Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.08 Billion |

| Market Size (2026) | USD 16.93 Billion |

| Market Size (2031) | USD 21.56 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Oil And Gas Upstream Market Analysis by Mordor Intelligence

The India Oil and Gas Upstream Market size is projected to be USD 16.08 billion in 2025, USD 16.93 billion in 2026, and reach USD 21.56 billion by 2031, growing at a CAGR of 4.95% from 2026 to 2031, reflecting the sector’s gradual transition from legacy production decline to technology-driven recovery initiatives.

Strong policy support, digital-oilfield roll-outs, and enhanced-oil-recovery (EOR) projects offset the drag from geological complexity, enabling operators to extract additional barrels from maturing assets and thereby slowing import growth. Capital is shifting toward deepwater prospects where large discoveries can be tied back to existing infrastructure, while a wave of decommissioning contracts emerges as India’s first generation of offshore platforms nears end-of-life. Private companies introduce agile drilling and completion technologies, yet state-owned enterprises retain strategic control through acreage holdings and legacy infrastructure. Supply-chain bottlenecks in rigs, proppants, and subsea equipment remain the principal operational headwinds but are gradually easing as domestic manufacturing expands under “Make in India” mandates.

Key Report Takeaways

- By resource type, crude oil retained 67.9% of 2025 revenue while natural gas is the fastest-growing segment is expected to advance at a 7.0% CAGR through 2031.

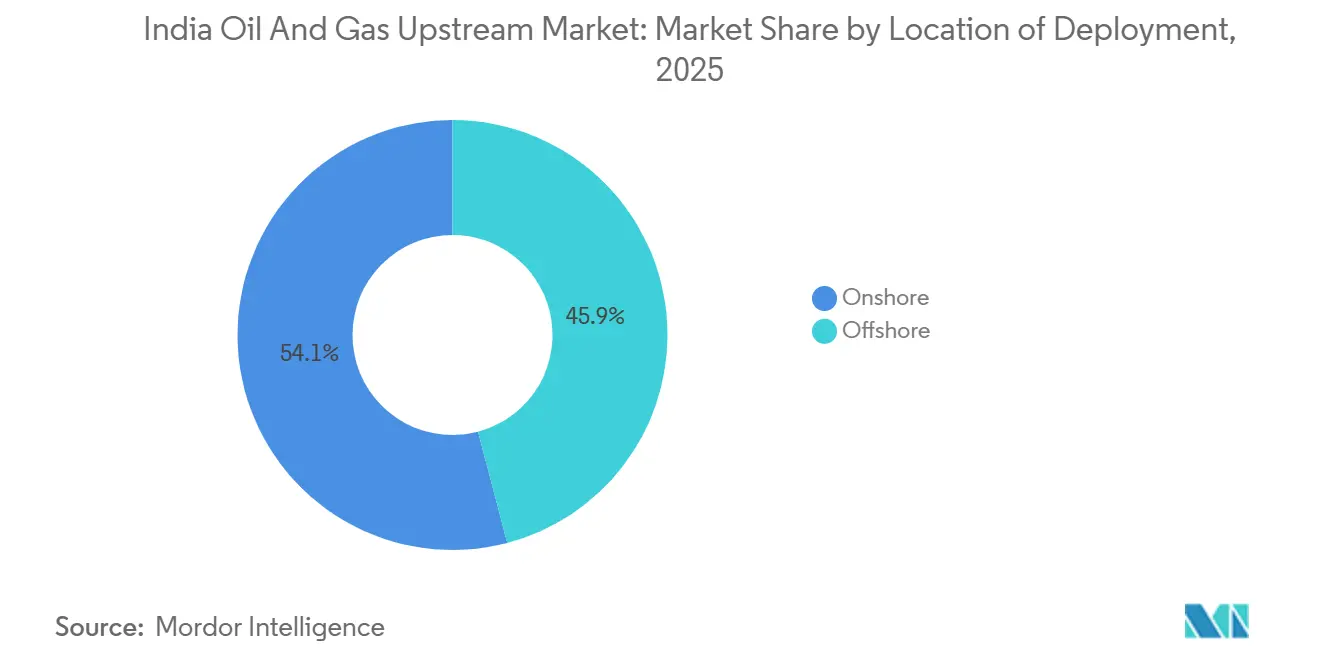

- By location of deployment, onshore fields led with 54.1% of the 2025 value, but offshore blocks, especially deep-water Krishna-Godavari, are projected to expand at 6.4% CAGR over 2026-2031.

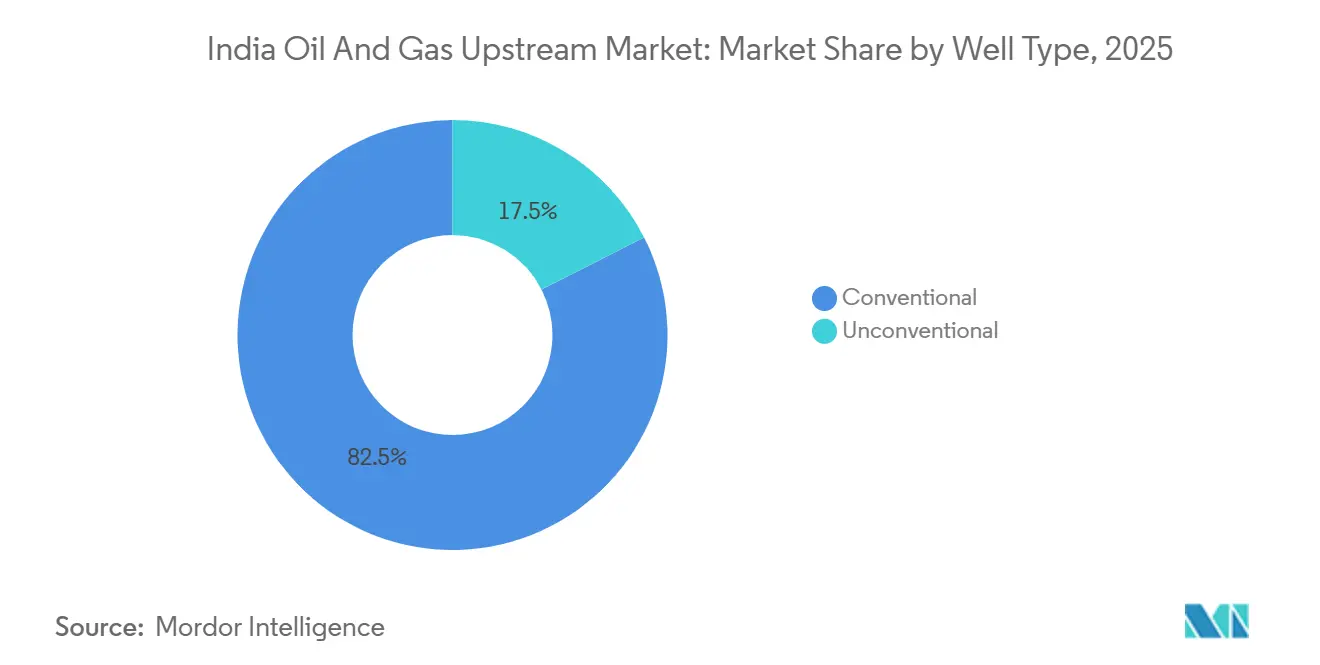

- By well type, conventional wells held 82.5% of 2025 activity, whereas unconventional wells are expected to climb at 6.2% CAGR through 2031.

- By service, development and production accounted for 64.7% of 2025 expenditure; decommissioning is expected to grow at 6.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining domestic output spurring EOR investments | +1.2% | National, concentrated in Mumbai High, Cambay Basin, Rajasthan | Medium term (2-4 years) |

| Expansion of OALP bid rounds & HELP incentives | +1.5% | National, with frontier basins in Andaman, Vindhyan, Saurashtra gaining traction | Long term (≥4 years) |

| Gas-price indexation reforms improving project economics | +1.0% | National, particularly benefiting KG Basin, Mahanadi Basin gas discoveries | Short term (≤2 years) |

| Digital-oilfield adoption led by Indian IT majors | +0.8% | National, early deployments in ONGC Mumbai High, OIL Assam fields | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Domestic Output Spurring EOR Investments

India’s crude output slipped to 29.4 million tonnes in 2025, intensifying the push for tertiary recovery methods that can lift ultimate recovery by 10-15%.[1]Ministry of Petroleum & Natural Gas, “Indian Petroleum Statistics 2025,” mopng.gov.in ONGC green-lit a USD 680 million alkali-surfactant-polymer flood at the Jhalora field, aiming for an extra 12 million barrels over eight years. Vedanta’s polymer program in the Mangala field already lifted the recovery factor from 28% to 36% by mid-2025, extending plateau production by up to six years. Oil India’s cyclic-steam pilot reached a favorable steam-oil ratio of 2.8, opening commercial prospects for 180 million barrels of heavy oil. These initiatives remain sensitive to Brent; a 15% price slide would erode project economics because tertiary barrels cost USD 22-28 per barrel to lift, roughly double primary extraction costs.

Expansion of OALP Bid Rounds & HELP Incentives

OALP Round X awarded 31 blocks covering 58,000 km² in February 2026, including nine deep-water Andaman tracts that had never drawn bids under earlier fiscal terms.[2]Directorate General of Hydrocarbons, “OALP Round X Press Release,” dghindia.gov.in HELP’s revenue-share contracts let operators deduct full exploration write-offs, trimming the effective tax burden on frontier discoveries to 52%. Participation broadened to 14 new entrants, three of them renewable-energy conglomerates hedging transition risk, though ONGC and Oil India still captured most acreage by offering higher government takes. A new drill-or-drop clause forces spud-in within 36 months, discouraging speculative hoarding that once left 42% of licensed acreage idle. Early 3D seismic in the Mahanadi offshore block has already mapped four leads with 1.2 Tcf of prospective gas, yet first production remains seven-plus years away because deep-water tiebacks demand upfront capital of USD 300-500 million.

Gas-Price Indexation Reforms Improving Project Economics

Quarterly indexation linked to Henry Hub, National Balancing Point, and AECO benchmarks raised the administered ceiling for legacy gas from USD 6.50 to USD 8.20 per MMBtu in 2025, shrinking the gap with spot LNG that averaged USD 11.40 in early 2026.[3]Petroleum Planning & Analysis Cell, “Gas Price Notification January 2025,” ppac.gov.in The higher ceiling improved internal rates of return on marginal fields by 3-4 percentage points. Reliance-BP’s USD 1.1 billion satellite development in KG-DWN-98/2 leverages the reform; the 22-kilometer flowline reaches existing infrastructure and will add 5 MMSCMD by late 2027. A floor of USD 4.00 per MMBtu protects projects from price shocks seen in 2020, yet coal-bed methane and shale gas remain capped at USD 5.61, discouraging unconventional investment despite sizeable resource potential.

Digital-Oilfield Adoption Led by Indian IT Majors

ONGC’s Pragya-AIX platform now streams 3,200 wellheads’ data into machine-learning models that forecast failures 72 hours ahead, cutting downtime by 18% and safeguarding USD 47 million of output in 2025. Tata Consultancy Services handles edge analytics to avoid cybersecurity and latency risks that cloud transmission poses to four offshore platforms in 2024. Schlumberger’s DELFI pilot at Oil India’s Jorajan field sliced drilling non-productive time from 22% to 14% by auto-calibrating geosteering parameters. Reliance-IBM digital twins modeled 10,000 production scenarios for KG-D6, extending plateau life by 18 months. The bottleneck is talent; only 8% of the 12,000 petroleum engineers graduating each year possess data-science skills, forcing operators to second-staff from IT firms at 40-60% cost premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geological complexity of mature onshore basins | -0.4% | National, acute in Assam-Arakan fault-block reservoirs, Cambay heterogeneous carbonates, Mumbai High pressure-depleted zones | Long term (≥4 years) |

| Prolonged environmental & land-acquisition approvals | -0.4% | National, particularly severe in ecologically sensitive zones like Dibru-Saikhowa, Western Ghats, coastal regulation zones | Long term (≥4 years) |

| Shortage of fracking-grade domestic proppant supply | -0.3% | National, constraining unconventional plays in Cambay shale, Damodar CBM, tight-gas formations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Geological Complexity of Mature Onshore Basins & Prolonged Environmental Approvals

Mumbai High’s 47-year output history has driven reservoir pressure below bubble-point in 60% of fault blocks, triggering gas breakout that undermines oil mobility. Water-alternating-gas schemes now cost USD 18-24 per incremental barrel. Cambay Basin carbonates vary in permeability by three orders of magnitude within 50 meters, making uniform waterfloods ineffective and forcing 18-24 months of reservoir modeling to calibrate geostatistics. In Assam-Arakan, faulted Barail sandstones average eight-hectare attic compartments that demand four to six vertical producers for commerciality, driving finding-and-development costs above USD 30 per barrel. Meanwhile, ONGC’s Dibru-Saikhowa campaign spent 31 months awaiting forest clearance; final approval limits drilling to four dry-season months and mandates real-time wildlife surveillance.[4]Ministry of Environment, “Forest Clearance Order for Dibru-Saikhowa,” moef.gov.in A 2024 Wildlife Act amendment also obliges operators to fund habitat trusts equal to 2% of project capex, extending payback periods by up to nine months.

Shortage of Fracking-Grade Domestic Proppant Supply

Anti-dumping duties imposed in 2025 cut Chinese ceramic-proppant imports by 22%, shrinking supply to 142,000 tonnes.[5]Directorate General of Trade Remedies, “Anti-Dumping Duty on Ceramic Proppant,” dgtr.gov.in ONGC’s Mehsana plant adds 60,000 tonnes annually, but its 8,000-psi crush strength limits use to formations shallower than 3,000 meters. Deep Cambay shale targets need 12,000-psi material, while Damodar coal-bed methane seams require blends of costly ceramic and resin-coated sand, inflating completion costs by USD 0.5 million per well. Nine unconventional pilots were delayed in 2025 as operators rationed proppant among higher-return wells. Carbo Ceramics is building a USD 85 million Gujarat facility due online in 2027, but supply will remain tight for at least another 18 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Momentum Outpaces Onshore Scale

Offshore developments are growing at 6.4% CAGR to 2031, while onshore assets expand by just 3.8%, yet onshore still contributed 54.1% of the 2025 value to the Indian oil and gas upstream market. Reliance-BP proved that subsea tiebacks can halve development timelines; KG-D6 moved from sanction to 28 MMSCMD within two years by leveraging existing manifolds. ONGC’s 98/2 deep-water plan needs a 180-kilometer pipeline that adds USD 620 million, delaying first gas to 2029.

Onshore projects benefit from mature flowline grids: Vedanta’s Barmer hub ties 340 wells into central processing at a finding-and-development cost 34% below typical offshore analogs, reinforcing near-surface economics. However, 14 of 37 shallow-water Cambay jackets need structural upgrades by 2028, a USD 190 million bill that depresses returns on maturing assets. The upcoming offshore-wind zoning has forced operators to relinquish 18% of prospective acreage in Gujarat and Tamil Nadu seas, curbing future exploration space.

By Resource Type: Gas Ascends While Oil Stagnates

Natural gas registers the highest growth in the Indian oil and gas upstream market, advancing at 7.0% CAGR through 2031 on the back of 12.8 million new city-gas connections added in 2025. Crude oil, despite 67.9% 2025 share, confronts structural headwinds as domestic volumes dipped to 29.4 million tonnes and import dependency hit 87.3%.

Reliance-BP lifted KG-D6 output to 30 MMSCMD in December 2025, covering 11% of national demand and trimming LNG imports priced at USD 11.20 per MMBtu. Power-sector gas use climbed 9.2% in 2025 with 4.8 GW of new combined-cycle capacity. Oil recovery factors remain low: Mumbai High averages 32%, spurring plans for miscible CO₂ injection that would require a USD 1.2 billion capture hub. Infrastructure lags hamper monetization; the Urja Ganga line ran at only 62% utilization owing to city-gas construction delays in Uttar Pradesh and Bihar.

By Well Type: Conventional Workhorses, Unconventional Promise

Conventional wells dominated 82.5% of 2025 activity in the Indian oil and gas upstream market, focusing on proven Miocene and Eocene reservoirs. Unconventional drilling is expanding at 6.2% CAGR, yet Cambay shale horizontals suffered 68% first-year decline, exposing the need for tighter spacing and multi-stage fracs constrained by proppant supply.

Optimization is data-driven: fiber-optic sensing on the Neelam platform restored 840 BOPD by catching behind-casing flow at a fraction of sidetrack costs. Heavy-oil cyclic-steam pilots achieved 22% recovery, but carbon intensity is three times that of conventional barrels, posing future regulatory risks. Coal-bed methane volumes rose 14% to 1.1 BCM, still minor because water-disposal ceilings cap output in ecologically sensitive districts.

By Service: Production Dominates, Decommissioning Emerges

Development and production captured 64.7% of 2025 spend; exploration received 18.2%, with ONGC budgeting USD 1.1 billion for 12,000 km² of 3D seismic in the Mahanadi and Andaman frontier basins. Decommissioning is the fastest-growing slice of the Indian oil and gas upstream market at 6.8% CAGR, as new rules require platform removal within five years of cessation, translating to sector-wide liabilities of USD 4.2 billion through 2035.

Heavy-lift vessel scarcity presents a logistical choke point; India fields only two units able to handle 4,000-8,000-tonne jackets, forcing operators to charter foreign assets at dayrates of USD 320,000-450,000. Production services are pivoting to automation: 87 wells now run Schlumberger electric submersible pumps that trim power by 11% and extend run life to 26 months, evidencing a move toward predictive maintenance.

Geography Analysis

Mature western-offshore and emerging eastern deep-water provinces jointly supplied 64% of the national upstream value in 2025, yet they present contrasting risk-reward profiles. Mumbai High yielded 11.8 million tonnes of crude in 2025, but the average water cut has risen to 52%, hiking operating costs to USD 22 per barrel. Gas-rich Krishna-Godavari fields ramped quickly; KG-D6 alone delivers 30 MMSCMD at a unit development cost of USD 1.8 per thousand cubic feet, 38% below standalone-platform averages.

Rajasthan’s Barmer basin produced 172,000 BOPD in 2025 from thick Fatehgarh sandstones; polymer floods here improve sweep efficiency and keep lifting costs competitive. Assam-Arakan’s thrust-faulted reservoirs generated 3.6 million tonnes, but demand multiple producers per lens, inflating costs above USD 30 per barrel. Cambay Basin’s carbonate heterogeneity drags waterflood recovery to 22%, prompting pilots for miscible-gas injection.

OALP has pushed the exploration frontier eastward: nine Andaman deep-water blocks and seven Vindhyan tracts were licensed in 2026, but first output is unlikely before 2031 given seismic, drilling, and pipeline lead times. Northeast gas monetization hinges on the delayed Barauni-Guwahati pipeline, now due 2027 after land-acquisition setbacks across 14 districts.

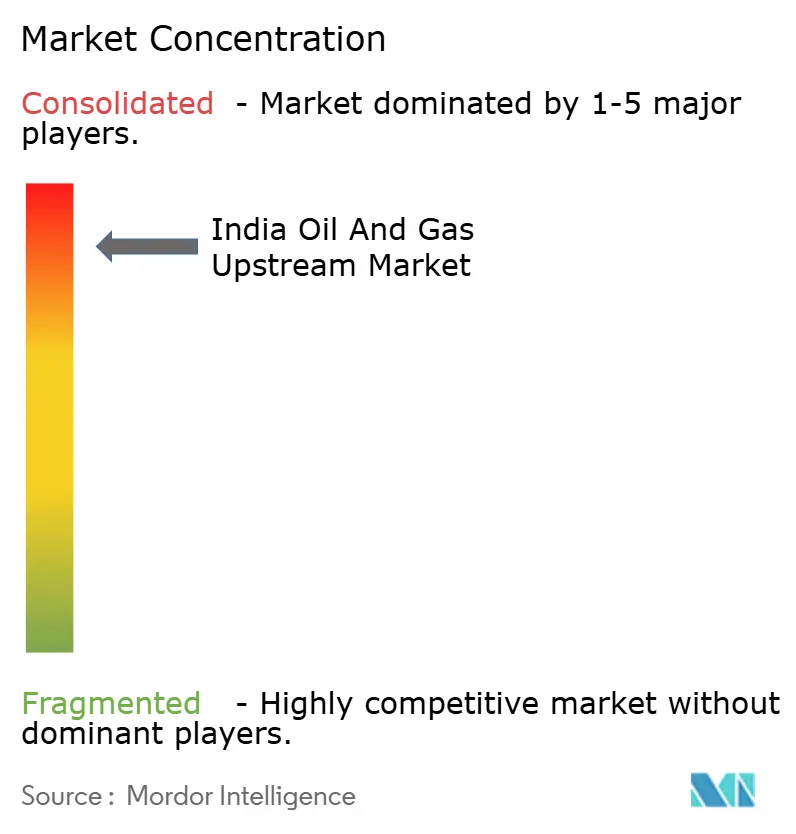

Competitive Landscape

The Indian oil and gas upstream market is consolidated. Private joint ventures such as Reliance-BP combine capital discipline with subsea know-how, achieving a 60% exploration success rate in the Krishna-Godavari basin, more than double the national mean. Vedanta’s polymer flood raised the Mangala recovery factor by eight percentage points, but break-even hinges on prices above USD 68 per barrel, leaving projects exposed to demand-side shocks.

White-space opportunities cluster in unconventional gas, decommissioning, and digital services. Only two domestic heavy-lift vessels exist for 127 platforms scheduled for removal, creating urgent demand for marine-contracting capacity. Digital twins and edge analytics trimmed ONGC downtime by USD 47 million in 2025, yet 60% of onshore wells still rely on manual choke adjustments, signaling uneven technology diffusion.

Smaller independents such as Hindustan Oil Exploration produce a combined 8,400 BOE/D, too little for stand-alone facilities; they must accept throughput fees that capture up to 24% of wellhead value, eroding project economics. Service companies answer with modular processing skids and rental compression, lowering threshold volumes for economic tie-ins.

India Oil And Gas Upstream Industry Leaders

Oil and Natural Gas Corporation

Reliance Industries Limited

Oil India Limited

Hindustan Oil Exploration Co.

Vedanta Ltd (Cairn)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The SEAMEC-led consortium has secured a USD 34.19 million contract from ONGC for the operation and maintenance of the offshore support vessel “Samudra Prabha” during the period 2026–2028.

- August 2025: SNF acquired Obsidian Chemical Solutions, a rapidly growing specialty chemicals provider in the Permian Basin. This acquisition enhances SNF’s capabilities in stimulation, acidizing, cementing, drill-out, and produced-water treatment. The deal expands SNF’s service efficiency, manufacturing capacity, and product offerings for oil and gas customers.

- August 2025: HPCL entered into a 10-year LNG supply agreement with ADNOC Gas for 0.5 mmtpa. This agreement strengthens India's natural gas supply and supports its objective of increasing the share of gas in its energy mix. The deal also enhances energy ties between India and the UAE, ensuring stable LNG imports through the Chhara terminal.

- July 2025: Reliance, ONGC, and BP signed a joint operating agreement for offshore exploration in Block GS-OSHP-2022/2 within the Saurashtra Basin, covering an area of 5,454 km². ONGC will lead the exploration efforts to evaluate the hydrocarbon potential of the block. This collaboration represents a significant step toward strengthening India’s long-term energy security.

India Oil And Gas Upstream Market Report Scope

Upstream refers to the exploration and production stages of the oil and gas industry. From the preliminary exploration stage through extraction, the upstream sector of the oil and gas industry focuses on all steps involved. The Indian oil and gas upstream market scope includes:

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decomissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decomissioning |

Key Questions Answered in the Report

What is the forecast value of the India oil and gas upstream market by 2031?

The India oil and gas upstream market is projected to reach USD 21.56 billion by 2031.

How fast is natural gas production expected to grow?

Natural gas output is forecast to expand at a 7.0% CAGR between 2026 and 2031, the quickest among resource types.

Which segment is rising fastest in services spending?

Decommissioning services are the fastest-growing slice, advancing at 6.8% CAGR as 127 platforms near end-of-life.

Why are enhanced-oil-recovery projects accelerating?

Declining mature-field output and supportive Brent prices have pushed operators to adopt polymer and chemical floods that can raise recovery by up to 15%.

How do recent gas-pricing reforms help project economics?

A higher ceiling of USD 8.20 per MMBtu and a USD 4.00 floor narrowed the gap with LNG, adding 3-4 percentage points to internal rates of return on marginal gas fields.

What supply bottleneck affects unconventional drilling?

Domestic shortages of high-strength ceramic proppant have delayed nine shale and CBM pilots, a gap only partly closed by ONGC's new Mehsana plant.

Page last updated on: