smart-factory tools, only 5% run enterprise-wide programs, leaving space for middleware that unites siloed pilots. Industrial IoT can trim cost of goods sold by one-quarter when data flows freely between OT and IT domains. Woodward’s adoption of ThingWorx linked product-lifecycle and execution systems to deliver real-time insights across plants, proving middleware’s bridging value.

Evolution of 5G & LPWAN Enhancing Massive IoT Connectivity

The GSMA forecasts 480 million 5G IoT connections by 2030, and Sateliot’s 5G NB-IoT satellite tests extend coverage beyond terrestrial footprints, forcing middleware to manage hybrid network maps. LoRaWAN’s integration into 5G core, plus enhanced security features, adds complexity that only multi-protocol orchestration layers can mask.

Cloud-Native Middleware Subscription Models Lowering Upfront CAPEX

Processing 300 sensor requests per second now costs roughly USD 57 per month on managed serverless stacks, showing the economics of pay-as-you-go middleware. Microsoft’s cloud unit alone surpassed USD 40 billion annual revenue, proving wide enterprise acceptance of subscription economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex integration of heterogeneous legacy OT systems | -2.3% | Global, heavy in mature manufacturing bases | Long term (≥ 4 years) |

| Escalating data-sovereignty and privacy compliance costs | -1.8% | Europe & North America | Medium term (2-4 years) |

| Lack of unified cross-domain semantic data models | -1.5% | Global | Long term (≥ 4 years) |

| Rising cloud-egress fees squeezing returns | -1.2% | Global, felt in multi-cloud deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Integration of Heterogeneous Legacy OT Systems

Plants worldwide still depend on machinery worth USD 6.8 trillion that was never designed for IP networking, demanding costly adapters and specialized skills for middleware onboarding. Although low-cost boards have proven integration feasibility on select lines, full rollouts multiply testing and cybersecurity overhead.

Escalating Data-Sovereignty and Privacy Compliance Costs

The EU-backed Gaia-X program mandates local data processing and clear audit paths, requiring middleware to embed localization and encryption toggles. India now operates regulatory sandboxes on IoT security, underscoring the global march toward sovereign stacks and inflating compliance budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Application Enablement Remains in Front

Application-enablement suites generated 47.35% of 2025 revenue as organizations favored end-to-end environments that speed prototype-to-production cycles. The IoT middleware market size for these suites is positioned to cross USD 19.14 billion by 2031 at an 10.6% CAGR. Connectivity-management solutions, the fastest sub-segment, benefit from remote SIM provisioning and eUICC mandates, delivering a 19.20% CAGR that lifts their value to USD 10.02 billion by 2031. Vendors now embed AI-driven anomaly detection and over-the-air firmware orchestration, blurring the line between application enablement and device management.

Enterprises migrating from proofs of concept to fleet-wide deployments need single control planes that tackle device onboarding, protocol translation, and data normalization. Low-code interfaces extend development to operational staff, while integrated edge runtimes cut latency for motion-control or AGV scenarios. These enhancements show how the IoT middleware market pushes toward unified, AI-ready environments that condense integration efforts.

By Deployment Model: Cloud Strength Meets Edge Ascendancy

Cloud architectures captured 70.40% of shipments in 2025 thanks to global availability and mature DevOps ecosystems. Yet edge and fog nodes are projected to post a 21.05% CAGR, lifting their IoT middleware market size above USD 15.05 billion by 2031 as factories and hospitals require local inference. Fog nodes deliver deterministic response for machine vision, and micro data centers respect regional data-protection rules.

A hybrid topology now dominates design blueprints. Central clouds provide noncritical analytics, while on-premise gateways process time-sensitive telemetry. Products such as SECO’s CLEA suite combine Yocto-based firmware with Kubernetes-native orchestration to simplify end-to-end observability. Hyperscalers complement this direction with managed edge containers, ensuring that the IoT middleware market meets both latency and compliance imperatives.

By End-User Industry: Manufacturing Holds Lead, Healthcare Accelerates

Manufacturing contributed 28.85% of 2025 spending, leveraging middleware for OEE optimization, predictive maintenance, and real-time SPC dashboards. Healthcare, advancing at a 19.65% CAGR, draws on 6G-enabled telemetry, digital twins, and asset tracking to improve clinical outcomes. Energy, logistics, and agriculture collectively represent a rising share as ESG reporting and supply-chain visibility gain prominence.

Hospitals like Kantonsspital Baden feature 7,000 IoT sensors linked by Siemens Xcelerator, cutting asset search times by 65% and improving patient throughput. On the factory floor, Habermaass adopted a custom MES that funnels OT data into middleware, giving operators real-time instructions and reducing micro-stoppages. Such case studies underline the diverse opportunities the IoT middleware market unlocks across verticals.

By Organization Size: Enterprise Dominance Tempered by SME Momentum

Large enterprises own 65.35% of 2025 invoicing, yet SMEs will add the most net new deployments at an 18.40% CAGR as subscription pricing narrows the capability gap. Cloud-native stacks allow startups to ingest telemetry, apply ML models, and expose dashboards in weeks, proving that company size no longer dictates digital ambition.

Managed services shift operational responsibility to specialists, freeing internal teams and minimizing up-front CAPEX. For example, a mid-size manufacturer now processes 50 million monthly events on a serverless bus for under USD 60, illustrating affordability. This inclusive growth guarantees a broadening user base, reinforcing the relevance of the IoT middleware market across firm sizes.

Geography Analysis

North America generated 36.90% of 2025 revenue through deep IT penetration and extensive venture funding for sensor-driven startups. United States cloud providers invested more than USD 80 billion in AI-ready data centers, feeding middleware innovation at scale. Canada’s Terrestar–Monogoto alliance merges cellular and satellite to cover remote assets, a model likely to spread across energy and transportation corridors. Mexico’s automotive clusters leverage middleware for traceability and downtime avoidance, bridging supply-chain gaps with near-real-time dashboards.

Asia Pacific is set to record a 20.95% CAGR up to 2031, driven by 1.8 billion mobile subscribers and public-sector pushes toward smart manufacturing. China leads NB-IoT roll-outs under state-backed budget subsidies, while India pilots regulatory sandboxes focused on indigenous encryption to secure local patient data. Japan and South Korea dominate 5G SA coverage, delivering fertile ground for edge-AI middleware in automotive plants and micro-factories.

Europe enjoys steady, compliance-driven adoption. The Gaia-X blueprint obliges providers to enable federated identity and lineage tracking, influencing architecture choices across Germany’s automotive suppliers and France’s energy utilities. The United Kingdom channels funds into smart-city pilots that rely on multi-service middleware for congestion analytics and emissions monitoring. Eastern Europe upgrades brownfield factories with LoRaWAN telemetry, using low-cost open-source stacks to bypass capital constraints, reinforcing the breadth of the IoT middleware market.

Regulatory Landscape

The regulatory environment for IoT middleware is increasingly shaped by product-security and data-governance mandates that push security and compliance controls into device-management, connectivity-management, and application-enablement layers. In the European Union, Regulation (EU) 2024/2847 (Cyber Resilience Act) entered into force in December 2024, introducing lifecycle cybersecurity obligations for connected products, with key provisions applying from June 11, 2026 (conformity-assessment body notification framework) and from September 11, 2026 (manufacturer reporting obligations). The United Kingdom's Product Security and Telecommunications Infrastructure (PSTI) regime, administered by the Office for Product Safety and Standards (OPSS), has been in force since April 2024, reinforcing baseline requirements around security features for relevant connectable products and influencing vendor selection for middleware stacks used in smart-home, smart-building, and enterprise endpoints.

In the United States, NIST updated guidance that many suppliers map to for IoT product cybersecurity programs, including finalizing NIST IR 8259r1 in April 2026 and issuing the initial public draft of NIST SP 800-213r1 in June 2026 for federal IoT product cybersecurity guidelines. Across Asia, cybersecurity and sovereignty requirements continue to fragment technical requirements: China's MIIT published an IoT Innovation and Development Action Plan (2026-2028) that references cybersecurity certification (GB/T 42427-2023) and calls for newer terminal capabilities (including 3GPP Release 18 RedCap support), while India's Bureau of Indian Standards (BIS) issued a draft standard (IS 17730:2026) that elevates data localization and sovereignty controls, increasing the need for middleware features such as policy-based routing, localized storage options, audit trails, and configurable encryption and key-management profiles.

Value Chain Analysis

The IoT middleware value chain begins with device and module suppliers (MCUs, sensors, gateways, RedCap and LPWAN modules, secure elements), continues through connectivity providers (cellular and LPWAN operators, satellite-IoT enablers, eUICC/SIM provisioning platforms), and then into platform vendors delivering protocol translation, device onboarding, OTA lifecycle management, and application enablement (often packaged with edge runtimes and observability). This layer increasingly depends on adjacent software infrastructure, including time-series databases, container platforms for edge and hybrid deployments, identity and key-management services, and AI inference toolchains that operationalize analytics close to endpoints.

Recent partner-led integrations show how participants reduce fragmentation across protocols, edge software, and data back ends. In March 2026, 1NCE and Netmore combined cellular and LoRaWAN access into a unified coverage proposition, aligning connectivity-management with multi-network orchestration needs. In April 2026, InfluxData partnered with Litmus to connect InfluxDB 3 Enterprise with Litmus Edge, tightening the link between edge data collection and industrial analytics that middleware stacks commonly orchestrate. Security-oriented collaborations also extend the chain upstream: in December 2025, SEALSQ partnered with Airmod on a quantum-ready middleware direction tied to secure hardware, reflecting how compliance and cryptographic posture influence platform selection and integration effort for OEMs and industrial users.

Competitive Landscape

The IoT middleware market shows medium concentration as hyperscalers and industrial stalwarts balance breadth and depth. Amazon Web Services, Microsoft Azure, and Software AG headline market perception; AWS registered USD 28.79 billion cloud revenue in Q4 2024, while Microsoft’s intelligent cloud hit USD 40 billion, giving both scale to integrate protocol brokers, twin services, and analytics in one pane. Software AG spun out Cumulocity in January 2025, allowing focused development on industrial workflows while freeing parent capital for core database and process-mining pursuits.

Partnerships define differentiation. Oracle’s Edge Cloud aligns with AT&T 5G APIs for managed QoS, and Google Cloud now inter-runs OCI workloads, giving clients multi-cloud continuity. Telit Cinterion embedded DeviceWise AI into Nvidia’s GPU-optimized stack to simplify visual inspection rollouts, reflecting a pivot toward AI-native middleware. Edge computing patents signal sustained R&D: Intel leads with 522 filings, Pure Storage follows at 279, and IBM holds 245, including a grant on distributed MEC orchestration.

Consolidation is accelerating. u-blox exited cellular IoT to redirect spend to GNSS, while Planon acquired Axonize to expand smart-building breadth. Emerging entrants such as Golioth offer AI-enabled device frameworks, courting developers with micro-service-ready building blocks. Regional champions in Asia sell integrated hardware-software bundles that address compliance locally, helping to balance global giants and keep the IoT middleware market competitive.

IoT Middleware Industry Leaders

Cisco Systems Inc.

IBM Corp. (Red Hat Inc.)

Oracle Corporation

ClearBlade Inc.

PTC Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven interoperability and data-access requirements create whitespace for middleware that productizes compliance as configurable services. The EU Cyber Resilience Act, in force since December 2024, brings mandatory cybersecurity requirements that translate into market need for embedded SBOM workflows, vulnerability disclosure processes, secure update orchestration, and auditable device identity across heterogeneous fleets. These capabilities sit directly in device-management and application-enablement middleware.

Protocol harmonization and edge-centric consolidation also expand addressable use cases where middleware simplifies multi-protocol orchestration across Wi-Fi, cellular, and LPWAN domains. The standards roadmap provides a concrete pull: ISO/IEC 30141:2024 (IoT Reference Architecture) offers common design patterns for interoperable systems, while ITU-T Recommendation Y.4477 (November 2025) frames interoperability for IoT service platforms through defined entities and interworking processes. On the vendor side, SUSE's February 2026 acquisition of Losant shows active consolidation around industrial IoT orchestration and real-time intelligence within edge software portfolios (including Kubernetes distributions such as K3s), supporting deployments that blend cloud control planes with edge runtimes. Together, these shifts favor middleware products that unify connectivity, security posture, and data governance across hybrid cloud and edge deployments while reducing integration effort for enterprises moving from pilots to fleet-scale operations.

Recent Industry Developments

- July 2026: IBM and Red Hat expanded the Lightwell commercial offering to support trust infrastructure for AI-era open source. The move strengthens the governance and security layer that enterprises look for when deploying hybrid cloud and edge software stacks that host IoT integration and event-processing workloads. It also reinforces vendor-backed building blocks for identity, integrity, and policy controls that sit adjacent to middleware in regulated deployments.

- February 2026: Cisco and AT&T launched a 5G Standalone-native IoT platform integrating AT&Ts 5G SA core with Ciscos Mobility Services Platform capabilities such as IoT Control Center. The release targets higher performance and more programmable connectivity, which increases the importance of connectivity-management middleware that can automate provisioning, apply policy, and operate across evolving radio features. It also tightens telco-cloud alignment for enterprise IoT rollouts that span private and public networks.

- January 2025: Software AG completed the sale of Cumulocity to a management-led group backed by European investors. The separation created a more focused operating model around an established IoT application enablement platform, while the parent company redirected capital to its core portfolio. For buyers, the change affected roadmap clarity, partner strategy, and packaging options in competitive evaluations of industrial IoT middleware suites.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software layers that help connect, manage, and integrate IoT devices, networks, and applications so data can move securely and reliably from endpoints to business systems.

Scope exclusions: Hardware devices and sensors, pure connectivity services, and standalone application software that does not provide middleware functions are excluded.

Segmentation Overview

- By Platform

- Application Enablement

- Integrated Suites

- Low-Code Platforms

- Device Management

- OTA Firmware Updates

- Remote Provisioning and Diagnostics

- Connectivity Management

- Cellular CMP

- LPWAN CMP

- Application Enablement

- By Deployment Model

- Cloud

- On-Premise

- Edge / Fog

- By End-User Industry

- Manufacturing

- Healthcare

- Energy and Utilities

- Transportation and Logistics

- Agriculture

- Retail and E-Commerce

- Smart Cities (Municipal and Gov.)

- Other Industries

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model and to keep assumptions realistic across regions and industries. We relied on public sources such as ITU connectivity indicators, NIST cybersecurity guidance, FCC and ETSI/3GPP related publications, and OECD digital economy datasets to understand adoption signals and policy direction.

For market mapping, we also reviewed company annual reports, investor decks, product documentation, and reputable press coverage to track common middleware capabilities and deployment patterns. A paid subscription for company financials and news intelligence, plus a patent database, was used selectively to cross-check business exposure to IoT middleware functions and to spot feature shifts like device lifecycle tools and edge enablement. These examples are not exhaustive, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased as middleware and how pricing is set across cloud, on-premise, and edge deployments. We spoke with a mix of platform teams, systems integrators, and enterprise users across APAC, EMEA, and the Americas to confirm adoption drivers, typical contract structures, and the split between device management, connectivity management, and application enablement needs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 38% |

| Mid tier: 56% | Functional/Unit leaders: 40% | EMEA: 37% |

| Smaller Players: 14% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that reconstructs middleware spend from IoT deployment activity, and then narrows it to what qualifies as middleware value. The model is corroborated with selective bottom-up checks such as sampled price points by deployment model and a roll-up of representative supplier revenue exposure, which are then used to adjust totals where gaps show up.

Key inputs that guided the math included connected device growth by region, cloud versus edge workload mix, adoption of device provisioning and OTA update tooling, SIM and LPWAN connectivity management usage, and integration intensity across manufacturing, utilities, logistics, and smart city programs. When primary feedback indicated a mismatch in pricing logic, ASPs were normalized to common units like per device, per connection, or per site, before being applied to volume indicators.

Forecasts were built using multivariate regression, where forward drivers like device base expansion, enterprise digitization budgets, and edge rollout pace were combined with scenario analysis for security and regulation sensitivity. If a bottom-up cross-check was missing for a niche region or vertical, the gap was handled using proxy penetration rates from similar markets and then re-tested with follow-up expert inputs.

Data Validation & Update Cycle

Outputs are validated through triangulation across desk signals, primary inputs, and internal consistency checks across platforms, deployment models, and regions. Outliers such as sudden regional spikes or unusual platform mix shifts are flagged, reviewed, and recalculated, and respondents are re-contacted when an assumption materially changes.

Before sign-off, the model and key assumptions go through multi-step analyst reviews so arithmetic, currency timing, and unit conversions are checked in a repeatable way. Reports are refreshed annually, and interim updates are made when major events change adoption or pricing. Right before delivery, a fresh final pass is done so clients receive the most current view available.

Mordor Intelligence's IOT Middle Ware Market Sizing Compared With Other Published Estimates

Published IoT middleware numbers often vary because different studies do not count the same things as middleware, and they also pick different time bases and pricing units. Differences show up quickly when one estimate emphasizes device management only, while another also includes application enablement suites and connectivity management fees.

Key gap drivers in this market typically come from scope choices (for example, whether edge and fog deployments are counted the same as cloud), how platform functions are grouped, and whether pricing is modeled per device, per connection, or as bundled enterprise subscriptions. Some estimates also lean on aggressive device growth curves or older currency conversions, which can widen totals if refresh cadence is slower.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.33 B (2026) | |

| Global Advisory A | USD 18.18 B (2025) | Uses a 2025 base year and a wider functional split that can pull adjacent platform layers into the total, and its pricing basis can lean more on subscription bundles than device or connection linked units. |

| Industry Publisher B | USD 14.74 B (2025) | Applies a narrower middleware lens that is closer to core device and connectivity management, and it can undercount application enablement and edge deployments when these are packaged inside broader IoT programs. |

The table shows most of the spread is explained by base year alignment and what gets counted as middleware versus adjacent IoT platform software, and then by how prices are normalized across units. By keeping application enablement, device management, and connectivity management as explicit value pools and rechecking unit economics during updates, the estimate stays traceable to repeatable inputs, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the IoT middleware market?

The IoT middleware market size is USD 21.33 billion in 2026.

How fast will the IoT middleware market grow over the next five years?

The market is projected to expand at an 18.43% CAGR, reaching USD 49.72 billion by 2031.

Which platform segment leads the IoT middleware market?

Application-enablement platforms lead with 47.35% of 2025 revenue.

Why is healthcare the fastest-growing vertical?

Smart-hospital roll-outs and 6G-ready patient monitoring drive a 19.65% CAGR for healthcare deployments.

What role does edge computing play in IoT middleware adoption?

Edge and fog nodes address latency and data-sovereignty needs, resulting in a 21.05% CAGR for distributed architectures.

Which region offers the highest growth opportunity?

Asia Pacific leads with a 20.95% CAGR due to extensive 5G coverage and supportive government policies.

Page last updated on: