Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

The India Surveillance Storage Market Report is Segmented by Storage Architecture (NAS, SAN, DAS, and More), Storage Media (Surveillance HDD, and More), Deployment (On-Premise Edge, and More), Capacity Tier (≤4 TB, 4-8 TB, and More), Video Retention (≤30 Days, and More), Camera Resolution (≤2 MP, 2-5 MP, and More), End-User Vertical (Government, Defense, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

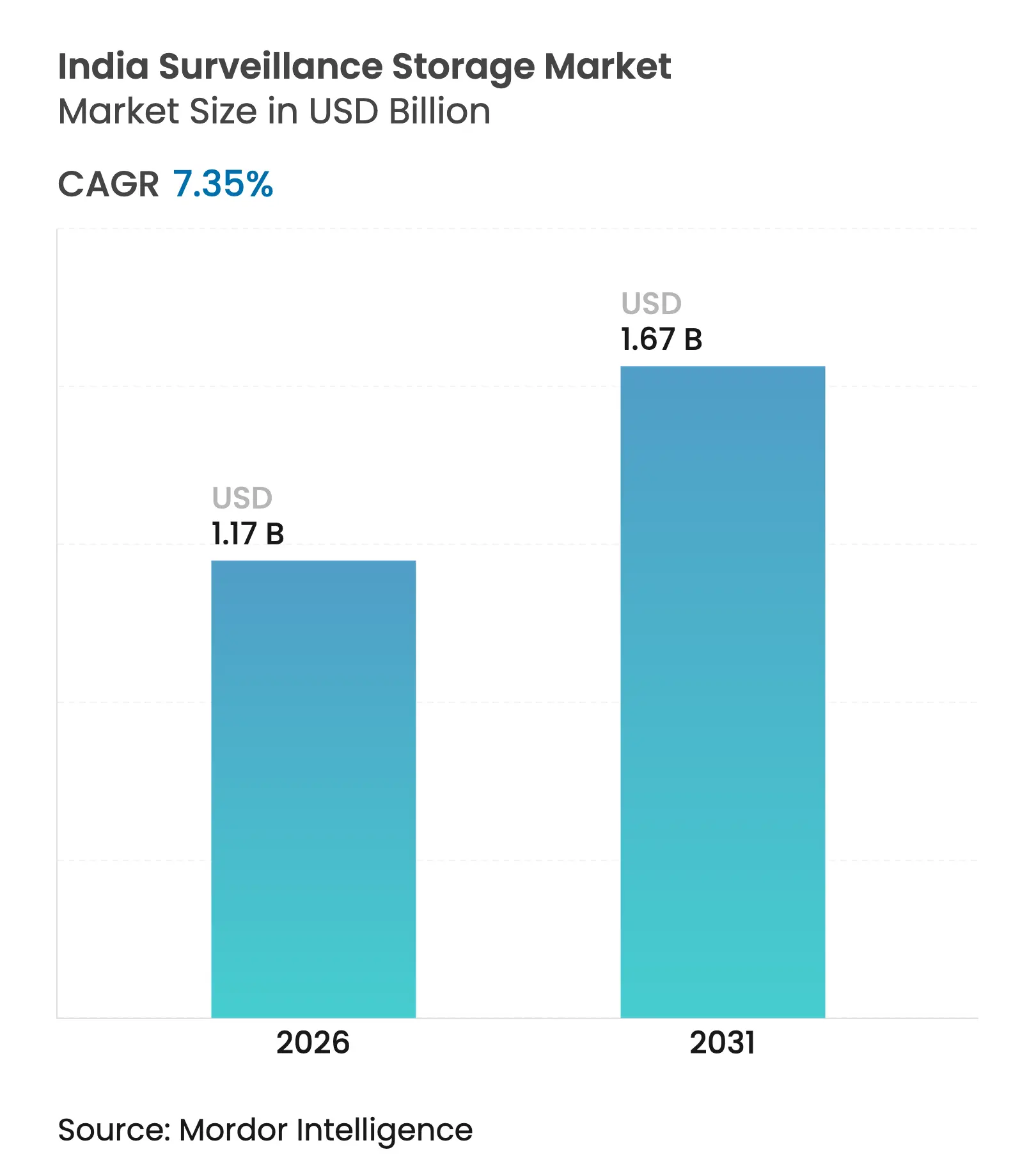

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 7.35 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The India surveillance storage market size is expected to grow from USD 1.09 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.67 billion by 2031 at 7.35% CAGR over 2026-2031. Demand is fueled by large-scale IP-camera roll-outs under the Smart Cities Mission, mandatory rail-coach video recording, and the shift toward AI-enabled analytics that multiply per-camera throughput requirements. Enterprises are prioritizing hyper-converged appliances and high-density drives to meet 90-day retention rules while minimizing rack footprint. On-premise arrays remain dominant as data-localization clauses discourage offshore cloud archiving, yet bandwidth improvements and tiered hybrid strategies are opening a controlled path to VSSaaS adoption. Pricing gains from ≥18 TB surveillance-grade HDDs and falling USD/TB metrics continue to improve total cost of ownership for large deployments.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government "Safe City" & Smart Cities projects accelerating large-scale IP camera roll-outs Government "Safe City" & Smart Cities projects accelerating large-scale IP camera roll-outs | +1.8% | National, with early gains in Delhi, Mumbai, Hyderabad | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:National, with early gains in Delhi, Mumbai, Hyderabad | Impact Timeline:Medium term (2-4 years) |

Mandatory on-board video surveillance for rail & metro coaches under Ministry of Railways Mandatory on-board video surveillance for rail & metro coaches under Ministry of Railways | +1.2% | National, concentrated in major railway corridors | Short term (≤ 2 years) | |||

Proliferation of 4K/8K and multi-sensor cameras quadrupling per-camera storage demand Proliferation of 4K/8K and multi-sensor cameras quadrupling per-camera storage demand | +2.1% | Urban centers, expanding to tier-2 cities | Medium term (2-4 years) | |||

Falling USD/TB for ≥18 TB surveillance-grade HDDs enabling 90-day retention compliance Falling USD/TB for ≥18 TB surveillance-grade HDDs enabling 90-day retention compliance | +1.4% | National, with higher impact in cost-sensitive segments | Short term (≤ 2 years) | |||

Edge-based AI analytics driving demand for high-IOPS on-prem storage nodes Edge-based AI analytics driving demand for high-IOPS on-prem storage nodes | +1.6% | Metropolitan areas, enterprise deployments | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Government “Safe City” & Smart Cities Projects Accelerating Large-Scale IP Camera Roll-Outs

Urban surveillance grids under the Smart Cities Mission continue to set the cadence for the India surveillance storage market. Budgetary outlays exceeding USD 550 million for the IndiaAI program in 2024-25 signal firm national commitment to AI-ready video infrastructure.[1]IndiaAI Secretariat, “Union budget 2024-25 allocates over 550 crores to the IndiaAI mission,” indiaai.gov.inMunicipal authorities in Hyderabad and Pune now specify STQC-certified storage back-ends, driving local vendor participation. Facial-recognition workloads enlarge daily ingest volumes, necessitating hyper-converged clusters that pool compute and storage for analytics in near real time. Cities are pairing IP-camera feeds with IoT sensor telemetry, creating multi-structured datasets that demand tiered retention policies. Collectively, these deployments reinforce the India surveillance storage market’s medium-term growth trajectory.

Mandatory On-Board Video Surveillance for Rail & Metro Coaches

Indian Railways’ fleetwide directive for IP-based recording adds thousands of rolling nodes to the India surveillance storage market. Each coach produces 2-4 TB of footage monthly, creating a centralized demand for NAS arrays capable of interfacing with disparate route bandwidths. Continuous recording requirements have accelerated procurement of surveillance-grade HDDs rated for 550 TB workloads. Edge buffers installed inside coaches ensure fail-safe capture during link outages, then synchronize to core repositories at station yards. The roll-out’s aggressive schedule supports a pronounced short-term spike in storage shipments.

Proliferation of 4K/8K & Multi-Sensor Cameras Quadrupling Per-Camera Storage Demand

Enterprises upgrading from 2 MP streams to 4K imaging are experiencing a four-fold expansion in daily data pools. Although H.265 encoding trims bandwidth by 40-50%, the sheer frame-size increase still drives aggregate capacity upward. Multi-sensor devices blend thermal, panoramic, and optical feeds, pushing heterogeneous write patterns that challenge legacy file systems. Airports deploying AI-based queue analytics now balance SSD tiers for inference with HDD tiers for bulk retention, accelerating convergence in storage design. These conditions solidify demand elasticity across high-density media offerings.

Edge-Based AI Analytics Driving Demand for High-IOPS On-Prem Storage Nodes

Inference workloads executed at network edges require sub-millisecond read-write profiles. NVMe SSDs coupled with GPU modules are emerging as the de facto configuration for metropolitan command centers. The EIQIS framework confirms that distributed indexing reduces core-datacenter bandwidth by carrying out first-level analytics locally.[2]arXiv Authors, “EIQIS: Toward an Event-Oriented Indexable and Queryable Intelligent Surveillance System,” arxiv.orgOrganizations are therefore adopting hybrid nodes that mix SSD front-ends with HDD bulk tiers, ensuring sustained throughput during AI bursts without inflating overall cost curves.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Power/network unreliability in tier-3/4 cities inflating TCO of on-prem arrays Power/network unreliability in tier-3/4 cities inflating TCO of on-prem arrays | -1.3% | Tier-3/4 cities, rural deployment areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.3% | Geographic Relevance:Tier-3/4 cities, rural deployment areas | Impact Timeline:Medium term (2-4 years) |

Data-localisation clauses in Digital Personal Data Protection Act limiting offshore cloud archival Data-localisation clauses in Digital Personal Data Protection Act limiting offshore cloud archival | -0.8% | National, affecting multinational enterprises | Short term (≤ 2 years) | |||

Budget diversion to cyber-hardening delays storage refresh in public sector Budget diversion to cyber-hardening delays storage refresh in public sector | -0.9% | Government and public sector deployments | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Power/Network Unreliability in Tier-3/4 Cities Inflating TCO of On-Prem Arrays

Voltage instability outside metropolitan hubs raises capex by 25-40% for UPS systems and diesel-backup units. Redundant microwave or fiber paths are equally essential where terrestrial links fail, compounding opex. Retail and manufacturing chains with dispersed footprints often downgrade to lower-resolution recording or shorter retention cycles to conserve capacity. These cost headwinds moderate near-term roll-outs, tempering the India surveillance storage market’s otherwise robust growth in underserved regions.

Data-Localisation Clauses in Digital Personal Data Protection Act Limiting Offshore Cloud Archival

Draft rules published in January 2025 reinforce that sensitive personal video must reside on domestic soil.[3]Ministry of Electronics & IT, “MeitY releases Draft Digital Personal Data Protection Rules, 2025 for public consultation,” pib.gov.inMultinationals accustomed to regional-hub clouds are reallocating budgets to on-prem arrays or local co-location sites. VSSaaS providers are responding with “trusted-region” availability zones, yet uncertainty around future whitelist changes encourages a measured adoption curve. In the interim, the India surveillance storage industry is witnessing hybrid architectures that retain the last 30 days on-prem while replicating only anonymized or low-frame footage to cloud tiers.

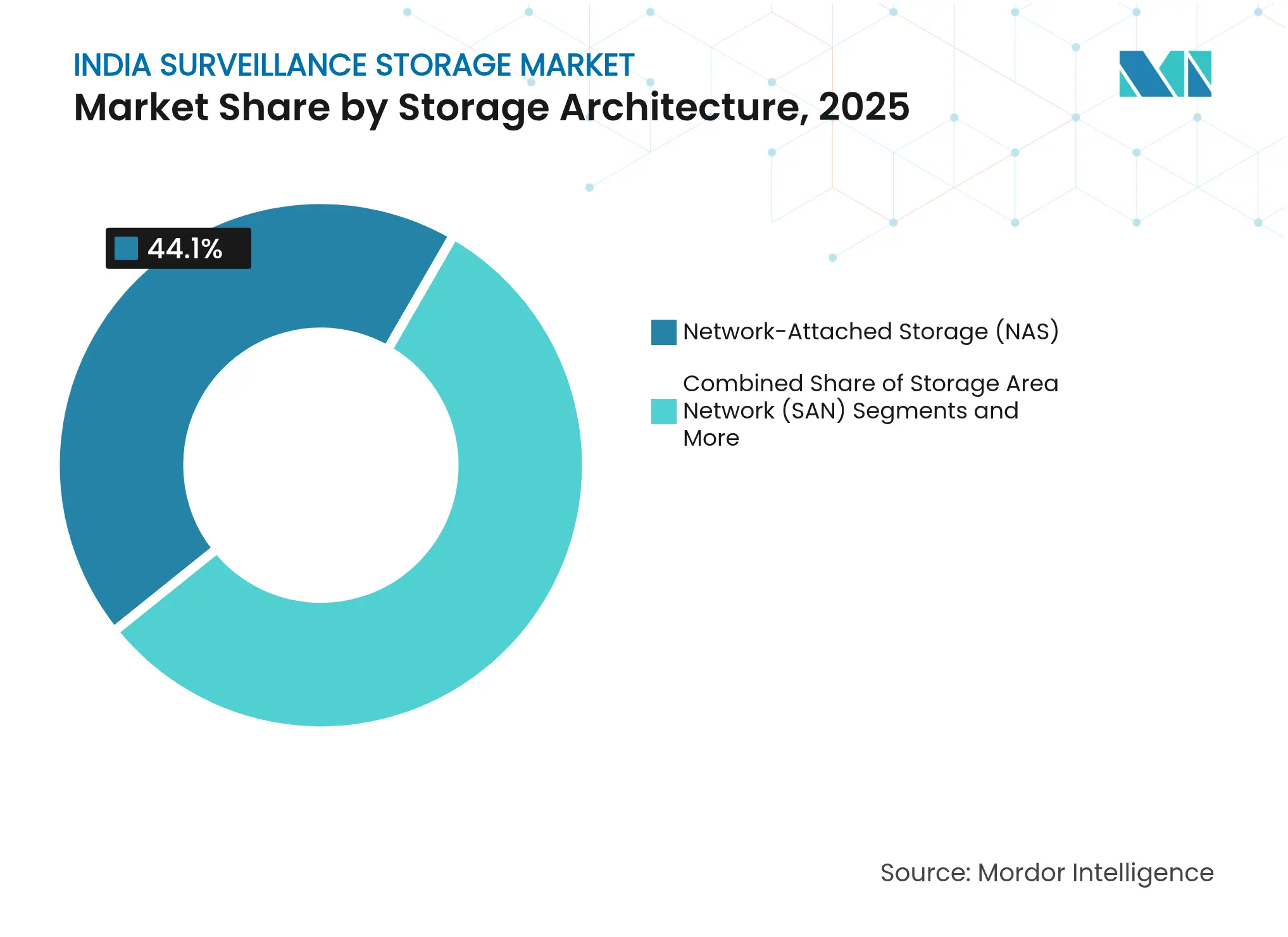

By Storage Architecture: NAS Dominance Faces Convergence Challenge

NAS arrays captured 44.10% of 2025 revenue, anchoring the India surveillance storage market with easy-to-scale, file-level access. Small and mid-sized enterprises prefer these appliances for their plug-and-play format and compatibility with IP-camera RTSP streams. SAN deployments retain relevance where throughput must exceed 10 Gb/s, notably in aviation control rooms and large malls. DAS remains niche, dedicated to isolated kiosks or ATMs with poor backhaul.

Hyper-converged systems are advancing at an 8.02% CAGR, outpacing conventional stacks as AI workloads converge compute and storage. Vendors bundle scale-out file systems, GPU accelerators, and policy-driven tiering to lower management overhead. This shift aligns with serviceability expectations in the India surveillance storage market, where lean IT teams value a single pane of glass for updates, analytics, and capacity adds.

Note: Segment shares of all individual segments available upon report purchase

By Storage Media: HDD Supremacy Challenged by SSD Performance Demands

Surveillance-grade HDDs hold 79.95% revenue share thanks to their USD/TB edge and 550 TB annual workload ratings. Enterprise SATA variants trail slightly, serving budget-centric roll-outs. SATA SSDs occupy a growing niche in applications requiring rapid data access for forensic analysis and real-time video processing.

NVMe SSD adoption is accelerating at 9.18% CAGR as AI inferencing requires sustained 1 M IOPS targets. Hybrid flash arrays combine these media types, auto-tiering hot clips to SSD while archiving cold streams to high-capacity HDDs. Future-proof roadmaps—such as Seagate’s Mozaic 3+ platform—indicate 3 TB-per-disk densities that will compress rack counts further seagate.com. Hybrid Flash Arrays represent a compromise solution, combining SSD performance for active data with HDD capacity for archival storage, appealing to organizations seeking to optimize both performance and cost.

By Deployment: On-Premise Preference Amid Cloud Transition

Local arrays comprised 67.55% of India surveillance storage market share in 2025 as CIOs prioritize control, low latency, and DPDP compliance. Core-datacenter clusters handle metropolitan mesh networks, while edge recorders address remote locations with intermittent connectivity. Public-cloud VSSaaS, expanding at 8.74% CAGR, is most attractive to SMEs that lack data-center space. Hybrid blueprints place critical first-day footage onsite and offload older clips to domestic hyperscale zones, balancing resilience with cost.

Private and hybrid cloud deployments offer compromise solutions that balance control with scalability, particularly appealing to organizations with distributed operations requiring centralized management capabilities. The India surveillance storage industry is also witnessing managed-service models where integrators host private clouds inside regional colocation hubs, giving enterprises SLA-backed uptime without surrendering sovereignty.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Capacity Tier: Enterprise Gravitates Toward High-Density Solutions

Arrays in the 10-100 TB band led with 39.15% revenue in 2025, striking cost-versus-management equilibrium for distributed offices. Yet >16 TB configurations are rising fastest at 9.22% CAGR as 4K/8K retention windows expand to 90 days. Consolidating into fewer high-density chassis reduces power and cooling overhead, a strategic imperative in power-capped Indian data halls. Vendors now bundle embedded analytics that flag spindle imbalances, pre-empting downtime in mission-critical deployments.

The trend toward higher-capacity storage reflects the economics of surveillance data management, where consolidating storage reduces per-terabyte costs and simplifies system administration. Large-scale deployments increasingly favor high-density storage configurations that minimize physical footprint while maximizing capacity utilization.

By Video Retention Requirement: Compliance Drives Extended Storage

Short-term retention periods (≤30 days) dominate with 51.35% market share in 2025, reflecting the baseline requirements for most commercial surveillance applications. The 30-90 day retention segment serves enterprises with enhanced security requirements or regulatory compliance obligations. Organizations in this tier typically implement tiered storage strategies that migrate older footage to lower-cost storage media while maintaining recent recordings on high-performance systems.

Retention periods exceeding 90 days represent the fastest-growing segment at 8.01% CAGR (2026-2031), driven by regulatory compliance requirements in banking, healthcare, and government sectors. The trend toward extended retention reflects the growing recognition of video surveillance as a critical business intelligence tool rather than merely a security measure.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

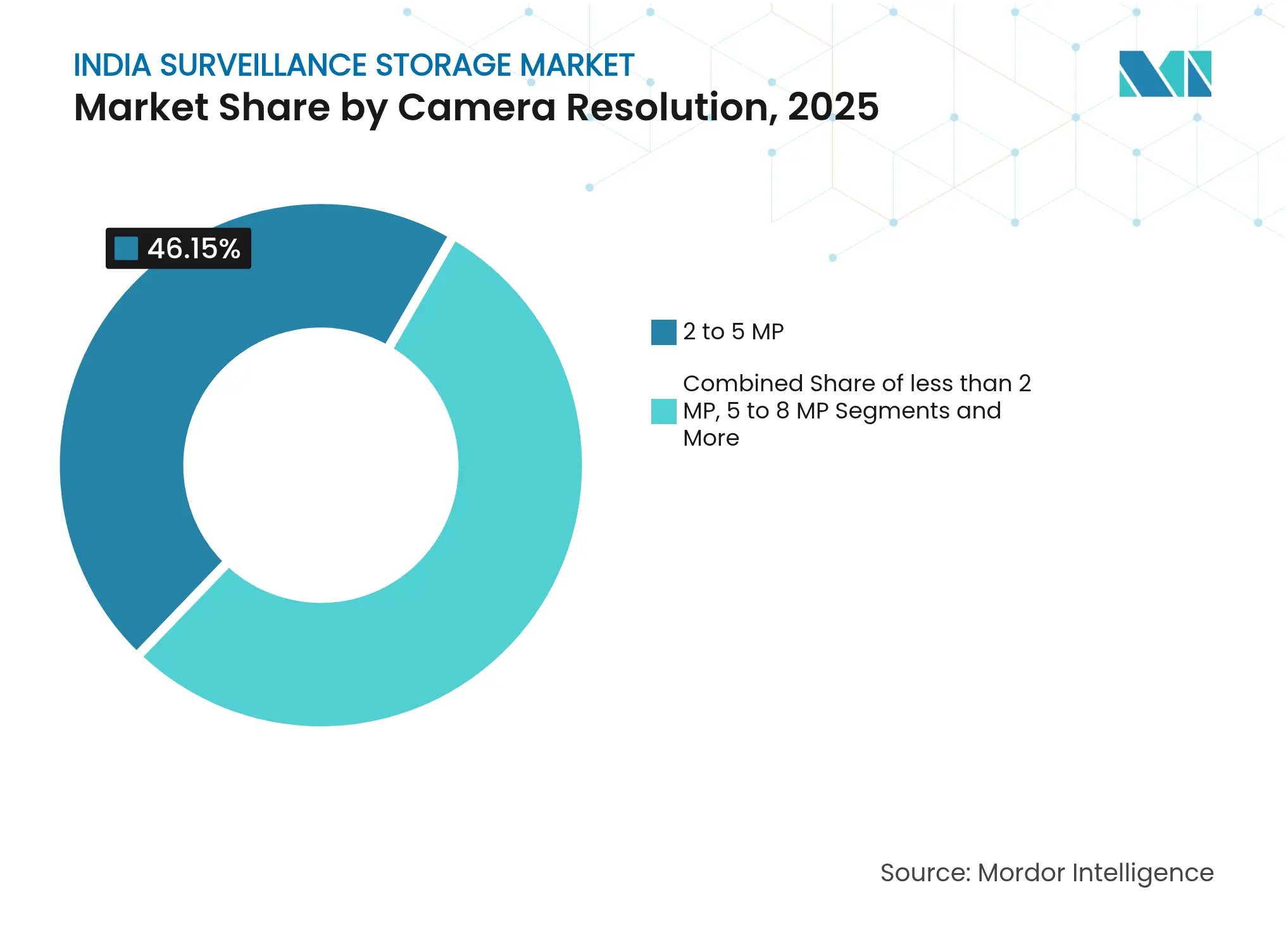

By Camera Resolution: Ultra-HD Adoption Accelerates Storage Demands

High-resolution camera support (>8 MP/4K) emerges as the fastest-growing segment at 8.12% CAGR (2026-2031), reflecting the market's transition toward ultra-high-definition surveillance systems. Lower resolution tiers (≤2 MP, 2-5 MP, and 5-8 MP) continue serving cost-sensitive applications where image quality requirements are less stringent. The resolution progression directly correlates with storage capacity requirements, as 4K cameras generate approximately four times the data volume of 1080p equivalents.

The ultra-HD segment's growth is driven by applications requiring detailed forensic analysis, such as facial recognition and license plate identification systems. Advanced compression technologies like H.265/HEVC are partially mitigating storage requirements, though the fundamental data volume increase remains substantial.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Government Leadership Faces Private Sector Challenge

Government and Smart City deployments maintain the largest market share at 28.10% in 2025, reflecting massive public sector investments in surveillance infrastructure. Public Safety and Defense applications represent the second-largest segment, driven by national security requirements and border surveillance initiatives. BFSI (Banking, Financial Services, and Insurance) sector deployments focus on fraud prevention and regulatory compliance, requiring high-reliability storage systems with extended retention capabilities.

Transportation and Logistics emerges as the fastest-growing end-user vertical at 8.29% CAGR (2026-2031), driven by comprehensive surveillance implementations across airports, seaports, and highway infrastructure. The National Highways Authority of India's video-based surveillance system at toll plazas exemplifies the sector's commitment to comprehensive monitoring capabilities Diigo.

Tier-1 metros—Delhi, Mumbai, and Bangalore—accounted for 44.30% of 2025 spending as fiber density, datacenter availability, and higher per-capita income lift surveillance adoption. Western and northern industrial belts, including Gujarat and Haryana, favor hyper-converged nodes that collocate analytics with storage to shorten incident response. Southern tech hubs such as Hyderabad lead in AI-assisted traffic analytics, further deepening the India surveillance storage market’s sophistication curve.

Smart-city funding is catalyzing tier-2 clusters—Pune, Chandigarh, and Jaipur—where municipal command-and-control centers standardize on STQC-approved platforms. Conversely, eastern corridors contend with power volatility; integrators deploy low-RPM archival drives with solar-backup arrays to sustain 24/7 capture. Across hinterland roll-outs, enterprises prefer NAS arrays with simplified UI owing to limited in-house IT expertise.

5G backbone upgrades will widen cloud-connected deployments from 2026 onward, enabling bandwidth-efficient edge-to-core replication. Regions with reliable power are poised to leapfrog directly into hybrid-flash architectures, while tier-3 markets will mature at a measured pace as infrastructure catches up.

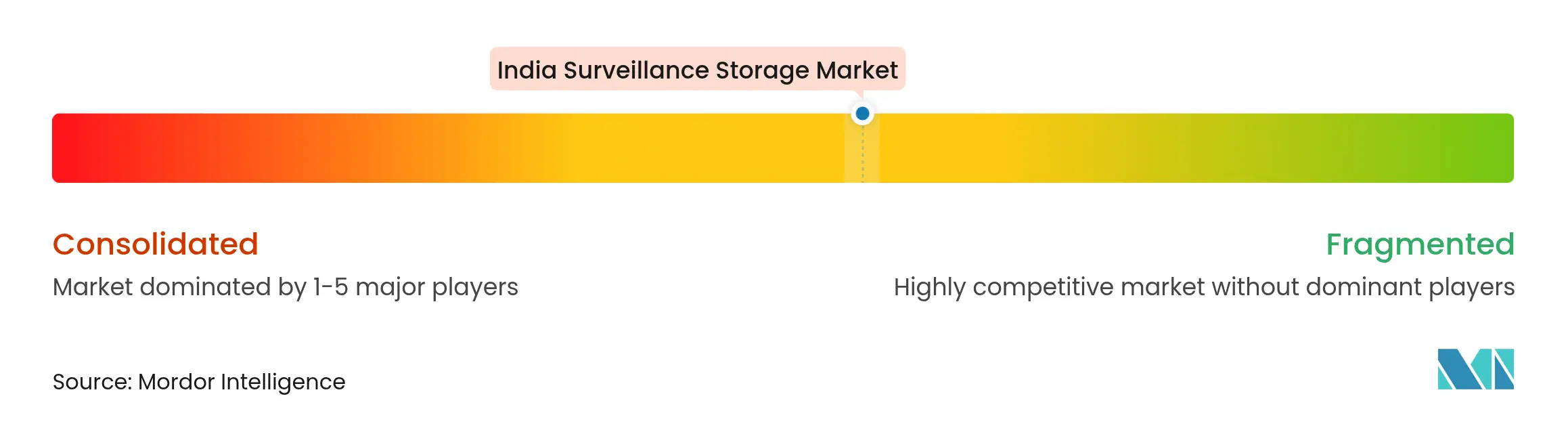

Market Concentration

The India surveillance storage market remains moderately fragmented: the top five brands jointly control an estimated 35-40% revenue, leaving space for specialized integrators. Western Digital and Seagate leverage vertical-integration and HDD roadmaps to maintain incumbency, while Promise Technology and QSAN position hyper-converged bundles for AI workloads. Domestic vendors such as CP Plus are capitalizing on BIS/STQC mandates, ramping monthly output to 2.5 million units to replace restricted Chinese gear.

Strategic alliances between camera OEMs and storage vendors streamline end-to-end certification, reducing project-bid friction. Vendors now emphasize NVMe-ready architectures and GPU pass-through to secure share in analytics-heavy bids. Managed-service providers bundle storage with VMS licenses, pushing competition toward recurring-revenue models over one-time box sales.

M&A chatter is intensifying as mid-tier arrays specialists seek capital to localize manufacturing under the Production-Linked Incentive scheme. Success will hinge on productized AI pipelines, seamless scalability, and demonstrable DPDP compliance.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Surveillance systems refer to a combination of recording devices installed for surveillance to prevent crime in private and public locations. Data storage is a critical component of the surveillance infrastructure. The scope and the market size only cover the video surveillance storage market.

The India surveillance storage market is segmented by product (NAS, SAN, and DAS), storage media (HDD and SSD), deployment (cloud and on-premise), and end-user vertical (government and defense, education, BFSI, retail, transportation and logistics, healthcare, home security, and other end-user verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.