Autoclaved Aerated Concrete (AAC) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

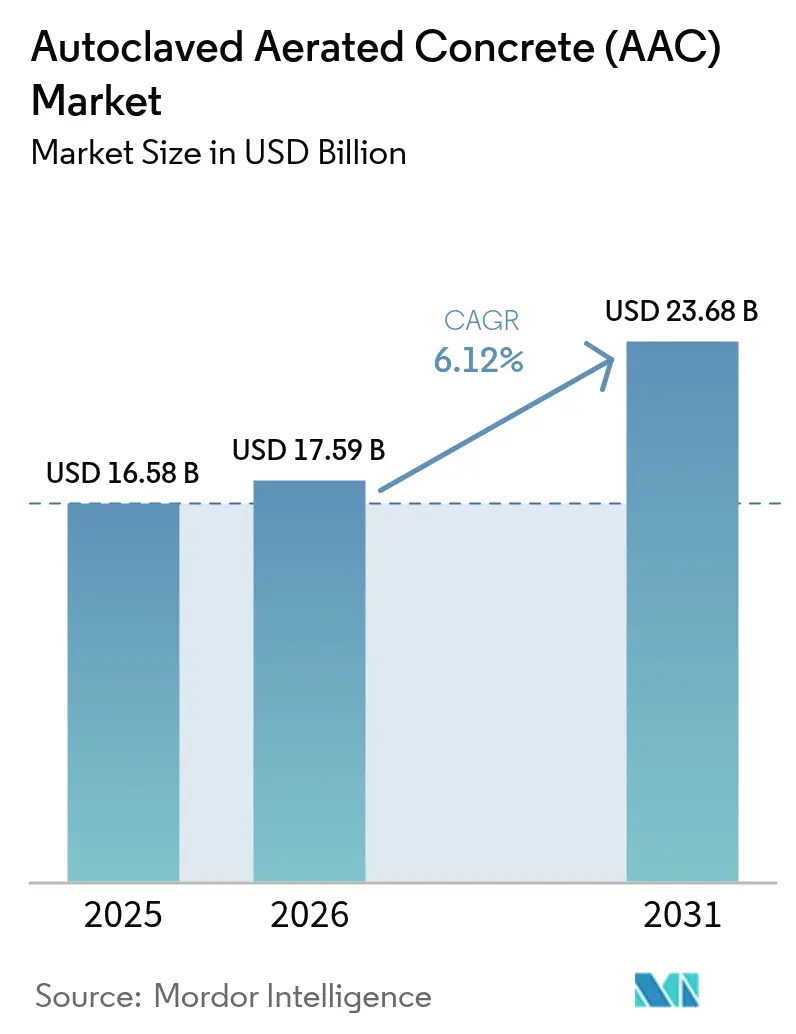

| Market Size (2026) | USD 17.59 Billion |

| Market Size (2031) | USD 23.68 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autoclaved Aerated Concrete (AAC) Market Analysis by Mordor Intelligence

The Autoclaved Aerated Concrete Market size is projected to be USD 16.58 billion in 2025, USD 17.59 billion in 2026, and reach USD 23.68 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031. Multiple public-procurement rules now reward low-embodied-carbon products, tilting specifications toward factory-cured mineral systems and away from kiln-fired clay or dense concrete masonry. Asia-Pacific’s dominance reflects urbanization, seismic code updates, and government-funded affordable-housing pipelines that favor lightweight walls able to cut foundation loads and speed construction. Europe’s renovation mandates and North America’s low-carbon procurement programs reinforce demand for insulating AAC panels that meet Energy Performance Certificate C ratings in a single lift. Capacity additions in China, India, Romania, and the United States illustrate how the Autoclaved aerated concrete market is scaling to serve prefabrication yards that require millimeter-level panel tolerances and just-in-time logistics.

Key Report Takeaways

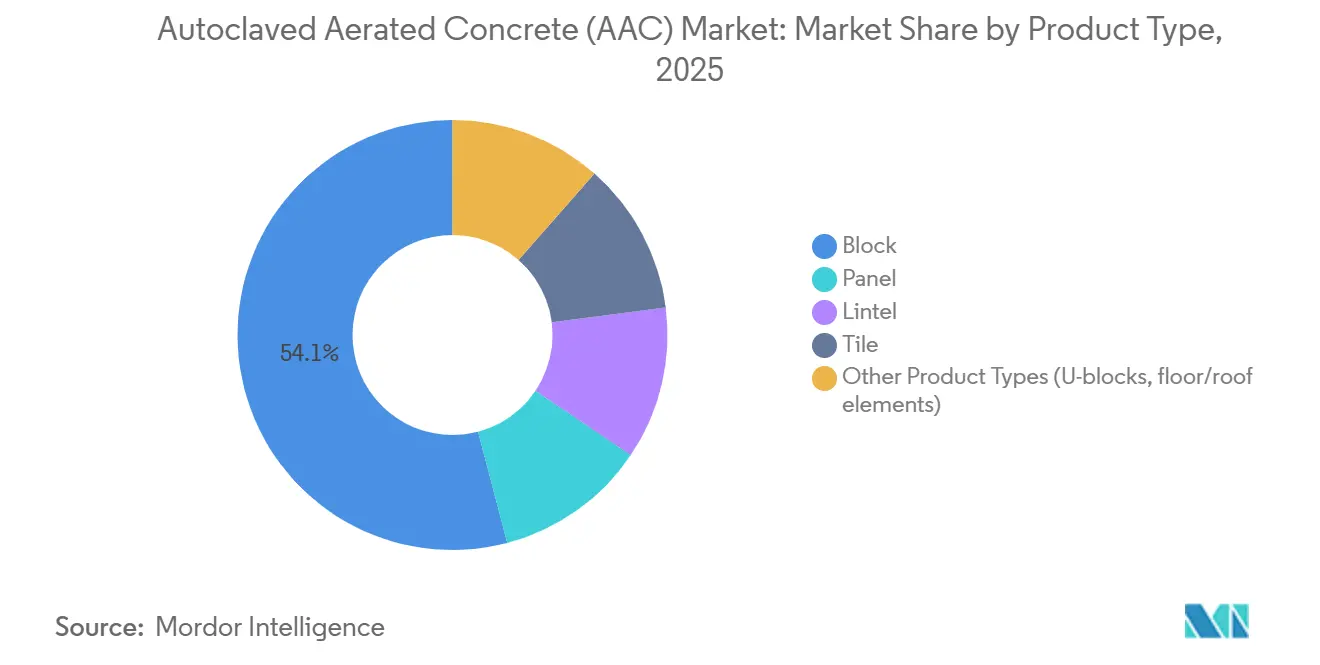

- By product type, block captured 54.10% of 2025 revenue, while panels are projected to expand at a 7.55% CAGR through 2031.

- By construction method, on-site masonry held 79.20% of the 2025 Autoclaved aerated concrete market share, whereas prefabricated/modular methods are forecast to grow at an 8.31% CAGR through 2031.

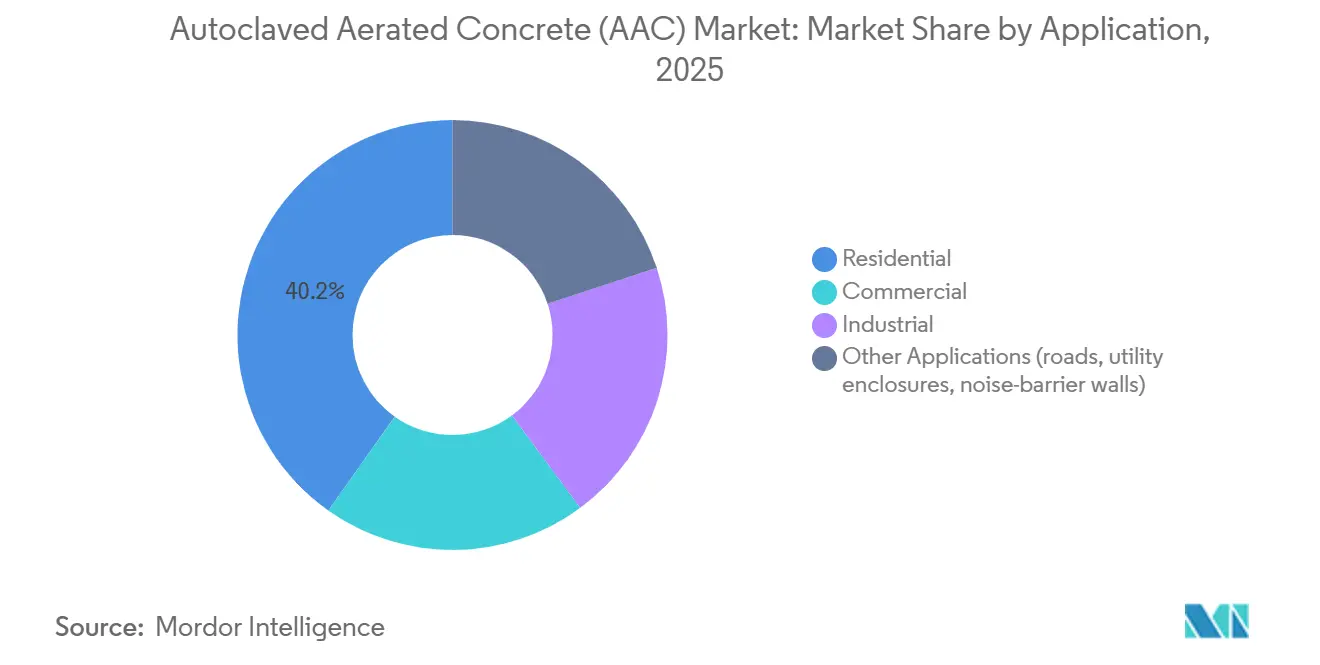

- By application, residential accounted for 40.20% of 2025 revenue and is advancing at a 6.63% CAGR through 2031.

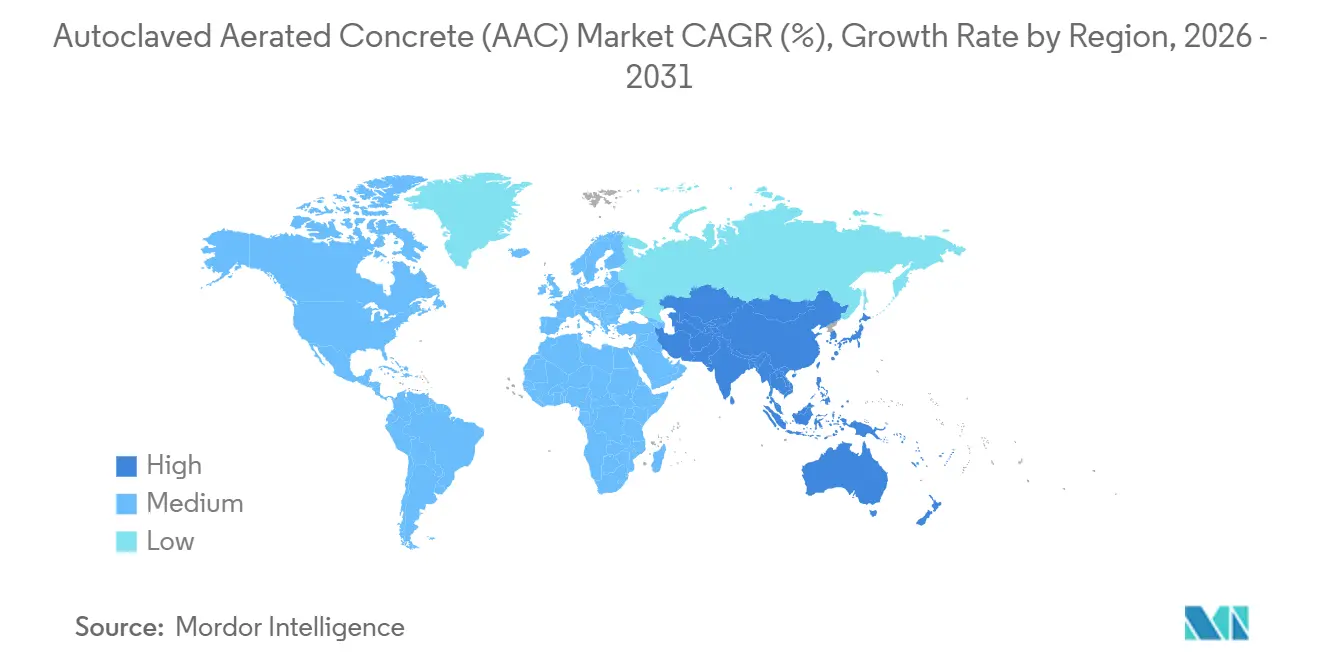

- By geography, Asia-Pacific led with 46.40% of 2025 revenue and is poised to grow at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autoclaved Aerated Concrete (AAC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from new-build and renovation construction | +1.8% | Global, with concentration in Asia-Pacific (China, India, ASEAN) and Europe (Germany, France, Netherlands) | Medium term (2-4 years) |

| Stringent green-building codes and LEED adoption | +1.5% | North America, Europe, APAC core markets (Japan, South Korea, Singapore) | Short term (≤ 2 years) |

| Government incentives for low-carbon materials | +1.3% | North America (USA, Canada), Europe (EU member states), spill-over to MEA | Medium term (2-4 years) |

| Modular off-site construction uptake | +1.1% | North America, Europe, APAC (Japan, Australia) | Long term (≥ 4 years) |

| Demand for seismic-resilient lightweight blocks | +0.9% | APAC (Japan, Indonesia, Philippines), North America (California, Pacific Northwest) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from New-Build and Renovation Construction

Urban housing shortages and mandatory energy-efficiency retrofits are simultaneously expanding new-build pipelines and refurbishment budgets. India targets 25 million affordable units by 2031, while China funded USD 1.4 trillion in 2024 construction outlays. The European Renovation Wave aims to upgrade 35 million buildings by 2030, channeling orders toward insulating AAC envelopes. ISO 16745 whole-life-carbon assessment is becoming a default tender requirement, meaning bids increasingly weigh embodied-carbon disclosures alongside first cost. Large panel-fabrication lines able to deliver cut-to-size elements in days are best positioned to win renovation work that demands schedule compression. Consequently, the Autoclaved aerated concrete market is shifting capital toward automated plants with higher panel output.

Stringent Green-Building Codes and LEED Adoption

Low-carbon clauses in the U.S. Inflation Reduction Act, Canada’s Green Buildings Strategy, and the EU’s Energy Performance of Buildings Directive require Environmental Product Declarations for public works[1]Government of Canada, “2030 Green Buildings Strategy,” canada.ca . LEED v4.1 and analogous Indian Green Building Council criteria reward materials with verified emissions profiles. Suppliers that cannot furnish third-party EPDs risk exclusion from high-value public and commercial bids. Certified producers therefore command price premiums of 5%-8%, reinforcing a two-tier Autoclaved aerated concrete market in which uncertified blocks compete mainly in price-sensitive housing.

Government Incentives for Low-Carbon Materials

Grants under the U.S. EPA’s C-MORE program cover up to 50% of incremental costs for low-carbon products purchased by federal projects. The United Kingdom’s Buy Clean initiative and Ireland’s IGBC rules similarly preference low-embodied-carbon wall systems. These policies create predictable, multi-year offtake volumes that justify new autoclaving lines and localized raw-material quarries. Tier 1 manufacturers are expanding capacity to secure these contracts, while smaller firms without public-sector access face scale disadvantages in the Autoclaved aerated concrete market.

Modular Off-Site Construction Uptake

Labor scarcity and schedule-reliability pressures are accelerating factory-built construction that can trim on-site labor by 30%-40%. AAC panels arrive pre-finished with utility chases, aligning with the takt-time discipline of modern production lines. DVI Production opened Europe’s largest AAC panel plant in Romania in 2025 to supply modular builders across Central Europe. If wall-panel suppliers fail to meet the precision and just-in-sequence delivery demands of automated yards, developers may backward-integrate, compressing margins across the Autoclaved aerated concrete market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost vs. clay and concrete blocks | -1.2% | Global, with acute impact in South Asia, Sub-Saharan Africa, and Latin America | Short term (≤ 2 years) |

| Structural limitations in load-bearing applications | -0.7% | Global, with regulatory tightening in Europe (UK, Ireland) and APAC (Singapore, Japan) | Medium term (2-4 years) |

| Volatile supply and price of aluminum powder foaming agent | -0.5% | Global, with supply concentration in China, India, and Middle-East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Clay and Concrete Blocks

AAC commands a 20%-30% price premium over conventional masonry, a hurdle for budget-constrained housing. Lifecycle savings from reduced mortar and quicker erection rarely sway developers targeting immediate cash flow. Public-sector subsidies like EPA C-MORE offset only institutional projects, leaving private residential builders to favor cheaper brick. Until incentives expand, cost sensitivity will cap residential penetration in the Autoclaved aerated concrete market.

Structural Limitations in Load-Bearing Applications

AAC’s compressive strength of 3-5 MPa restricts unreinforced walls to four-story structures. The United Kingdom’s RAAC school-closure emergency underscored durability concerns when reinforcement corrodes[2]Government of the United Kingdom, “Reinforced Autoclaved Aerated Concrete Guidance,” gov.uk . Singapore now mandates pre-consultation for structural RAAC, while ACI 526R-19 demands steel spreader plates under point loads. Such scrutiny confines AAC to infill unless detailed engineering support is provided, limiting high-rise adoption in the Autoclaved aerated concrete market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Panels Accelerate on Precision and Speed

Blocks generated 54.10% of 2025 revenue, yet panels are forecast to grow at 7.55% through 2031, representing the fastest rising slice of the Autoclaved aerated concrete market size. Aircrete Europe and Yuanzhu’s 500,000 m³ annual plant embodies the automation required to hit ±2 mm tolerances demanded by prefab yards. In markets where labor costs outstrip material premiums, contractors prefer ready-to-install panels that shorten wall cycles by two days per floor. The block segment still underpins rural and low-budget projects because it relies on low-skill labor and readily available small-batch mortar. Lintels and specialty elements capture niche demand for thermal-bridge-free openings and fire-rated floor plates, but they lack the volume to move the overall Autoclaved aerated concrete market.

The differential growth path means block-only producers risk stagnation unless they retrofit factories with tilt-cake cutters and reinforcement cages. Such upgrades can lift capital intensity by USD 8-10 million per line, which smaller regional players struggle to finance. Panel producers meanwhile lock in multiyear offtake contracts with modular builders, stabilizing factory utilization at 85%-90%. As more public tenders specify whole-wall U-values rather than R-values per course, integrated panels that combine structure, insulation, and finish gain competitive traction inside the Autoclaved aerated concrete market.

By Construction Method: Prefabrication Gains Momentum Despite Masonry Dominance

On-site masonry held 79.20% of 2025 revenue, illustrating AAC’s historical role as a drop-in brick substitute. Prefabricated and modular is projected to rise at 8.31% CAGR through 2031. Factory assembly slashes weather downtime and rework, curbing total installed cost even when material premiums persist. Large U.S. yard operators integrate AAC panels with steel frames to deliver hurricane-resistant hotel rooms; Asian developers use panels in school dormitories to reduce project schedules by 30%.

Yet masonry will not disappear overnight. Availability of low-cost labor in India and Sub-Saharan Africa sustains block demand, and contractors there lack digital modeling skills to sequence panel deliveries. The transition is likely to follow a tipping pattern: once modular commands 15%-20% of yearly starts, distributors retool around panel logistics, accelerating the pivot. Suppliers that bridge both channels—offering blocks for infill and panels for prefab—can hedge demand swings, a strategic hedge increasingly visible in the Autoclaved aerated concrete market.

By Application: Residential Provides Volume, Commercial Delivers Margin

Residential contributed 40.20% of 2025 revenue and will advance at a 6.63% CAGR. Affordable-housing drives unit volume, such as India’s Pradhan Mantri Awas Yojana, where lightweight AAC cuts footing costs by 10% and meets thermal mandates without cavity insulation. Commercial command higher price premiums because hotels and offices need 2-hour fire walls that AAC meets at half the thickness of dense concrete. Industrial warehouses adopt AAC to stabilize HVAC loads, especially in cold-chain logistics hubs.

In unit economics, residential orders keep kilns loaded year-round, giving scale economies that lower unit cost and defend share within the Autoclaved aerated concrete market size. Commercial wins, by contrast, fund R&D and panel-line upgrades because margins can exceed 20% EBIT when bundled with design-assist services. A balanced portfolio across housing, commercial, and industrial therefore maximizes both capacity utilization and profitability, a critical lesson for mid-tier players eyeing expansion inside the Autoclaved aerated concrete market.

Geography Analysis

Asia-Pacific generated 46.40% of 2025 revenue and is forecast to expand at 7.11% CAGR, reinforcing its role as the core growth engine of the Autoclaved aerated concrete market. India’s 60% urbanization target and China’s USD 1.4 trillion 2024 construction outlay prioritize lightweight walls that cut foundation loads. ASEAN’s adoption of seismic codes that limit wall mass further strengthens regional demand. Local giants such as Infra.Market now run nine AAC factories totaling 3 million m³ per year to serve tier-2 cities where clay brick shortages and rising labor costs make AAC blocks attractive.

Europe demand is fueled by the EU Renovation Wave that mandates upgrades for 35 million buildings by 2030. Germany, France, and the Netherlands retrofit aging masonry with AAC panels to hit EPC C ratings, while Romania’s DVI facility positions Central Europe for prefab uptake. The United Kingdom’s RAAC crisis creates mixed signals: unreinforced blocks gain share, but reinforced planks undergo heavier scrutiny, pressing suppliers to certify products under BS EN 12602.

North America contributes a smaller yet growing slice, hinging on state modular codes and embodied-carbon procurement. California, Washington, and New York lead in factory-built housing, while AAC East’s South Carolina expansion targets hurricane-prone coastal counties where the material’s impact and termite resistance add value. Canada’s 30% embodied-carbon reduction by 2030 boosts prospects, but clay-brick incumbents lobby aggressively, slowing momentum. South America and the Middle-East present nascent yet strategic options. Brazil’s São Paulo industrial corridor is investing in AAC for warehouse envelopes, whereas Saudi mega-projects like NEOM need fire-resistant, termite-proof walls for desert climates. Education of local contractors remains the gating factor in these emerging slices of the Autoclaved aerated concrete market.

Competitive Landscape

The Autoclaved aerated concrete market is fragmented: Xella International, H+H International, UltraTech Cement Ltd., ACICO Group, and Biltech Building Elements Ltd. together held roughly 54% of 2025 global revenue. Vertical integration into lime, cement, and aluminum powder allows these leaders to hedge input volatility and sustain 18%-22% gross margins. Regional specialists exploit localized logistics to offer two-day delivery in India, Indonesia, and Central Europe, compensating for smaller scale with speed.

Technology is the second battleground. Aircrete Europe’s In Control 4.0 system uses IoT sensors to maintain slice variation below 1 mm, enabling glued-joint installation without site trimming. DVI Production and Holcim Romania are adopting similar automation to meet prefab tolerances and reduce waste by 5%-7%. Integrated cement majors such as UltraTech and Holcim leverage distribution heft to cross-sell AAC blocks alongside bagged cement, squeezing stand-alone producers on channel access.

Reputational risk is rising after the U.K. RAAC school-plank failures. Suppliers now publish 50-year warranties and accelerated-aging test data to reassure specifiers, adding certification overhead that favors well-capitalized firms. Precontech’s lower-cost non-autoclaved technology could disrupt by slashing capex two-thirds, but its lower compressive strength limits initial reach to non-load-bearing walls. The outcome is an Autoclaved aerated concrete market where scale, certification, and automation determine long-run survivability.

Autoclaved Aerated Concrete (AAC) Industry Leaders

Xella International

ACICO Group

H+H UK Limited

UltraTech Cement Ltd.

Biltech Building Elements Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BirlaNu Limited commenced commercial production of Autoclaved Aerated Concrete (AAC) blocks at its Chennai plant through a new production line, effectively increasing its capacity to address rising regional demand. The new production line (Line 2) added 211,700 cubic meters (m³) of capacity to the plant, raising the total AAC block capacity to 448,220 m³ from the previous 236,520 m³.

- April 2025: DVI Production inaugurated a EUR 40 million (approximately USD 43 million) autoclaved aerated concrete (AAC) plant in Iernut, Romania, with a production capacity of 2,000 m³ per day, making it the largest in Europe. The fully automated facility, operating under the Fortem brand, was designed to supply AAC blocks and panels to regional markets, with plans to include panel production capacity.

Global Autoclaved Aerated Concrete (AAC) Market Report Scope

Autoclaved aerated concrete (AAC) is an ultra-light concrete masonry product, weighing as little as one-fifth as much as ordinary concrete due to its distinct cellular structure featuring millions of tiny pockets of trapped air.

The autoclaved aerated concrete (AAC) market is segmented by product type, constuction method, application, and geography. By product type, the market is segmented into block, panel, lintel, tile, and other product types (U-blocks, floor/roof elements). By construction method, the market is segmented into on-site masonry and prefabricated/modular. By application, the market is segmented into residential, commercial, industrial, and other applications (roads, utility enclosures, noise-barrier walls). The report also covers the market size and forecasts for autoclaved aerated concrete (AAC) in 23 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Block |

| Panel |

| Lintel |

| Tile |

| Other Product Types (U-blocks, floor/roof elements) |

| On-site masonry |

| Prefabricated/Modular |

| Residential |

| Commercial |

| Industrial |

| Other Applications (roads, utility enclosures, noise-barrier walls) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Poland | |

| Netherlands | |

| Romania | |

| Czech Republic | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Israel | |

| Qatar | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Block | |

| Panel | ||

| Lintel | ||

| Tile | ||

| Other Product Types (U-blocks, floor/roof elements) | ||

| By Construction Method | On-site masonry | |

| Prefabricated/Modular | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| Other Applications (roads, utility enclosures, noise-barrier walls) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Poland | ||

| Netherlands | ||

| Romania | ||

| Czech Republic | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Israel | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for the Autoclaved aerated concrete market in 2031?

The market is projected to reach USD 23.68 billion by 2031.

How fast is the Autoclaved aerated concrete market expected to grow between 2026 and 2031?

It is forecast to register a 6.12% CAGR over the period.

Which region is expanding the fastest in Autoclaved aerated concrete adoption?

Asia-Pacific is growing at a 7.11% CAGR, the highest among regions.

Why are AAC panels gaining share over blocks?

Panels arrive factory-cut, reduce wet trades, and align with modular construction, enabling a 7.55% CAGR compared with blocks.

Page last updated on: