Hollow Concrete Block Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

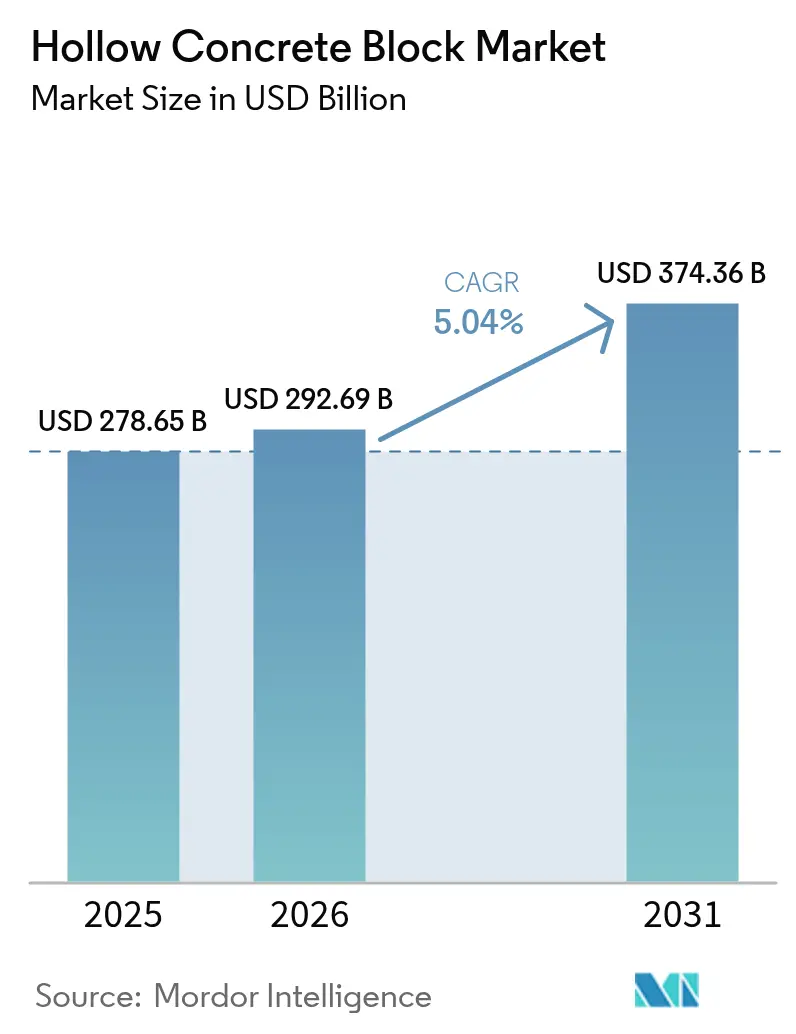

| Market Size (2026) | USD 292.69 Billion |

| Market Size (2031) | USD 374.36 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hollow Concrete Block Market Analysis by Mordor Intelligence

The Hollow Concrete Block Market size was valued at USD 278.65 billion in 2025 and estimated to grow from USD 292.69 billion in 2026 to reach USD 374.36 billion by 2031, at a CAGR of 5.04% during the forecast period (2026-2031). Urbanization pressures, affordable housing mandates, and infrastructure resilience programs create durable demand, while producers gain pricing power by aligning with green-building credits and modular construction trends. Asia-Pacific leads consumption due to large-scale Indian housing schemes and continued Chinese urban renewal. Split-faced blocks dominate global product adoption for their architectural appeal, yet smooth-faced and specialty formats retain relevance in functional walls and industrial layouts. Competitive momentum centers on vertical integration and low-carbon technologies as major cement groups acquire regional masonry assets and retrofit plants for carbon-capture readiness. Manufacturers able to supply high-volume traditional units and value-added eco-blocks are positioned to outperform.

Key Report Takeaways

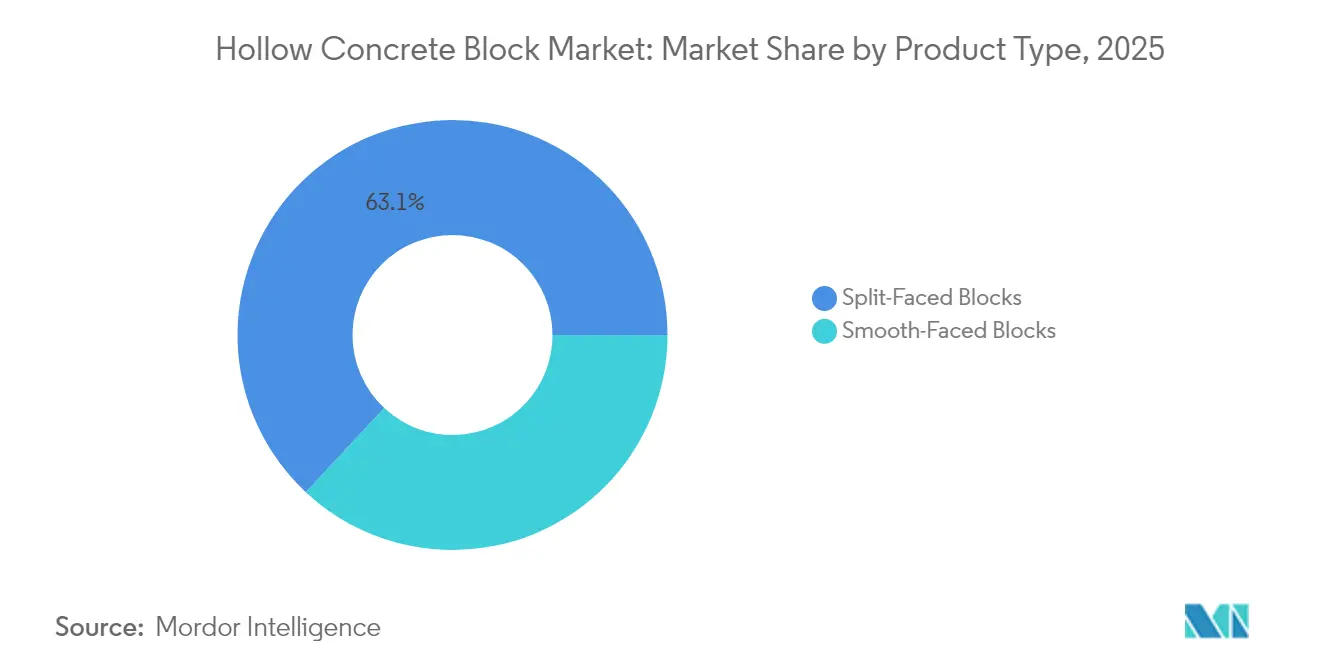

- By product type, split-faced blocks held 63.05% of the hollow concrete blocks market share in 2025 and are projected to expand at a 6.18% CAGR through 2031.

- By end-user industry, residential accounted for 46.62% share of the hollow concrete blocks market size in 2025, while other end-user industries are set to advance at a 6.06% CAGR to 2031.

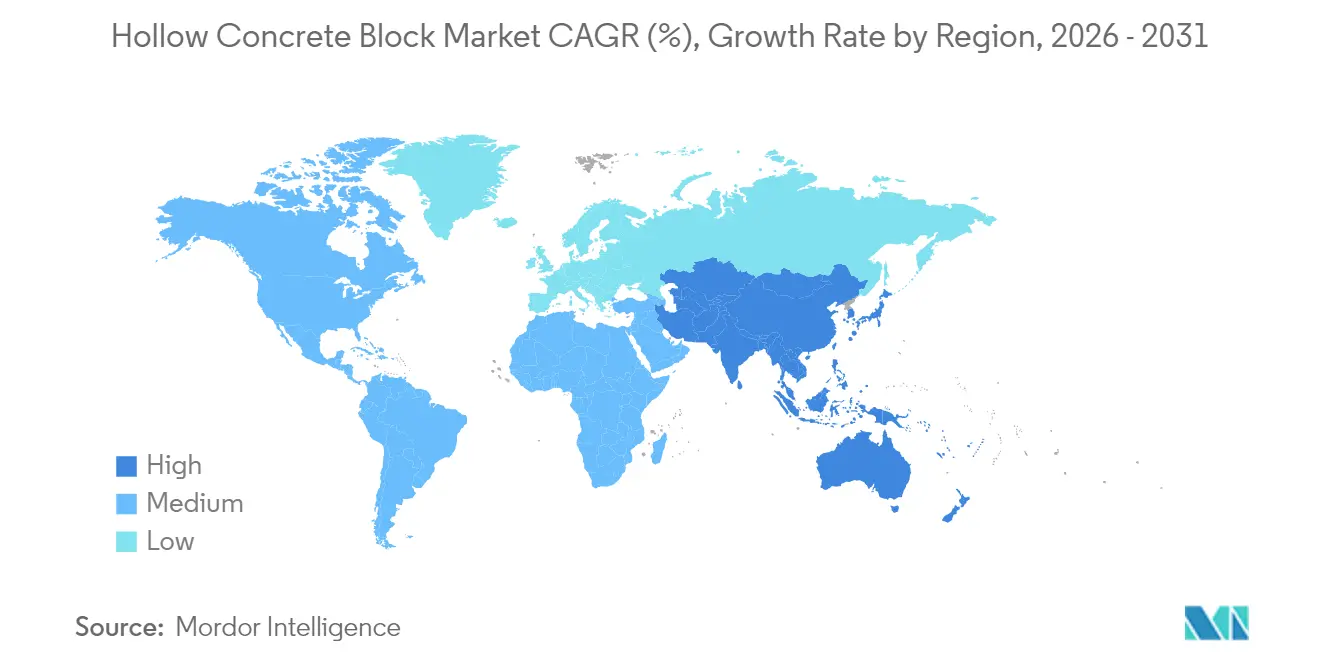

- By geography, Asia-Pacific commanded 46.05% revenue in 2025 and is poised to grow at a 5.93% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hollow Concrete Block Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation boosting affordable housing demand | +1.80% | Global, with concentration in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Surge in green-building certifications driving lightweight masonry | +1.20% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising labour costs prompting modular construction adoption | +0.90% | North America & Western Europe | Medium term (2-4 years) |

| Growth of disaster-resilient infrastructure programmes | +0.70% | Global, with priority in hurricane/earthquake zones | Long term (≥ 4 years) |

| Expansion of e-commerce warehouses & logistics hubs | +0.60% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization Boosting Affordable Housing Demand

National housing programs continue to set aggressive construction targets that favor concrete blocks for speed and cost efficiency. India’s Pradhan Mantri Awas Yojana has already sanctioned 118.64 lakh urban homes and 321 lakh rural units, with budget approvals for another 2 crore dwellings, sustaining a multi-year pipeline for hollow concrete blocks manufacturers. African governments replicate similar schemes, supported by new local cement plants that shorten supply chains and stabilize price volatility. Although Chinese cement output fell 10% year-on-year in 2024, urban renewal and provincial public-housing quotas preserve baseline block demand. These concurrent programs anchor long-duration growth for the hollow concrete blocks market.

Surge in Green-Building Certifications Driving Lightweight Masonry

Concrete contributes to 25 of 55 LEED v4 credits, allowing hollow units to unlock up to 74 points when combined with recycled content and superior thermal mass[1]National Ready Mixed Concrete Association, “CSR11 - Concrete's Contribution to LEED v4,” nrmca.org . Use of processed lightweight aggregates derived from plastics can secure 8 additional credits while lowering structural weight and transport emissions. European material groups such as Wienerberger target 75% of revenue from net-zero-ready products by 2026 and report renovation resilience despite a sluggish new-build cycle. Premium-priced eco-blocks, therefore, reinforce profitability as green regulations tighten.

Rising Labor Costs Prompting Modular Construction Adoption

Skilled-trade shortages raise labor premiums and elongate schedules in North America and Europe, pushing developers toward factory-built wall panels that integrate hollow concrete blocks. Industry surveys rank masonry among the trades with the greatest recruitment gaps, prompting contractors to automate repetitive tasks and retrain crews. Experimental robotic bricklayers already place 3.75 m² per hour, triple traditional rates, signalling future scalability for block placement. Prefabricated concrete wall studies confirm lower total installed cost once transportation, quality control, and on-site labor savings are netted. Combined, these factors drive modularization, enhancing demand for dimensionally precise blocks manufactured in controlled settings.

Growth of Disaster-Resilient Infrastructure Programmes

FEMA’s Building Resilient Infrastructure and Communities program allocated approximately USD 2.30 billion in FY 2022 to upgrade vulnerable structures, with concrete masonry units endorsed for tsunami, hurricane, and tornado resistance[2]Federal Emergency Management Agency, “Guidelines for Design of Structures for Vertical Evacuation from Tsunamis,” fema.gov . The National Institute of Building Sciences quantifies that USD 1 spent on resilient construction saves USD 11 in recovery costs, supporting municipal mandates for stronger wall assemblies. Post-earthquake housing analyses in Türkiye demonstrate that integrating community facilities with block-built homes compresses per-unit costs while elevating safety outcomes. These policy directions cement hollow block usage in hazard zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cement & aggregate prices | -1.10% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Stringent carbon-emission regulations on cement industry | -0.80% | EU and North America, expanding globally | Medium term (2-4 years) |

| Skilled-labour shortage for block masonry in developed markets | -0.60% | North America & Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cement & Aggregate Prices

Global freight disruptions, export levies, and regional carbon fees can widen cement price bands from USD 90–130 per ton to as high as USD 160–240 per ton, squeezing block makers’ margins[3]World Cement Association, “Cement Prices Set to Rise as Tariffs on Imports and Carbon Costs Reshape the Industry,” worldcementassociation.org . Smaller producers located far from quarries or ports face disproportionate input cost swings, triggering capacity rationalization and heightening dependence on integrated cement majors. Consolidation in China, where producer numbers may contract from 300 to 30 by 2030, exemplifies how volatility accelerates market restructuring.

Stringent Carbon-Emission Regulations on Cement Industry

Concrete production contributes 8% of global CO₂ output, leading regulators to demand carbon-capture retrofits and supplementary cementitious material adoption. Studies project Hebei Province emissions could fall 50% by 2035 under enhanced low-carbon scenarios, underscoring required investment and process overhauls. Calcium sulphoaluminate cements provide lower-carbon alternatives but present durability and reinforcement challenges at scale. Producers that secure slag, fly ash, or geopolymer substitutes gain cost and compliance advantages, whereas laggards risk fines and supply-chain exclusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Architectural Preference Fuels Split-Faced Dominance

Split-faced blocks captured 63.05% of the hollow concrete blocks market in 2025 and will outpace other formats at a 6.18% CAGR to 2031. Their textured exteriors resemble hewn stone yet preserve the dimensional accuracy and load-bearing capacity of conventional concrete masonry units, appealing to architects specifying visually exposed facades. The hollow concrete blocks market size for split-faced units is projected to widen fastest in premium residential and civic projects that blend function with street-level aesthetics. Smooth-faced blocks hold steady demand in industrial and back-of-house walls where painting or parging masks surface finish. Innovations such as Spherical Block LLC’s interlocking arch modules illustrate how geometry advances expand hollow block applications into curved roofs and domes, creating fresh value pools.

Manufacturing trends reinforce this hierarchy. Semi-automated split-face lines adopt abrasive splitting stations followed by robotic palletizing, lifting output volumes while maintaining consistent texture. Plants deploying geopolymer binders report up to 40% lower embodied carbon relative to Portland blends, enhancing their LEED contribution and winning specification in green public tenders. As green-building codes tighten, producers able to certify Environmental Product Declarations across their split-faced range can command price premiums and defend share.

By End-User Industry: Housing Leads, Infrastructure Accelerates

Residential construction generated 46.62% of global revenue in 2025, supported by large-scale public schemes in South and Southeast Asia that mandate hollow blocks for costed disaster resilience. Affordable housing grants in India require local material use, directing procurement toward nearby block yards and reinforcing rural employment. The hollow concrete blocks market size for residential applications will remain anchored by such domestic content rules even as alternative panels emerge. Other end-user industries, including logistics, data centers, and public utilities, form the fastest-growing cohort at 6.06% CAGR through 2031. These sectors value blocks’ fire rating, impact resistance, and thermal mass in high-occupancy or high-heat environments. Infrastructure bills in North America and seismic improvement programs in Japan further scale non-housing demand, while emerging hydrogen and battery plants specify heavy-duty CMU enclosures for blast mitigation.

Growth of the “other” category accelerates supplier diversification strategies. Block makers partner with engineering firms to pre-detail wall systems complete with reinforcing cages and grouted cells to meet rigorous industrial codes. Such turnkey packages shorten project schedules and create switching costs that insulate suppliers from pure price competition.

Geography Analysis

Asia-Pacific retained 46.05% global share in 2025 and is on track for 5.93% CAGR through 2031, buoyed by sovereign housing blueprints, metro expansions, and regional manufacturing relocation. Indian demand alone absorbs vast concrete output, with the government approving an additional 2 crore dwellings that stipulate resilient wall systems built from locally sourced hollow units. Although Chinese cement production dipped by 10% in 2024, ageing urban stock and coastal flood-defence upgrades sustain steady block consumption. Southeast Asian nations welcome electronics and EV assembly plants that require rapid warehouse construction, driving imports of automated block lines from Japan and Germany to meet quality tolerances.

North America benefits from federal infrastructure stimulus and an accelerating shift toward off-site construction. Over 60,000 projects funded under the Infrastructure Investment and Jobs Act expand highways, ports, and broadband corridors, each demanding durable boundary walls and substation enclosures. Hollow concrete blocks market share gains in the region reflect adoption of modular wall panels that integrate insulation and anchor plates, reducing crane picks and labor hours. FEMA’s resilience grants channel additional block demand into coastal rebuilds, while private e-commerce investors specify concrete masonry for distribution centers to meet fire-rating insurance requirements.

Europe faces subdued new-home starts yet demonstrates resilience in renovation and public-works segments. Producers mitigate lower volumes by emphasizing value-added low-carbon units and thermal upgrades in retrofit markets. Wienerberger reports over half of 2024 revenue now stems from renovation and infrastructure, cushioning the impact of weak German housing starts. Eastern EU markets show healthier momentum as EU funds flow into transport corridors and climate-adaptation schemes, with hollow concrete blocks chosen for their robustness and local aggregate compatibility. The region’s stringent carbon-pricing environment accelerates adoption of supplementary cementitious materials, prompting cross-border knowledge transfer on geopolymer mix designs.

Regulatory Landscape

Regulatory requirements for hollow concrete blocks are anchored in regional performance and test standards for loadbearing CMU, with compliance anchored on compressive strength, density, dimensional tolerances, and durability metrics such as water absorption and shrinkage. In the United States, ASTM International maintains the core specification for loadbearing CMU, with the 2024 update cycle moving from ASTM C90-24 to ASTM C90-24a, reinforcing the need for producers to keep test protocols and QA documentation aligned with the most current revision.

In high-volume emerging markets, national standards and codes guide unit classification, mix design practices, and acceptance criteria used in public procurement and housing programs. India references Bureau of Indian Standards documents such as IS 2185 (Part 1):2005 (concrete masonry units) and IS 2572:2005 (code of practice for construction with hollow and solid blocks), while other jurisdictions publish comparable specifications via national standards bodies, such as the Tanzania Bureau of Standards concrete blocks specification. Across these frameworks, construction chemicals and admixtures are indirectly regulated through final unit performance requirements, making in-house or third-party lab testing and certification critical for supplying government and institutional projects.

Value Chain Analysis

The value chain begins upstream with cement, aggregates, water, and admixtures used to tune workability and strength. Local sourcing patterns anchor procurement strategies to regional standards such as the Tanzania Bureau of Standards concrete blocks specification, and large producers often rely on integrated cement and aggregate networks to reduce price volatility and freight costs.

Manufacturing centers on batching, mixing, vibration-compression forming (dry-cast), de-molding, and curing, followed by palletizing and dispatch. Distribution typically splits between direct supply to large developers and contractors for machine-made volumes and regional yard networks that serve fragmented local demand. Energy costs for plant operation and curing times, along with labor availability, remain bottlenecks, which elevate the value of automation, captive supply, and tighter quality-control systems to meet strength and carbon disclosure requirements.

Competitive Landscape

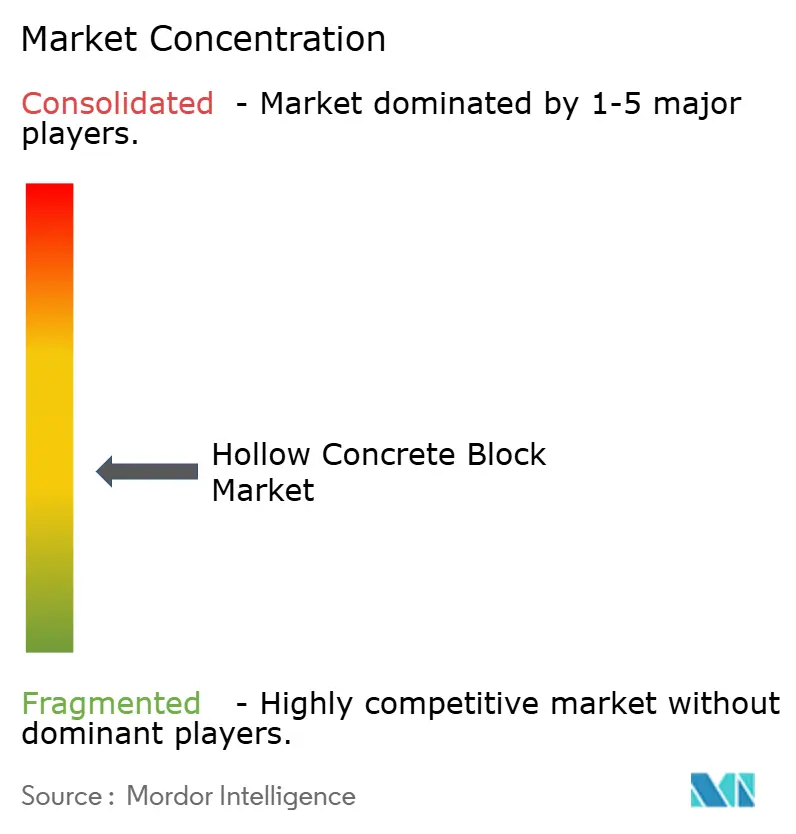

The sector exhibits moderately fragmented concentration. Top global cement groups leverage quarry ownership and downstream distribution to integrate masonry lines, capturing synergies in raw-material flow and logistics. CRH’s USD 2.10 billion Texas acquisition amplified its Southwest masonry footprint, aligning cement mills with block plants to reduce freight costs and stabilize pricing. UltraTech’s capacity expansion to 151.60 million tonnes per annum positions Indian players to defend domestic share against imports while meeting housing-program targets. Heidelberg Materials and Holcim pursue bolt-on aggregate and sand deals across the United States to ensure resilient supply for their concrete block affiliates.

Innovation-driven challengers occupy specialized niches. French start-up MATERRUP commercialized uncalcined clay-based hollow units that cut lifecycle emissions 44%, aligning with EU net-zero procurement thresholds. Adoption of AI-based quality control, automated cubing, and RFID-enabled pallet tracking spreads quickly among mid-tier producers seeking cost parity with vertically integrated giants.

Customer purchasing criteria evolve toward full-lifecycle performance, forcing suppliers to bundle design support, carbon disclosure, and end-of-life recyclability assurances. Firms that meet these layered requirements while maintaining just-in-time delivery stand to consolidate regional contracts as general contractors down-select to fewer strategic partners.

Hollow Concrete Block Industry Leaders

CEMEX S.A.B de C.V

CRH Americas

Holcim

UltraTech Cement Ltd.

Wienerberger

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated in differentiated, code-compliant wall systems that bundle structural performance with lower embodied carbon and better thermal characteristics. In the United States, FEMA resilience guidance and programs such as BRIC have supported upgrades to vulnerable structures, while green-building frameworks like LEED v4 emphasize masonry units that document recycled content, thermal mass benefits, and Environmental Product Declarations. This environment opens whitespace for premium hollow blocks and assemblies, including insulated and interlocking formats that reduce on-site labor and improve envelope performance.

Low-carbon process and product pathways have moved from concepts into demonstrated routes that block makers and their supply chains can operationalize. A June 2026 MIT study with CarbonCure reported that CO2 injection during cement paste mixing improves early hydration and supports an average 4-6% cement reduction, directly addressing the cement intensity of concrete masonry. Product-side innovation is also visible in research on composite insulated interlocking concrete blocks using recycled aggregate concrete and EPS, reported in February 2026 with a 73.5% CO2 reduction versus conventional blocks, creating a tangible development track for producers serving markets with tighter energy codes and embodied carbon screening. On the manufacturing side, automation upgrades from equipment suppliers, including fully automatic block production lines and servo-hydraulic control improvements, align with labor scarcity and the need for tighter dimensional control demanded by modular wall panel applications.

Recent Industry Developments

- July 2026: Fujian UNIK Machinery Technology launched a fully automatic concrete block production line covering batching, mixing, forming, curing, and palletizing for medium-to-large capacity plants. The release strengthens the ecosystem for higher-throughput, more consistent hollow block output where labor shortages and tighter tolerance requirements are pushing producers toward automation.

- June 2026: CRH announced an agreement to acquire Arcosa, Inc. for about USD 8.5 billion to expand its aggregates and critical infrastructure products footprint in the United States. The deal reinforces vertical integration across aggregates and downstream construction products, improving supply security and cost positioning for concrete masonry and related wall-building materials.

- August 2024: Oldcastle APG (CRH Americas) completed the acquisition of Master Block, Inc., expanding concrete block manufacturing capability in the Phoenix metropolitan area. The acquisition added local production capacity and network density in a high-growth construction region, supporting faster fulfillment and improved logistics efficiency for block supply.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market counts the value of hollow concrete blocks sold for building and civil construction, where blocks have internal voids and are used in load-bearing and non-load-bearing walls across typical construction activity.

Scope exclusions: This sizing does not include solid concrete blocks, AAC blocks, bricks, pavers, or ready-mix concrete sold as a separate material.

Segmentation Overview

- By Product Type

- Split-Faced Blocks

- Smooth-Faced Blocks

- By End-User Industry

- Residential

- Commercial

- Industrial

- Other End-User Industry (Infrastructure, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand pool and the supply context before any sizing was done. We relied on public construction indicators and materials signals such as national statistics releases, building permit series, and housing starts where available, which helps anchor how much walling material demand can exist in a given year.

Sources referenced included U.S. Census Bureau construction data, Eurostat construction and housing indicators, UN Comtrade trade statistics for cement and concrete articles (as applicable), and World Bank macroeconomic series. We also reviewed standards and technical guidance published by bodies such as ASTM. In addition, company annual reports, investor presentations, and reputable construction press were reviewed to understand typical product pricing logic and how regional mixes shift. In a few places, paid databases were used only for company financials and intelligence, and for shipment-level import and export checks. This list is illustrative, and many other public sources were reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with block manufacturers, distributors, contractors, and project-side stakeholders who specify masonry products. Since this is a global market, discussions were intentionally balanced across major construction regions to sanity-check price movements, capacity utilization behavior, and the practical split between residential and non-residential demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 19% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where construction output, housing completions, and infrastructure activity are converted into an addressable walling material demand pool, then hollow-block penetration rates and regional usage norms are applied. Once that demand pool was formed, it was translated into value using region-specific average selling price ranges that reflect block type, project mix, and distribution margins.

To keep totals realistic, we corroborated the outcome with selective bottom-up approximations. These included sampled manufacturer capacity and utilization checks, channel feedback on volume ranges, and simple price times volume tests for major regions. Inputs that mattered most included cement price trends, aggregates availability, building permits and housing starts, urbanization and affordable housing programs, and the share of non-residential construction that typically uses block masonry. Where bottom-up data was patchy, gaps were handled by using conservative utilization bands and cross-checking against import-export signals and construction spending direction.

Forecasting leaned on scenario analysis supported by a light multivariate view, where the outlook for construction output, housing demand, and materials inflation was stress-tested with primary expert expectations. Assumptions were kept transparent, so changes in activity levels or pricing can be replayed and the model can be updated without needing hard-to-access data.

Data Validation & Update Cycle

Outputs were validated through stepwise checks that compare model totals against independent construction indicators and materials signals, then against the practical volume and pricing ranges heard in fieldwork. When a region showed an unusual jump or drop, the drivers were re-opened, and respondents were re-contacted to confirm whether the change came from price, mix, or real demand movement.

Before sign-off, the model is reviewed in multiple analyst passes to check arithmetic consistency, unit conversions, and year-over-year logic, followed by a final sense check against macro conditions. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp cement cost swings, major policy changes, or construction slowdowns. Right before delivery, a fresh review is done so clients receive the most current view available at that time.

Mordor Intelligence's Hollow Concrete Block Market Estimate Compared With Other Published Estimates

Published market sizes for hollow concrete blocks can vary even when they appear to describe the same scope, because the year used, the currency conversion timing, and how prices are averaged across regions are not consistent across sources. Differences can also come from how quickly assumptions are refreshed when construction activity or cement-linked pricing shifts.

In this study, the numbers are kept aligned by re-checking base-year pricing bands, applying currency timing consistently, and re-validating region mixes through recent construction indicators and interview feedback, which is why the 2026 value is presented at USD 292.69 B by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 292.69 B (2026) | |

| Global Consultancy A | USD 375.26 B (2024) | Uses an earlier base year and appears to apply a broader price deck across regions, which can lift the total when cement inflation is not normalized and regional mix is not re-checked close to the estimate year. |

| Industry Publisher B | USD 247.10 B (2022) | Anchors the series to an older base year, and the value looks more tied to historical pricing levels, which can understate the market when later-year construction volumes and ASP progression are not carried forward consistently. |

Overall, the spread in published values is mainly explained by base-year selection, how ASPs are rolled up across regions, and how frequently assumptions are refreshed when construction and input costs shift. By keeping each step traceable to demand signals and price logic that can be re-run, we end up with a balanced estimate that is easier to reconcile against real-world construction cycles.

Key Questions Answered in the Report

What is the current value of the hollow concrete blocks market?

The market is valued at USD 292.69 billion in 2026 and is projected to reach USD 374.36 billion by 2031 at a 5.04% CAGR.

Which region leads the hollow concrete blocks market?

Asia-Pacific holds the largest share at 46.05% in 2025, supported by India’s large-scale housing programs.

Which product category dominates global demand?

Split-faced blocks command 63.05% share and are expected to grow at 6.18% CAGR through 2031.

Why are hollow concrete blocks favored in green-building projects?

They contribute to up to 74 LEED v4 points thanks to thermal mass, recycled content options, and lower embodied carbon mixes.

How are labor shortages influencing block construction?

Rising labor costs push builders toward modular and robotic block-laying solutions that cut installation time and total project expense.

What role does disaster resilience play in market growth?

Government programs like FEMA’s BRIC fund resilient infrastructure, boosting demand for block walls that withstand extreme weather events.

Page last updated on: