Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

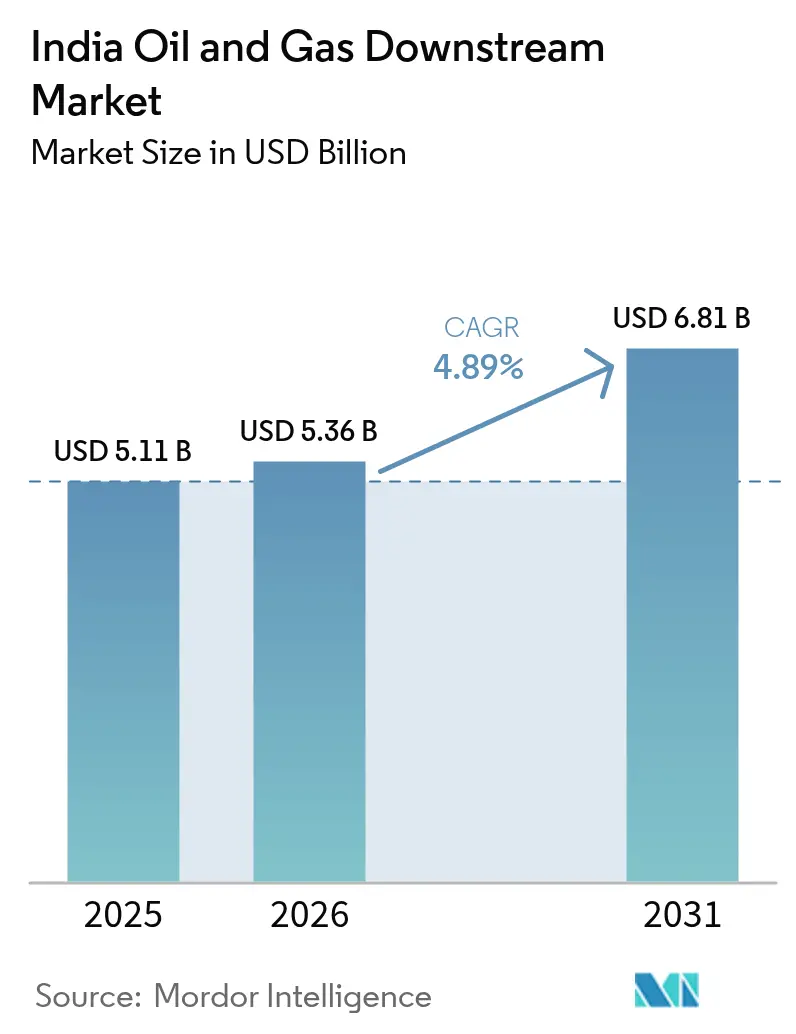

| Base Year Market Size (2025) | USD 5.11 Billion |

| Market Size (2026) | USD 5.36 Billion |

| Market Size (2031) | USD 6.81 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

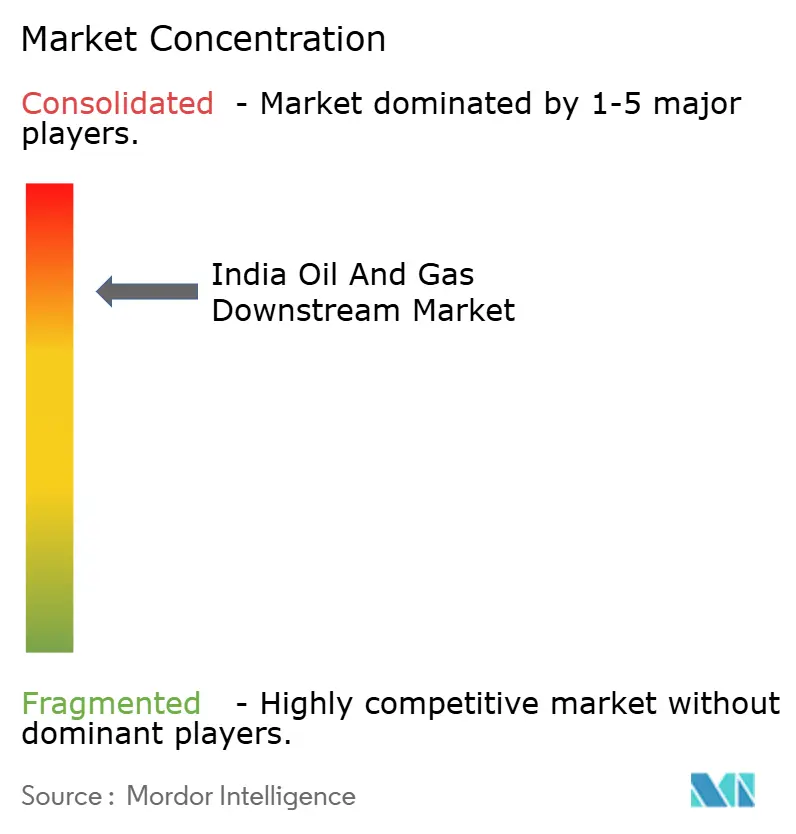

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Oil And Gas Downstream Market Analysis by Mordor Intelligence

The India Oil And Gas Downstream Market size was valued at USD 5.11 billion in 2025 and estimated to grow from USD 5.36 billion in 2026 to reach USD 6.81 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031).

Robust public- and private-sector investments, expanding petrochemical demand, and ongoing refinery modernizations keep the growth engine well-oiled, despite the energy transition's headwinds. Capacity additions totaling 652,000 barrels per day scheduled by 2027 reinforce India's ambition to serve both domestic consumption and regional export needs. Regulatory catalysts, such as the Bharat Stage-VI (BS-VI) fuel norms, the 20% ethanol-blending mandate, and the national hydrogen roadmap, are accelerating technology upgrades, operational digitalization, and feedstock diversification. Integrated refinery–petrochemical complexes, exemplified by Reliance's Jamnagar hub, illustrate how operators are hedging gasoline-demand uncertainty by tilting toward higher-margin chemicals. Meanwhile, retail fuel distribution is undergoing a digital makeover—routine deployment of IoT sensors, mobile payments, and AI-driven inventory tools is redefining last-mile efficiency and customer engagement.

Key Report Takeaways

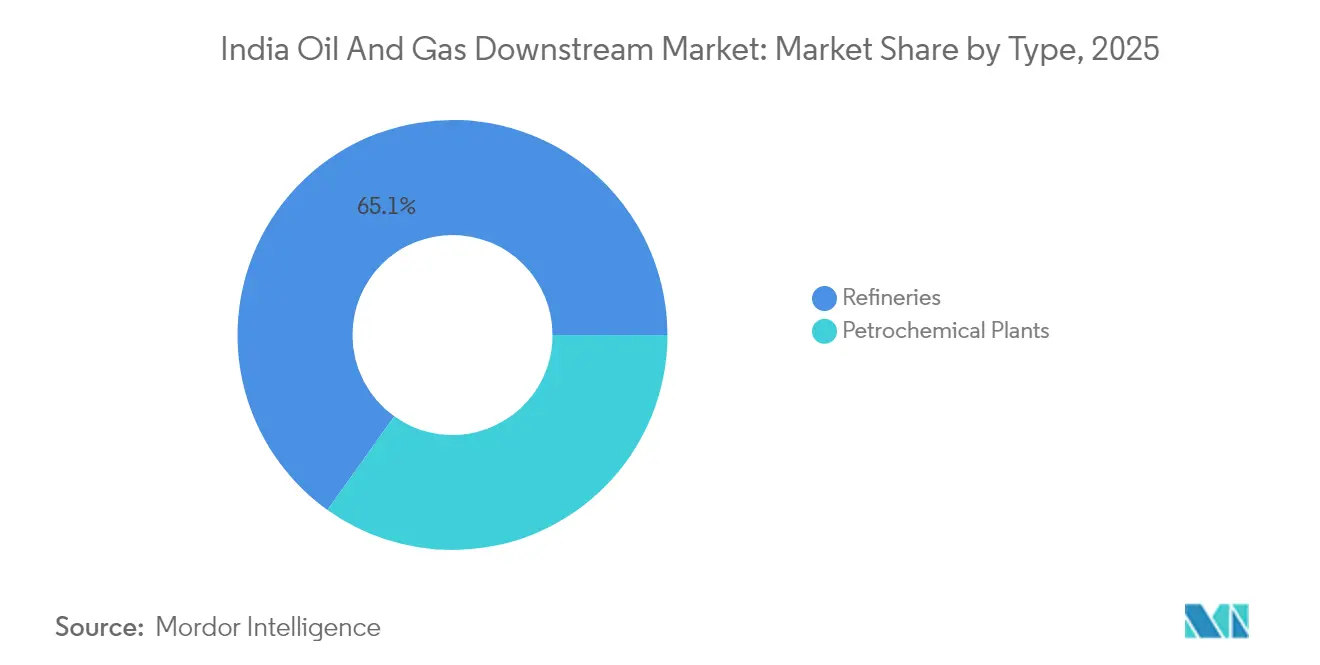

- By type, refineries led with 65.12% of India's oil and gas downstream market share in 2025, while petrochemical plants are projected to register a 7.22% CAGR through 2031—the fastest growth within the market.

- By product type, refined petroleum products accounted for 67.54% share of the India oil and gas downstream market size in 2025, while petrochemicals are set to expand at a 6.94% CAGR to 2031.

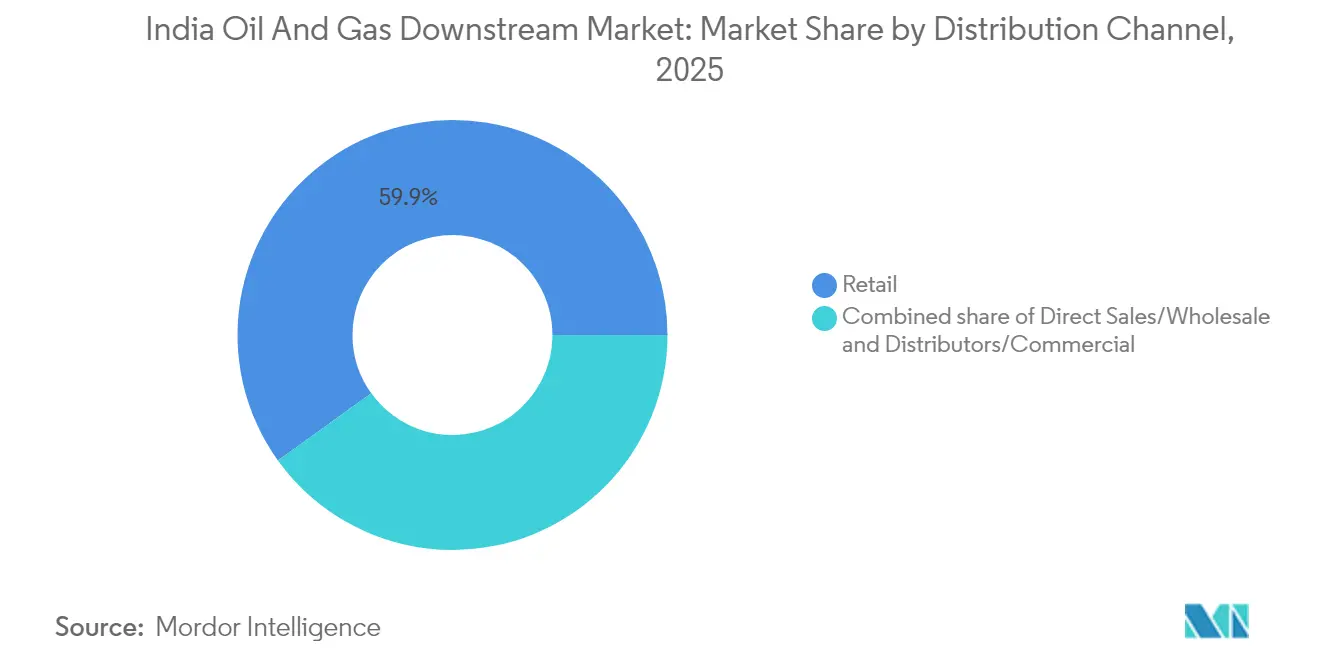

- By distribution channel, retail fuel outlets captured a 59.92% share of the India oil and gas downstream market size in 2025 and are expected to advance at a 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class fuel demand | +1.2% | Tier-2 cities nationwide | Medium term (2-4 years) |

| BS-VI compliance capex | +0.8% | Major refining hubs | Short term (≤2 years) |

| Petrochemicals demand growth | +0.6% | Gujarat–Maharashtra corridor | Long term (≥4 years) |

| Hydrogen & bio-fuels blending push | +0.4% | Select pilot states | Long term (≥4 years) |

| Digital refinery OPEX optimization | +0.3% | Pan-India refineries | Medium term (2-4 years) |

| Aviation traffic rebound | +0.2% | Metro airports | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Fuel Demand

Vehicle ownership in Tier-2 and Tier-3 cities is increasing at a rate of 12% annually, outpacing the plateauing metros and creating dispersed demand nodes across the India oil and gas downstream market.[1]Ministry of Road Transport and Highways, “Automobile Statistics 2025,” morth.nic.in Indian Oil Corporation plans to establish 5,000 new rural retail outlets by 2026, targeting these growth centers. Middle-class purchasing power is also driving the consumption of premium lubricants and specialty products, thereby boosting per-unit margins for retailers. Aviation turbine-fuel demand mirrors this trend as passenger numbers are set to double by 2030, further underpinning jet-fuel cracks. Together, these dynamics strengthen revenue visibility for refiners and marketers, supporting fresh investments in storage, logistics, and customer-facing technologies.

Bharat Stage-VI Compliance Capex

Sector-wide capex topping USD 15 billion has upgraded hydrotreaters, catalytic reformers, and blending systems to comply with BS-VI sulfur limits. Hindustan Petroleum’s Vizag refinery alone invested USD 1.2 billion, completing upgrades ahead of peers and freeing funds for capacity growth in the India oil and gas downstream market.[2]Hindustan Petroleum Corporation, “Annual Report 2024,” hpcl.co.in Early movers now sell premium BS-VI fuels domestically and export to sulfur-stringent markets, widening gross-refining margins. Smaller refiners face a capital-access squeeze and are considering joint ventures or mergers to dilute compliance costs. The regulatory milestone consequently accelerates industry consolidation and the diffusion of technology.

Hydrogen & Bio-Fuels Blending Push

India’s 20% ethanol mandate, effective 2025, drives the creation of storage, blending, and quality-control assets compatible with higher biofuel ratios.[3]Ministry of Petroleum and Natural Gas, “Ethanol Blending Program,” mopng.gov.in Indian Oil Corporation has earmarked USD 2 billion for 1,000 compressed-biogas plants by 2027, positioning the company as a multi-fuel supplier. The National Green Hydrogen Mission aims to achieve 5 million tonnes of annual production by 2030, creating opportunities for refiner-run electrolysis units that leverage captive renewables and desalinated water. While feedstock pricing remains volatile, government purchase incentives and global interest in green ammonia offtake provide revenue certainty and diversify the India oil and gas downstream market.

Digital Refinery OPEX Optimization

Partnerships such as HPCL-Mittal Energy and AVEVA deploy AI-enabled digital twins to reduce unplanned downtime and cut operating costs by 15%.[4]AVEVA, “HPCL-Mittal Energy Selects AVEVA Digital Twin,” aveva.com Predictive maintenance applications extend equipment life, while advanced process controls maximize energy efficiency, shaving several dollars per barrel off manufacturing cost. Blockchain pilots are enhancing product traceability, a growing requirement for aviation-grade fuel and petrochemical exports. Consequently, digital spend is being capitalized as a competitive edge rather than pure overhead, accelerating ROI cycles and attracting investor attention toward technologically mature players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex overruns & delays | -0.70% | National, affecting major expansion projects | Medium term (2-4 years) |

| Margin volatility vs crude prices | -0.50% | National, with higher impact on smaller refiners | Short term (≤ 2 years) |

| ESG / net-zero capital flight | -0.40% | National, with focus on coal-dependent regions | Long term (≥ 4 years) |

| EV adoption biting gasoline demand | -0.30% | Metro cities and EV adoption corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capex Overruns & Delays

Project delays averaging 18–24 months and cost overruns up to 40% plague greenfield and expansion schemes, straining balance sheets and diluting forecast capacity additions in the India oil and gas downstream market. Environmental clearances, land acquisition disputes, and skilled labor shortages emerge as the primary bottlenecks. Bharat Petroleum’s Bina expansion, for instance, slipped 30 months and ballooned to USD 4.1 billion, eroding IRR assumptions. Financing costs rise with each schedule slippage, curtailing dividend flexibility and nudging boards toward more conservative investment pacing or asset-light partnerships.

Margin Volatility vs. Crude Prices

Rapid crude swings compress refinery gross-processing spreads, especially for simple refineries lacking residue-conversion units. Smaller players with limited trading desks struggle to hedge effectively, leading to cash-flow shocks and inventory-loss accounting when prices whipsaw. Integrated operators counter this risk through petrochemical-linked offtake contracts and hedging strategies, but volatility remains a drag on sector-wide profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Capacity Dominated by Refineries While Petrochemicals Accelerate

Refineries account for 65.12% of India's oil and gas downstream market share in 2025, reflecting the long-standing government emphasis on energy security through import-substitution refining. Jamnagar alone processes more than 1.3 million barrels per day, underpinning India's status as a net product exporter. This segment benefits from additional residential upgrading investments that increase diesel and jet-fuel yields and support lucrative exports to Europe and Africa. However, petrochemical plants—though smaller in base—are set to log a 7.22% CAGR to 2031, driving the fastest volumetric expansion across the India oil and gas downstream market.

The push toward integrated O2C complexes allows operators to toggle feedstocks between fuels and chemicals based on margin signals. ONGC Petro Additions Limited's Dahej complex exemplifies such flexibility, channeling refinery naphtha into polymer chains that command higher spreads compared to simple distillates. Technology upgrades under the Petroleum and Explosives Safety Organisation framework improve process safety, further strengthening investor confidence in new chemical units adjacent to legacy refineries.

By Product Type: Refined Fuels Dominate as Petrochemicals Surge

Refined petroleum products held 67.54% share of the India oil and gas downstream market size in 2025, led by diesel for freight transport and gasoline for a growing vehicle fleet. BS-VI premium fuel sales and middle-class lubricant upgrades buoy the segment even as efficiency gains temper volume trajectories. In contrast, petrochemicals’ 6.94% CAGR through 2031 positions chemicals as the structural growth pillar, reflecting the manufacturing renaissance spurred by domestic value-addition incentives.

Polymer-grade propylene and specialty aromatics gain prominence as plastic-processing, textile, and automotive clusters proliferate. Reliance’s O2C strategy secures feedstock integration, enabling seamless naphtha transfer from the CDU to the cracker, thereby maximizing margin capture. Meanwhile, ESG frameworks stimulate investment in cleaner production methods such as low-emission ethane crackers and carbon-capture-ready aromatics units.

By Distribution Channel: Retail Dominance With Digital Evolution

Retail fuel outlets captured 59.92% share of the India oil and gas downstream market size in 2025, a testament to the country’s sprawling highway network and dispersed urbanization. Direct-sales contracts service large industrial accounts, whereas independent dealers sustain hinterland availability. Digital transformation is elevating operational efficiency—Indian Oil’s nationwide rollout of IoT-enabled dispensers provides real-time inventory and quality monitoring, reducing shrinkage and enhancing billing transparency. Retail sites increasingly bundle compressed natural gas, EV charging, and biofuel blends, future-proofing forecourt relevance.

Wholesale channels navigate thinner margins but benefit from volume stability through contract markets, such as railways, defense, and state transport units. Distributor-led secondary logistics remain crucial for remote districts, though their margin stack is under pressure from rising fuel logistics costs and increasing digital disintermediation.

Geography Analysis

Gujarat leads the India oil and gas downstream market with more than 2 million barrels per day refining capacity anchored by the coastal Jamnagar and Vadinar complexes. Maharashtra follows, leveraging the Mumbai–Pune petrochemical corridor that supports the demand for specialty chemicals in automotive and consumer goods manufacturing. Northern belt states consume substantial volumes of diesel for agriculture and trucking, thereby sustaining refinery output from Mathura, Panipat, and Bathinda.

Southern states—including Tamil Nadu, Karnataka, and Telangana—are emerging as petrochemical hotspots, propelled by electronics, textile, and pharma clusters. This shift drives storage-terminal development at Ennore and Krishnapatnam ports, which shortens supply lead times and lower domestic freight costs. Eastern India’s downstream template is evolving; Assam’s crude output and Numaligarh Refinery’s expansion promise regional self-sufficiency, while West Bengal’s industrial base presents demand opportunities despite infrastructural gaps.

The geographically varied environmental regulations shape investment behavior; coastal refineries face stringent marine-emission norms, whereas inland units confront air-quality directives targeting particulate matter. Consequently, capital-budget allocation differs by state, introducing complexity to cross-portfolio optimization strategies for multi-location refiners.

Competitive Landscape

Market concentration is at a moderate level, with Indian Oil, Bharat Petroleum, Hindustan Petroleum, and Reliance Industries controlling the majority of refining and retail assets. State-owned enterprises safeguard national energy security through broad depot and pipeline coverage, whereas Reliance pushes the envelope in terms of process complexity and export orientation. Nayara Energy and HPCL-Mittal Energy bring private-sector dynamism, scaling capacity through brownfield expansions and technology partnerships.

Differentiation now hinges on integration depth, digital maturity, and carbon transition readiness, rather than mere throughput. AI-driven predictive maintenance, blockchain-powered supply chain validation, and customer experience applications weigh heavily in investment narratives. Niche players exploit whitespace in specialty chemicals, biofuels, and green-hydrogen off-take agreements, circumventing head-to-head competition with incumbents. The Petroleum and Natural Gas Regulatory Board’s transparent pipeline tariff regime and open-access rules facilitate new entrant participation without compromising system integrity.

India Oil And Gas Downstream Industry Leaders

Indian Oil Corporation Limited

Bharat Petroleum Corporation Limited

Hindustan Petroleum Corporation Limited

Reliance Industries Limited

Nayara Energy Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Shipping Corporation of India Limited (SCI) has signed an MoU with BPCL, HPCL, and IOCL to jointly acquire, own, and operate a fleet of crude oil tankers for transporting petroleum, petrochemicals, and other hydrocarbon cargo both internationally and along the coast.

- August 2025: BPCL is planning a major INR 95,000 crore investment to build a new refinery and petrochemical complex near Ramayapatnam Port in Andhra Pradesh, with a capacity to refine about 9 million tonnes of crude oil each year.

- April 2025: Indian Oil Corporation Ltd. (Indian Oil) signed an MoU with the Government of Odisha to establish an INR 61,077-crore world-class petrochemical complex at Paradip.

- January 2025: Nayara Energy, backed by Rosneft, announced plans to invest ₹68,000 crore to build a 1.5 mtpa ethane cracker at its Vadinar refinery in Gujarat, marking a significant overseas investment to strengthen India’s growing petrochemical sector, with front-end engineering work already underway.

India Oil And Gas Downstream Market Report Scope

The processes of refining, marketing, and eventually selling petroleum products are referred to as downstream. In the downstream business, a corporation refines crude oil and natural gas and markets and sells petroleum products to wholesale and retail customers. Processed natural gas is often sold directly to electric and gas utilities.

The India Oil and Gas Downstream Market is segmented by refineries and petrochemical plants. The report offers the market size and forecasts for refining capacity (million barrels per day) for all the above segments.

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

How large is the India oil and gas downstream market in 2026?

The India oil and gas downstream market size is USD 5.36 billion in 2026, projected to reach USD 6.81 billion by 2031.

What CAGR is expected for India's downstream sector between 2026 and 2031?

The market is forecast to post a 4.89% CAGR over 2026-2031.

Which segment is growing fastest within India's downstream value chain?

Petrochemical plants are expected to grow at 7.22% CAGR through 2031, outpacing traditional fuel refining.

What role does BS-VI fuel compliance play in market growth?

BS-VI regulations triggered over USD 15 billion in refinery upgrades, enabling higher-quality fuel output and spurring efficiency gains.

How is rising EV adoption affecting gasoline demand?

EV penetration could displace up to 20% urban gasoline demand by 2031, prompting refiners to shift focus toward jet fuel, marine bunkers and petrochemicals.

Which states house the largest refining capacities in India?

Gujarat leads with Jamnagar and Vadinar complexes, followed by Maharashtra and northern belt facilities such as Mathura and Panipat.

Page last updated on: