India Precipitated Silica Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

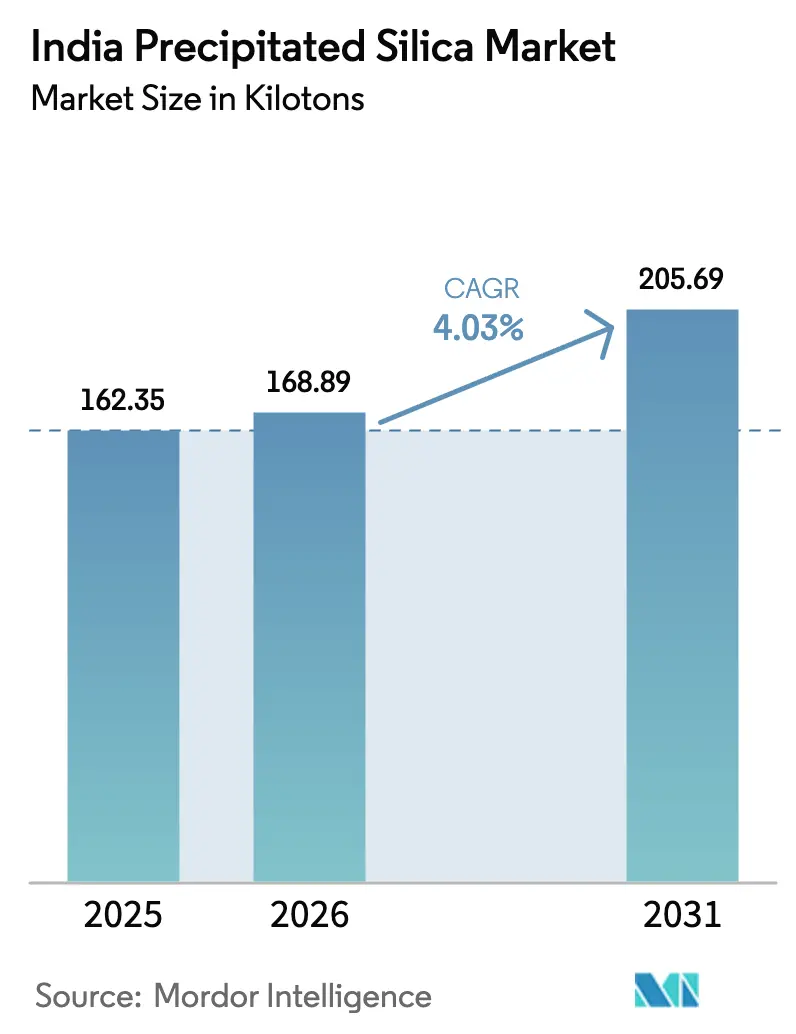

| Base Year Market Size (2025) | 162.35 kilotons |

| Market Volume (2026) | 168.89 kilotons |

| Market Volume (2031) | 205.69 kilotons |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Precipitated Silica Market Analysis by Mordor Intelligence

The India Precipitated Silica Market size was valued at 162.35 kilotons in 2025 and estimated to grow from 168.89 kilotons in 2026 to reach 205.69 kilotons by 2031, at a CAGR of 4.03% during the forecast period (2026-2031). Momentum stems from the automotive sector’s shift toward fuel-efficient tires, the premiumization of fast-moving consumer goods, and policy support for localized solar-glass and agrochemical manufacturing. Tire makers continue to optimize rolling resistance and durability, lifting silica loading per unit and underpinning steady offtake. Consumer trends toward low-VOC toothpastes and cosmetics accelerate demand for specialty grades that command higher margins. On the supply side, capacity additions by domestic chemical majors and soda-ash expansions in Gujarat improve raw-material availability, although environmental compliance costs and Chinese imports weigh on margins. These forces collectively propel the India precipitated silica market toward higher-value, application-specific products rather than pure tonnage growth, signaling a transition phase in industry maturity.

Key Report Takeaways

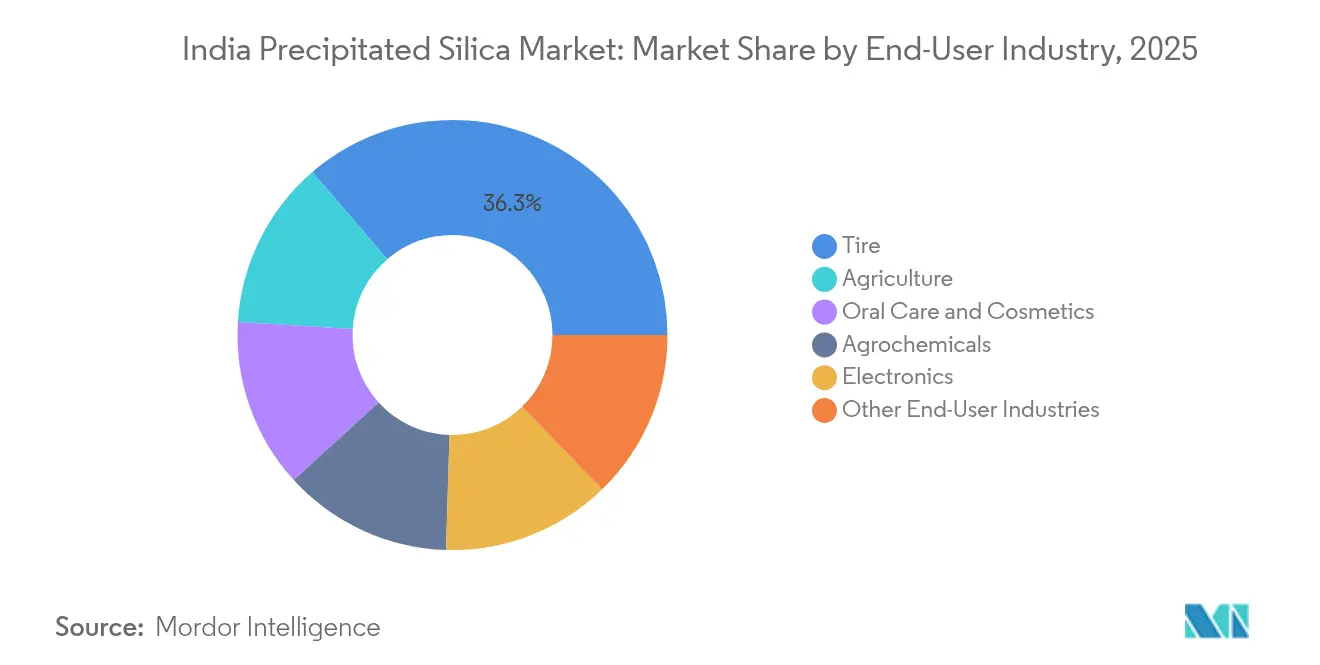

- By end-user industry, tires held 36.30% of the India precipitated silica market share in 2025, while oral care and cosmetics are projected to expand at a 5.12% CAGR through 2031.

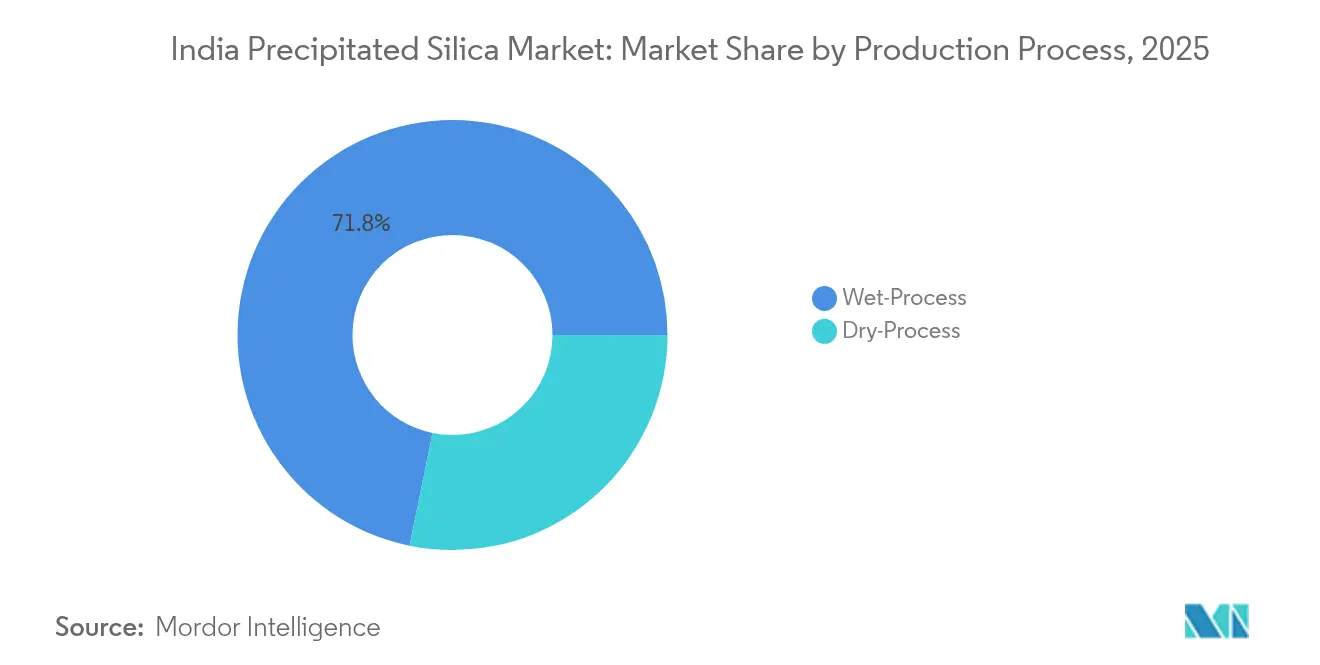

- By production process, the wet method held a 71.80% share in 2025; the dry method is expected to advance at a 4.19% CAGR between 2026 and 2031.

- By product form, powder accounted for 48.60% revenue share in 2025, whereas micro-pearls are forecast to grow at a 4.87% CAGR through 2031.

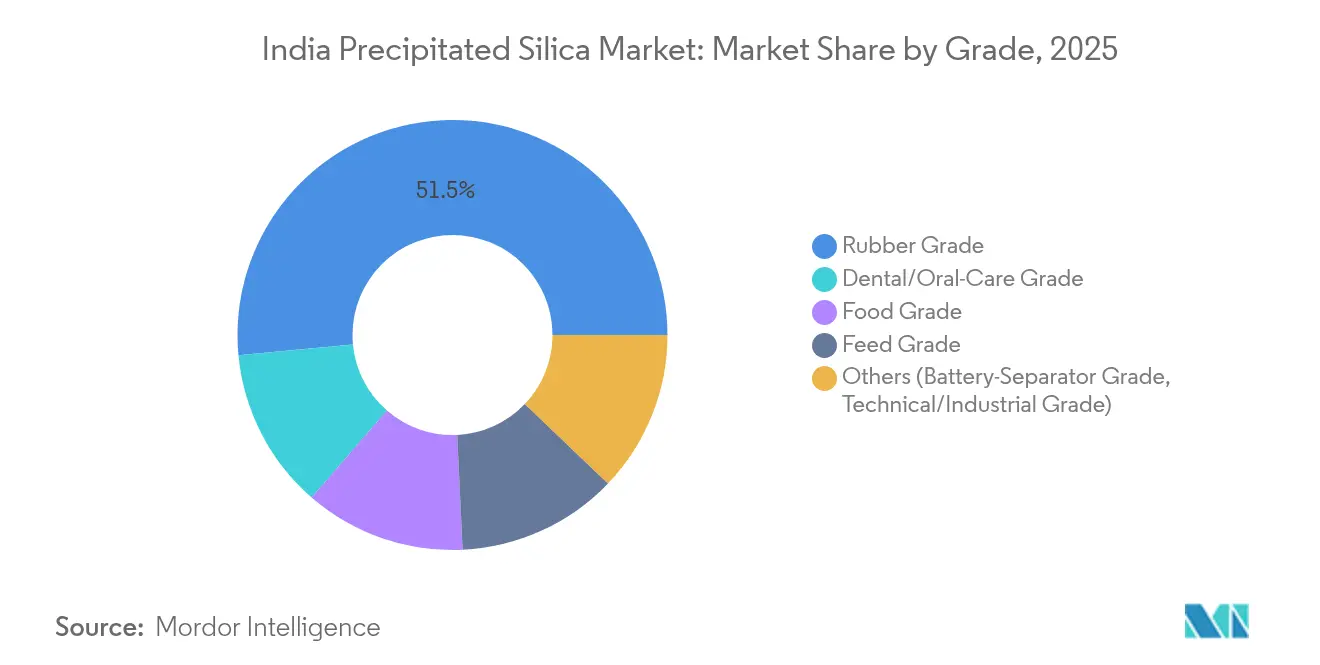

- By grade, rubber grade commanded 51.50% of the India precipitated silica market size in 2025; food grade is expected to register the fastest growth at 5.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on precipitated silica market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Precipitated Silica Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tire-grade silica demand from domestic OEM-focused rubber industry | +1.20% | West & South India with spillover to North India | Medium term (2-4 years) |

| Rapid shift toward low-VOC toothpastes by FMCG majors | +0.80% | National, early gains in urban markets | Short term (≤2 years) |

| Government push for solar PV glass fabs | +0.60% | Gujarat, Tamil Nadu expanding nationwide | Long term (≥4 years) |

| Mandatory BIS compliance for agrochemical wettable powders | +0.40% | National, agrochemical hubs | Medium term (2-4 years) |

| Start-up-led silica-based battery anode R&D | +0.20% | Karnataka, Telangana, potential national spread | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Tyre-Grade Silica Demand from Domestic OEM-Focused Rubber Industry

Domestic tire manufacturers now integrate higher silica loadings to meet stringent fuel-efficiency and emission norms, positioning precipitated silica as a performance-critical additive rather than a commodity input. CEAT’s ramp-up from 105 tons per day to 160 tons per day in its off-highway tire unit, along with its 25% export revenue target, illustrates how scale and global diversification underpin demand resilience. Import restrictions that reclassified several tire categories from “Free” to “Restricted” in 2020 cut foreign inflows by more than 80%, effectively channeling silica demand to domestic supply chains. Growing SUV sales and the radialization wave translate into larger tire dimensions and greater silica dosage, further anchoring consumption. The India precipitated silica market benefits directly as high-performance mixes offer pricing latitude that preserves manufacturer margins amid feedstock volatility. These interlinked automotive trends provide a multi-year volume corridor sustaining a progressive upswing in specialty rubber grades.

Rapid Shift Toward Low-VOC Toothpastes by FMCG Majors

FMCG players are reformulating oral-care lines to eliminate volatile organic solvents, incentivizing the use of precipitated silica as both an abrasive and rheology modifier. Colgate Palmolive India aims to triple premium-segment revenues, where margins are 5-8 percentage points higher, and mandates silica grades that deliver enhanced whitening and mouth-feel properties. Rural hygiene penetration remains low, with only 20% of urban consumers brushing their teeth twice daily, indicating untapped volume upside as awareness increases. BIS standard IS 6356:2001 formally lists precipitated silica among accepted polishing agents, providing regulatory certainty for formulators. Combining premiumization and compliance unlocks a new value pool for the India precipitated silica market, even before considering spillovers into cosmetics and personal-care categories.

Government Push for Solar PV Glass Fabs (Greenfield)

The Production Linked Incentive scheme, earmarking INR 4,500 crore for solar module manufacturing, enforces domestic value-addition thresholds that cascade upstream to specialty silica used in solar glass[1]Press Information Bureau, “National Programme on High Efficiency Solar PV Modules,” pib.gov.in . Planned additions of 10 GW integrated capacity call for local sourcing of high-purity silica to optimize melt coefficients and transmission rates. GHCL’s clearance for a 500,000-ton soda-ash expansion in Kutch underscores the strategic coupling of alkali chemicals and renewable infrastructure. A 10% import duty on solar glass and content requirements across subsidy programs shield emerging fabs from price erosion, bolstering predictable silica uptake. Although this driver manifests over a longer horizon, its scale could reshape regional demand clusters, cementing India's precipitated silica market as a pivotal materials contributor to the energy transition.

Mandatory BIS Compliance for Agrochemical Wettable Powders

BIS mandates on pesticide formulations are accelerating reformulation activity among agrochemical makers, who rely on precipitated silica for flow control, dispersion stability, and anti-caking performance. India Chemicals Management and Safety Rules require registration for substances above 1 tonne annually, formalizing demand for consistent-quality silica grades. Water-dispersible granules developed by IPFT emphasize solvent-free systems, aligning with silica’s functional advantages in particle-size optimization. Anti-dumping duties on sodium cyanide imports further localize chemical supply chains, indirectly fortifying domestic silica demand. Compliance drivers thus create a defensible, regulation-anchored growth pocket that buffers the India precipitated silica market from automotive cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening effluent norms on sodium silicate effluents | -0.70% | Nationwide, stricter in industrial clusters | Short term (≤2 years) |

| Volatility in soda-ash prices | -0.50% | National footprint | Short term (≤2 years) |

| Import penetration of low-cost Chinese grades | -0.30% | National, acute in price-sensitive applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Effluent Norms on Sodium Silicate Effluents

Regulatory scrutiny over liquid discharges is escalating capital requirements for wet-process units, which account for more than 70% of domestic capacity. Draft CPCB guidelines mandate zero-liquid-discharge systems, dust suppression, and water recycling across the silica value chain, inflating compliance costs. The May 2024 fire at Aksharchem’s Gujarat plant illustrates operational vulnerabilities faced during modernization. Smaller players lacking financial muscle may exit or delay upgrades, consolidating volume among large, compliant manufacturers. The India precipitated silica market, therefore, navigates a near-term supply tightening that offsets part of the demand gains while reinforcing competitive barriers.

Import Penetration of Low-Cost Chinese Grades

Despite elevated freight costs, Chinese suppliers still undercut domestic prices in powder and standard rubber grades. Local buyers in price-sensitive agrochemical or footwear sectors occasionally favor imports, pressuring domestic realizations. While import curb measures on tires absorbed some silica inflow, similar protections do not uniformly apply to filler chemicals, keeping a structural cost arbitrage open. Sustained R&D and customer partnerships are necessary for domestic players to defend shares in the India precipitated silica market until broad-based cost parity or additional trade measures materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Tire Dominance Drives Market Evolution

The tire segment captured 36.30% of the India precipitated silica market share in 2025, reflecting the automotive sector’s entrenched role in filler demand. Volume visibility remains high as OEMs integrate silica-reinforced compounds to hit rolling-resistance targets and emission standards. Concurrently, oral care and cosmetics, while having a smaller base, are forecast to post a 5.12% CAGR through 2031, evidencing diversification and premiumization in fast-moving consumer goods.

Tire-makers are regionalizing production; CEAT’s export-oriented capacity expansion and Apollo’s plans for greenfield off-the-road units highlight the global positioning of domestic brands. Meanwhile, agrochemical formulators adopt precipitated silica for wettable powder compliance, creating ancillary demand insulated from automotive swings. Electronics applications, though nascent, align with national semiconductor and battery programs, hinting at future pull for high-purity grades. This mosaic of use-cases nudges the India precipitated silica market toward specialized product lines, mitigating risk concentration in a single end-use.

By Production Process: Wet-Process Leadership Faces Technological Transition

Wet-process technology retained 71.80% dominance in 2025 as installed units leverage sunk costs and broad formulation acceptance. Yet environmental mandates and water-usage restrictions accelerate the dry-process CAGR to 4.19%, signaling gradual realignment toward lower-effluent routes.

Wet-process producers are retrofitting effluent-treatment plants to comply with tightened norms, which lifts capex per ton and may erode cost advantages. Dry-process adopters pitch energy savings and tighter morphology control, finding traction in oral-care and micro-pearl niches. Over the forecast horizon, the India precipitated silica market expects coexistence: wet processes serving large-volume, price-sensitive rubber applications, and dry processes capturing specialty and export-oriented segments.

By Product Form: Powder Prevalence Meets Specialty Morphology Growth

Powder grades held a 48.60% share in 2025, underscoring logistic familiarity and blending ease across industries. However, micro-pearls are set to grow at a 4.87% CAGR through 2031, driven by automated compounding lines that favor dust-free, free-flowing inputs.

Micro-pearls command premium pricing rooted in precise spray-drying techniques that fashion spherical particles with narrow size distribution. Downstream converters in the tire and personal care industries value these traits for reduced housekeeping and faster dispersion. Granules and beads occupy smaller niches where specific flow rate profiles are mandatory. The ascendancy of specialized morphologies confirms the India precipitated silica market’s maturation toward differentiated value propositions.

By Grade: Rubber Grade Strength Supports Food Grade Opportunities

Rubber grade silica dominated at 51.50% share in 2025, directly mirroring tire sector volumes. Food grade ranks as the fastest-growing at 5.07% CAGR to 2031, as fortified beverages, nutraceuticals, and food-additive formulations proliferate.

Rubber grade demand remains tightly correlated with vehicle production and replacement cycles, but its cyclicality is tempered by export footprints of domestic tire makers. Food, dental, and feed grades, governed by stringent purity standards, fetch higher margins and offer counter-cyclical buffers. Growing regulatory oversight and health awareness expand addressable volume, while feed and technical grades exploit inroads into battery separators and insulation composites. These grade dynamics diversify revenue streams, reducing the India precipitated silica market’s exposure to a single industrial macrocycle.

Geography Analysis

West India commanded 34.00% of the India precipitated silica market in 2025, buoyed by Maharashtra’s automotive corridor and Gujarat’s chemical ecosystem that anchors integrated supply chains. The proximity of tire OEMs, soda-ash producers, and port infrastructure around Mumbai and Kandla compresses freight costs and supports export logistics. Expansionary moves like GHCL’s soda-ash project and Wacker’s Kolkata-Panagarh network underscore continuous investment in the region’s materials backbone.

South India is the fastest-growing region, with a 4.41% CAGR through 2031, as the Tamil Nadu’s Sriperumbudur-Oragadam belt and Karnataka’s Bengaluru cluster attract automotive, FMCG, and electronics manufacturers. Tata Chemicals’ acquisition of Allied Silica’s Cuddalore unit and semiconductor fab announcements illustrate a pivot toward higher-value chemicals downstream of silica. The technology-startup ecosystem in Bengaluru also incubates battery-materials ventures, sowing early-stage demand for ultra-high-purity grades.

North India and East & North-East India hold smaller shares but contribute stable baseline volumes. North India leverages proximity to the agricultural heartland, driving steady purchase of silica for pesticide formulations. East India’s industrial base around Jharkhand and Odisha feeds rubber and refractories demand. Infrastructure upgrades and ongoing capacity expansions promise incremental growth, ensuring the India precipitated silica market maintains balanced geographic exposure.

Competitive Landscape

The India precipitated silica market is highly consolidated, with domestic incumbents like Tata Chemicals, Madhu Silica, and Aksharchem competing against global majors such as Evonik, Wacker, and Solvay. Tata Chemicals’ strategy to quintuple capacity through brownfield debottlenecking and the Allied Silica acquisition typifies aggressive scaling to protect share[2]Tata Chemicals Limited, “Company Showcase,” ibef.org . Evonik’s creation of “Smart Effects” integrates its silica and silane portfolios to deliver composite solutions for tires, construction, and healthcare, reinforcing technological differentiation.

International players retain leadership in specialty grades by leveraging cross-regional R&D and application labs. Wacker’s Kolkata plant supports local oral-care converters, while its Panagarh site supplies electronics-grade silicas to emerging semiconductor value chains. Solvay focuses on high-dispersibility silica variants for next-generation tires, aligning with emission standards. Domestic challengers stake claims through cost competitiveness and responsive customer service, although rising compliance capital expenditures may recalibrate the playing field in favor of scale players.

White-space opportunities in battery separators, high-purity electronics, and nano-silica open doors for start-ups and joint ventures. Partnerships between chemical producers and academic institutions in Bengaluru and Hyderabad are exploring the pilot-scale production of silica-coated battery anodes, signaling potential future disruption. Overall, competitive dynamics hinge on a blend of capacity scale, environmental compliance, and technical support that collectively shape positioning in the India precipitated silica market.

India Precipitated Silica Industry Leaders

Evonik Industries AG

Madhu Silica Pvt. Ltd.

PPG Industries Inc.

Ralington Pharma

Tata Chemicals Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AksharChem (India) Ltd. has announced the completion of its precipitated silica facility expansion in Dahej, Gujarat, adding 6,000 TPA. With this development, the company's total precipitated silica capacity has increased to 18,000 TPA.

- January 2025: Evonik has combined its Silica and Silanes divisions into "Smart Effects," creating a global platform to deliver integrated solutions across key sectors and strengthening its position in precipitated silica applications. This initiative is expected to boost the Indian precipitated silica market by driving innovation and offering advanced solutions.

India Precipitated Silica Market Report Scope

Precipitated silica is a form of amorphous silica that is produced through a chemical process called precipitation. It consists of finely divided particles with high surface area and porosity. Precipitated silica is commonly used as a filler and reinforcing agent in various products, including rubber, plastics, paints, coatings, adhesives, and cosmetics. It helps improve mechanical properties, such as strength and abrasion resistance and provides benefits, such as enhanced flow, increased viscosity control, and improved texture.

The India Precipitated Silica is segmented by End-user Industry (Agriculture, Cosmetics, Automotive, Electronics, and Other End-user Industries). The report offers market size and forecasts for India Precipitated Silica in volume (Kilo Tons) for all the above segments.

| Agriculture |

| Oral Care and Cosmetics |

| Agrochemicals |

| Tire |

| Electronics |

| Other End-User Industries |

| Wet-Process |

| Dry-Process |

| Powder |

| Beads |

| Micro-pearls |

| Granules |

| Rubber Grade |

| Food Grade |

| Dental/Oral-Care Grade |

| Feed Grade |

| Others (Battery-Separator Grade, Technical/Industrial Grade) |

| By End-user Industry | Agriculture |

| Oral Care and Cosmetics | |

| Agrochemicals | |

| Tire | |

| Electronics | |

| Other End-User Industries | |

| By Production Process | Wet-Process |

| Dry-Process | |

| By Product Form | Powder |

| Beads | |

| Micro-pearls | |

| Granules | |

| By Grade | Rubber Grade |

| Food Grade | |

| Dental/Oral-Care Grade | |

| Feed Grade | |

| Others (Battery-Separator Grade, Technical/Industrial Grade) |

Key Questions Answered in the Report

What is the projected volume for the India precipitated silica market by 2031?

The market is expected to reach 205.69 kilo tons by 2031, expanding at a 4.03% CAGR from the 2025 base of 162.35 kilo tons.

Which end-use sector drives the highest demand for precipitated silica in India?

The tire segment leads, holding 36.30% share in 2025 due to the automotive industry’s shift toward fuel-efficient, silica-reinforced compounds.

Which production process is gaining popularity for environmental reasons?

The dry process is advancing at a 4.19% CAGR as manufacturers seek lower effluent generation and tighter morphology control.

What regulatory driver is influencing agrochemical demand for precipitated silica?

Mandatory BIS compliance for wettable powder formulations is pushing agrochemical firms to increase silica loading for flow control and anti-caking performance.

How are environmental regulations impacting silica producers?

Tightening effluent norms require investments in zero-liquid-discharge systems, elevating operating costs and favoring larger, well-capitalized companies.

Page last updated on: