Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

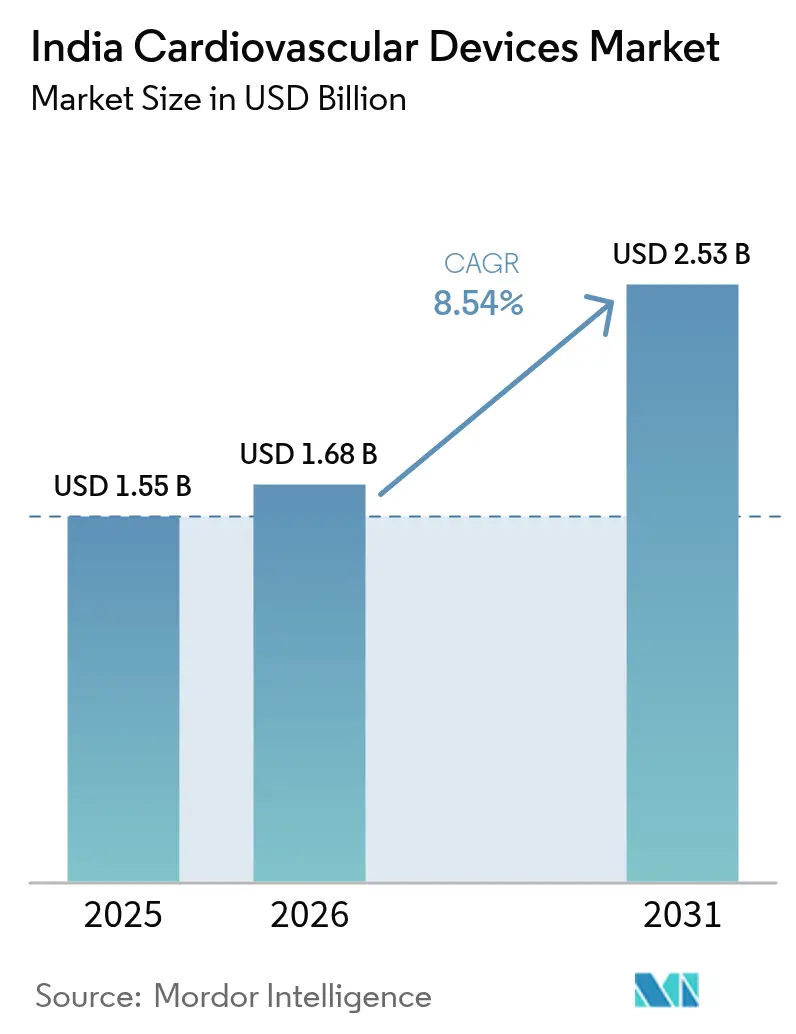

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 8.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cardiovascular Devices Market Analysis by Mordor Intelligence

The India cardiovascular devices market size was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.68 billion in 2026 to reach USD 2.53 billion by 2031, at a CAGR of 8.54% during the forecast period (2026-2031). The India cardiovascular devices market is growing because an aging population, greater insurance coverage, and domestic manufacturing incentives align to boost procedure volumes and device availability. Government spending on health has risen to 1.84% of GDP, while out-of-pocket spending has fallen sharply, signaling stronger public purchasing power for devices. Production-Linked Incentive (PLI) subsidies have prompted 19 greenfield medical-device plants that target high-end modalities once imported, easing supply bottlenecks for the India cardiovascular devices market.

Key Report Takeaways

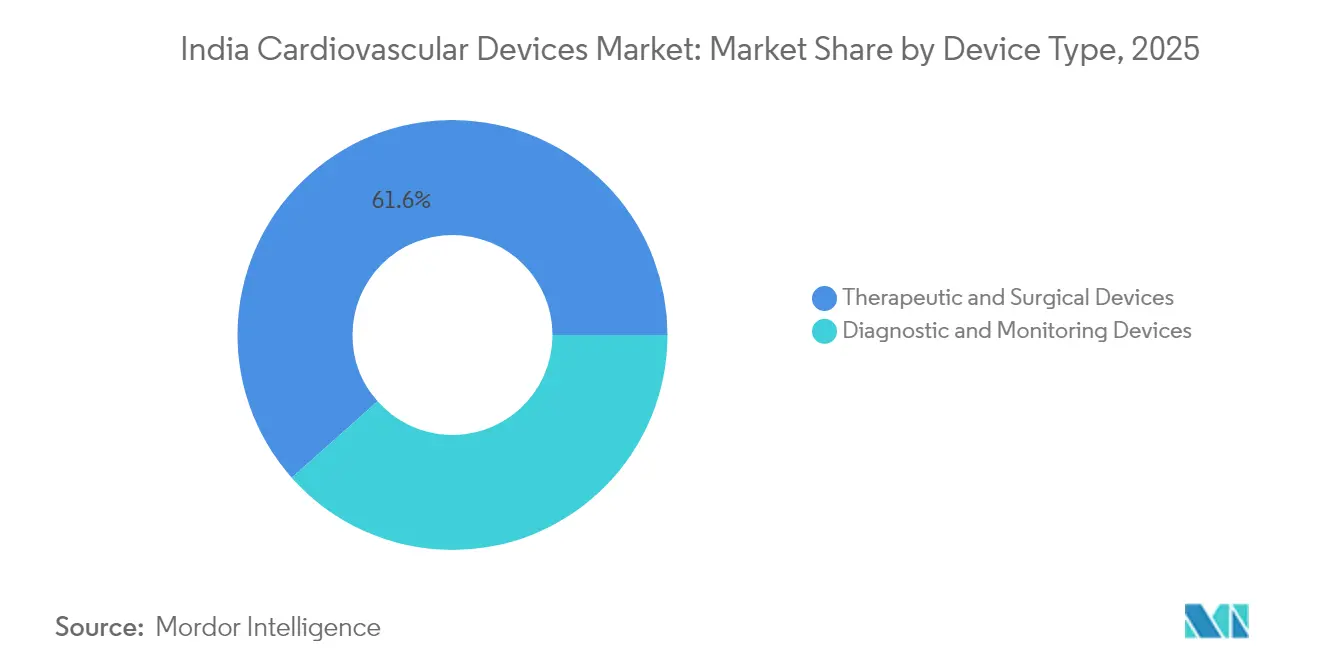

- By device type, therapeutic and surgical products captured 61.55% of India cardiovascular devices market share in 2025; diagnostic and monitoring devices are projected to grow at 9.62% CAGR through 2031.

- By application, coronary artery disease led with a 42.12% revenue share in 2025, while arrhythmia and conduction disorders are poised to advance at a 8.98% CAGR between 2026-2031.

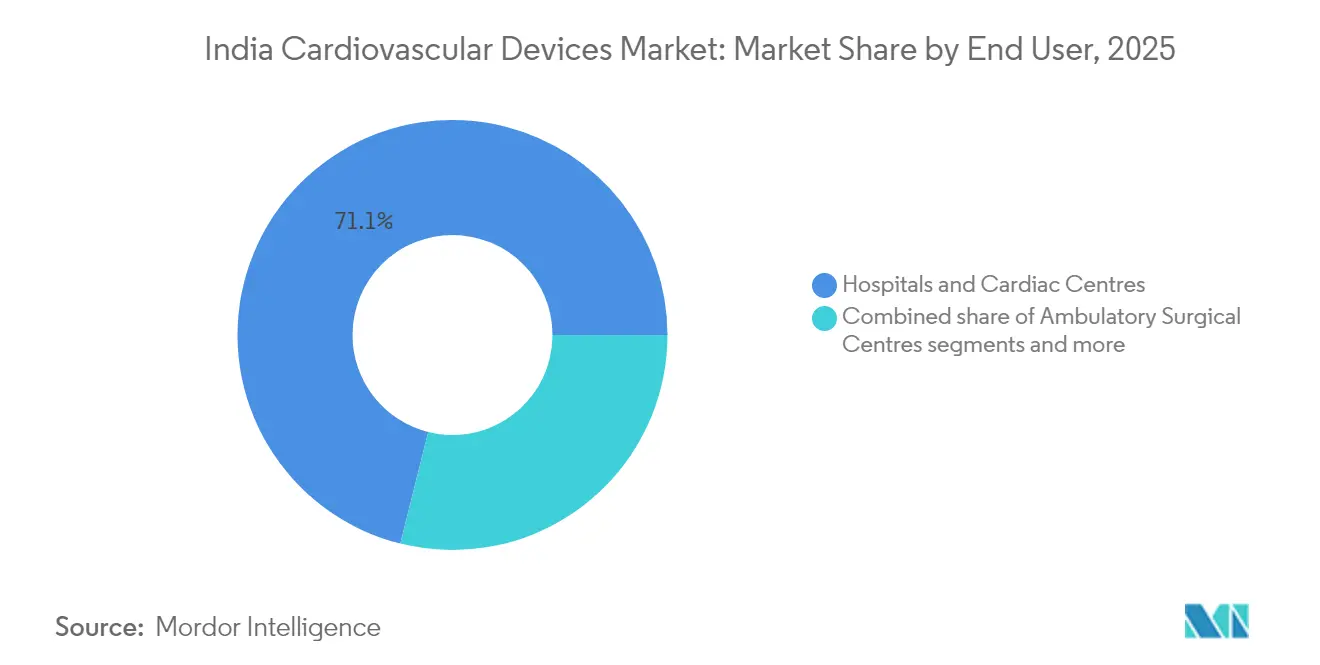

- By end user, hospitals and cardiac centers accounted for 71.10% of India cardiovascular devices market size in 2025; home-care programs are expanding at 8.63% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CVD prevalence & ageing population | +2.1% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Increasing healthcare expenditure & insurance penetration | +1.8% | National, with accelerated adoption in tier-2/3 cities | Medium term (2-4 years) |

| Expansion of cath-labs in tier-2/3 Indian cities | +1.5% | Tier-2/3 cities, rural catchment areas | Medium term (2-4 years) |

| Government PLI scheme boosting local device manufacturing | +1.3% | Manufacturing hubs in Karnataka, Tamil Nadu, Maharashtra | Long term (≥ 4 years) |

| Digital-twin based cardiac surgery planning adoption | +0.9% | Metro cities, premium healthcare facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising CVD Prevalence & Ageing Population

India’s elderly will account for 22.5% of residents by 2051, and CVDs already contribute 14.1% of national DALYs, double 1990 levels. Ischemic heart disease and stroke cases have risen 2.3-fold since 1990, creating sustained demand for stents, grafts, and rhythm devices. Urban lifestyles compound risk via hypertension and obesity, accelerating procedural volumes in the India cardiovascular devices market. The South-Asian coronary anatomy—smaller vessels and diffuse lesions—drives reliance on surgical grafting technologies. Remote monitoring platforms help manage the rising caseload by shifting routine follow-ups outside hospitals, easing congestion in tertiary centers.

Increasing Healthcare Expenditure & Insurance Penetration

Central health spending tripled to INR 3,169 per capita between 2014-2022, lifting the public share of total health outlays to 48%. Ayushman Bharat now insures 594 million citizens for up to INR 500,000, slashing out-of-pocket cardiac procedure costs by 21%. Coronary angioplasty admissions surpassed 471,000 under the scheme, directly enlarging the India cardiovascular devices market. Tier-2/3 hospitals operate at just INR 10-15 lakh per bed versus INR 1.5 crore in metros, enabling rapid cath-lab rollouts in smaller cities. Investor plans to add 17,800 private beds worth INR 14,600 crore underscore the financing momentum.

Expansion of Cath-Labs in Tier-2/3 Indian Cities

Corporate chains apply hub-and-spoke models to bring interventional cardiology closer to underserved populations, with Narayana Health scaling 7,000 beds across 51 facilities. Nearly 30% of national hospital capacity already sits in rural districts, signaling latent volume for diagnostics and consumables. Government ambulance networks and tele-ECG programs shrink response times, lifting device utilization rates outside metros. Procedure costs—heart surgery at USD 1,600 versus USD 200,000 abroad—draw regional medical tourism, enlarging local demand. Micro-insurance tie-ups widen affordability, stabilizing order pipelines for mid-priced stents and balloons.

Government PLI Scheme Boosting Local Device Manufacturing

By March 2025 the PLI scheme logged INR 1.61 lakh-crore investment and authorized 19 device factories, including CT and MRI lines, reducing 70-80% import dependence. Siemens Healthineers committed INR 91.9 crore for imaging production, while Wipro GE pledged INR 8,000 crore for device R&D and manufacturing. IIT Kanpur’s Hridayantra artificial heart and AIIMS’s domestic 1.5-tesla MRI underscore indigenous R&D progress. Import curbs on refurbished machines shelter domestic entrants, helping price-competitive valves and pacemakers reach the India cardiovascular devices market. Exports also benefit; medical-device shipments doubled to USD 4 billion in three years, signaling future scale economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced implantables | -1.4% | National, with higher impact in rural and semi-urban areas | Medium term (2-4 years) |

| Limited reimbursement coverage | -1.1% | Tier-2/3 cities, rural areas with limited insurance penetration | Long term (≥ 4 years) |

| Dependence on imported critical components | -0.8% | Manufacturing centers, supply chain dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Implantables

The National Pharmaceutical Pricing Authority allowed stent prices to rise to INR 38,933 for drug-eluting models. Branded heart-failure drugs sell at up to 15.8 times generic rates. Customs duties on devices remain among the world’s highest at 5-7.5% and a 5% health cess. With more than 80% of critical implantables still imported, currency volatility transmits directly to end-user prices. Rural families, who shoulder travel and lodging expenses for surgery, delay care, tempering volume growth for the India cardiovascular devices market.

Limited Reimbursement Coverage

Ayushman Bharat excludes many outpatient diagnostics and next-generation therapies. Field studies in Karnataka found insured patients still incurred notable out-of-pocket costs. Smaller district hospitals struggle to meet empanelment criteria. While the September 2024 policy adds all citizens aged 70+, reimbursement ceilings remain static despite rising device prices. Delayed claim settlements discourage stocking high-ticket implants, capping the premium end of the India cardiovascular devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Dominance Drives Volume Growth

Therapeutic and surgical systems generated 61.55% of India cardiovascular devices market size in 2025 on the back of almost half-a-million angioplasties reimbursed under Ayushman Bharat. Drug-eluting stents remain flagship items despite price ceilings, supported by anatomical complexity that demands high efficacy coatings. Pacemaker upgrades such as Abbott’s AVEIR dual-chamber leadless system target pocket-infection reduction, driving rhythm-device sales in the India cardiovascular devices market. Transcatheter valves advance quickly; Myval’s balloon-expandable platform recently enabled a TAVI-in-TAVI rescue, indicating durability.

Diagnostic and monitoring devices will grow at 9.62% CAGR, lifting their India cardiovascular devices market share by the decade’s end. Domestic MRI and CT production can lower capital prices by 50%, unlocking installations in secondary cities. Wearable ECG patches that sync with telemedicine apps identify arrhythmias early, increasing preventative follow-up visits. Digital-twin planning relies on high-definition imaging datasets, reinforcing demand for 256-slice CT and 3-Tesla MRI as prerequisites for virtual modeling.

By Application: Coronary Leadership Faces Arrhythmia Upside

Coronary artery disease continues to anchor 42.12% of revenue, sustained by 23.8 million ischemic-heart cases and almost half-a-million annual angioplasties. Small vessel diameters and diffuse lesions encourage bypass grafting, feeding consistent pump-oxygenator and conduit demand in the India cardiovascular devices market. India attracts medical tourists with cardiac-surgery pricing 90% below developed-world tariffs, adding incremental device volume.

Arrhythmia and conduction-disorder devices will post a 8.98% CAGR, the fastest among applications. Aging drives atrial-fibrillation incidence, while remote monitoring spots asymptomatic events, channeling patients toward ablation or pacing earlier. Personalized heart digital twins enhance ventricular-tachycardia ablation success by identifying critical substrate better than conventional voltage mapping. Structural-heart procedures gain momentum; the Tria polymer mitral valve posted zero valve-related mortality in Indian trials, signaling future diffusion.

By End User: Hospital Dominance Meets Home-Care Innovation

Hospitals and cardiac centers held 71.10% of India cardiovascular devices market share in 2025 because advanced imaging, cath-labs, and hybrid OR suites require large-scale infrastructure. Private chains have earmarked INR 14,600 crore for 17,800 new beds, while government builds additional AIIMS campuses, guaranteeing robust institutional demand. Three-dimensional mapping labs and robotic systems concentrate in tertiary units, underscoring the premium segment of the India cardiovascular devices market.

Home-care and remote-monitoring programs will expand at 8.63% CAGR through 2031, reflecting policy focus on telehealth and the National Digital Health Mission. Wearables feed real-time data into cloud dashboards, enabling physicians to adjust therapy between visits, preventing readmissions and opening annuity-style revenue streams for vendors in the India cardiovascular devices market. Ambulatory surgical centers handle day-care angioplasties, easing hospital occupancy and spreading device consumption geographically.

Geography Analysis

Industrial clusters in Maharashtra, Karnataka, and Tamil Nadu anchor supply lines with 19 PLI-backed factories that fabricate imaging consoles, catheters, and cardiac-monitor shells, fortifying the India cardiovascular devices market against logistic shocks. Siemens Healthineers localized CT and MRI at its Bengaluru unit to cut customs delays, while Wipro GE’s multi-modality campus targets export as well as domestic demand. Southern states leverage medical-tourism inflows; cardiac packages priced at USD 1,600 attract patients from the Middle East and Africa, boosting throughput for implant and graft suppliers.

Tier-2/3 cities represent the fastest-growing geography for the India cardiovascular devices market because hospitals there can be built for one-tenth metro capex, allowing more cath-labs per million residents. Remote-robotic demonstrations, like the Gurugram-to-Jaipur heart surgery, prove specialist access can leapfrog traditional referral chains. Rajasthan, Uttar Pradesh, and Odisha recorded the steepest Ayushman Bharat cardiac-claim growth, indicating readiness for higher-end devices.

Rural districts, though the smallest slice today, hold latent potential. Government ambulance fleets and new AIIMS branches shorten referral times, while micro-insurance partnerships plug affordability gaps. Disability-adjusted life years for ischemic heart disease vary nine-fold across states, suggesting targeted outreach could unlock under-served demand for the India cardiovascular devices market. Mobile cath-lab vans and indigenous low-cost imaging expand diagnostics where brick-and-mortar builds lag, seeding future sales.

Competitive Landscape

Competition in the India cardiovascular devices market features global majors and agile domestic firms. Domestic producers close the gap by leveraging PLI incentives. Poly Medicare saw 23% H1 FY25 revenue growth and earmarked INR 800 crore for catheter capacity, riding export tariffs on Chinese goods. Meril Life’s Myval valve secures CE research access while addressing local affordability, and Sahajanand Medical Technologies scales drug-eluting stent lines for both domestic and African tenders.

Multinationals sign technology-transfer MOUs to tap PLI credits, while Indian players license digital-twin software and robotic modules to climb the value chain. Procurement committees emphasize total-lifecycle cost, rewarding vendors that package disposables, training, and service inside bundled contracts, shifting competitive levers across the India cardiovascular devices market.

India Cardiovascular Devices Industry Leaders

Abbott Laboratories

Terumo Corporation

W. L. Gore & Associates

Medtronic PLC

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SSI Mantra 3 robotic system executed India’s first cardiac telesurgeries across 250 km, proving low-latency remote operation at one-third imported costs

- March 2025: National Pharmaceutical Pricing Authority raised coronary-stent ceilings to INR 38,933 for drug-eluting models, adjusting for 1.74% WPI inflation

India Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular devices are developed to assist in managing different conditions or irregularities related to the heart. These devices include cardiac rhythm management devices, catheters, grafts, and heart valves.

The India cardiovascular devices market is segmented by device type, which includes diagnostic & monitoring devices and therapeutic & surgical devices. The diagnostic and monitoring devices include electrocardiogram (ECG), remote cardiac monitoring, and other diagnostic and monitoring devices. The therapeutic and surgical devices include cardiac assist devices, cardiac rhythm management devices, catheters, grafts, heart valves, stents, and other therapeutics and surgical devices. The report offers the value in USD for the above segments.

By Product Type

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Application

| Coronary Artery Disease |

| Arrhythmia & Conduction Disorders |

| Heart Failure & Cardiomyopathy |

| Structural & Congenital Heart Defects |

| Peripheral Vascular Disease |

By End User

| Hospitals & Cardiac Centres |

| Ambulatory Surgical Centres |

| Cardiology/EP Clinics |

| Home-care & Remote Monitoring Programs |

| By Product Type | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Application | Coronary Artery Disease | ||

| Arrhythmia & Conduction Disorders | |||

| Heart Failure & Cardiomyopathy | |||

| Structural & Congenital Heart Defects | |||

| Peripheral Vascular Disease | |||

| By End User | Hospitals & Cardiac Centres | ||

| Ambulatory Surgical Centres | |||

| Cardiology/EP Clinics | |||

| Home-care & Remote Monitoring Programs | |||

Key Questions Answered in the Report

What is the current value of the India cardiovascular devices market?

The market is valued at USD 1.68 billion in 2026 and is expected to reach USD 2.53 billion by 2031, reflecting an 8.54% CAGR.

Which device category leads sales?

Therapeutic and surgical systems command 61.55% of sales in 2025, backed by high angioplasty and bypass volumes.

Which application shows the fastest growth?

Arrhythmia and conduction-disorder devices are forecast to expand at 8.98% CAGR between 2026-2031.

How does the PLI scheme affect manufacturers?

PLI incentives have attracted INR 1.61 lakh-crore investment and enabled 19 device plants, cutting import dependence and lowering costs.

Are home-care cardiac devices becoming mainstream?

Yes, home-care and remote-monitoring programs are growing at 8.63% CAGR as telehealth platforms link patients in tier-2/3 cities to specialists.

What price controls exist for coronary stents?

The National Pharmaceutical Pricing Authority caps drug-eluting stent prices at INR 38,933 and adjusts annually to the wholesale-price index.

Page last updated on: