Automated Feeding Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

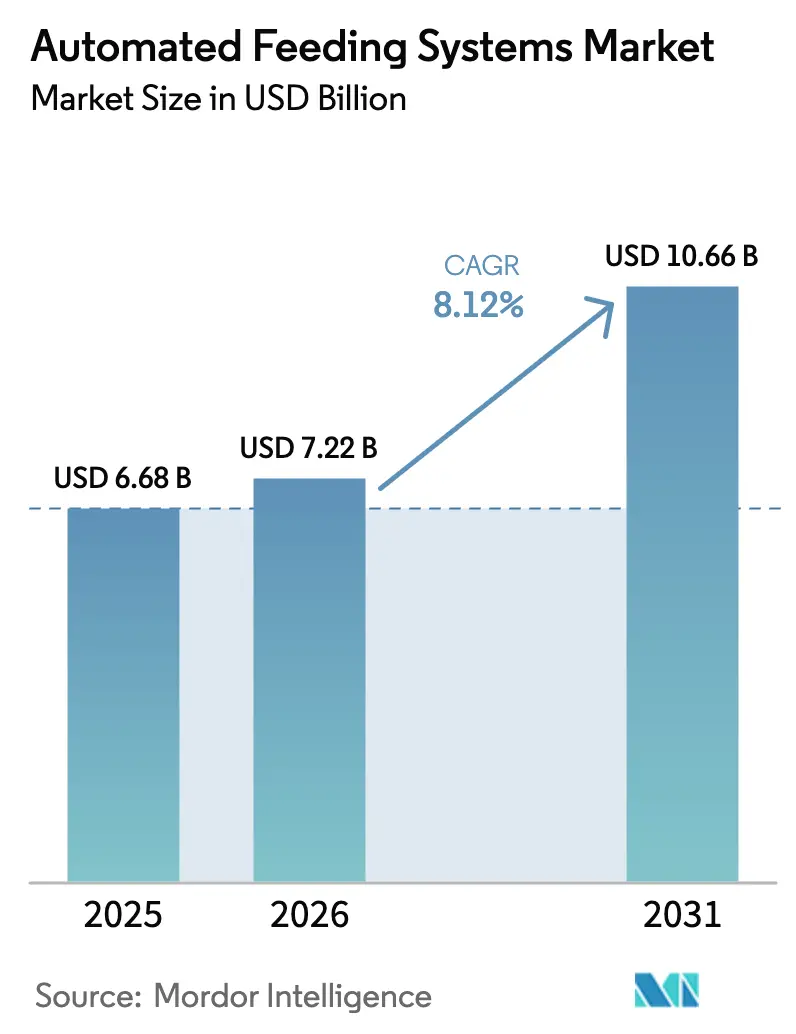

| Market Size (2026) | USD 7.22 Billion |

| Market Size (2031) | USD 10.66 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Feeding Systems Market Analysis by Mordor Intelligence

The automated feeding systems market size was valued at USD 6.68 billion in 2025 and estimated to grow from USD 7.22 billion in 2026 to reach USD 10.66 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). Rising demand for precision livestock farming, escalating labor costs, and sustained pressure on feed efficiency continued to propel investment in data-enabled automation. Advances in artificial intelligence strengthened individualized rationing, while modular retrofit kits widened the addressable base among small farms. Meanwhile, environmental regulation in Europe and carbon-credit schemes in North America encouraged solutions that lower methane intensity. Competitive rivalry stayed moderate as incumbents defended share through integrated platforms and service contracts, yet software-led entrants targeted underserved segments with analytics-first offerings.

Key Report Takeaways

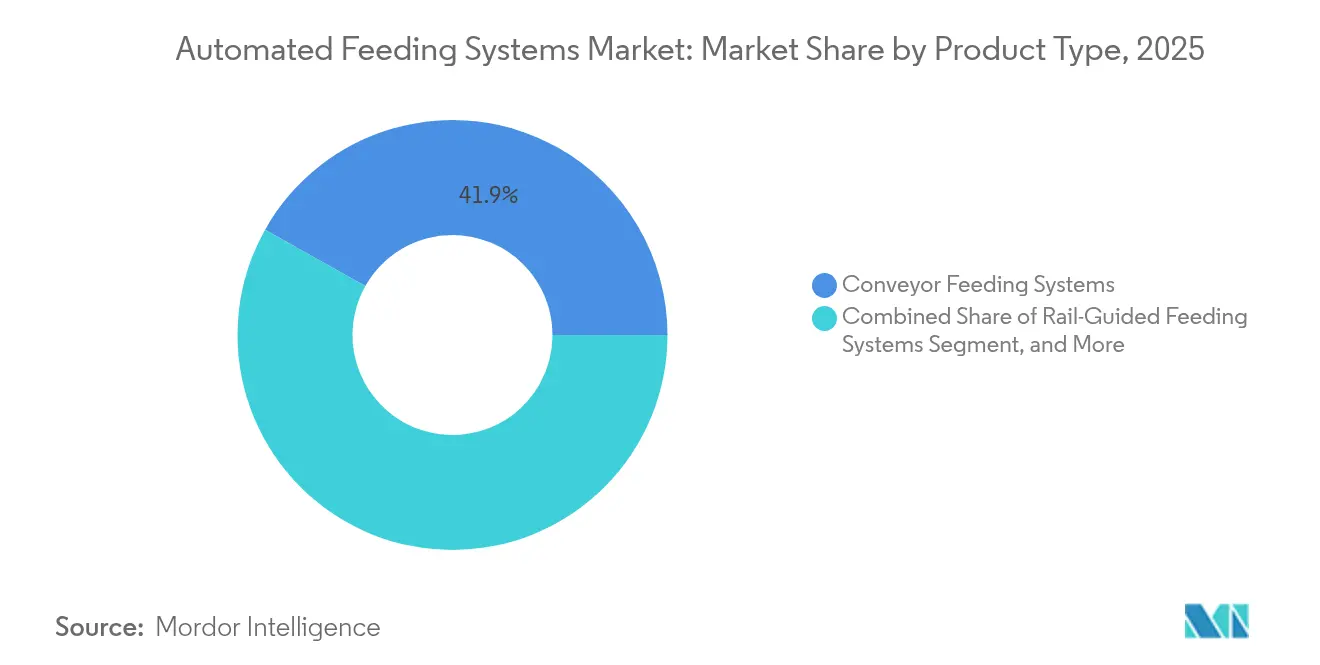

- By product type, conveyor feeding systems held 41.85% of automated feeding systems market share in 2025, while self-propelled units posted the fastest 10.78% CAGR to 2031.

- By livestock, ruminants accounted for 45.90% share of the automated feeding systems market size in 2025; poultry automation is advancing at a 9.56% CAGR through 2031.

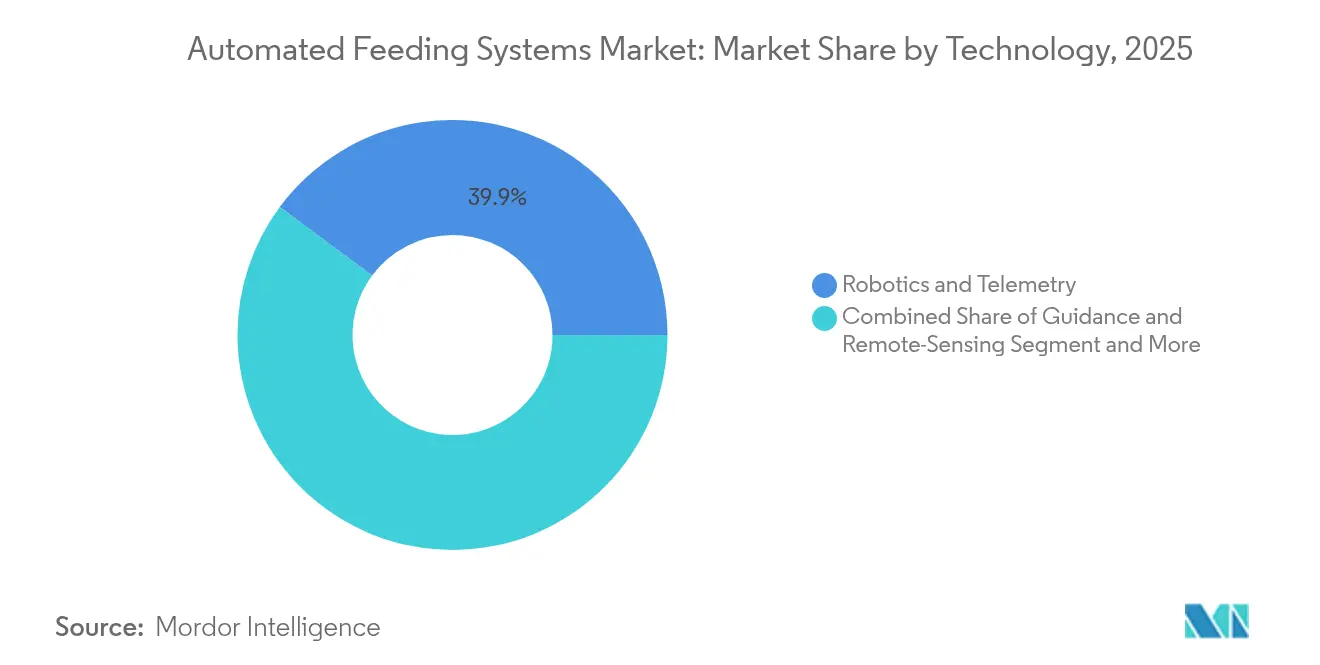

- By technology, robotics and telemetry remained dominant at 39.85% revenue share in 2025, yet machine-vision and AI analytics are forecast to expand at a 12.15% CAGR.

- By farm size, large farms (>500 head) commanded 36.75% of automated feeding systems market share in 2025, whereas small farms (≤100 head) are growing at a 10.42% CAGR.

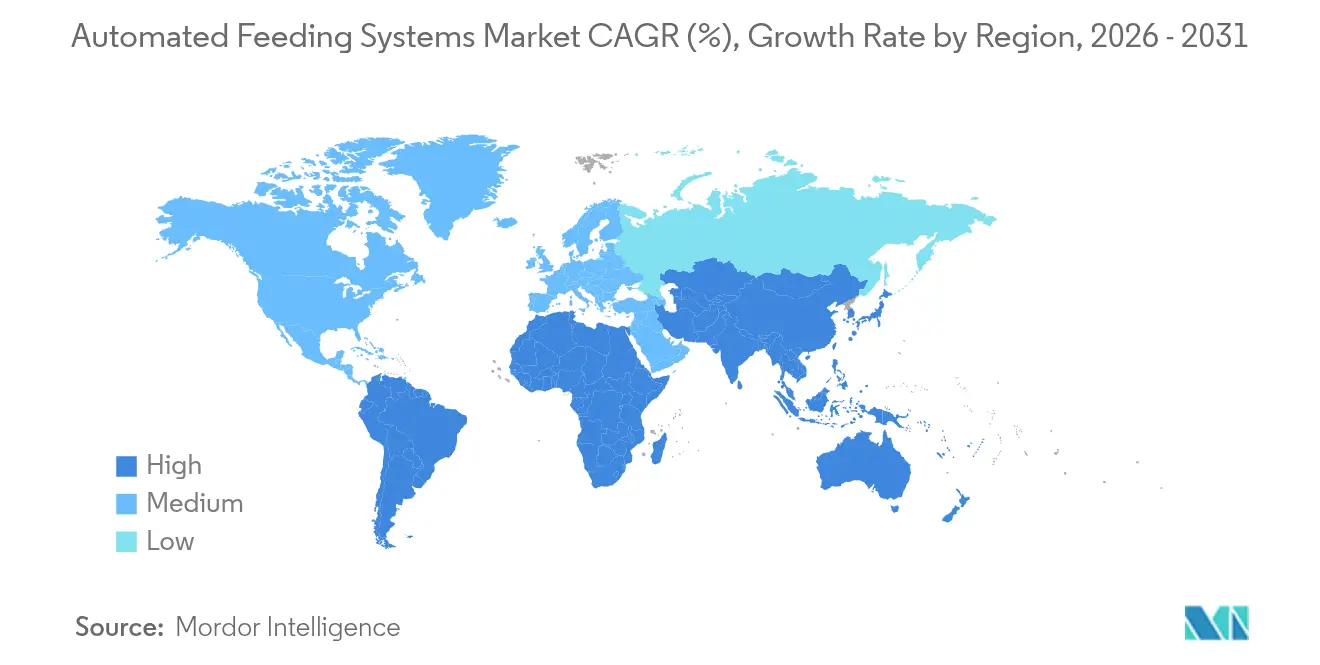

- By geography, Europe led geographically with 32.90% revenue share in 2025; Asia-Pacific is the fastest-growing regional automated feeding systems market with a 9.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Feeding Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising dairy herd sizes in emerging economies | +1.2% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Labor shortages and escalating wage costs | +1.8% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Precision-feeding demand to optimize feed conversion ratio | +2.1% | Global, led by intensive farming regions | Medium term (2-4 years) |

| AI-driven individualized rationing algorithms | +1.5% | North America, Europe, developed APAC markets | Long term (≥ 4 years) |

| Carbon-credit incentives for low-methane feeding | +0.8% | Europe, North America, Australia | Long term (≥ 4 years) |

| Modular retrofit kits for smallholder farms | +0.9% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Dairy Herd Sizes in Emerging Economies

Average herd sizes expanded quickly in India, Brazil, and parts of Southeast Asia, prompting farmers to adopt scalable automation that keeps labor inputs flat as headcounts grow. Consolidation among smallholders into cooperative models heightened interest in shared feeding infrastructure. In Brazil, installations of automated systems exceeded 500-cow thresholds on many operations, supported by local manufacturers that tailored equipment to tropical forage conditions. [1]InoBram, “Automação e tecnologia para granjas,” inobram.com.br Larger herds also created richer data sets, enabling more accurate ration algorithms and accelerating returns on sensor investments.

Labor Shortages and Escalating Wage Costs

Agricultural workforces in Europe and North America continued to age, while immigration curbs further restricted seasonal hiring pools. Hourly pay for skilled dairy workers rose faster than general inflation, turning feed delivery into a prime automation target. Michigan State University Extension reported that automated systems cut labor hours by 20% and redeployed remaining staff toward health management tasks. Producers used these savings to justify capital outlays even when feed price volatility complicated budget planning.

Precision-Feeding Demand to Optimize Feed Conversion Ratio

Feed remained 60-70% of production cost, so incremental efficiency gains had outsized profit leverage. Integrated scales, cameras, and bunk sensors generated continuous intake data that platforms used to fine-tune nutrient density. A peer-reviewed study found that individualized rations lifted milk yield 5-10% while trimming feed bills on automated dairies. Similar benefits emerged in swine and broiler houses where over-feeding protein previously reduced margins and raised nitrogen emissions.

AI-Driven Individualized Rationing Algorithms

Machine-learning models processed behavior, weather, and historical performance to recommend daily recipe adjustments for each pen or cow. Systems from Precision Livestock Technologies predicted intake fluctuations hours ahead, enabling proactive ration balancing. Early anomaly detection flagged health issues before clinical signs appeared, lowering veterinary costs and mortality. Continuous learning improved algorithm accuracy, strengthening competitive moats for vendors offering cloud updates and remote support contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital and long pay-back period | -1.3% | Global, particularly impacting small-medium farms | Short term (≤ 2 years) |

| Multi-brand equipment interoperability gaps | -0.7% | Global, with higher impact in fragmented markets | Medium term (2-4 years) |

| Cyber-security risks to connected feeding robots | -0.5% | Developed markets with high connectivity | Long term (≥ 4 years) |

| Forage-quality variability limiting algorithm accuracy | -0.4% | Regions with inconsistent feed supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital and Long Pay-Back Period

Turn-key installations ranged from USD 150,000 to USD 275,000 in 2025, and multi-robot layouts could exceed USD 1 million on large sites. Payback often stretched 7–12 years, a horizon many family farms considered risky against volatile milk or hog prices. Steel and aluminum tariffs increased hardware bills by 7–8%, delaying purchase decisions. Lenders asked for detailed ROI modelling, pushing suppliers to bundle financing and extended warranties to ease adoption.

Multi-Brand Equipment Interoperability Gaps

Feeding robots, milking units, and climate controllers frequently ran proprietary protocols that hindered plug-and-play integration. Producers juggling several vendors incurred extra software and hardware bridges, raising total cost of ownership. While ISOBUS standards progressed, inconsistent implementation still forced operators to maintain multiple control terminals. The issue remained most acute on retrofits where legacy gear lacked modern gateways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Self-Propelled Systems Drive Innovation

Conveyor units dominated in 2025 with 41.85% automated feeding systems market share, reflecting their proven reliability in high-volume dairies. Continuous belts delivered uniform rations to bunk lines with limited supervision, supporting steady milk output. However, self-propelled robots captured attention by removing the fixed rail cost that previously limited layout flexibility. This category is forecast to expand at an 10.78% CAGR, outpacing the overall automated feeding systems market. DeLaval’s OptiWagon illustrated the shift with autonomous route mapping and recipe customization that served up to 1,000 cows.

The automated feeding systems market size for self-propelled platforms is projected to nearly double between 2026 and 2031 as beef and goat enterprises join dairy adopters. Rail-guided trolleys remained a middle-ground choice where barns already possessed track beams, while batch lines gained favor on boutique farms seeking controlled portioning. TMR mixers integrated directly with robotic arms to ensure homogenous blends, reinforcing milk-fat stability and reducing sort-back waste.

By Livestock: Poultry Automation Accelerates

Ruminant operations held 45.90% automated feeding systems market share in 2025 since dairy margins could absorb capital investment and complex ration software. Systems tailored to cow rumen physiology fine-tuned forage-to-concentrate ratios, boosting feed efficiency by several points. The automated feeding systems market size tied to poultry barns is expected to eclipse USD 2.17 billion by 2031 after growing at 9.56% annually, as integrators standardize climate-controlled houses that pair chain feeders with data dashboards. Big Dutchman introduced scalable conveyors delivering precise pellet counts, improving broiler uniformity.

Swine producers continued shifting toward liquid feeding modules that blend whey or brewery by-products, lowering ration cost while enhancing daily gain. Aquaculture emerged from a niche into a meaningful sub-segment once AI-enabled blowers synchronized feed pulses with fish appetite patterns. Advantech documented shrimp ponds where optical sensors trimmed feed waste and lifted conversion metrics.

By Technology: Machine Vision and AI Analytics Lead Innovation

Robotics and telemetry accounted for 39.85% revenue in 2025, supplying the motion control, sensor fusion, and remote alerts fundamental to any automated feeding systems market deployment. Yet demand pivoted toward machine-vision modules and AI inference chips that bring contextual decision-making onboard. The automated feeding systems market size linked to vision-AI bundles is set to increase at a 12.15% CAGR through 2031. Depth cameras and YOLO V8 algorithms achieved 86% accuracy in detecting leftover feed in duck troughs, guiding real-time dispense reductions.

RFID and IoT tags expanded traceability by connecting individual animal IDs to consumption logs. Combined with cloud dashboards, managers benchmarked productivity across farms and triggered early alerts when deviations emerged. Guidance and remote-sensing innovations such as ultra-wideband beacons improved indoor positioning, enabling smoother robotic navigation in tightly packed barns.

By Farm Size: Small Farms Drive Unexpected Growth

Operations above 500 head still captured 36.75% automated feeding systems market share in 2025 because return on investment rose along with feed volume handled. These sites typically integrated feeding robots with manure scrapers, ventilation, and parlor analytics to maximize data synergy. Nevertheless, small-scale holdings recorded a 10.42% CAGR as vendors introduced modular kits priced under USD 50,000. FodderWorks offered containerized sprouts systems sized from 110-pound daily output upward, letting goat and sheep keepers automate without trenching electrical lines.

The automated feeding systems market size among medium farms remained steady as owners selectively mechanized the most labor-heavy chores while waiting for cost curves on full robotics to fall. Leasing models and cooperative ownership schemes also surfaced, lowering upfront barriers and letting neighbors share high-tech assets.

Geography Analysis

Europe retained leadership at 32.90% of 2025 revenue, energised by Common Agricultural Policy measures that rewarded nutrient-use efficiency. Germany’s Federal Ministry of Food and Agriculture funded 36 AI agriculture projects totaling EUR 44 million (USD 47 million), many focused on livestock data platforms. The Netherlands extended its early-mover advantage as Lely scaled global installations of robotic feeders and milking units. Scandinavian countries mandated slurry-nitrogen caps that further stimulated precision feeding adoption to cut excreted surplus.

Asia-Pacific delivered the fastest 9.34% CAGR forecast, underpinned by dietary shifts toward animal protein and government modernization drives. Chinese beef operators piloted intelligent barn management to address low equipment utilization and high per-unit feed costs. India’s cooperative dairies launched automation pilots under Digital Milk Mission schemes, while Japan subsidized smart sensors for aging farmers seeking labor relief. Rising poultry integrator capex in Thailand and Vietnam created pull-through for chain feeders and optical pellet counters. North America faced headwinds from steel tariffs that lifted robot list prices and squeezed tractor sales by 15.8% in January 2025 versus prior-year levels. Yet chronic labor scarcity and animal-welfare scrutiny preserved a solid replacement pipeline. John Deere and DeLaval’s Milk Sustainability Center exemplified holistic platforms that merge agronomy, emissions, and feeding data so operators could document nutrient-use efficiency for processors. South America advanced on the back of Brazilian swine integrators like ROBOAGRO, while Argentina’s carbon-neutral beef pilot credited feed-efficiency gains when awarding certification.

Competitive Landscape

The automated feeding systems market displayed moderate concentration. DeLaval, GEA, and Lely leveraged global service footprints, vertically integrated hardware, and long-term software subscriptions to protect share. DeLaval doubled its automatic milking machine capacity in 2024 and released the Milking Automation MA Series parlour retrofit in January 2025, extending its ecosystem reach. GEA secured FDA clearance for its Monobox robotic milker, pairing it with synchronized ration dispensers to promote all-in-one procurement. [4]Feedstuffs, “Automated milking system cleared by FDA for Grade A milk production,” feedstuffs.com

Lely celebrated its 5,000th Astronaut robot in mid-2024 and bundled new feeding modules under its Farm of the Future roadmap. Precision Livestock Technologies emerged as a disruptor, using AI predictive models that run on commodity edge devices and integrate with third-party mixers. Advantech targeted aquaculture with optical sensors and cloud analytics, an area where incumbent dairy specialists held limited domain expertise.

Partnerships intensified as hardware makers sought data talent, evidenced by John Deere collaborating with DeLaval. Meanwhile, regional specialists such as InoBram in Latin America carved niches by customizing to local forage and barn layouts. Overall, top five suppliers controlled roughly 55-60% of revenue, leaving room for nimble entrants who focused on software, retrofit kits, or underserved geographies.

Automated Feeding Systems Industry Leaders

DeLaval International AB

GEA Group AG

Lely Industries N.V.

Trioliet B.V.

Schauer Agrotronic GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Precision Livestock Technologies rolled out an AI-powered predictive cattle feeding system that links behavior, ration, and weather data to automated dispensing recommendations.

- June 2025: GEA’s Monobox Automated Milking System earned FDA Grade A clearance, integrating rapid-milking robotics with inline sensors.

- January 2025: John Deere and DeLaval launched the Milk Sustainability Center to correlate crop nutrient data with cow performance for improved feed planning.

- January 2025: DeLaval introduced the Milking Automation MA Series with FlexiCommand controls for conventional parlours.

Global Automated Feeding Systems Market Report Scope

Automated feeding systems have emerged as vital instruments, enhancing efficiency, minimizing waste, and streamlining the supply of animal feed. Leveraging advanced technology, these systems dispense exact feed quantities at predetermined times. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Automated Feeding Systems Market is segmented by type (Conveyor Feeding Systems, Rail-Guided Feeding Systems and Self-Propelled Feeding Systems), by livestock (Ruminants, Swine, Poultry and Others), by technology (Robotics & Telemetry, Guidance and Remote Sensing Technology, RFID Technology and Other Technologies) and by geography (North America, Europe, Asia Pacific, South America and Middle East & Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Conveyor Feeding Systems |

| Rail-Guided Feeding Systems |

| Self-Propelled Feeding Systems |

| Total Mixed Ration (TMR) Feeding Systems |

| Batch vs Continuous Feeding Lines |

| Ruminants |

| Swine |

| Poultry |

| Aquaculture |

| Others |

| Robotics and Telemetry |

| Guidance and Remote-Sensing |

| RFID and IoT Tracking |

| Machine-Vision and AI Analytics |

| Small (≤100 head) |

| Medium (101-500 head) |

| Large (>500 head) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Conveyor Feeding Systems | ||

| Rail-Guided Feeding Systems | |||

| Self-Propelled Feeding Systems | |||

| Total Mixed Ration (TMR) Feeding Systems | |||

| Batch vs Continuous Feeding Lines | |||

| By Livestock | Ruminants | ||

| Swine | |||

| Poultry | |||

| Aquaculture | |||

| Others | |||

| By Technology | Robotics and Telemetry | ||

| Guidance and Remote-Sensing | |||

| RFID and IoT Tracking | |||

| Machine-Vision and AI Analytics | |||

| By Farm Size | Small (≤100 head) | ||

| Medium (101-500 head) | |||

| Large (>500 head) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the size of the automated feeding systems market in 2026?

The market was valued at USD 7.22 billion in 2026.

How fast is the automated feeding systems market expected to grow?

It is projected to rise at an 8.12% CAGR, reaching USD 10.66 billion by 2031.

Which product category is growing the fastest?

Self-propelled feeding robots are forecast to expand at an 10.78% CAGR to 2031.

Why are small farms adopting automation more quickly now?

Modular retrofit kits priced under USD 50,000 and higher labor costs have made automation economically viable even for herds of ≤100 head.

Which region offers the highest growth potential?

Asia-Pacific leads with a projected 9.34% CAGR because of rising protein demand and government technology subsidies.

What is the main barrier to wider adoption?

High upfront capital that can exceed USD 150,000 per installation and long 7-12 year payback periods remain the principal hurdles.

Page last updated on: