India Electric Rickshaw Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

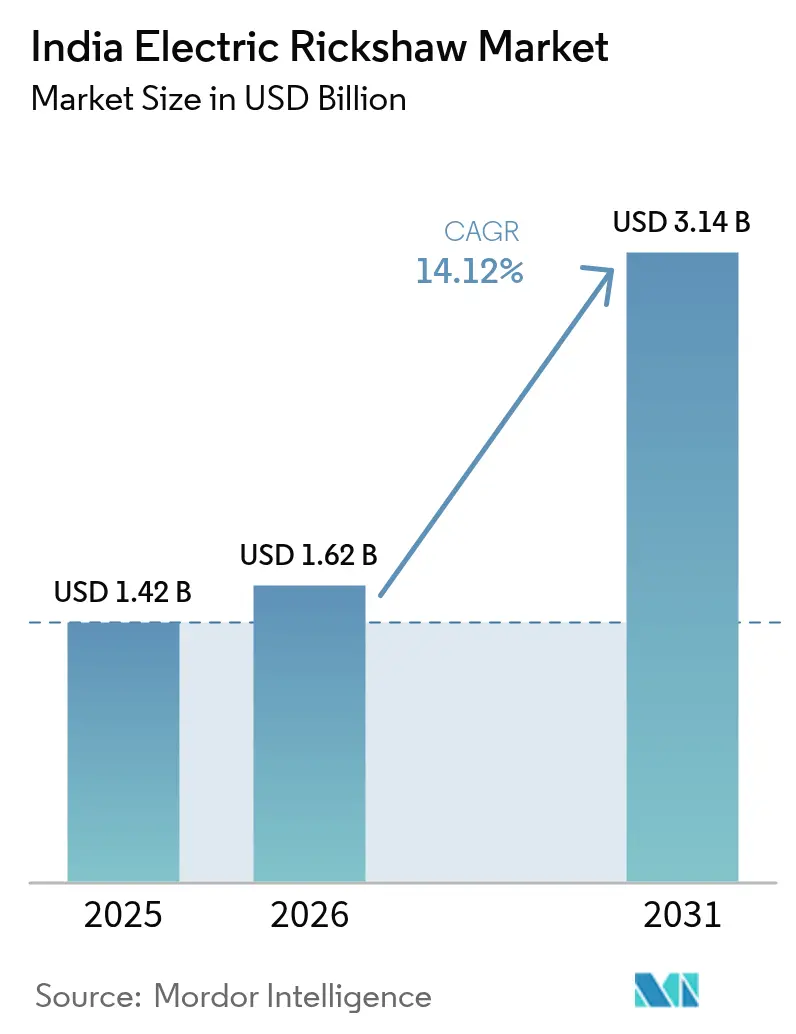

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 3.14 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Electric Rickshaw Market Analysis by Mordor Intelligence

The Indian electric rickshaw market size was valued at USD 1.42 billion in 2025 and estimated to grow from USD 1.62 billion in 2026 to reach USD 3.14 billion by 2031, at a CAGR of 14.12% during the forecast period (2026-2031). This rapid expansion reflects government incentives, aggressive state-level policies, growing e-commerce demand, and heightened urban air-quality goals. Passenger carrier dominance, strong recycling economics for lead-acid batteries, and the swift pivot of e-commerce logistics toward electric cargo variants are sustaining volume momentum. Parallel advances in battery chemistry, modular finance models, and power-train efficiency are widening the total addressable base beyond Tier-I metros into Tier-II and Tier-III towns. Competitive rivalry intensifies as legacy OEMs, innovative start-ups, and global automakers commit capital and engineering talent to capture the next wave of growth.[1]"India leads electric three-wheeler market with 20% rise in sales," International Energy Agency, iea.org

Key Report Takeaways

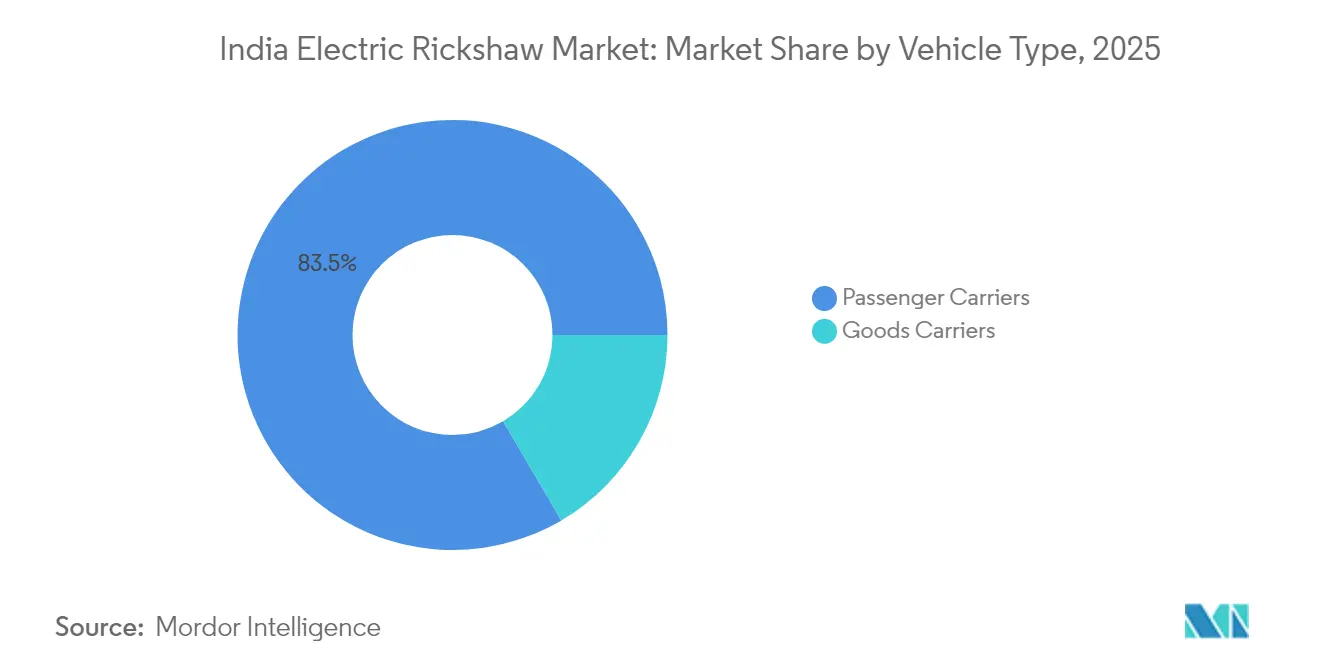

- By vehicle type, passenger carriers led with 83.45% revenue share in 2025, while goods carriers are projected to expand at a 28.10% CAGR to 2031.

- By power output, the 1–1.5 kW segment held 53.90% of the Indian electric three-wheeler market share in 2025; above 1.5 kW, the market is advancing at a 30.95% CAGR.

- By battery type, lead-acid commanded 71.40% share of the Indian electric three-wheeler market size in 2025, whereas lithium-ion (LFP) is set to grow at a 37.10% CAGR.

- By battery capacity, up to 3 kWh accounted for 61.20% share of the Indian electric three-wheeler market size in 2025; 3–6 kWh will expand at a 33.85% CAGR through 2031.

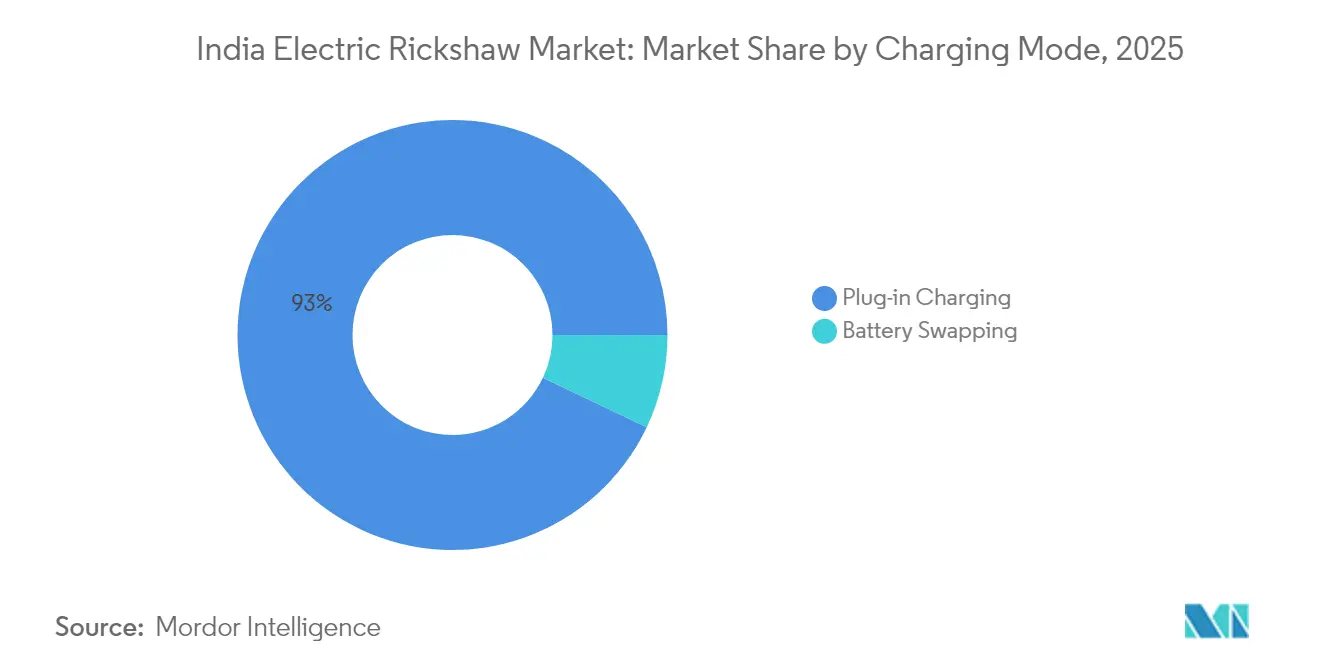

- By charging mode, plug-in charging dominated with 92.95% share in 2025, yet battery swapping is forecast to rise at a 42.30% CAGR.

- By ownership model, individual owner-drivers controlled 87.50% of 2025 volume, while fleet operators record the fastest CAGR at 30.10%.

- By state, Uttar Pradesh captured 37.80% of sales in 2025; Punjab shows the highest growth trajectory at 27.20% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Electric Rickshaw Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAME-II and state incentives boosting tier-II adoption | +2.2% | Pan-India, with concentration in Tier-II cities | Medium term (2-4 years) |

| Shared mobility demand rising in urbanizing towns | +1.7% | Urban and peri-urban areas across India | Medium term (2-4 years) |

| E-commerce firms adopting cargo e-rickshaws | +1.5% | Metropolitan cities, expanding to Tier-II cities | Short term (≤ 2 years) |

| Battery recycling cutting ownership costs | +1.3% | Pan-India, with higher impact in established markets | Medium term (2-4 years) |

| BaaS models reducing upfront capex | +0.8% | Urban centers with developed charging networks | Short term (≤ 2 years) |

| ICE three-wheelers to be phased out in Delhi-NCR by 2030 | +0.7% | Delhi-NCR, with spillover to other metro regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FAME-II Subsidy Extension and State Incentives Accelerating Tier-II Adoption

Federal continuity between the extended FAME-II program and the Electric Mobility Promotion Scheme 2024 keeps per-vehicle subsidies intact, lowering acquisition cost barriers for drivers outside major metros. State top-ups—ranging from purchase rebates to road-tax waivers in Maharashtra, Karnataka, and Delhi—stack further savings, making electric three-wheelers price-competitive with ICE models at the point of sale. Subsidy density correlates strongly with registrations; assessments reveal a 46.16% sales uplift for each standard-deviation rise in state support intensity. Local financiers report shorter payback periods, encouraging broader credit participation. Combined, these fiscal levers push the Indian electric three-wheeler market deeper into cost-sensitive Tier-II clusters where informal transit demand is surging.[2]“Subsidy Impact on Electric Three-Wheeler Uptake,” IEEFA, ieefa.org

Rising Demand for Last-Mile Shared Mobility in Rapidly Urbanising Towns

India’s expanding network of mid-sized cities relies heavily on auto-rickshaws to bridge first- and last-mile gaps in public transit. Electric variants cut running expenses to INR 0.50–0.70/km against INR 3–4/km for petrol or CNG, creating immediate earnings upside for owner-drivers. Shared-mobility aggregators such as Uber and Rapido are onboarding e-rickshaws to meet municipal clean-air mandates and rider price sensitivity. High daily utilization amplifies fuel-cost arbitrage, accelerating payback on the higher upfront purchase. Seamless digital booking elevates asset productivity, further reinforcing operator economics and boosting adoption across the Indian electric three-wheeler market.

E-Commerce Logistics Embracing Cargo E-Rickshaws for Intra-City Delivery

Surging online retail volumes require nimble, low-emission delivery modes that can navigate urban congestion and access restricted zones. Cargo electric three-wheelers offer 20–25% cost savings per drop relative to small diesel vans, while meeting corporate ESG targets. Flipkart, Amazon India, and grocery platforms are scaling dedicated fleets; Bajaj’s supply pact for over 1,000 units to Flipkart exemplifies the trend. Telematics-enabled route optimization raises daily delivery counts, maximizing revenue per vehicle. As e-commerce demand spreads to secondary cities, platform commitments lock in multi-year volume visibility for OEMs.

Lead-Acid Battery Recycling Ecosystem Lowering Total Cost of Ownership

A near-closed-loop supply chain recovers 99% of lead from spent batteries, monetizing end-of-life value and defraying initial purchase price. Local recyclers pay competitive buy-back rates, effectively compressing lifecycle energy storage costs. Because 60% of India’s lead-acid demand already serves transportation, collection channels are mature and well-distributed. For cash-constrained owner-drivers, predictable residual value underpins financing confidence and manageable EMIs. Until lithium-ion prices fall further, this recycling dividend secures lead-acid’s volume edge in the Indian electric three-wheeler market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Informal financing limiting driver purchases | -2.1% | Pan-India, more severe in rural areas | Medium term (2-4 years) |

| Slow battery standard rollout hindering interoperability | -2.0% | Urban centers with multiple battery swapping operators | Medium term (2-4 years) |

| Chassis safety concerns on rural roads | -1.7% | Rural and semi-urban areas with poor road infrastructure | Medium term (2-4 years) |

| Low-quality lead-acid batteries from unorganised supply | -1.3% | Tier-II and Tier-III cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented & Informal Financing Channels Constraining Driver Purchases

The lack of scale credit pipelines keeps effective interest rates high and loan-to-value ratios low, dampening uptake among independent drivers whose livelihood depends on daily fare receipts. Technology-risk perceptions lead many lenders to treat electric variants as non-standard assets, constricting credit lines despite lower running costs. Informal money-lenders bridge the gap but charge punitive rates, eroding total cost of ownership benefits. Development-finance institutions advocate blended-finance pools to de-risk retail lending, yet implementation remains slow outside major cities. Until mainstream banks normalize underwriting for electric three-wheelers, growth will undershoot potential in segments most sensitive to up-front affordability.

Safety Concerns Over Chassis Integrity on Rural Roads

Uneven road surfaces and overloading expose structural limitations in low-cost models, fueling rider apprehension and higher insurance premiums. Surveys highlight instability, limited crash protection, and rollover fear, especially among women and older passengers. Because a sizable share of production comes from small-scale assemblers, adherence to uniform structural standards is inconsistent. Financing agencies factor accident risk into loan pricing, further constraining credit flow. Harmonized safety certification and localized test facilities could allay these concerns, but progress remains uneven across states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Cargo Carriers Leverage E-Commerce Tailwinds

India electric rickshaw market share is currently dominated by the passenger carrier segment, which accounted for 83.45% of unit sales in 2025, cementing its role as the backbone of intra-city shared mobility. Dense urban routes and all-day utilization let drivers exploit penny-per-kilometer energy costs, reinforcing segment resilience. Goods carriers, however, are registering the fastest 28.10% CAGR as online retail pushes demand for nimble, emissions-free last-mile delivery. Amazon India, Flipkart, and quick-commerce players are formalizing procurement pipelines with established OEMs, ensuring predictable volume growth. Segment-specific designs such as refrigerated bodies widen addressable markets in food distribution and pharmaceuticals. Higher payload ratings and telematics integration make cargo e-rickshaws an essential piece of future city-logistics blueprints.

In absolute volume terms, passenger variants will continue to dominate the Indian electric three-wheeler market, yet the value contribution from cargo units will rise steadily through premium specification mixes. Tax breaks for commercial vehicles and dedicated micro-fulfillment hubs in Tier-II cities will push cumulative cargo penetration higher. As urban congestion charges tighten, freight operators will prefer electric three-wheelers over light trucks, cementing the segment’s long-term upside.

By Power Output: High-Power Motorizations Unlock Premium Use-Cases

India electric rickshaw market share by power output was led by the 1–1.5 kW motor segment, which accounted for 53.90% of total demand in 2025. This power band delivers sufficient torque for frequent stop-start city driving while conserving battery life, making it ideal for typical passenger operations. Operators value its balanced offering—affordable upfront cost with practical range—especially in high-usage urban duty cycles.

In contrast, powertrains rated above 1.5 kW are witnessing the fastest growth in the India electric rickshaw market, expanding at a 30.95% CAGR as payload demands and gradient-handling requirements rise. The segment is benefiting from advancements in e-axle technologies, including integrated motor controllers and IP-rated enclosures, which enhance durability during India’s heavy monsoon conditions and boost fleet confidence.

The higher-powered bracket supports refrigerated cargo, steep-gradient hill-stations, and premium ride-hailing tiers that demand faster trip times. Component suppliers are localizing magnets and stators, cutting imported content and stabilizing price points. As unit economics improve, the Indian electric three-wheeler market size for the above-1.5 kW class is projected to widen its revenue share, ushering in a new competitiveness layer focused on performance rather than solely cost.

By Battery Type: LFP Chemistry Disrupts Legacy Dominance

Lead-acid batteries retained 71.40% share in 2025 owing to low entry cost and robust recycling value. Familiarity among neighborhood mechanics and abundant second-hand spares keep service downtime minimal. However, limited depth-of-discharge tolerance shortens real-world range, driving multi-day charging cycles that crimp revenue. Falling cell prices and enhanced safety credentials are propelling LFP lithium-ion packs, now the fastest-growing chemistry at a 37.10% CAGR. Domestic cell assembly under the Production-Linked Incentive scheme further narrows cost gaps.

Thermal stability, longer cycle life, and higher usable capacity give operators more trips per charge, directly boosting earnings. OEMs pair LFP packs with advanced battery-management systems that issue predictive maintenance alerts, reducing unexpected breakdowns. As warranty terms lengthen, financiers are re-rating residual values, expanding loan tenures. The Indian electric three-wheeler market share tilt toward LFP will accelerate once standardized cell formats unlock swapping interoperability.

By Battery Capacity: Mid-Range Packs Hit Cost-Performance Sweet Spot

Up to 3 kWh packs dominated with 61.20% of 2025 installations, adequate for 80–90 km urban duty cycles. Their lower mass supports lighter chassis and reduces tire wear, appealing to independent driver-owners. Yet, longer routes for peri-urban commuters and logistics hubs require extended autonomy. The 3–6 kWh bracket is set to sprint at a 33.85% CAGR, supplying 110–160 km real-world range without excessive price inflation. Pack engineering advances raise gravimetric energy density, allowing OEMs to slot higher capacity into legacy footprints.

Bulk procurement programs by fleet operators favor the 3–6 kWh class because it balances initial cash outlay with route flexibility, mitigating mid-shift charging downtime. As depot chargers reach higher kw ratings, turnaround times shrink, lifting daily revenue potential. Consequently, the Indian electric three-wheeler market size attributed to mid-capacity packs will expand steadily through the decade.

By Charging Mode: Battery Swapping Expands Operational Uptime

Plug-in charging commanded 92.95% of 2025 deployments due to its simplicity and compatibility with household sockets. Rural and semi-urban drivers rely on overnight top-ups, leveraging lower off-peak tariffs. Nevertheless, business models demanding near-continuous vehicle availability see productivity losses when vehicles are tethered for hours. Battery swapping, scaling at a 42.30% CAGR, compresses downtime to minutes, a game-changer for logistics fleets. Subscription-based energy access spreads costs over utilization, aligning with cash-flow realities of daily wage drivers.

Policy drafts targeting standardized pack dimensions promise to unlock cross-network interoperability, an inflection point for mass adoption. Investment from energy majors into swap-station rollouts underpins confidence that the Indian electric three-wheeler market will soon enjoy comprehensive urban coverage. Over time, blended strategies—plug-in at night, swap during peak hours—will dominate best-practice fleet operations.

By Ownership Model: Organized Fleets Professionalize the Ecosystem

Individual drivers owned 87.50% of electric three-wheelers in 2025, reflecting the sector’s grassroots origins. Informal routes, flexible hours, and family labor underpin their business logic. Yet professional fleet operators recorded the highest 30.10% CAGR by bundling vehicle leasing, maintenance, and digital freight brokerage into turnkey offerings. Alt Mobility’s lease-to-own program links drivers with aggregators, ensuring assured earnings that de-risk financing.

Commercial contracts with e-commerce giants secure predictable kilometre utilization, justifying larger battery packs and telematics investments. Data-driven maintenance lowers downtime, improving asset turns and extending lifespan. As fleets standardize procurement, OEMs gain volume visibility, enabling component localization and cost deflation. This virtuous cycle will progressively tilt overall volume toward organized entities within the Indian electric three-wheeler market.

Geography Analysis

Uttar Pradesh stood out in 2025 with 37.80% of national sales, driven by dense urban populations, robust policy incentives, and a maturing dealership network. The state registered 266,106 units, underscoring how a targeted nodal-agency approach can scale adoption quickly. Bihar followed with 89,683 units, benefiting from high per-capita dependence on auto-rickshaws for short-haul mobility and incentives that offset initial sticker shock. Delhi’s directive to phase out fossil-fuel autorickshaws by 2025, coupled with plans for 13,200 chargers, is reshaping the capital’s transport mix at an accelerated clip.

Punjab, with a 27.20% CAGR forecast, combines agricultural market-yard logistics and rising urban commute needs to fuel demand. Targeted subsidies and simplified registration norms shorten adoption cycles. Maharashtra leads electric commercial-vehicle sales nationally; its 2,279 three-wheeler registrations in 2024 reflect state-level scrappage bonuses and toll exemptions. Karnataka’s tech-hub economy supports app-based ride-sharing pilots, creating stable utilization benchmarks that encourage financiers.

Infrastructure disparities remain pronounced. Chandigarh has the highest charger-to-road-length ratio, while Delhi ranks first in absolute charger count, offering one unit every 12.5 km. States with aligned electricity-tariff concessions and clear municipal parking guidelines are recording higher utilisation per charger. As more states adopt phased ICE retirement schedules, the Indian electric three-wheeler market will witness a geographic diffusion of demand beyond early-adopter corridors, balancing north-centric concentration with southern and western growth pockets.

Competitive Landscape

More than 575 manufacturers participate, yet leadership is coalescing around brands with scale and service depth. Mahindra Last Mile Mobility is evolving as a key player, leveraging its all-India service footprint and a tie-up with Vidyut to roll out battery-subscription financing. Bajaj Auto, scaling output on its Chakan line, confirming that established OEM quality systems and parts networks resonate with risk-averse buyers. YC Electric scaling through price-aggressive models that appeal to rural and Tier-III segments.

Domestic challenger Euler Motors specializes in cargo applications, partnering with e-commerce fleets to validate total-cost-of-ownership claims through data dashboards. Battery Smart focuses solely on swapping, using asset-light franchise models to expand network density. Hyundai's January 2025 entry announcement brings high-precision engineering, raising the bar on safety features and energy efficiency across the board.[3]Jee-hyun Kim, “Hyundai Launches E-Rickshaw Initiative in India,” The Chosun Ilbo, chosun.com

Strategic focus is shifting from standalone hardware to lifecycle value propositions. Piaggio’s battery-subscription plan lowers ex-showroom cost to INR 259,000, broadening the buyer funnel. Mahindra experiments with pay-per-kilometer energy bundles bundled with extended warranties. OEMs are also lobbying state utilities for fleet-tariff categorization, locking in long-term electricity cost visibility. As technology and financing models converge, differentiation will pivot on ecosystem completeness—spare-parts availability, uptime guarantees, and residual-value management—rather than unit price alone.

India Electric Rickshaw Industry Leaders

-

YC Electric Vehicle

-

Saera Electric Auto Pvt. Ltd.

-

Mahindra Electric Mobility Ltd.

-

Terra Motors India Corp.

-

Piaggio Vehicles Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Delhi government released EV Policy 2.0 mandating fossil-fuel three-wheeler phase-out by Aug 2025 and earmarked 13,200 public chargers.

- April 2025: Piaggio Vehicles unveiled a battery subscription for its Apé Elektrik range, covering up to 150,000 km under an 8-year term.

- April 2025: Vidyut raised USD 2.5 million from Flourish Ventures to scale its Battery-as-a-Service platform across additional vehicle segments.

- May 2024: Borzo launched an electric three-wheeler fleet in Mumbai, targeting 1,000 daily deliveries and a 30% fleet electrification goal.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every India-registered, battery-powered three-wheeler designed to carry passengers or light cargo, including L3 passenger e-rickshaws and L5 cargo variants, so long as propulsion is supplied exclusively by an electric drivetrain and the vehicle is licensed for public road use. One bundled figure is reported for value (USD) and another for units.

Exclusions: Kit retrofits, e-carts confined to private campuses, and prototypes not yet homologated have been kept outside the scope.

Segmentation Overview

-

By Vehicle Type

- Passenger Carriers

- Goods Carriers

-

By Power Output

- Up to 1 kW

- 1 – 1.5 kW

- Above 1.5 kW

-

By Battery Type

- Lead-Acid

- Lithium-ion (NMC/NCA)

- Lithium-ion (LFP)

- Other Chemistries (Li-Polymer, Ni-MH)

-

By Battery Capacity

- Up to 3 kWh

- 3 – 6 kWh

- Above 6 kWh

-

By Charging Mode

- Plug-in Charging

- Battery Swapping

-

By Ownership Model

- Individual Owner-Drivers

- Fleet Operators

- Aggregators / MaaS Platforms

-

By State

- Uttar Pradesh

- Delhi

- Maharashtra

- Bihar

- Rajasthan

- Karnataka

- Tamil Nadu

- Punjab

- Telangana

- Rest of India

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews with vehicle assemblers, fleet financiers, state transport officials, and organized fleet operators across Uttar Pradesh, Delhi NCR, Maharashtra, and Assam enabled us to sanity-check reported prices, downtimes, and charging patterns. Follow-up online surveys of independent owner-drivers balanced the institutional view with real-world operating cost data.

Desk Research

Mordor analysts began with transport data released by the Ministry of Road Transport & Highways, state-level VAHAN registration feeds, and monthly sales digests from JMK Research. Additional direction came from FAME-II incentive disbursement ledgers, Directorate General of Commercial Intelligence & Statistics export files, and policy papers issued by NITI Aayog, which together clarified volumes, battery chemistries, and subsidy uptake.

Company filings on the MCA portal, investor presentations of listed electric three-wheeler makers, and news captured through Dow Jones Factiva helped us benchmark average selling prices and cost trajectories. Patent searches on Questel highlighted upcoming battery swap architectures that influence our long-run adoption curve.

The sources cited above are illustrative only; many more were tapped for cross-checks and context building.

Market-Sizing & Forecasting

A top-down build was first created from 2024 VAHAN registrations, which are then adjusted for scrappage and gray-market inflows. Selective bottom-up roll-ups of sampled OEM shipments and fleet procurement deals validated the totals. Key variables inside the model include annual subsidy allocation under FAME-II and EMPS, average lead-acid scrap price, lithium-ion import landed cost, domestic electricity tariff for LT commercial meters, and state-specific passenger fare ceilings, each steering price or volume levers. Multivariate regression links these drivers to historical uptake before the outputs are projected through 2030, while scenario analysis widens the forecast band when policy shifts appear likely.

Data Validation & Update Cycle

Outputs run through variance tests versus quarterly MCA revenue filings and monthly registration flashes. Senior reviewers sign off once anomalies are resolved. Mordor Intelligence refreshes every twelve months, and extraordinary policy moves trigger interim recalculations so users always receive the latest view.

Why Mordor's India Electric Rickshaw Baseline Inspires Confidence

Published estimates for this market often differ, and that gap usually stems from inconsistent scope, mixed treatment of unorganized sales, and currency conversions done on outdated rates.

Key gap drivers include competitor studies that exclude cargo variants, rely solely on organized-sector invoices, or annualize limited monthly data without adjusting for festival-season spikes. A few inflate totals by adding unregistered retrofit kits. Mordor's disciplined variable set, annual refresh cadence, and dual cross-check process reduce those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.42 B (2025) | Mordor Intelligence | - |

| USD 3.90 B (2024) | Global Consultancy A | Bundles electric autos and low-speed campus carts, no scrappage discount |

| USD 0.31 B (2024) | Industry Journal B | Counts only organized OEM invoices, omits gray-market sales and cargo units |

The comparison shows that while external figures swing widely, our balanced top-down build aligned with ground interviews provides a transparent, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the Indian electric three-wheeler market?

As of 2026, the India electric rickshaw market size is estimated at USD 1.62 billion, and it is projected to reach USD 3.14 billion by 2031, growing at a CAGR of 14.12% during the forecast period (2026-2031).

Which segment is growing fastest in the Indian electric three-wheeler market?

The cargo carrier segment is the fastest-growing by vehicle type, expanding at a 28.10% CAGR through 2031.

How are Battery-as-a-Service models influencing adoption?

BaaS lowers up-front costs by 35–40%, aligns energy payments with vehicle usage, and attracts both fleet operators and individual drivers.

Which battery chemistry is gaining momentum?

Lithium iron phosphate (LFP) batteries are the fastest-growing battery type in the Indian electric rickshaw market, with a 37.10% CAGR.

What policy changes are most impactful?

The extension of federal incentives under EMPS 2024 and Delhi’s mandate to retire ICE three-wheelers by 2025 are two pivotal regulatory drivers.

Which state currently leads in electric three-wheeler sales?

Uttar Pradesh leads with 37.80% of national sales in 2025, supported by strong policy incentives and high urban ridership.

Page last updated on: