India Wood Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.59 Billion |

| Market Size (2026) | USD 19.54 Billion |

| Market Size (2031) | USD 25.09 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

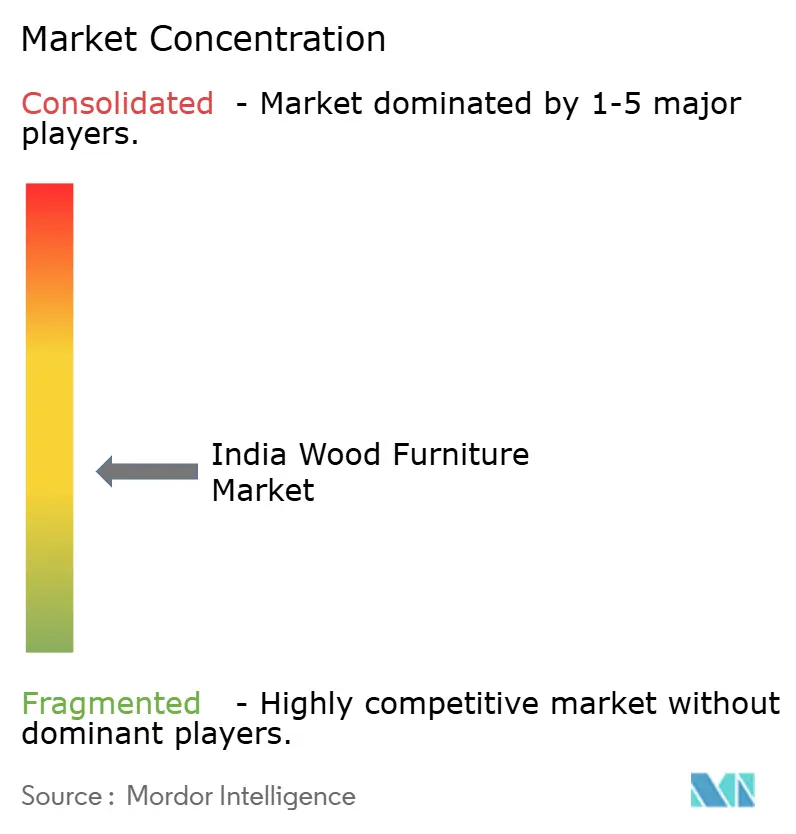

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wood Furniture Market Analysis by Mordor Intelligence

The India wood furniture market size was valued at USD 18.59 billion in 2025 and is estimated to grow from USD 19.54 billion in 2026 to reach USD 25.09 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). Market expansion is shifting from informal workshops to organized brands. These brands can tap into institutional capital, comply with environmental regulations, and leverage data-driven marketing. Multi-segment demand tailwinds are emerging from residential construction, hotel re-openings, and commercial real estate investments. As disposable incomes rise, the premium segment flourishes. Simultaneously, e-commerce broadens its reach, catering to mid-range buyers who prioritize customization and doorstep delivery. Demand for engineered and sustainable wood solutions is on the rise. Initiatives such as the National Bamboo Mission and favorable GST rates on bamboo and wood components support this growth. Organized players are channeling investments into automation and CNC production lines. This shift facilitates just-in-time customization, a feat once exclusive to informal carpenters, and slashes lead times.

Key Report Takeaways

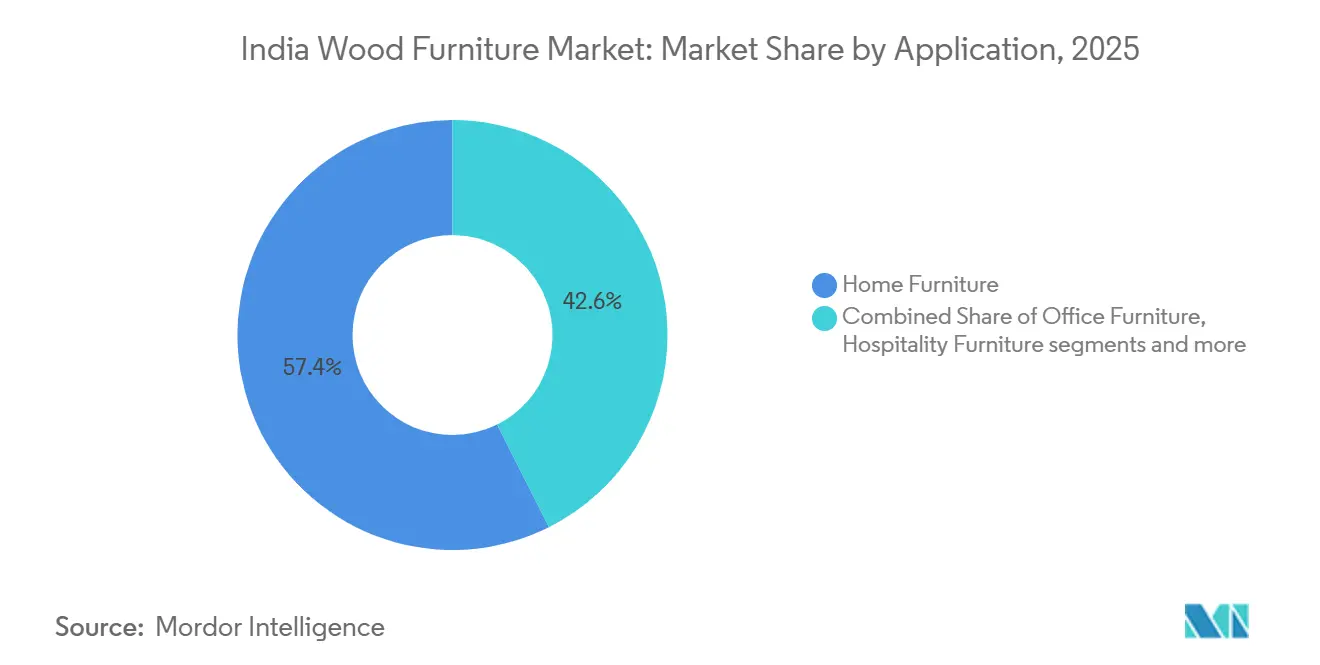

- By application, home furniture commanded 57.36% of India's wood furniture market size in 2025, whereas hospitality furniture is poised to expand at a 12.35% CAGR through 2031, the highest among all applications, and a signal that hotel pipeline growth is translating into steady contract orders.

- By material, engineered wood captured 46.64% market share of the India wood furniture market in 2025, reflecting its cost-to-performance advantage; bamboo and rattan products are the fastest movers, growing at a 16.64% CAGR that outstrips every other material class.

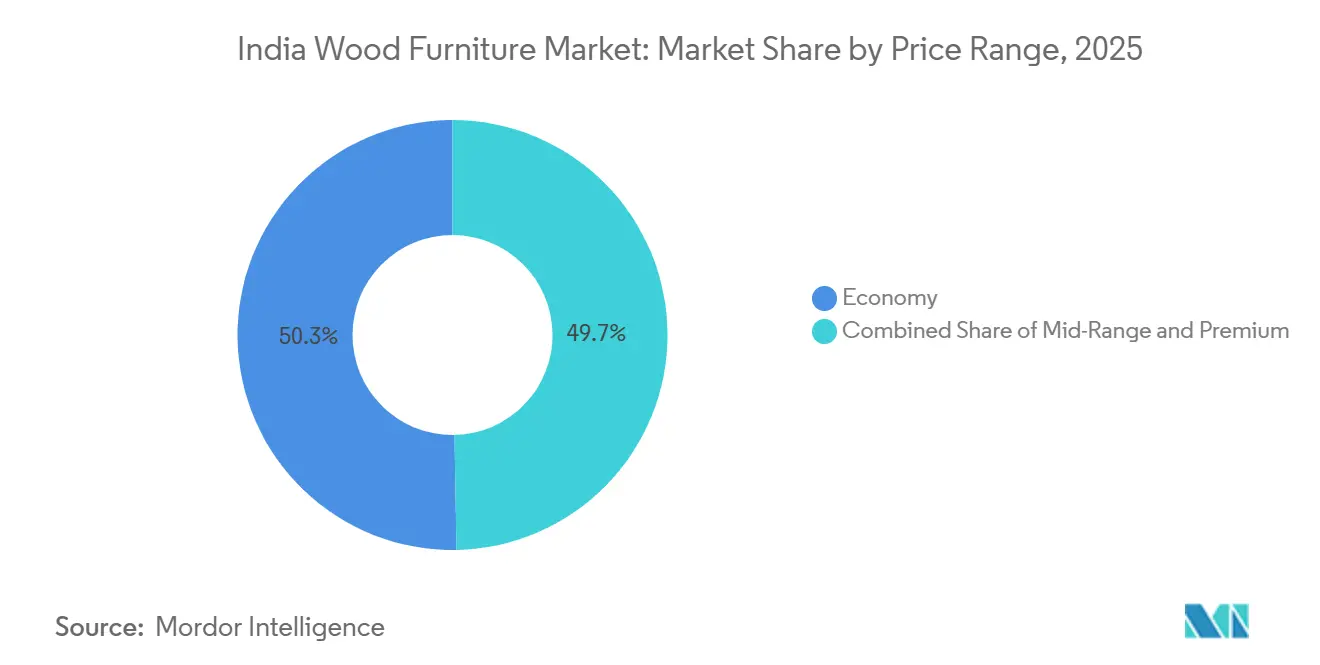

- By price range, the economy tier retained 50.32% of India's wood furniture market size in 2025, while the premium tier is set to post an 11.37% CAGR through 2031, the strongest growth within the pricing hierarchy.

- By distribution, specialty furniture stores led with 42.76% of India's wood furniture market size in 2025; online channels are projected to clock an 18.12% CAGR to 2031, making them the quickest-growing route to market.

- By geography, South India contributed 29.24% of India's wood furniture market size in 2025, and East India is forecast to expand at an 11.46% CAGR, the fastest regional clip through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Wood Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of co-working spaces is boosting modular demand | +0.8% | Metros such as Bengaluru, Mumbai, Delhi-NCR, Hyderabad | Medium term (2-4 years) |

| Growth in e-commerce and demand for customization | +1.2% | National, especially Tier-1 cities | Short term (≤ 2 years) |

| Housing-for-All and related construction initiatives | +1.0% | Tier-2 and Tier-3 cities nationwide | Long term (≥ 4 years) |

| GST rate adjustments supporting wood component usage | +0.6% | National | Short term (≤ 2 years) |

| Rapid urbanization and increasing disposable incomes | +0.9% | South and West India | Long term (≥ 4 years) |

| Short-term rental and coliving trends driving turnover | +0.4% | Metros and Tier-1 hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Co-Working Spaces is Boosting Modular Demand.

Flexible workspace operators are redefining commercial furniture buying cycles as they prioritize modular solutions that can be reconfigured quickly, accommodate varied tenant counts, and shorten replacement horizons to three–five years, compared with seven–ten years for fixed office installations [1]BS Reporter, “Luxury furniture brand Stanley Lifestyles gains 30% on trade debut,” business-standard.com. Repeat purchase patterns, therefore, intensify demand volumes, even while per-unit prices compress because of standardization. Manufacturers that have invested in rapid-turnaround production systems, such as Featherlite with a monthly output of 30,000 chairs and 8,000 workstations, are seizing share because they ship on tight timelines while matching professional aesthetic requirements. The co-working boom also accelerates product innovation, pushing suppliers to integrate height-adjustable desks, mobile screens, and cable-management solutions as default features. Legacy office suppliers that rely on bulk, one-off contracts risk share erosion unless they deploy modular catalogs and establish service agreements that guarantee swift re-layout support. Because co-working operators often expand via asset-light franchise models, they favor vendors who can deliver consistent specifications across multiple locations, strengthening the role of national-scale organized players within the India wood furniture market.

Growth in E-commerce and Demand for Customization

Online furniture marketplaces are demolishing geographic limitations by allowing consumers from any postal code to browse full catalogs, request bespoke dimensions, and preview finishes through augmented-reality overlays. WoodenStreet’s ambition to quadruple revenue to INR 10 billion (USD 117 million) within three years, supported by INR 43 million (USD 0.5 million) from Premji Invest, highlights strong venture-capital confidence and the significant scale potential still available in online furniture retail. In contrast, Pepperfry’s 30% decline in revenue to INR 189 crore (USD 22 million) in FY24 underscores the limits of a purely digital approach. Conversion rates rise sharply when customers visit physical stores, reinforcing that tactile evaluation remains critical for high-value furniture purchases. The implication is that winning strategies combine digital discovery with physical closure, especially because the average online ticket size remains close to one-third of the in-store benchmark. Customization drives basket size because shoppers willing to choose upholstery, legs, and wood tones are also willing to pay modest premiums for uniqueness. Consequently, logistics complexity is rising as return rates drop but outbound shipments become more personalized, prompting retailers to invest heavily in order-management systems that can route micro-batch production across multiple plants.

Housing-for-All and related Construction Initiatives

The Pradhan Mantri Awas Yojana has sanctioned 3.79 crore (37.9 million) homes, with 2.69 crore (26.9 million) already completed, releasing a wave of first-time owners who typically allocate 8%–12% of the house budget to furniture [2]Press Information Bureau, “GST Reforms 2025: Relief for Common Man, Boost for Businesses,” pib.gov.in. These incremental homeowners live largely in Tier-2 and Tier-3 cities where organized showrooms were scarce until recent years, forcing manufacturers to broaden distribution footprints beyond metros. Builders often bundle basic furniture packages to speed up occupancy certificates, opening direct-procurement channels for organized brands. Because the scheme funds small plots and compact apartments, demand leans toward space-saving beds, wardrobes with sliding doors, and convertible dining sets, segments where scalable engineered-wood designs excel. Stanley Lifestyles reports that 80% of its annual sales correlate with new-home handovers, demonstrating how real-estate cycles feed directly into the India wood furniture market. As GST reductions on cement to 18% accelerate project completions, the lag between civil handover and furniture buying shrinks, thereby compressing the sales cycle and spurring faster inventory turns for organized retailers.

GST Rate Adjustments Supporting Wood Component Usage

September 2025 GST reforms that reduced taxes on bamboo flooring, joinery, and wooden packing cases from 12% to 5% instantly lowered input costs for furniture producers [3]Press Information Bureau, “GST Reforms 2025: Relief for Common Man, Boost for Businesses,” pib.gov.in. By consolidating multiple slabs into uniform 5% and 18% rates, the reform cuts compliance expenses, especially for micro and small workshops migrating into the formal GST network. Lower working-capital blockages allow these firms to channel freed-up cash into better machinery, quality certifications, and showroom upgrades. Organized players benefit disproportionately because they can pass on part of the savings to price-sensitive buyers while widening gross margins. Moreover, the GST clarifies the playing field between domestic manufacturers and importers by eliminating hidden duties embedded in port handling and warehousing fees. The net result is faster formalization of production ecosystems that can then qualify for large government or institutional furniture tenders demanding IS 14276 certification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in timber prices is affecting supply costs | -0.7% | National, heavier on solid-wood specialists | Short term (≤ 2 years) |

| Price wars from large, unorganized sector players | -0.9% | North and East India pockets | Medium term (2-4 years) |

| Challenges in last-mile and reverse logistics | -0.5% | Tier-2 and Tier-3 towns | Medium term (2-4 years) |

| Costs of meeting sustainability certification standards | -0.3% | Export clusters and luxury brands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Timber Prices is Affecting Supply Costs.

Global timber indices remain choppy due to extreme-weather disruptions, currency shifts, and trade policy gyrations, making it difficult for manufacturers to lock long-term contracts without cost-escalation clauses. India imported USD 2.3 billion worth of timber in 2024, up sharply from earlier years, magnifying foreign-exchange exposure. Stanley Lifestyles sources wood mainly from Canada and New Zealand, keeping an 80:20 import-to-local ratio that enlarges currency risk [4]USDA Foreign Agricultural Service, “Wood and Wood Products Update 2024 – India,” fas.usda.gov. . To cushion volatility, the company plans to raise local sourcing to 70%–80% within several years, aligning with a broader industry shift toward plantation timber and engineered substitutes. Smaller workshops, which lack hedging facilities, pass sudden price surges directly to customers, often sacrificing orders in fierce price-sensitive zones of the India wood furniture market.

Price Wars from Large, Unorganized Sector Players

An estimated 60%-70% of the industry still sits outside the GST net, enabling informal outfits to avoid taxes and skirt labor compliance, which translates into visibly lower sticker prices. Organized firms, therefore, struggle to enforce uniform pricing, particularly in North India and parts of East India, where street-corner workshops can undersell branded catalogs by 20% on equivalent designs. Product recalls and service issues remain rampant in the informal channel, yet value-conscious buyers tolerate those risks in exchange for upfront savings. September 2025 GST reforms should compress the cost gap through stricter e-invoicing mandates and input-credit benefits that accrue only to registered suppliers. Nevertheless, transitional pain persists because small carpenters often adjust by trimming features or reducing plank thickness, intensifying quality variance across the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Furniture Retains Primacy as Hospitality Gains Momentum

Home furniture accounted for 57.36% of the 2025 market size, anchored by beds, wardrobes, and dining sets that are essential in every new residence, and this dominance delivers large, recurring volumes to organized manufacturers. In absolute terms, the segment generated more than USD 10 billion in 2024 revenue, illustrating why brands such as Nilkamal and Godrej Interio concentrate on full-home collections. The hospitality segment is much smaller today, yet its double-digit trajectory and 12.35% CAGR suggest that it will contribute a growing share of incremental growth to the India wood furniture market size over the next five years. Pipeline data from hotel-consulting firms show that nearly 47,000 keys are under construction, implying robust contract activity for lobby seating, headboards, and built-in wardrobes. Office furniture demand plateaued temporarily when hybrid work diluted workstation density, but spending is now tilting toward collaborative pods, acoustic panels, and ergonomic seating, keeping volumes stable. Educational and healthcare furniture remain niche slices yet benefit from public-sector capital expenditure programs that favor vendors with IS 14276 certification, giving organized brands a compliance-driven advantage.

Stanley Lifestyles illustrates the application mix evolution because 55% of its FY24 revenue came from sofas and recliners, reflecting heavy exposure to the living-room category. To dilute concentration risk, the company is moving into modular kitchens and cabinetry, which together represented 6% of FY24 turnover but are projected to reach double digits by FY27. Godrej Interio’s split is almost the mirror image because B2B accounts for 55% of its turnover, anchoring the brand in project-based revenue. The difference shows how diverse strategies can coexist: retail-oriented brands rely on repeat footfall and seasonal promotions, while project-oriented players cultivate long design-build contracts with institutions.

By Material: Engineered Wood Dominates Even as Bamboo Scales Up

Engineered wood held a 46.64% market share in 2025, underpinned by plywood, MDF, and particle board that allow precision machining, uniform surface finishes, and fast installation. The plywood segment alone is worth INR 30,000 crore - INR 40,000 crore (USD 3.51 billion - USD 4.68 billion), yet only 25%-30% is in organized hands, creating a deep runway for branded conversion. MDF, due to 22% historical growth since FY21, now boasts 80% organized penetration because technology barriers deter informal plants. Century Ply’s INR 550 crore (USD 64.3 million) particle-board line in Chennai adds 240,000 cubic-meter annual capacity, signaling scale bets on value-added engineered panels. Solid wood retains aspirational appeal due to natural grain and longevity, but supply availability is constrained, and prices swing with global lumber cycles.

Reclaimed timber addresses sustainability and cost concerns; Jodhpur’s Traditional Handicraft Centre converts 1,200 tonnes of salvaged teak into premium pieces each year, proving market willingness to pay for heritage wood. Bamboo and rattan combined accounted for a modest share in 2025, yet a 16.64% CAGR through 2031 signals sizeable upside, supported by 408 nurseries and 528 processing units funded by the National Bamboo Mission. Hybrid composites that merge wood with metal legs or epoxy-filled river tables cater to urban design aficionados, broadening the material palette and lifting average selling prices.

By Price Range: Economy Still Leads, but Premium Picks Up Speed

The economy tier captured 50.32% of 2025 sales, anchored by unorganized carpenters and lower-GST-bracket items that meet mass affordability thresholds. Mid-range products, typically priced between INR 15,000 and INR 50,000 (USD 175 - USD 584) per piece, sit squarely within the rising aspirational household’s purchase capacity and therefore absorb much of the organized sector’s marketing spend. Premium pieces, meanwhile, are registering an 11.37% CAGR through 2031 as disposable incomes climb and global brands introduce curated collections. IKEA’s progressive shift to 50% local sourcing by 2030 is shrinking cost gaps, nudging mid-range buyers upward as Scandinavian design becomes more attainable. Stanley Lifestyles, valued at more than INR 2,000 crore (USD 234 million) after its June 2024 IPO, straddles super-premium and luxury brackets, offering more than 1,000 designs, 3,000 SKUs, and 300+ leather colorways. Customization at that level lifts gross margins and fosters customer loyalty that price warriors find hard to match. Nilkamal’s @home chain illustrates how mid-range players hedge by selling both entry-level particle-board wardrobes and imported Italian leather recliners under one roof, capturing a broader wallet share without fragmenting brand identity.

By Distribution Channel: Specialty Stores Retain Clout While Online Accelerates

Specialty stores delivered 42.76% of the 2025 value, buoyed by tactile product trials, assisted selling, and immediate pickup, elements that remain decisive in big-ticket categories. HomeTown, with 44 outlets across 26 cities, exemplifies the format’s resilience as it pushes toward INR 1,100 crore (USD 128.6 million) turnover. Godrej Interio has gone deeper, launching about two new showrooms every week, taking its network above 1,000 stores. Online channels are growing fastest, at 18.12% CAGR through 2031, but pure clicks are giving way to clicks-plus-bricks as return rates, last-mile damages, and conversion bottlenecks force a physical overlay. WoodenStreet operates 100+ experience studios that double as distribution nodes, a model that raises capital intensity yet shrinks order-to-delivery cycle times. Pepperfry’s performance shows that build-out speed must be matched by store productivity; despite a 135+ showroom footprint, execution missteps pushed FY24 revenue down 30%. B2B and project channels remain relationship-driven, with sales teams bundling installation and maintenance in multi-year facility contracts. Big-box home centers akin to Home Depot remain nascent, but as organized retail supply chains mature, analysts expect a handful of entrants to test warehouse-style formats in the top six cities within five years.

Geography Analysis

In 2025, South India accounted for 29.24% of the market share, driven by its early adoption of organized retail, higher per capita spending, and its proximity to ports that support containerized exports. Manufacturing hubs like Hosur, Sriperumbudur, and Tumakuru cater to both local showrooms and international buyers, generating foreign exchange that funds technology advancements. State incentives such as tax holiday parks and ready-to-use sheds attract plywood and MDF producers, creating integrated supply chains. In Bengaluru and Chennai, a growing preference for sustainable furniture is evident, leading premium brands to emphasize FSC-certified timber and eco-friendly finishes. As apartment sizes shrink in IT hubs, there is a surge in demand for modular and space-saving furniture, such as fold-away desks and wardrobes. Retailers that provide in-house design and space planning services not only capture a larger share of consumer spending but also strengthen brand loyalty.

Meanwhile, East and Northeast India are carving a niche with bamboo and cane-based furniture. This momentum is supported by the National Bamboo Mission’s nurseries, which ensure a consistent feedstock and price stability. Improved infrastructure, particularly broad-gauge rail links, has reduced lead times from Guwahati to Kolkata. This efficiency has encouraged organized distributors to establish cross-dock centers. With rising consumer incomes, largely driven by remittances, there is a noticeable shift in demand from basic chairs to complete dining sets and hybrid decor items. Additionally, government procurement for schools and hospitals provides a stable anchor. Compliance with IS codes tends to favor formal manufacturers over informal carpenters. The moderate competition within the region offers early players an opportunity to consolidate their market presence before saturation occurs. Collectively, these trends strengthen both production capabilities and the reach of organized retail in the area.

Competitive Landscape

The India wood furniture market is characterized by moderate fragmentation, with organized players holding a meaningful but still limited share of the overall industry value. This points to an early phase of consolidation, where a handful of national brands are expanding steadily while regional and unorganized players continue to retain a large presence. Although the unorganized segment still dominates value sales, organized brands are gradually gaining ground through stronger omnichannel networks, brand visibility, and compliance with quality and certification standards. Recent capital-market activity highlights growing investor confidence, as evidenced by Stanley Lifestyles’ public listing in mid-2024, which supported expansion plans and premium positioning. Global entrants are also intensifying competition, with IKEA committing to long-term investments and increasing local sourcing, compelling domestic players to sharpen design, pricing, and execution. Established Indian brands such as Godrej Interio are leveraging financial strength and rapid store expansion to deepen regional penetration and accelerate share gains in key southern markets.

Technology investment is the separator between category leaders and mid-pack players. Stanley Lifestyles’ CNC milling lines and automated leather-cutting machines enable 72-hour turnaround on made-to-order sofas, outperforming industry averages of 12–15 days. Pepperfry and WoodenStreet deploy AR visualization, cutting return rates by up to 40% compared with static catalog webshops. Rental-as-a-service startups such as Furlenco fill a white space for mobile consumers unwilling to commit capital outlays, and their subscription models supply a predictable revenue stream that cushions macrocycle swings. Established manufacturers counter by offering buy-back guarantees or trade-in credits that mimic subscription flexibility, illustrating competitive convergence.

Market consolidation is likely because smaller workshops must either formalize to claim GST credits and institutional orders, or retreat to hyperlocal carpentry niches. Yet barriers to entry remain low at the small-ticket end, preserving a tail of micro-players who serve budget shoppers. Organized incumbents seek differentiation through extended warranties, free design consultations, and zero-cost EMI financing, bundling value-added services that informal rivals cannot replicate at scale. Sustainability compliance is emerging as another moat, since audits and traceability systems are costly to replicate. Over the medium term, the top ten organized players are projected to lift their combined share above 40%, but rapid population growth and diversified price points will keep absolute opportunities alive for new entrants.

India Wood Furniture Industry Leaders

Godrej Interio

Durian Industries Ltd

Nilkamal Ltd

Urban Ladder

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: In a move to bolster its presence in India, IKEA launched online sales in the Delhi-NCR region, backed by a sprawling 180,000 ft² distribution center in Gurgaon, ensuring customers a promise of next-day delivery.

- July 2025: Nilkamal Ltd agreed to acquire the healthcare furniture business of Imedfurns Private Limited for INR 3 crore (USD 0.35 million), that to be paid over four years, marking its entry into the specialized healthcare furniture segment. The deal includes intellectual property, existing contracts, employee transfers, and goodwill, aiming to diversify Nilkamal’s product portfolio and tap new institutional demand.

- June 2024: Stanley Lifestyles completed an initial public offering of INR 537 crore (USD 62.8 million), listing on BSE and NSE at a 35% premium to the issue price of INR 369 (USD 4.31), achieving a market capitalization exceeding INR 2,000 crore (USD 234 million). The company raised INR 200 crore (USD 23.4 million) through fresh equity to fund store expansion, renovations, and machinery capex, reflecting strong investor confidence in the premium furniture segment.

India Wood Furniture Market Report Scope

The wood market in India refers to the extraction, processing, and production of wood and wood-based products. It consists of activities such as logging, sawmilling, and the manufacturing of products like timber, plywood, veneers, furniture, and wood-based panels. This industry serves various sectors, including construction, furniture making, and interior design, and is driven by factors like urbanization, economic growth, and rising consumer demand for wood products.

The Indian wood market is segmented into application, material, price range, distribution channel, and geography. By application, the market is segmented into home furniture, office furniture, hospitality furniture, educational furniture, healthcare furniture, and other applications. By material, the market is segmented into solid wood, engineered wood, bamboo & rattan, reclaimed wood, and hybrid/composite materials. By price range, the market is segmented into economy, mid-range, and premium. By distribution channel, the market is segmented into B2C/retail and B2B / project. By geography, the market is segmented into North India, West India, South India, East & North-East India. The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Home Furniture | Chairs |

| Tables (Side Tables, Coffee Tables, Dressing Tables, etc.) | |

| Beds | |

| Wardrobe | |

| Sofas | |

| Dining Tables/Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (Bathroom Furniture, Outdoor Furniture, etc.) | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (Public Places, Retail Malls, Government Offices, etc.) |

| Solid Wood (Teak, Sheesham, Mango, etc.) |

| Engineered Wood (Plywood, MDF, Particle Board) |

| Bamboo & Rattan |

| Reclaimed Wood |

| Hybrid/Composite Materials |

| Economy |

| Mid-Range |

| Premium |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

| North India |

| West India |

| South India |

| East India |

| By Application | Home Furniture | Chairs |

| Tables (Side Tables, Coffee Tables, Dressing Tables, etc.) | ||

| Beds | ||

| Wardrobe | ||

| Sofas | ||

| Dining Tables/Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (Bathroom Furniture, Outdoor Furniture, etc.) | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (Public Places, Retail Malls, Government Offices, etc.) | ||

| By Material | Solid Wood (Teak, Sheesham, Mango, etc.) | |

| Engineered Wood (Plywood, MDF, Particle Board) | ||

| Bamboo & Rattan | ||

| Reclaimed Wood | ||

| Hybrid/Composite Materials | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | North India | |

| West India | ||

| South India | ||

| East India | ||

Key Questions Answered in the Report

How large is the India wood furniture market in 2026?

The market stands at USD 19.54 billion in 2026 and is projected to reach USD 25.09 billion by 2031.

Which segment grows fastest through 2031?

Hospitality furniture records the quickest pace, advancing at a 12.35% CAGR on the back of new hotel openings.

What material leads current sales?

Engineered wood captures 46.64% of 2025 revenue because it balances cost, durability, and design flexibility.

How fast are online channels expanding?

Online sales are set to grow at an 18.12% CAGR through 2031, the strongest among all distribution routes.

Why is bamboo furniture gaining popularity?

Government-funded nurseries and a lower post-GST tax rate make bamboo more affordable while meeting sustainability preferences.

Which region offers the highest growth runway?

East India is forecast to clock an 11.46% CAGR through 2031, leveraging bamboo abundance and infrastructure upgrades.

Page last updated on: