Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Indonesia Data Center Processor Market is Segmented by Processor Type (GPU, CPU and More), Application( Advanced Data Analytics, AI/ML Training and Inference, High-Performance Computing and More), Architecture (X86, ARM-Based, RISC-V and Power), Data Center Type (Enterprise, Colocation, Cloud Service Providers / Hyperscalers). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

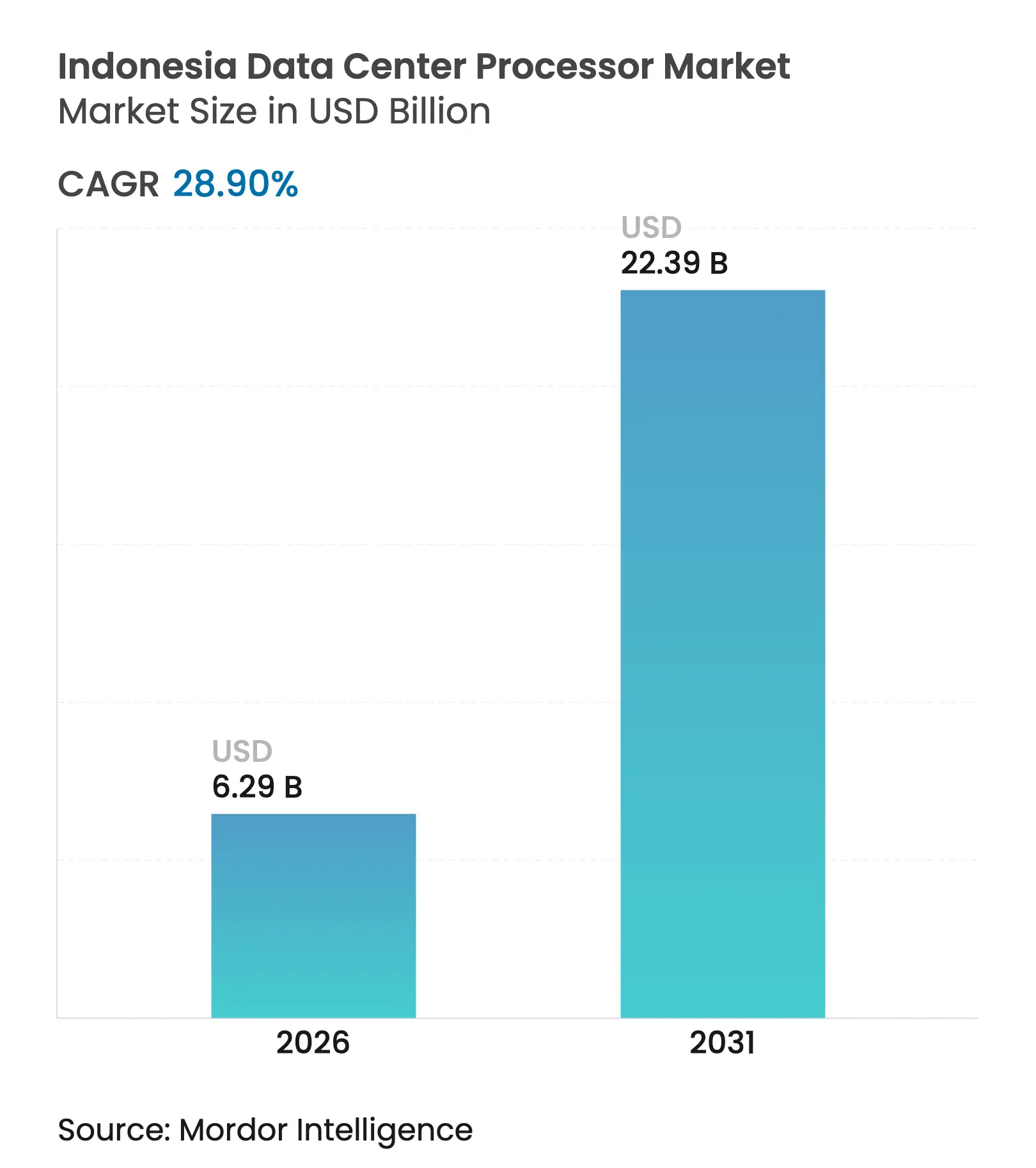

| Market Size (2026) | USD 6.29 Billion |

| Market Size (2031) | USD 22.39 Billion |

| Growth Rate (2026 - 2031) | 28.90 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Indonesia data center processors market size was valued at USD 4.88 billion in 2025 and estimated to grow from USD 6.29 billion in 2026 to reach USD 22.39 billion by 2031, at a CAGR of 28.9% during the forecast period (2026-2031). Capacity build-outs by hyperscalers, enforcement of domestic data-storage rules, and rising AI workloads together underpin this momentum. Ongoing subsea-cable landings and edge-friendly regulations strengthen regional connectivity, while falling colocation tariffs accelerate adoption among small and mid-sized enterprises. Competition is shifting from capacity expansion toward differentiation in power efficiency, sovereign-cloud compliance, and AI-ready rack densities.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Robust hyperscaler CAPEX pipeline

Robust hyperscaler CAPEX pipeline

| +8.2% | National, concentrated in Greater Jakarta and Batam | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

+8.2%

|

Geographic Relevance

:

National, concentrated in Greater Jakarta and Batam

|

Impact Timeline

:

Medium term (2-4 years)

|

Government AI and Digital Economy programmes Government AI and Digital Economy programmes | +6.8% | National, with priority zones in Java and emerging hubs | Long term (≥ 4 years) | |||

Demand for GPU-dense cloud instances

Demand for GPU-dense cloud instances

| +7.4% | National, with hyperscale concentration in Jakarta | Short term (≤ 2 years) | |||

Data-localisation regulations

Data-localisation regulations

| +5.1% | National, affecting all cloud service providers | Medium term (2-4 years) | |||

New subsea cable landings boosting east-Indonesia colos

New subsea cable landings boosting east-Indonesia colos

| +2.8% | Eastern Indonesia, particularly Sulawesi and Maluku | Long term (≥ 4 years) | |||

Carbon-credit backed "green-core" processors

attracting ESG funds

Carbon-credit backed "green-core" processors

attracting ESG funds

| +1.9% | National, with green energy integration focus | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Robust Hyperscaler CAPEX Pipeline

The Indonesian data center processors market is benefiting from an unprecedented wave of hyperscaler investment commitments. Microsoft’s USD 1.7 billion pledge and Tencent’s USD 500 million program headline a national project pipeline exceeding 400 MW in planned IT load. Jakarta’s colocation revenues are expected to reach USD 938 million by 2027, with hyperscale-linked facilities forming 72% of the total. EdgeConneX, for instance, is expanding to more than 200 MW in Bekasi, tripling its present footprint. These sizable site additions translate directly into multi-generation processor refresh cycles, driving consistent demand for CPUs, GPUs, and AI accelerators across new racks

Government AI and Digital Economy Programmes

Strategic initiatives such as Vision 2045, the National AI Strategy, and the Digital Indonesia Roadmap align ministries under a shared digital-transformation mandate. The Coordinating Ministry for Economic Affairs estimates that AI could lift GDP by USD 366 billion by 2030, while KORIKA orchestrates public-private collaboration on smart-city and health-tech pilots. The state-backed National Data Center in Cikarang, featuring 25,000 processor cores, showcases institutional commitment to sovereign infrastructure. Together, these programmes secure long-term funding streams and provide regulatory certainty that stimulates processor upgrades across government and enterprise workloads.[1]Coordinating Ministry for Economic Affairs, “Indonesia National AI Strategy,” ekon.go.id

Demand for GPU-Dense Cloud Instances

AI/ML training intensity is reshaping facility design, pushing rack densities toward 500-1,000 kW to support AI factory clusters. Lintasarta’s GPU Merdeka service—the first sovereign AI cloud built on NVIDIA hardware—gives domestic firms elastic access to high-performance GPUs while complying with data-localisation rules. This shift is mirrored by growing enterprise preference for private AI infrastructure that mitigates data-sensitivity concerns in sectors such as banking, gaming, and education. Resultant demand boosts shipments of accelerators and powers the Indonesian data center processors market through short-term refresh cycles.[2]Lintasarta, “GPU Merdeka Sovereign AI Cloud Launch,” lintasarta.co.id

Data-Localisation Regulations

Government Regulation 71/2021 requires electronic-system operators to keep critical data within national borders. Global cloud providers have responded by building sovereign regions, which in turn anchor new processor installations domestically. Lintasarta’s Cloud Sovereign service and Bank Rakyat Indonesia’s advanced analytics platform illustrate how localisation rules amplify local processor demand while fostering trusted-cloud offerings. As the Personal Data Protection Law comes into full effect, compliance considerations will continue to reinforce domestic processor procurement over the forecast window.

Restraint Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of advanced-node semiconductor talent

Shortage of advanced-node semiconductor talent

| -3.4% | National, acute in specialized AI/ML roles | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

-3.4%

|

Geographic Relevance

:

National, acute in specialized AI/ML roles

|

Impact Timeline

:

Medium term (2-4 years)

|

High utility tariffs vs. neighbouring hubs

High utility tariffs vs. neighbouring hubs

| -2.8% | National, particularly affecting hyperscale operations | Short term (≤ 2 years) | |||

Grid instability outside Java delaying tier-IV builds

Grid instability outside Java delaying tier-IV builds

| -2.1% | Outer islands, particularly Sumatra and Kalimantan | Long term (≥ 4 years) | |||

Seismic risk elevating TCO for processor racks

Seismic risk elevating TCO for processor racks

| -1.6% | Java and Sumatra, affecting infrastructure design | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Advanced-Node Semiconductor Talent

Local design and optimisation of cutting-edge processors are hampered by a limited pool of engineers skilled in sub-10 nm nodes and AI frameworks. Although NVIDIA pledges to train 20,000 students, Indonesia still faces talent leakage to higher-paying markets such as Singapore. The workforce gap inflates project timelines, raises total cost of ownership, and increases dependency on imported expertise. National semiconductor hub programmes should ease constraints over the medium term, yet the talent shortage will likely temper the Indonesian data center processors market expansion rate until at least 2028. [3]United Nations Industrial Development Organizations, “Industrial Development Report,"unido.org

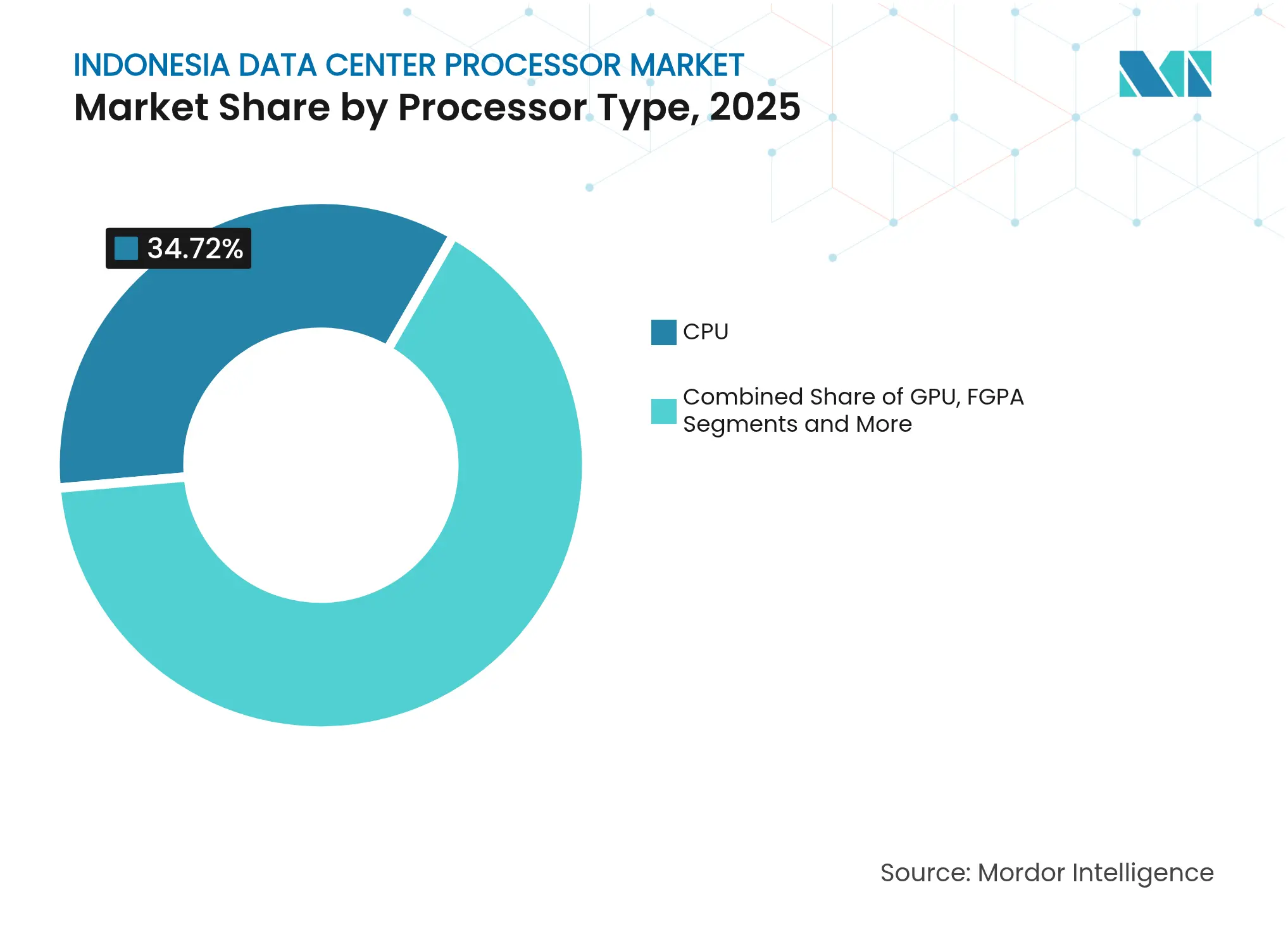

By Processor Type: AI Accelerators Drive Next-Generation Workloads

CPUs held 34.72% Indonesian data center processors market share in 2025 due to their versatility across general-purpose workloads. Intel Xeon chips underpin e-commerce giants such as Tokopedia, ensuring a stable core market. AI Accelerators/ASICs, however, are on a 30.05% CAGR trajectory that will reshape the processor mix through 2031. Their ascent is fuelled by demand for large-scale AI inference, with Lintasarta’s GPU Merdeka bringing sovereign GPU-as-a-Service to local firms. FPGA uptake is rising within fintech and telecom applications that require deterministic low-latency processing. AMD’s EPYC-powered ALELEON supercomputer further diversifies the performance landscape by providing public high-performance computing access.

As hyperscalers upgrade to support transformer-based models, the Indonesia data center processors market continues to migrate toward heterogeneous architectures. CPUs still dominate legacy and transactional loads, yet the growing volume of AI inference calls accelerates ASIC adoption. Indications of this shift include rack-density blueprints aimed at 30 kW per cabinet and above. FPGA demand, while smaller, is expected to outpace legacy architectures in financial-trading and mission-critical telco networks.

Note: Segment shares of all individual segments available upon report purchase

By Application: Advanced Analytics Accelerates Digital Transformation

AI/ML training and inference retained a 33.05% share of the Indonesian data center processors market size in 2025 as enterprises raced to operationalize vision and language models. Bank Mandiri’s data platform, which prevents USD 1 billion in fraud losses, underscores AI’s enterprise value. Advanced analytics shows the swiftest 30.52% CAGR because CIOs now integrate real-time data streams into decision support. High-performance computing (HPC) moves from university labs to commercial-scale CFD and genome-sequencing tasks, aided by ALELEON’s public access terms.

Security & encryption spending climbs steadily in response to the Personal Data Protection Law and a surge in ransomware incidents. Network functions virtualisation also gains ground: operators like Indosat Ooredoo Hutchison deploy local language models to optimise 5G edge traffic. These application trends collectively sustain incremental processor-unit demand, reinforcing the expansion of the Indonesia data center processors market through 2031.

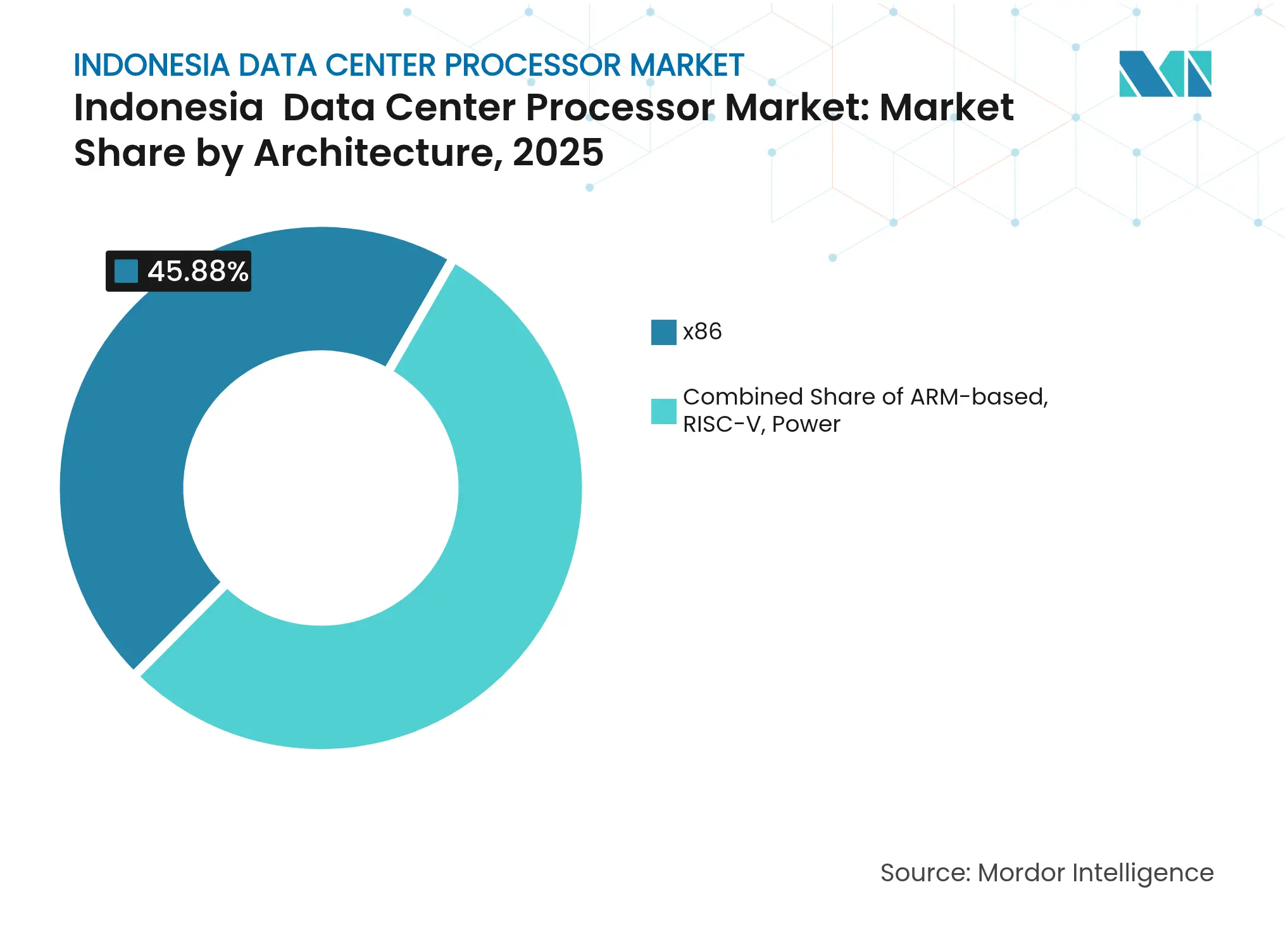

By Architecture: RISC-V Emerges as Open Alternative

x86 chips controlled 45.88% Indonesian data center processors market size in 2025, reflecting their entrenched software ecosystem. ARM architectures are gaining importance for edge workloads, given energy-efficiency advantages. Meanwhile, open-source RISC-V enjoys a 30.96% CAGR as Indonesia pursues technology sovereignty, encouraged by the USD 45.74 billion silica-downstreaming roadmap. Government interests in customising processors for local language AI accelerate RISC-V trials across academic labs and emerging-tech startups.

Power architecture sustains a niche in ultra-reliable financial and governmental compute clusters. Collectively, the architectural mix showcases an Indonesian data center processors market progressing toward heterogeneity: x86 remains indispensable for mainstream cloud, ARM addresses edge-compute niches, and RISC-V aligns with long-term sovereign design goals

Note: Segment shares of all individual segments available upon report purchase

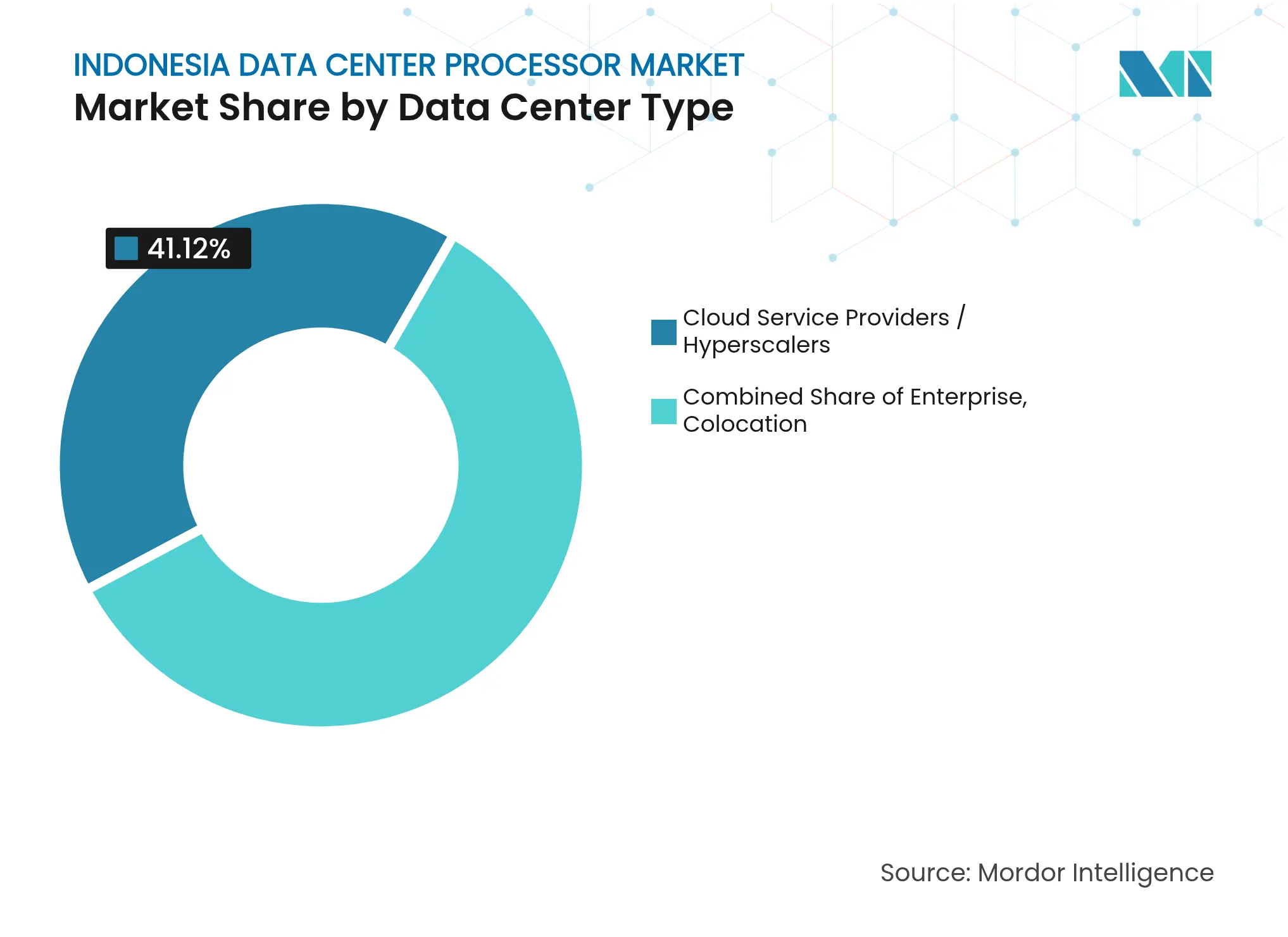

By Data Center Type: Colocation Expansion Drives Infrastructure Growth

Cloud service providers and hyperscalers captured 41.12% Indonesia data center processors market share in 2025 on the back of sustained CAPEX from Microsoft, Tencent, Amazon, and Google. Colocation operators, however, post the fastest 31.38% CAGR as mid-market enterprises adopt pay-as-you-grow models to avoid upfront capital outlay. NeutraDC’s 51 MW Batam site typifies strategic edge expansions that benefit from subsea-cable landings.

Enterprise data centers persist for workloads constrained by compliance boundaries, mainly in banking and government. Meanwhile, renewable-powered campuses such as BDx’s 500 MW site respond to ESG-driven procurement criteria. This diversity ensures that the Indonesia data center processors market serves both hyperscale and distributed edge needs, reinforcing processor-demand resilience across varying facility classes.

Note: Segment shares of all individual segments available upon report purchase

Greater Jakarta remains the gravitational centre of the Indonesia data center processors market, hosting 35 operational projects and multiple hyperscale builds. The region’s mature power grid, fiber density, and proximity to 30 million metropolitan users protect its status as first-choice landing zone for global cloud regions. Real-estate scarcity and rising land valuations, however, prompt operators to explore secondary clusters such as Bekasi and Cikarang, where EdgeConneX and STT GDC are scaling multi-megawatt campuses.

Batam’s strategic location and submarine-cable intersections elevate the island into a national gateway hub. Projects like Nongsa Digital Park’s 221 MW campus and the forthcoming Nongsa–Changi cable enable latency-sensitive cross-border traffic between Indonesia and Singapore. Eastern regions gain momentum after the Palapa Ring completion and the Bifrost Cable System landing in Manado. These links underpin edge-data-center deployments aimed at content-delivery networks and cloud gaming, contributing fresh volumes to the Indonesian data center processors market.

Sumatra and Kalimantan represent long-horizon prospects, combining lower land prices with abundant geothermal reserves that appeal to ESG investors. Government plans to situate one national data center in the new capital Nusantara reinforce eastern diversification. Attention now turns to grid-reliability upgrades that can support tier-IV builds. By distributing future builds beyond Java, Indonesia mitigates seismic and power-capacity risks, while enlarging the total addressable footprint for processor suppliers

Market Concentration

Indonesian telecommunications incumbents such as Telkom Indonesia (NeutraDC) and Indosat Ooredoo Hutchison are intensifying investment in sovereign cloud and GPU curtains to defend share against foreign entrants. International majors—Digital Realty, EdgeConneX, STT GDC—leverage joint ventures to access licenses and land banks swiftly, injecting global best practices into build-outs. Colocation pricing has fallen from USD 400 to USD 300–320 per kVA, illustrating competitive pressure as capacity outstrips current demand in Jakarta’s core zones.

Strategic differentiation now centres on AI-ready design, sustainability credentials, and cross-border interconnect richness. PT DCI Indonesia’s solar-powered campus and BDx’s 500 MW renewable facility showcase early-mover advantage in green power. Lintasarta’s GPU Merdeka positions itself as the sovereign AI on-ramp, while NeutraDC’s Batam build synchronises with subsea-route growth.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Indonesia Data Center Processor Market Analysis Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 4.88 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 2.80 B (2024) | Regional Consultancy A | Bundles facility construction and wider IT hardware yet omits GPU attach growth | ||

USD 0.20 B (2025) | Global Consultancy B | Tracks rack-server shipments only; excludes discrete GPUs and ASIC cards | ||

USD 5.80 M (2023) | Industry Association C | Limits scope to locally assembled CPUs; ignores imports and accelerator categories |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.