Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

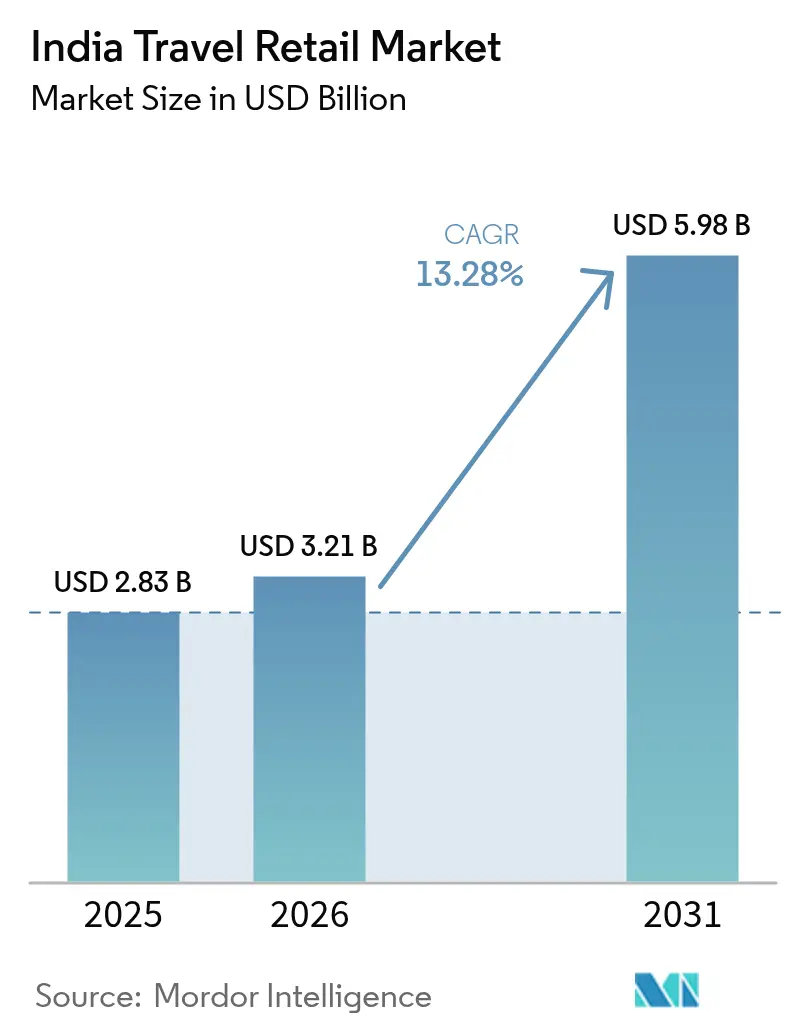

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 5.98 Billion |

| Growth Rate (2026 - 2031) | 13.28% CAGR |

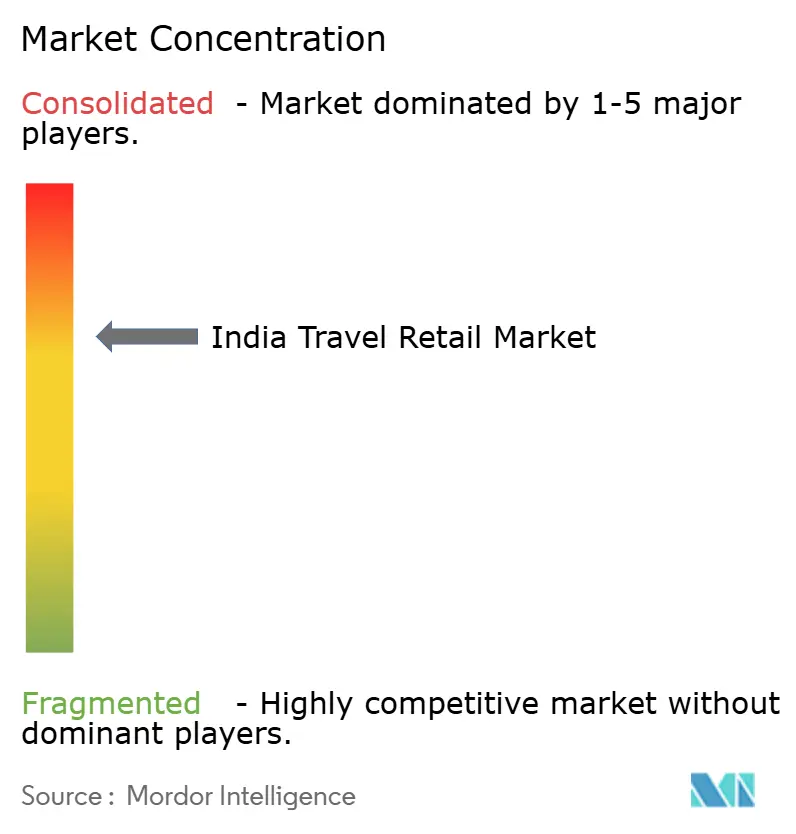

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Travel Retail Market Analysis by Mordor Intelligence

The Indian travel retail market size was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.21 billion in 2026 to reach USD 5.98 billion by 2031, at a CAGR of 13.28% during the forecast period (2026-2031), reflecting a robust demand cycle anchored in airport-led distribution and premium category depth. A key near-term catalyst is the revision of Baggage Rules effective February 2, 2026, which raised the duty-free allowance for Indian residents to USD 834.74 (INR 75,000), supporting higher ticket baskets for premium goods. At the same time, large public investments in terminal capacity and airside operations are dispersing footfall across more locations, which strengthens store productivity and brand activation quality. Digital pre-order and airside pickup continue to reduce friction for time-constrained travelers by ensuring availability and faster gate handovers. These shifts together reinforce multi-year growth in the India travel retail market as operators refine their assortments, loyalty integrations, and checkout journeys to match evolving traveler profiles.

Key Report Takeaways

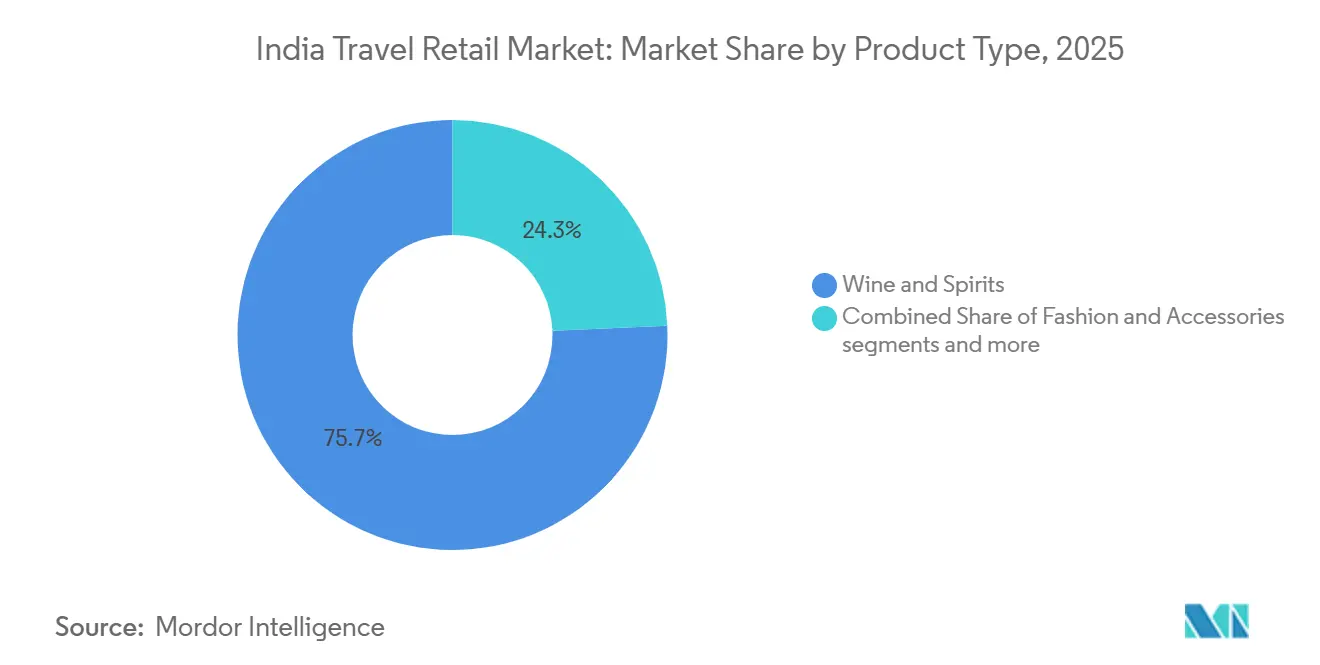

- By product type, Wine and Spirits led with 75.68% of the India travel retail market share in 2025; Fragrances and Cosmetics are forecast to expand at a 14.92% CAGR to 2031.

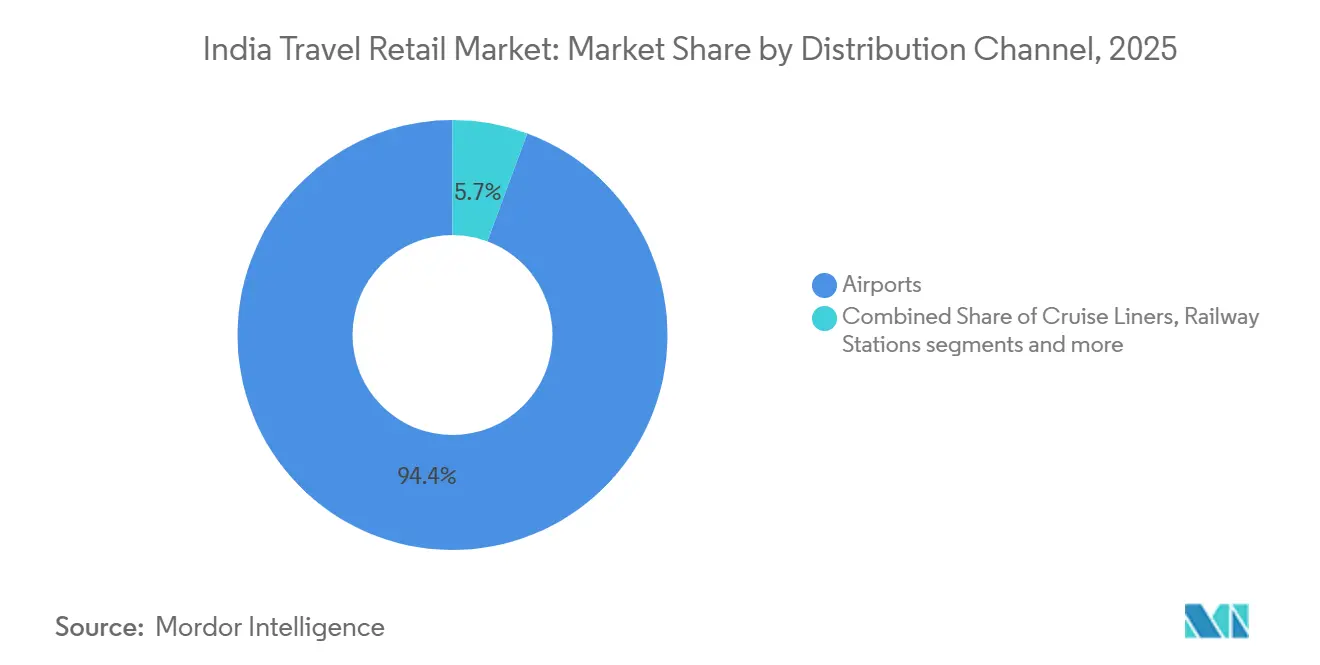

- By distribution channel, Airports held 94.35% of the India travel retail market share in 2025, while Cruise Liners are projected to record the highest CAGR at 18.55% through 2031.

- By traveler demographics, Leisure Travelers accounted for 40.88% of the India travel retail market share in 2025, while Student Travelers are projected to grow at a 13.46% CAGR through 2031.

- By geography, North India accounted for 30.85% of the India travel retail market share in 2025, while South India is projected to expand at an 11.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of airport capacities in tier-2 cities | +2.1% | National, early gains in Tier-2/3 corridors (Varanasi, Bagdogra, Jodhpur, Udaipur) | Medium term (2-4 years) |

| Indian outbound leisure traffic to surge post-2025 | +3.5% | National, the highest in West India (12.2% CAGR) and North India (11.8% CAGR) | Long term (≥ 4 years) |

| FDI-driven upgrades in duty-free retail formats | +1.8% | National, concentrated in metro airports (Delhi, Mumbai, Bengaluru) | Short term (≤ 2 years) |

| Premiumization of Indian spirits and craft liquor | +2.3% | Global with spill-over to outbound travelers, domestic craft hubs (Goa, Bengaluru) | Medium term (2-4 years) |

| Increased adoption of digital payment wallets | +1.6% | National, led by UPI adoption at major airports, and select international acceptance. | Short term (≤ 2 years) |

| Expansion of loyalty coalitions between airlines and retailers | +0.9% | National with international airline partnerships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Airport Capacities in Tier-2 Cities

India’s airport operator has committed to 50 development projects through FY 2028-29, which will add new gates, terminals, and aprons in Tier-2 and Tier-3 corridors to distribute passenger flows previously concentrated in metros. The national build-out aims to scale India to 350 airports by 2047, embedding retail adjacencies earlier in terminal design and elevating the baseline for airside store productivity [1]Economic Times Travel, “India plans to build 350 airports by 2047, says Aviation Minister Naidu at Davos 2026,” Economic Times Travel, travel.economictimes.indiatimes.com. Safety incidents at large hubs in January and February 2026 highlighted the operational strain on congested metros, strengthening the case for diversifying throughput across regional gateways that can add fresh concession capacity. This capacity pivot supports the India Travel Retail Market by enlarging the pool of travel nodes where duty-free and specialty retail can scale with right-sized footprints and faster pre-order pickup lanes.

Indian Outbound Leisure Traffic to Surge Post-2025

Indian nationals recorded 30.89 million departures in 2024, and air travel accounted for 98% of those departures, positioning airports as the primary setting for discretionary purchases tied to international travel [2]Ministry of Tourism, Government of India, “Indian Nationals’ Departures 2024,” Ministry of Tourism, tourism.gov.in. Delhi processed 23.97% of total departures, followed by Mumbai at 20.16% and Cochin at 7.48%, and these concentrations align with the largest footprints for premium spirits and beauty at airside stores. The structure of leisure itineraries favors pre-order behavior for gifts and premium SKUs, and this behavior is now supported by click-and-collect services that reduce checkout time to a few minutes. Airlines are adding or resuming long-haul links that channel more outbound leisure traffic through hub concourses where retail windows align with departure banks. These patterns sustain a multi-year runway for the India Travel Retail Market as leisure travel broadens across destinations and deepens spend in categories with strong store-level curation.

Increased Adoption of Digital Payment Wallets

UPI One World went live at New Delhi International Airport in February 2026, with per-transaction and monthly wallet caps for foreign delegates, reducing friction from currency conversion and card network fees at checkout [3]The Economic Times Staff, “UPI ‘One World’ Launch at New Delhi Airport,” The Economic Times, economictimes.indiatimes.com. Cross-border acceptance gained traction when Qatar Duty Free enabled UPI in 2025, reinforcing the habit among Indian travelers of preferring wallet payments for smaller discretionary purchases. Smoother payments pair well with pre-order because they allow a faster handover window near gates and lower the risk of queue abandonment during peak departure waves. Bengaluru handles 130,000 passengers and 100,000 vehicles daily, and curbside lane management helps reduce landside wait times, allowing more time to be devoted to airside browsing and pickup. This digital shift supports higher conversion rates and faster transaction velocity at congested terminals in the India Travel Retail Market.

Expansion of Loyalty Coalitions Between Airlines and Retailers

Etihad Guest added 250,000 new members per month in India during 2025 and announced five India-focused partnerships in January 2026, spanning credit cards, department store loyalty, food delivery, e-commerce coin exchange, and boutique hotels [4]Etihad Airways Corporate Communications, “Etihad Guest India Partnership Updates,” Etihad Airways, etihad.com. The airline operates 185 weekly flights to 11 Indian gateways, which provides a large funnel to seed targeted retail offers linked to flight itineraries. Coalition benefits that let travelers earn or redeem points on airport purchases boost perceived value and increase average basket sizes during peak periods. Retailers inside airports are reinforcing this playbook by opening new beauty and fashion outlets sized for fast-moving categories and younger shopper cohorts. These partnerships expand reach and strengthen conversion levers across the India Travel Retail Market without requiring equal increases in floor area.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High customs duties are impacting non-duty-free pricing | -1.7% | National, acute in luxury goods | Medium term (2-4 years) |

| Regulatory uncertainty in tobacco and liquor allowances | -0.9% | National, selected categories | Short term (≤ 2 years) |

| Congested metro airports are reducing passenger dwell time | -1.2% | Mumbai, Delhi, Bengaluru | Short term (≤ 2 years) |

| Counterfeit risks are hindering luxury brand stores expansion | -1.4% | National, higher sensitivity in beauty and fashion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Customs Duties are Impacting Non-Duty-Free Pricing

The incentive to defer purchases to airport stores narrows when domestic channels offer competitive pricing in some categories, thereby reducing the effectiveness of duty-free as a pure price play. The 50% allowance increase that took effect in February 2026 improves headroom for premium baskets inside the duty-free cap, although the impact is uneven across categories. Operators are responding by leaning on limited editions, first-to-market placements, and curated bundles that cannot be matched in domestic channels. The United Kingdom-India trade track, which envisages staged tariff reductions for select premium spirits, would gradually narrow price gaps and increase the importance of exclusivity and service. These shifts keep assortment strategy and activation quality central to differentiation within the India Travel Retail Market.

Regulatory Uncertainty in Tobacco and Liquor Allowances

Baggage Rules 2026 enforce firm limits on alcohol volume and cigarette stick counts, and breaches can trigger seizure or punitive duty assessment, which complicates multi-unit purchases. Interpretive ambiguities on mixed bottle sizes and alternatives like cigars or loose tobacco raise compliance risk for travelers who plan purchases across connecting airports. Duty-free operators respond with compliant bundles and clearer shelf signage to reduce the risk of over-limit baskets. Operators also integrate pre-order guidance to flag allowance constraints before checkout, allowing adjustments to be made without delaying boarding. These measures moderate, but do not eliminate, demand friction in the India Travel Retail Market for the affected categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirits Anchor Share, Cosmetics Lead Growth

Wine and Spirits accounted for 75.68% in 2025, positioning the category as the anchor of the India Travel Retail Market across major hubs, with deeper premium assortments and strong trade-up rates. The India Travel Retail market share lead in Wine and Spirits is reinforced by Indian single malts gaining domestic leadership in 2024 and rising in global rankings, elevating brand credibility at airside stores. Amrut Expedition 15-year secured a top-tier placement in global whisky guides, which supports price realization and halo effects for other premium SKUs on the shelf. Operators at Delhi consolidated control across the concession in December 2025, which improves the ability to match premium bottle availability to high-yield flights. These tactics sustain category density and aid cross-selling to travelers buying for both gifting and personal consumption inside the India Travel Retail Market.

Fragrances and Cosmetics is the fastest-growing line from 2026 to 2031 at a 14.92% CAGR, supported by broader assortments and quick-serve consultation formats that translate well in tight dwell times. The India Travel Retail market for Fragrances and Cosmetics is expanding as stores add more travel sets and discovery kits that align with outbound gifting needs. Food and Confectionery maintain steady impulse sales that complement larger-ticket baskets without requiring long browsing time. Tobacco encounters compliance ceilings that limit multi-unit bundles even when category interest persists. Fashion and Accessories performance depends on exclusives and personalization that differentiate from domestic e-commerce options in the India Travel Retail Market.

By Distribution Channel: Airports Dominate, Cruises Scale Fast

Airports accounted for 94.35% of distribution in 2025, which aligns with the 98% air modal share for outbound departures, and this concentration sustains the central role of terminals in premium-category sales. Delhi’s 23.97% share of all departures, Mumbai’s 20.16%, and Cochin’s 7.48% underline the structure of channel leadership where larger hubs hold deeper and broader assortments. Express pickup and queue-aware layouts near security exits and gate clusters are improving throughput at peak departure banks. Capacity additions across 50 projects through FY 2028-29 will spread airport-based retail into new corridors and reduce sensitivity to single-hub bottlenecks. These shifts keep airports at the core of the India Travel Retail Market’s channel mix and revenue base.

Cruise Liners are projected to scale at an 18.55% CAGR through 2031, and longer dwell times on voyages support experiential curation and destination-led bundles that raise per-passenger spend. Railway Stations remain a modest base for international traffic, and formats there lean on modular kiosks and pre-order pickup to limit fixed costs. Other channels, such as select seaports and road border points, contribute niche volumes that benefit from targeted assortments when regulations are clear and flows are predictable. As airport capacity scales in Tier-2 markets, operators can deploy proven airside playbooks that group express pickup areas near high-traffic security chokepoints. This approach strengthens conversion and sales density across all high-traffic channels within the India Travel Retail Market.

By Traveler Demographics: Leisure Leads, Students Surge

Leisure Travelers held a 40.88% share in 2025, and this cohort favors premium spirits, beauty, and curated gifts that fit outbound itineraries and family visits. Airport stores capture this demand with bundles timed to seasonal peaks and route profiles that sustain basket size. Business Travelers deliver steady premium demand in short windows near gates, supported by express pickup and curated accessories. Visiting Friends and Relatives and Medical and Wellness Tourists contribute a stable volume that helps staffing and inventory cycles. Airlines and retailers coordinate promotions with peak outbound months to improve conversion and loyalty engagement in the India Travel Retail Market.

Student Travelers are projected to grow at a 13.46% CAGR through 2031, and this group adopts digital pre-order and wallet payments quickly to guarantee stock and minimize queue time. Device upgrades, skincare routines, and gift items are common use cases for reservation and fast collection at pickup desks. Coalition loyalty that rewards airport purchases improve value perception for budget-conscious students and can push add-on items into the basket. Clearer guidance on allowances during pre-orders reduces compliance anxiety for travelers connecting to strict downstream jurisdictions. These adjustments widen demographic coverage and support durable demand across the India Travel Retail Market.

Geography Analysis

North India’s share of leadership rests on Delhi’s role as an international gateway, which accounts for 30.85% of all national departures and underpins the breadth of premium categories at airside counters. Capacity programs across North Indian Tier-2 locations are underway, designed to reduce over-reliance on a single hub by adding multiple nodes to support concession growth. December 2025 controlling stake in Delhi Duty Free enables faster shelf rebalancing toward gates where specific flight mixes lift conversion in premium spirits and beauty. UPI One World at New Delhi builds a more inclusive acceptance stack for events and inbound visitor flows through transaction and monthly limits that are easy to communicate at tills. As Noida’s greenfield capacity phases in, the region will diversify retail demand across multiple terminals and reduce pinch points during peak waves for the India Travel Retail Market.

South India is projected to expand at an 11.74% CAGR through 2031 as terminals complete expansions that add gates and retail zones designed for higher throughput during departure banks. Chennai’s expansion improves the base for more beauty and premium spirits activations that rely on space for discovery and quick service, even in short shopping windows. Bengaluru’s curb control program handles 130,000 daily passengers and 100,000 vehicles, with lane management designed to reduce landside delays, which can indirectly increase the time available to complete airport purchases. Retailers are also moving toward express pickup zones placed near security exits and heavy-load gates to capture transactions in 2 to 3 minutes. These measures support higher conversion while maintaining flow during peak periods in the India Travel Retail Market.

West India contributes a large base because Mumbai handles 20.16% of national departures, but dual-hub dynamics are now in play after a greenfield platform entered phase one service in late 2025. Split traffic increases the need for brand exclusives and digitally visible pre-orders that travelers can reserve before they leave for the airport. Queue analytics can route travelers to pick-up points closer to their gates and help keep dwell times within a 3-to-5-minute window during rush periods. East and Central India are earlier in the cycle, but select stations posted double-digit traffic growth in late 2025, which suggests demand can materialize quickly once international routes are added. As AAI’s 50-project plan proceeds, these regions gain consistent frameworks for concession standards that help operators replicate formats across the India Travel Retail Market.

Competitive Landscape

The India Travel Retail Market has moderate consolidation at metro hubs, where a few integrated airport and concession operators manage prime footprints and shape activation calendars for premium categories. A December 2025 transaction raised a leading operator’s stake in Delhi Duty Free to 66.93% for USD 20.3 million, which aligns real estate planning with merchandising control. This structure improves shelf productivity and allows premium SKU allocation to flights with higher conversion propensity, guided by live manifests and gate assignments. International concessionaires bring brand relationships that complement domestic execution strengths, which support broader and deeper assortments at scale. These dynamics sustain premium positioning while accommodating traffic growth in the India Travel Retail Market.

Technology adoption differentiates performance, including queue forecasting, shopper-flow analytics, and smarter replenishment that keeps fast movers available during peak departure banks. E-commerce pre-order with airside pickup has become standard for high-intent buyers who want certainty and short handover windows at the gate. Airline-retailer loyalty coalitions extend their reach via airline apps and email channels, making it easier to attach targeted offers to specific itineraries. These programs helped an airline add 250,000 new India-based members each month in 2025, which expands the pool of shoppers who can be activated for airside purchases. Together, these tools support higher sales density per square foot for the India Travel Retail Market without proportional expansion in store area.

Category suppliers are reinforcing assortments through capacity investments and premium launches that align with airport retail strengths. Spirit portfolios are emphasizing premium Indian single malts that have received international recognition, which supports trade-up at the shelf. Beauty brands are adding travel sets and shade extensions tailored to gifting and personal use that sell well within 3 to 5-minute decision windows. Operators are also tightening quality systems and authentication to preserve shopper trust in high-value categories as storefront counts grow. These elements provide a stable base for competitive rivalry while enabling steady category growth in the India Travel Retail Market.

India Travel Retail Industry Leaders

Delhi Duty Free Services Pvt Ltd

Flemingo International

Mumbai Duty Free (DFS)

Bangalore Duty Free (BIAL)

Hyderabad Duty Free Retail Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UPI One World wallet launched at New Delhi International Airport for foreign delegates, with per-transaction and monthly wallet caps designed for air-side acceptance. The launch reduces friction from currency conversion and card network fees during checkout at duty-free stores. It also sets a framework for broader cross-border acceptance that aligns with Indian traveler preferences in the India Travel Retail Market.

- January 2026: Etihad Guest unveiled five India-focused partnerships spanning a co-branded credit card, department store loyalty, food delivery, e-commerce coin exchange, and luxury hotels. The airline added 250,000 India-based members each month in 2025 and operates 185 weekly flights to 11 Indian gateways. These moves expand reach for airside retail offers and increase earn-and-burn utility linked to airport purchases in the India Travel Retail Market.

- December 2025: GMR Airports acquired equity to lift its stake in Delhi Duty Free Services to 66.93% for USD 20.3 million and consolidated control over the country’s busiest hub concession. The platform reported revenue growth from FY 2023 to FY 2025, reflecting demand recovery and improved merchandising agility. The transaction supports faster shelf resets tied to flight mixes in the India Travel Retail Market.

- August 2025: Shoppers Stop opened a 9,053-square-foot store at Delhi Airport Terminal 1 to target connecting and domestic passengers with curated beauty and fashion. The placement increases touchpoints for beauty discovery and fast pickup before boarding.

India Travel Retail Market Report Scope

Travel retail refers to the sale of goods to international travelers in transit environments, including airports, seaports, train stations, cruise ships, and border zones. It comprises duty-free (tax-exempt) and duty-paid outlets, offering competitively priced products such as perfumes, cosmetics, luxury items, alcohol, tobacco, fashion, and confectionery due to reduced taxes.

The India travel retail market report is segmented by product type (fashion and accessories, wine and spirits, tobacco, food and confectionary, fragrances and cosmetics, other product types), distribution channel (airports, cruise liners, railway stations, other distribution channels), traveler demographics (business travelers, leisure travelers, visiting friends & relatives, medical & wellness tourists, student travelers), and geography (North India, South India, West India, East India, Central India). The market forecasts are provided in terms of value (USD).

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionary |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends & Relatives (VFR) |

| Medical & Wellness Tourists |

| Student Travelers |

By Geography

| North India |

| South India |

| West India |

| East India |

| Central India |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionary | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends & Relatives (VFR) | |

| Medical & Wellness Tourists | |

| Student Travelers | |

| By Geography | North India |

| South India | |

| West India | |

| East India | |

| Central India |

Key Questions Answered in the Report

What is the India Travel Retail market size in 2026 and the growth to 2031?

The India travel retail market was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.21 billion in 2026 to reach USD 5.98 billion by 2031, at a CAGR of 13.28%.

Which categories and channels lead sales in India's travel retail?

Wine and Spirits held 75.68% in 2025, and Airports accounted for 94.35% of distribution, with Cruise Liners projected to grow at 18.55% CAGR to 2031.

Which traveler cohorts drive the most value in airport shops?

Leisure Travelers accounted for 40.88% in 2025, and Student Travelers are projected to grow at a 13.46% CAGR through 2031 with strong adoption of pre-order and wallet payments.

Which regions in India contribute most to airport retail sales?

North India held 30.85% in 2025, with Delhi alone handling 23.97% of all departures, while South India is projected at 11.74% CAGR to 2031 on capacity additions.

What measures are improving conversion in busy terminals?

UPI wallet acceptance with per-transaction and monthly caps, express pickup counters, and queue-aware store layouts reduce checkout time and lifts conversion.

What recent moves by operators and airlines affect India's travel retail?

GMR lifted its stake in Delhi Duty Free to 66.93% for USD 20.3 million, and Etihad Guest added 250,000 members monthly in 2025, with five India-focused partnerships announced in 2026.

Page last updated on: