Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

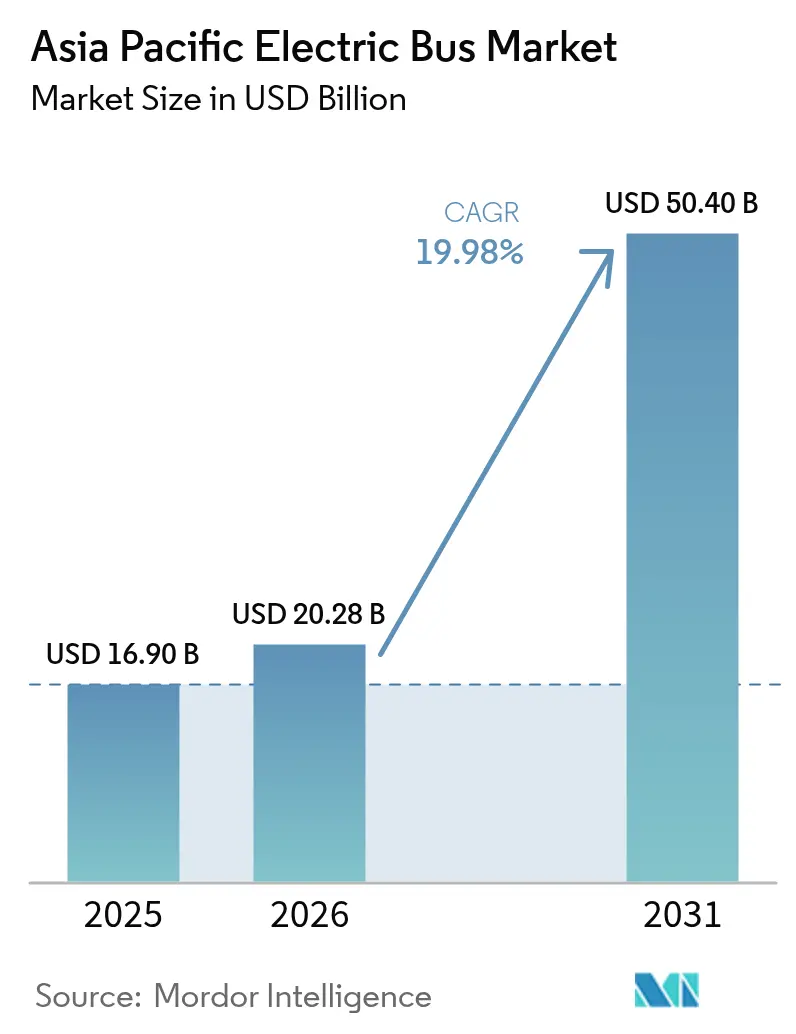

| Base Year Market Size (2025) | USD 16.90 Billion |

| Market Size (2026) | USD 20.28 Billion |

| Market Size (2031) | USD 50.4 Billion |

| Growth Rate (2026 - 2031) | 19.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Electric Bus Market Analysis by Mordor Intelligence

The Asia Pacific electric bus market size was valued at USD 16.90 billion in 2025 and estimated to grow from USD 20.28 billion in 2026 to reach USD 50.4 billion by 2031, at a CAGR of 19.98% during the forecast period (2026-2031). Falling lithium-iron-phosphate battery prices, synchronized subsidy cycles in China and India, and expanding hydrogen corridors in Japan and South Korea work together to compress the total cost of ownership, stimulate bulk orders, and diversify propulsion choices. Manufacturing scale is rising just as depot-charging software trims grid-upgrade costs, allowing tier-2 and tier-3 cities to enter procurement pipelines. National zero-emission fleet mandates add regulatory certainty that unlocks green-bond financing, while local-content policies encourage ASEAN assembly hubs and create cross-border supply-chain opportunities. As a result, the Asia Pacific electric bus market is moving toward balanced growth across public and private fleets, urban and inter-city routes, and mid-size and high-capacity vehicle classes.

Key Report Takeaways

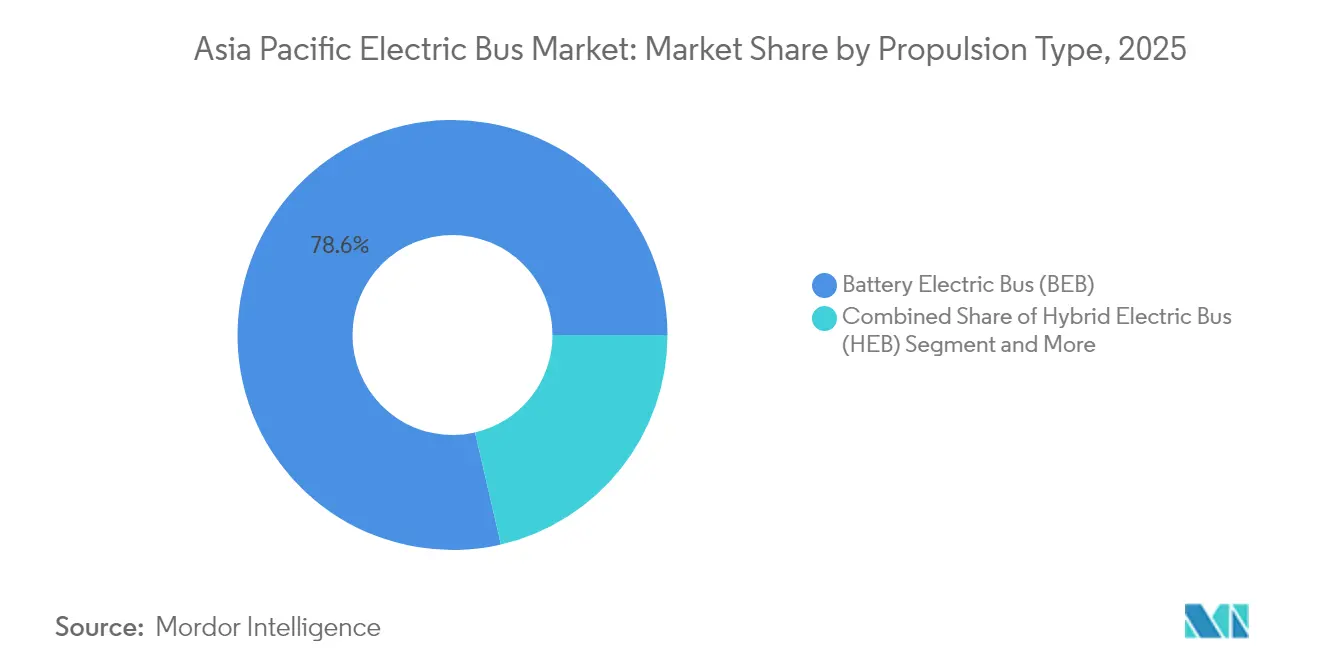

- By propulsion type, battery electric buses led with 78.62% of the Asia Pacific electric bus market share in 2025, while fuel-cell electric buses recorded the highest 27.88% CAGR projected through 2031.

- By bus length, the 9–14 meter class accounted for 56.71% of the Asia Pacific electric bus market size in 2025; buses longer than 14 meters are forecast to expand at 21.65% CAGR to 2031.

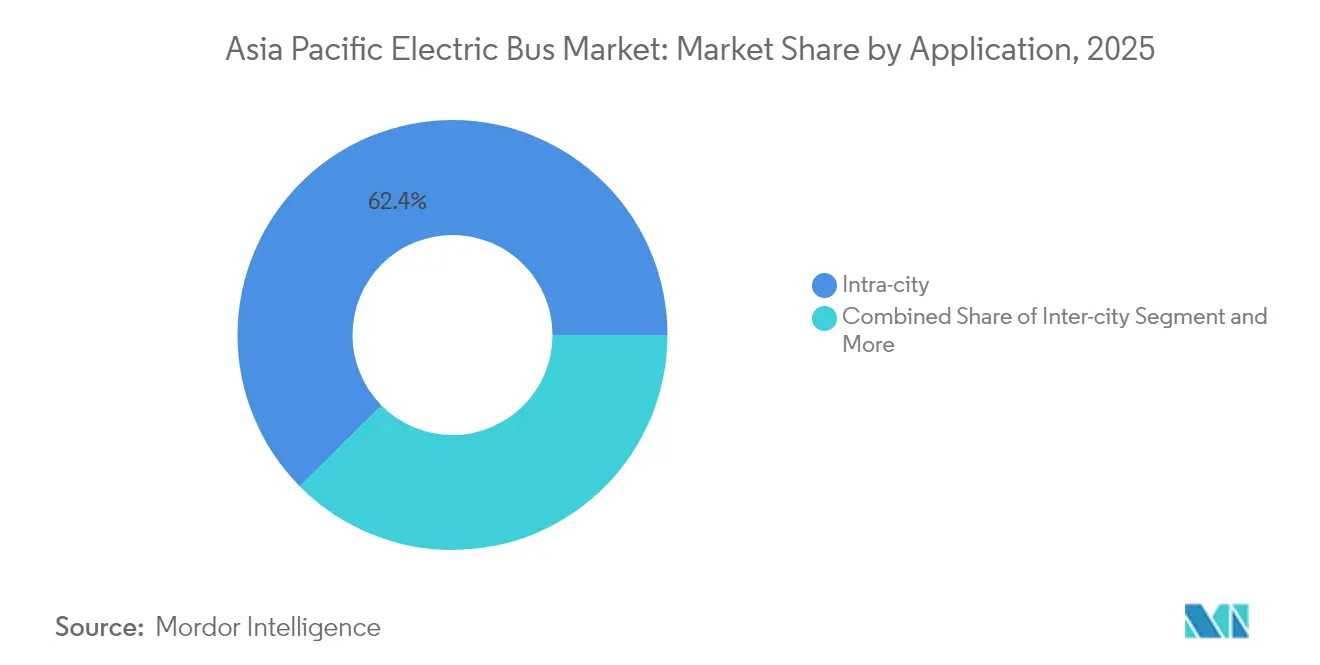

- By application, intra-city service held 62.44% of the Asia Pacific electric bus market share in 2025, whereas inter-city routes are poised for 20.92% CAGR growth through 2031.

- By end user, public transport authorities controlled 71.86% of the Asia Pacific electric bus market revenue in 2025, but private fleet operators are advancing at a 22.03% CAGR over 2026-2031.

- By country, China retained 77.25% of the Asia Pacific electric bus market share in 2025, and Japan is projected to post the fastest 46.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Electric Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream Purchase-Subsidy Renewal | +4.2% | China, India, spillover to ASEAN | Medium term (2–4 years) |

| Lithium Iron Phosphate (LFP) Battery Packs Below USD 100 kWh | +3.8% | Cost-sensitive ASEAN markets | Short term (≤ 2 years) |

| Zero-Emission Fleet Mandates | +2.9% | Singapore, South Korea, Japan, select Indian states | Long term (≥ 4 years) |

| Transit-Agency Green-Bond Financing | +2.1% | Urban centers across Asia Pacific | Medium term (2–4 years) |

| Depot-Charging Load-Management Software | +1.7% | Tier-1 cities first, then tier-2/3 | Short term (≤ 2 years) |

| Incentives for ASEAN Hubs | +1.4% | Thailand, Indonesia, Malaysia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream Purchase-Subsidy Renewal Waves in China and India

Synchronizing subsidy extensions has generated steady backlog-driven demand that justifies large production runs and tightens component supply contracts. Beijing’s bus incentive with 70% local-content rules protects domestic suppliers, while India’s INR 5,500 crore (USD 660 million) allocation channels state tenders into multi-year fleet plans. Manufacturers secured a significant number of orders within weeks of both programs’ renewal, locking in factory utilization rates and advancing cost parity against diesel fleets without perpetual fiscal support.

Falling LFP Battery-Pack Prices Below USD 100 kWh Enabling TCO Parity

In 2024, lithium-iron-phosphate (LFP) pack prices experienced a significant decline, driven by the increased production capacity of Chinese plants. This milestone allowed manufacturers to distribute fixed costs over larger volumes, making the technology more cost-effective. The reduced costs have notably shortened payback periods for standard urban routes, making electric vehicle purchases more financially viable even without subsidies. Additionally, improved cost predictability has enabled leasing firms to offer mileage-indexed contracts, mitigating battery-performance risks for financially constrained agencies. Southeast Asian buyers are expected to benefit the most from this development.

National Zero-Emission Fleet Mandates (e.g., Singapore 2040, S-Korea 2030)

Binding fleet mandates are driving long-term procurement schedules and infrastructure developments. Singapore aims for a cleaner energy public bus fleet by 2040, focusing on electric and hybrid buses, backed by substantial funding for vehicles and chargers. South Korea aspires to have 21,200 hydrogen buses operational by 2030, while Japan plans to roll out 1,200 fuel-cell units by the same year. These ambitious targets create sustained demand, prompting manufacturers to establish localized assembly lines, ensuring parts availability and minimizing warranty risks.

Dedicated Green-Bond Financing Models for Transit Agencies

In 2024, green bonds designated for bus electrification in the Asia Pacific gained significant traction, offering coupon rates notably lower than conventional municipal debt. These reduced borrowing costs empower agencies to expedite procurement timelines, facilitating smoother fleet-replacement cycles and allowing them to secure commodity prices ahead of potential fluctuations in battery-metal prices. Investors driven by ESG principles are willing to accept narrower yields, valuing the assurance of audited emissions-reduction metrics. Furthermore, many bond issues incorporate step-up clauses, imposing penalties for non-compliance, thereby ensuring adherence to operational commitments. In a bid to fast-track its sustainability goals, Seoul successfully raised funds at a competitive rate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal Balance-Sheet Constraints | −2.8% | Urban centers in India and ASEAN | Short term (≤ 2 years) |

| Sub-MW Depot-Connection Bottlenecks | −2.1% | Secondary cities in India, Indonesia, Philippines, Vietnam | Medium term (2–4 years) |

| Excess Battery-Cell Capacity | −1.6% | Chinese supply chain | Short term (≤ 2 years) |

| Range Anxiety on Hilly Routes | −1.3% | Mountainous regions across Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Municipal Balance-Sheet Constraints After Pandemic Fare Losses

Municipal ledgers are struggling with significant revenue shortfalls compared to pre-pandemic levels, creating challenges for financial stability. These ongoing gaps are restricting access to credit lines and delaying fleet-replacement tenders, which would otherwise prioritize the adoption of electric buses. In Mumbai, BEST is facing considerable financial losses, which have forced a substantial reduction in its procurement plans, even though there is clear evidence of potential savings in operating costs. Similarly, Bangkok’s transit agency has been compelled to make similar cutbacks, citing financial deficits stemming from the pandemic that have limited its ability to secure additional borrowing.

Sub-MW Depot Connection Bottlenecks in Tier-2/3 Indian and ASEAN Cities

Operators face challenges in managing their fleets due to limitations in electrical feeds, which restrict the number of buses that can be charged simultaneously. This constraint forces fleets to be distributed across multiple yards, creating complexities in maintenance schedules and route dispatching. In Indore, the bus program is divided among several depots, resulting in inefficiencies such as increased driver travel without passengers and higher operational costs per kilometer. Similarly, cities in Indonesia encounter prolonged delays in upgrading their distribution grids, which hampers the progress of new tenders even when financial resources are available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEB Dominance Faces FCEB Challenge

Battery electric buses (BEBs) account for 78.62% of 2025 deliveries, offering proven depot-charging ecosystems that fit dense urban loops. This slice translates to the largest Asia Pacific electric bus market share, underscoring how LFP chemistry and low-floor chassis designs align with short-haul scheduling. High-power depot chargers, energy-price arbitrage, and shorter payback windows reinforce BEB economics. Yet the segment’s growth is decelerating compared with emerging fuel-cell electric buses, whose hydrogen refueling parity on inter-city routes is eroding BEB’s growth lead.

Fuel-cell electric buses notch a projected 27.88% CAGR by leveraging Japan and South Korea’s hydrogen roadmaps, which include 900 refueling stations by 2030 . Route modeling shows FCEBs outperform batteries on distance-weighted cost when daily mileage exceeds 400 km. OEMs now bundle hydrogen supply agreements into bus contracts, easing operator fears over price volatility. Meanwhile, hybrid and plug-in hybrid variants persist in Thailand and Malaysia, where phased electrification spreads capital cost over longer cycles.

By Bus Length: Mid-Size Optimization Drives Segment Leadership

The 9–14 meter class holds 56.71% of 2025 shipments, confirming its sweet spot for maneuverability, passenger density, and TCO. Its prominence also yields the largest Asia Pacific electric bus market size sub-segment, with repeat orders from Shanghai, Jakarta, and Delhi validating lifecycle economics. OEM platforms integrate 350-450 kWh packs under low-floor designs, keeping aisle layouts intact.

Buses above 14 meters are projected to expand 21.65% CAGR through 2031 as operators target driver labor savings and network consolidation. Double-deck and articulated formats address peak-hour crowding in Seoul and Hong Kong, while battery-swap variants are entering Taiwan’s coastal express lines. Sub-9-meter minibuses remain niche but gain traction in campus, airport, and feeder services.

By Application: Intra-City Dominance Challenged by Inter-City Growth

Intra-city routes commanded 62.44% of 2025 demand, reflecting high stop density and predictable duty cycles conducive to overnight depot charging. Cities like Shenzhen, which runs an all-electric fleet, demonstrate notable opex savings versus legacy diesel operations.

Inter-city adoption is projected to climb at a 20.92% CAGR. New 350 kW roadside chargers along China’s G60 and South Korea’s Seoul-Busan highways support 300-plus km range requirements that previously required diesel or CNG coaches. Private coach lines in Thailand and Vietnam are signing fixed-price electricity contracts that hedge fuel exposure, making inter-city electrification financially viable. Airport and school services continue moderate growth in line with terminal expansions and air-quality regulations.

By End-User: Public Authorities Lead While Private Operators Accelerate

Public agencies accounted for 71.86% of orders in 2025 because central subsidies flow mainly through municipal tenders, aligning fleets with national policy targets. Their scale enables depot-site aggregation, bulk electricity pricing, and training programs that reinforce early-stage market expansion.

Private Fleet Operators are rising at 22.03% CAGR, driven by corporate ESG pledges, ride-sharing integration, and employee-shuttle contracts. The Asia Pacific electric bus industry now sees tech-platform partners incorporating vehicle-to-grid services for additional revenue. Leased models, usage-based billing, and guaranteed-uptime warranties reduce capital barriers and open the market to logistics, tourism, and university sectors.

Geography Analysis

China maintained a 77.25% share in 2025, thanks to vertically integrated OEMs that fuse battery cells, vehicle assembly, and charging into turnkey offerings . Subsidies remain until 2025, but tapering now channels sales toward tier-2 and tier-3 cities, which account for a significant share of new bids.

India is also one of the largest markets by volume; FAME-II funds and state mandates secure multi-year tenders, yet grid upgrades lag. Maharashtra and Tamil Nadu enforce 100% electric procurement, while Surat and Kochi pilot battery-swap depots to offset connection delays.

Japan posts a 46.85% CAGR forecast, propelled by national hydrogen policy, planned refueling stations, and premium pricing accepted by prefectural transit agencies. South Korea follows suit under its Green New Deal, targeting a significant number of hydrogen-powered buses by 2030, backed by low-coupon green bonds. ASEAN markets vary: Thailand’s 60% local-content rule spurs new assembly plants, Indonesia ties bus targets to nickel-based battery value chains, and Singapore’s city-state coordination accelerates 2040 fleet electrification despite higher costs.

Regulatory Landscape

Across Asia Pacific, electric-bus adoption is being shaped by purchase incentives, fleet mandates, and tighter local-content requirements that affect sourcing and assembly decisions. In India, the Ministry of Heavy Industries is amending the Phased Manufacturing Program (PMP) requirements to mandate domestic manufacturing of traction motors and transmissions for M2 and M3 electric buses effective September 1, 2026, extending localization beyond final assembly.

In China, regulators and ministries have coordinated technical standardization to support faster deployment and interoperability, including GB/T 40032-2021 related to battery swapping and its infrastructure. UNECE R100 is referenced as a harmonized safety framework for battery systems, while national e-mobility strategies provide longer-dated policy anchors, including China aiming for full electrification of public service vehicles by 2035 and country-level targets and roadmaps in Japan, South Korea, and Singapore that influence procurement schedules and charging or hydrogen refueling buildouts.

Value Chain Analysis

The value chain is anchored on upstream battery materials and cells, then packs, e-axles or traction motors and power electronics, vehicle integration, charging or hydrogen refueling equipment, and finally fleet operations and lifecycle services. China-based OEMs such as BYD, Yutong, and Foton AUV operate integrated models that bundle vehicles with batteries and charging, and they support cross-border fulfillment through export logistics and port shipments (for example, deliveries routed through Yantai Port), which helps shorten lead times for overseas operators.

Downstream, the market is increasingly service-led, covering depot energy management, training, spares, and uptime guarantees. OEMs and partners are expanding localized support footprints, including resident engineering teams and after-sales service setups in South Asian markets (notably by BAIC Foton AUV). Distributor-led models also extend reach into smaller procurement lots, including Yutong electric buses distributed in the UK via Pelican Bus and Coach, which supports municipal council procurements. On supply risk, India is pursuing resilience through programs such as the India Semiconductor Mission and the National Critical Mineral Mission, aimed at reducing exposure to single-source dependencies for components and inputs relevant to batteries and motors.

Competitive Landscape

Market concentration is moderate. BYD and Yutong together hold a notable share of regional volume, underpinned by LFP vertical integration and aggressive overseas assembly rollouts. Hyundai, Tata Motors, and VinFast build local partnerships to comply with content regulations and tap untapped segments such as airport ground support.

Technology is the key differentiator. Chinese firms anchor on LFP cost leadership, Japanese incumbents refine fuel-cell stacks, and European entrants emphasize fleet-management software that integrates predictive maintenance with charging orchestration. Patent filings increasingly center on thermal management, silicon-carbide inverters, and artificial-intelligence route planning.

Strategic moves in 2025 include BYD’s autonomous Level 4 pilot in Singapore, Yutong’s launch of a 12-meter double-deck BEB, and Hyundai’s first commercial delivery to a Japanese operator [3]“Yutong debuts U12DD,” Yutong Bus Co., yutong.com. Start-ups such as Gogoro explore battery-swap buses aimed at dense Southeast Asian corridors, while Ola Electric tests direct-to-operator sales that bypass traditional distributor layers.

Asia Pacific Electric Bus Industry Leaders

BYD Company Ltd.

Zhengzhou Yutong Bus Co., Ltd.

Beijing Foton AUV Bus Co., Ltd.

Xiamen King Long Motor Group Co., Ltd.

Tata Motors Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, program-driven procurement pipelines across Asia support near-term whitespace for OEMs, integrators, and financing partners, especially where tenders bundle vehicles with charging, depot upgrades, and service guarantees. Regional roadmaps cited by multilateral and industry bodies point to sizable planned deployments through 2030, and India has articulated a tendering ambition of around 40,000 electric buses by FY30, which elevates demand for localized drivetrain components, depot connection solutions, and fleet-availability service models.

Grid-aware operating models are creating new lanes for software and energy services as agencies look to expand fleets without proportional increases in grid-capex. Vehicle-to-grid (V2G) pilot programs in Japan and South Korea that incorporate electric buses as distributed storage strengthen the case for charging orchestration, demand-response participation, and energy-as-a-service contracting. At the same time, India’s PMP localization for traction motors and transmissions from September 2026 reinforces opportunities for regional suppliers to scale e-drive manufacturing, while pushing OEMs to deepen local partnerships to improve compliance and lifecycle support.

Recent Industry Developments

- July 2026: BYD reached a manufacturing milestone of 17 million new energy vehicles (NEVs). The achievement highlights sustained scale in BEV output and reinforces BYD's leadership in global electric mobility. It also strengthens supply-chain leverage for Asia-Pacific buyers, as production efficiencies support competitive pricing and faster deployment.

- June 2026: BYD announced plans to expand its bus battery production line in Brazil. The expansion increases regional manufacturing capacity and aligns with local content intentions, with potential to reduce logistics costs for Asia-Pacific buyers and expand export opportunities from the Americas.

- June 2026: Mega Motor Company, BYD’s official partner in Pakistan, delivered an additional fleet of BYD electric vehicles to Islamabad Capital Police and Islamabad Traffic Police. The delivery points to growing overseas fleet procurement and local market penetration, indicating broader scope for Asia-Pacific police and municipal fleet adoption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia-Pacific electric bus market includes electric buses used to move passengers, and it is measured in market value based on sales into transit agencies and fleet operators across APAC.

Scope exclusions: We exclude private passenger cars, electric trucks, and charging infrastructure revenues, unless they are bundled within the electric bus transaction value.

Segmentation Overview

- By Propulsion Type

- Battery Electric Bus (BEB)

- Hybrid Electric Bus (HEB)

- Plug-in Hybrid Electric Bus (PHEB)

- Fuel-Cell Electric Bus (FCEB)

- By Bus Length

- Below 9 M

- 9 - 14 M

- Above 14 M

- By Application

- Inter-city

- Intra-city

- Airport Shuttle

- School Transport

- By End-User

- Public Transport Authorities

- Private Fleet Operators

- By Country

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first draft of the demand picture, and to set clear guardrails around what counts as an electric bus sale in APAC. We relied on public sources such as national transport and statistics ministries, customs and trade statistics portals, and city transit authority procurement releases that indicate planned and delivered bus volumes.

To keep assumptions realistic, we also reviewed sources such as IEA EV outlook style publications, UNECE transport and vehicle standards references, and academic papers that discuss battery chemistries and duty cycles for buses. Company annual reports, investor presentations, and reputable press coverage helped us understand production plans, tender pipelines, and price direction. In a few places, paid subscriptions for company financials and intelligence, shipment level import and export records, and global tenders were used only to verify totals and timing. The sources listed here are not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what is actually being procured and delivered, since policy targets can look larger than real deployments. We spoke with a mix of bus OEM and component-side participants, transit buyers, depot and fleet managers, and industry experts across the major APAC markets so assumptions on volumes, pricing, and technology mix could be corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | |

| Mid tier: 57% | Functional/Unit leaders: 37% | |

| Smaller Players: 16% | Managers: 48% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs value from APAC electric bus unit demand signals, which are then converted into market value using country-level price ranges and mix splits. What made the model practical was that, once public procurement plans, subsidy programs, and delivery announcements were organized by country, the total demand pool became visible and could be stress-tested.

We then cross-checked the totals with selective bottom-up approximations, including sampled average selling price (ASP) by bus length class, a rollout of expected deliveries from disclosed production and tender pipelines, and channel checks on typical order sizes for public transit operators. Key inputs used in the model include annual electric bus registrations or deliveries where available, fleet replacement cycles for urban buses, tender award volumes and delivery schedules, battery chemistry mix shifts (such as LFP share), and ASP movement tied to battery pack cost direction. For forecasting, scenario analysis was applied to handle policy intensity and funding timing, and expert feedback was used to choose realistic adoption curves by country. When bottom-up checks had gaps, we used conservative ranges and only scaled totals when at least two independent signals supported the adjustment.

Data Validation & Update Cycle

Validation was done through triangulation across procurement volumes, delivery or registration signals, and implied ASP bands, before results were locked. We also ran variance checks by country and by application so one large market did not distort the regional total, and any unusual jump in implied pricing or unit growth was reviewed again.

Before sign-off, the model goes through multiple analyst reviews, and assumptions are re-checked with respondents when a new tender wave, subsidy change, or supply constraint creates a meaningful shift. Reports are refreshed annually, and interim updates are made when major policy or volume events occur. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Asia Pacific Electric Bus Market Sizing Compared With Other Published Estimates

Published market sizes for APAC electric buses can look far apart, mainly because each publisher counts a slightly different revenue pool and uses different timing for volumes and pricing. Differences also show up when one estimate leans heavily on policy targets, while another stays closer to delivered units and confirmed orders.

By tracking delivered and awarded volumes country by country and refreshing ASP bands with tender outcomes and inflation checks, Mordor Intelligence keeps the APAC electric bus value tied to bus sales, instead of mixing in charging infrastructure or wider electric commercial vehicle revenues. The spread in published numbers is also affected by whether plug-in hybrids and fuel-cell buses are included, how currency conversion timing is handled, and how quickly assumptions are updated after subsidy changes or big city tenders.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.90 B (2025) | |

| Industry Publisher A | USD 48.48 B (2025) | This estimate appears to align with a broader revenue interpretation that may include adjacent value pools discussed alongside buses (such as charging equipment and major drivetrain components) and may apply higher blended ASPs across markets. |

| Regional Research House B | USD 43.00 B (2023) | The figure is presented with a different base year and is likely closer to a deployment and policy-led snapshot, where procurement intent and earlier-year volume peaks can raise the stated value versus a delivered-sales view. |

The table shows that scope boundaries and pricing logic are usually the biggest drivers of the gap, even before growth assumptions are discussed. When we keep the model anchored to observable tenders, deliveries, and realistic ASP ranges by market, the result is a market size that can be explained step by step and updated in a repeatable way.

Key Questions Answered in the Report

How fast is electrification advancing among Asia Pacific public bus fleets?

Fleet electrification is expanding at a 19.98% CAGR, supported by subsidies, battery-price declines, and national zero-emission mandates.

Which propulsion format is growing quickest?

Fuel-Cell Electric Buses lead growth at 27.88% CAGR thanks to hydrogen investments in Japan and South Korea.

Why do mid-size buses dominate orders?

The 9–14 meter class balances passenger capacity and street maneuverability, capturing 56.71% of 2025 shipments.

What financing tools help cities afford new buses?

Green bonds with coupons and energy-as-a-service contracts lower up-front costs and smooth cash flows for agencies.

Page last updated on: