Intermediate Bulk Container Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.97 Billion |

| Market Size (2031) | USD 14.72 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intermediate Bulk Container Market Analysis by Mordor Intelligence

The IBC market size was valued at USD 11.48 billion in 2025 and estimated to grow from USD 11.97 billion in 2026 to reach USD 14.72 billion by 2031, at a CAGR of 4.23% during the forecast period (2026-2031). Accelerating adoption of IoT-enabled containers, strict traceability mandates in global chemical and pharmaceutical supply chains and growing circular-economy regulations are reinforcing steady demand for advanced bulk-handling solutions. Flexibility in design, including collapsible and foldable variants, is allowing shippers to lower empty-return costs while maintaining payload integrity, a factor particularly attractive to exporters of high-margin ingredients. Parallel expansion of biosimilar drug production and specialty chemical capacity across Asia-Pacific keeps rigid composite configurations in favor even as flexible formats post faster growth.[1]Chemical and Engineering News, “Asia’s Chemical Capacity Expands,” cen.acs.org Consolidation among leading suppliers, with a focus on integrated reconditioning and digital service platforms, is enhancing after-sales value capture and intensifying competition at the premium end of the IBC market.[2]Greif Inc., “Greif Completes Acquisition of Ipackchem Group,” greif.com

Key Report Takeaways

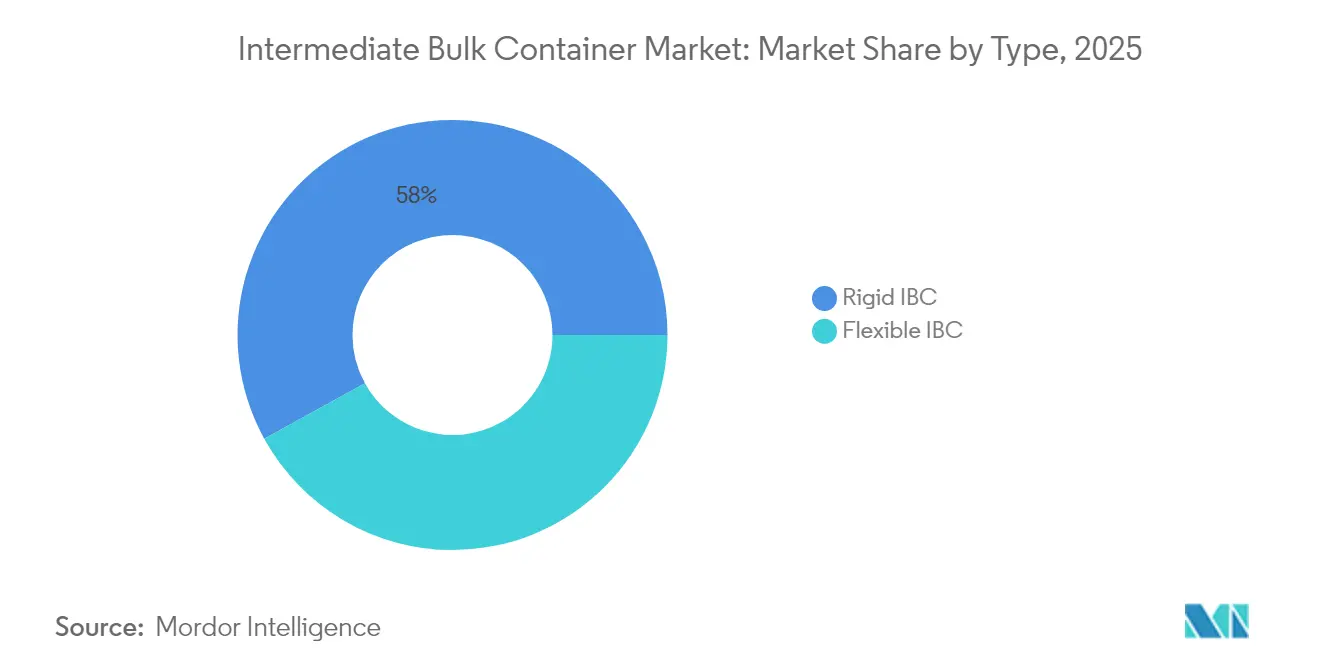

- By type, rigid variants held 58.02% of the IBC market share in 2025 while flexible designs are projected to expand at a 5.55% CAGR through 2031.

- By material, plastic commanded 39.10% of the 2025 IBC market size, whereas composite formats are forecast to grow at a 6.55% CAGR to 2031.

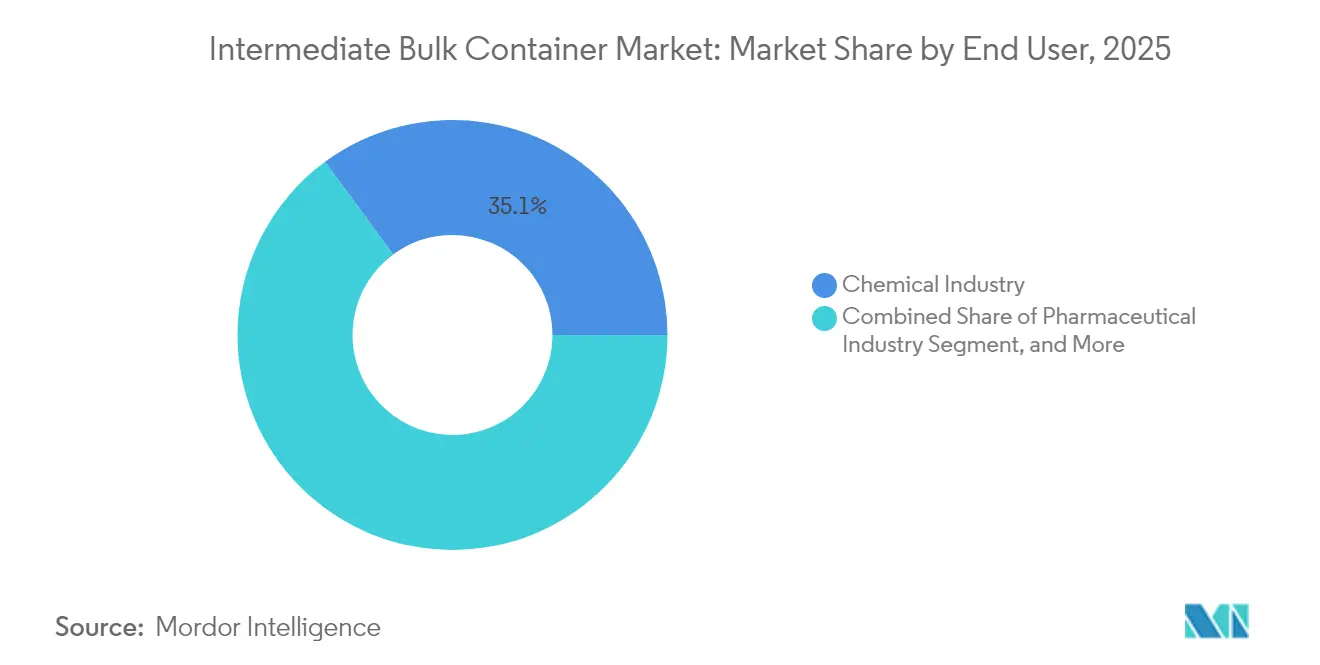

- By end user, chemical applications led with 35.10% revenue share in 2025; pharmaceutical uses are expected to register a 7.02% CAGR through 2031.

- By design, standard containers retained 40.95% of the IBC market size in 2025, yet smart IoT-integrated options are advancing at a 7.45% CAGR to 2031.

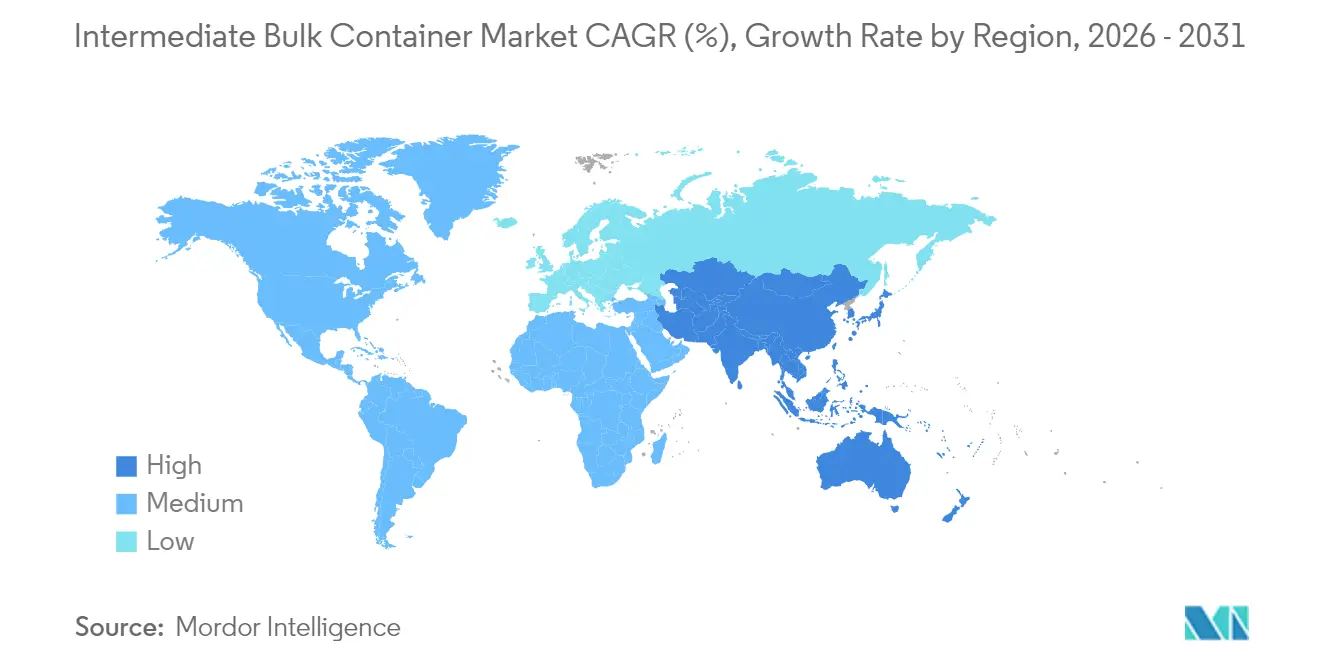

- By geography, Asia-Pacific accounted for 40.10% of the IBC market in 2025 and is set to grow at a 6.55% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intermediate Bulk Container Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing export of IBC-packed products | +0.8% | Global, APAC and Europe | Medium term (2-4 years) |

| Expansion of chemical and pharmaceutical output | +1.2% | APAC core, spill-over to North America | Long term (≥4 years) |

| Shift toward reusable industrial packaging | +0.6% | Europe and North America, expanding to APAC | Long term (≥4 years) |

| Deployment of IoT-enabled smart IBCs | +0.7% | North America and Europe, early APAC | Short term (≤2 years) |

| Growth in food and beverage bulk logistics | +0.4% | Global, strong in emerging markets | Medium term (2-4 years) |

| Carbon-border taxes boosting circular packaging | +0.5% | Europe primary, trade partners | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Chemical and Pharmaceutical Output

Asia-Pacific lifted regional chemical capacity by 12% in 2024, sparking sustained container demand for raw materials and finished products. India’s surging biosimilar facilities and Vietnam’s new specialty complexes favor standardized composite IBCs that meet corrosive-resistance benchmarks. Continuous-manufacturing lines require closed-loop transfer systems, pushing adoption of smart sensors for sterility verification. Suppliers that integrate digital monitoring directly into container walls gain a pricing edge with pharmaceutical buyers. Over the long term, these production hubs are expected to underpin roughly one-third of incremental IBC market growth.

Growing Export of IBC-Packed Products

Cross-border flows of liquid chemicals reached USD 2.1 trillion in 2024, with exporters prioritizing weight-optimized flexible IBCs to curb freight costs. Temperature-controlled routes for active pharmaceutical ingredients now rely on insulated composite drums outfitted with data-logging patches that validate chain-of-custody. Extended voyage times between Asia and Europe further highlight the cost advantage of foldable empty returns. As maritime decarbonization drives carriers to scrutinize payload density, exporters adopting lighter, RFID-tagged liners are positioned to negotiate favorable rates, reinforcing the pull on the IBC market.

Deployment of IoT-Enabled “Smart” IBCs

Smart-container fleets rose 180% year-on-year in 2024, led by pharmaceutical compliance needs for real-time serialization. Embedded sensors now detect pressure variances within ±0.2 bar, instantly flagging seal failures. Cloud dashboards synthesize temperature, geolocation and vibration data, reducing spoilage by up to 25% through predictive interventions. Early movers in Europe and North America leverage these analytics to cut emergency maintenance costs, shortening payback to four reuse cycles. Demand is spreading to Asia as regional regulators mirror European traceability codes, sustaining a near-term boost to the IBC market.

Shift Toward Reusable Industrial Packaging

Fortune 500 sustainability pledges are stripping virgin plastic from purchase requisitions, accelerating multi-trip container strategies. Reusable IBCs deliver total cost savings of 40-60% across ten life cycles, outpacing single-use drums even before factoring in landfill levies. Europe’s 65% recycling mandate effective 2030 is catalyzing investment in composite shells with separable inner linings. Brands adopting closed-loop logistics stamp ESG credentials onto product labels, unlocking premiums in consumer chemicals and food ingredients. Reconditioning networks thus evolve from cost-play to strategic differentiator, reinforcing positive momentum in the IBC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising use of reconditioned and rebottled IBCs | -0.9% | Global, cost-sensitive markets | Medium term (2-4 years) |

| Environmental scrutiny of plastic containers | -0.6% | Europe and North America, global spread | Long term (≥4 years) |

| EPA SCCAP rule raises stationary-source risk | -0.3% | United States | Short term (≤2 years) |

| Recycled HDPE supply-chain volatility | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Use of Reconditioned and Rebottled IBCs

Specialized refurbishers now attain 95% performance parity with newly manufactured units, drawing cost-focused buyers toward lower-priced alternatives. Inflationary pressures during 2024 amplified this shift as chemical shippers deferred capex cycles. Regulatory bodies increasingly certify reconditioned containers for non-pharma materials, converting what once was a stopgap into a mainstream procurement option. New IBC sales therefore confront a structural headwind, particularly in commoditized segments of the IBC market.

Environmental Scrutiny of Plastic Containers

The EU Single-Use Plastics Directive, slated to include industrial formats by 2026, is intensifying demand for bio-based resins and recyclable metal-composite hybrids.[3]European Commission, “Single-Use Plastics Directive – Extension Proposal,” ec.europa.eu Consumer-facing conglomerates such as Nestlé now audit upstream packaging footprints, trimming purchase volumes of HDPE-dominant skus. Compliance adds certification costs and forces redesigns that erode margins on traditional plastic IBCs. As global brands ripple these standards through supplier networks, the restraint is expected to chip 0.6 percentage points from the IBC market’s growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rigid Solutions Dominate Despite Flexible Growth

Rigid containers retained 58.02% of the 2025 IBC market share, owing to high mechanical stability in chemical and pharmaceutical filling lines. Standardized pallet footprints allow high-speed robotic handling, an asset in 24/7 production environments. The IBC market size for flexible variants is projected to rise at a 5.55% CAGR, underpinned by 40% empty-return space savings that translate into lower freight emissions. Food ingredient shippers increasingly favor these liners for non-hazardous fluids, though IoT retrofits remain less straightforward than with rigid shells. Major producers are adding flexible capacity in Southeast Asia, signalling a long-term rebalancing of the IBC market.

Rigid adoption persists where UN Group II and III classifications prevail, such as acids and agrochemicals. Integrated dip-tube outlets boost line throughput by 12%, supporting just-in-time delivery models. Flexible designs, conversely, are carving niches in flavor concentrates and plant-based oils where contamination risk is lower and disposal simplicity ranks high. As sensors shrink and adhesive power supplies mature, the technology gap will likely narrow, triggering faster smart-feature infusion into flexible IBC market offerings.

By Material: Plastic Leadership Faces Composite Challenge

Plastic held 39.10% of the IBC market share in 2025, leveraging cost-efficient blow-molding lines and broad chemical compatibility. Composite shells, however, are advancing at a 6.55% CAGR through 2031 as shippers prioritize corrosion resistance against high-purity solvents. Recyclable, layered structures allow inner HDPE bottles to be replaced independently of outer metal cages, extending service life by 25%. Volatility in recycled HDPE prices widens the relative attractiveness of glass-fiber reinforced polypropylene, positioning composites to chip away at the established plastic IBC market.

Metal drums still dominate extreme-temperature and high-pressure applications, while fiberboard attracts organic food exporters requiring biodegradable containers. Pharmaceutical buyers remain cautious, demanding USP-class formulations that plastics meet more readily, yet increasing regulatory emphasis on carbon disclosures could tilt preferences toward lighter composites over the forecast window. Material innovators that provide cradle-to-cradle certification are likely to secure premium contracts in the evolving IBC market.

By End User: Chemical Dominance Meets Pharmaceutical Dynamism

Chemical producers accounted for 35.10% of 2025 revenue, reflecting entrenched use of standardized 1,000-liter units for acids, solvents and agricultural inputs. Predictable rotation cycles favor rigid plastic and metal variants with proven performance in closed-loop circuits. Pharmaceutical buyers, while a smaller base, underpin the fastest 7.02% CAGR thanks to expanded biosimilar pipelines and serialization mandates. Smart IBC adoption accelerates here, as real-time logging supports Good Distribution Practice validation.

Food and beverage processors expand at moderate pace, lured by bulk-ingredient efficiency and sanitary liners certified to FDA 21 CFR standards. Agriculture emerges as an incremental growth pocket with precision-application fertilizers demanding calibrated dosing systems. Logistics providers now bundle cleaning, inspection and telemetry services, deepening ecosystem stickiness and broadening revenue beyond the sale of physical containers, which in turn elevates service content in the IBC market.

By Design: Standard Solutions Yield to Smart Innovation

Standard configurations commanded 40.95% of the IBC market size in 2025 since they meet baseline requirements at the lowest unit cost. Nevertheless, IoT-integrated variants posting a 7.45% CAGR signal a shift toward data-rich value propositions. Sensor arrays sampling temperature every 30 seconds prevent thermal excursions in vaccines, securing regulatory clearance from both FDA and EMA auditors. Collapsible formats trim warehouse footprints by 60% when empty, ideal for urban micro-fulfillment nodes.

Heated coils embedded in stainless-steel walls maintain viscous materials above solidification thresholds, enabling just-in-time processing of fats and resins. Market entrants focusing on retrofit sensor caps allow legacy fleets to digitize without wholesale replacement, a transitional pathway that accelerates smart-fleet penetration. As these advanced designs mature, their aggregated data outputs will create secondary analytics revenues, bolstering margins within the IBC market.

Geography Analysis

Asia-Pacific dominated the IBC market with 40.10% share in 2025 and is projected to expand at 6.55% CAGR through 2031. China’s USD 1.7 trillion chemical output and India’s 15% export surge in pharmaceuticals underpin continuous container demand across raw-material and finished-drug logistics. Local governments offer tax incentives for reusable packaging assets, lowering payback periods for smart composite units. Emerging ASEAN clusters, notably Vietnam and Thailand, are installing new polymer and aromatic complexes, each including dedicated IBC cleaning bays to sustain multi-trip schemes.

Europe showcases nuanced, regulation-driven demand that skews toward high-end, circular-compliant solutions. German and French pharma firms top global rankings in sensor-equipped fleets, leveraging Industry 4.0 frameworks for predictive maintenance. EU Packaging and Packaging Waste rules drive 65% recycling targets by 2030, accelerating adoption of detachable liner systems. The regulatory-first environment enables suppliers to command 10-15% price premiums for certified low-carbon IBC market offerings.

North America centers on quality-critical pharmaceutical and specialty chemical sectors. The United States chemical output of USD 553 billion in 2024 translates into robust baseline volumes, especially for UN Class 8 corrosives moved via rail and drayage. Mexico’s near-shoring wave is spurring fresh demand for rigid composite containers as new resin plants come online. Mature road and rail networks facilitate asset-tracking platforms that optimize fleet rotation, reinforcing digital-service revenue within the regional IBC market.

Competitive Landscape

The market displays moderate concentration, with Greif, Mauser Packaging Solutions and Schuetz anchoring global share through extensive manufacturing and reconditioning footprints. Their vertical integration, spanning resin compounding to end-of-life recycling, sharpens cost control and speeds response to regional spikes in demand. Greif’s USD 576 million Ipackchem acquisition in 2024 augmented flexible-container capacity and widened specialty-chemical customer reach. Mauser’s Pune facility launch enhances South Asian supply resilience, aligning with pharmaceutical cluster growth.

Technology differentiation is intensifying. Schuetz’s composite innovations pair corrosion resistance with component separability, boosting recyclability to 90%. Schoeller Allibert’s Smartlink platform couples sensor hardware with SaaS dashboards, monetizing data subscriptions and driving customer stickiness. Disruptors offering retrofit IoT kits broaden access for mid-tier fleets, narrowing technology gaps. Success increasingly hinges on pairing durable containers with predictive analytics and efficient reconditioning networks, securing recurring revenue and elevating service intensity in the IBC market.

Intermediate Bulk Container Industry Leaders

Greif Inc.

Bulk Lift International LLC

Global-Pak LLC

FlexiTuff Ventures International Ltd.

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Greif announced pilot deployment of blockchain-enabled certificates of reconditioning to verify container provenance for pharmaceutical customers.

- October 2024: Greif completed its USD 576 million acquisition of Ipackchem Group, expanding flexible IBC capacity across three continents.

- September 2024: Schoeller Allibert launched Smartlink-enabled IBCs fitted with multisensor nodes for real-time location and condition monitoring.

- August 2024: HOYER Group acquired Tank Management Partners to bolster North American fleet services.

Global Intermediate Bulk Container Market Report Scope

The Intermediate Bulk Container Market typically comprises of rigit and flexible bulk containers typically made up of polymers, plastic composits or metals. These are used mainly for storage and transport of materials or finished goods in various industries like chemicals, pharmaceuticals, food and beverage, among others.

The Report Includes Global Intermediate Bulk Container Suppliers and the Market is segmented by Type (Rigid and Flexible), End User(Chemicals, Pharmaceuticals, Food and Beverage, Others) and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD ) for all the above segments.

| Rigid IBC |

| Flexible IBC |

| Plastic IBC |

| Metal IBC |

| Composite IBC |

| Fiberboard IBC |

| Chemical Industry |

| Pharmaceutical Industry |

| Food and Beverage Industry |

| Agriculture |

| Transport and Logistics |

| Other End Users |

| Standard IBC |

| Collapsible / Foldable IBC |

| Heated IBC |

| Smart / IoT-Enabled IBC |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Type | Rigid IBC | ||

| Flexible IBC | |||

| By Material | Plastic IBC | ||

| Metal IBC | |||

| Composite IBC | |||

| Fiberboard IBC | |||

| By End User | Chemical Industry | ||

| Pharmaceutical Industry | |||

| Food and Beverage Industry | |||

| Agriculture | |||

| Transport and Logistics | |||

| Other End Users | |||

| By Design | Standard IBC | ||

| Collapsible / Foldable IBC | |||

| Heated IBC | |||

| Smart / IoT-Enabled IBC | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the IBC market in 2026?

The IBC market size is USD 11.97 billion in 2026 and is projected to reach USD 14.72 billion by 2031.

Which region leads adoption of smart IBCs?

Europe and North America currently lead smart-container deployment, with Asia-Pacific rapidly catching up.

What is the fastest-growing IBC material type?

Composite containers are forecast to grow at a 6.55% CAGR, outpacing plastic and metal formats.

Why are pharmaceutical companies investing in IoT-enabled IBCs?

Real-time monitoring ensures cold-chain integrity and supports regulatory serialization mandates, reducing spoilage and compliance risk.

How do reuse programs impact total packaging cost?

Reusable IBCs deliver 40-60% lifetime savings versus single-use drums across typical ten-cycle service lives.

What is driving flexible IBC demand?

Exporters favor flexible designs for their 40% empty-return space savings, which lower freight costs and emissions.

Page last updated on: