Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

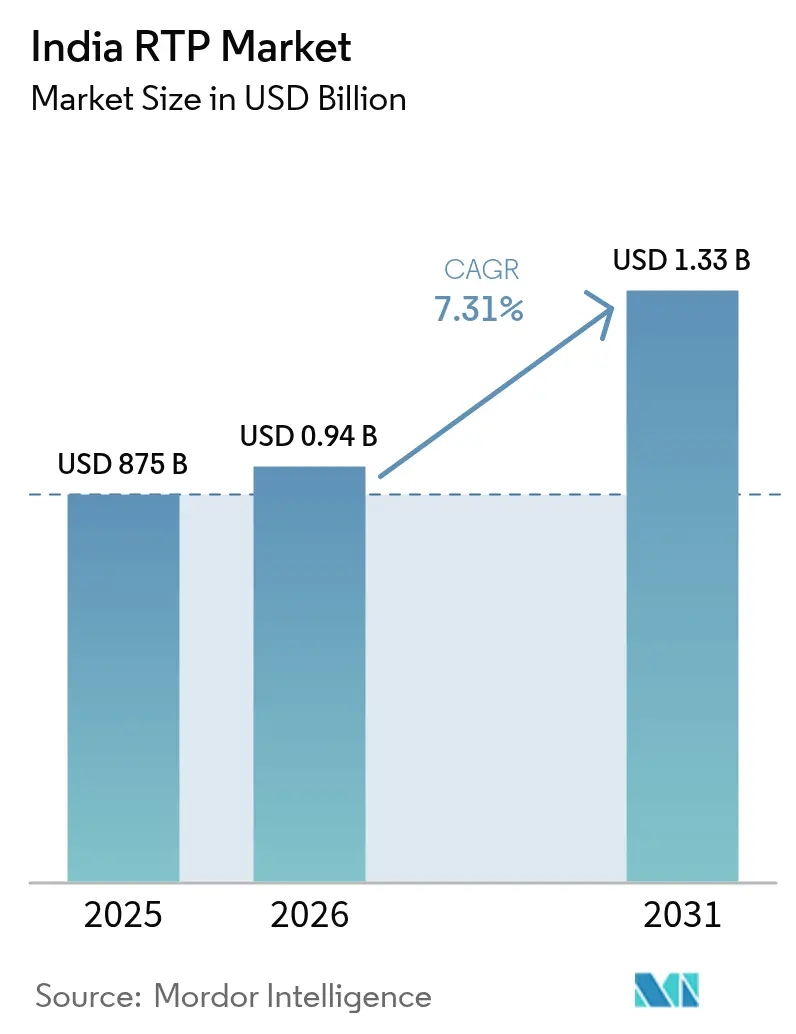

| Base Year Market Size (2025) | USD 875 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India RTP Market Analysis by Mordor Intelligence

The India returnable transport packaging market size was valued at USD 875 million in 2025 and estimated to grow from USD 938.96 million in 2026 to reach USD 1.33 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Rising regulatory pressure, especially the Extended Producer Responsibility (EPR) mandate that stipulates 30% recycled content in rigid plastics by April 2025, is accelerating the transition from single-use to multi-cycle assets. The rapid surge of e-commerce toward a USD 300 billion opportunity by 2030 is magnifying demand for pooled pallets, crates, and Intermediate Bulk Containers that can circulate across fragmented last-mile networks. Consolidation of asset pools, such as LEAP India’s acquisition of CHEP India, is adding scale efficiencies while embedding digital track-and-trace systems that curb an estimated 10% annual pallet loss rate. Meanwhile, the National Logistics Policy’s vision to trim logistics costs to global benchmarks by 2030 underpins infrastructure investments that facilitate faster asset turns and improved utilization across the India returnable transport packaging market.

Key Report Takeaways

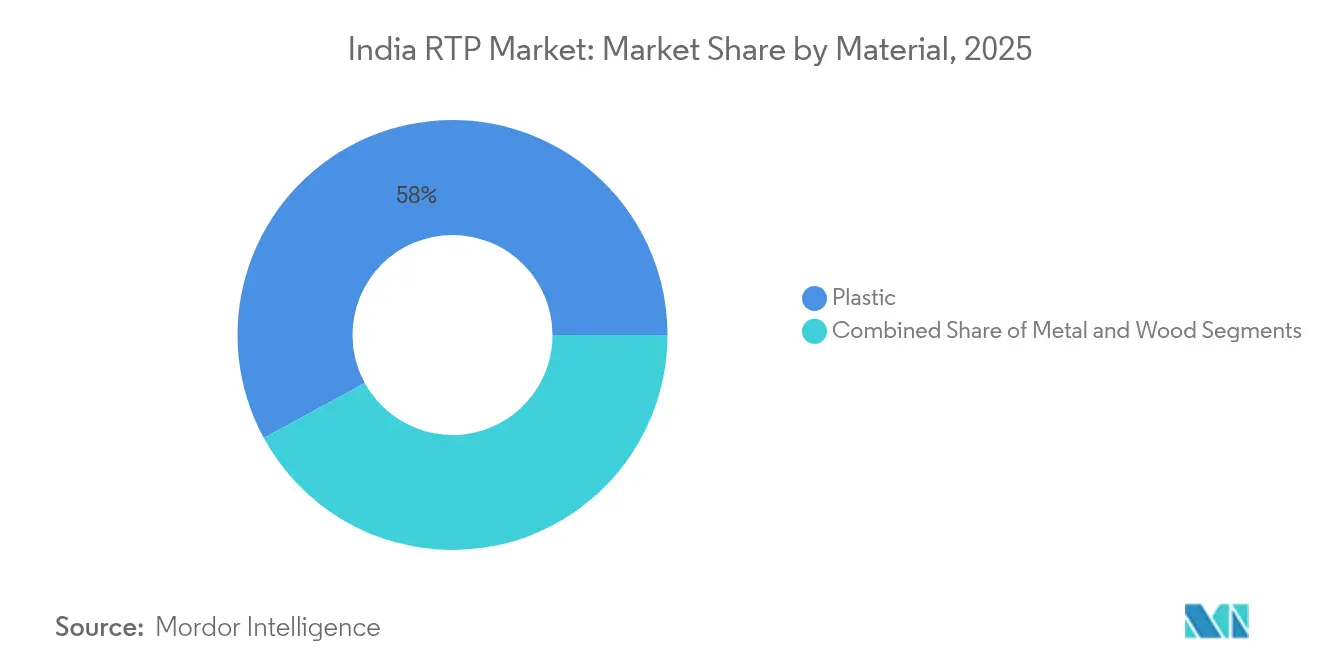

- By material, plastic led with 57.95% of the India returnable transport packaging market share in 2025, while metal is projected to expand at a 9.05% CAGR through 2031.

- By product type, pallets captured 34.95% of the India returnable transport packaging market size in 2025, whereas Intermediate Bulk Containers are advancing at an 8.68% CAGR to 2031.

- By end-user industry, food and beverage commanded 37.55% revenue share in 2025; pharmaceuticals and healthcare is forecast to grow fastest at 8.95% CAGR through 2031.

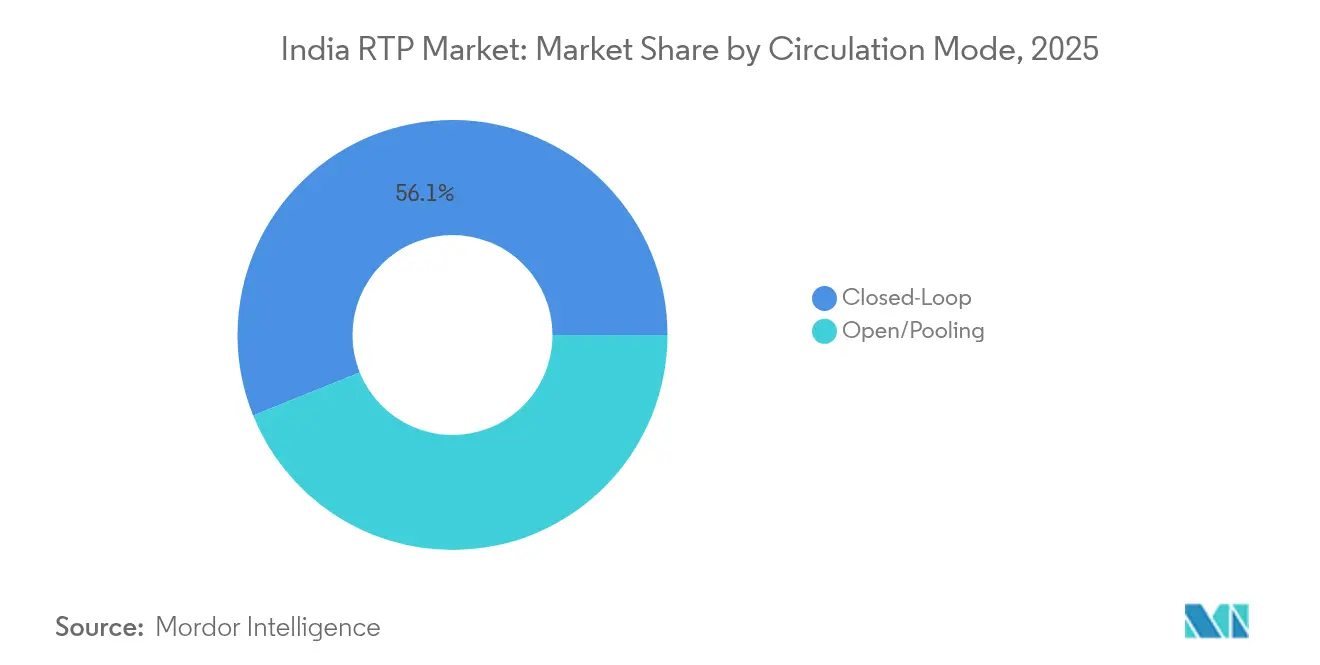

- By circulation mode, closed-loop systems accounted for 56.10% share of the India returnable transport packaging market in 2025 and are expanding at an 8.03% CAGR to 2031.

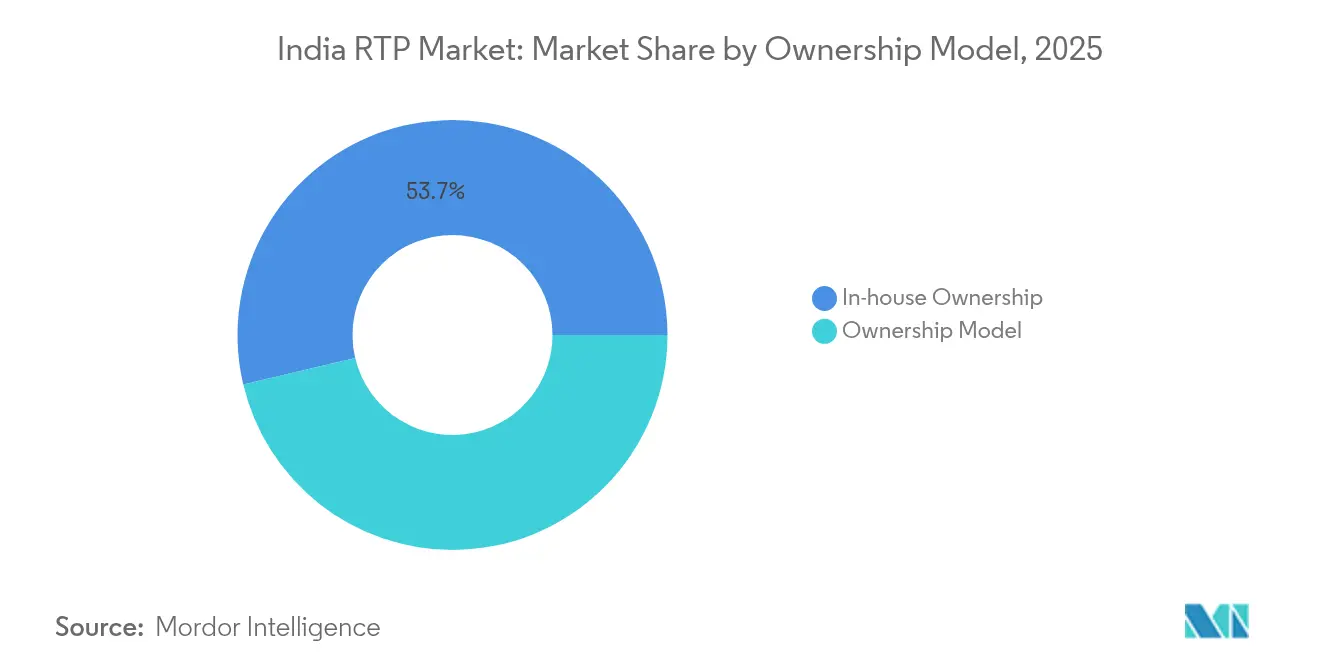

- By ownership model, in-house programs held 53.70% share in 2025, while rental/leasing solutions are recording the highest projected CAGR at 8.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India RTP Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government EPR and recycled-content mandates | +1.8% | National, with early gains in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Explosive growth of e-commerce 3PL pooling | +2.1% | National, concentrated in Delhi NCR, Mumbai, Bangalore, Hyderabad | Short term (≤ 2 years) |

| Cost-saving push by Food and beverage and electronics OEMs | +1.5% | National, with manufacturing hubs in Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| OEM demand for RFID-enabled zero-defect logistics | +0.9% | National, early adoption in automotive corridors | Long term (≥ 4 years) |

| Cold-chain pharma export boom needing insulated RTP | +1.2% | National, concentrated in Hyderabad, Ahmedabad, Mumbai pharmaceutical clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government EPR and Recycled-Content Mandates

Mandatory 30% recycled content for rigid plastics effective April 2025 is prompting beverage, FMCG, and electronics players to redesign supply chains around reusable assets. Resistance from bottlers has exposed recycling-capacity gaps, but EPR is simultaneously rewarding early movers such as Ganesha Ecopet, which tripled PET recycling output to 42,000 tpa in 2024. [1]Starlinger, “Ganesha Ecopet: Mitigating the Effects of Climate Change,” starlinger.com Anticipated expansion of EPR to all substrates by 2026 will widen compliance terrain, placing the India returnable transport packaging market at the center of corporate circularity strategies. Companies with established reverse-logistics loops now enjoy a regulatory moat that raises switching costs for laggards. Investments in deposit-return schemes and reverse-vending networks across Maharashtra and Gujarat illustrate how regional policy leadership can accelerate asset circulation.

Explosive Growth of E-commerce 3PL Pooling

Tier II and III cities contributed 41.5% of online retail volumes in 2022, compelling 3PLs to adopt standardized totes and foldable crates that survive multiple touchpoints without repacking costs.[2]IBEF, “India’s Grade A Warehousing Supply to Top 300 Million ft² by 2025,” ibef.org Warehousing stock exceeded 300 million ft² by 2025, and operators such as NIDO Group are automating sortation with scanners that read RFID tags embedded in shared crates. The collective scale is shrinking unit logistics spend by up to 15%, a saving that directly feeds e-commerce’s competitive pricing model. Government e-Marketplace orders topping USD 24 billion in FY 2023 further validate pooled-asset economics for institutional procurement channels. These dynamics widen the India returnable transport packaging market’s customer base beyond traditional manufacturing, anchoring growth in digital trade corridors.

Cost-Saving Push by Food and beverage and Electronics OEMs

Polypropylene prices rising to USD 970–990 t CFR in early 2025 have tightened packaging margins, nudging brands toward longer-life RTP assets that amortize costs over dozens of trips. For electronics, where packaging can be 5% of ex-factory cost, reusable dunnage yields direct savings while curbing electrostatic risk. Balaji Wafers’ installation of robot-assisted palletizers integrating HDPE pallets cut unplanned downtime to zero, proving that automation and returnable packaging are complementary investments. [3]Intralox, “Back-End Automation That’s Future Ready,” intralox.comAs flexible-packaging converters saw profitability slide to an 8% decade low in FY 2024, the case for shifting capital to reusable systems became more compelling. These economics reinforce adoption curves within the India returnable transport packaging market and temper exposure to resin price volatility.

OEM Demand for RFID-Enabled Zero-Defect Logistics

Automotive, white-goods, and precision-engineering OEMs now stipulate RFID-embedded pallets that transmit condition and geo-coordinates every few seconds. Annual pallet attrition, estimated at 10% of fleet size, costs industry millions. Pilot programs in Pune’s auto corridor reduced loss incidents by 30% after device rollout. Wiliot’s ambient IoT labels extend tracking to temperature and humidity, a capability prized by fresh-produce exporters. Patent activity around automated inventory boxes and single-piece re-closable packs underscores continued R&D momentum. As sensor prices fall, the India returnable transport packaging market is transitioning from asset pooling to data-rich service platforms that monetize visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and ROI uncertainty | -1.2% | National, particularly affecting SMEs in Tier II/III cities | Short term (≤ 2 years) |

| Fragmented reverse-logistics infrastructure | -0.8% | National, acute in rural and semi-urban areas | Medium term (2-4 years) |

| GST compliance hurdles for pooled assets | -0.6% | National, complex in multi-state operations | Medium term (2-4 years) |

| Asset loss from lack of pallet-tracking standards | -0.9% | National, severe in high-theft corridors and unorganized sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and ROI Uncertainty

A comprehensive RTP program can demand millions of USD in tooling, moulds, and fleet build-out, which challenges the cash flow of small enterprises. Time Technoplast’s Rs 1,500 crore (USD 180 million) outlay illustrates the scale required for nationwide presence. With payback periods spanning 18–36 months, CFOs hesitate amid volatile resin prices and demand swings. Supreme Industries’ revenue dip during Q2 FY 2025, aggravated by PVC price fluctuations, highlights how material cycles can stretch ROI horizons. Limited access to asset-financing instruments keeps many SMEs on the fence, muting potential penetration in the India returnable transport packaging market.

Fragmented Reverse-Logistics Infrastructure

Collection and refurbishment facilities remain scarce outside tier-one cities, forcing empty assets to deadhead hundreds of kilometers, inflating total landed costs. Studies of fastener manufacturers reveal inefficient backhaul pathways as a primary barrier to reverse-logistics adoption. Government plans for 35 multi-modal logistics parks promise relief, but execution lags and current operators rely on ad-hoc regional tie-ups. Quality inconsistency across third-party refurbishers worsens cycle-time predictability, dissuading brand owners from large-scale commitments. Until network density improves, infrastructure gaps will cap the growth rate of the India returnable transport packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Amid Metal’s Rapid Ascent

Plastic retained 57.95% of the India returnable transport packaging market in 2025, reflecting its lightweight strength and affordable tooling costs. The segment’s leadership is entrenched in beverage, FMCG, and electronics supply chains that prioritize speed over heavy-duty performance. Yet escalating sustainability mandates and the need for higher heat resistance are steering pharmaceutical and chemical exporters toward metal containers, propelling the segment at a 9.05% CAGR to 2031. Polypropylene’s price creep is pushing buyers to scrutinize total life-cycle economics rather than upfront unit costs, a calculus that often favors stainless-steel or aluminum IBCs for high-margin payloads. Nilkamal’s investment in food-grade HDPE crates underlines niche specialization as a defense against metal incursion. Bio-based PLA initiatives backed by Rs 2,000 crore (USD 240 million) in new capacity could reorder material preference by late decade, adding a green premium layer to the India returnable transport packaging market.

Material supply stability now influences sourcing contracts as much as price. Resin buyers monitor refinery shutdowns and freight disruptions with new urgency, adopting dual-spec packaging qualified across plastic and metal to hedge risk. Meanwhile, metal pool operators highlight 8-10-year service lives and secondary scrap value that offsets higher capex. As circular-economy scorecards become part of tender evaluations, brand owners increasingly refresh bills of material to reflect quantified CO2 reductions linked to closed-loop polymers and infinitely recyclable alloys. The competitive interplay is likely to sustain plastic’s headline dominance yet chip away incremental share in regulated end-markets, keeping material choice fluid across the India returnable transport packaging market.

By Product Type: Pallets Lead While IBCs Surge

Pallets represented 34.95% of the India returnable transport packaging market size in 2025, cementing their status as the universal workhorse of domestic logistics. Standardized footprints, especially the 1200 × 1000 mm base, mesh well with automated storage and retrieval systems now proliferating in Grade A warehouses. Collaborative robots at snack-food plants stack pallet loads 12% faster, cutting labor cost per ton and reinforcing the pallet’s centrality to factory automation strategies. Intermediate Bulk Containers are the fastest riser with an 8.68% CAGR, drawing demand from chemical, agrochemical, and pharmaceutical exporters that value their high payload density and compatibility with ISO tank freight lanes. Fold-flat models pare backhaul volume by up to 65%, a compelling benefit as diesel remains above INR 90 per liter in key corridors.

Product development is tilting toward smart variants: RFID-enabled pallets capable of plug-and-play sensor integration, insulated IBCs with phase-change materials for 120-hour cold hold, and collapsible crates that self-lock to cut manual clip usage. Time Technoplast’s 60% share in large plastic drums shows how dominance in a niche can shield margins even when broader product lines face commoditization pressures. Over the forecast period, demand convergence around omnichannel fulfillment will blur product boundaries, birthing hybrid solutions such as pallet-sized foldable boxes fitted with dunnage inserts. These innovations will elevate product mix complexity across the India returnable transport packaging market.

By End-User Industry: Food and beverage Leadership Amid Pharma Acceleration

Food and beverage captured 37.55% of the India returnable transport packaging market share in 2025 as high-velocity SKUs, from dairy pouches to bottled water, relied on reusable crates and pallets for just-in-time replenishment of modern trade shelves. Chilled milk routes in Tamil Nadu now standardize on HDPE boxes certified under new BIS norms, reinforcing hygiene compliance and reducing film wrap consumption. Margin compression in flexible packaging is prompting snack makers to pivot toward returnable bins for distribution centers, trimming carton waste and freight cube. Pharmaceuticals and healthcare deliver the fastest growth at 8.95% CAGR through 2031 off the back of vaccine exports and biologic API shipments that demand GDP-compliant totes with thermal liners.

Regulators increasing audit frequency at vaccine plants spur cold-chain certification of packaging fleets, pushing pharma users toward dedicated assets within the India returnable transport packaging market. Automotive manufacturers remain steady adopters of heavy-duty racks and collapsible bulk boxes protecting painted body panels during cross-country moves. Meanwhile, consumer-electronics assemblers in Noida mandate ESD-safe trays to curb static discharge during board transport. This end-user mosaic is expanding the addressable market, yet each vertical applies unique specification filters, challenging suppliers to build modular portfolios that balance customization with scale economics.

By Circulation Mode: Closed-Loop Systems Maintain Dominance

Closed-loop routes controlled by a single brand owner or a tight consortium held 56.10% of the India returnable transport packaging market in 2025, scaling at 8.03% CAGR as companies pursue guaranteed asset availability and predictable return cycles. CHEP’s share-and-reuse blueprint illustrates the benefits: frequent inspection, on-demand repair, and a digital passport for every pallet. In automotive supply chains, closed-loop reuse between component vendor clusters and OEM assembly plants limits contamination risk and shortens cycle time to as low as four days. Open pooling remains essential for SMEs and 3PLs that cannot justify owning fleets sized for seasonal peaks, but its penetration is capped by loss exposure and variable service quality across regions.

Digitalization is blurring mode distinctions: hybrid models allow proprietary assets to enter shared networks for backhaul legs, maximizing equipment turns without surrendering full control. Brambles estimates that cutting uncompensated losses by 30% yields USD 150 million in annual cash savings globally, signaling how asset intelligence can unlock capital trapped in dormant stock. Y-2025 pilots in Rajasthan integrate blockchain-based custody handovers that timestamp every exchange, pre-figuring industry-wide adoption and reinforcing the value proposition of closed-loop models in the India returnable transport packaging market.

By Ownership Model: In-House Control Leads Despite Rental Growth

In-house programs accounted for 53.70% of the India returnable transport packaging market in 2025, reflecting entrenched habits of asset ownership among consumer-goods majors. Ownership enables customization, brand-colored crates, special vent slots, tamper-evident RFID locks, that rental fleets rarely offer at scale. Yet capex sensitivity and the shift toward asset-light balance sheets are driving 8.66% CAGR for rental/leasing packages. LEAP India’s takeover of CHEP India expanded its fleet past 11 million assets and 33 depots, giving customers a one-invoice solution spanning pallets, bins, and crates nationwide.

Rental providers now bundle predictive-maintenance apps that ping downtime alerts, easing user concerns about hidden refurbishment costs. Some roll out variable-term contracts that sync with peak festival seasons, trimming idle fees. Hybrid schemes, purchase palettes for captive lanes, lease extras for promos, are emerging inside FMCG procurement playbooks. Over time, asset-as-a-service economics will keep eroding the ownership premium, tilting equilibrium gradually toward OPEX-based models inside the India returnable transport packaging market.

Geography Analysis

Western and southern industrial belts, Maharashtra, Gujarat, Tamil Nadu, and Karnataka, generate about 59.25% of demand in 2025 as they house automotive, textiles, and petrochemical hubs. The Delhi NCR cluster leads e-commerce parcel volume, prompting 3PLs to stock versatile fold-flat crates that ride mixed-load vans. Hyderabad and Ahmedabad dominate pharma exports, and their need for GDP-compliant totes drives localized manufacturing of insulated RTP assets. Government plans for 35 multi-modal logistics parks, including nodes near Chennai and Nagpur, promise to tighten return loops and cut empty runs, directly benefiting the India returnable transport packaging market.

Grade A warehouse supply surpassed 300 million ft² in 2025, with Pune and NCR commanding 45% of premium capacity. Developers increasingly allocate refurbishment bays inside parks, allowing instant triage of damaged assets, reducing downtime from ten days to four. Meanwhile, Time Technoplast’s forthcoming Konkan plant positions the firm close to western ports, trimming export lead time for composite cylinders and industrial drums. Karnataka’s circular-economy pilot converting agro-waste to ethanol underscores the state’s appetite for reusable containers in biofuel value chains.

Tier II/III cities, from Indore to Coimbatore, benefit from rising disposable incomes and smartphone penetration, lifting local e-commerce fulfillment that relies on pooled totes for reverse logistics collection. The Union Budget 2025’s track-and-trace mandate for pooled assets, coupled with clearer input-tax credit on plant infrastructure, should lower compliance friction across state lines. Local language interfaces on pooling apps and partnerships with regional transport cooperatives are becoming differentiators, ensuring that the India returnable transport packaging market achieves nationwide coverage without diluting service quality.

Competitive Landscape

Competition remains moderate yet tilting toward consolidation. LEAP India’s January 2025 purchase of CHEP India unites two large pools, creating network density that enhances turnaround velocity and raises entry barriers for smaller rivals. Brambles is embedding over 550,000 self-powered trackers that feed utilization data into AI engines, guiding asset repositioning and cutting losses 30% year on year. Time Technoplast leverages its 60% share in plastic drums to cross-sell crates and IBCs into the chemicals sector, demonstrating product adjacency as a growth tactic.

Tech-driven startups inject fresh competition. Amplepac offers blockchain-verified shareable packaging whose smart locks timestamp each custody exchange, targeting waste-free e-grocery deliveries. Loop Industries collaborates with Ester to build an Infinite Loop facility in Gujarat producing 100% recycled PET resin by 2027, ensuring captive supply of circular raw material for poolers. IFCO’s ESG disclosures spotlight score-carded carbon abatement, helping retailers meet Scope 3 goals and nudging procurement toward providers with verifiable sustainability credentials.

Strategic moves span mergers, capacity expansion, and digital services. Mahindra’s launch of the ZEO electric four-wheeler adds clean-mobility heft to last-mile loops, lowering total emissions per trip. CHEP Europe’s FalConic container, made with 80% post-consumer resin, raises the performance bar and may debut in India via global accounts. Collectively, these initiatives sharpen competitive dynamics while advancing technology adoption across the India returnable transport packaging market.

India RTP Industry Leaders

GEFCO Group

Nefab AB

Signode Limited

CHEP Logistics

LEAP India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: LEAP India acquired CHEP India Private Limited, expanding to 33 warehouses and over 11 million assets.

- February 2025: Loop Industries and Ester confirmed Q2 2025 groundbreaking for an Infinite Loop PET plant in Gujarat.

- January 2025: IFCO Systems released its ESG Report 2024 outlining circularity milestones.

- October 2024: CHEP Europe unveiled the FalConic reusable container featuring 80% PCR content.

India RTP Market Report Scope

Returnable Transport Packaging (RTP) is a system of reusable racks, pallets, hand-held containers, or bulk containers that move products safely and efficiently throughout the supply chain. These packaging systems are constructed using durable materials like wood, plastic, and metal. Unlike one-way packaging, they are intended for multiple uses across various end-user industries, including Automotive, Food, and Beverages, Consumer Goods., Electronics and Appliances.

By Material

| Plastic |

| Metal |

| Wood |

By Product Type

| Pallets |

| Crates and Trays |

| Intermediate Bulk Containers (IBCs) |

| Drums and Barrels |

| Dunnage and Racks |

By End-user Industry

| Automotive |

| Food and Beverage |

| Consumer Goods and Retail |

| Electronics and Appliances |

| Pharmaceuticals and Healthcare |

| Other End-User Industry |

By Circulation Mode

| Closed-Loop |

| Open/Pooling |

By Ownership Model

| Rental/Leasing |

| In-house Ownership |

| By Material | Plastic |

| Metal | |

| Wood | |

| By Product Type | Pallets |

| Crates and Trays | |

| Intermediate Bulk Containers (IBCs) | |

| Drums and Barrels | |

| Dunnage and Racks | |

| By End-user Industry | Automotive |

| Food and Beverage | |

| Consumer Goods and Retail | |

| Electronics and Appliances | |

| Pharmaceuticals and Healthcare | |

| Other End-User Industry | |

| By Circulation Mode | Closed-Loop |

| Open/Pooling | |

| By Ownership Model | Rental/Leasing |

| In-house Ownership |

Key Questions Answered in the Report

What is the current value of the India returnable transport packaging market?

The market stands at USD 938.96 million in 2026 and is projected to hit USD 1.33 billion by 2031.

Which material dominates India’s returnable transport packaging?

Plastic leads with 57.95% share in 2025, though metal containers are growing fastest at a 9.05% CAGR.

Why are pharmaceuticals driving demand for insulated returnable packaging?

Strict cold-chain regulations for vaccines and biologics require temperature-controlled Intermediate Bulk Containers that can be reused across multiple export cycles.

How is e-commerce affecting demand for pooled assets?

Rapid growth toward a USD 300 billion e-commerce market by 2030 is escalating demand for foldable crates and pallets that can circulate efficiently through 3PL networks.

What ownership model is growing fastest?

Rental and leasing solutions are expanding at an 8.66% CAGR as companies seek asset-light strategies.

How are RFID and IoT technologies influencing the sector?

Trackers embedded in pallets and crates cut loss rates, provide real-time visibility, and enable predictive maintenance, thereby improving ROI on reusable assets.

Page last updated on: