Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

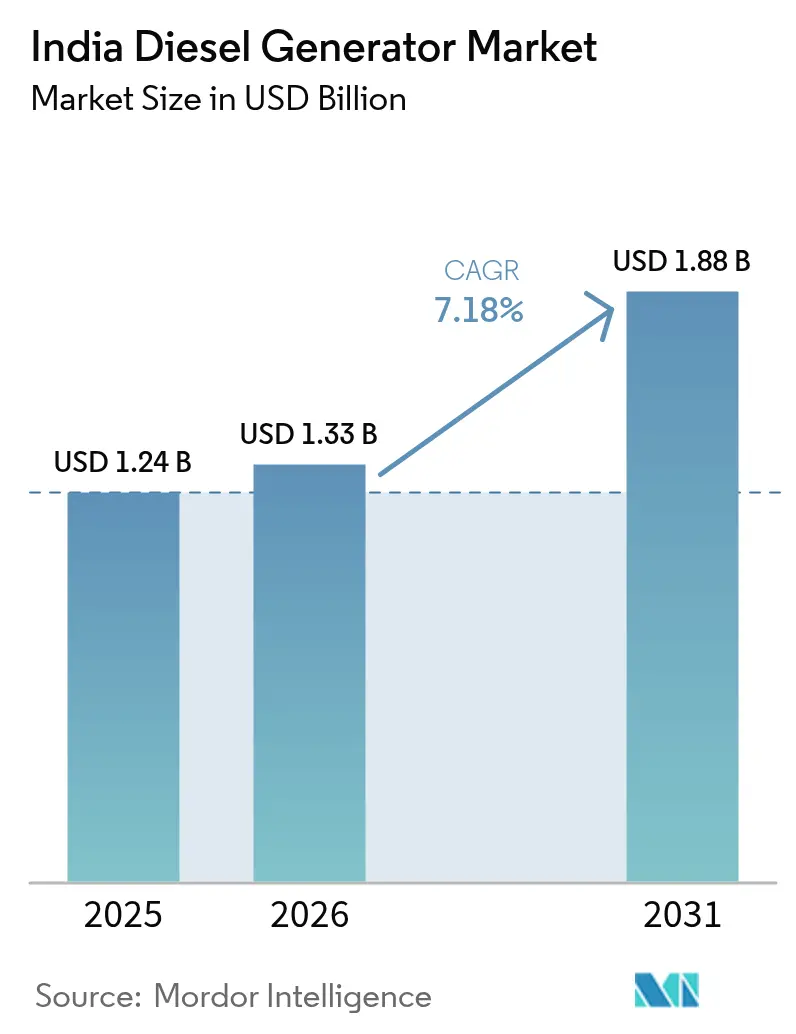

| Base Year Market Size (2025) | USD 1.24 Billion |

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

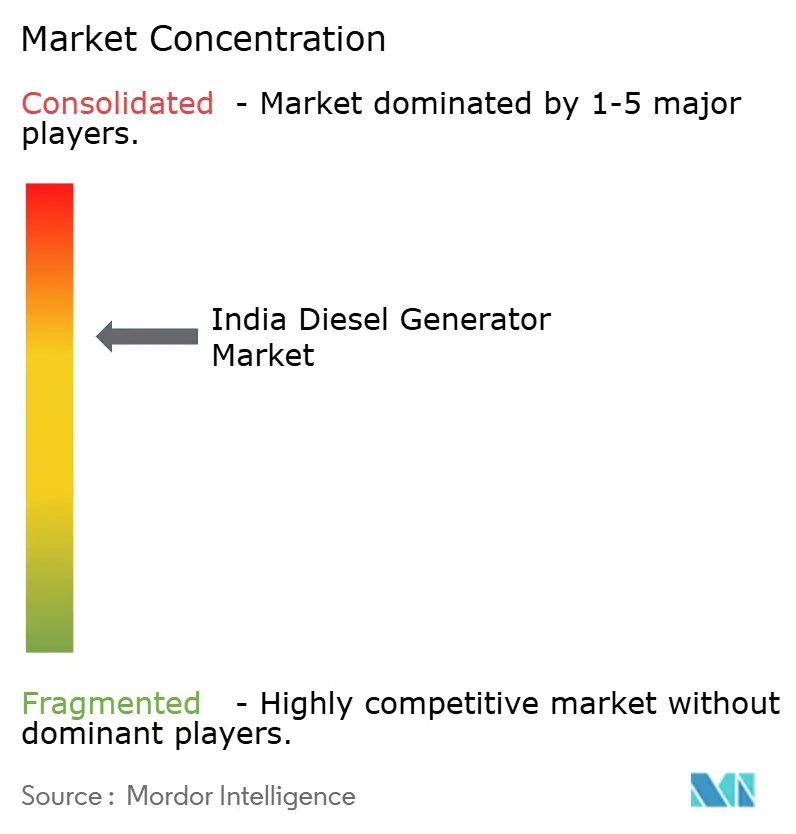

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Diesel Generator Market Analysis by Mordor Intelligence

The India Diesel Generator Market size was valued at USD 1.24 billion in 2025 and estimated to grow from USD 1.33 billion in 2026 to reach USD 1.88 billion by 2031, at a CAGR of 7.18% during the forecast period (2026-2031).

Growth persists even as the national energy-deficit metric has nearly disappeared, because voltage fluctuations and localized outages continue to interrupt commerce in Tier-II and Tier-III cities.(1)LocalCircles, “Tier-II/III Power Outage Survey,” LOCALCIRCLES.COM The infrastructure super-cycle further underpins demand, the rapid scale-up of hyperscale data-center facilities, and leasing models that shift gensets from capex to opex for small businesses. Regulatory tightening under CPCB IV+ has triggered a premiumization wave that favors OEMs with certified emission-control technologies. At the same time, rooftop solar paired with battery storage has begun to erode use-cases in grid-connected residences, although prime-power applications in construction sites, telecom towers, and remote industrial assets continue to rely on diesel for multi-hour autonomy.(2)Ministry of New and Renewable Energy, “PM Surya Ghar Muft Bijli Yojana Progress,” MNRE.GOV.IN

Key Report Takeaways

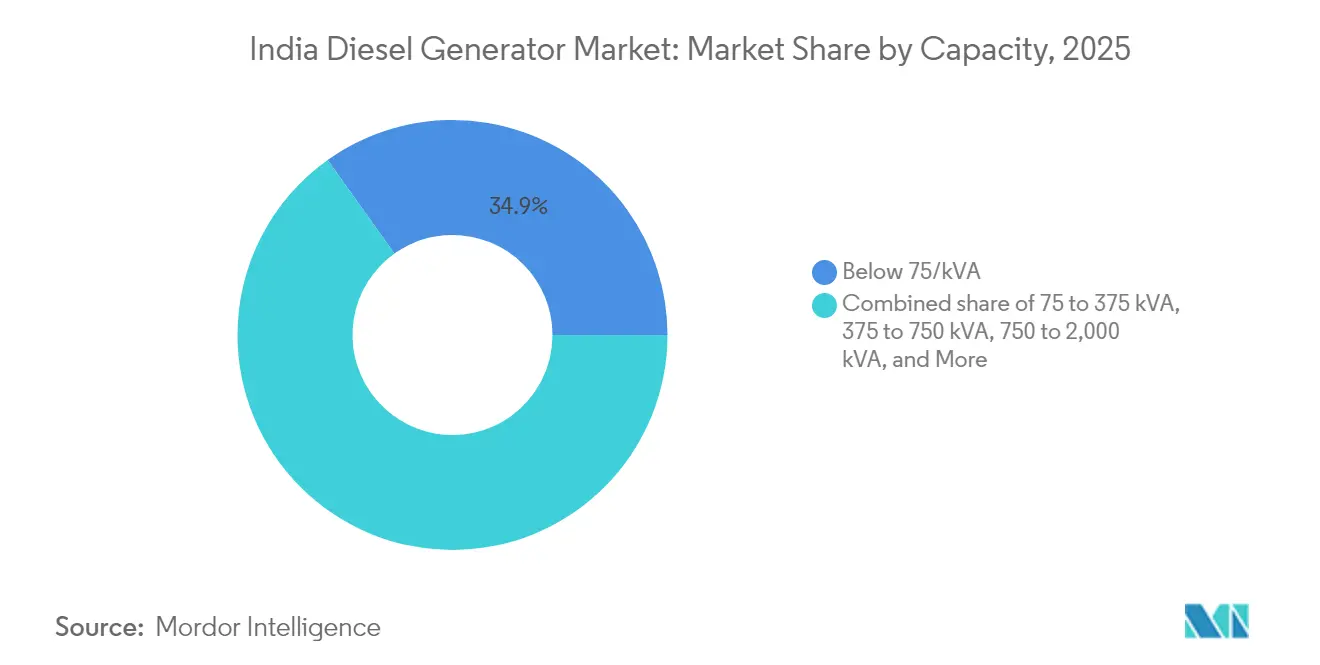

- By capacity, units below 75 kVA led with 34.86% of India's diesel generator market share in 2025; the 375 to 750 kVA bracket is forecast to expand at an 8.75% CAGR through 2031.

- By application, standby/backup accounted for 60.25% of the Indian diesel generator market size in 2025, while prime/continuous power is expected to accelerate at an 8.17% CAGR through 2031.

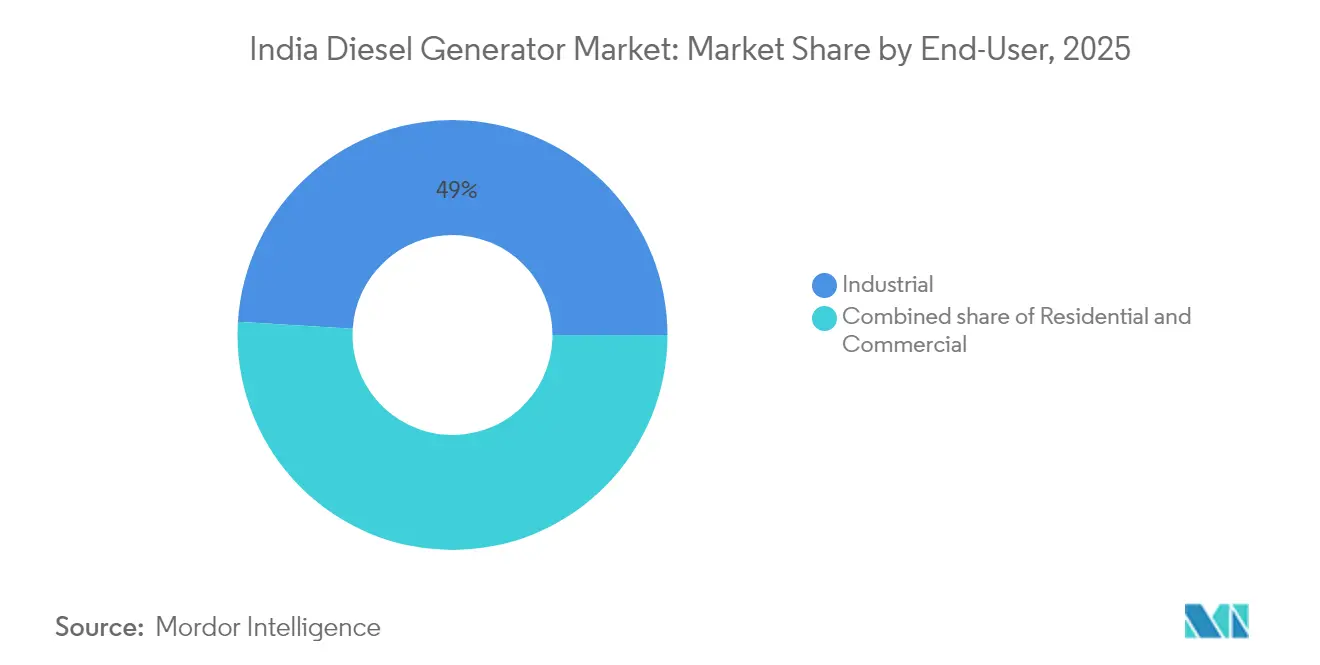

- By end user, industrial sites held a 49.02% share in 2025; residential demand is growing at the fastest rate, with a 8.98% CAGR to 2031.

- Cummins India, Kirloskar Oil Engines, Caterpillar, Mahindra Powerol, and Greaves Cotton collectively commanded about 55%–60% of organized revenue in 2024, highlighting a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising power outages in Tier-II & Tier-III cities | +1.8% | Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan | Short term (≤ 2 years) |

| Infrastructure boom in construction & real estate | +2.1% | Mumbai, Bengaluru, NCR, Hyderabad | Medium term (2-4 years) |

| Telecom-tower proliferation in rural India | +0.9% | Northeast and Central clusters | Medium term (2-4 years) |

| Advancements in generator efficiency & remote monitoring | +0.7% | Metros and Tier-I cities | Long term (≥ 4 years) |

| Mandatory backup for new data-center colocation facilities | +1.4% | Mumbai, Chennai, Hyderabad, NCR | Medium term (2-4 years) |

| Growth of genset-leasing models for MSMEs | +0.6% | Gujarat, Tamil Nadu, Maharashtra | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Power Outages in Tier-II & Tier-III Cities

Localized reliability gaps keep the India diesel generator market indispensable outside the metros. A survey showed that 85% of households in smaller cities still suffer from 2- to 4-hour daily outages, despite the national deficit falling to 0.1%. Commercial chains, diagnostic labs, and cold-storage outlets cannot tolerate voltage sags, so gensets remain budgeted as core operating costs. The Revamped Distribution Sector Scheme allocates USD 36 billion for feeder and smart-meter upgrades; however, fiscally weaker states lag, perpetuating reliance on gensets.(3)Government of India, “Power Sector at a Glance,” POWERMIN.GOV.IN Even after average urban supply improved to 23.4 hours, the residual downtime often coincides with evening peaks, prompting buyers to size units for full-load duty. Consequently, sets below 75 kVA continue to rotate on a five- to seven-year replacement cycle across Tier II and Tier III clusters.

Infrastructure Boom in Construction & Real Estate

India's construction sector, valued at USD 1.4 trillion, now accounts for approximately 9% of the country's GDP and employs around 71 million workers. Government capex of USD 134 billion in FY25 under the PM Gati Shakti plan channels funds into expressways, metros, airports, and industrial corridors. Early-stage civil works are powered by rented 375 to 750 kVA generators because distribution connections are not available until structural milestones are reached. Real growth of 13.3% year-over-year in Q3 2023 and 80 million tonnes of new cement capacity signal a multi-year surge in power demand. Flagship projects such as the Delhi-Mumbai Industrial Corridor or GIFT City each require multi-megawatt standby fleets for cranes, pumps, and welders. The rollout of affordable housing under PM Awas Yojana across peri-urban zones adds further depth to mid-range genset demand.

Telecom-Tower Proliferation in Rural India

India operates more than 0.71 million telecom towers, and diesel still accounts for roughly one-third of the operating energy costs at these sites.(4)Department of Telecommunications, “5G Infrastructure Rollout,” DOT.GOV.IN Rollout of 5G triples per-tower energy draw, amplifying the need for reliable prime power where grid extension is uneconomical. Hybrid solar-battery pilots cut fuel consumption but cannot yet deliver the multi-day autonomy required during monsoon months. Demand therefore concentrates in the 75 to 375 kVA band, sustaining off-grid supply chains for DEF, spare filters, and remote-monitoring modules. OEMs that bundle IoT telematics with service contracts enjoy higher renewal rates as tower companies prioritize uptime SLAs.

Advancements in Generator Efficiency & Remote Monitoring

OEMs have upgraded engines with electronic fuel-injection, SCR systems, and diesel particulate filters to meet CPCB IV+. These technologies reduce NOx and PM emissions by approximately 90% while reducing fuel consumption by 3% to 5%.(5)Greaves Cotton, “CPCB IV+ Range Launch,” GREAVESCOTTON.COM IoT gateways stream runtime data to cloud dashboards, enabling predictive maintenance that minimizes unplanned stoppages. Early adopters include metro-based data centers and hospitals that face steep penalties for failure. Over the long term, connected gensets will migrate to mid-tier cities as component prices fall, anchoring after-sales revenue for leading OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of rooftop solar + storage systems | -1.2% | National, strongest in Gujarat, Rajasthan, Karnataka, Maharashtra | Medium term (2-4 years) |

| Stricter CPCB IV+ emission norms inflating capex | -0.9% | National, enforcement concentrated in Delhi NCR, Mumbai, Bengaluru | Short term (≤ 2 years) |

| NBFC credit-tightening limiting contractor purchases | -0.6% | National, most acute in construction hubs Gujarat, Maharashtra, Tamil Nadu, NCR | Short term (≤ 2 years) |

| Diesel-supply disruptions during festival/election seasons | -0.4% | National, with periodic spikes in states with weak logistics infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Rooftop Solar + Storage Systems

Residential rooftop installations reached 3.2 GW by March 2024, and the PM Surya Ghar Muft Bijli Yojana added another 1.8 GW in six months through simplified approvals and capital subsidies. Commercial users have deployed roughly 4 GW, increasingly paired with battery storage, as tariffs for stand-alone BESS fell through the viability gap due to funding. Storage tenders totaling 6.1 GW in Q1 2025 reveal that utilities view batteries as an economic substitute for peaking diesel fleets. Telecom operators now run photovoltaic hybrids at select towers, slashing CO₂ output by up to 58%. These trends compress demand in grid-connected light-commercial and residential segments, although off-grid prime-power niches remain protected by renewable intermittency.

Stricter CPCB IV+ Emission Norms Inflating Capex

The CPCB IV+ framework, which has been in force since July 2024, requires SCR, DPF, and advanced injectors, resulting in factory prices increasing by 15% to 20% and total life-cycle costs rising by up to 18%. Delhi NCR imposes additional rules, including seasonal bans and 3-meter stack heights, which increase installation complexity. Smaller assemblers that once served the below 75 kVA niche struggle to absorb R&D expenses, accelerating consolidation. NBFC lending standards have also tightened for construction borrowers, slowing replacement cycles among price-sensitive buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity (kVA): Mid-Range Units Gain as Data Centers Scale

The 375–750 kVA class is projected to grow at an annual rate of 8.75% to 2031, significantly outpacing the 7.18% baseline, as colocation halls and large construction sites increasingly favor units that can parallel seamlessly for N+1 redundancy. Below 75 kVA sets still command 34.86% of India's diesel generator market share, anchored in gated communities and corner stores across Tier-II cities, yet rooftop solar cuts into fresh installations. The 75 to 375 kVA range services mid-sized factories, retail chains, and hospitals that must replace aging fleets with CPCB IV+ models, as pre-2024 units reach the end of their life. Larger machines, with capacities of 750 to 2,000 kVA, supply manufacturing plants, mining sites, and public-sector utilities that require multi-megawatt clusters. Premiumization is most visible in mid-range orders, where buyers request IoT-enabled monitoring, five-year warranties, and expedited spare parts fulfillment. Kirloskar Oil Engines has responded by bundling fuel-agnostic engines and cloud dashboards that reduce unplanned downtime, thereby cementing its hold on high-value accounts.

A second driver for mid-range uptake is the mandatory backup requirement embedded in several state data-center policies. Each 1 MW of IT load requires up to 1.5 MW of standby diesel, resulting in clusters of synchronized 500 to 750 kVA units rated for a 10-second black-start capability. Cummins reported a 30.8% revenue surge in Q2 FY25, driven by such orders, a segment that was negligible three years ago. OEMs with proven SCR and DPF service capacity thus command healthy price premiums. Smaller assemblers, meanwhile, face margin compression as buyers pivot to warranty-rich branded sets. The India diesel generator market consequently tilts toward organized players within the 375 to 750 kVA sweet spot, even as the sub-75 kVA category maintains a broad but low-margin installed base.

By Application: Prime Power Gains as Off-Grid Projects Proliferate

Standby duty still dominates, representing 60.25% of the India diesel generator market size in 2025, because most urban facilities keep gensets as insurance rather than daily workhorses. Yet prime or continuous power applications are expanding at an 8.17% CAGR, led by telecom towers in rural corridors and construction projects where grid extension remains financially unviable. India’s 0.71 million tower fleet increasingly requires dual-fuel or hybrid configurations, but diesel remains the backbone during extended monsoon cloud cover. Peak-shaving roles are limited to large industrial subscribers facing punitive time-of-day tariffs; however, falling BESS pricing poses a future risk to this niche. Data centers fall under standby classification, but their monthly full-load tests and grid-maintenance runs push annual hours closer to prime territory, shortening replacement intervals to roughly eight years. OEMs now capture service revenue by offering contracts tied to run-hour thresholds rather than calendar years, a model that aligns with the high-utilization realities of data-center clusters.

By End User: Residential Surges as Affluence Spreads

Industrial plants held a 49.02% share in 2025, covering process industries, warehouses, and fabrication lines that cannot afford unscheduled downtime. Residential demand, however, is rising at the fastest rate, with a 8.98% CAGR, as middle-class households in states such as Uttar Pradesh and Bihar view gensets as essential infrastructure. Gated complexes require backup for elevators, pumps, and security, resulting in a brisk turnover of portable units. Commercial establishments—hotels, retail chains, and diagnostic labs—have upgraded their fleets to CPCB IV+ models with 24/7 service contracts, tilting market economics in favor of Cummins, Greaves Cotton, and Kirloskar. Industrial buyers are experimenting with biodiesel blends and gas-conversion kits to hedge against future carbon pricing, although adoption is currently limited to large corporations with dedicated ESG budgets. Residential substitution risk from rooftop solar is mitigated by the high upfront cost of battery packs, which can power a typical 3–5 kW home load for four hours. Consequently, the India diesel generator market continues to serve as a bridge technology for middle-income consumers until storage prices fall materially.

Geography Analysis

Regional demand correlates inversely with grid reliability and directly with economic activity. Tier-II and Tier-III cities across Uttar Pradesh, Bihar, Madhya Pradesh, and Rajasthan remain heavy adopters because households still face 2- to 4-hour outages despite national figures showing near-zero deficit. Metro clusters, including Mumbai, Bengaluru, Chennai, Hyderabad, and NCR, anchor data center and Class-A commercial requirements. Mumbai alone houses more than 50% of the current colocation power, while Chennai gains a share due to its proximity to subsea cable nodes. The India diesel generator market size tied to these metros grows in tandem with hyperscaler expansions, insulating OEM revenues from cyclical swings in manufacturing.

Industrial belts in Gujarat’s Vapi-Ankleshwar corridor, Tamil Nadu’s Coimbatore-Tiruppur textile hub, and Maharashtra’s Pune-Nashik auto cluster rely on gensets for peak-shaving and outage coverage. BESS pilots are emerging, but diesel remains the least-cost option for multi-hour autonomy. Rural Northeast and Central India see brisk telecom-tower buildout, driving steady orders in the 75–375 kVA class. Government infrastructure outlays of USD 134 billion for highways, metros, and industrial corridors further concentrate rentals along the Golden Quadrilateral and Delhi-Mumbai Expressway alignments.

Policy diversity adds complexity. Gujarat and Rajasthan offer net-metering incentives that accelerate the uptake of solar-plus-storage systems, thereby reducing diesel runtime for small businesses. By contrast, states with weaker fiscal capacity, such as Bihar and Jharkhand, lag in distribution upgrades, thereby locking in dependence on gensets. Delhi NCR’s anti-pollution edicts are pushing buyers toward CPCB IV+ compliance and hybrid architectures, a framework that is likely to spread to other metros over the next three years. Coastal states host export-oriented SEZs that require stringent uptime to meet delivery windows; land-locked interiors lean on cyclical construction activity for demand. Rural electrification gains have reduced genset usage in agriculture; however, cold-chain logistics for dairy and horticulture still require portable power during 2- to 11-hour supply gaps.

Competitive Landscape

The India diesel generator industry remains moderately concentrated. The top five players, Cummins India, Kirloskar Oil Engines, Caterpillar (FG Wilson), Mahindra Powerol, and Greaves Cotton, collectively hold a share of 55% to 60% of the organized revenue. Cummins leveraged its July 2024 CPCB IV+ rollout to secure high-capacity orders, resulting in a 30.8% revenue increase in Q2 FY25. Kirloskar targets USD 780 million in FY25 sales, driven by IoT-enabled Optiprime gensets and pilot hydrogen-fuel-cell solutions that hedge against the long-term decline of diesel. Greaves Cotton’s 5–2,250 kVA portfolio integrates SCR, DPF, and five-year warranties across 450 service outlets, capturing buyers who prize total cost of ownership.

Smaller assemblers face rising entry barriers because CPCB IV+ adds 15% to 20% to factory cost and requires embedded electronics. Many struggle to finance research and development (R&D) for proprietary emission controls, which can lead to market exits or acquisitions. Jakson Group has pivoted toward solar-plus-storage, marketing diesel sets as interim solutions while positioning for a BESS future. Leasing firms backed by private equity are consolidating the rental segment, leveraging fleet-utilization synergies and GST input-credit rules that favor operating expense (Opex) models. NBFC tightening for construction loans, however, constrains the ability of smaller contractors to refresh their fleets, widening the gap between organized lessors and fragmented owner-operators.

Technology differentiation intensifies as OEMs embed telematics, predictive analytics, and remote firmware updates. Clients now evaluate not just kilowatt pricing but uptime guarantees and compliance documentation. Brands with nationwide service trucks and spare-parts depots enjoy a widening moat. Consequently, competitive pressure revolves around after-sales contracts and financing bundles rather than headline engine specifications, a shift that entrenches incumbency advantages for the leading five manufacturers.

India Diesel Generator Industry Leaders

Kirloskar Oil Engines Ltd.

Mahindra Powerol Ltd.

Ashok Leyland Ltd.

Caterpillar Inc. (incl. FG Wilson)

Cummins India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ashok Leyland unveiled its SAATHI platform at the Bharat Mobility Global Expo 2025, integrating CPCB IV+ gensets with predictive maintenance software that reduces unplanned downtime for construction and logistics fleets.

- July 2024: Greaves Cotton launched a CPCB IV+-compliant 5–2,250 kVA range featuring SCR and DPF technology, supported by a five-year warranty and a 450-point service network.

- July 2024: Cummins India introduced CPCB IV+ gensets, up to 800 kVA, with OptiNAS+ filtration, and reported a 30.8% revenue growth in Q2 FY25, driven by data-center demand.

- May 2024: Jakson Group rolled out CPCB IV+ gensets across Uttarakhand while partnering with Cummins to co-market solar-plus-storage hybrids.

India Diesel Generator Market Report Scope

A diesel generator is a device that combines a diesel engine and an electric generator to generate electricity. This is an example of an engine generator. A diesel compression-ignition engine is typically designed to run on diesel fuel, but specific models are also capable of running on other liquid fuels or natural gas.

Power ratings, end-user, and application segments of the Indian diesel generator market. By power rating, the market is segmented into below 75 kVA, 75-350 kVA, and above 350 kVA. By end-user, the market is segmented into residential, commercial, and industrial. By application, the market is segmented into Standby Backup Power, Prime/Continuous Power, and Peak Shaving Power. The market sizing and forecasts are based on revenue (USD) for each segment.

By Capacity (kVA)

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Stand-by/Backup Power |

| Prime/Continuous Power |

| Peak-shaving/Load Management |

By End User

| Residential |

| Commercial |

| Industrial |

| By Capacity (kVA) | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Stand-by/Backup Power |

| Prime/Continuous Power | |

| Peak-shaving/Load Management | |

| By End User | Residential |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

How large is the India diesel generator market in 2026?

The India diesel generator market size hit USD 1.33 billion in 2026 and is on track to reach USD 1.88 billion by 2031.

What is driving demand for diesel gensets in Tier-II cities?

Frequent 2- to 4-hour daily outages and voltage fluctuations keep businesses and households reliant on backup power despite national grid improvements.

Which capacity band is growing fastest?

Units rated 375 - 750 kVA are rising at an 8.75% CAGR because hyperscale data centers and large construction projects need synchronized, emission-compliant sets.

How do CPCB IV+ norms affect genset prices?

Compliance adds 15% - 20% to factory cost and raises five-year ownership expenses by as much as 18% due to SCR and DPF requirements.

Will rooftop solar and batteries replace diesel generators soon?

Solar-plus-storage is eroding demand in grid-connected residences, but diesel remains dominant for multi-hour autonomy in off-grid, prime-power, and data-center applications until storage costs fall further.

Page last updated on: