India Contract Manufacturing Organization (CMO) Market Size

Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

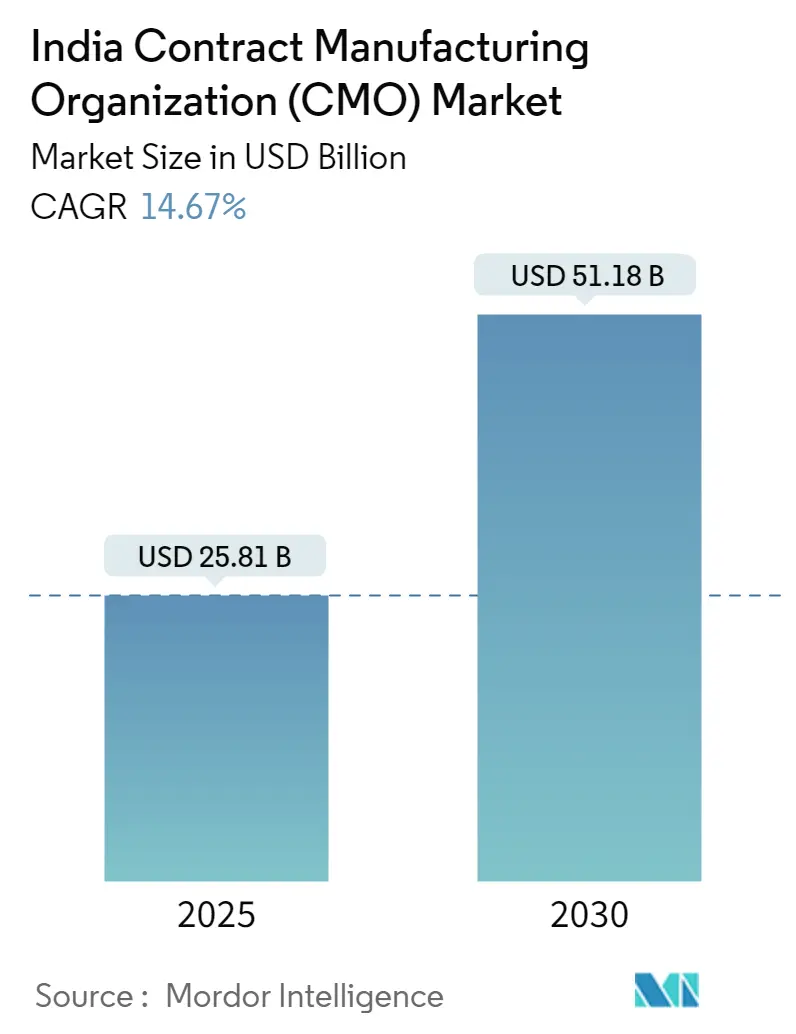

| Market Size (2025) | USD 25.81 Billion |

| Market Size (2030) | USD 51.18 Billion |

| Growth Rate (2025 - 2030) | 14.67% CAGR |

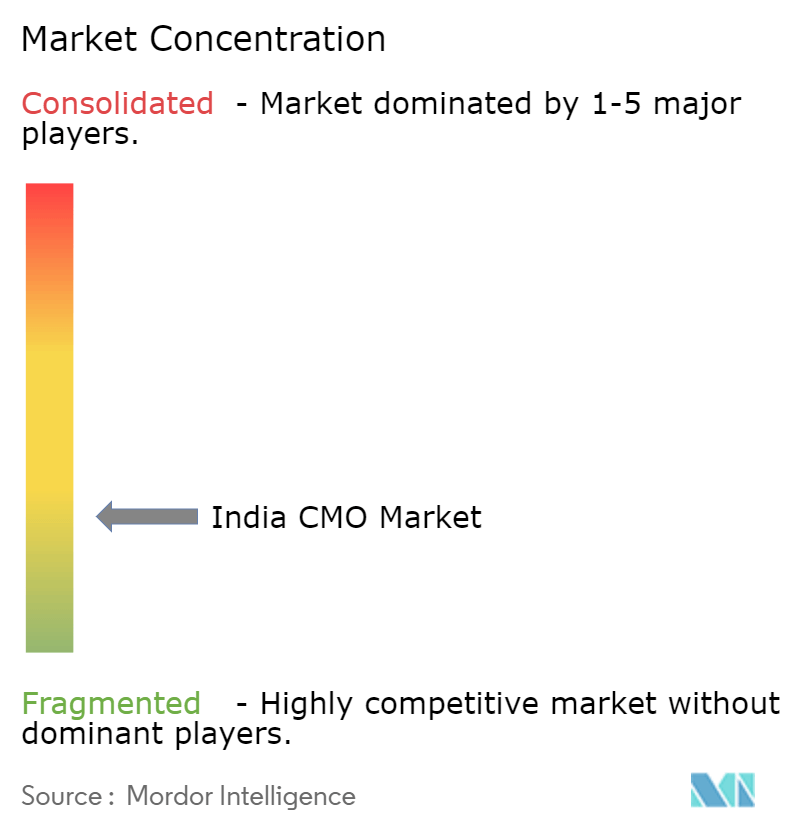

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Contract Manufacturing Organization (CMO) Market Analysis

The India Contract Manufacturing Organization Market size is worth USD 25.81 Billion in 2025, growing at an 14.67% CAGR and is forecast to hit USD 51.18 Billion by 2030.

India's pharmaceutical industry, including its thriving CMO industry, continues to assert its global prominence, playing a pivotal role in the supply of generic medicines and vaccines worldwide. As a leading supplier of generic drugs to the United States and a key player in global vaccine production, India's position is underpinned by its cost-efficient manufacturing capabilities and a robust network of U.S. FDA-approved facilities. In 2023, this foundation is further strengthened by increased investments in research and development, alongside supportive government initiatives such as the Production Linked Incentive (PLI) scheme. These efforts collectively aim to enhance the sector's infrastructure, output, and global competitiveness, ensuring sustained growth.

Amidst this dynamic landscape, the contract manufacturing organization pharma (CMO) and contract development and manufacturing organization (CDMO) market in India is witnessing significant growth. This expansion is fueled by the rising demand for generic drugs, biosimilars, and injectable formulations, coupled with the growing trend of strategic outsourced manufacturing by pharmaceutical companies. Notable developments, such as Aurigene Pharmaceutical Services' establishment of a state-of-the-art facility offering contract manufacturing services for antibodies, viral vectors, and proteins in May 2023, highlight the sector's momentum. Additionally, advancements in manufacturing technologies, including automation and continuous manufacturing, are reshaping the CDMO industry, driving improvements in efficiency and quality.

The growth trajectory of India's CMO and CDMO market is supported by a combination of macroeconomic trends and specific industry drivers. India's established leadership in pharma contract manufacturing, combined with its cost advantages, creates a strong foundation. Meanwhile, the increasing demand for generics and biosimilars, alongside the adoption of advanced manufacturing technologies, propels the market forward. Strategic investments and facility expansions by leading contract manufacturing companies in india, such as Aragen's new finished solid dose manufacturing facility in Hyderabad in October 2023, further underscore the sector's potential. Together, these factors position India as a critical player in the global pharmaceutical contract manufacturing market, with a promising outlook for continued innovation and growth.

India Contract Manufacturing Organization (CMO) Market Industry Segmentation

Availability of Skilled Labor at Relatively Lower Cost

The availability of skilled labor at competitive costs continues to be a pivotal factor driving market dynamics. This advantage enables organizations to access a proficient workforce while maintaining operational cost efficiency. As of 2023, India stands out with a significant number of United States Food and Drug Administration (U.S. FDA) approved manufacturing facilities, supported by a robust pharmaceutical sector and a highly skilled talent pool, which benefits both established pharmaceutical firms and CMO companies. The presence of trained professionals, including scientists and technicians, underpins the industry's capacity to deliver high-quality outputs, including advanced contract manufacturing services. This combination of cost-effectiveness and expertise positions the region as a compelling destination for companies aiming to optimize their operational expenditures.

Moreover, the cost advantage is further amplified by the region's growing emphasis on research and development initiatives. The ability to execute complex tasks at competitive rates enhances the region's attractiveness as a contract development and manufacturing hub. This dynamic not only fosters market growth but also solidifies the region's role as a critical player in the global pharmaceutical contract manufacturing market.

Sustained Increase in Outsourcing Volumes by Big Pharma Companies

The increasing trend of outsourcing by major pharmaceutical companies represents another significant market driver. Outsourcing enables these companies to leverage the specialized capabilities of contract manufacturing organizations pharmaceutical (CMOs) and CDMOs. Recent surveys indicate a strong inclination among industry players to outsource manufacturing processes. As of 2023, India has emerged as a leading supplier of generic drugs to the United States and other global markets, reflecting the growing confidence in the region's manufacturing capabilities and cost advantages.

Through pharmaceutical outsourcing, companies can concentrate on their core competencies while benefiting from the expertise and infrastructure of CMOs and CDMOs. This approach not only reduces costs and enhances efficiency but also provides access to advanced manufacturing technologies. The increasing reliance on outsourcing underscores the strategic importance of the region in the global pharmaceutical industry's operations.

Geographical Advantage in the Form of Access to Large Markets in the APAC Region

The region's geographical positioning, offering access to expansive markets within the Asia-Pacific (APAC) area, serves as a significant competitive advantage. Proximity to major economies such as China, Japan, and Southeast Asia facilitates streamlined supply chain operations and minimizes logistical challenges. As of 2023, India ranks among the top global producers of pharmaceuticals by volume and contributes significantly to global vaccine production, including a substantial share of the World Health Organization's (WHO) demand for essential vaccines. This strategic advantage ensures the timely delivery of pharmaceutical products to key markets.

The region's location also enhances its role as a hub for pharmaceutical trade and manufacturing. Its ability to serve diverse markets strengthens its position within the global pharmaceutical landscape. This geographical advantage, coupled with other market drivers, continues to propel the region's growth and competitiveness.

India Contract Manufacturing Organization (CMO) Market Trends

API and Intermediates India CMO Market Analysis

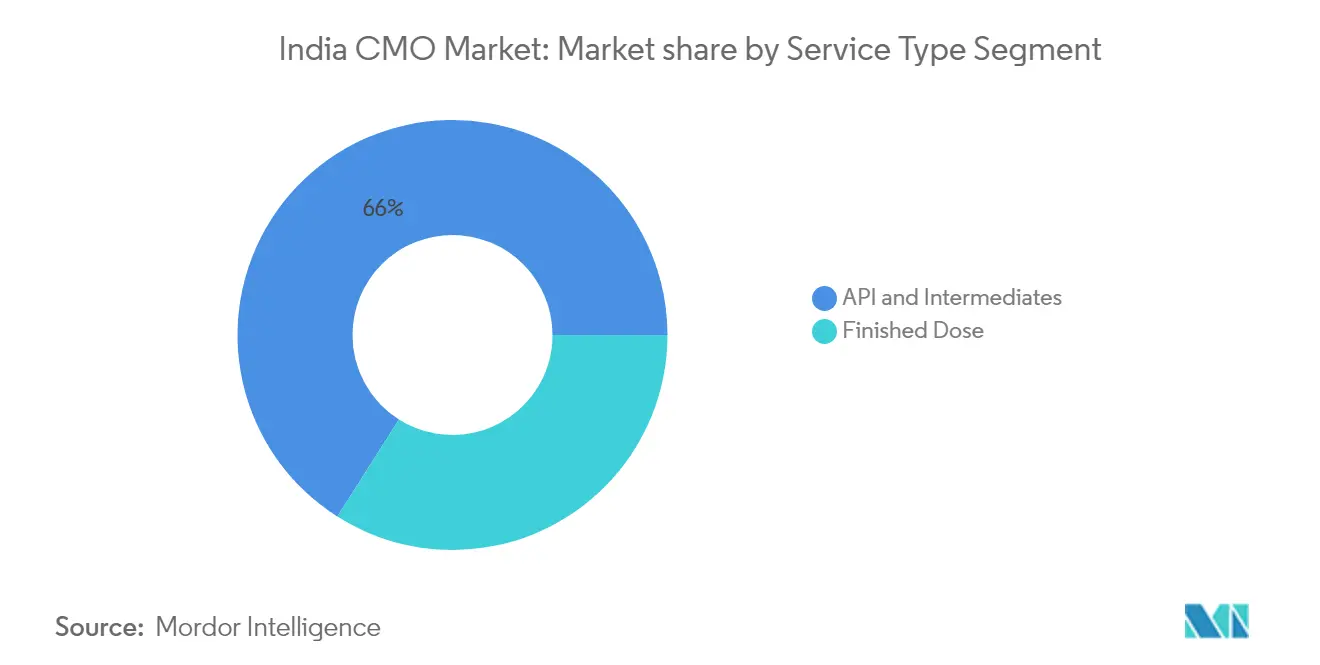

The API and Intermediates segment is the largest segment in the India CMO market, holding a significant market share of approximately 66% as of 2022. This segment is pivotal in the pharmaceutical manufacturing process, providing the active ingredients necessary for drug formulation, making API manufacturing a critical component of the industry. The dominance of this segment is driven by India's robust capabilities in chemical synthesis and cost-effective production, making it a global hub for API manufacturing companies in india. Additionally, the increasing demand for generic drugs and the outsourcing of pharmaceutical production by global companies have further bolstered this segment's growth in pharmaceutical contract manufacturing. The segment is also witnessing advancements in technology, such as continuous manufacturing and green chemistry, which enhance efficiency and sustainability for contract manufacturing organizations pharmaceutical. Furthermore, the growing focus on specialty APIs, including peptides and high-potency APIs, is creating new opportunities for CDMO companies within this segment. With a forecasted CAGR of approximately 10% from 2023 to 2028, the API and Intermediates segment continues to be a cornerstone of the India contract manufacturing market.

Finished Dose India CMO Market Analysis

The Finished Dose segment, while smaller than the API and Intermediates segment, is the fastest-growing segment in the India pharma contract manufacturing market, with a projected CAGR of approximately 12% from 2023 to 2028. This segment encompasses the final drug products ready for patient use, including tablets, capsules, and injectables, highlighting the role of injectable contract manufacturing organization. The rapid growth of this segment is attributed to the increasing demand for contract drug manufacturing of finished dosage forms, driven by the need for cost efficiency and scalability in pharmaceutical production. Additionally, the rising prevalence of chronic diseases and the expansion of healthcare access in emerging markets are fueling demand for finished dose medications, providing opportunities for pharma CDMO companies in india. Innovations in drug delivery systems, such as sustained-release formulations and biologics, are also contributing to the segment's growth in biologics contract manufacturing. Moreover, the trend towards pharmaceutical outsourcing by pharmaceutical companies to focus on core competencies is further accelerating the expansion of this segment. As a result, the Finished Dose segment is playing an increasingly important role in the India contract manufacturing organization pharma market.

India CMO Industry Overview

Top contract manufacturing companies in india

- Dr. Reddy's Laboratories

- Cadila Healthcare Limited

- MSN Laboratories Pvt Ltd

- Viatris Inc (Mylan Laboratories Ltd)

- Medipaams India Pvt Ltd

- Cipla Ltd.

- Eisai Pharmaceuticals India Pvt Ltd

- Delwis Healthcare Pvt Ltd

- Maxheal Pharmaceuticals India Ltd

- Rhydburg Pharmaceuticals Ltd

- Theon Pharmaceuticals Limited

- BDR Pharmaceuticals International

- Akums Drugs and Pharmaceuticals Limited

- Wockhardt Limited

- Unichem Laboratories Ltd

- Ciron Drugs & Pharmaceuticals Pvt Ltd

The India CMO Market is highly competitive, with companies focusing on enhancing their manufacturing capabilities and investing in research and development. Strategic partnerships, acquisitions, and collaborations are common as firms aim to strengthen their market position in the pharmaceutical contract manufacturing market. Product innovation is a significant trend, with emphasis on complex APIs, biologics, and specialized dosage forms. Operational efficiency and global expansion are also priorities for CMO pharma companies, leveraging India's cost advantages and skilled workforce.

Diverse players in a consolidating market

The India CMO Market features a mix of global and local players, including conglomerates and specialized firms. Consolidation is evident, with larger companies acquiring smaller CDMO companies to expand capabilities. Mergers and acquisitions are driven by the need for technological expertise and market expansion. Outsourcing by global pharmaceutical companies to Indian CDMOs is increasing due to cost advantages and regulatory compliance, highlighting the contract manufacturing opportunities in india.

Scale economies and the complexity of drug development drive market consolidation. Local players are enhancing their positions through partnerships and advanced technology investments. The strong regulatory framework in India attracts international clients. Companies are also expanding their global presence to serve diverse markets.

Innovation and regulatory compliance key to success

Incumbents in the India CMO Market should focus on technological innovation and expanding service offerings to maintain competitiveness. Advanced manufacturing capabilities, such as continuous manufacturing, can provide an edge. Contenders can specialize in niche areas like cell and gene therapies to gain market share. Diversifying client base and therapeutic focus is crucial to mitigate risks.

End-user concentration is significant, with large pharmaceutical companies dominating outsourcing volumes. Substitution risk is moderate due to high switching costs. Regulatory compliance is critical, requiring companies to adapt to evolving global standards. Success depends on maintaining quality, investing in regulatory expertise, and navigating regulatory landscapes effectively.

India Contract Manufacturing Organization (CMO) Market Leaders

-

Dr. Reddy’s Laboratories

-

Cadila Healthcare Limited

-

Cipla Ltd.

-

Akums Drugs and Pharmaceuticals Limited

-

Viatris Inc (Mylan Laboratories Ltd)

- *Disclaimer: Major Players sorted in no particular order

India Contract Manufacturing Organization (CMO) Market News

- July 2024: Sanofi Healthcare India Pvt. Ltd (SHIPL) unveiled plans to bolster its Global Capability Centre (GCC) in Hyderabad, with a substantial investment of EUR 400 million (USD 432 million) earmarked over the next six years. By 2026, the GCC is set to accommodate around 2,600 employees, solidifying its position as the largest among Sanofi's quartet of global hubs. These hubs, often called the company's nerve centres, facilitate centralization, modernization, and the scalability of services across Sanofi's value chain. They offer a comprehensive suite of services, from commercial and manufacturing to research and development and digital solutions.

- June 2024: Akums Drugs & Pharmaceuticals Ltd unveiled Rabeprazole + Levosulpiride SR Capsules. The Drug Controller General of India (DCGI) greenlit these capsules, which are designed to provide heightened relief for patients with gastrointestinal tract (GIT) disorders. Rabeprazole sodium, a potent antisecretory compound, selectively inhibits gastric acid secretion by targeting the H+ and K+ ATPase on the surface of gastric parietal cells.

India Contract Manufacturing Organization (CMO) Market Overview

Contract manufacturing organizations (CMOs) assist pharmaceutical and biotechnology firms in producing cutting-edge drug substances. CMOs typically offer various services, including commercial production, drug development, formal stability assessments, formulation development, etc. The market study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

India Contract Manufacturing Organization is Segmented by Service Type (API and Intermediates and Finished Dose). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for the Above Segments.

| By Service Type | API and Intermediates | ||

| Finished Dose | Solids | ||

| Liquids | |||

| Semi-solids and Injectables | |||

| API and Intermediates | |

| Finished Dose | Solids |

| Liquids | |

| Semi-solids and Injectables |

India Contract Manufacturing Organization (CMO) Market Research FAQs

How big is the India CMO Market?

The India CMO Market size is worth USD 25.81 billion in 2025, growing at an 14.67% CAGR and is forecast to hit USD 51.18 billion by 2030.

What is the current India CMO Market size?

In 2025, the India CMO Market size is expected to reach USD 25.81 billion.

Who are the key players in India CMO Market?

Dr. Reddy’s Laboratories, Cadila Healthcare Limited, Cipla Ltd., Akums Drugs and Pharmaceuticals Limited and Viatris Inc (Mylan Laboratories Ltd) are the major companies operating in the India CMO Market.

What years does this India CMO Market cover, and what was the market size in 2024?

In 2024, the India CMO Market size was estimated at USD 22.02 billion. The report covers the India CMO Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India CMO Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: December 24, 2024