Ferrosilicon Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

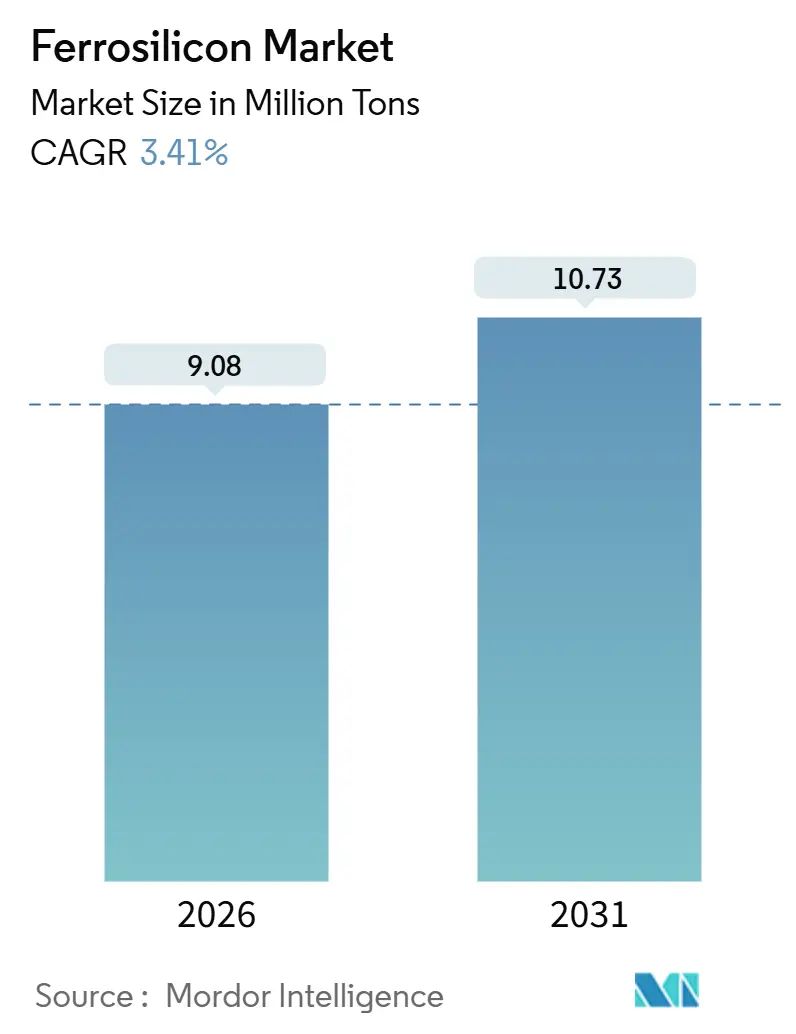

| Market Volume (2026) | 9.08 Million tons |

| Market Volume (2031) | 10.73 Million tons |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ferrosilicon Market Analysis by Mordor Intelligence

The Ferrosilicon Market size is estimated at 9.08 million tons in 2026 and is expected to reach 10.73 million tons by 2031, at a CAGR of 3.41% during the forecast period (2026-2031). This steady expansion rests on four interlocking forces. First, steelmakers are retrofitting basic-oxygen and electric-arc furnaces to run higher-silicon blends that improve ladle metallurgy yields. Second, photovoltaic manufacturers increasingly divert submerged-arc-furnace capacity toward metallurgical-grade silicon, intensifying raw-material pull at times of buoyant solar demand. Third, atomized powders made from ferrosilicon are gaining favor in lithium-spodumene and iron-ore dense-media-separation circuits because lower viscosity cuts media losses, streamlining mining costs. Finally, policy-driven infrastructure outlays in the United States and India, combined with hydrogen-ready direct-reduced-iron projects in the Middle East and Europe, anchor a visible pipeline of alloy offtake for the next decade.

Key Report Takeaways

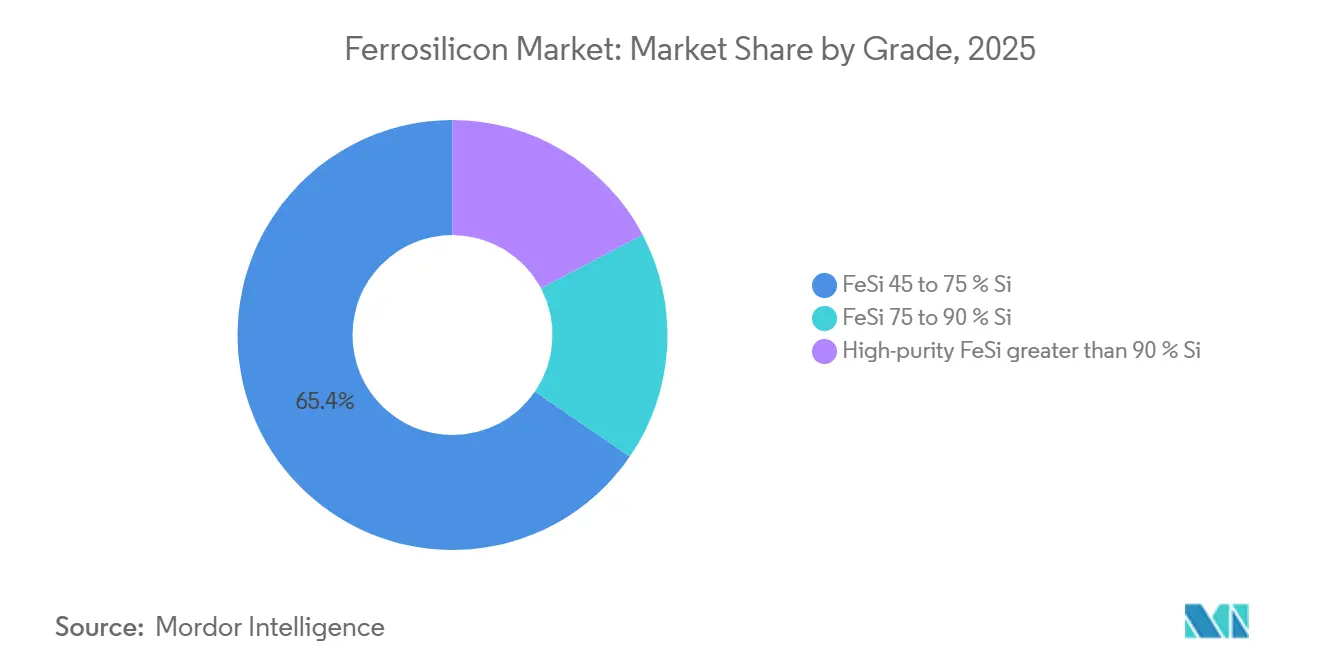

- By grade, the FeSi 45–75% segment held 65.44% of the ferrosilicon market share in 2025 and is projected to grow at a 4.06% CAGR through 2031.

- By form, lump alloys accounted for 36.71% of the ferrosilicon market size in 2025 and are advancing at a 4.17% CAGR during the forecast horizon.

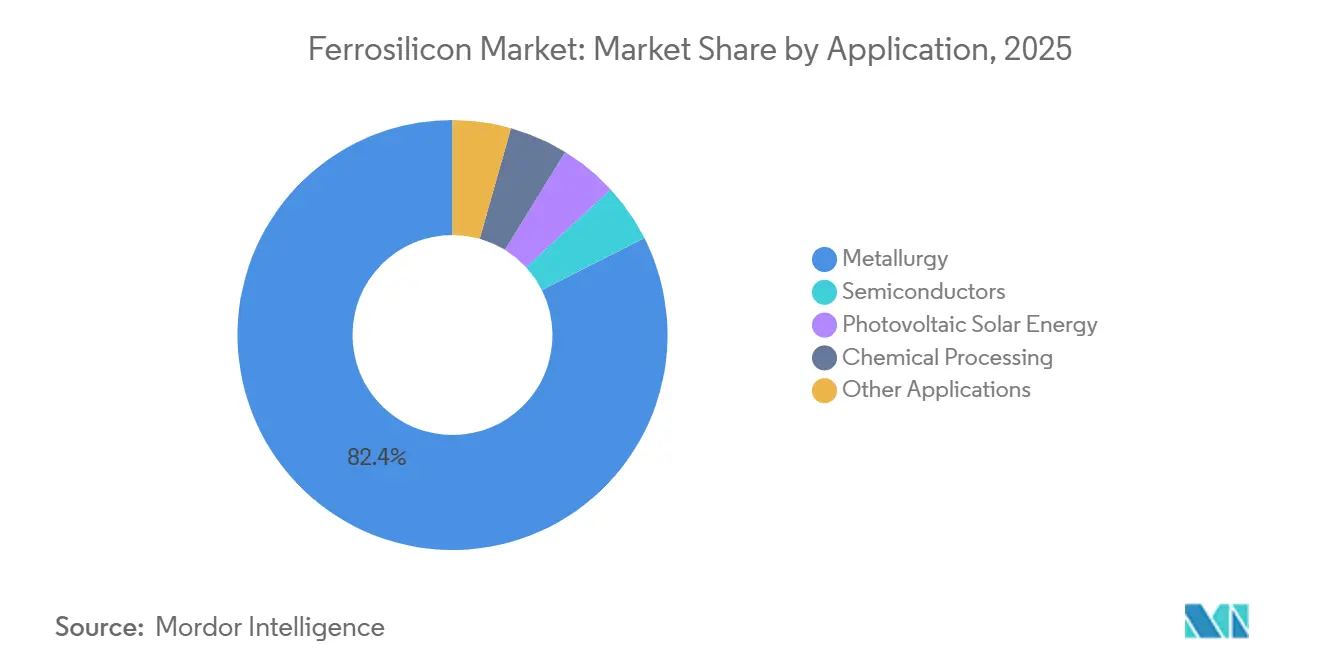

- By application, metallurgy dominated with 82.45% share of the ferrosilicon market size in 2025, while photovoltaic solar energy is expanding at the fastest 5.01% CAGR to 2031.

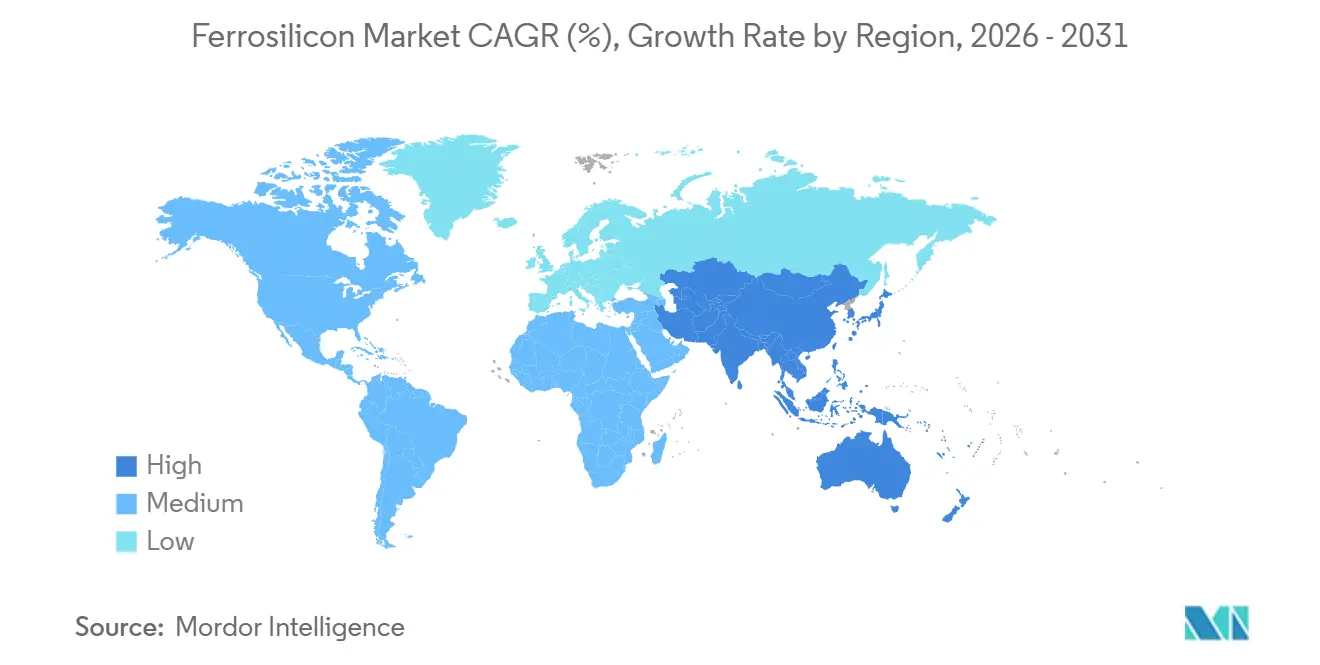

- By geography, Asia-Pacific led with 58.81% ferrosilicon market share in 2025; the region is forecast to post a 4.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ferrosilicon Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising steel-capacity additions across the Asia-Pacific | +1.2% | China, India, South Korea, ASEAN | Medium term (2–4 years) |

| Electrification spurring electrical-steel demand for EV motors | +0.8% | Global, with early gains in China, EU, North America | Long term (≥4 years) |

| Infrastructure stimulus in North America and India | +0.6% | United States, Canada, India | Short term (≤2 years) |

| Hydrogen-ready DRI mills adopting higher-Si alloy blends | +0.5% | MENA, Australia, EU (pilot scale); spillover to APAC | Long term (≥4 years) |

| Growth of dense-media recycling using atomised FeSi powders | +0.4% | Australia, South Africa, Chile (lithium/iron ore hubs) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Steel-Capacity Additions Across Asia-Pacific

Between 2025 and 2027, OECD data reveals plans for new steelmaking capacity, with a significant portion concentrated in the Asia-Pacific region. In fiscal 2025, India’s finished-steel capacity surpassed expectations. India's zero-import-duty policy on ferrous scrap, coupled with a Production-Linked Incentive scheme for specialty steel, is driving heightened demand for deoxidizers at its integrated mills. While China aims for annual growth in crude steel through 2026, energy restrictions in Inner Mongolia and Ningxia have led to intermittent shutdowns of older coal-fired furnaces. This has pushed operators to adopt newer, energy-efficient submerged-arc units. Even as hot-rolled coil prices dipped in 2024, steelmakers maintained the use of ferrosilicon per ton of crude steel, stabilizing baseline consumption. Consequently, the region sees an increase in medium-grade alloy demand.

Electrification Spurring Electrical-Steel Demand for EV Motors

Electrical steel, an iron-silicon sheet with silicon content, is deemed critical for traction motors by the U.S. Department of Energy. Each battery electric vehicle (EV) requires laminations made from this material[1]U.S. Department of Energy, “Solar Supply Chain Review 2025,” ENERGY.GOV . In anticipation of the growing EV market, POSCO, Baowu, and JFE Steel have introduced new grain-oriented and non-oriented production lines, set to ramp up by 2026. These mills are also opting for higher-purity ferrosilicon to minimize magnetic-core losses. The International Energy Agency projects a surge in global EV sales in the coming years[2]International Energy Agency, “Global EV Outlook 2025,” IEA.ORG . Additionally, as grid-transformer installations for renewable energy interconnections grow, there's a heightened demand for grain-oriented electrical steel, especially since step-up transformers depend on it. While the supply of electrical steel is concentrated in China, Japan, South Korea, and Germany, these regional hotspots experience less cyclicality compared to bulk carbon-steel uses. This stability in alloy offtake persists even when there's a downturn in construction steel.

Infrastructure Stimulus in North America and India

Through 2028, the United States, under its Bipartisan Infrastructure Law, has allocated significant funding for steel-centric projects, including bridges and rail corridors. Meanwhile, India's National Infrastructure Pipeline is set to invest heavily by 2030, with the Ministry of Steel forecasting that the sector will account for a substantial portion of the nation's steel demand by 2027. In structural grades, ferrosilicon is used as silicon boosts deoxidation efficiency and aids in manganese-silicon co-alloying. Canada, recognizing the significance of silicon metal and classifying it as a critical mineral in 2024, is exploring hydro-powered smelters in Québec and British Columbia. However, environmental approvals are pushing timelines to the early 2030s. As Mexico experiences a surge in near-shoring, driving up demand for automotive and appliance sheets, it's noteworthy that the nation relies on the U.S. and Brazil for most of its ferrosilicon, underscoring the continent's supply interdependencies.

Hydrogen-Ready DRI Mills Adopting Higher-Silicon Blends

OECD data forecasts a DRI capacity increase by 2030, yet currently, only a small percentage harness hydrogen as the reductant. Pilot plants in Sweden, Germany, and the UAE have found that hydrogen DRI yields a porous, low-carbon sponge iron. This requires electric-arc operators to boost ferrosilicon additions to reestablish silicon levels. This presents a significant new opportunity for producers in Brazil, Malaysia, and Norway, who are already marketing a low-carbon supply. While achieving cost parity with natural-gas DRI hinges on carbon prices exceeding certain thresholds, regions rich in renewable power, like the Middle East and Australia, are forging ahead, bolstered by national green-hydrogen strategies. These initiatives create early adoption pathways, sending ripples through the global ferrosilicon supply chain.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile quartzite and electricity costs | -0.3% | Global, acute in South Africa, Europe, China | Short term (≤2 years) |

| Tightening CO₂-emission regulations on smelters | -0.2% | EU (CBAM), China (dual-control), emerging in India | Medium term (2–4 years) |

| Shift to Al-Si master-alloys in auto castings | -0.1% | EU (primary impact), limited adoption in North America, Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Quartzite and Electricity Costs

Producing a ton of silicon consumes significant electricity, making energy costs account for nearly half of a smelter's expenses. Due to annual Eskom tariff hikes, Glencore adjusted its furnace operations in Mpumalanga. Simultaneously, Ferroglobe had to halt operations in Spain and France, reacting to high European day-ahead electricity prices. For quartzite feedstock, a high SiO₂ content is essential. However, disruptions in the Red Sea and Panama Canal have led to a spike in shipping costs. China's dual-control policy is tightening winter electricity supplies in Inner Mongolia and Ningxia, reducing utilization rates and driving up spot alloy prices. While hydropower-abundant Norway and Paraguay present some cost relief, many smelters in regions with high tariffs find it challenging to break even, especially when ferrosilicon prices remain under pressure.

Tightening CO₂-Emission Regulations on Smelters

Submerged-arc furnaces emit significant amounts of CO₂, with the majority of emissions tied to carbonaceous reductants. Under China's 14th Five-Year Plan, a reduction in intensity is mandated by 2025. This pushes operators to retrofit waste-heat boilers and transition to partial biomass reductants. While the EU’s Carbon Border Adjustment Mechanism, set to be fully operational in 2026, doesn't explicitly mention ferrosilicon, European steelmakers are increasingly seeking low-carbon alloys to reduce embedded emissions. Elkem’s Limpio plant in Paraguay stands out, utilizing eucalyptus charcoal and hydropower, paving the way for a near-zero-scope-1 emissions pathway. Although carbon capture technology is still in its infancy, challenges arise from the low CO₂ concentration in SAF off-gas. Implementing scrubbing could inflate costs, jeopardizing market competitiveness. Meanwhile, electro-reduction in molten salt holds potential, but requires a decade of pilot testing before it can be commercialized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Mid-Silicon Alloys Anchor Steelmaking Deoxidation

The FeSi 45–75% slice held 65.44% of 2025 volume and is forecast to expand faster than any other grade at a 4.06% CAGR. This grade integrates effortlessly into carbon-steel ladles and cast-iron inoculation, delivering high silicon recoveries without excessive heat. Chinese measures aimed at increasing crude steel production underpin incremental offtake, and India’s capacity additions amplify the pull. Standard 75% material serves electric-arc furnaces and foundries but grows more slowly because scrap-heavy melting requires less material compared to blast furnaces. High-purity grades over 90% silicon meet semiconductor and solar wafer standards; producers toggle furnaces between traditional alloy and metallurgical-grade silicon when polysilicon prices justify the switch. Pricing spreads validate that choice, giving agile smelters the margin incentive to chase solar-cycle peaks. Recycled photovoltaic silicon may eventually seed a circular supply, yet industrial-scale collection and refining infrastructure is still embryonic.

By Form: Lump Alloys Dominate Blast-Furnace Additions

Lump material captured a 36.71% share in 2025 and is on track for a 4.17% CAGR through 2031. Operators of blast furnaces and basic oxygen facilities prefer 10–50 mm granules. These granules dissolve predictably in high-temperature slag, reducing dust carry-over. According to OECD forecasts, by 2027, a majority of the world's new steel capacity will still rely on blast-furnace methods, bolstering the demand for lumps. Atomized powders fuel dense-media separation circuits in mining, where media losses can decrease significantly, leading to notable operational savings. Lithium ventures in Pilbara and Atacama, coupled with iron-ore facilities in South Africa and India, are driving increased demand for these powders. Briquettes and specialty granules, used in welding electrodes and pyrotechnics, are seeing growth parallel to industrial GDP. Freight economics play a pivotal role in material adoption: lump ferrosilicon, with high bulk densities, maximizes container load factors. In contrast, powders require anti-caking liners, inflating logistics costs.

By Application: Photovoltaic Solar Emerges as Fastest-Growing End-Use

Metallurgy retained 82.45% of 2025 volume, yet photovoltaic solar outpaces every other segment at a 5.01% CAGR. Submerged-arc furnaces, initially tailored for alloys, can swiftly adapt to produce metallurgical-grade silicon. Notably, a portion of the global MGS is now directed towards polysilicon production. Xinjiang, with its substantial share of this capacity, has drawn the attention of the U.S. and E.U., leading to domestic polysilicon plant incentives under the CHIPS Act and the European Solar Alliance. Though semiconductor applications utilize a smaller volume annually, they fetch high prices, drawing in niche players like Wacker Chemie. Chemical derivatives, notably silicone elastomers and fumed silica, consistently capture a steady market share, driven by demand from the automotive and construction sectors. Meanwhile, other applications like magnesium reduction and welding fluxes see modest growth, aligning with the broader industrial output trends, yet they don't significantly alter the supply-demand balance.

Geography Analysis

Asia-Pacific owned 58.81% of the ferrosilicon market share in 2025 and is projected to clock the highest 4.53% CAGR through 2031. Despite energy policies causing some legacy furnaces in Inner Mongolia and Ningxia to idle, China stands firm as the leading producer. India is channeling increased alloy demand to its domestic suppliers and Bhutan's Tashi Group, thanks to its specialty-steel incentive scheme and zero-duty scrap imports. Meanwhile, Japan and South Korea, collectively importing substantial quantities annually, see an added boost from POSCO’s electrical-steel expansion, potentially increasing demand further.

North America, accounting for a notable portion of global demand, saw the U.S. rely on five smelters, one of which was idled, alongside imports from Brazil, Canada, and Malaysia. Thanks to the Bipartisan Infrastructure Law, an annual uptick is anticipated as steel tonnage flows into bridge and rail projects. While Canada pushes for critical minerals and proposes hydro-powered plants (albeit with permitting delays into the 2030s), Mexico's near-shoring trend is driving up flat-steel demand for appliances and automotive. However, the region's reliance on imports for ferrosilicon underscores a significant interdependence.

Europe, with a substantial annual consumption, grapples with high power prices. While Ferroglobe has curtailed operations in Spanish and French furnaces, Norway capitalizes on hydropower to maintain competitive costs. Furthermore, Norway is channeling significant investment into a solar-grade silicon complex at Herøya. South America, primarily driven by Brazil's hydro-advantaged capacity, finds itself shipping significant quantities to both the U.S. and Europe. In the Middle East and Africa, South Africa takes center stage. However, with Eskom's tariff hikes and load-shedding challenges, capacity utilization remains restricted. Yet, there's a glimmer of hope with Saudi infrastructure projects hinting at modest incremental demand.

Regulatory Landscape

Trade and climate-linked policies are increasingly shaping ferrosilicon flows. In the United States, the Department of Commerce issued antidumping and countervailing duty orders on ferrosilicon from Brazil, Kazakhstan, and Malaysia in May 2025 following affirmative material injury findings by the U.S. International Trade Commission. This tightening of access for key supplying countries is also shifting procurement toward alternative origins and domestic output.

In Europe, the European Commission implemented a three-year safeguard measure covering certain ferro-alloying elements, including ferrosilicon, effective 18 November 2025 via Commission Implementing Regulation (EU) 2025/2351. The measure applies country-specific tariff-rate quotas referenced to 2022-2024 import levels, while the EU Carbon Border Adjustment Mechanism (CBAM) moving into its full phase in 2026 is reinforcing buyer preference for documented, lower-embedded-emissions alloy supply, even where ferrosilicon is not explicitly singled out in the policy text.

Value Chain Analysis

The ferrosilicon value chain starts with quartzite (high SiO2) and carbon reductants (coal/coke, and increasingly biocarbon), with electricity typically representing close to half of smelter cash costs in submerged-arc furnace (SAF) operations. Production is concentrated in a small number of power-advantaged regions. With China accounting for a dominant share of global output in 2025, grid policy, seasonal power controls, and environmental compliance (including carbon-intensity targets and furnace modernization) are central determinants of availability and cost.

Downstream, ferrosilicon moves through traders and distributors to steel mills and foundries (dominant end users), and to niche channels such as atomized powder suppliers serving dense-media separation in mining. The chain has become more policy-sensitive: U.S. AD/CVD enforcement actions initiated in 2024 and the resulting 2025 orders have altered historical import lanes, while EU safeguard quotas introduced in late 2025 have constrained duty-free volumes and increased the importance of contract coverage, origin diversification, and producers with flexible product slates. On the supply side, producers have used curtailments to manage weak pricing and inventories, as illustrated by Elkem curtailing ferrosilicon production at its Rana (Norway) and Iceland plants.

Competitive Landscape

The ferrosilicon market is moderately fragmented. In the atomized-powder supply for dense-media separation, opportunities arise as lower media losses lead to significant economic benefits for customers. Additionally, hydrogen-ready DRI mills emerge as a new avenue, requiring higher alloy doses per heat to adjust silicon levels in low-carbon sponge iron. Technology investments span from biocarbon substitution, already in commercial use in Paraguay, to electro-reduction in molten salt. The latter, while aiming to reduce energy consumption, is still in the laboratory phase. Meanwhile, recycling innovators are experimenting with the closed-loop recovery of end-of-life photovoltaic silicon. Their goal is to produce low-grade FeSi for foundries, achieving a targeted reduction in carbon emissions, although commercial volumes remain limited.

Ferrosilicon Industry Leaders

Ferroglobe

Elkem ASA

China Minmetals Corporation

Erdos Group

OM Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two near-term whitespace areas are forming around supply security and decarbonization credentials. In the United States, the May 2025 antidumping and countervailing duty orders on ferrosilicon from Brazil, Kazakhstan, and Malaysia have reshaped buying patterns and increased the premium on reliable non-subject supply and domestic availability. In Europe, safeguard measures effective from 18 November 2025 have introduced quota-managed import access, pushing steelmakers and distributors to rebalance sourcing strategies and to prioritize suppliers that can document consistent origin and footprint attributes.

Incremental capacity and modernization projects outside the most constrained power-cost regions represent a second opportunity lane. A notable example is the Kazakhstan project announced in February 2026 for a new ferroalloy plant in Ekibastuz targeting FeSi-75 grade production (80,000-89,900 tonnes per year) backed by the Development Bank of Kazakhstan and the Chevron Direct Investment Fund, signaling investor appetite for energy-advantaged, export-capable production hubs. In India, project tracking in June 2026 referenced proposed installation of new ferroalloy units including 42,000 TPA of ferrosilicon at a Chhattisgarh Steel & Power Limited site, aligning with the country’s steel capacity build-out and tightening regional supply chains around integrated steel plants. On the product side, higher-purity ferrosilicon for electrical steel and atomized powders for dense-media separation continue to reward producers that can offer tighter chemistry control and reliable particle-size distributions.

Recent Industry Developments

- May 2026: Ferroglobe reported its first-quarter 2026 results, noting higher ferroalloy shipment volumes in the United States and Europe, supported by recently enacted trade measures. The update highlights how trade enforcement can redirect volumes and improve realized sales traction for suppliers positioned within protected markets.

- November 2025: The European Union implemented safeguard measures on imports of certain ferroalloys from third countries, covering products that include ferrosilicon and running through November 2028. The measure introduced quota-managed import access, influencing sourcing decisions for steelmakers and distributors across the region.

- October 2024: Elkem announced curtailments of ferrosilicon production at its Rana, Norway and Iceland plants amid weak market conditions, rising inventories, and lower prices. The action underscored producers' use of operational flexibility to rebalance supply in energy-sensitive markets and protect margins during downcycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers ferrosilicon alloy produced and sold as an iron-silicon input material, typically used in steelmaking and foundries for deoxidation and inoculation, and in a few other industrial uses.

Scope exclusions: We do not count silicon metal, silicomanganese, or finished downstream components where ferrosilicon is no longer traded as an alloy product.

Segmentation Overview

- By Grade

- FeSi 45–75% Si

- FeSi 75–90% Si

- High-purity FeSi greater than 90% Si

- By Form

- Lumps

- Powder

- Briquettes and Others

- By Application

- Metallurgy

- Semiconductors

- Photovoltaic Solar Energy

- Chemical Processing

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down supply, trade, and pricing context that can be verified year to year. We refer to public sources such as USGS mineral summaries, UN Comtrade trade statistics, World Steel Association output indicators, and customs or statistical office releases in major producing and consuming countries. Price direction and contract language are also checked using exchange notices and association updates where available.

To connect these signals to company behavior, we review annual reports, investor decks, and public news for capacity additions, furnace restarts, and regional demand changes. In parallel, we use paid subscriptions for company financials and intelligence, patent databases, and import and export shipment-level checks when it helps close a data gap. The sources listed here are illustrative, and many other public documents were also reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what is actually shipped, what is substituted, and how prices move by grade and delivery terms. We spoke with respondents across producers, traders and distributors, steel and foundry buyers, and a small set of equipment and raw material participants, with coverage balanced across APAC, EMEA, and the Americas so regional realities were not missed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 48% |

| Mid tier: 51% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 16% | Managers: 47% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down view where steel and foundry activity is translated into ferrosilicon demand using usage factors, grade mix, and trade adjustments, and then reconciled against producer output signals. To keep the totals realistic, we also run selective bottom-up checks using sampled supplier sales splits, channel checks on import availability, and an average price per ton multiplied by estimated volumes.

A few practical inputs guide the model, such as crude steel production trends, foundry output direction, typical ferrosilicon addition rates by process, import and export flows for key corridors, and the mix shift between common grades (for example, around 75% silicon) versus lower silicon material. Pricing assumptions are handled carefully because alloy prices swing with energy costs and feedstock tightness, so we separate volume movement from price movement before translating to USD values.

For forecasting, scenario analysis is used so slower steel cycles, faster restocking, or energy-driven cost spikes can be reflected without overfitting. Where bottom-up datapoints are missing for smaller countries, gaps are filled using peer-market intensity ratios tied to steel output and trade dependence, and then validated in follow-up calls.

Data Validation & Update Cycle

Checks are run in layers so the final number is not driven by one source. Model outputs are compared with independent signals such as regional steel output changes, trade balances, and price direction to see if the story holds together, and then unusual jumps are reviewed before sign-off. When a large mismatch shows up, we re-check unit conversions, re-test usage factors, and re-contact a few interviewees to understand what changed.

Reports are refreshed annually, and interim updates are done when material events occur such as major furnace closures, new capacity, tariffs, or a sharp change in energy costs. Before delivery, an analyst completes a fresh pass across key datapoints so clients receive the latest updated view.

Mordor Intelligence's Ferrosilicon Market Estimate Compared With Other Published Estimates

Published ferrosilicon market values can look far apart because different studies pick different units, different product definitions, and different assumptions on how prices evolve. In practice, the spread usually comes from whether the estimate is volume-led or value-led, and how aggressively price cycles are treated in the base year.

The biggest gaps often come from scope choices around adjacent silicon products and from how a blended price is converted across regions and contract terms. Some estimates also anchor on a single year of spot pricing, while others smooth prices over a longer period, which can swing the USD total even when tons are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.01 B (2026) | |

| Trade Journal A | USD 11.91 B (2024) | This figure appears to be value-first and can be inflated when broader silicon-related categories are grouped together, and when a higher blended price is applied without clear grade and delivery-term separation. |

| Regional Consultancy B | USD 3.50 B (2025) | This estimate likely uses a narrower value pool and a different average price per ton assumption, and it is sensitive to whether producer selling prices or traded import prices are treated as the primary reference. |

Scope separation between ferrosilicon alloy and nearby silicon products explains much of the spread, a modeling choice applied by Mordor Intelligence. With the volume signal kept central and the price layer built from checked regional assumptions, the output stays traceable to simple drivers that can be repeated and reviewed each year.

Key Questions Answered in the Report

How large is the ferrosilicon market in 2026?

The ferrosilicon market size reached 9.08 million tons in 2026 and is projected to climb to 10.73 million tons by 2031, registering a CAGR of 3.41%.

Which region leads demand growth?

Asia-Pacific held a 58.81% share in 2025 and is expected to post the fastest 4.53% CAGR through 2031, driven by capacity ramps in China and India.

What is driving ferrosilicon use in electric vehicles?

Each battery electric vehicle needs 40–100 kg of electrical steel, an iron-silicon alloy, so rising EV sales boost demand for higher-purity ferrosilicon.

How do energy costs affect producers?

Electricity can be 50% of smelter cash costs; tariff hikes in South Africa and Europe have forced furnace curtailments and squeezed margins.

What technology trends could reshape supply?

Biocarbon reductants are commercial, while electro-reduction in molten salt aims at zero-carbon silicon but remains in early pilot phases.

Page last updated on: