India Retail Fuel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Growth Rate | 2.59% CAGR |

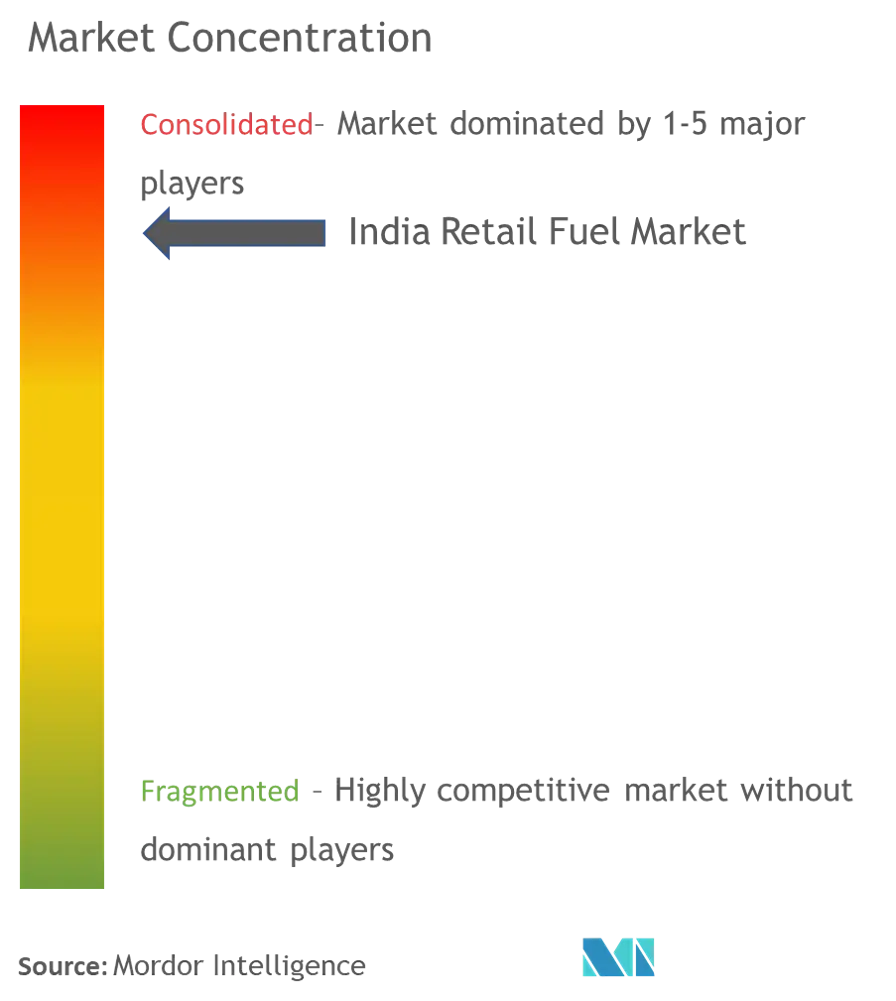

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Retail Fuel Market Analysis by Mordor Intelligence

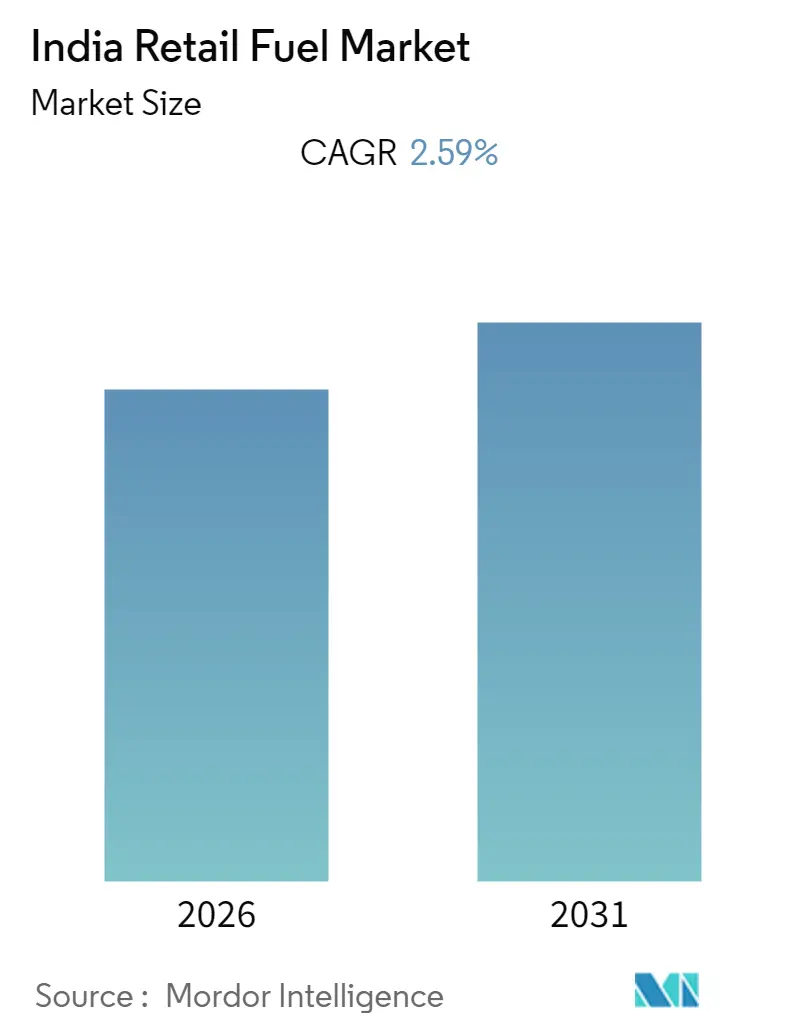

The India Retail Fuel market size is expected to grow from USD 54.8 billion in 2025 to USD 56.22 billion in 2026 and is forecast to reach USD 63.87 billion by 2031 at 2.59% CAGR over 2026-2031.

India's retail fuel market landscape is undergoing significant transformation driven by evolving market dynamics and structural changes in the energy sector. The market is characterized by a concentrated competitive structure, with public sector undertakings dominating the fuel market distribution network. As of 2022, the market share of petroleum companies in India shows Indian Oil Corporation Limited commanding 38% of the market, followed by Bharat Petroleum Corporation Limited at 20.1%, Hindustan Petroleum Corporation Limited at 18%, and private players collectively holding 21.7% of the market share. This established network of over 77,000 retail outlets across major public sector players demonstrates the robust infrastructure supporting fuel distribution across the country.

The transportation sector is witnessing a paradigm shift towards sustainable alternatives, impacting the traditional petrol market. Indian Railways has made substantial progress in its electrification initiative, achieving electrification of 52,247 Route Kilometers out of a total 65,414 RKM, marking a significant step towards its goal of complete electrification. Additionally, the government's ambitious plan to replace approximately 30,000 diesel-run buses with electric powertrain vehicles in the next 2-3 years signals a strong push towards clean mobility solutions, particularly in urban transportation.

The market is experiencing dynamic changes in response to demographic and economic factors. With India's population projected to reach 1.515 billion by 2030 and a median age of 28.7 years as of 2022, the country's young demographic is driving increased vehicle ownership. This trend is reflected in the passenger vehicle sales, which reached 3.07 million units in FY 2022, marking a 13% increase from the previous year. The growing middle class and increasing urbanization continue to shape consumption patterns in the fuel companies in India sector.

The discovery of significant mineral resources is poised to influence the industrial demand for retail fuels. In February 2023, India announced the discovery of 5.9 million tonnes of lithium reserves in the Reasi district of Jammu and Kashmir, positioning India among the world's top lithium reserve holders. This discovery, coupled with Coal India Ltd's January 2023 announcement of nine new coal mining projects with a combined production capacity of 127 million tonnes, indicates substantial industrial activity that will drive fuel demand in the mining and quarrying sectors, despite the gradual transition towards sustainable energy solutions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Retail Fuel Market Trends and Insights

Strong Public Sector Infrastructure and Government Support

The robust infrastructure network and government backing of Public Sector Undertakings (PSUs) serve as a significant driver for India's size of the retail market in India. PSUs like Indian Oil Corporation (IOC), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL) have established an extensive network of fuel stations, pipelines, terminals, and storage facilities, ensuring widespread fuel availability across urban and rural areas. This infrastructure advantage is further strengthened by continuous investments, as evidenced by Indian Oil Corporation Limited's announcement in February 2023 to invest USD 25.44 million in West Bengal for expanding and developing greener fuel retail infrastructure.

The government's support in pricing policies and infrastructure development has enabled PSUs to maintain competitive pricing while ensuring fuel quality and safety standards. This is reflected in their expansion of green auto fuel availability, which is set to grow from 275 retail outlets in 2022 to more than 1,000 by the end of 2024. The strong government backing also allows PSUs to maintain stable fuel costs, providing price security to consumers while ensuring consistent fuel availability. According to the Ministry of Petroleum and Natural Gas, India witnessed a significant increase of more than 6% in petroleum products consumption between April 2022 and April 2023, with PSU retail outlets accounting for the majority of this consumption.

Rising Vehicle Ownership and Automotive Market Growth

The substantial increase in vehicle ownership across India has emerged as a crucial driver for the fuel retail business, supported by rising disposable incomes and accelerating urbanization. According to the Society of Indian Automobile Manufacturers, vehicle sales in India demonstrated remarkable growth with a more than 20% increase between 2021 and 2022, directly translating to increased fuel consumption and more frequent visits to fuel retail stations. This trend is further reinforced by the automotive industry's continued expansion and introduction of new vehicles, as exemplified by BMW's announcement in May 2023 regarding the launch of their X3 M40i model in India.

The growth in vehicle ownership is creating sustained demand for petrol retail, particularly in urban areas where car ownership is rapidly increasing. The automotive market's dynamism is evident in the introduction of new high-performance vehicles, such as BMW's upcoming X3 M40i featuring a 3.0-liter six-cylinder turbocharged petrol engine, which indicates a continued strong demand for retail fuels. This increasing vehicle population not only drives higher fuel consumption but also necessitates the expansion of retail fuel infrastructure to meet the growing demand, creating a positive feedback loop that further strengthens the market's growth trajectory.

Segment Analysis

Public Sector Undertakings Segment in India Retail Fuel Market

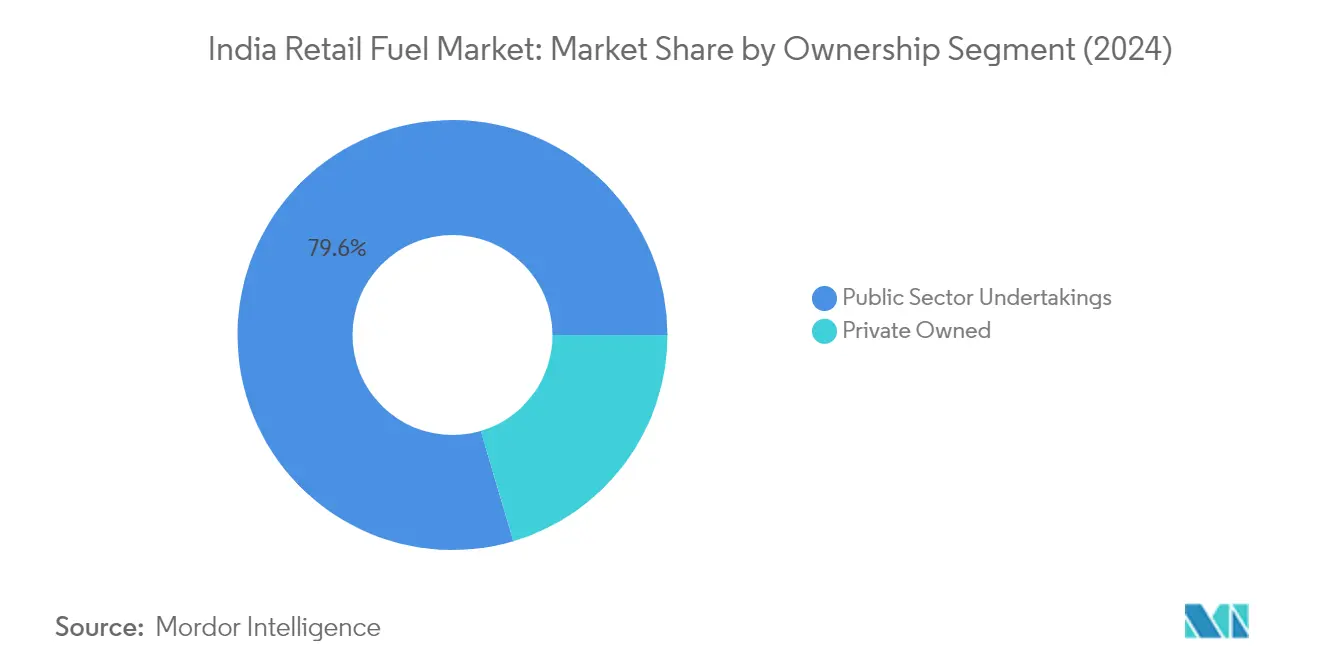

The Public Sector Undertakings (PSU) segment dominates the India fuel retail industry, commanding approximately 79.25% fuel market share in 2025. This segment, led by major players like Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL), demonstrates both market leadership and robust growth potential. The segment's strong performance is driven by several factors, including extensive retail network coverage, competitive fuel pricing compared to private players, and strategic capacity expansion initiatives. PSU companies collectively operate over 77,000 retail outlets across India, with IOCL alone managing more than 35,500 outlets. The segment is projected to maintain its growth trajectory at around 9.3% annually from 2026 to 2031, supported by increasing fuel demand from end-users and ongoing expansion of refining capacities. The government's support and the PSUs' ability to maintain lower fuel prices compared to private players continue to strengthen their market position.

Private Owned Segment in India Retail Fuel Market

The Private Owned segment, while smaller in fuel market share, plays a crucial role in India's retail fuel landscape by introducing competition and innovative service offerings. This segment includes prominent players like Reliance Industries Limited, Nayara Energy, and Shell, who collectively operate thousands of retail outlets across the country. The segment's operations are characterized by premium quality fuels, superior customer service, and modern retail infrastructure. Despite facing challenges from price differentials with PSU players, private retailers continue to maintain their presence through value-added services and strategic location selection. The segment's growth is supported by the government's liberalization of fuel retailing policies and increasing demand for premium fuel products in urban areas.

Segment Analysis: End-User

Private Sector Segment in India Retail Fuel Market

The private sector segment dominates the India retail fuel market, commanding approximately 87% petrol market share in India in 2024. This segment encompasses various end-users, including manufacturing industries, agriculture, retail consumers, and private transportation. The robust growth in this segment is driven by India's expanding population, which has reached over 1.41 billion, making it the world's most populous country with a relatively young median age of 28.7 years. The segment has shown remarkable resilience and growth potential, supported by increasing passenger vehicle sales, expansion in manufacturing industries, and growing agricultural sector demands. The government's implementation of various supply-side policies to boost manufacturing has further strengthened this segment's position, making India an increasingly attractive destination for investments. Additionally, the retail consumer base within this segment continues to expand, driven by urbanization and rising disposable incomes.

Public Sector Segment in India Retail Fuel Market

The public sector segment, while holding a smaller market share of around 13% in 2024, plays a crucial role in India's retail fuel market. This segment primarily serves government entities, public transportation systems, railways, and state-owned enterprises. The segment's growth is closely tied to public infrastructure development, government initiatives in transportation, and public sector industrial activities. Key consumers in this segment include railways, state transport undertakings, public sector mining operations, and government-owned power generation facilities. The segment's development is particularly influenced by the government's push towards infrastructure development and public transportation expansion, though this is being balanced against initiatives for electrification and sustainable transport solutions.

Competitive Landscape

Top Companies in India Retail Fuel Market

The Indian retail fuel market is dominated by major public sector undertakings, including Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL), alongside private players like Nayara Energy, Reliance Industries, and Shell. These petrol pump companies in India are actively pursuing product innovation through the introduction of premium and cleaner fuels while expanding their service offerings to include convenience stores, car wash facilities, and EV charging stations. The industry is witnessing significant operational transformations through digital initiatives and automation of fuel stations. Strategic partnerships and joint ventures, such as the collaboration between Reliance and BP, are reshaping market dynamics. Companies are aggressively expanding their retail networks, particularly in untapped regions, while simultaneously upgrading existing outlets to modern mobility stations with integrated services.

PSU Dominance Shapes Market Competition Landscape

The Indian retail fuel market exhibits a unique structure characterized by strong public sector dominance, with PSUs controlling the majority of market share through their extensive retail network and established supply chain infrastructure. The market demonstrates moderate consolidation, with three major PSUs holding significant market positions, while private players operate in specific regional strongholds. Recent years have witnessed increased participation from global energy majors through joint ventures and strategic partnerships, particularly in premium fuel segments and value-added services. The competitive dynamics are further influenced by government policies regarding fuel pricing and retail licensing, creating distinct operational environments for public and private sector players.

The market has experienced notable merger and acquisition activities, primarily driven by private sector players seeking to establish or expand their presence in the Indian market. Joint ventures between domestic and international players have emerged as a preferred mode of market entry, combining local market knowledge with global expertise. The industry is witnessing vertical integration attempts by major players, extending from refining to retail operations, while smaller players focus on niche segments or regional markets. Cross-industry partnerships, particularly in the areas of digital payments, convenience retailing, and electric mobility, are becoming increasingly common as companies seek to diversify their revenue streams.

Innovation and Diversification Drive Future Growth

Success in the Indian retail fuel market increasingly depends on companies' ability to innovate across multiple dimensions, from fuel quality and service offerings to digital integration and customer experience. Incumbent players must focus on modernizing their retail networks, implementing advanced technologies for operations management, and developing value-added services to maintain their market position. The ability to manage fuel pricing effectively while maintaining profitability, particularly during periods of international price volatility, remains crucial. Companies need to invest in supply chain optimization and storage infrastructure to ensure consistent fuel availability and maintain competitive pricing.

For new entrants and smaller players, success lies in identifying and exploiting niche market segments, developing differentiated service offerings, and building a strong regional presence before expanding nationally. The increasing focus on alternative fuels and electric mobility presents opportunities for market disruption, requiring players to develop adaptive strategies. Regulatory compliance, particularly regarding environmental standards and safety requirements, will become increasingly important as the government pushes for cleaner fuels and sustainable practices. Customer service excellence, brand building, and loyalty programs will play crucial roles in maintaining competitive advantage, while strategic partnerships across the value chain will become essential for sustainable growth. Companies such as fuel retail companies and Indian petrol pump companies are well-positioned to leverage these trends.

India Retail Fuel Industry Leaders

Indian Oil Corporation Ltd

Bharat Petroleum Corp Ltd

Hindustan Petroleum Corporation Limited

Nayara Energy Limited

Reliance Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: The Government of India announced the launch of E20 fuel across 11 states and union territories at 84 retail outlets in India. The Indian government aims to achieve 20% blending of ethanol with petrol by 2025 in the country. The step was taken to control the environmental emission from conventional fuels and progress towards a greener fuel economy. Oil marketing companies (OMC), including HPCL, have set up plants to accomplish the goal.

- February 2023: Jio-bp, one of India's leading retail fuel companies, began selling E20 gasoline. Customers with E20 petrol-compatible vehicles will be able to choose this fuel at select Jio-bp locations, and the service will be spread across the network shortly.

- December 2022: Indian Oil Corporation (IOCL) announced that for five years, Indian Oil Corporation (IOC) had chosen Reliance Jio to connect its 7,200 IOC sites using SD-WAN (Software Defined Wide Area Network). Jio will connect 7,200 IOC sites with an SD-WAN managed service solution, zero-touch provisioning, and real-time monitoring 24 hours a day, seven days a week.

India Retail Fuel Market Report Scope

Retail fuels refer to the types of fuels available for purchase by individual consumers at retail or gas stations. These fuels are used for vehicles and equipment and sold in small quantities for personal or commercial use. The most common types of retail fuels include Petrol, Diesel, Gas, Liquefied Petroleum Gas, and Others.

The India Retail Fuel Market is segmented by Ownership and End User. By Ownership, the market is segmented into Public Sector Undertakings and Private Owned, and by End User, the market is segmented into Public Sector and Private Sector. The report offers the market size and forecasts for India retail fuel market in thousand tons for all the above segments.

| Public Sector Undertakings |

| Private Owned |

| Public Sector |

| Private Sector |

| Ownership | Public Sector Undertakings |

| Private Owned | |

| End User | Public Sector |

| Private Sector |

Key Questions Answered in the Report

What is the current India Retail Fuel Market size in 2026?

The India Retail Fuel Market size is USD 56.22 billion in 2026, and the market is projected to register a CAGR of 2.59% during the forecast period (2026-2031)

Who are the key players in India Retail Fuel Market?

Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Hindustan Petroleum Corporation Limited, Nayara Energy Limited and Reliance Industries Limited are the major companies operating in the India Retail Fuel Market.

What years does this India Retail Fuel Market cover?

The report covers the India Retail Fuel Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the India Retail Fuel Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: