Microporous Insulation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 358.84 Million |

| Market Size (2031) | USD 432.61 Million |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microporous Insulation Market Analysis by Mordor Intelligence

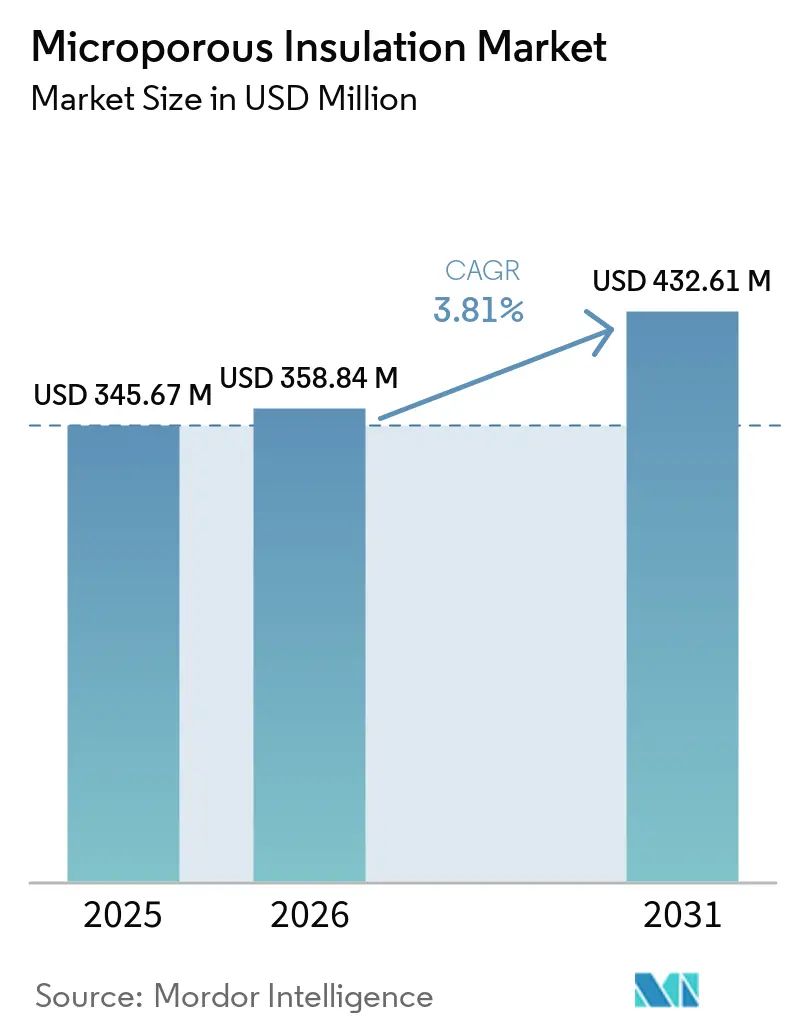

The Microporous Insulation Market size is projected to expand from USD 345.67 million in 2025 and USD 358.84 million in 2026 to USD 432.61 million by 2031, registering a CAGR of 3.81% between 2026 to 2031. Aerogel-based products are being adopted in cryogenic and aerospace applications due to their ability to achieve thermal conductivity below 0.02 watts per meter-kelvin (W/m·K) while reducing installed weight by over 20%. This combination supports lower fuel consumption in aircraft and reduced energy losses in the hydrogen infrastructure. Silica-based grades, expected to account for 44.66% of revenue in 2025, are now competing with ceramic-aerogel composites capable of withstanding operating temperatures above 1,200°C without phase-change degradation. Form-factor preferences are shifting toward flexible blankets, as offshore oil platforms, LNG vessels, and equipment with irregular geometries prioritize ease of installation and adaptability over rigid mechanical strength. Global safety and emission regulations, such as the EPA SOCMI rules in the United States and amendments to the EU Industrial Emissions Directive, are driving petrochemical operators to retrofit high-temperature furnaces with insulation that reduces heat loss and stack-gas intensity. Additionally, the development of green hydrogen terminals in the Asia-Pacific region is driving demand for ultra-low-conductivity panels designed to maintain liquid hydrogen boil-off rates below 0.05% per day.

Key Report Takeaways

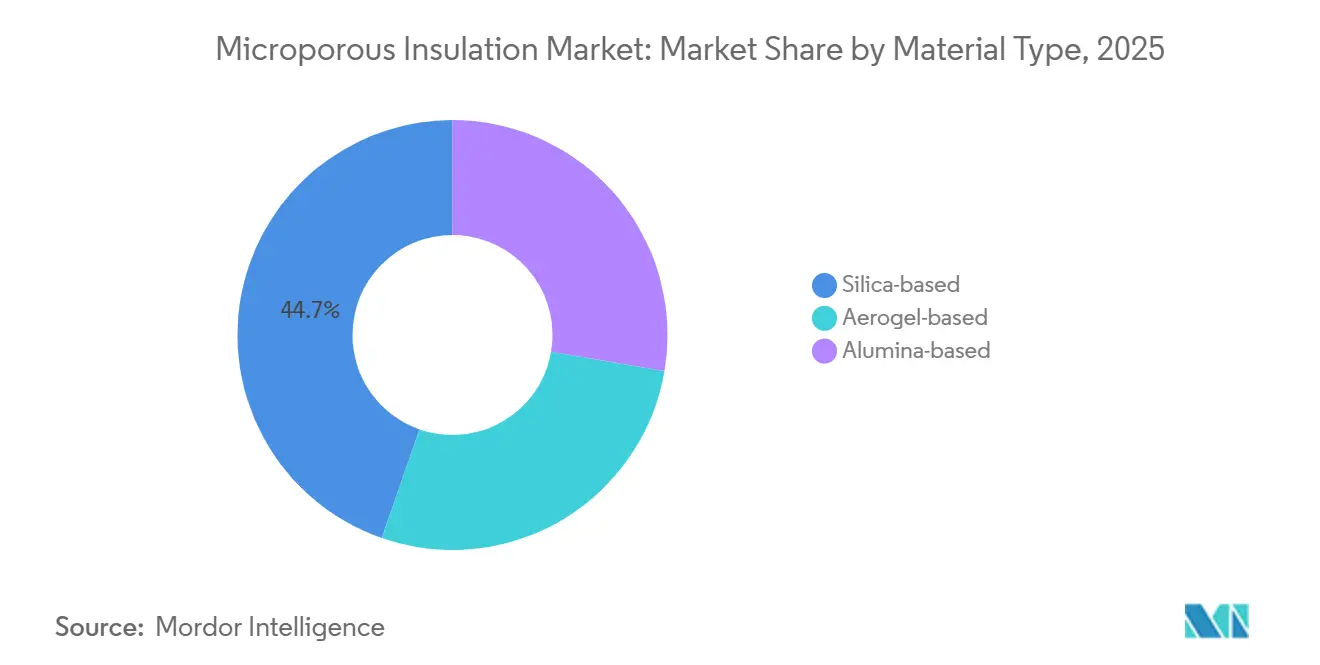

- By material type, silica-based grades led with 44.66% of the microporous insulation market share in 2025. Aerogel-based products are forecast to record the fastest 4.68% CAGR through 2031 within the microporous insulation market size.

- By form factor, panels and boards contributed 41.13% of the microporous insulation market share in 2025, while blankets and flexible mats are projected to rise at a 4.25% CAGR to 2031.

- By operating temperature range, the 600-1,000 °C band captured 45.66% of the microporous insulation market size in 2025, yet the above-1,000 °C range will advance at a 4.11% CAGR through 2031.

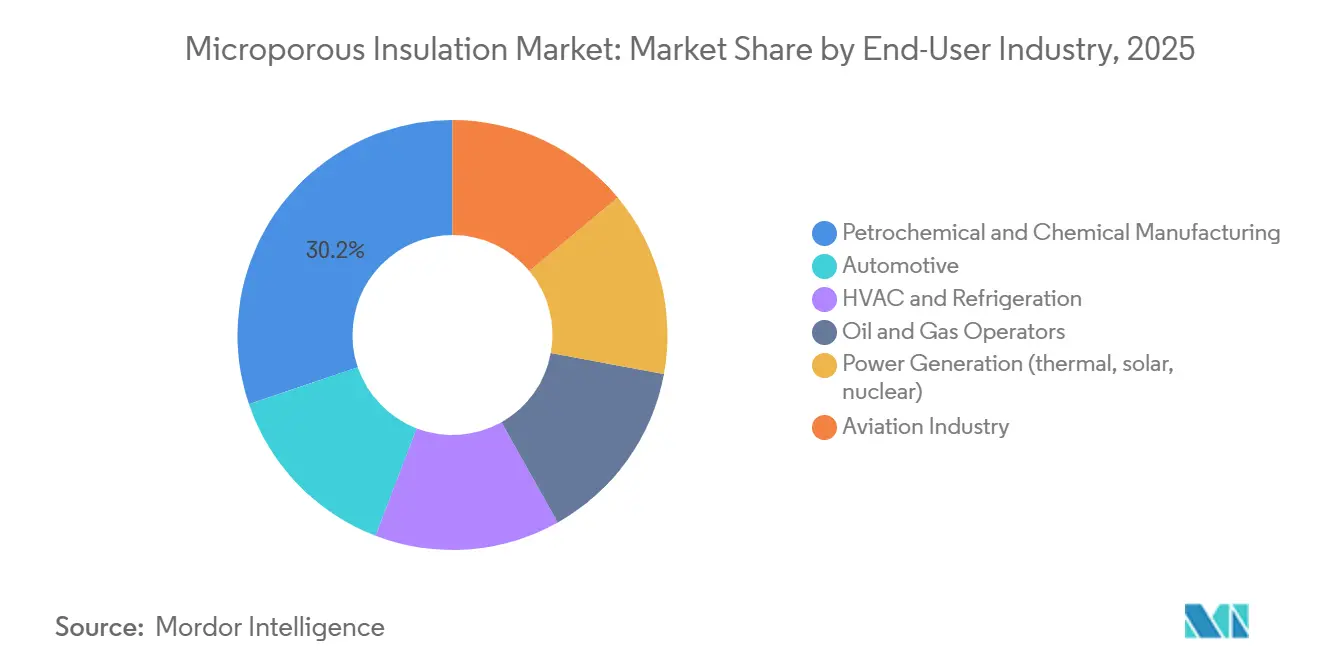

- By end-user industry, petrochemical and chemical manufacturing represented 30.22% of the microporous insulation market share in 2025, whereas the aviation industry poised for the highest 4.83% CAGR by 2031.

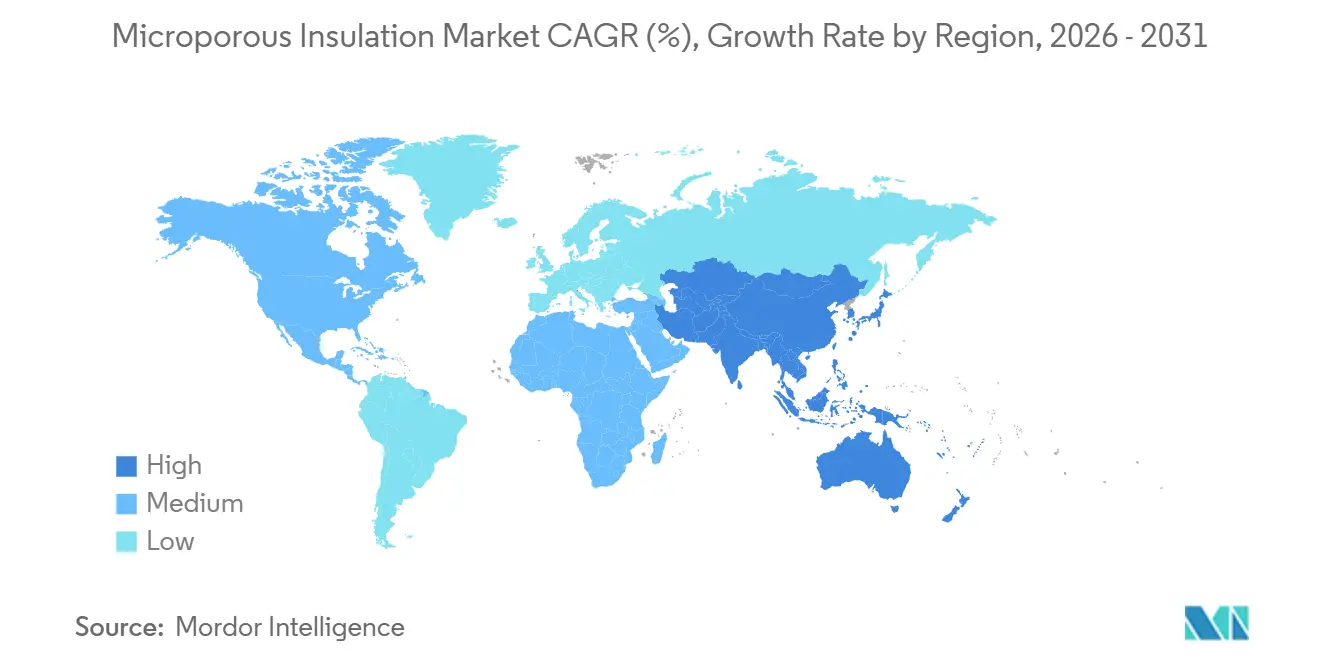

- By geography, Asia-Pacific held 42.21% of the microporous insulation market size in 2025 and is forecast to compound at 4.23% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microporous Insulation Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight and space-saving demand in aerospace and O&G | +0.9% | North America & EU, spill-over to Middle East offshore fields | Medium term (2–4 years) |

| Energy-efficient cryogenic and LNG infrastructure build-out | +1.2% | APAC core (China, India), secondary growth in Middle East | Long term (≥4 years) |

| Stricter safety and emission regulations | +0.7% | Global, led by North America & EU | Short term (≤2 years) |

| Hydrogen-liquefaction and LH₂ bunkering projects | +0.6% | APAC (Japan, South Korea, India), EU pilot corridors | Long term (≥4 years) |

| Thermal-runaway barriers for solid-state battery gigafactories | +0.5% | APAC manufacturing hubs, North America EV supply chain | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lightweight and Space-Saving Demand in Aerospace and O&G

Offshore platforms and wide-body aircraft operate under strict weight constraints, where every additional kilogram impacts operating costs. AIS Group’s ContraFlame MS200 microporous belly pan, used in Qatar’s Ruya project, reduced 488 tons of steel compared to traditional mineral wool while meeting a thermal envelope requirement of 0.25 W/(m²·K)[1]AIS Group, “ContraFlame MS200 Ruya Project,” aisgroup.co.uk. Aspen Aerogels’ Cryogel Z blankets reduced LNG pipe outer diameters by 24%, lowering structural steel usage by 1.83 tons per meter and reducing installation schedules by 30%. The FAA’s 14 CFR 25.856 regulation requires nacelle thermal barriers to resist flame penetration for four minutes, prompting airlines to replace fiberglass mats with silica-aerogel blankets, reducing nacelle weight by 12-18 kg. Subsea gas pipelines are adopting aerogel-filled pipe-in-pipe systems capable of withstanding 150-bar hydrostatic pressure over 40-km tiebacks without compressive collapse, extending economic reach. Twin-aisle aircraft programs estimate fuel savings at approximately USD 3,000 per kilogram of weight reduction over the aircraft’s lifespan, highlighting the cost benefits of advanced insulation solutions.

Energy-Efficient Cryogenic and LNG Infrastructure Build-Out

New liquefied natural gas (LNG) regasification terminals are projected to add 50 million tons per annum (tpa) by 2025, with two-thirds of this capacity located in China and India. Each site is implementing vacuum-jacketed or microporous systems designed to limit boil-off rates to below 0.05% per day[2]International Gas Union, “2025 LNG Additions Report,” igu.org. In India, the Petroleum and Natural Gas Regulatory Board (PNGRB) has issued a 2025 blending roadmap mandating insulation with thermal conductivity below 0.03 W/m·K under cryogenic conditions to address hydrogen-induced steel embrittlement. Meanwhile, Japan’s Ministry of Economy, Trade and Industry (METI) has allocated JPY 37 billion (USD 250 million) in 2026 for liquid hydrogen (LH₂) import terminals in Kobe and Yokohama, which will utilize variable-density multilayer insulation capable of achieving 0.001 W/m·K under high vacuum. Hyundai Heavy Industries has developed a 20,000-m³ LH₂ carrier prototype that reduces boil-off to 0.15% by using aerogel powder to fill annular gaps. Additionally, Middle Eastern fertilizer plants adopting ammonia cracking technologies are now specifying flexible microporous blankets that prevent liquid-ammonia permeation while adapting to the shape of spherical tanks.

Stricter Safety and Emission Regulations

The Environmental Protection Agency's (EPA) updated Synthetic Organic Chemical Manufacturing Industry (SOCMI) and Polymers National Emission Standards for Hazardous Air Pollutants (NESHAP), effective January 2024, reduces ethylene oxide fenceline limits to 0.2 parts per million (ppm), requiring petrochemical furnaces to retrofit insulation to lower surface temperatures and reduce leak potential. The European Union (EU) Industrial Emissions Directive revision mandates an 8% reduction in energy intensity for refineries by 2028, compared to 2020 baselines, driving the adoption of less than or equal to 0.025 W/m·K panels rated for 600°C. In the United States, the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 90.1-2022 and 15-2022 codes impose stricter R-value requirements for commercial duct insulation, encouraging HVAC retrofits to use aerogel mats capable of achieving R-30 with a 25 mm thickness. Meanwhile, China's 2025 ultra-low nitrogen oxides (NOₓ) standard limits gas boiler emissions to 30 milligrams per cubic meter (mg/m³), necessitating the maintenance of combustion-chamber temperatures above 1,200°C through the use of high-temperature microporous linings. Collectively, these regulatory measures position compliance as a significant driver of growth in the microporous insulation market .

Hydrogen-Liquefaction and LH₂ Bunkering Projects

Hydrogen liquefaction consumes up to 35% of the fuel's lower heating value, making insulation performance a significant cost factor. India's National Green Hydrogen Mission, funded with Indian Rupees (INR) 4,440 crore (USD 530 million) by 2026, mandates cryogenic storage with thermal conductivity below 0.005 W/m·K to minimize re-liquefaction losses. Fukushima's 5-tons-per-day (tpd) liquid hydrogen (LH₂) pilot plant utilizes aerogel-clad transfer lines, reducing boil-off rates to 0.08% per day compared to perlite-based systems. Hyundai Rotem and Korea Gas Corporation (KOGAS) are testing rail tankers capable of maintaining -250 °C for 72 hours without active refrigeration, using multilayer aerogel composites. In Germany, the Federal Ministry for Economic Affairs and Climate Action (BMWK) has allocated EUR 120 million by 2025 for LH₂ terminals requiring microporous insulation with thermal conductivity of less than or equal to 0.005 W/m·K. Additionally, maritime bunkering vessels now employ powder-filled jackets designed to withstand thermal cycling between -253°C and ambient temperatures during port operations without cracking.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability issues under severe thermal cycling | -0.4% | Global, acute in cyclic-furnace applications | Medium term (2–4 years) |

| Raw-material price volatility (fumed silica, opacifiers) | -0.5% | Global supply chain, Asia manufacturing clusters | Short term (≤2 years) |

| End-of-life recycling complexity and landfill restrictions | -0.3% | EU regulatory zone, emerging in North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Durability Issues Under Severe Thermal Cycling

ASTM C1171 and C1512 tests indicate that silica-based boards can lose up to 15% of their compressive strength after 50 thermal cycles between 200°C and 800°C. This has led glass and ceramics plants to transition toward alumina composites, which offer higher fracture toughness. Hydrothermal aging tests conducted per ASTM C1303 reveal a moisture uptake of 8% by weight, resulting in a decline in thermal conductivity from 0.020 to 0.035 watts per meter-kelvin (W/m·K) and reducing life expectancy by 30%. Cryogenic blankets are susceptible to micro-cracking at temperatures below -200°C, an issue partially addressed by the use of flexible binders, though these binders increase thermal conductivity by 10-15%. In nuclear reactors governed by the American Society of Mechanical Engineers (ASME) Section III, radiation stability requirements of up to 1 megagray (MGy) over 40 years exclude many products with organic binders. These mechanical and environmental stresses limit adoption in applications involving cyclic or high-radiation conditions.

Raw-Material Price Volatility

Fumed silica spot prices ranged between USD 5,000 and 6,000 per ton during 2025-2026, following production disruptions at Cabot and Evonik facilities, which together account for 40% of global hydrophobic capacity. Zirconium-silicate opacifier prices increased by 18% in Q1 2026 due to reduced African ilmenite exports, leading to a compression of gross margins by 200-300 basis points. Prices for Methyltrimethoxysilane (MTMS) and Tetraethyl Orthosilicate (TEOS) silane precursors rose by 22% year-over-year in 2025, driven by European natural gas curtailments, which particularly impacted producers lacking long-term contracts. Currency depreciation further increased cost pressures, with a 10% decline in the yuan raising landed European costs by 8-12%. Bio-silica derived from rice-husk ash remains at a pilot scale, with production below 2,000 tons per annum and a 40% price premium over petrochemical alternatives, providing no immediate cost relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aerogel Variants Gain Traction in Cryogenic Niches

Aerogel grades recorded a 4.68% compound annual growth rate (CAGR) in the microporous insulation market size between 2026 and 2031, driven by demand from hydrogen-liquefaction plants for sub-0.02 W/m·K thermal performance and 20% weight reduction. Silica-based materials accounted for 44.66% of 2025 revenue, supported by a cost structure of USD 8-12 per square meter and established supply chains. Alumina-based panels, designed for refractory linings requiring compressive strengths above 2 megapascals (MPa) and resistance to alkaline slag, commanded 40-60% price premiums, which specific clients accepted.

Industry focus is shifting towards ceramic aerogels, such as silicon nitride (Si₃N₄) and aluminum oxide-silicon dioxide (Al₂O₃-SiO₂) composites, which achieve thermal conductivity below 0.015 W/m·K at 1,200 degrees Celsius, offering potential applications in solar receivers and gas turbines. However, capacity constraints persist, with nameplate aerogel blanket production reaching approximately 50 million square meters in 2025. Key players, including Aspen Aerogels, Cabot-backed Yangu, and Armacell, accounted for nearly two-thirds of this output. Meanwhile, bio-silica pilot plants in Southeast Asia produced less than 2,000 tons per annum (tpa), falling short of commercial viability. Despite higher costs, the performance advantages of aerogels continue to support their market share growth in the Microporous Insulation Market through 2031.

By Form Factor: Blankets Advance on Installation Speed

Panels and boards represented 41.13% of the microporous insulation market share in 2025, supported by refinery retrofits and furnace walls requiring rigid, load-bearing capabilities. Blankets and flexible mats are expected to grow at a Compound Annual Growth Rate (CAGR) of 4.25%, driven by applications such as Liquefied Natural Gas (LNG) pipe wraps, subsea tiebacks, and aviation nacelles, where their conformability reduces field labor by 30% and decreases steel weight by 1.83 tons per pipe-meter. Tube sections used in Heating, Ventilation, and Air Conditioning (HVAC) systems benefit from factory-applied vapor barriers, which reduce onsite labor by 15-20%.

Powders and granules are used in vacuum-insulated panels and double-wall tanks, achieving thermal conductivity of 0.03 W/m·K under vacuum conditions but losing effectiveness at atmospheric pressure. Regulatory standards, such as the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 90.1-2022, are driving increased demand for blankets by mandating R-30 duct performance, which can be achieved with 25 mm aerogel layers instead of 75 mm elastomeric foams. However, end-of-life challenges remain: dispersed powders complicate recycling and increase abatement costs, while blankets and panels are more compatible with emerging take-back programs.

By Operating Temperature Range: Ultra-High-Temperature Segments Capture Petrochemical Upgrades

The 600-1,000 °C range accounted for 45.66% of the microporous insulation market size in 2025, primarily serving steam crackers and catalytic reformers, where panels with thermal conductivity of less than or equal to 0.025 watts per meter-kelvin (W/m·K) achieve economic feasibility. Applications above 1,000°C are projected to grow at a compound annual growth rate (CAGR) of 4.11%, driven by the use of alumina and ceramic aerogels to delay thermal propagation in solid-state battery production facilities and petrochemical debottlenecking projects.

Morgan Advanced Materials and Unifrax lead the market in applications exceeding 1,200°C, utilizing alumina-silica fibers that resist silica’s cristobalite phase transformation. The less than or equal to 600 °C segment supports liquefied natural gas (LNG) terminals and chilled-water pipelines, addressing heating, ventilation, and air conditioning (HVAC) retrofits with 0.02 W/m·K aerogel blankets that reduce heat influx by 30-40% compared to polyisocyanurate (polyiso) insulation. European Union (EU) and Chinese nitrogen oxides (NOₓ) regulations are driving demand for high-temperature durability, while American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) refrigeration safety updates sustain demand in the sub-600 °C segment.

By End-User Industry: Aviation Accelerates on Flammability Mandates

Petrochemical complexes are expected to account for 30.22% of the Microporous Insulation Market share in 2025, driven by ongoing furnace retrofits in compliance with stricter Environmental Protection Agency (EPA) regulations. The aviation segment is projected to achieve a compound annual growth rate (CAGR) of 4.83% through 2031, supported by Federal Aviation Administration (FAA) 14 Code of Federal Regulations (CFR) 25.856, which encourages the use of aerogel blankets to reduce flame penetration and aircraft weight. The automotive sector is also advancing, with manufacturers like Volvo and other original equipment manufacturers (OEMs) incorporating PyroThin and similar barriers into solid-state battery packs.

In the oil and gas industry, microporous belly pans are used to reduce topside weight, as demonstrated by the 488-ton weight reduction on Qatar’s Ruya Floating Production Storage and Offloading (FPSO) unit. Power-generation utilities are adopting ceramic composites for steam lines and molten-salt tanks to meet the 40-year compliance requirements of the American Society of Mechanical Engineers (ASME) Section III standards. The heating, ventilation, and air conditioning (HVAC) sector is seeing increased adoption of aerogel-lined ducts, driven by EPA refrigerant leak regulations effective in 2026, positioning aerogel as an alternative to foam-based solutions.

Geography Analysis

Asia-Pacific accounted for 42.21% of the microporous insulation market size in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 4.23% through 2031. Key factors include India’s INR 44,400 million (USD 472.90 million) green-hydrogen initiative, China’s CNY 5 billion (USD 0.72 billion) Chongqing aerogel project, and Japan’s JPY 37 billion (USD 0.23 billion) investment in liquid hydrogen (LH₂) terminals, collectively supporting demand for sub-0.005 W/m·K insulation solutions. In China, revenue from microporous blankets is expected to increase from CNY 7.15 billion (USD 1.03 billion) in 2026 to CNY 15.83 billion (USD 2.29 billion) by 2033, reflecting a CAGR of 12.02%. Companies such as Jiangsu Hanxin Tiancheng and Inner Mongolia Langying are contributing to this growth by adding 100,000 cubic meters of new production capacity.

North America and Europe demonstrate slower volume growth but maintain higher value density due to the adoption of specialty grades and compliance with stringent regulations. Germany’s EUR 120 million (USD 138.04 million) hydrogen-terminal grants, Environmental Protection Agency (EPA) Synthetic Organic Chemical Manufacturing Industry (SOCMI) compliance projects, and updates to American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) codes support premium pricing in these regions. Aspen Aerogels’ third-quarter 2026 subsea project win in the North Sea highlights the continued demand for high-performance insulation solutions, even as overall macro volume growth remains subdued.

South America and the Middle East-Africa regions contribute smaller market shares but exhibit growth in specific segments, particularly in oil-and-gas and renewable energy applications. Projects such as Saudi Arabia’s NEOM, the United Arab Emirates’ (UAE) hydrogen alliance, and Brazil’s pre-salt retrofits leverage aerogel systems to reduce offshore weight and enhance thermal efficiency. Additionally, South Africa’s organic Rankine cycle (ORC) pilot project integrates microporous insulation with waste-heat recovery systems, indicating the gradual adoption of this technology in coal-dependent energy grids.

Competitive Landscape

The microporous insulation market is moderately fragmented. Aspen Aerogels reported a revenue decline in Q4 2025 to USD 271.1 million following the demobilization of its Statesboro facility. The company shifted its focus toward the automotive sector and secured a contract for a North Sea pipeline. Additionally, it projects USD 450 million in electric vehicle (EV) sales by 2028. Chinese companies, including Cabot-backed Zhejiang Yangu and China Chemical with its 300,000 cubic meter Chongqing plant, are contributing to the commoditization of silica aerogels by leveraging domestic demand and cost-efficient scaling.

Established mineral-fiber manufacturers such as ROCKWOOL and Johns Manville are integrating stone wool with microporous cores to meet Underwriters Laboratories (UL) 94 V-0 and American Society for Testing and Materials (ASTM) E84 standards. BASF’s Slentite employs supercritical drying at its Ludwigshafen facility to achieve a thermal conductivity of 0.018 watts per meter-kelvin (W/m·K), while Saint-Gobain’s Quartzel fused silica is designed to meet the stringent requirements of semiconductor equipment. Morgan Advanced Materials and Unifrax maintain leadership in high-temperature applications exceeding 1,200°C with their Superwool and Kaowool ceramic fiber products.

Emerging technological opportunities focus on bio-based silica precursors, though pilot production costs remain 40% higher than petrochemical alternatives, and current capacities below 2,000 tons per annum (tpa) limit significant market impact before 2031. Patent activity in silicon-nitride aerogels indicates a potential competitive race for intellectual property protection in ultra-high-temperature applications. Overall, competitive dynamics are shaped by large-scale production capabilities in Asia and product differentiation strategies in Western specialty markets.

Microporous Insulation Industry Leaders

Morgan Advanced Materials plc

Alkegen

Etex Group

ARMACELL

Unicorn Insulations

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Aspen Aerogels has set a target of 20% revenue growth by 2026 and projected European EV thermal barrier sales, supported by microporous insulation technology, to reach USD 450 million by 2028, following the acquisition of a contract with Volvo.

- January 2026: India allocated INR 44,400 million (USD 472.90 million) under the National Green Hydrogen Mission to develop 3 GW of electrolyzers and produce 862,000 tons per year of green hydrogen, which is expected to increase the demand for microporous insulation in cryogenic applications

Global Microporous Insulation Market Report Scope

Microporous insulation is a material with low thermal conductivity, made from compacted inorganic powders, typically fumed silica, and opacifiers. It contains microscopic pores smaller than 2 nanometers (nm) and provides thermal resistance with minimal thickness and weight. It performs 4-5 times more effectively than conventional insulation at high temperatures ranging from 1000°C to 1200°C.

The microporous insulation market is segmented by material type, form factor, operating temperature range, end-user industry, and geography. By material type, the market is segmented into silica-based, aerogel-based, and alumina-based. By form factor, the market is segmented into panels and boards, tubes and pipe covers, blocks/sheets, blankets and flexible mats, and powder/granules. By operating temperature range, the market is segmented into up to 600°C, 600-000 °C, and above 1,000°C. By end-use industry, the market is segmented into automotive, petrochemical and chemical manufacturing, HVAC and refrigeration, oil and gas operators, power generation (thermal, solar, nuclear), and the aviation industry. The report also covers the market size and forecasts for microporous insulation in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Silica-based |

| Aerogel-based |

| Alumina-based |

| Panels and Boards |

| Tubes and Pipe Covers |

| Blocks / Sheets |

| Blankets and Flexible Mats |

| Powder / Granules |

| Up to 600 °C |

| 600 – 1 000 °C |

| Above 1 000 °C |

| Automotive |

| Petrochemical and Chemical Manufacturing |

| HVAC and Refrigeration |

| Oil and Gas Operators |

| Power Generation (thermal, solar, nuclear) |

| Aviation Industry |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Silica-based | |

| Aerogel-based | ||

| Alumina-based | ||

| By Form Factor | Panels and Boards | |

| Tubes and Pipe Covers | ||

| Blocks / Sheets | ||

| Blankets and Flexible Mats | ||

| Powder / Granules | ||

| By Operating Temperature Range | Up to 600 °C | |

| 600 – 1 000 °C | ||

| Above 1 000 °C | ||

| By End-user Industry | Automotive | |

| Petrochemical and Chemical Manufacturing | ||

| HVAC and Refrigeration | ||

| Oil and Gas Operators | ||

| Power Generation (thermal, solar, nuclear) | ||

| Aviation Industry | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will the Microporous Insulation Market grow between 2026 and 2031?

The Microporous Insulation Market size is projected to expand from USD 345.67 million in 2025 and USD 358.84 million in 2026 to USD 432.61 million by 2031, registering a CAGR of 3.81% between 2026 to 2031.

Which material will gain the most share by 2031?

Aerogel-based grades will post the quickest 4.68% CAGR as hydrogen and aerospace users favor sub-0.02 W/m·K performance.

What is the largest end-user segment today?

Petrochemical and chemical manufacturing held 30.22% of 2025 revenue due to furnace and reactor retrofits under stricter emission rules.

Why is the Asia-Pacific important for suppliers?

The region accounted for 42.21% of 2025 sales and continues at 4.23% CAGR, driven by China’s LNG build-out and India’s green-hydrogen push.

Page last updated on: