Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The Indonesia Furniture Market Report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and More), Material (Wood, Metal, Plastic & Polymer, Other Materials), Price Range (Economy, Mid-Range, Premium), Distribution Channel (B2C/Retail, B2B/Project), and Geography (Java, Sumatra, Kalimantan, Sulawesi, Bali & Nusa Tenggara, Maluku & Papua). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

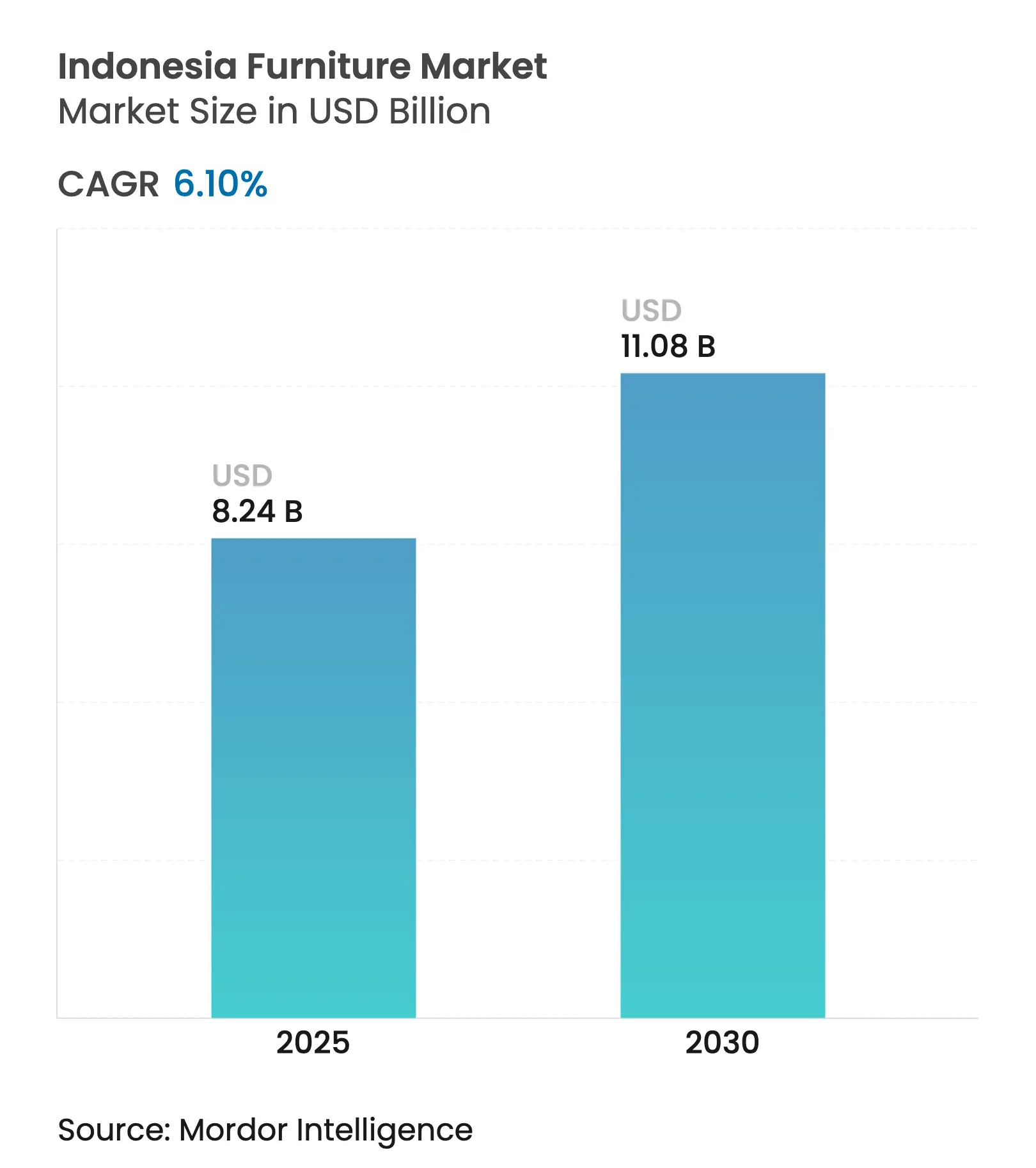

| Market Size (2025) | USD 8.24 Billion |

| Market Size (2030) | USD 11.08 Billion |

| Growth Rate (2025 - 2030) | 6.10 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Indonesia furniture market size stands at USD 8.24 billion in 2025 and is projected to reach USD 11.08 billion in 2030, translating into a 6.10% CAGR during the forecast window. Demand resilience is anchored by the government-led “3 million houses per year” build-out, e-commerce conveniences that break geographic barriers, and the expanding middle class that prioritizes functional yet stylish interiors across urban centers. Within the Indonesian furniture market, premium upgrades coexist with a vast economy base, compelling branded retailers to curate tiered assortments that match evolving spending power. Marketplace data analytics equip manufacturers with real-time insight, shrinking product-development cycles and reinforcing agile design strategies. At the same time, U.S. tariff hikes and teak cost swings squeeze export margins, driving experimentation with plastic composites and new market entries across South Asia and the Middle East.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising middle-class refurbishments

Rising middle-class refurbishments

| +1.2% | Java, Sumatra cities | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Java, Sumatra cities

|

Impact Timeline

:

Medium term (2-4 years)

|

E-commerce portal acceleration

E-commerce portal acceleration

| +0.9% | National (Java focus) | Short term (≤ 2 years) | |||

Organized retail expansion

Organized retail expansion

| +0.7% | Java to Sulawesi | Medium term (2-4 years) | |||

“3 million houses” program

“3 million houses” program

| +1.5% | Nationwide, rural weighted | Long term (≥ 4 years) | |||

Carpentry-cluster digitization

Carpentry-cluster digitization

| +0.4% | Central & East Java | Long term (≥ 4 years) | |||

Eco-furnishing for green resorts

Eco-furnishing for green resorts

| +0.3% | Bali, Nusa Tenggara | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Middle-Class Spending on Urban Housing Refurbishments

Stable income growth across larger cities fuels continuous demand for aesthetic upgrades and functional remodeling of existing apartments. Retailers such as INFORMA stimulate purchases with cashback of up to IDR 1.7 million and bundled room sets priced from IDR 4.5 million, reinforcing premiumization trends[1]“Promo Kemerdekaan di INFORMA Ada Banyak Diskon Produk Furnitur Lokal,” TribunJogja, tribunnews.com. PT Home Center Indonesia operates 100+ stores and 35,000 SKUs, providing one-stop access to curated collections that suit aspirational interior themes. Refurbishment spending extends furniture replacement cycles, enabling recurring revenue streams for suppliers that offer modular customization and installment financing. As urban households prioritize ergonomic designs for compact living spaces, value migration shifts toward configurable, space-saving furniture that commands higher margins. The driver’s medium-term horizon aligns with continued urbanization and rising household formation across Java and Sumatra.

Rapid Growth of E-Commerce Furniture Portals

Tokopedia, Shopee, and Ruparupa collectively reshape purchase journeys by combining extensive digital catalogs, 3-D visualization tools, and same-day delivery. Ruparupa lists items ranging from IDR 89,000 to IDR 13.7 million and promotes discounts of 30-66%, widening reach to both economy and premium shoppers. Omnichannel linkages allow click-and-collect services at affiliated stores, mitigating the traditional reluctance to buy bulky goods sight unseen. Investment in AI-driven recommendation engines enhances cross-selling of décor accessories, elevating average transaction values. For manufacturers, marketplace analytics deliver granular demand insights, informing agile inventory planning and faster design refreshes. The impact materializes quickly given Indonesia’s 205 million internet users and high mobile commerce penetration.

Expansion of Organized Retail Chains Beyond Java

IKEA, Informa, Mitra10, and Guardian extend footprints to Surabaya, Bandung, and Makassar, reducing logistics costs and service gaps in secondary cities. IKEA’s 9,000 m² Surabaya outlet exemplifies strategic clustering near emerging malls. PT Hero Supermarket, the local IKEA operator, posted IDR 2.25 trillion net revenue in H1 2024, underpinned by store expansion[2]Dimas Andi, “Hero Supermarket Andalkan IKEA dan Guardian,” Kontan, kontan.co.id. Standardized layout, consistent warranties, and ready-to-assemble formats raise consumer expectations of after-sales support, prompting smaller outlets to upgrade displays and financing programs. Geographic diversification also unlocks new supplier bases nearer to plantation hardwoods in Kalimantan and Sulawesi, shortening lead times and reducing raw-material transport expenses.

Government-Backed “3 million Houses” Public-Housing Program

The flagship housing mandate targets 2 million rural houses and 1 million urban apartments annually, aimed at eliminating a 9-million-unit backlog. In its first 100 days, the program facilitated 87,736 subsidized mortgage approvals through the FLPP scheme, signaling execution capacity. Foreign investors from Qatar, the UAE, and Singapore pledge capital for low-income communities, de-risking procurement cycles for furniture suppliers. Standardized modular kitchens, wardrobes, and study units are bundled within builder packages, transferring bulk orders to compliant manufacturers that can meet delivery milestones. Tax incentives such as BPHTB exemptions further stimulate ownership and associated furniture purchases, solidifying the program’s long-term effect on the Indonesia furniture market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Teak & mahogany price spikes

Teak & mahogany price spikes

| -0.8% | Java mills | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Java mills

|

Impact Timeline

:

Short term (≤ 2 years)

|

SME ESG-certification burden

SME ESG-certification burden

| -0.6% | National clusters | Medium term (2-4 years) | |||

Fire-safety approval delays

Fire-safety approval delays

| -0.4% | Urban hospitality | Short term (≤ 2 years) | |||

Port congestion cost inflation

Port congestion cost inflation

| -0.5% | Jakarta & Surabaya | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Teak & Mahogany Log Prices Due to Upstream Export Controls

Perhutani's auction prices fluctuate between IDR 12.5 million and IDR 20 million per cubic meter, exerting pressure on exporters reliant on premium hardwoods[3]“Source Teak Wood Product from Indonesia Suppliers,” Indotrading, indotrading.com. The mandatory SVLK legality scheme, while adding documentation costs, facilitates preferential access to EU markets under a Voluntary Partnership Agreement. Exporters face challenges in maintaining profitability due to these rising costs and price fluctuations. To mitigate risks, manufacturers like PT Indoexim have adopted vertical integration by securing log procurement and diversifying into acacia furniture production. This strategy helps them manage supply chain uncertainties and reduce dependency on premium hardwoods. However, short-term volatility remains a concern until export-quota policies stabilize. Additionally, the maturation of plantation rotations is critical for ensuring long-term supply stability and market equilibrium.

Fragmented SME Base Facing Rising ESG Certification Costs

Approximately 90% of registered furniture firms employ fewer than 50 workers, which limits their financial capacity to conduct sustainability audits. Research identifies low environmental awareness and a lack of government incentives as key obstacles to adopting green supply-chain practices. Asmindo has recommended upstream-only SVLK enforcement to alleviate the burden on downstream workshops. However, global retailers are increasingly demanding full supply-chain traceability to meet international standards. This divergence in priorities creates challenges for smaller firms trying to remain competitive in the global market. The inability to comply with these requirements may lead to stalled export agreements, further straining the financial health of micro enterprises. Over time, non-compliant firms may exit the market entirely. This could result in sector consolidation as larger or more adaptable firms absorb market share. Such shifts highlight the growing pressure on the furniture market to balance sustainability with economic viability.

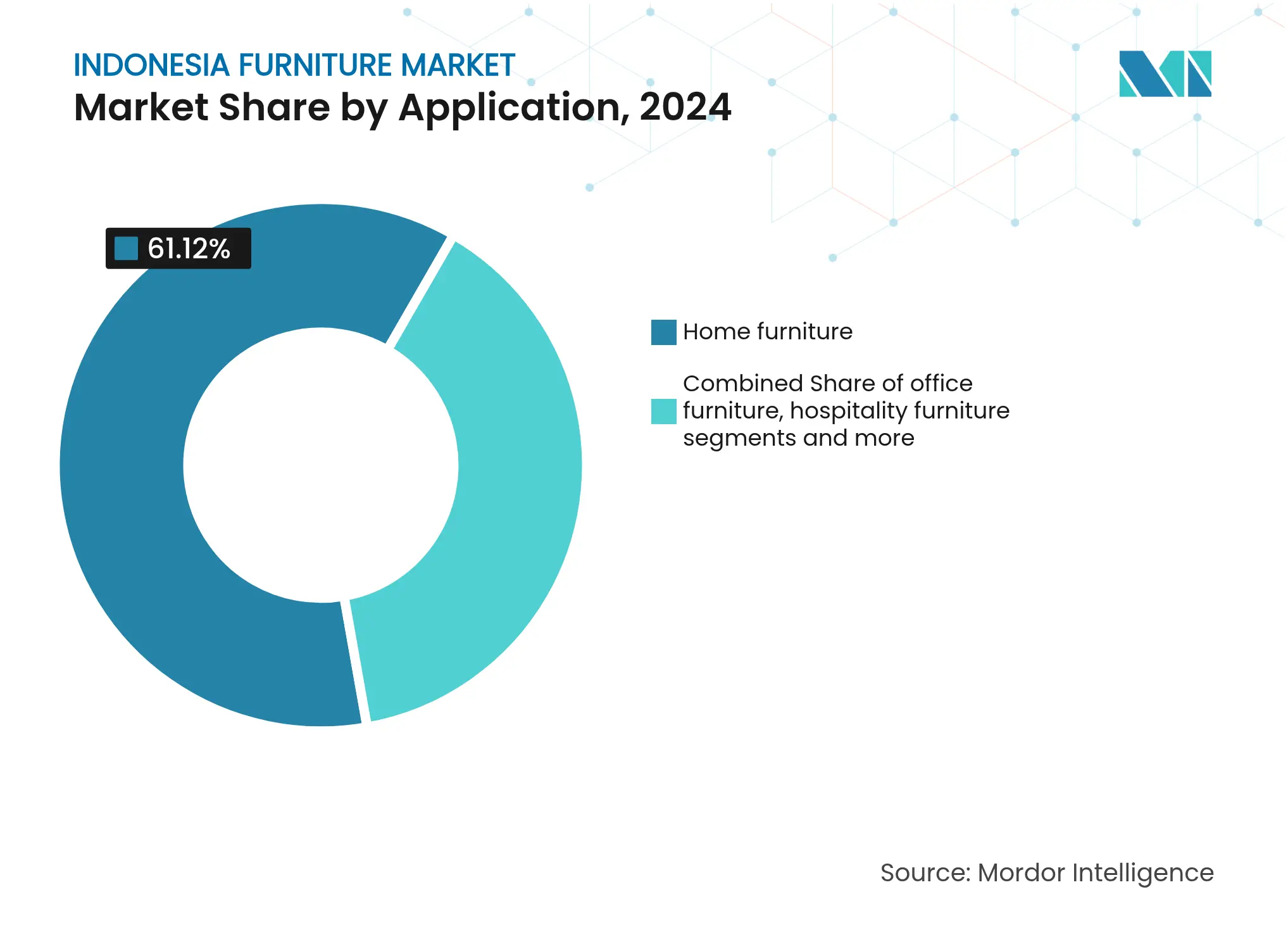

By Application: Home Furniture Anchors Demand Amid Construction Boom

Home furniture produced 61.12% of 2024 revenue and continues to chart a 6.54% CAGR that mirrors housing completions under the “3 million houses” plan. Bulk procurement for subsidized mortgages secures large repetitive orders for bedroom and living room sets, allowing factories to optimize production lines with fewer changeovers. Urban middle-class renovators inject incremental volume into the Indonesian furniture market as modular wardrobes, convertible sofa-beds, and under-stairs cabinetry gain traction on social platforms. Contract players integrate design-build-install packages, attracting developers who seek rapid fit-out cycles and single-invoice convenience. Outside pure residential, office furniture grows steadily, fueled by co-working expansions and ergonomic upgrades for hybrid workforces in Jakarta and Bandung. Hospitality demand rebounds on tourism recovery, prompting luxury resorts to commission bespoke teak loungers and bamboo cabanas that satisfy low-VOC standards. Educational institutions modernize classrooms with stackable desks and digital-device charging pedestals, while healthcare entities replace legacy waiting-room benches with anti-microbial polymer seats. Each adjacent niche widens the home-furniture supplier network, yet none presently eclipses the sheer scale of beds, wardrobes, and kitchen counters delivered into newly finished residences of the Indonesia furniture market.

Second-order momentum stems from Asmindo’s partnership with BRIN to commercialize rattan-based panel boards that reduce weight and cut installation time by 20%, giving home-furniture producers material flexibility and exportable product stories. Branded retail chains overlay lifestyle storytelling—Scandinavian, Japandi, or Modern-Industrial—to differentiate collections and uphold margin even within mid-range price tags. Meanwhile, 3-D room-builder apps embedded on e-commerce sites let buyers drag-and-drop digital replicas of sofas and coffee tables into floor plans, boosting cross-category basket sizes. As the Indonesian furniture market scales, sustainability audits such as BREEAM for residential developments trickle into furniture procurement templates, nudging suppliers to substitute water-based lacquers and FSC-certified bamboo ply. With regulators sharpening energy-efficiency codes for apartments, lightweight composite cabinets emerge that reduce structural load yet sustain premium finishing, cementing home furniture’s leadership through 2030.

Note: Segment shares of all individual segments available upon report purchase

By Material: Wood Holds Pre-eminent Share While Polymer Captures Fast-Track Growth

Wood retained 64.23% of 2024 sales, underpinned by Indonesia’s abundant teak, mahogany, rattan, and bamboo resources as well as legacy hand-carving expertise in Jepara. SVLK legality documentation enables seamless EU market access, preserving export competitiveness for seasoned producers. Inside the domestic arena, rural customers still associate solid teak with status longevity, supporting price resilience despite raw-log volatility. Integrated players vertically manage plantation forests, veneer mills, and cabinet assembly floors to buffer cost shocks and secure continuity. Nevertheless, the Indonesian furniture market is witnessing polymer furniture sprint ahead at a 7.43% CAGR. Injection-molded polypropylene chairs, HDPE wicker patio sets, and ABS study tables appeal to cost-conscious renters and hospitality operators in high-humidity zones.

Plastic’s ascendancy is also powered by colorfastness and recyclability campaigns, as manufacturers infuse up to 30% post-consumer pellets to satisfy emerging ESG scorecards. Polywood hybrids—sawdust mixed with recycled plastic—mimic timber grain without warping, offering hotel chains a maintenance-light alternative. PT Polymindo Permata’s USD 4.84 million export run in 2024 exemplifies international appetite for synthetic rattan built to stringent UV-resistance standards[4]“Supply Chain Data of PT Polymindo Permata,” Trademo, trademo.com. Metal remains important for office chairs, adjustable desks, and bunk beds in mining camps, yet growth lags due to steel price unpredictability. Composite newcomers blend magnesium board cores and bamboo veneers, providing fire-retardant yet lightweight solutions that have begun to win hospital contracts. The widening materials palette underscores the Indonesia furniture market’s pivot from single-source hardwood dominance toward a diversified, innovation-oriented supply base.

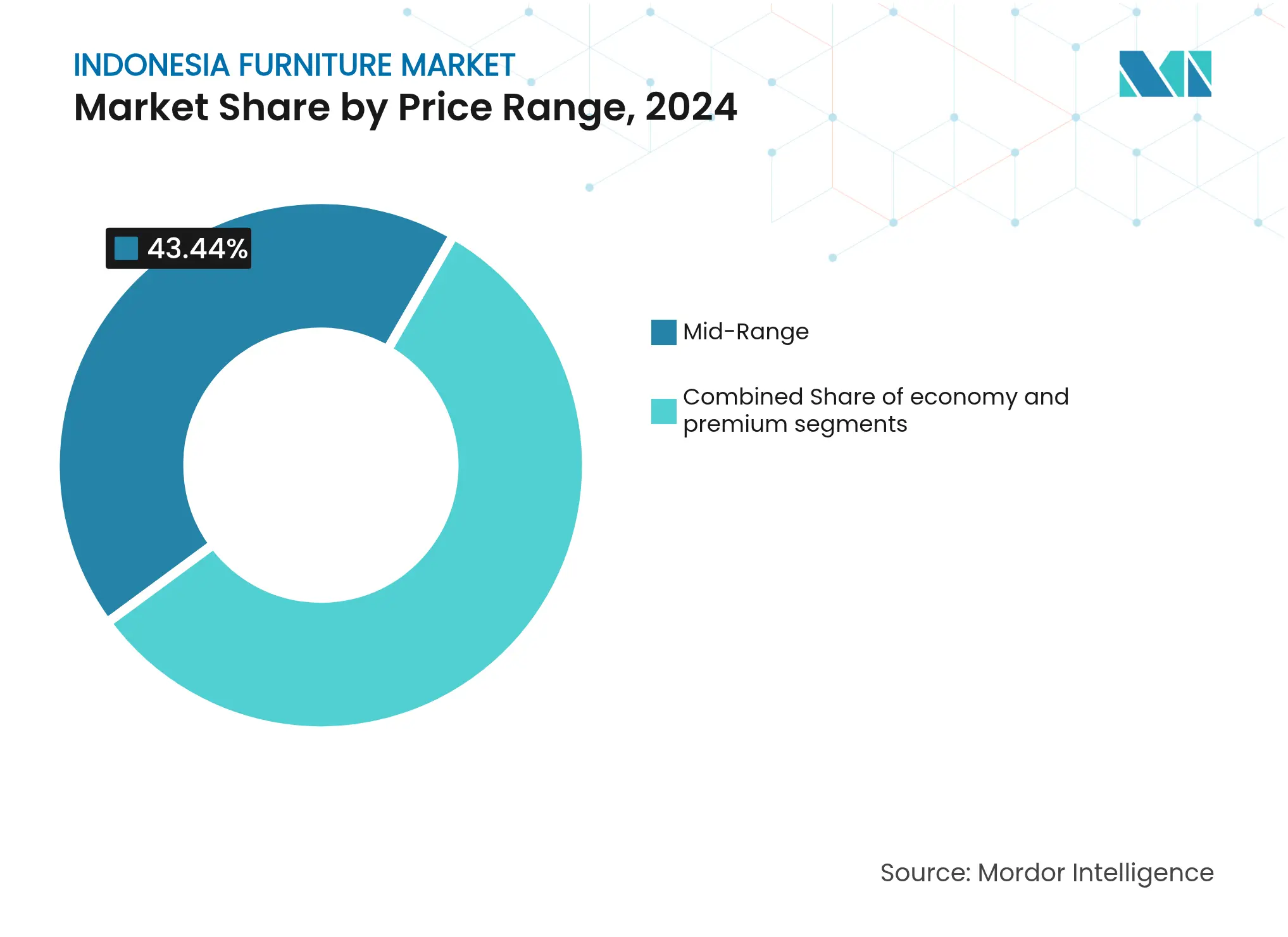

By Price Range: Mid-Range Dominance Continues as Premium Ascends

Mid-range SKUs commanded 43.44% of the Indonesia furniture market size in 2024, servicing aspirational homeowners who prioritize quality over low-cost disposability yet remain budget conscious. Retailers tailor installment plans of 0% for 12-24 months, enabling middle-income buyers to upgrade to engineered-wood wardrobes with soft-close hinges. Embedded credit scoring within e-commerce checkouts brings unbanked consumers into formal purchase ecosystems, swelling volume for mid-tier brands. In parallel, premium furniture logs the fastest 6.24% CAGR through 2030, boosted by imported Italian leather recliners, German motorized ergonomic desks, and bespoke teak dining tables hand-finished in Central Java studios. Melandas Indonesia alone delivered USD 26.2 million in revenue in 2024 from distributing Natuzzi and La-Z-Boy portfolios, indicating a widening high-end appetite.

The premium ascent coincides with luxury condo completions in Jakarta’s SCBD district and Bali’s cliffside villa boom, each bundling curated furnishing packages into property sales contracts. Manufacturers court architects early with 3-D parametric libraries that slot seamlessly into BIM workflows, locking in specifications long before site handover. Economy lines remain indispensable for government social-housing tenders, commanding sheer volume via compressed-particleboard wardrobes shipped flat-pack to remote islands. Still, automation in particle press lines and edge-banding technology is lifting durability, narrowing the perceived quality delta with mid-range. Consequently, value migration in the Indonesian furniture market becomes less about absolute price and more about lifestyle storytelling, service, and sustainability attributes.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Omnichannel Retail Captures Customer Lifetime Value

B2C retail, including large-format stores, specialty boutiques, and digital marketplaces, generated 70.56% of the 2024 value and is forecast to expand at a 7.03% CAGR. In-store experiences evolve into discovery hubs—giant screens stream AR room visualizations, while cafe corners extend dwell time, driving soft attachment sales such as cushions and candles. Ruparupa supports same-day delivery in Jakarta and two-day service across Java, leveraging micro-fulfillment centers attached to Ace Hardware outlets. Online campaigns featuring user-generated content and influencer walkthrough videos democratize design ideas, funneling first-time buyers into repeat cycles of add-on accessories.

Project-based B2B channels retain strategic relevance, especially for office towers in the new Nusantara capital and international hotel chains refreshing Bali inventories. Procurement criteria now weigh carbon footprints and lifecycle costing, prompting suppliers to provide cradle-to-grave documentation. Local carpentry SMEs participate through consortium bids, bundling bespoke lobby installations with standardized guestroom case goods to satisfy both creativity and volume needs. Some mid-sized factories explore direct-to-site shipping models, cutting out local distributors and passing savings on to contractors, although after-sales servicing remains a challenge. The interplay between B2C immediacy and B2B customization broadens the Indonesia furniture market’s distribution matrix, ultimately maximizing customer lifetime value for agile suppliers.

Java retained 46.21% of 2024 revenue as its dense population, industrial parks, and dual megaports provide unmatched economies of scale. Jakarta’s outer belt warehouses integrate WMS and RFID tagging, slashing pick times and enabling next-day delivery to 40 million residents. Jepara artisans embrace CNC routers to translate intricate baroque patterns into repeatable code, fusing heritage craftsmanship with German precision cutters. Surabaya’s nearby plantation estates ensure steady teak and acacia feedstock, reducing inbound freight costs. Local governments sponsor SMK vocational curricula specializing in cabinet assembly, injecting skilled labor into factories and reinforcing Java’s preeminence within the Indonesian furniture market.

Sumatra’s GDP uplift from downstream palm-oil processing and improved inter-island ferries catalyze furniture demand in Medan and Palembang malls. Retailers pilot “store-within-truck” pop-ups that tour secondary cities, capturing latent appetite without committing to high lease costs. Kalimantan gears for government infrastructure tied to the Nusantara capital move, ordering office workstations and modular dormitory beds for civil-service relocations. Sulawesi hosts aluminum smelters that feed raw frames for knock-down bunk beds shipped nationwide, anchoring a budding metal-furniture niche.

Bali & Nusa Tenggara boast the highest 6.95% CAGR forecast as green resort pipelines specify locally crafted bamboo sun-loungers and FSC-certified teak headboards. Benoa Port’s dredging to 12 m depth allows 4,000-passenger cruise ships, quadrupling shore-excursion furniture purchases by hospitality operators. SMEs partner with international designers to create low-VOC, water-resistant chaise collections, commanding premium margins and exporting under Bali provenance branding. Maluku and Papua remain nascent yet hold promise for rattan sourcing, which could shorten supply lines for polymer-core wicker exporters.

Market Concentration

Indonesia’s manufacturers tapestry remains fragmented, with more than 14,000 registered entities but only a dozen surpassing USD 100 million turnover. PT Integra Indocabinet pioneered forest-carbon credit monetization, targeting 5-7% of revenue initially and up to 50% within 10 years, thereby hedging against commodity cycles and boosting ESG credentials. PT Golden Dacron’s partnership with INFORMA fulfills the Ministry of Industry’s localization mandate, enhancing domestic content ratios and shortening lead times. Furnindo Utama Asia’s HOMAG automation cut defect rates to 2% and raised throughput, signaling ROI potential for Industry 4.0 adoption in mid-tier factories.

SME digitization accelerates as SaaS platforms bundle quotation, nesting optimization, and payment gateways, empowering micro-workshops to sell nationwide via marketplace storefronts. Exporters diversify target geographies after 32% U.S. tariffs enacted in April 2025; India, Australia, and the Netherlands emerge as promising lanes courtesy of favorable MFN duties and home-improvement booms. Retail brands weaponize data analytics to track SKU velocity by district, refining assortment, and reducing markdown exposure. Sustainability emerges as a decisive tiebreaker; companies attaining PEFC and FSC certifications secure long-term hotel contracts, marginalizing uncertified rivals.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value in USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Furniture are movable articles used in a room or space suitable for working and living. The scope includes furniture used in residential, commercial, hospitality, and other applications. Indonesia Furniture Market is Segmented by Material (Wood, Metal, Plastic and Other Materials), by Application (Home Furniture, Office Furniture, Hospitality Furniture, and Other Furniture) and by Distribution Channel (Supermarkets, Specialty Stores, Online, and Other Distribution Channels). The Report Offers Market Size and Forecasts for the Indonesia Furniture Market in Value (USD Billion) for all the above Segments.

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.