China Data Center Processor Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

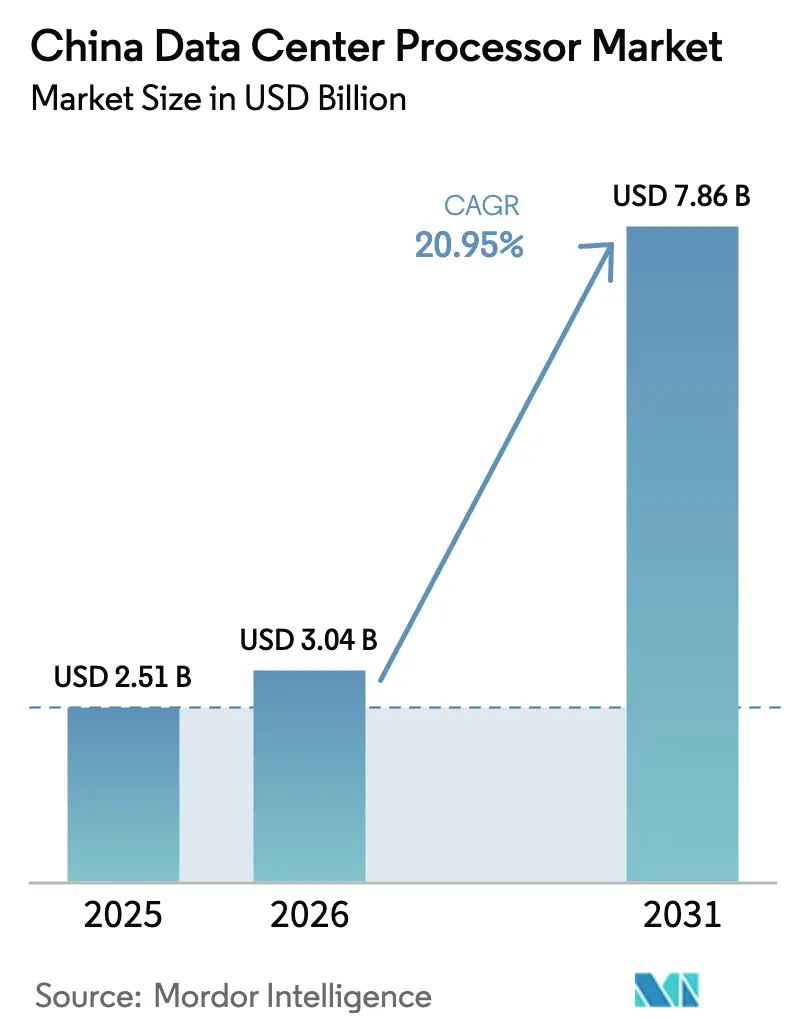

| Base Year Market Size (2025) | USD 2.51 Billion |

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 7.86 Billion |

| Growth Rate (2026 - 2031) | 20.95% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center Processor Market Analysis by Mordor Intelligence

The China data center processor market size is expected to grow from USD 2.51 billion in 2025 to USD 3.04 billion in 2026 and is forecast to reach USD 7.86 billion by 2031 at 20.95% CAGR over 2026-2031. This expansion reflects Beijing’s strategic pivot toward technological self-sufficiency, large-scale cloud investments, and aggressive infrastructure roll-outs under the “East Data, West Compute” program. Export restrictions on advanced foreign chips are simultaneously stimulating home-grown CPU, GPU, and AI-accelerator innovation while creating white-space opportunities for local manufacturers. Energy-efficiency rules capping Power Usage Effectiveness (PUE) at 1.5 for new facilities are driving preference for high-performance yet low-power processors, especially in western renewable-energy hubs

Key Report Takeaways

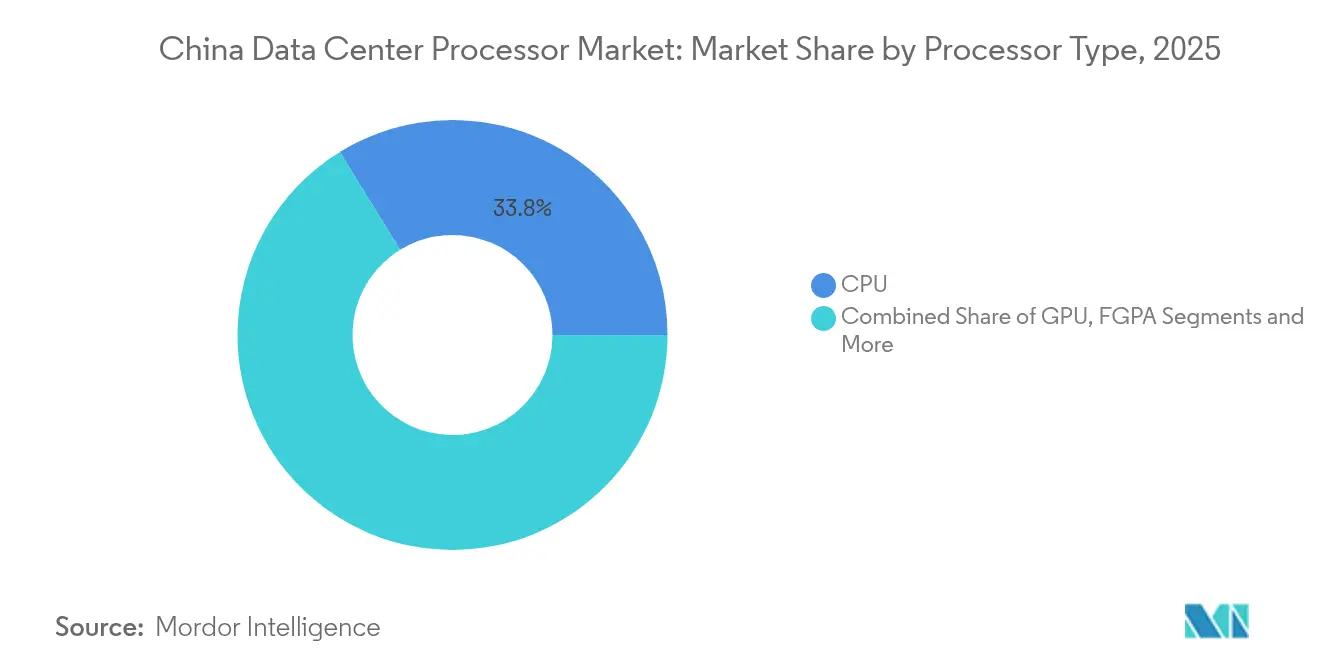

- By processor type, the CPU segment led with 33.78% of China data center processor market share in 2025, while AI Accelerators/ASICs are poised for the fastest 21.85% CAGR through 2031.

- By application, AI/ML Training & Inference accounted for 30.15% share of the China data center processor market size in 2025; Advanced Data Analytics is projected to grow at a 21.25% CAGR to 2031.

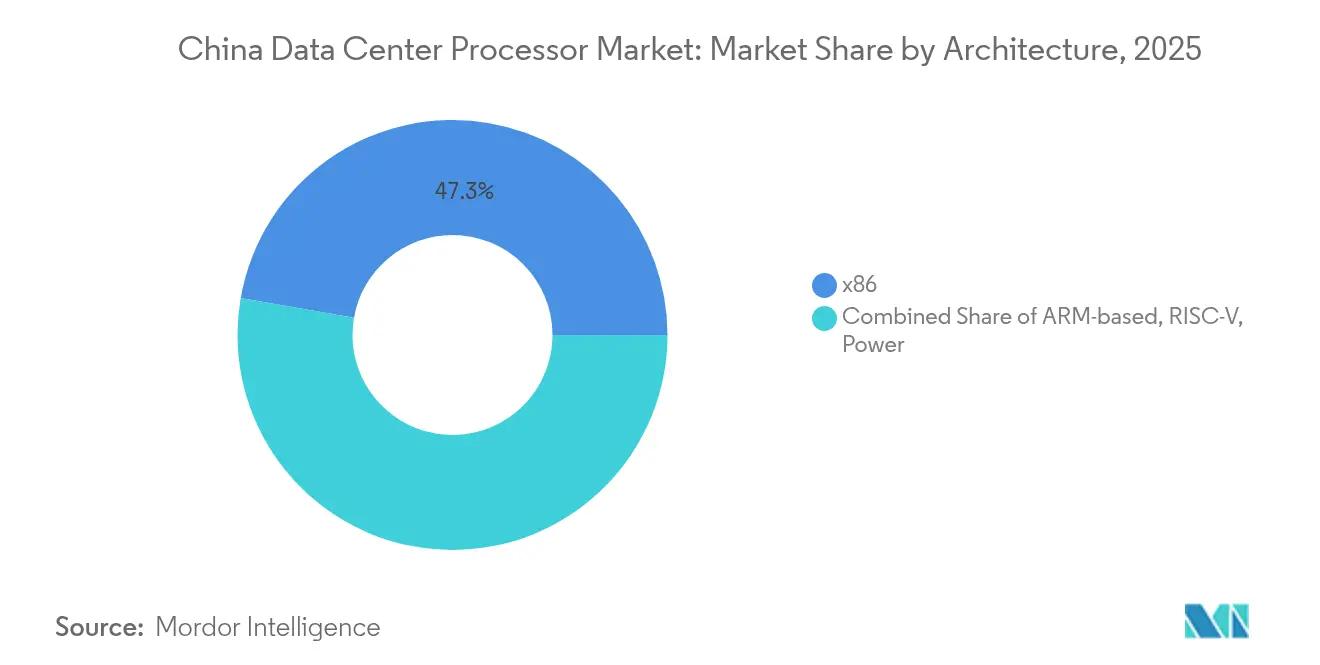

- By architecture, x86 retained 47.25% share in 2025; RISC-V processors are forecast to expand at a 22.35% CAGR.

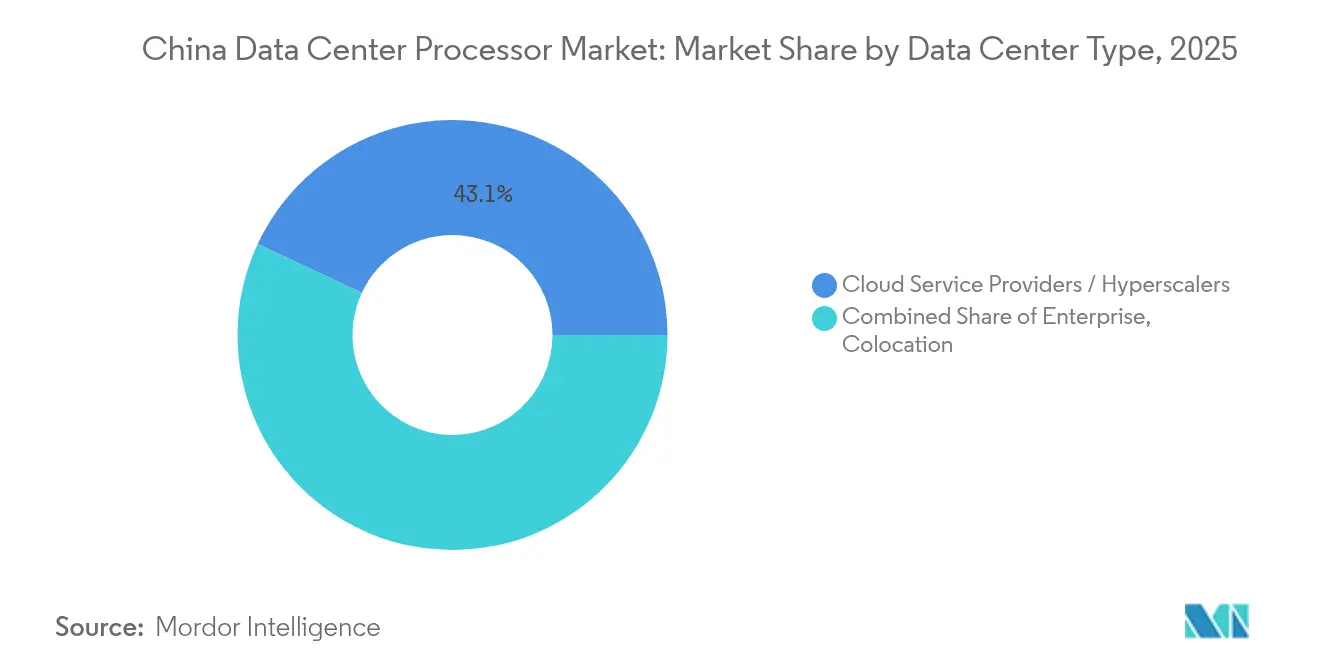

- By data center type, cloud service providers held 43.05% of China data center processor market share in 2025, whereas colocation facilities are forecast to expand at a 22.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of China. The data center processor market share in our global report expresses these relative weights.

China Data Center Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-service hyperscalers' shift toward AI-centric GPU clusters | +4.2% | National, concentrated in eastern tier-1 cities | Medium term (2-4 years) |

| Beijing's "East Data • West Compute" project accelerating regional data-center builds | +3.8% | National, western regions primary beneficiaries | Long term (≥ 4 years) |

| Mandatory domestic-content targets for government workloads | +2.9% | National, government and SOE sectors | Medium term (2-4 years) |

| Rapid adoption of liquid-cooling enabling faster processor refresh cycles | +2.1% | National, hyperscale and enterprise facilities | Short term (≤ 2 years) |

| Emergence of home-grown RISC-V CPUs in custom servers | +1.7% | National, early adoption in research institutions | Long term (≥ 4 years) |

| China's forthcoming AI-focused VAT rebates | +1.5% | National, certified data-center operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-service hyperscale's’ shift toward AI-centric GPU clusters

Hyperscale providers are rebuilding compute fleets around AI-optimized servers, with AI server shipments forecast to reach 2.07 million units in 2025. Projects such as GB200 clusters demand high-bandwidth memory and advanced packaging, fuelling sustained processor refreshes and liquid-cooling retrofits. Domestic cloud firms accelerate these deployments to train large language models amid foreign-chip constraints. The scale of orders is catalyzing local ASIC vendors and broadening the China data center processor market for specialist accelerators.

“East Data, West Compute” project accelerating regional builds

A USD 6.1 billion state investment, coupled with over CNY 200 billion (USD 27.86 billion) in private capital, is erecting eight computing hubs that will house 1.95 million racks. Western sites leverage cheaper land and renewable energy, handling compute-heavy eastern workloads while meeting mandates for 80% green power by 2025. This policy is stimulating demand for energy-efficient processors and is expected to cut carbon emissions up to 20% by 2030 while adding USD 53 billion in economic value.[1]Xinyan Yu, “China’s ‘East Data, West Compute’ plan accelerates data-centre build-out,” South China Morning Post, scmp.com

Mandatory domestic-content targets for government workloads

The “Made in China 2025” rule specifies 70% local content in public-sector data centers. Feiteng CPUs have already shipped 10 million units through government projects, and TencentOS Server V3 now ships with Kunpeng, Hygon, and Feiteng support. These procurement rules compel systems integrators to standardize on domestic chips, cementing predictable demand even as performance gaps with foreign offerings narrow.[2] Ian Cutress, “Feiteng CPUs Hit 10 Million Milestone,” Tom’s Hardware, tomshardware.com

Rapid liquid-cooling adoption enabling faster refresh cycles

Liquid cooling is now used in 22% of Chinese facilities and is expanding 15% annually, enabling rack densities up to 80 kW quadrupling the capability of conventional air-cooled deployments. The technology shortens processor refresh intervals, underpins AI training clusters, and helps operators meet the PUE ≤ 1.5 requirement for new builds.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. export controls on advanced process nodes | -3.4% | National, affecting advanced chip access | Long term (≥ 4 years) |

| Stricter energy-use quotas for hyperscale facilities | -2.1% | National, major metropolitan areas | Medium term (2-4 years) |

| Funding volatility for fab-less AI-chip start-ups | -1.8% | National, concentrated in tech hubs | Short term (≤ 2 years) |

| Shortage of senior chip-architecture talent | -1.2% | National, acute in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S. export controls on advanced process nodes

The December 2024 Bureau of Industry and Security update placed 140 Chinese firms on the Entity List and tightened rules on lithography and high-bandwidth memory. Foundries such as SMIC struggle to access sub-7 nm tools, and U.S. EDA software restrictions add further hurdles. NVIDIA absorbed a USD 4.5 billion reserve for restricted H20 GPU exports, highlighting the scale of lost opportunities. [3]CSIS Strategic Technologies Program, “Updated Semiconductor Export Controls to China,” Center for Strategic and International Studies, csis.org Yet the squeeze has triggered accelerated R&D at firms like Huawei, whose Ascend 910C now delivers 60% of H100 inference performance.

Shortage of senior chip-architecture talent

China needs 789,000 semiconductor professionals by 2024, yet supply trails by one-third. Wage inflation has doubled entry-level salaries since 2018, while only 40% of graduates gain meaningful internships. The deficiency is most acute in advanced CPU and GPU design, slowing the roll-out of competitive domestic processors despite heavy state investment in training programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: AI Accelerators Drive Next-Generation Computing

CPU products retained leadership with 33.78% China data center processor market share in 2025, reflecting their suitability for versatile cloud and enterprise workloads. AI Accelerator/ASIC units, however, are expanding at a 21.85% CAGR as hyperscalers pursue efficiency for model training and inference. GPU deployments continue to rise for both AI and graphics, while FPGA sales meet niche reconfigurable computing demand.

The migration toward accelerator-rich servers is reshaping procurement: DeepSeek will deploy 32,000 Ascend 910C chips in its next model, and Biren Technology plus Moore Threads are raising fresh capital to position as domestic “NVIDIA alternatives”. This bifurcation is widening the addressable China data center processor market and encouraging cross-licensing among local vendors.

By Application: AI/ML Training Reshapes Infrastructure Demands

AI/ML Training & Inference consumed 30.15% of the China data center processor market size in 2025, underscoring the sector’s pivot toward intelligence-first services. Advanced Data Analytics leads future growth at 21.25% CAGR, reflecting enterprises’ demand for real-time insights. High-Performance Computing serves academia and national supercomputing centers, while Security & Encryption gains traction amid heightened cyber threats.

National AI compute capacity is set to reach 1,037 EFLOPS by 2025. Tencent and Alibaba now integrate self-designed ASICs in their stacks, supported by USD 912 billion of public AI research investment. This vibrant startup ecosystem pressures processor vendors to supply cost-effective yet powerful silicon

By Architecture: RISC-V Disrupts Traditional x86 Dominance

x86 still commanded 47.25% share in 2025, buoyed by a mature software base. RISC-V, however, is surging at a 22.35% CAGR as developers exploit the open ISA to tailor chips for cloud and edge workloads. ARM solutions serve mobile-cloud convergence, and POWER architectures endure in selected HPC clusters. Loongson’s 32-core 3D5000, formed from two chiplets and drawing 130-170 W, illustrates how local firms leverage RISC-V for data-center scale. Government-backed RISC-V Innovation Alliance partnerships and new training centers further erode legacy lock-in.

By Data Center Type: Cloud Providers Lead Infrastructure Transformation

Cloud Service Providers remain the principal buyers of processors, fueling more than half of server demand. The colocation market is growing fastest at 22.85% CAGR as enterprises balance cloud agility with dedicated control. Enterprise-owned facilities persist where data residency or compliance rules dictate isolated hardware.

State-owned operators China Mobile and China Telecom have invested 239 billion yuan in “East Data, West Compute” hubs, strengthening public-sector leverage over compute capacity. The shift supports domestic chip suppliers through bulk orders tied to procurement mandates.

Geography Analysis

Eastern metros such as Beijing, Shanghai, and Guangzhou still host the densest concentration of data centers, but face strict power-quota ceilings and land scarcity. Western provinces—Guizhou, Inner Mongolia, Xinjiang—are now absorbing compute-intensive workloads as renewable energy and cooler climates lower operating costs

Talent pools remain skewed eastward; Beijing, Shanghai, and Shenzhen aggregate most chip-design engineers, giving local incubators a head start on next-generation CPU and GPU projects. Western facilities thus favor standardized, energy-efficient processors that can be operated remotely while local universities scale semiconductor curricula.

Environmental rules are diverging: Beijing bans new data centers with PUE above 1.5, whereas western authorities incentivize >80% renewable power. Processor vendors are tailoring line-ups accordingly—offering low-power SKUs for urban cores and high-density accelerators for renewable-rich regions.

Mordor Intelligence examines the data center processor market across diverse other regional markets as well, including Asia, while also offering granular country-level perspectives for South Korea, Thailand, Netherlands, France, Germany, United Kingdom, Singapore, and Indonesia and more.

Competitive Landscape

The China data center processor market presents a dual track: foreign leaders dominate ultra-high-end GPUs, yet domestic challengers gain share through policy support and niche specialization. Chinese vendors follow two playbooks. First, parity seekers pump R&D to match flagship performance; Ascend 910C now delivers 60% of H100 inference throughput. Second, cost disruptors exploit mandatory local content, winning public contracts even at modest speeds. AMD’s 2024 data-center revenue surge to USD 12.6 billion shows foreign brands can still thrive by emphasizing energy efficiency and rapid roadmap cadence.

Hyperscalers are meanwhile designing custom ASICs to sidestep traditional suppliers. DeepSeek’s software-led AI breakthroughs illustrate how optimization can offset raw silicon gaps, compelling chipmakers to bundle hardware with tailored toolchains and ecosystem services.

China Data Center Processor Industry Leaders

Intel Corporation

NVIDIA Corporation

Ampere Computing

Arm Ltd.

Advanced Micro Devices Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DeepSeek unveiled an open-source LLM rivaling GPT-4 at a fraction of cost, triggering a 17% slide in NVIDIA’s share price and spotlighting local AI competitiveness.

- January 2025: AMD posted record USD 12.6 billion 2024 data-center revenue, up 94% YoY, with EPYC and AI products exceeding USD 5 billion.

- December 2024: U.S. BIS added 140 entities to the Entity List and tightened controls on advanced semiconductors and tools.

- December 2024: Biren Technology raised CNY 2 billion (USD 280 million) from Guangzhou government investors following export-control placement

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China data center processor market as revenue earned from new CPUs, GPUs, FPGAs, and AI accelerators that are deployed inside enterprise, colocation, and hyperscale data-center servers handling production workloads. The estimate excludes discrete memory ICs, networking NICs, and refurbished or second-life chips.

Scope Exclusion: Edge gateways and consumer graphics cards are not counted because they serve fundamentally different power, cooling, and duty-cycle profiles.

Segmentation Overview

- By Processor Type (Value)

- GPU

- CPU

- FPGA

- AI Accelerator/ASIC

- By Application (Value)

- Advanced Data Analytics

- AI/ML Training and Inference

- High-Performance Computing

- Security and Encryption

- Network Functions Virtualisation

- Others

- By Architecture (Value)

- x86

- ARM-based

- RISC-V

- Power

- By Data Center Type (Value)

- Enterprise

- Colocation

- Cloud Service Providers / Hyperscalers

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chip architects, server OEM product managers, data-center operators across Beijing, Guizhou, and Shenzhen, and power-utility engineers. These conversations clarified real rack densities, procurement lead times, and expected transition rates toward domestic ARM and RISC-V parts, filling gaps left by public statistics.

Desk Research

We began with public datasets from the Ministry of Industry and Information Technology, the China Academy of Information and Communications Technology, General Administration of Customs shipment codes, and the China Semiconductor Industry Association, which together anchor domestic production, import, and utilization trends. Supplemental insights came from annual reports and 10-Ks of leading cloud providers, patent families mined through Questel, and peer-reviewed IEEE papers on high-density AI server design. To map pricing and vendor shares, analyst pulls from D&B Hoovers and Dow Jones Factiva tracked quarterly channel commentary and spot ASP movements. The sources cited are illustrative; dozens of additional datasets fed the validation loop.

Market-Sizing & Forecasting

One top-down reconstruction converts MIIT server-shipment volumes into processor counts, adjusts for multi-socket ratios, and multiplies by weighted average selling prices. Results are cross-checked with a sampled bottom-up roll-up of supplier invoices and channel checks, enabling fine-tuning where the two views diverge. Key drivers inside the model include: annual cloud CAPEX budgets, GPU attach rate for AI training clusters, average power usage effectiveness caps set at 1.5, rack density migration toward >100 kW liquid-cooled enclosures, and domestic content mandates under the "East Data West Compute" program.

A multivariate regression that links these drivers to historical revenue underpins the 2025-2030 forecast, and scenario tests stress energy-price spikes and export-control shifts. When bottom-up gaps appear for niche FPGA use, we interpolate using verified adoption ratios from expert interviews.

Data Validation & Update Cycle

Before sign-off, analysts run variance checks against CAICT cloud index trends and independent import logs; anomalies trigger re-contact of at least one industry source. Every report is refreshed annually, with interim updates when material policy or supply events surface, and a final audit is performed just before client delivery.

Why Mordor's China Data Center Processor Baseline Commands Confidence

Published estimates often differ because firms mix broader chip classes, apply varying years, or assume uniform pricing. Our disciplined scope and annual refresh cadence keep numbers aligned with on-the-ground realities.

Key gap drivers include rival models that merge memory and networking silicon into the same total, use conservative ASPs that ignore AI premium pricing, or stretch forecasts without validating cloud CAPEX pipelines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.51 B (2025) | Mordor Intelligence | - |

| USD 1.07 B (2024) | Global Consultancy A | earlier base year and aggregates all data-center chips, understating AI uplift |

| USD 3.50 B (2030) | Trade Journal B | forward year projection plus bundled accelerator and networking revenue inflates total |

These contrasts show that Mordor's balanced bottom-up checks, transparent variable set, and strict processor-only boundary give decision-makers a reliable, reproducible baseline.

Key Questions Answered in the Report

What is the current size of the China data center processor market?

The market is valued at USD 3.04 billion in 2026 and is projected to hit USD 7.86 billion by 2031.

How are liquid-cooling technologies influencing the market?

They enable rack densities up to 80 kW, shorten processor refresh cycles, and help operators meet the PUE ≤ 1.5 regulation for new data centers

Which processor segment is growing fastest?

AI Accelerator/ASIC units are expanding at a 21.85% CAGR as hyperscalers rebuild fleets for large language models.

Why are RISC-V processors important for China?

RISC-V’s open architecture reduces foreign IP dependence and is growing at a 22.35% CAGR, supported by government alliances and training programs.

Page last updated on: