India Kitchen Sink and Other Related Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

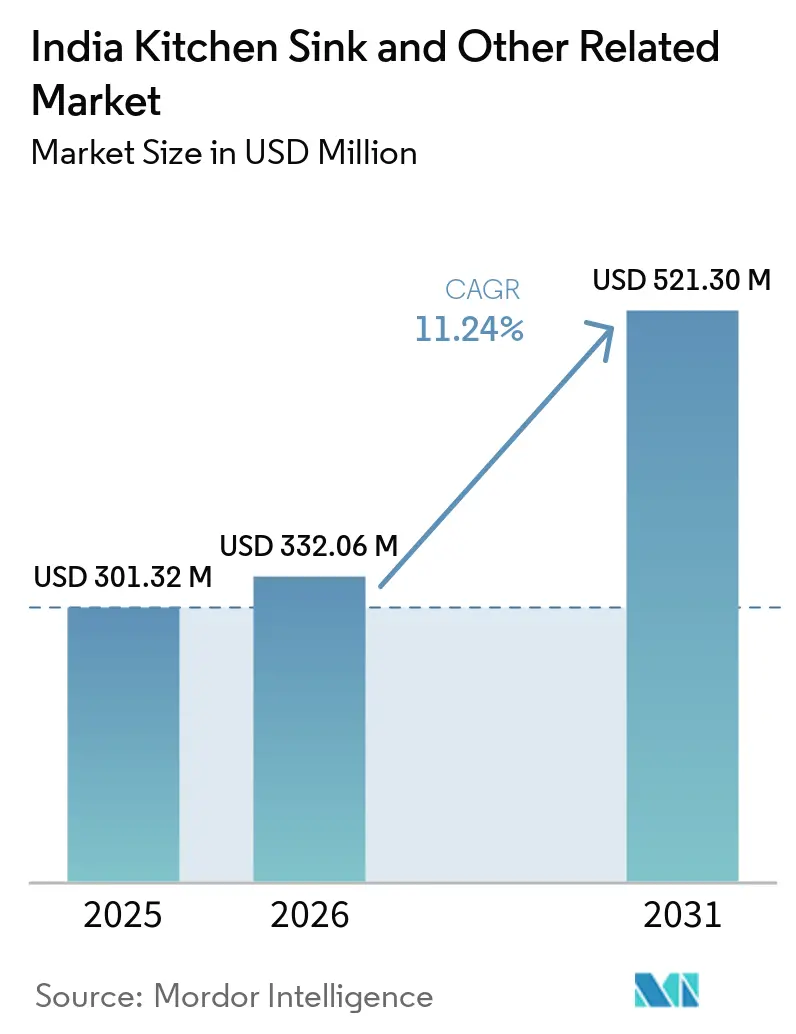

| Base Year Market Size (2025) | USD 301.32 Million |

| Market Size (2026) | USD 332.06 Million |

| Market Size (2031) | USD 521.30 Million |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Kitchen Sink and Other Related Market Analysis by Mordor Intelligence

The India kitchen sink and other related market size is expected to increase from USD 301.32 million in 2025 to USD 332.06 million in 2026 and reach USD 521.3 million by 2031, growing at a CAGR of 11.24% over 2026-2031. Residential apartment handovers in Mumbai, Delhi NCR, and Bengaluru anchor fixture purchases and create predictable order cycles for organized brands that are specified at the construction stage[1]India Brand Equity Foundation, “Residential Real Estate Trends and Completions FY25,” India Brand Equity Foundation, ibef.org. Modular-kitchen adoption in tier-1 and tier-2 households is accelerating the shift to integrated sink-faucet ecosystems and workstation-led accessories, lifting average selling prices and cross-sell rates for premium portfolios. Digital channels are shortening discovery and purchase cycles, with online marketplaces already contributing a meaningful slice of sales and projected to grow faster than traditional outlets through 2031. Quality-control enforcement under Indian standards is consolidating supply toward ISI-marked, QR-verifiable products, which supports trust-based retailing in large-format chains and government procurement[2]Bureau of Indian Standards, “IS 13983:1994 Requirements for Stainless-Steel Kitchen Sinks,” Bureau of Indian Standards, bis.gov.in. Stainless steel remains the workhorse material but faces margin pressure from input-cost swings, while value-added quartz composites are gaining traction due to design latitude and perceived durability benefits among urban renovators.

Key Report Takeaways

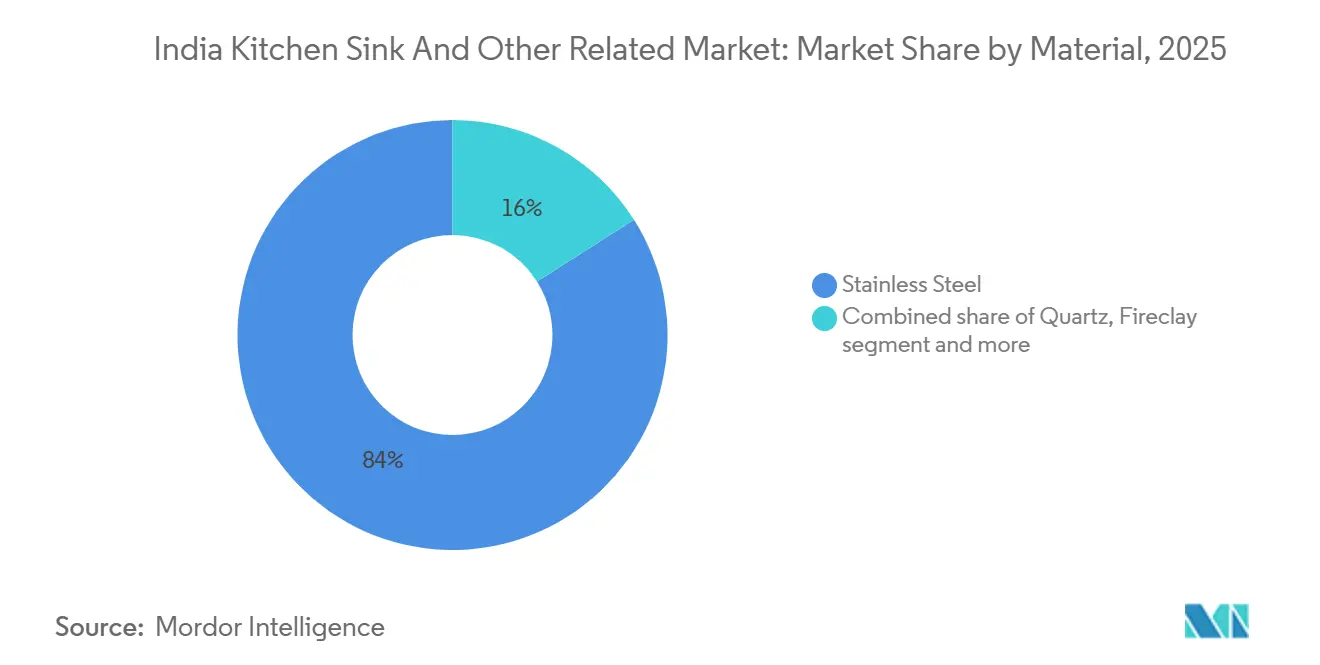

- By material, stainless steel led with 84% revenue share in 2025 in the India kitchen sink and other related market, while quartz composites are forecast to expand at a 16.39% CAGR through 2031.

- By installation type, top-mount formats held 30% share in 2025 in the India kitchen sink and other related market, and dual-mount variants are projected to grow at a 12.26% CAGR through 2031.

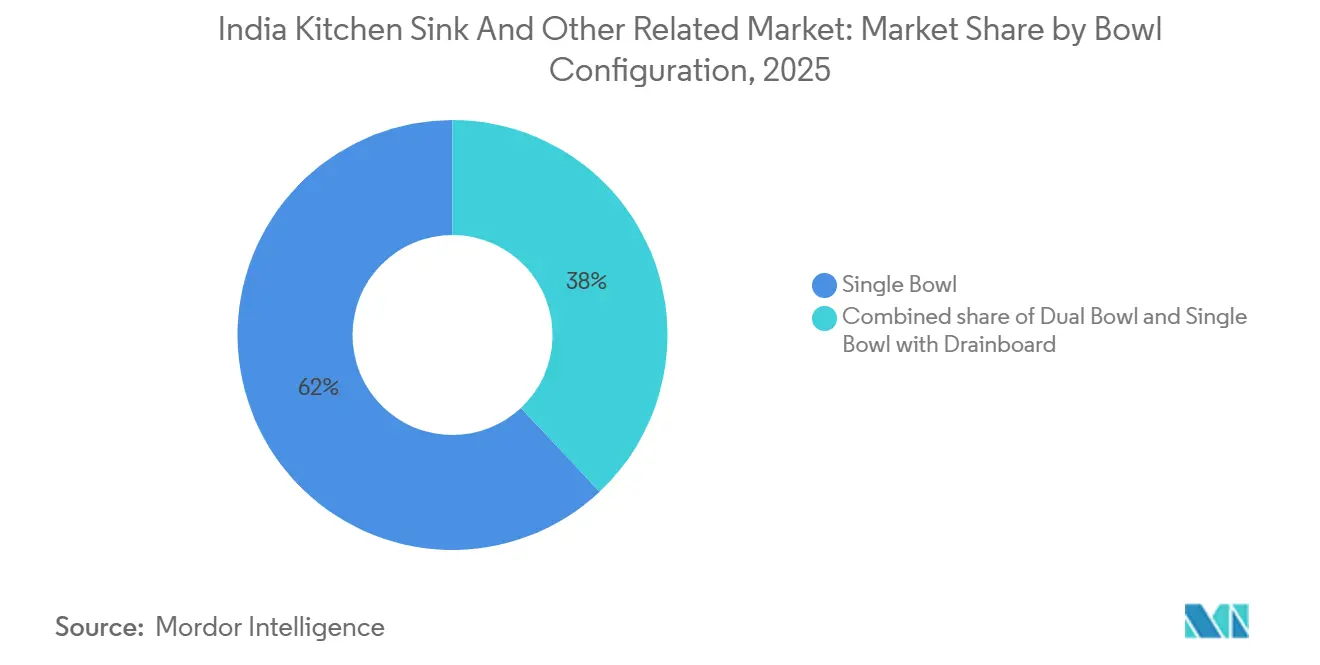

- By bowl configuration, single-bowl designs accounted for 62% share in 2025 in the India kitchen sink and other related market, with single bowls featuring drainboards advancing at a 12.13% CAGR to 2031.

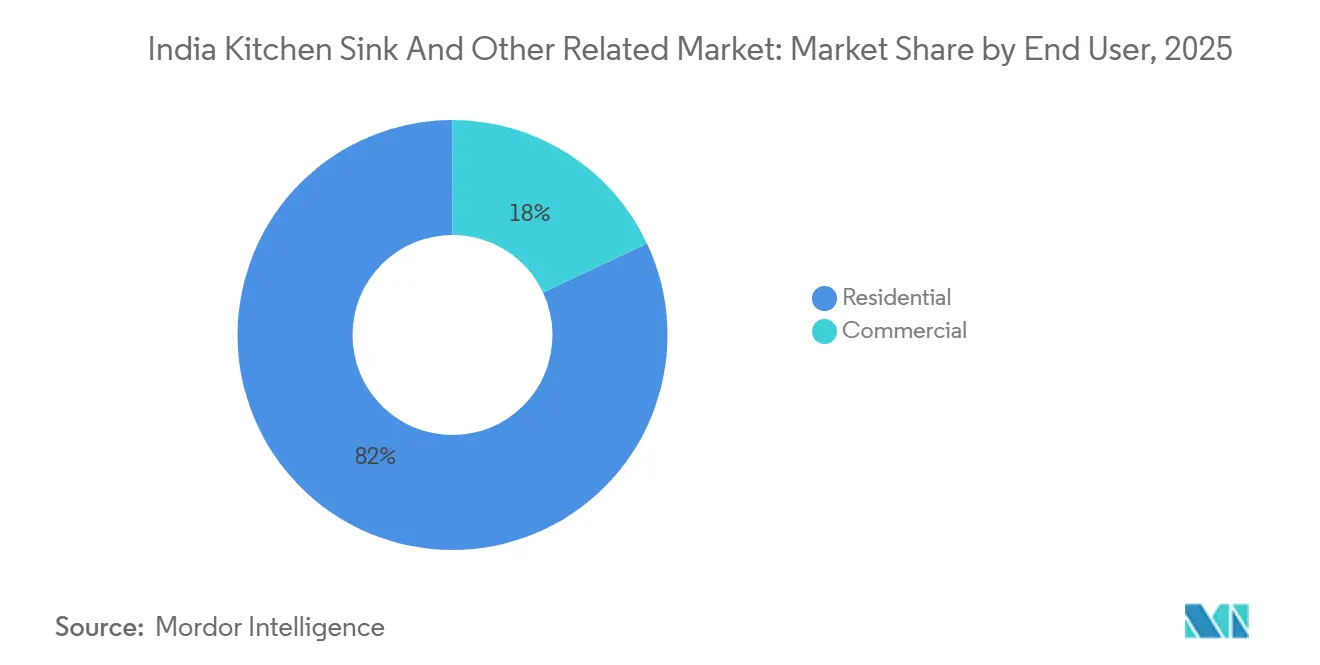

- By end user, residential applications held 82% share in 2025 in the India kitchen sink and other related market, while commercial applications are poised to grow at a 12.28% CAGR through 2031.

- By distribution channel, traditional hardware stores and plumbing distributors commanded an estimated 50–55% share in 2025 in the India kitchen sink and other related market, and online marketplaces are projected to record the fastest growth at a 16.57% CAGR through 2031.

- By geography, South India led with a 25.27% regional share in 2025 in the India kitchen sink and other related market, while the North-East region is the fastest growing at a 12.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Kitchen Sink and Other Related Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Modular-Kitchen Adoption in Urban India | + 1.8% | Tier-1 and tier-2 urban centers, Bengaluru, Pune, Delhi NCR | Long term (≥ 4 years) |

| Housing Completions and New Launches Supporting Sink Demand | + 2.1% | Mumbai, Delhi NCR, Bengaluru | Medium term (2-4 years) |

| Omnichannel Retail Expansion for Kitchen Hardware | + 1.4% | Tier-2 and tier-3 cities, rural corridors | Short term (≤ 2 years) |

| Premiumization Toward Quartz or Granite Aesthetics | + 1.0% | Metro cities and high-income suburbs | Long term (≥ 4 years) |

| BIS-Led Quality Standardization Is Shifting Demand to Organized Brands | + 0.9% | Gujarat, Tamil Nadu, and Punjab hubs | Medium term (2-4 years) |

| Countertop Upgrade Cycles Enabling Undermount Formats | + 1.2% | Pan-India, especially semi-urban | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Modular-Kitchen Adoption in Urban India

India’s modular-kitchen category is scaling as households prioritize compact layouts, storage efficiency, and integrated fixtures, with spending on coordinated sinks and faucets rising alongside cabinetry and countertop upgrades. Developers in premium apartment projects have moved pre-bundle branded sinks into handovers to standardize finish quality and reduce post-occupancy service calls, which sets a benchmark that influences later retrofit cycles in the same micro-markets. Urban consumers are treating the kitchen as a social and functional center, which supports demand for workstation-style sinks that integrate accessories and improve prep ergonomics. Organized brands are deepening collaboration with modular-kitchen OEMs and gallery networks, so sinks are specified early in the design, a shift that results in larger order values and lower return rates than aftermarket replacements. Penetration beyond metros remains a runway as tier-2 and tier-3 households seek aspirational upgrades and respond to experiential showrooms and digital visualization tools that clarify fit and finish choices.

Housing Completions and New Launches Supporting Sink Demand

Residential unit deliveries across India’s top markets rose in FY25, and the 406,889 completed units reported for the top nine cities translate directly into first-fix demand for sinks specified by developers and contractors. Premium projects in larger cities are increasingly opting for dual-mount or undermount formats that elevate countertop continuity and visual appeal, which then shape homeowner expectations in the resale and renovation cycles. Mid-market launches often choose durable stainless-steel models to meet cost and maintenance criteria, reinforcing the breadth of price points within the India kitchen sink and other related markets. As launches and land acquisitions extend deeper into tier-2 locations, organized brands gain access to markets that were once served mainly by local fabricators, opening room for certified products and structured warranties. The tilt toward high-specification housing sustains a pathway for value-added sink materials and accessories that deliver visible differentiation for buyers upgrading kitchens as part of broader interior investments.

Omnichannel Retail Expansion for Kitchen Hardware

Online marketplaces account for a rising share of sink sales and are projected to grow at a 16.57% CAGR through 2031, which outpaces physical retail due to discovery convenience and logistics improvements in smaller cities. Amazon’s home-and-kitchen vertical posted 25% growth in Odisha in FY 2024, which underscores that online demand is no longer confined to metros and can scale in states with limited big-box showroom density. Organized brands are embracing virtual consultants, augmented-reality overlays, and 3D kitchen visualizers that let buyers test placement and clearances before ordering, which shortens decision cycles and reduces returns. Direct-to-consumer initiatives like Carysil Online Limited highlight the strategic benefit of bypassing multi-tier distribution for faster SKU turns and tighter pricing control. As compliance markers such as ISI and QR-based verification become visible on product pages, algorithmic merchandising favors certified SKUs, which can steadily guide share from unorganized to organized sellers over the forecast period.

Premiumization Toward Quartz/Granite Aesthetics

Quartz composite sinks are forecast to register a 16.39% CAGR through 2031, driven by scratch resistance, color variety, and a close match with granite or engineered-stone countertops that premium buyers prefer. The category benefits from broader kitchen investments where sinks serve as design anchors within workstation concepts and accessory rails that declutter prep areas in compact apartments. Carysil’s long-running partnership with IKEA Supply AG and capacity upgrades, including expansion toward an additional 100,000 quartz sinks, reflect the scale-up required to serve rising demand in India and export markets[3]. Even with growing interest among urban homeowners, the current penetration of quartz remains low, which leaves a multi-year runway for education-led adoption and gallery-based demonstrations that showcase functional benefits. As awareness improves and integrators specify quartz alongside high-traffic countertops, the Indian kitchen sink and other related market gains from higher realization per unit and stronger attachment rates for accessory bundles over the ownership cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unorganized Price Competition in Stainless Steel | - 0.9% | Pan-India, rural and tier-3 cities | Short term (≤ 2 years) |

| Raw-Material Cost Volatility Is Pressuring Margins | - 1.2% | Nationwide | Short term (≤ 2 years) |

| Installation Skill Gaps for Undermount or Flush Formats | - 0.7% | Tier-2 and tier-3 cities, rural areas | Medium term (2-4 years) |

| Compliance Cost Burden for MSMES Under QCO | - 0.8% | Pan-India, MSME clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unorganized Price Competition in Stainless Steel

Price-led competition from unorganized fabricators continues to strain entry-level SKUs, especially in rural and tier-3 corridors where cash-and-carry buying and hyper-local distribution are entrenched. These vendors typically avoid certification costs and operate at lower overheads, which enables sharp undercutting against branded 304-grade offerings that meet formal specifications. The result is a constraint on premium-feature adoption at the lowest price tiers, slowing the migration to noise-dampening pads, anti-condensation coatings, and accessory-ready ledges. As quality-control orders tighten and ISI marking becomes mainstream in procurement, traceable SKUs gain an advantage in large-format retail and public tenders, which can shift demand toward organized labels over time. For brands, the near-term response centers on education, warranty reinforcement, and dealer-incentive structures that highlight lifecycle value rather than headline price.

Raw-Material Cost Volatility Pressuring Margins

Volatility in inputs such as nickel, chromium, and manganese drives irregular cost swings in stainless-steel production, which complicates pricing and inventory planning for sink manufacturers. When coil costs escalated in early 2025, organized brands faced timing gaps between input inflation and retail price adjustments that compressed short-term margins. Mid-sized fabricators felt working-capital pressure as inventory revaluation cycles ran ahead of sell-through, complicating procurement schedules and dealer credit. Some producers explored product-mix shifts and hedging approaches to stabilize gross margins while protecting volume share in regions where low-cost alternatives remain visible. The medium-term effect is a sharper bifurcation between compliant, value-added stainless lines and commodity-grade options, with the Indian kitchen sink and other related markets leaning toward traceable specifications and serviceable warranties where buyers can assess long-term ownership costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Stainless Steel Anchors, Quartz Composites Accelerate Innovation

Stainless steel accounted for 84% share in 2025, and quartz composites are projected to advance at a 16.39% CAGR through 2031 as design-led formats gain attention among urban homeowners. Stainless steel remains the primary choice across budgets due to corrosion resistance, installer familiarity, and a broad catalog of sizes that fit Indian kitchens. Its ubiquity also reflects wide dealer coverage in traditional hardware stores and plumber-led channels that influence sink selection at the installation stage. Over the forecast horizon, cost spikes in steel inputs and rising preference for coordinated aesthetics with engineered-stone surfaces support incremental share gains for composites. The India kitchen sink and other related market benefits, as organized labels scale workstation-led offerings that integrate cutting boards, racks, and colanders for compact counters and dual-income households.

Quartz composites enable color-matched installations and seamless visual lines with granite or engineered-stone counters, which premium developers and modular-kitchen integrators highlight in showflats and studios. As experiential retail expands, homeowners can map accessories fit and clearance in galleries and through digital visualizers, which reduces post-install friction. Certified products and QR-verifiable markings also become important as retailers and public buyers emphasize traceability, and these elements further formalize the India kitchen sink and other related market size for higher-spec materials tied to warranties and service. Organized suppliers with diversified portfolios can spread certification costs and inventory planning across multiple SKUs, which supports steady availability in popular sizes. In parallel, capacity additions in composites by integrated players support faster lead times and ensure consistency that benefits both builders and renovators.

By Installation Type: Dual-Mount Emerges as Upgrade-Cycle Catalyst

Top-mount installations held 30% share in 2025, while dual-mount formats are forecast to grow at a 12.26% CAGR through 2031 as homeowners seek flexibility to switch between drop-in and undermount placements during renovation cycles. Undermount formats improve wipe-down convenience and visual continuity on stone counters but require skilled installers and precision tools that are unevenly available outside metros. This capability gap slows undermount adoption in semi-urban markets where installers may charge premiums for stone cutting and epoxy sealing. Dual-mount designs bridge this gap by allowing drop-in installation today and an undermount switch later without replacing the sink, which aligns with phased remodel budgets. As a result, the India kitchen sink and other related market sees higher accessory attachment on dual-mount SKUs, particularly where workstation ledges add prep efficiency in compact kitchens.

Premium galleries and modular-kitchen studios often showcase undermount and dual-mount side by side, which helps buyers visualize task flows and cleaning routines. Organized brands are standardizing clip systems and edge profiles to simplify reconfiguration and reduce installer time on site. This also supports service networks that can guarantee fit across common countertop thicknesses and stone types. The India kitchen sink industry uses these upgrade paths to improve lifecycle value and encourage repeat purchases of accessories matched to sink geometry. With growing countertop replacement cycles in apartments handed over in the past decade, dual-mount offerings capture a meaningful slice of renovation-driven demand.

By Bowl Configuration: Single Bowls Dominate, Drainboard-Equipped Units Gain Traction

Single-bowl sinks accounted for 62% in 2025 as compact urban apartments prioritize space-efficient fixtures, while single bowls with integrated drainboards are projected to grow at a 12.13% CAGR through 2031. Dual-bowl formats serve larger homes and households that parallelize prep and cleanup, often with 60 or 40 splits to fit large utensils without crowding the second basin. Workstation formats are in early adoption but appeal to buyers who value integrated accessories that keep counters uncluttered. In smaller homes without dishwashers, drainboards provide a drying surface that preserves counter space and reduces water pooling around the sink edge. These use cases sustain the Indian kitchen sink and other related markets as product managers tune slope angles and perforation patterns for efficient drainage and long-term durability.

In metro and tier-1 suburbs, showroom traffic indicates higher experimentation with workstation bundles that solve prep bottlenecks for dual-income households. Organized brands are investing in corrosion-resistant drainboard finishes and gasketed joints to extend product lifespans in humid kitchens. Dealers also pair bowls and accessories into curated sets that match common counter cutouts, which reduces return risk and increases average order value. As visual content and digital try-ons improve fit confidence, more buyers in semi-urban markets adopt single-bowl drainboard units for hygienic air-drying. This evolution supports a steady share for single bowls while enabling growth for drainboard-equipped variants within the India kitchen sink and other related market.

By End User: Residential Anchors, Commercial Segment Surges on QSR Boom

Residential applications held 82% share in 2025, and commercial applications are forecast to grow at a 12.28% CAGR as restaurants, cloud kitchens, and hospitality assets expand in tier-2 cities. Institutional buyers prioritize traceability and hygiene features, which channels demand toward brands with testing certifications and nationwide service coverage. In residential, renovation-driven purchases are rising as owners upgrade counters and switch to undermount or composite sinks within broader interior refreshes. Online and omnichannel bundles that include faucets and accessories encourage ecosystem buying and simplify logistics for homeowners and installers. As a result, the Indian kitchen sink and other related market gains from both first-fit in new apartments and recurring replacement cycles that are now more frequent than a decade ago.

Commercial kitchens require robust triple-bowl steel sinks and accessory sets that withstand extended daily use, which raises the importance of warranty fulfillment and spare-part availability. These requirements favor organized players with service networks and formal quality documentation. Hospitals and institutional facilities adopt stainless specifications that meet food-contact and hygiene expectations, further anchoring demand into traceable SKUs. Over time, this bifurcates the market into mass commodity offerings and value-added, compliant lines that carry brand trust. The Indian kitchen sink and other related markets will continue to reflect this split as buyers vary by application, usage hours, and service needs.

By Distribution Channel: Supermarkets/Hypermarkets Lead, Online Marketplaces Post Fastest CAGR

Traditional hardware stores and plumbing distributors hold the largest share today, but online marketplaces are projected to post the fastest growth at a 16.57% CAGR through 2031 as logistics and digital payments spread across tier-2 and tier-3 cities. Supermarkets and hypermarkets play an important role in tactile inspection and immediate take-home purchases, especially for replacement buyers who need quick swaps. Dealer galleries and brand showrooms support premiumization by offering design consultants and live kitchens that demonstrate undermount installations and workstation accessories. Online channels reduce friction through AR fit checks and virtual visualization that lower return rates and improve buyer confidence. This blended approach continues to formalize the India kitchen sink and other related markets as brands balance reach, experience, and speed to delivery.

Modular-kitchen OEMs increasingly bundle sinks into end-to-end quotes, which routes share away from wholesale-led distribution while lifting attachment of faucets and accessories. Gallery formats emphasize certified SKUs and ISI markings, which build trust in markets where quality claims matter for warranty and service. On the digital front, algorithmic merchandising highlights certification and verified reviews, elevating compliant brands. Over the next cycle, smaller distributors can protect margins by pivoting to installation and warranty services that justify value beyond inventory holding. The India kitchen sink and other related market will continue to reward omnichannel orchestration that guides buyers to the right mix of touch and convenience.

Geography Analysis

South India led regional distribution with 25.27% share in 2025, reflecting concentrated demand in Bengaluru and Chennai and earlier adoption of high-spec kitchen fixtures in surrounding metro suburbs. West India is a large demand center driven by Mumbai, Pune, and Ahmedabad, where premium housing density supports value-added sink formats. Pune’s home completions increased markedly in FY25 and contributed directly to new sink installations tied to handover schedules. South-focused manufacturing footprints and distribution corridors further support availability and lead time advantages across Tamil Nadu, Kerala, Karnataka, and Andhra Pradesh. The Indian kitchen sink and other related market responds to this activity with deeper assortments in metro-adjacent districts where modular-kitchen penetration is structurally higher than the national average.

North India accounts for a sizable share centered on Delhi NCR, supported by steady new launches and active renovation cycles in nearby tier-2 hubs. Organized brands in the region tailor assortments by micro-market, pairing durable stainless-steel SKUs for mid-market projects with composite and undermount offerings for premium towers and villas. Distribution coverage extends through hardware clusters and dealer galleries that serve both retail and builder segments. As mortgage affordability cycles improve, upgrade-led purchases in suburban corridors bolster demand for flexible formats such as dual-mount designs. The Indian kitchen sink and other related markets, therefore, benefit from both new-build momentum and retrofit waves that move with local housing cycles.

Organized brands have expanded distribution in Assam, Odisha, and West Bengal with a focus on assured after-sales service and certified SKUs that differentiate from unorganized alternatives. As road connectivity and logistics improve, online channels further complement sparse showroom networks in smaller cities. The net effect is a steady increase in formal retail share as buyers evaluate certified SKUs with transparent specifications and accessible warranties. This dynamic gradually raises the India kitchen sink and other related market sizes in regions that were once constrained by limited assortment and variable quality[4]India Brand Equity Foundation, “City-Level Housing Deliveries and Demand Indicators FY25,” India Brand Equity Foundation, ibef.org.

Competitive Landscape

The India kitchen sink and other related market shows moderate concentration, with Jaquar, Hindware, Carysil, Franke Faber, and Kohler together holding significant share in 2025, while a long tail of regional fabricators compete on local preferences and pricing. Integrated players emphasize cross-category portfolios spanning sinks, faucets, and appliances, which support bundling strategies in modular-kitchen quotes. Carysil’s scale-up in quartz and complementary lines, combined with long-standing partnerships for global sourcing programs, demonstrates the value of capacity, compliance, and coordinated design. Kohler’s experiential retail rollout with Studio Kohler in India extends brand-led discovery and consultative selling, which is aligned with affluent buyer expectations in large urban centers. Over the forecast, compliance maturity and omnichannel fluency are likely to be key differentiators as buyers weigh traceability, service, and delivery speed.

Quality-control orders and ISI marking requirements reinforce the advantage of organized brands that can certify SKUs and maintain consistent finish standards across batches. These brands also leverage QR-based verification and documentation to streamline participation in large-format retail and public procurement. Meanwhile, omnichannel orchestration, including visualization tools and gallery consults, reduces friction in buyer journeys and elevates attachment for accessories. Organized players are optimizing clip systems for dual-mount formats and workstation geometries that improve utility and reduce installation time. The India kitchen sink industry is thus consolidating around players who can support design-led assortments with dependable after-sales networks.

Examples of strategic moves include capacity expansions in quartz and stainless-steel lines, new experiential showrooms that improve discovery, and bundling programs that raise average order values. Hindware expanded its sinks and complementary kitchen lineup in 2024 to better serve mid-segment buyers through coordinated product introductions that simplify selection and fit. Carysil’s capacity planning in composites and faucet lines supports shorter lead times and consistent color matching for large projects and export orders. As certification visibility grows across online listings, algorithmic merchandising increasingly rewards traceable SKUs, which can steadily advance the organized share among first-time buyers and renovators in tier-2 and tier-3 cities.

India Kitchen Sink and Other Related Industry Leaders

Nirali NG

Carysil Limited

Jaquar Group

Hindware Home Innovation Ltd.

Franke

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nirali NG launched a premium Ceramic Art gallery in Gota, Ahmedabad, allowing customers to explore sink designs, sizes, and colors, as part of a push toward experiential retail in tier-1 and tier-2 cities.

- October 2024: Kohler India opened its first Studio Kohler experiential center in Hyderabad, showcasing luxury kitchen and bath innovations, including Cairn kitchen sinks in a composite material designed for durability and aesthetics.

- August 2025: Hindware Home Innovation announced a new manufacturing plant in Uttarakhand to strengthen capacity for kitchen sinks, chimneys, and hobs, targeting North India expansion by FY26.

India Kitchen Sink and Other Related Market Report Scope

A kitchen sink is a vital fixture for washing dishes and food preparation. This report will provide a detailed analysis of the kitchen sink and other related markets in India. The report delves into the market dynamics, highlights emerging trends in segment and regional markets, and offers insights into different product and application categories. The report delves into the key players and assesses the competitive landscape.

In India, the kitchen sink market and its related segments are categorized based on the number of bowls ranging from single to multi-bowl sinks. In addition, the segmentation is done by material, with options such as metallic and granite. The market is divided into specific categories, including the kitchen sink market, the stainless steel market, and the quartz kitchen sink market. The report offers market size and forecasts for the India kitchen sink and other related markets regarding revenue (USD) for all the above segments.

| Stainless Steel |

| Quartz |

| Fireclay |

| Granite/Marble |

| Acrylic |

| Others |

| Top-Mount / Drop-In |

| Undermount |

| Farmhouse / Apron-Front |

| Flush Mount |

| Dual Mount |

| Others |

| Single Bowl |

| Dual Bowl |

| Single Bowl with Drainboard |

| Residential |

| Commercial |

| Supermarkets/Hypermarkets |

| Exclusive Stores |

| Online |

| Other |

| North India |

| South India |

| West India |

| East India |

| By Material | Stainless Steel |

| Quartz | |

| Fireclay | |

| Granite/Marble | |

| Acrylic | |

| Others | |

| By Installation Type | Top-Mount / Drop-In |

| Undermount | |

| Farmhouse / Apron-Front | |

| Flush Mount | |

| Dual Mount | |

| Others | |

| By Bowl Configuration | Single Bowl |

| Dual Bowl | |

| Single Bowl with Drainboard | |

| By End User | Residential |

| Commercial | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Exclusive Stores | |

| Online | |

| Other | |

| By Geography | North India |

| South India | |

| West India | |

| East India |

Key Questions Answered in the Report

What is the current value of the Indian kitchen sink market?

The market is valued at USD 301.32 million in 2025 and is projected to reach USD 521.30 million by 2031.

Which material dominates sales?

Stainless steel leads with 84% share in 2025, due to durability and well-established supply chains.

What is the current size and growth outlook for the India kitchen sink and other related market through 2031?

The India kitchen sink and other related market size is USD 301.32 million in 2025 and is expected to reach USD 521.3 million by 2031 at an 11.24% CAGR over 2026-2031.

Which materials and formats are most influential in shaping buyer decisions in India?

Stainless steel leads by volume due to durability and familiarity, while quartz composites are gaining on a 16.39% CAGR as buyers seek color-matching and scratch resistance, with dual-mount formats enabling flexible upgrades over time.

How are online channels affecting how sinks are discovered and purchased in India?

Online marketplaces contribute a growing share and are projected to expand at a 16.57% CAGR, supported by AR visualization, faster last-mile logistics, and visible certification markers that guide buyers toward traceable SKUs.

Which regions in India are the largest and fastest growing for sinks?

South India leads with a 25.27% share, while the North-East is the fastest growing at a 12.22% CAGR through 2031, reflecting infrastructure upgrades and rising incomes that expand the addressable base.

What factors most constrain premium-feature adoption in the India kitchen sink industry?

Price-lead competition from unorganized suppliers in rural and tier-3 cities and installer skill gaps for undermount formats limit upscale adoption, while input-cost volatility pressures margins on branded stainless SKUs.

Page last updated on: