Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 197.19 Billion |

| Market Size (2030) | USD 489.64 Billion |

| Growth Rate (2025 - 2030) | 19.95% CAGR |

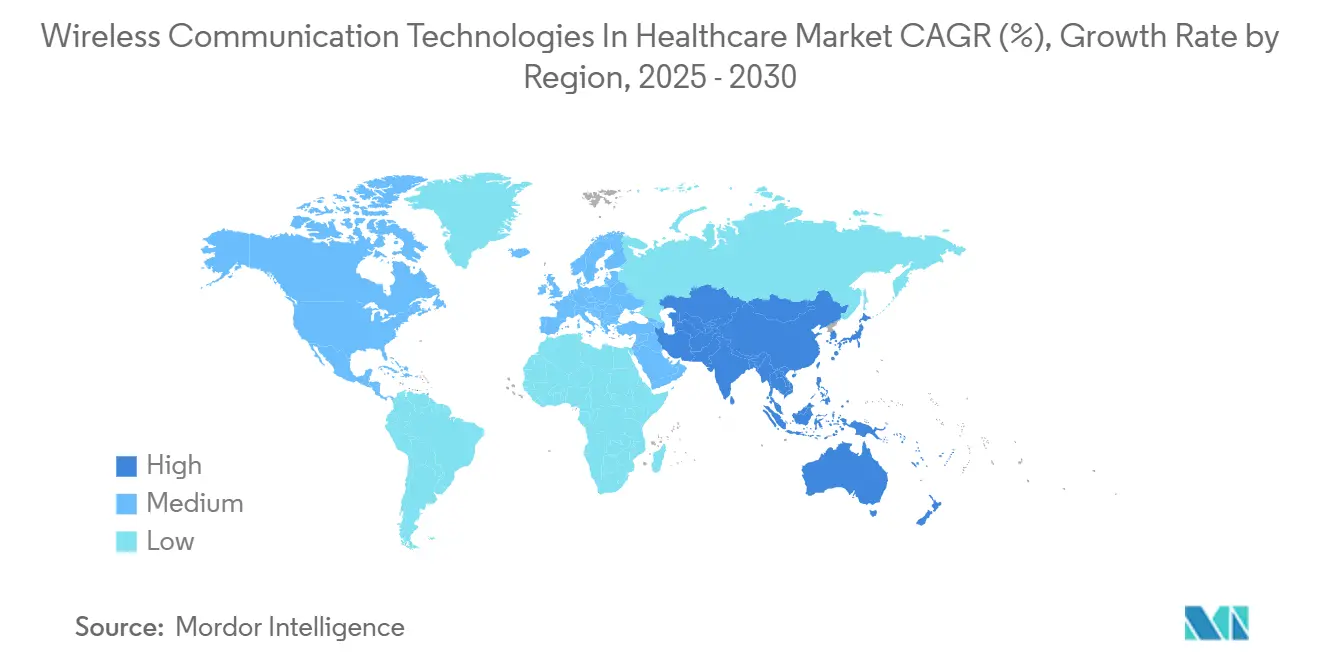

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

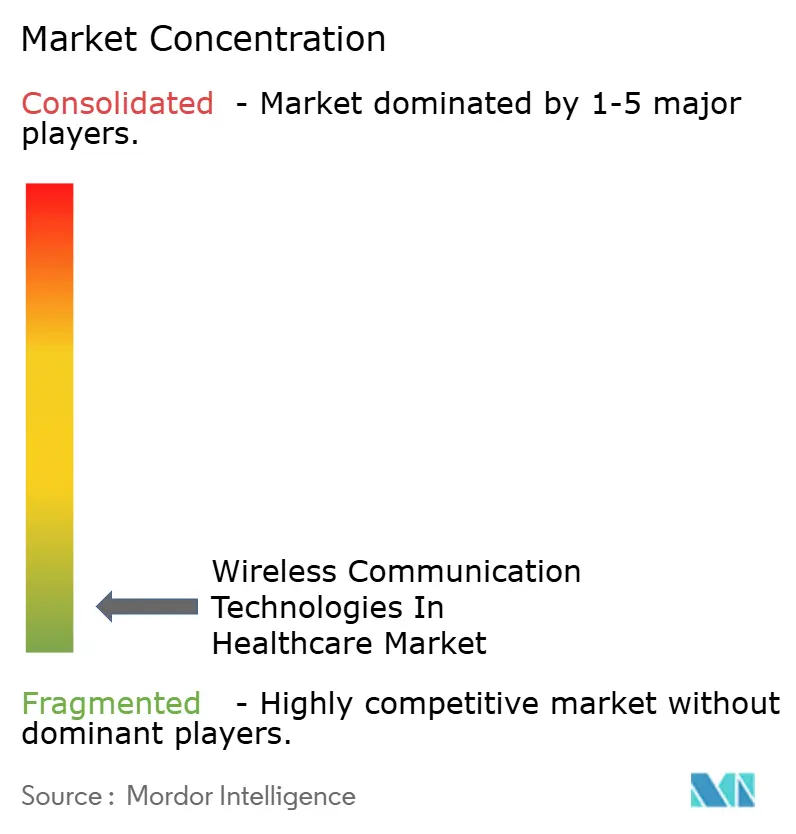

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Communication Technologies In Healthcare Market Analysis by Mordor Intelligence

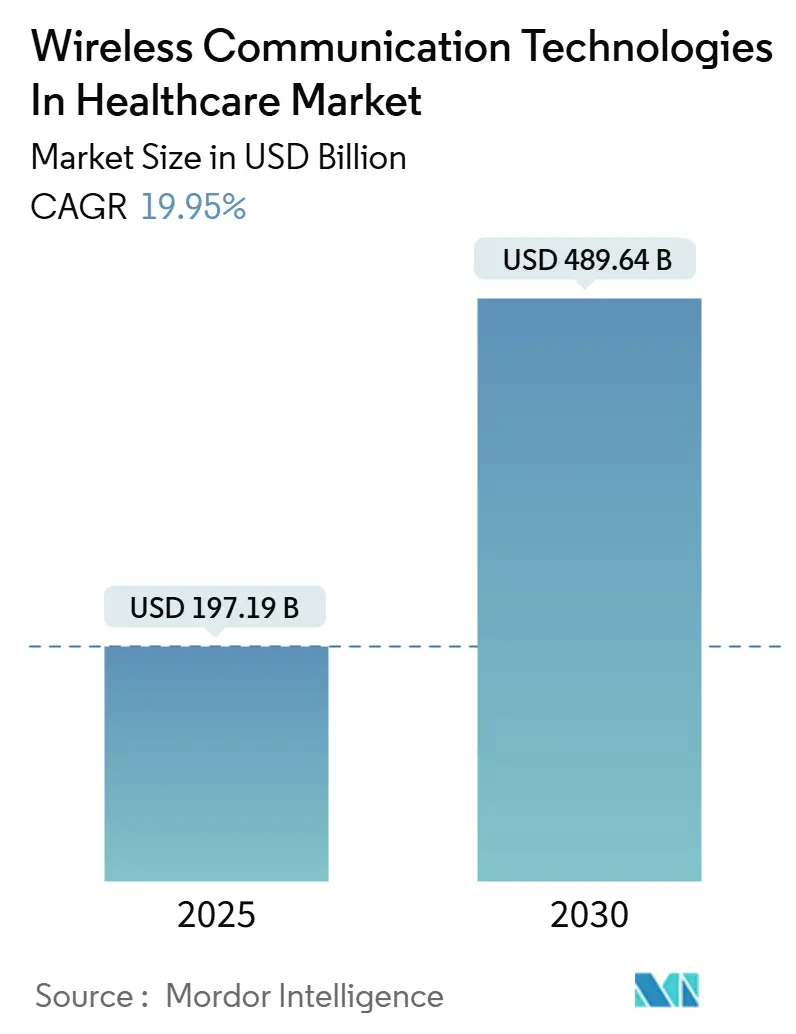

The wireless communication technologies in healthcare market size reached USD 197.19 billion in 2025 and is projected to touch USD 489.64 billion by 2030, expanding at a 19.95% CAGR over the forecast period. Rapid migration from episodic in-facility care to continuous home-based monitoring, combined with sovereign digital health mandates, is accelerating demand for 5G private networks, Wi-Fi 6E retrofits, and cloud-native device orchestration platforms. Falling sensor prices, expanding value-based reimbursement, and tighter interoperability rules are drawing investments from hospitals, insurers, and device makers alike. Competitive intensity is rising as telecom carriers, medical-device OEMs, and hyperscale cloud providers seek to monetize device data. At the same time, cybersecurity staffing gaps and spectrum congestion in older campuses temper the pace of infrastructure refreshes.

Key Report Takeaways

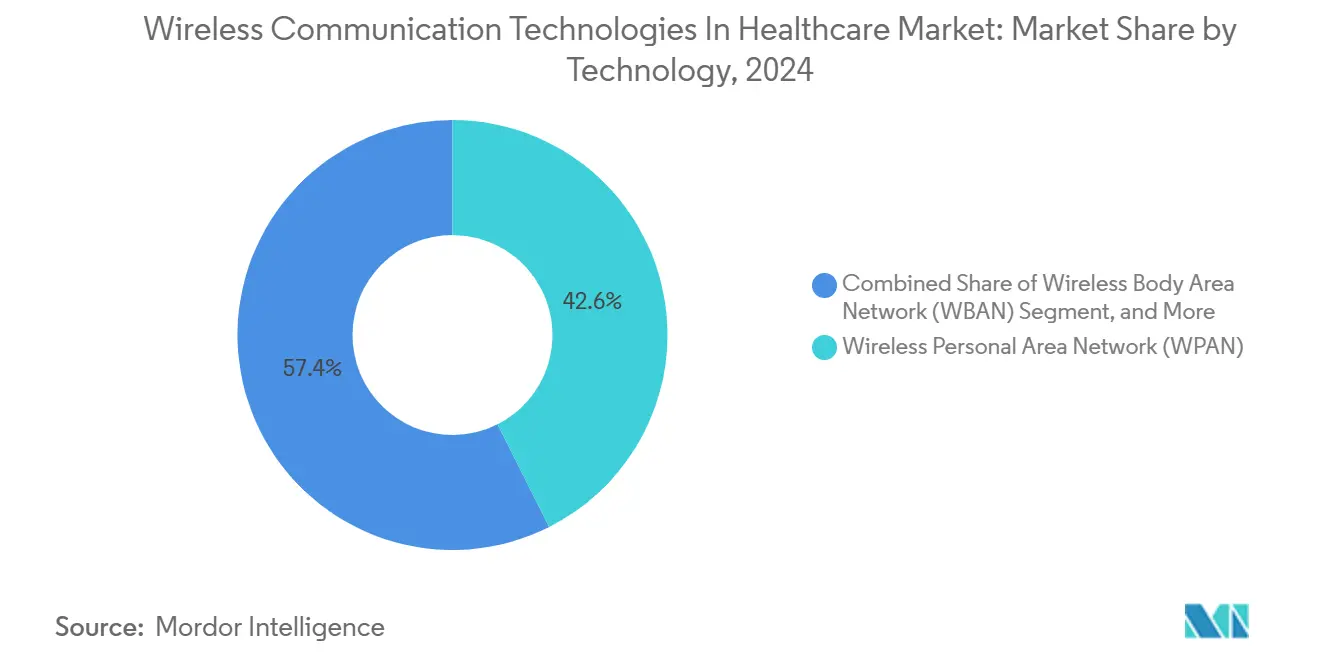

- By technology, wireless personal area network held 42.57% of the wireless communication technologies in healthcare market share in 2024, while Wireless Body Area Network is advancing at a 20.42% CAGR to 2030.

- By component, hardware accounted for 48.52% of the wireless communication technologies in healthcare market size in 2024, whereas software platforms are expanding at a 21.77% CAGR.

- By application, remote patient monitoring platforms led with 37.75% revenue share in 2024; home care is forecast to pace the field with a 22.31% CAGR through 2030.

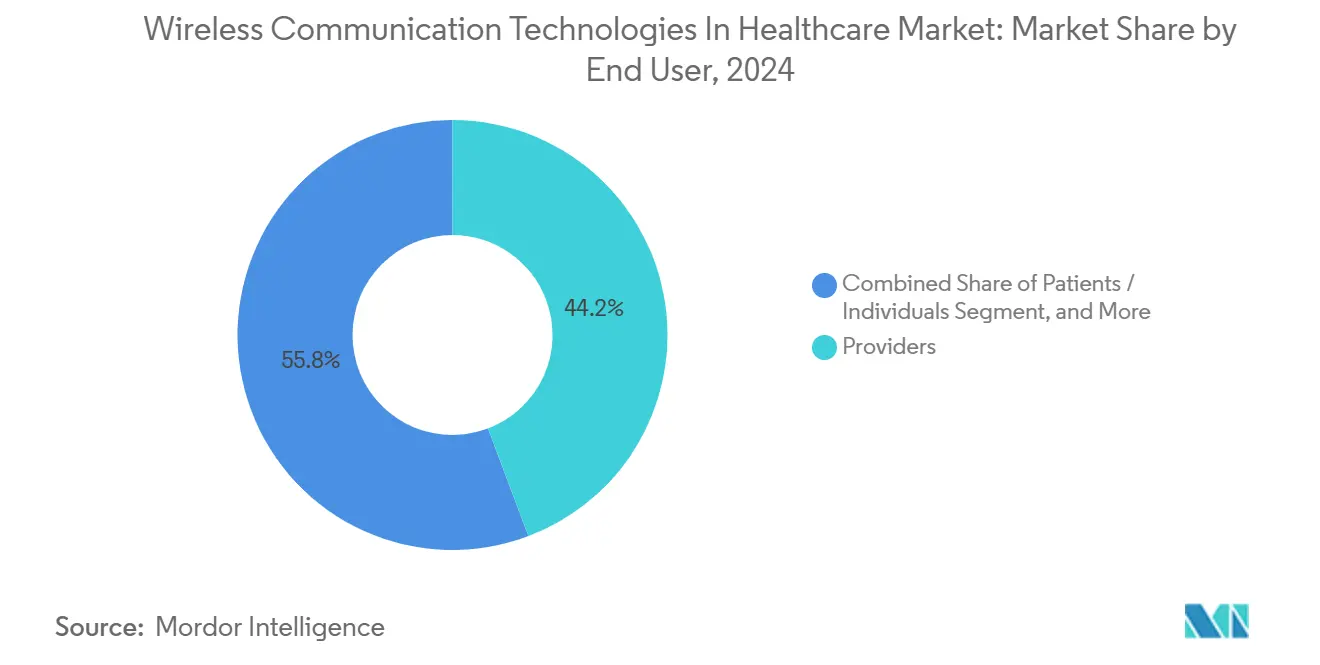

- By end user, providers represented 44.24% of 2024 spending; however, the patients and individuals segment is growing fastest at a 20.87% CAGR.

- By device connectivity, Wi-Fi and WLAN commanded a 38.45% share in 2024, while cellular links are growing at a 21.63% CAGR as 5G slicing gains traction.

- By geography, North America captured 40.12% revenue in 2024; Asia-Pacific is projected to record the highest CAGR at 22.56% to 2030.

Global Wireless Communication Technologies In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G-Enabled Remote Patient Monitoring | +4.2% | North America, Asia-Pacific core, spill-over to Europe | Medium term (2–4 years) |

| Proliferation of Wearable and Implantable Sensors | +3.8% | Global, with early gains in United States, Germany, Japan | Short term (≤ 2 years) |

| Expansion of Hospital Wi-Fi 6E and Wi-Fi 7 Upgrades | +3.1% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Cloud-Native Integration of Connected Device Data | +2.9% | Global, led by United States, United Kingdom, Australia | Long term (≥ 4 years) |

| Value-Based Care Incentives for Home Tele-Care | +2.7% | United States, Canada, select European Union markets | Short term (≤ 2 years) |

| National Digital-Health Infrastructure Spending | +2.3% | China, India, European Union, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G-Enabled Remote Patient Monitoring

Private 5G networks now deliver sub-20 ms latency, supporting robotic surgery consoles and augmented-reality navigation. More than 200 U.S. health systems have deployed on-premises Citizens Broadband Radio Service cores, enabling bandwidth slicing that separates critical telemetry from administrative traffic. [1]Federal Communications Commission, “6 GHz Unlicensed Spectrum,” fcc.govChina’s mandate that all new tertiary hospitals install 5G stations by 2026 is speeding rollouts in coastal provinces. Qualcomm’s Snapdragon X75 modem, certified in 2025, embeds Release 18 features, including network-verified time synchronization, which cardiac-device makers use to time-stamp arrhythmia events with sub-microsecond precision. [2]Qualcomm Technologies, “Snapdragon X75 5G Modem-RF System,” qualcomm.com Japan’s NTT Docomo and Nihon Kohden piloted 5G electrocardiogram patches that stream 12-lead waveforms every 10 seconds to cloud AI engines. Power efficiency gains of 30% compared to 4G modems extend battery life and enable round-the-clock monitoring for patients with chronic respiratory conditions.

Proliferation of Wearable and Implantable Sensors

Continuous glucose monitors posted 40% year-over-year unit growth in 2024, driven by the clearance of Dexcom G7 and Abbott FreeStyle Libre 3. Implantable cardiac monitors, such as the Medtronic Reveal LINQ II, harvest kinetic energy, eliminating the need for battery replacement surgeries. New EU guidance requires Class IIb implantables to support over-the-air firmware updates, thereby accelerating the adoption of Bluetooth 5.4. Wearable wound-monitoring patches integrate NFC tags, allowing clinicians to retrieve temperature and moisture data with a quick smartphone tap, thereby reducing the need for manual rounds. Increasing sensor accuracy and miniaturization, coupled with reimbursement expansion, move the market from pilot to mainstream.

Expansion of Hospital Wi-Fi 6E and Wi-Fi 7 Upgrades

Wi-Fi 6E shifts medical-device traffic into the 6 GHz band, tripling available channels and reducing interference. Cisco Catalyst 9166 access points support 160 MHz channels that handle high-resolution surgical video. Europe harmonized 500 MHz of 6 GHz spectrum in late 2024, prompting pilots at Charité Berlin that achieved 2.4 Gbps throughput for 300 concurrent pumps and monitors. Wi-Fi 7 introduces multi-link operation, which bonds 2.4, 5, and 6 GHz radios, thereby eliminating packet loss during nurse handoffs. Extreme Networks offers firmware-upgradable access points, lowering the total cost of ownership and easing transition paths. Hospitals are retiring disparate nurse-call systems and unifying telemetry, voice, and data on one wireless fabric.

Cloud-Native Integration of Connected-Device Data

Amazon HealthLake, Microsoft Azure IoT Hub, and Google Healthcare API now ingest device observations natively in FHIR, reducing custom integration overhead. [3]Amazon Web Services, “Amazon HealthLake,” aws.amazon.com Interoperability mandates in the United States Cures Act and pending European Health Data Space regulation require vendors to expose standardized APIs. Edge gateways from Hewlett Packard Enterprise enable on-device inference, which filters out false alarms before forwarding alerts, resulting in a 40% reduction in network egress costs. Hybrid cloud-edge patterns balance latency, data residency, and cost. Subscription revenue for analytics and predictive maintenance is displacing one-time hardware sales, reshaping vendor business models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Skill Shortages in Provider IT Teams | -1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Spectrum Congestion in Legacy Hospital Campuses | -1.3% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Battery-Swap Requirements for High-Duty Sensors | -0.9% | Global, with higher impact in resource-constrained settings | Long term (≥ 4 years) |

| Fragmented Reimbursement for Continuous RPM | -1.1% | United States, select European markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Skill Shortages in Provider IT Teams

Vacancies exceed 60% for security operations center roles, leaving wireless devices vulnerable to ransomware. The HIMSS 2024 survey found 73% of hospitals cite staffing shortfalls as the top barrier to zero-trust IoT segmentation. FDA draft guidance now requires a software bill of materials and secure-by-design evidence, yet many legacy pumps lack the capacity for modern encryption. Managed security service uptake remains below 30% due to concerns over data sharing and tight budgets. Rural facilities face the highest risk because technology-sector wages outstrip hospital pay scales, widening the competency gap.

Spectrum Congestion in Legacy Hospital Campuses

Hospitals built before 2010 rely on 2.4 GHz Wi-Fi, which offers only three non-overlapping channels. An American Hospital Association study found that packet loss above 5% occurred during peak census in 68% of surveyed facilities, triggering false telemetry alarms. Retrofitting concrete wings with 6 GHz cabling necessitates asbestos abatement and fire-code compliance, thereby increasing upgrade costs. Paging systems persist on VHF because cellular coverage is often unreliable in basements and stairwells. Limited 6 GHz allocations in Japan further crowd hospital LANs. The slow transition to voice-over-Wi-Fi smartphones delays the full retirement of one-way pagers, which clinicians still trust for instant alerts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: WBAN Adoption Accelerates on Implantable Uptake

Wireless Personal Area Network technology accounted for 42.57% of the 2024 revenue base, reflecting widespread use of Bluetooth-enabled oximeters, thermometers, and cuffs in outpatient and home settings. Wireless Body Area Network solutions are growing at a 20.42% CAGR as implantable rhythm monitors and continuous glucose sensors adopt ultra-wideband and body-coupled links, which reduce power draw. Wi-Fi continues its steady march as Wi-Fi 6E replaces 802.11ac hardware in surgery suites, and 5G upgrades underpin ambulances that require seamless backhaul. Worldwide Interoperability for Microwave Access remains a niche technology, primarily used in rural telemedicine kiosks. The IEC 60601-1-8 electromagnetic-compatibility standard, published in 2024, harmonizes WBAN protocols, easing multi-vendor deployment.

Bluetooth Low Energy 5.4 halves duty-cycle power consumption through periodic advertising with responses, extending sensor wear time and shrinking battery footprints. IEEE 802.15.4z ultra-wideband enables centimeter-level ranging, which Zebra Technologies pilots for real-time asset tracking. Body-coupled communication leverages the conductivity of human tissue, thereby mitigating MRI-suite interference. Regulators steer spectrum use, the FCC’s 6 GHz allocation and ETSI’s 60 GHz harmonization channel capital into high-bandwidth, low-latency links.

By Component: Software Platforms Monetize Device Data

Hardware still delivered 48.52% of 2024 revenue, driven by gateways, modems, and sensor modules. Software, however, is expanding at 21.77% CAGR as providers license middleware that translates diverse protocols into FHIR Observations, fueling analytics dashboards and population-health models. Services spanning installation, training, and managed security round out the mix. Subscription pricing is replacing one-time Box sales; Philips HealthSuite now charges per-bed fees that bundle storage, algorithm upgrades, and cyber patches. GE HealthCare Edison added Apple HealthKit connectivity in 2025, signaling convergence between consumer and clinical data sets.

Interoperability mandates such as the United States Trusted Exchange Framework and Common Agreement and the forthcoming European Health Data Space compel vendors to open APIs. Open-source EHRs are adding device connectors, lowering entry barriers for small clinics in emerging economies. Cybersecurity software tailored for medical IoT posts double-digit growth as hospitals adopt agentless scanning to flag rogue endpoints without touching regulated devices.

By Application: Home Care Surges on Reimbursement Tailwinds

Remote patient monitoring platforms held 37.75% share in 2024, aggregating vitals from home devices for chronic-disease oversight. Home care is the fastest-growing use case, with a 22.31% CAGR, following the expansion of Medicare Advantage reimbursements for remote physiologic and therapeutic monitoring under CPT codes 99453-58. Hospitals and nursing homes continue to rely on bedside telemetry; however, penalties for readmissions are pushing budgets toward post-discharge surveillance. Pharmaceuticals deploy connected inhalers and pill bottles in decentralized trials to verify adherence. Emergency medical services transmit electrocardiograms from ambulances, allowing catheterization labs to mobilize before arrival.

Private insurers follow public-payer policy moves. Humana now covers continuous glucose monitoring for all insulin users, adding roughly 2 million beneficiaries. Germany’s Digital Healthcare Act compels statutory insurers to reimburse digital applications, and similar frameworks are emerging in France and Spain. High broadband penetration in the United States, Canada, and Scandinavia supports the rapid adoption among aging populations that prefer aging in place over institutional care. HIPAA and GDPR compliance requirements drive encryption and on-device processing to satisfy data-minimization principles.

By End User: Consumer Adoption Outpaces Provider Upgrades

Providers made up 44.24% of 2024 spending, investing in Wi-Fi 6E, 5G cores, and EMR integrations. The patients and individuals segment is growing at the fastest rate, with a 20.87% CAGR, fueled by the clinical validation of smartwatches and patches that generate reimbursable data. The Apple Watch Series 9 has added sleep-apnea detection, gaining FDA De Novo clearance. The Samsung Galaxy Watch 6 has secured CE marking for its body-composition metrics. Payers ingest wearable data to stratify risk, yet device purchases still flow through consumer channels.

Interoperability hurdles persist because consumer platforms maintain proprietary clouds. The Sync for Science project launched FHIR-based donation paths, allowing patients to seamlessly port wearable observations into research and care workflows. Fitbit Health Solutions enables bulk data export for employer wellness programs. Direct-to-consumer glucose monitors, such as Abbott Lingo, expand the market beyond insulin users, blurring the boundaries between medical and wellness.

By Device Connectivity: 5G Slicing Drives Cellular Momentum

Wi-Fi and WLAN accounted for 38.45% of 2024 revenue, supporting hospital networks and home gateways. Cellular links are scaling at 21.63% CAGR as embedded SIM modules simplify logistics and 5G slicing guarantees latency. Bluetooth stays the dominant short-range link for body-worn sensors, while NB-IoT and LoRa address rural deployments that need multi-year battery life. Verizon’s 5G Edge offers healthcare slices priced above consumer plans but delivers near-real-time performance for robotic surgery. AT&T runs private 5G networks on Citizens Broadband Radio Service spectrum to isolate medical devices from guest traffic.

Regulatory moves hasten migration; the FCC sunsetted 3G in 2023, prompting manufacturers to upgrade legacy telemetry to LTE-M1 with over-the-air diagnostics. Remote SIM provisioning reduces field-service costs when devices cross borders, and battery-optimized 5G chipsets extend the life cycles of wearables.

Geography Analysis

North America led with 40.12% share in 2024 as CMS remote physiologic monitoring codes funnel USD 60 per patient per month to clinicians, creating predictable recurring revenue. More than 200 hospitals operate private Citizens Broadband Radio Service networks, and Wi-Fi 6E adoption accelerated once the FCC opened 1,200 MHz of 6 GHz spectrum. Canada funds satellite-backhauled telehealth for remote indigenous communities, while Mexico’s social-security institute equips tens of thousands of diabetes patients with cellular glucometers.

Asia-Pacific is the fastest-growing region at 22.56% CAGR. China’s Healthy China 2030 blueprint earmarks CNY 200 billion (USD 28 billion) for 5G ambulances and smart wards. India’s Ayushman Bharat Digital Mission mandates Fast Healthcare Interoperability Resources-based exchanges nationwide. Japan reimburses remote cardiac rehabilitation, South Korea invests KRW 500 billion (USD 375 million) in 5G hospital coverage, and Australia halves approval time for software-as-a-medical-device platforms.

Europe commands a sizable share under the Medical Device Regulation and GDPR rules, which channel funds into on-premises edge computing and federated learning architectures. Germany reimburses digital therapeutics, the United Kingdom mandates cybersecurity assessments in procurement, and France’s Health Data Hub expands to ingest wearable streams. Middle East and Africa gain momentum as Gulf sovereign funds build smart hospitals and Nigerian LoRa pilots scale maternal-health monitoring.

Competitive Landscape

Competition is fragmented as telecom carriers, device OEMs, and cloud giants overlap. AT&T and Verizon deploy millimeter-wave 5G slices but rely on integrators to bridge clinical workflow gaps. Cisco and Extreme Networks dominate the Wi-Fi market, yet they face pressure from open-source software that reduces capital expenditures. Qualcomm licenses modem IP to device makers even as Apple tightens vertical integration with custom radio silicon.

Cybersecurity-as-a-service for medical IoT is a ripe gap; managed service providers can offset the 60% staffing deficit in hospital SOCs. Start-ups like Particle Health aggregate wearable data via Fast Healthcare Interoperability Resources APIs and sell insights to payers, while Claroty adapts industrial OT security for hospital floors.

Zebra Technologies’ ultra-wideband location services displace legacy RFID, and Stryker’s System 8 wireless tools embed Bluetooth analytics for preventive maintenance. Spectrum liberalization in the Citizens Broadband Radio Service and 6 GHz bands lowers entry barriers for regional integrators, allowing them to establish private networks without carrier partnerships.

Wireless Communication Technologies In Healthcare Industry Leaders

Cisco Systems, Inc.

Apple Inc.

Honeywell International Inc.

Samsung Electronics Co., Ltd.

AT&T Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Qualcomm Snapdragon X75 5G modem received Global Certification Forum approval for Release 18 features, enabling cardiac devices to time-stamp events with sub-microsecond precision.

- February 2025: Medtronic launched Reveal LINQ II implantable monitor powered by a piezoelectric harvester, removing battery-replacement surgeries while sending Bluetooth 5.2 data to smartphones.

- January 2025: European Medicines Agency and United Kingdom MHRA mandated over-the-air firmware support for all Class IIb implantables, fast-tracking Bluetooth 5.4 encrypted broadcasts.

- December 2024: Google Cloud Healthcare API added DICOM-over-HTTPS streaming from wireless probes to PACS archives, cutting imaging latency in point-of-care settings.

Global Wireless Communication Technologies In Healthcare Market Report Scope

The Wireless Communication Technologies in Healthcare Market refers to the integration of wireless communication systems and technologies within the healthcare industry, enabling seamless data transfer, remote monitoring, and enhanced connectivity among devices, patients, and healthcare providers. These technologies play a crucial role in enhancing healthcare delivery, improving patient outcomes, and increasing operational efficiency.

The Wireless Communication Technologies in Healthcare Market Report is Segmented by Technology (Wireless Personal Area Network, Wi-Fi, Wireless Wide Area Network, Worldwide Interoperability for Microwave Access, Wireless Body Area Network), Component (Hardware, Software, Services), Application (Hospitals and Nursing Homes, Home Care, Pharmaceuticals, Remote Patient Monitoring Platforms, Other Applications), End User (Providers, Payers, Patients and Individuals), Device Connectivity (Bluetooth, Wi-Fi and WLAN, Cellular, LPWAN), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

By Technology

| Wireless Personal Area Network (WPAN) |

| Wi-Fi |

| Wireless Wide Area Network (WWAN) |

| Worldwide Interoperability for Microwave Access (WiMAX) |

| Wireless Body Area Network (WBAN) |

By Component

| Hardware |

| Software |

| Services |

By Application

| Hospitals and Nursing Homes |

| Home Care |

| Pharmaceuticals |

| Remote Patient Monitoring Platforms |

| Other Applications |

By End User

| Providers |

| Payers |

| Patients / Individuals |

By Device Connectivity

| Bluetooth |

| Wi-Fi / WLAN |

| Cellular (3G/4G/5G) |

| LPWAN (NB-IoT, LoRa) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Wireless Personal Area Network (WPAN) | ||

| Wi-Fi | |||

| Wireless Wide Area Network (WWAN) | |||

| Worldwide Interoperability for Microwave Access (WiMAX) | |||

| Wireless Body Area Network (WBAN) | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Application | Hospitals and Nursing Homes | ||

| Home Care | |||

| Pharmaceuticals | |||

| Remote Patient Monitoring Platforms | |||

| Other Applications | |||

| By End User | Providers | ||

| Payers | |||

| Patients / Individuals | |||

| By Device Connectivity | Bluetooth | ||

| Wi-Fi / WLAN | |||

| Cellular (3G/4G/5G) | |||

| LPWAN (NB-IoT, LoRa) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the wireless communication technologies in healthcare market today?

The market reached USD 197.19 billion in 2025 and is on track to approach USD 489.64 billion by 2030.

Which connectivity type is growing fastest in hospital use?

Cellular links, especially 5G with network slicing, are expanding at 21.63% CAGR as hospitals deploy private cores and embedded SIM devices.

What is propelling home-based remote monitoring adoption?

Expanded reimbursement under CMS CPT codes 99453-58 and private-payer coverage for devices such as continuous glucose monitors are driving a 22.31% CAGR in the home-care segment.

Why are hospitals investing in Wi-Fi 6E and Wi-Fi 7?

The 6 GHz band triples available channels, reduces interference, and supports high-bandwidth video and telemetry, solving congestion issues in legacy 2.4 GHz deployments.

Which regions will post the strongest growth through 2030?

Asia-Pacific leads with a projected 22.56% CAGR, lifted by large-scale digital-health funding in China, India, Japan, and South Korea.

What is the main cybersecurity challenge for wireless medical devices?

A global 60% shortage of qualified SOC analysts limits hospitals’ ability to implement zero-trust segmentation and continuous monitoring.

Page last updated on: