Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

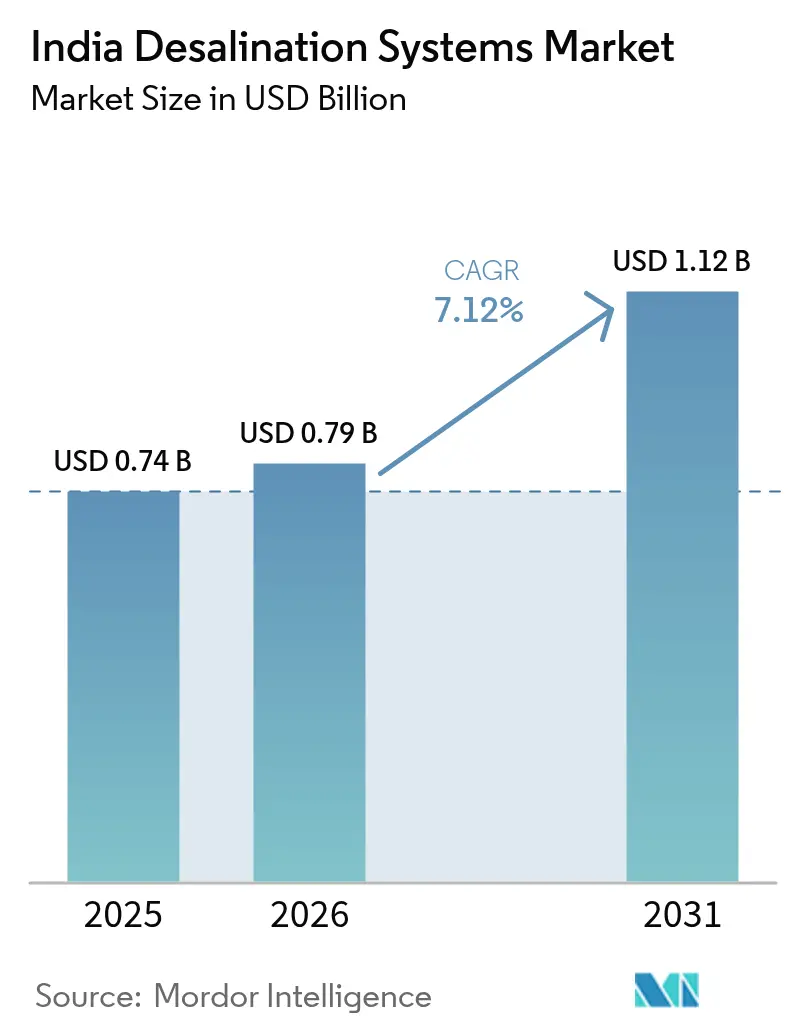

| Base Year Market Size (2025) | USD 0.74 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

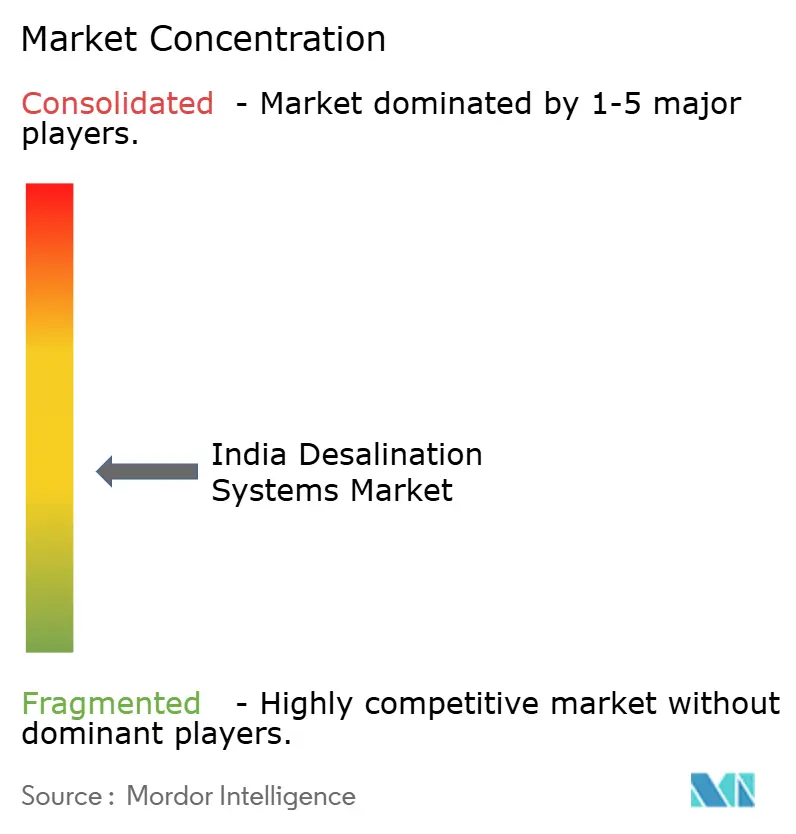

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Desalination Systems Market Analysis by Mordor Intelligence

The India Desalination Systems Market size is expected to grow from USD 0.74 billion in 2025 to USD 0.79 billion in 2026 and is forecast to reach USD 1.12 billion by 2031 at 7.12% CAGR over 2026-2031. The upward curve reflects the country’s deepening water stress, rapid coastal urban growth, and supportive public spending under programs such as Jal Jeevan Mission. Investments are concentrating on energy-efficient reverse-osmosis installations, solar-powered plants, and hybrid systems that meet Zero Liquid Discharge (ZLD) mandates for industry. Developers are also racing to serve renewable-energy clusters and green-hydrogen hubs that require ultrapure process water. As capital intensity edges down and domestic membrane manufacturing scales up, project viability is improving even in mid-tier cities. Market opportunities now extend from municipal seawater plants to rural brackish-water schemes, industrial wastewater recycling, and mineral-recovery applications.

Key Report Takeaways

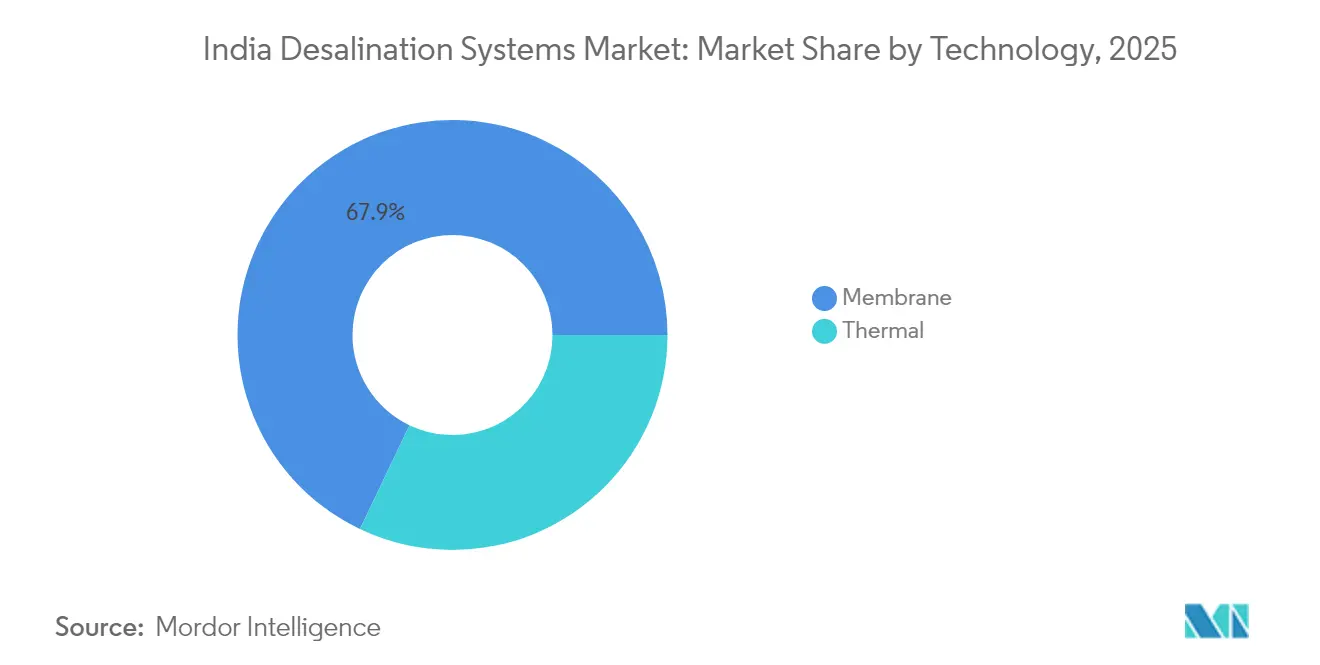

- By technology, membrane systems held 67.92% India desalination systems market share in 2025, while the same segment is projected to expand at a 7.53% CAGR through 2031.

- By application, municipal schemes accounted for 55.78% of the India desalination systems market size in 2025, whereas industrial usage is growing at a 7.28% CAGR to 2031.

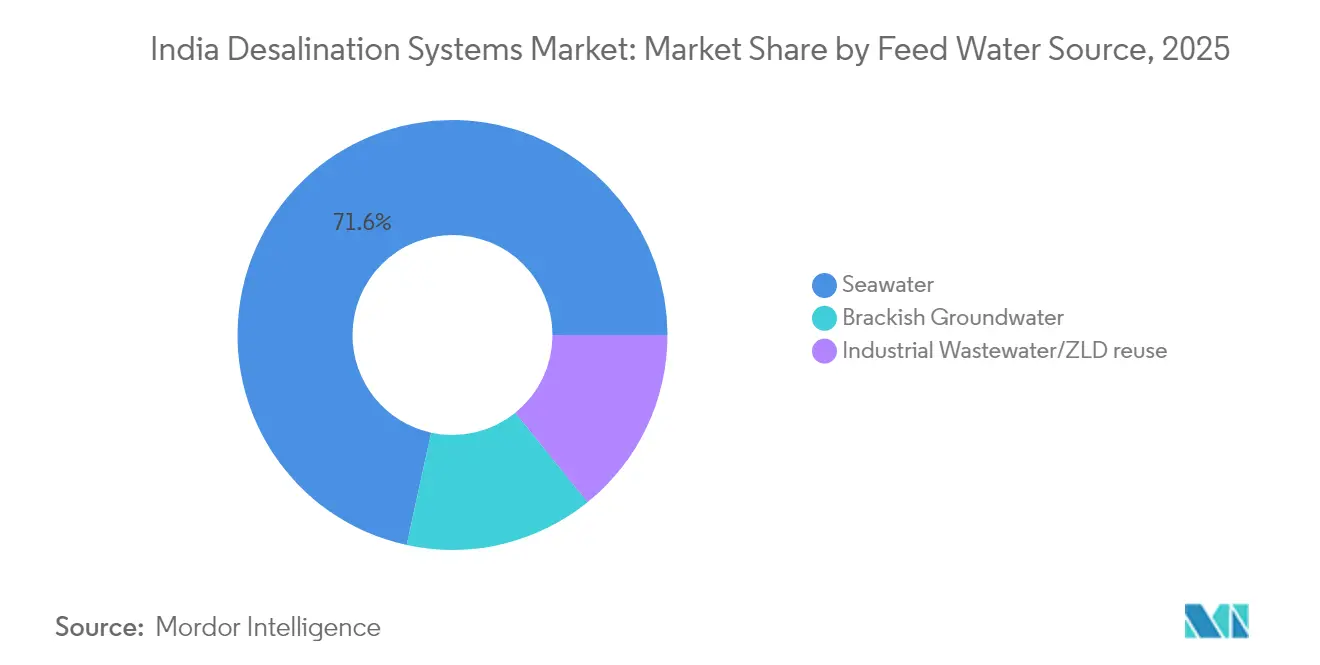

- By feed water source, seawater captured 71.58% India desalination systems market share in 2025; industrial wastewater/ZLD reuse is set to post the quickest 7.52% CAGR through 2031.

- By plant capacity, medium installations (10-100 MLD) commanded 43.88% of the India desalination systems market size in 2025 and large-scale plants (greater than 100 MLD) are advancing at a 7.34% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Desalination Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic water-supply deficit vs demand | +2.10% | Nationwide; acute in Rajasthan, Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Accelerated coastal urbanization and Smart-City desal mandates | +1.80% | West & South coastal corridors | Medium term (2-4 years) |

| Jal Jeevan Mission tie-ins for rural brackish-water RO | +1.40% | National rural belts | Medium term (2-4 years) |

| Grid-parity solar PV enables renewable-powered RO | +1.60% | High-irradiation states: Rajasthan, Gujarat, Andhra Pradesh | Short term (≤ 2 years) |

| Green-hydrogen grade ultrapure-water demand | +0.90% | Coastal RE hubs in Gujarat, Andhra Pradesh, Tamil Nadu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Water-Supply Deficit vs Demand

Groundwater extraction surpassed 245.64 billion m³ in 2024, while recharge hit 446.90 billion m³, masking severe local mismatches[1]Ministry of Jal Shakti, “India’s Groundwater Revival,” pib.gov.in . Over-exploited units fell to 11.13%, yet saline intrusion persists along coasts and in arid belts. Consequently, state utilities are embedding desalination in long-term supply portfolios. NAQUIM-led aquifer mapping and artificial-recharge projects highlight that demand-side restraint alone is inadequate, cementing desalination’s role as a structural supply augmenter. Revised approval norms now prioritize energy-efficient designs and brine-management plans, favoring developers that integrate energy-recovery devices and beneficial-reuse schemes.

Accelerated Coastal Urbanization & Smart-City Desal Mandates

Gujarat’s five-plant blueprint and similar initiatives in Maharashtra and Tamil Nadu show how population shifts are outstripping river and groundwater sources. Smart-City frameworks bundle desalination with IoT metering, real-time leak detection, and predictive asset maintenance, lowering non-revenue water and operating costs. Experience from Chennai’s Minjur plant drove newer designs towards high-pressure RO membranes and turbine-based energy recovery, trimming specific energy to 3.3 kWh/m³. Municipalities now view desalination as foundational infrastructure that unlocks industrial expansion and port-led growth.

Jal Jeevan Mission Tie-ins for Rural Brackish-Water RO Schemes

Over 15 crore households had tapped connections by 2024. Funding extensions to 2028 ensure a stable pipeline for village-level RO packages, especially across fluoride- and arsenic-affected belts in Uttar Pradesh, Bihar, and Rajasthan. Community-scale solar-RO skids are emerging, with batch electrodialysis pilots reporting 22% lower lifetime costs than grid-powered RO[2]Wei He et al., “Flexible Batch Electrodialysis for Low-Cost Solar-Powered Brackish Water Desalination,” Nature Water, nature.com . Local service entrepreneurs trained under the Jal Jeevan frameworks are improving uptime, bolstering long-term sustainability.

Grid-Parity Solar PV Makes Renewable-Powered RO Bankable

Module prices below USD 0.20/W and high insolation states have pushed PV water costs to about USD 1.66/m³ for brackish feed. Hybrid PV-wind plus battery layouts now support 24/7 operation, and real-time demand response cuts grid draw during peak tariffs. NTPC’s USD 21.6 billion green-hydrogen cluster in Andhra Pradesh exemplifies co-located desal, RE, and electrolysis assets. Large EPCs increasingly bundle power-purchase agreements within water-purchase contracts, derisking energy exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy cost & tariff volatility | -1.20% | Nationwide; steeper in high-tariff states | Short term (≤ 2 years) |

| Brine-disposal compliance costs | -0.80% | Coastal states with stringent norms | Medium term (2-4 years) |

| Local-content rules inflate CAPEX for advanced membranes | -0.60% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Brine-Disposal Compliance Costs

Central Pollution Control Board draft norms mandate diffuser-equipped outfalls, salinity plume modeling, and marine-bio monitoring, pushing disposal spend to as high as 33% of total costs in some new bids. Coastal ZLD directives for chemicals and textiles amplify capex. On the upside, emerging crystallization and mineral-recovery technologies aim to monetize salts, gypsum, and magnesium, potentially offsetting compliance outlays if product-grade purity can be reached.

Local-Content Rules Inflate CAPEX for Advanced Membranes

Domestic value-addition thresholds in large municipal tenders increase bid prices for high-pressure RO elements and specialty hollow fibers, as imports attract duties and longer logistics. Ion Exchange’s expanded Goa line, plus rollouts announced by DuPont and Toray, are eroding price gaps. Volume-linked subsidies for Make-in-India components could further narrow the differential, but near-term budgets still reflect higher ticket sizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Membrane Systems Consolidate Leadership

The membrane segment dominated the India desalination systems market with a 67.92% share in 2025 and is set for a 7.53% CAGR as membrane efficiency climbs and unit costs fall. Within the basket, reverse osmosis rules because of robust performance at salinities up to 45,000 ppm, while electrodialysis shines for brackish feeds below 10,000 ppm. Ion Exchange’s Goa plant broadened local RO element supply, trimming lead times and foreign exchange risk. DuPont’s ultra-high-pressure RO modules rated to 120 bar cut energy draw by up to 50% compared to thermal multis-age flash lines.

Thermal desal still finds niches where waste heat is free, notably in refineries and petrochemical parks. Multi-effect distillation retrofits into cogeneration loops in Jamnagar exemplify such synergies. Hybrid layouts pairing RO with vapor compression are emerging for refinery effluents where oil-bearing streams challenge conventional membranes. Advances in graphene-oxide coatings and zwitterionic surfaces are extending membrane life and slashing chemical cleaning frequency, strengthening long-term economics for membrane centric plants.

By Application: Industrial Uptake Accelerates

Municipal bodies commanded a 55.78% share in 2025, yet industrial demand is clocking the faster 7.28% CAGR. ZLD regulations for textiles, pharma, and dyes in states like Tamil Nadu and Gujarat are the prime spur. The India desalination systems market size for industrial users will widen as companies integrate water recycling within ESG roadmaps. Textile parks in Tirupur now operate common-effluent ZLD clusters featuring RO plus thermal concentrators, curbing freshwater withdrawals by over 80%. Petrochemical complexes such as CPCL’s upcoming 60 MLD build-own-operate plant in Nagapattinam illustrate rising capex appetite for captive seawater intake and high-recovery trains. Municipal programs still underpin headline volumes, but protracted tender cycles and public-acceptance hurdles temper growth relative to nimble private projects.

By Feed Water Source: Seawater Dominates While Wastewater Reuse Surges

Seawater represented 71.58% of installed capacity in 2025, reflecting India’s 7,500 km coastline and mega-city clustering. Intake-outfall engineering, anti-fouling screens, and environmental clearances shape project critical paths. Yet the India desalination systems market share for industrial wastewater and ZLD reuse is ballooning, rising at a 7.52% CAGR as discharge norms bite. Brackish-groundwater schemes remain vital inland, especially in Rajasthan’s Thar and Gujarat’s Kachchh belts, where TDS of 4,000-15,000 ppm precludes direct use. Wastewater-fed plants face variable feed chemistry that accelerates membrane fouling; however, inline coagulation, ceramic UF pre-filters, and machine-learning dosing algorithms are lifting uptime to municipal-grade benchmarks.

By Plant Capacity: Larger Projects Gain Traction

Medium-sized plants (10-100 MLD) held 43.88% of the India desalination systems market size in 2025 because they balance scale economics with manageable capex. They remain the workhorse for tier-1 and tier-2 cities. Large schemes exceeding 100 MLD are expanding at a 7.34% CAGR as utilities chase lower unit water costs via energy-recovery turbines and bulk chemical procurement. Gujarat’s Saurashtra cluster, featuring individual projects of 100-200 MLD, typifies this pivot toward mega-scale. Smaller modules under 10 MLD stay relevant for island territories, army bases, and niche industrial estates where rapid deployment and modular expansion are prized. Digital twin platforms now enable capacity-phased rollouts with predictive O&M, de-risking initial capital and smoothing cash flows.

Geography Analysis

West India’s 38.05% revenue share in 2025 mirrors early adoption and aggressive state incentives. Gujarat blends desalination with recharge canals and leak-curbing programs, lowering overall non-revenue water. Maharashtra’s Mumbai-Pune industrial belt taps captive RO and wastewater-reuse loops to safeguard productivity amid erratic monsoons. Ports at Mundra and Hazira add offtake security through long-term utility tie-ups.

South India shows the most dynamic trajectory with a 7.23% CAGR. The Chennai metropolitan zone, already running two 100 MLD plants, is bidding a third 150 MLD unit with record-low water tariffs. Renewable-powered RO pilots in Tuticorin leverage abundant solar-irradiance and wind resources, shrinking levelized costs while slashing Scope 2 emissions. Karnataka’s electronics and biotech parks depend on 0.5 µS/cm ultrapure back-end polishers, pushing vendors to integrate electrodeionization with high-selectivity membranes.

North and East, though nascent, present latent upside. Rajasthan’s Jal Jeevan rollouts include village-cluster solar RO skids that feed 2,000-5,000 families each. Jharkhand’s steel mills retrofit blow-down recovery units to cut freshwater draw by 30%, illustrating industrial drivers beyond coastal zones. Odisha’s port-based petro-complexes are scoping 50-80 MLD seawater RO with deep-sea diffusers to meet upcoming brine norms. Cross-subsidy tariff reforms and viability-gap grants could accelerate penetration in these regions if executed effectively.

Competitive Landscape

The market remains moderately fragmented. Wabag leverages EPC plus 15-year O&M contracts to lock in annuity revenue, having commissioned the 150 MLD Chennai-Nemmeli phase-II plant in 2025. Thermax scales modular 5-25 MLD ZLD systems, bundling heat-pump evaporators with RO to capture industrial segments that demand rapid delivery. Ion Exchange doubled domestic RO-element output to 3 million m² per year, shortening lead times and enhancing localization scores.

Global majors maintain a technological edge. Veolia deploys digital twin software (Aquavista) across its Indian portfolio, lifting membrane life by 12 months on average. DuPont unveiled the WAVE PRO web suite in March 2025, providing scenario-based ultrafiltration modeling in Indian conditions. Collaboration between DuPont and Indian EPCs is rising as PLI-style incentives reward local assembly. Evoqua, post-merger with Xylem, markets skid-mounted electro-deionization lines aimed at green-hydrogen developers on both coasts.

Niche disruptors are entering renewable-powered and containerized desal spaces. Start-ups branded under Make-in-India fabricate graphene-oxide coated flat-sheets that claim 25% higher flux. Others bundle PV arrays, batteries, and remote-monitoring under lease-own models, targeting resorts and island territories. Competition is progressively shifting from lowest-capex bids toward lifecycle-cost guarantees, performance-based payments, and integrated water-energy service contracts.

India Desalination Systems Industry Leaders

Aquatech International LLC

IEI

SUEZ SA

Thermax Ltd

WABAG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Coromandel International, a leading agri-solutions provider in India and part of the Murugappa Group, has entered into an agreement with Veolia Water Technologies and Solutions (India) to enhance its seawater desalination capacity from 6 million liters per day (MLD) to 9 MLD.

- March 2025: DuPont Water Solutions introduced WAVE PRO, a web-based ultrafiltration modeling tool designed for seawater desalination. It offers economic evaluation, scenario analysis, and cross-platform collaboration, aiding technology selection and project optimization in India.

India Desalination Systems Market Report Scope

Desalination systems use different methods to get rid of or reduce the amount of salt in salty water, like seawater or brackish groundwater. The desalination systems market in India is segmented by technology and application. By technology, the market is segmented into thermal technology and membrane technology. By thermal technology, the market is segmented into multi-stage flash distillation, multi-effect distillation, and vapor compression distillation. By membrane technology, the market is segmented into electrodialysis, electrodialysis reversal, reverse osmosis, and other membrane technologies. By application, the market is segmented into municipal and industrial. The report provides market size and forecasts for the market in terms of value (USD million).

By Technology

| Thermal | Multi-Stage Flash (MSF) |

| Multi-Effect Distillation (MED) | |

| Vapor Compression Distillation | |

| Membrane | Electrodialysis (ED) |

| Reverse Osmosis (RO) | |

| Electrodialysis Reversal (EDR) | |

| Other Membrane Technologies (Nanofiltration, Ultrafiltration and Microfiltration) |

By Application

| Municipal |

| Industrial |

By Feed Water Source

| Seawater |

| Brackish Groundwater |

| Industrial Wastewater/ZLD reuse |

By Plant Capacity

| Small (less than 10 MLD) |

| Medium (10–100 MLD) |

| Large (greater than 100 MLD) |

| By Technology | Thermal | Multi-Stage Flash (MSF) |

| Multi-Effect Distillation (MED) | ||

| Vapor Compression Distillation | ||

| Membrane | Electrodialysis (ED) | |

| Reverse Osmosis (RO) | ||

| Electrodialysis Reversal (EDR) | ||

| Other Membrane Technologies (Nanofiltration, Ultrafiltration and Microfiltration) | ||

| By Application | Municipal | |

| Industrial | ||

| By Feed Water Source | Seawater | |

| Brackish Groundwater | ||

| Industrial Wastewater/ZLD reuse | ||

| By Plant Capacity | Small (less than 10 MLD) | |

| Medium (10–100 MLD) | ||

| Large (greater than 100 MLD) | ||

Key Questions Answered in the Report

How large is the India desalination systems market in 2026?

It is valued at USD 0.79 billion with a 7.12% CAGR outlook to 2031.

Which technology type leads adoption?

Membrane-based systems, especially reverse osmosis, held 67.92% share in 2025 and continue to grow fastest.

Why are industrial users accelerating purchases?

Tighter Zero Liquid Discharge rules and sustainability targets push industries to secure reliable, compliant water through captive desalination.

Which region is expanding quickest?

South India posts the highest 7.23% CAGR thanks to renewable-energy projects and technology-sector demand.

What role does renewable energy play in project economics?

Grid-parity solar and hybrid PV-wind setups cut operating energy costs by around 40%, improving bankability of RO plants.

Page last updated on: